NEPSE’s New Volatility Regime Gets Immediate Stress Test

NEPSE enters a new trading regime after doubling its daily circuit band to 15%, immediately testing volatility across both upside and downside extremes.

A 15% upper-circuit band went live. The first stock tested it within three sessions. Sanima Bank issued the first non-dilutive Tier-1 raise of this cycle. The SEBON Chairperson selection started while the former NEPSE Chief passed away.

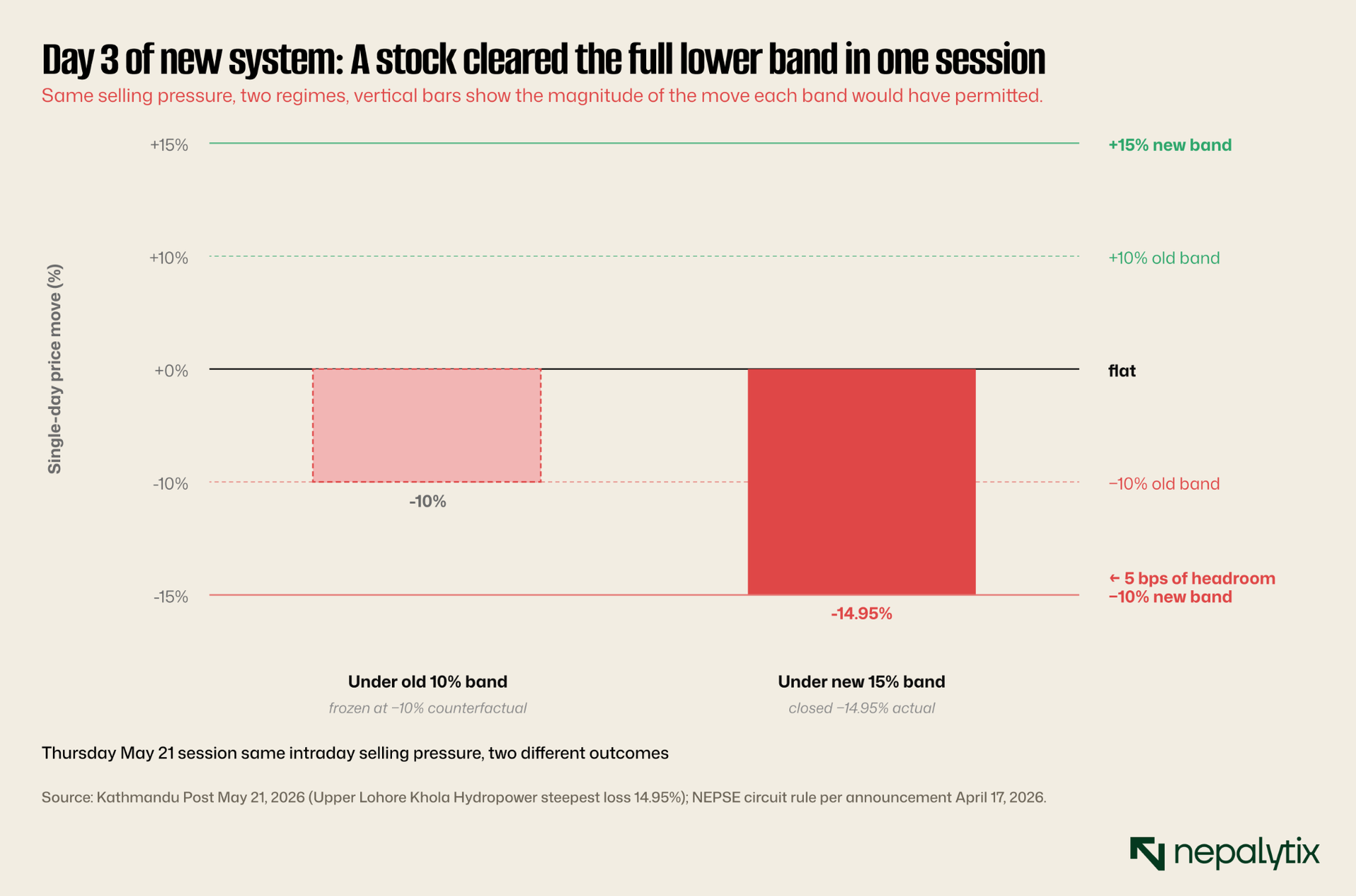

→NEPSE doubled the daily upper-circuit band from 10% to 15% and introduced an 8% index-level halt. The largest single-step change to NEPSE trading rules since the 2022 floor-trading transition. Upper Lohore Khola Hydropower closed −14.95% on Thursday broke past the old 10% band by nearly 500 bps and almost tested the entire new 15% band on day three of live operation

→Sanima Bank's 8.25% Perpetual Non-Cumulative Preference Share listed May 21, first non-dilutive Tier-1 capital raise of this cycle. Coupon sits roughly 250–300 bps above current fixed deposit yields and ~150 bps below the average Cluster 3 commercial bank's implicit cost of equity. A new instrument category for NEPSE

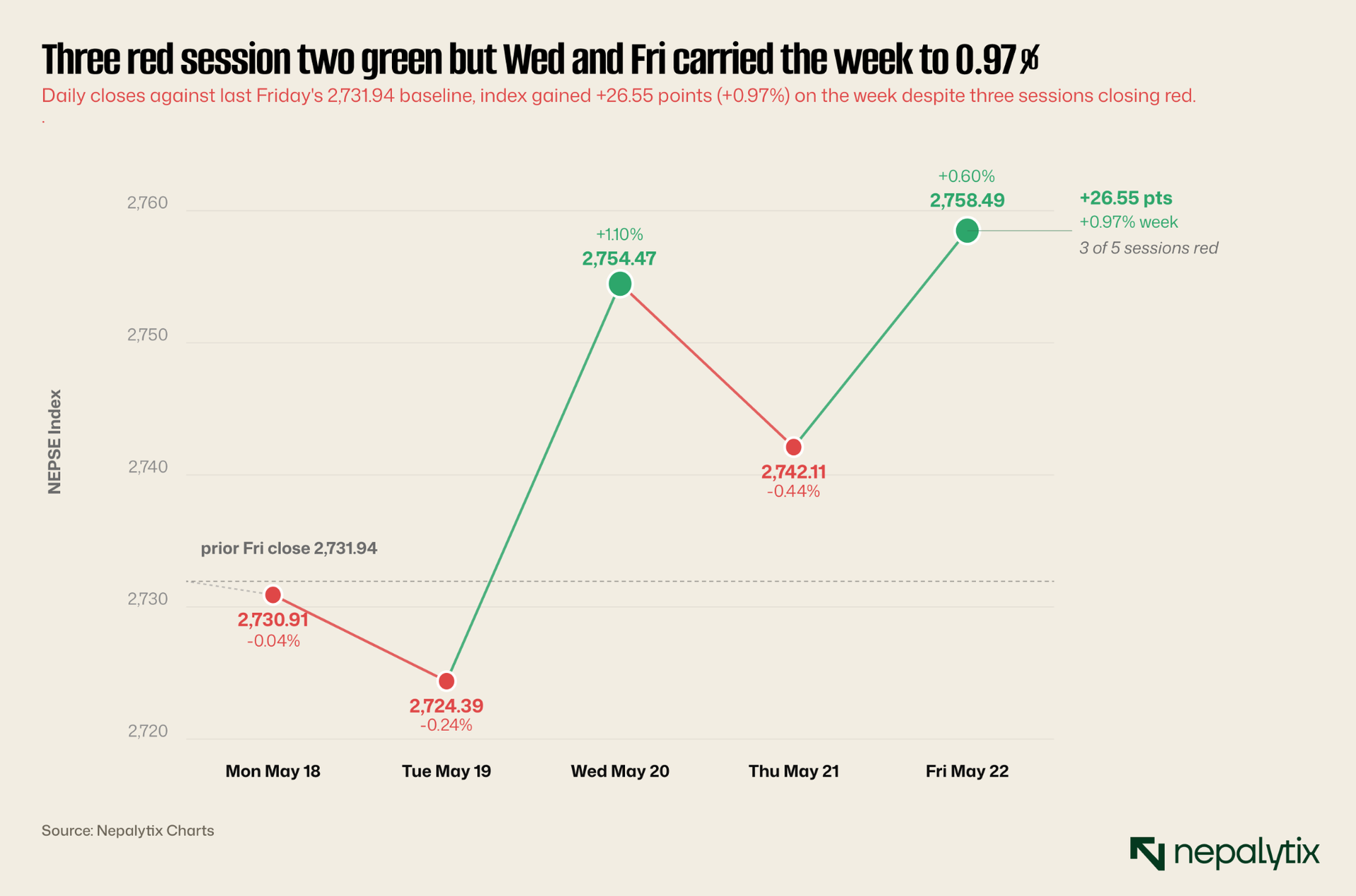

→NEPSE 5-session trajectory: 2,730.94 → 2,724.39 → 2,754.48 → 2,742.11 → 2,758.49. Soft Mon-Tue, sharp Wed reversal, Thu sell-off, Fri rally. Weekly close +26.55 points (+0.97%) the index gained on the week despite Thursday's 72:188 breadth implosion

→Thursday's breadth: only Mutual Fund (+0.14%) sub-index closed green. Trading unchanged. Eleven of thirteen sub-indices closed red, the third confirmed instance of the institutional-defense fingerprint in two weeks

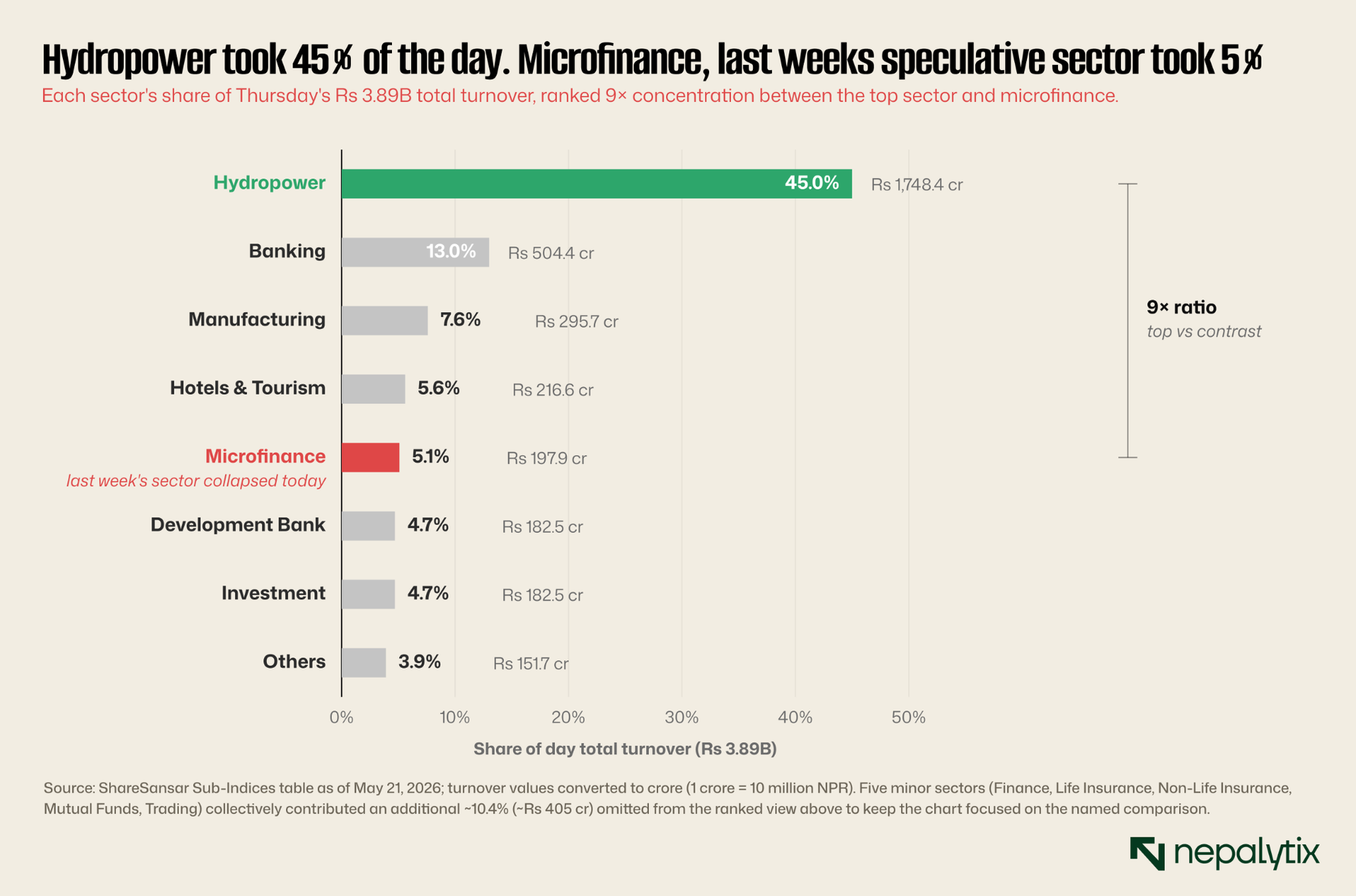

→Hydropower took 45% of Thursday's Rs 3.89B turnover, Rs 1.74 billion in a single sector. Banking added 13%. Microfinance, last edition's speculation hub, has gone quiet (5% share, −0.45%). The rotation venue changed

→SEBON Chairperson shortlist announced May 19. Former NEPSE Chief Shankar Man Singh passed away May 21. Institutional transition at the regulator and the exchange coincides with the largest rule change in three years

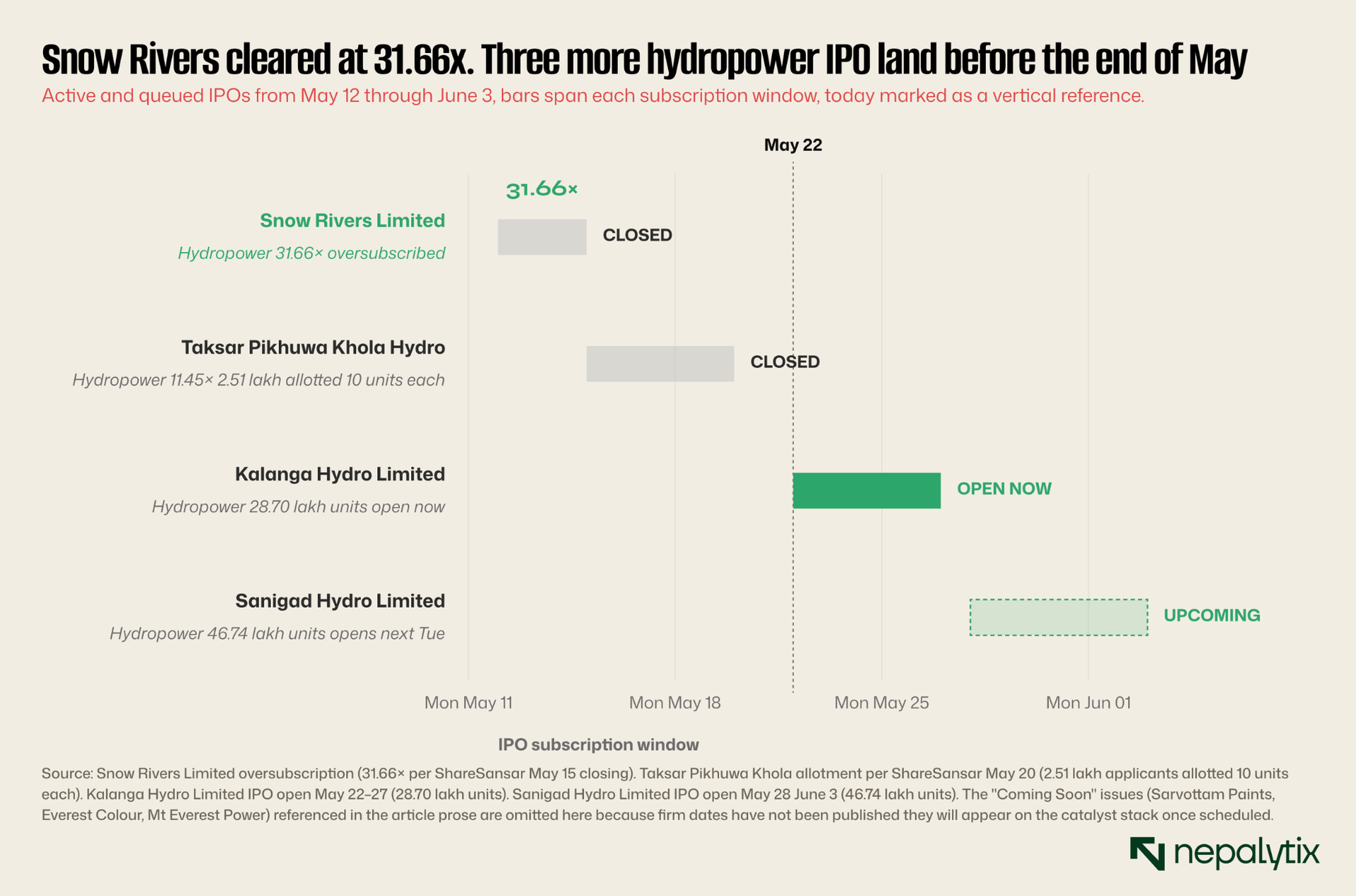

→IPO pipeline running hot: Snow Rivers closed oversubscribed 31.66×; Taksar Pikhuwa Khola Hydropower allotted 2.51 lakh applicants; Kalanga Hydro opened Friday May 22; Sanigad Hydro opened May 28. Primary-market enthusiasm under a wider secondary band

→Macro backdrop: trade deficit widened nearly 15% (Sharesansar May 22); gold +Rs 1,800/tola Wednesday risk-off signals at the margin while NEPSE primary activity remains elevated

I. I.The 15% circuit goes live and gets tested in three days

NEPSE operated for years on a 10% single-stock daily band. On April 17, the exchange announced that the band would widen to 15%, a 50% expansion with a new 8% index-level halt added as a complementary brake. This is the first full trading week under the new system. The math is straightforward and severe: a name that previously needed two consecutive upper-circuit sessions to clear a 15% move can now do it in one. A name that previously stalled at a midday lower circuit can now keep selling for the rest of the session. The volatility profile of every single listed stock just changed.

The system got tested faster than anyone reasonably expected. On Thursday May 21, Upper Lohore Khola Hydropower closed at −14.95% almost the entire new lower band, in a single session, three trading days after the rule went live. Under the old 10% band, that selling pressure would have hit the lower circuit at around midday and frozen the stock until Friday losses would have been bounded at −10%, the additional ~500 basis points of decline could not have cleared. Under the new band, it cleared. The price discovery the new system was designed to enable just happened, in the negative direction, in the first week.

The new system isn't just about individual stocks. It changes intraday risk management for brokers (margin call frequencies recalibrate to wider bands), retail behavior (loss limits hit faster, position-sizing logic changes) and market-maker spreads (wider price uncertainty implies wider quotes). None of those effects are visible in a single index print. They show up in the distribution of daily extremes over the next four weeks.

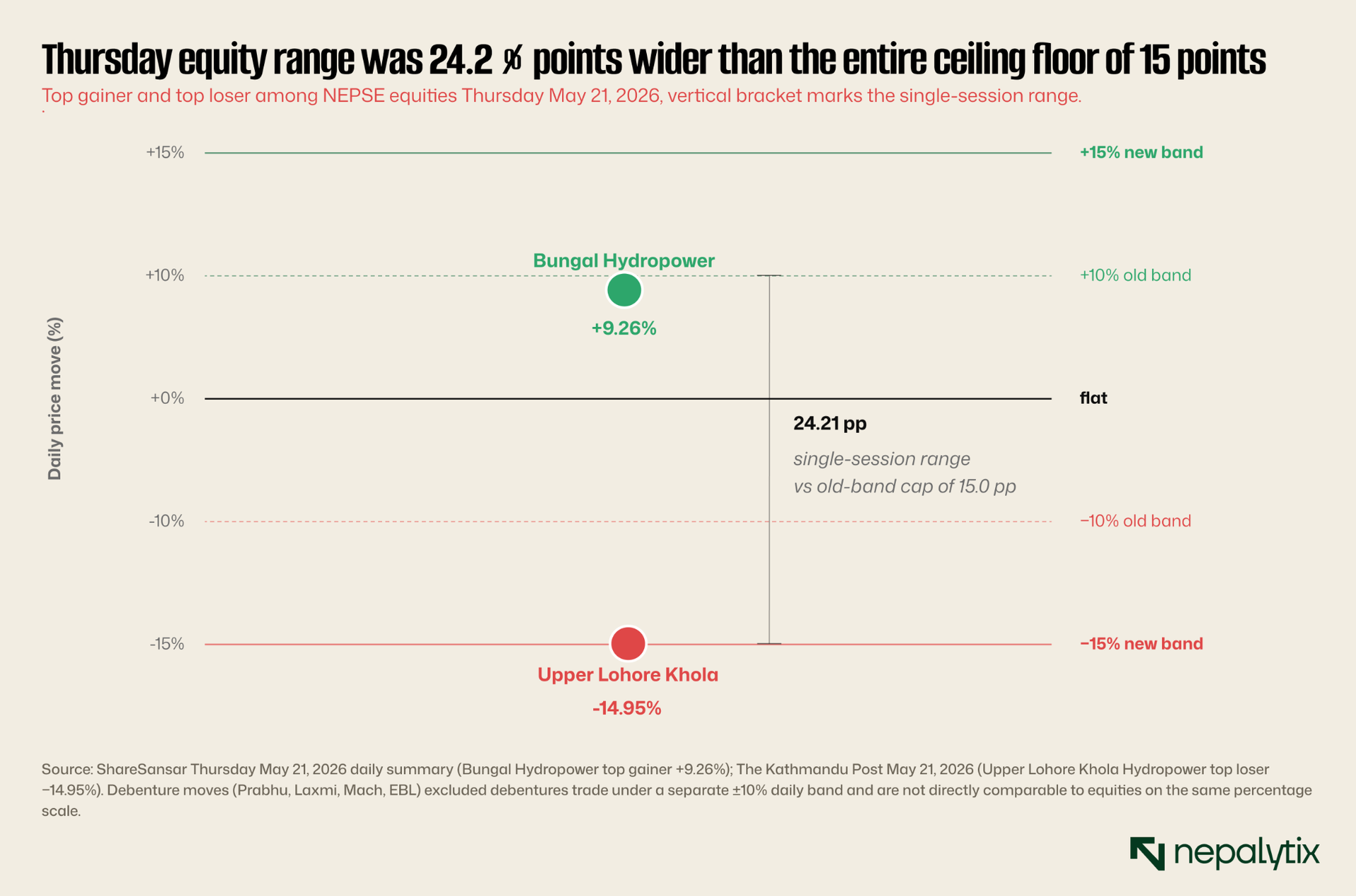

The asymmetry in the chart is the early signal and it is sharper than it looks at first. The upside extreme this week landed at +9.26% (Bungal Hydro) which didn't even reach the old 10% band, let alone test the new 15%. The downside extreme landed at −14.95% (Upper Lohore Khola) which blew through the old 10% band by ~500 basis points and nearly tested the entire new 15% floor. Sellers used the new regime; buyers didn't. Under the old system, the upside extreme would have been the same +9.26% (no band hit), but the downside would have been bounded at −10% with another ~500 bps of decline locked out. If this asymmetry holds for another two weeks, the wider band is functionally a one-sided expansion amplifying drawdowns much more than rallies. That is precisely the opposite of the retail intuition that motivated support for widening the band in the first place.

The five-session pattern is now readable. Mon and Tue drifted softly red (−1.03 and −6.52). Wednesday produced a sharp +30.08 rally, the largest single-session gain of the week. Thursday gave most of it back with the 72:188 breadth implosion documented above. Friday closed at 2,758.49 (+16.38, +0.60%) on Rs 4.05 billion turnover, the largest single-session turnover of the week and rescued the headline number. The index gained +26.55 points (+0.97%) on the week despite three of five sessions closing red. A green week generated by two strong sessions (Wed and Fri) against three weak ones is itself a continuation of the institutional-defense fingerprint last week documented: a small number of heavyweight names rescuing the composite from broader weakness.

II. Hydropower ate the speculation flow

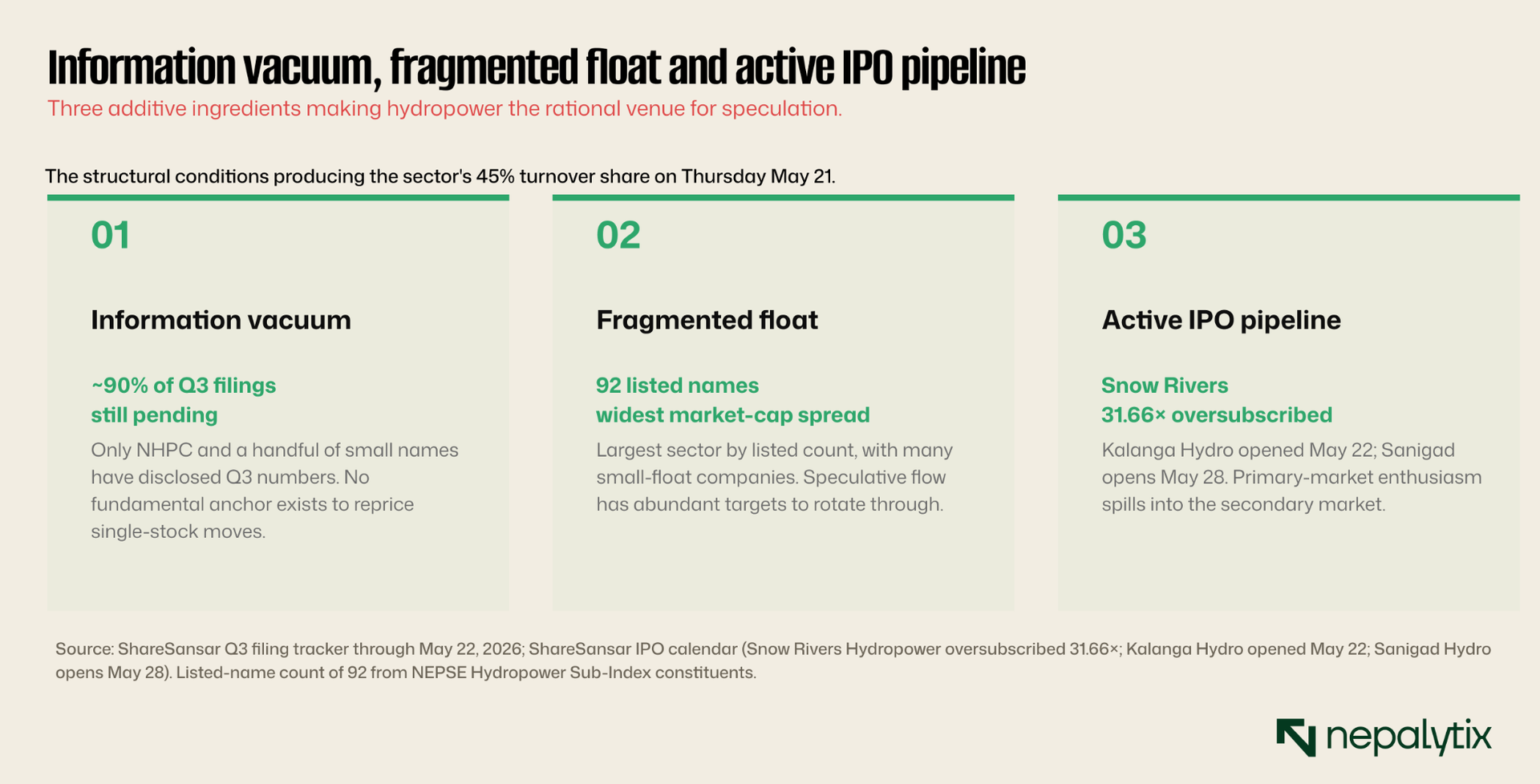

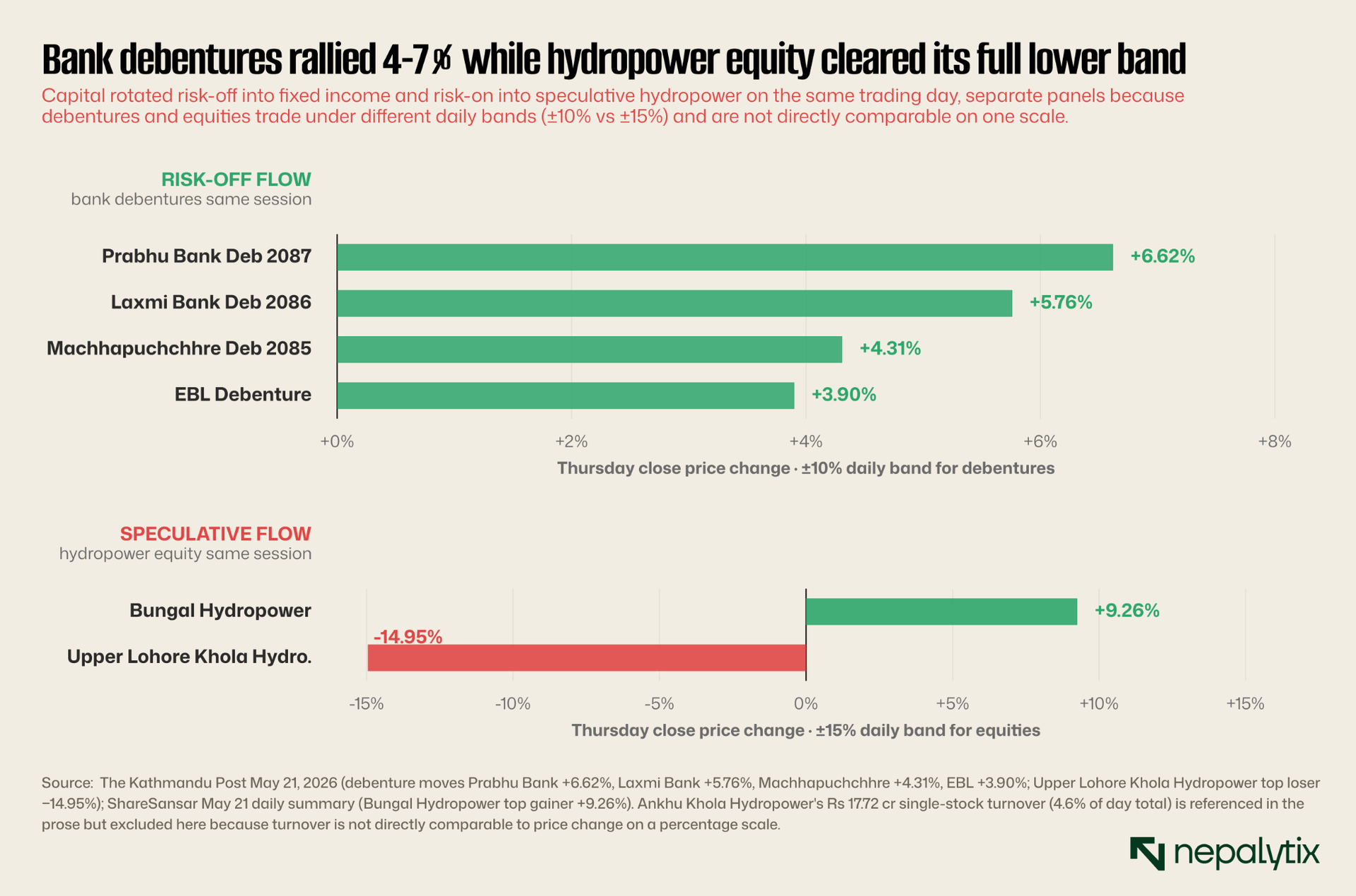

Last week documented that microfinance was the speculation venue: DHPL upper-circuit Tuesday May 12, FOWAD the week before, wide intra-sector dispersion, sector index essentially flat while individual names moved violently. This week, that pattern moved venues. On Thursday May 21, hydropower took Rs 1.74 billion in turnover 45% of the day's Rs 3.89B total. Microfinance took Rs 198 million, about 5%. The speculation venue has rotated from microfinance to hydropower in two weeks.

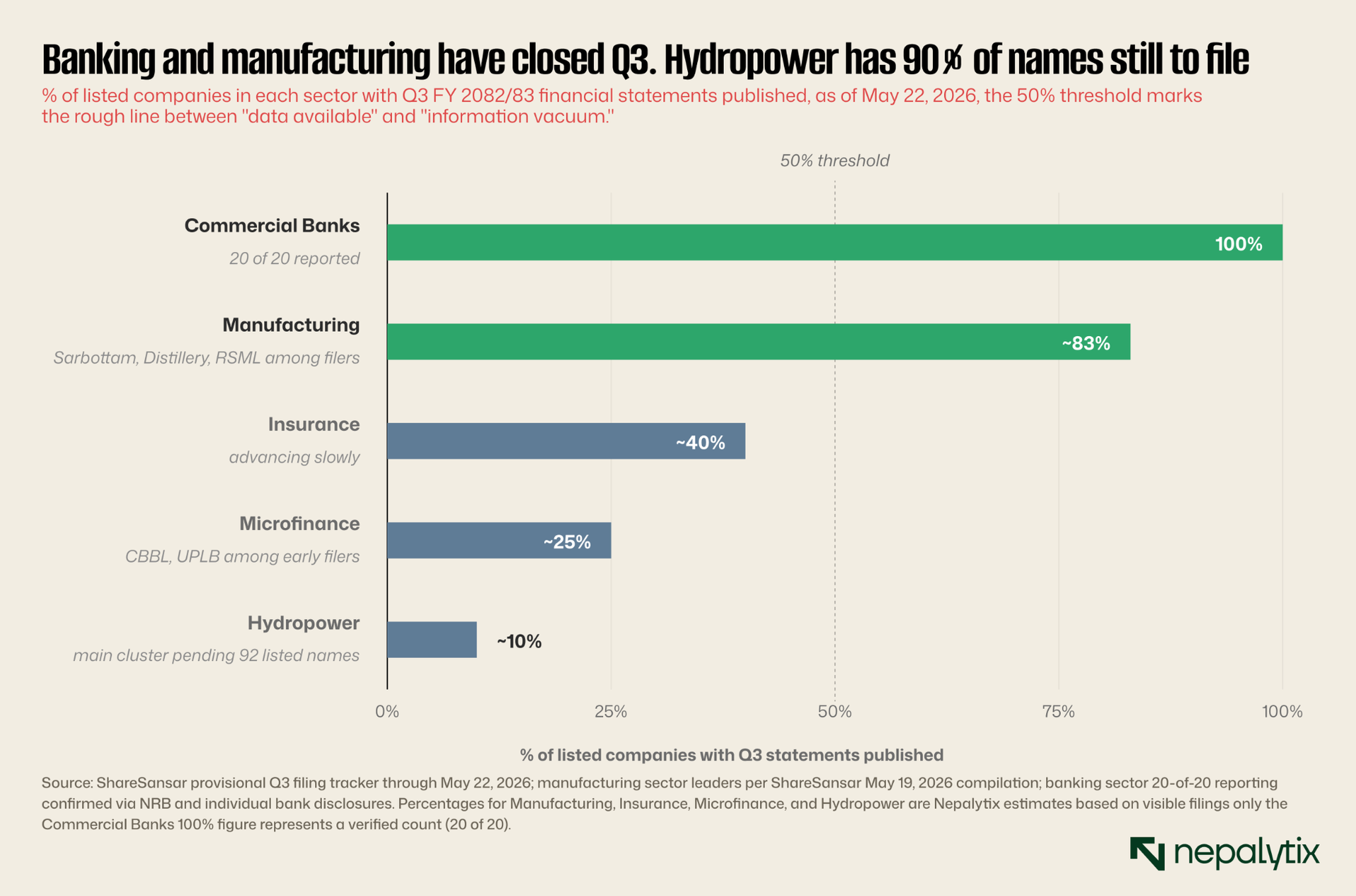

Why hydropower? Three conditions align that make it the cleanest available venue for speculative flow right now. First, the sector has roughly 90% of its Q3 financial statements still unfiled, a near-complete information vacuum which means no fundamental anchor can immediately reprice any single-stock move. Second, hydropower has the largest number of listed companies of any sector with a wide market-cap distribution giving speculation lots of small-float names to chase. Third, the active IPO pipeline this week (Kalanga Hydro opened Friday, Sanigad opened May 28, Snow Rivers closed 31.66× oversubscribed) keeps primary-market enthusiasm spilling into the secondary market for the same sector.

The bank-debenture rally on the same day: Prabhu Bank Debenture +6.62%, Laxmi Bank Debenture +5.76%, Machhapuchchhre +4.31%, EBL +3.90% tells the corresponding story on the other side of the risk curve. Debentures are fixed-income instruments with limited speculative upside; a 4-7% same-day rally in multiple bank debentures, on the same session as a hydropower stock cleared its full −15% band, is the bifurcation pattern. Conservative capital ran to debentures; speculative capital ran to hydropower. The market split itself in two on Thursday.

Bifurcation explains why headline breadth was so lopsided (72 advancers vs 188 decliners) while the index moved only 0.44%. Capital wasn't selling broadly and parking in cash; it was rotating from speculative equity into bank debentures within the same trading session. That kind of rotation usually precedes a regime change risk-off positioning ahead of a known event. The forward calendar in Section VI confirms there are several plausible events worth positioning for. Section III takes the new instrument that just gave that risk-off flow somewhere to go: Sanima Bank's perpetual.

III. Sanima's 8.25% perpetual, the yield curve just got real

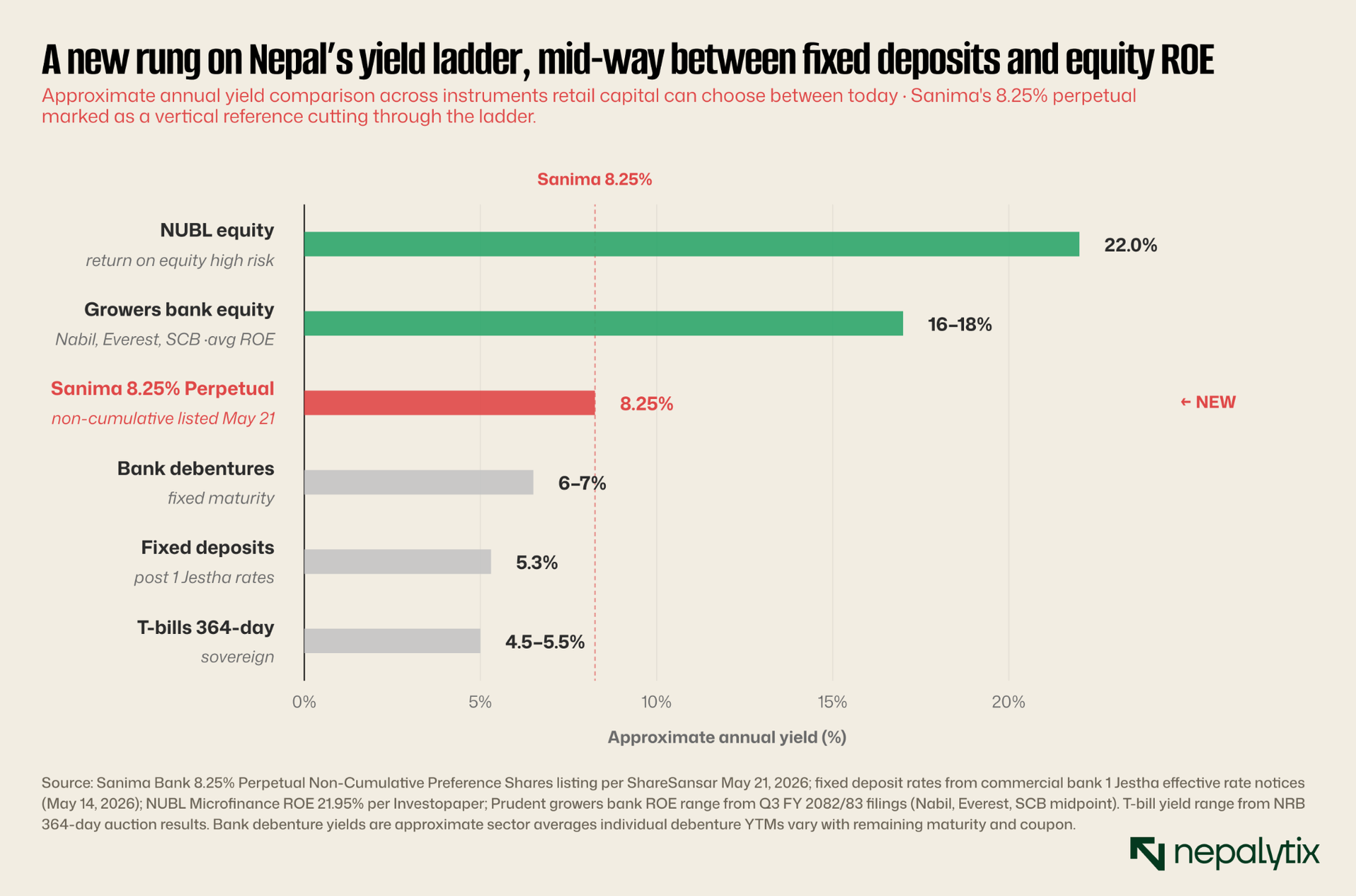

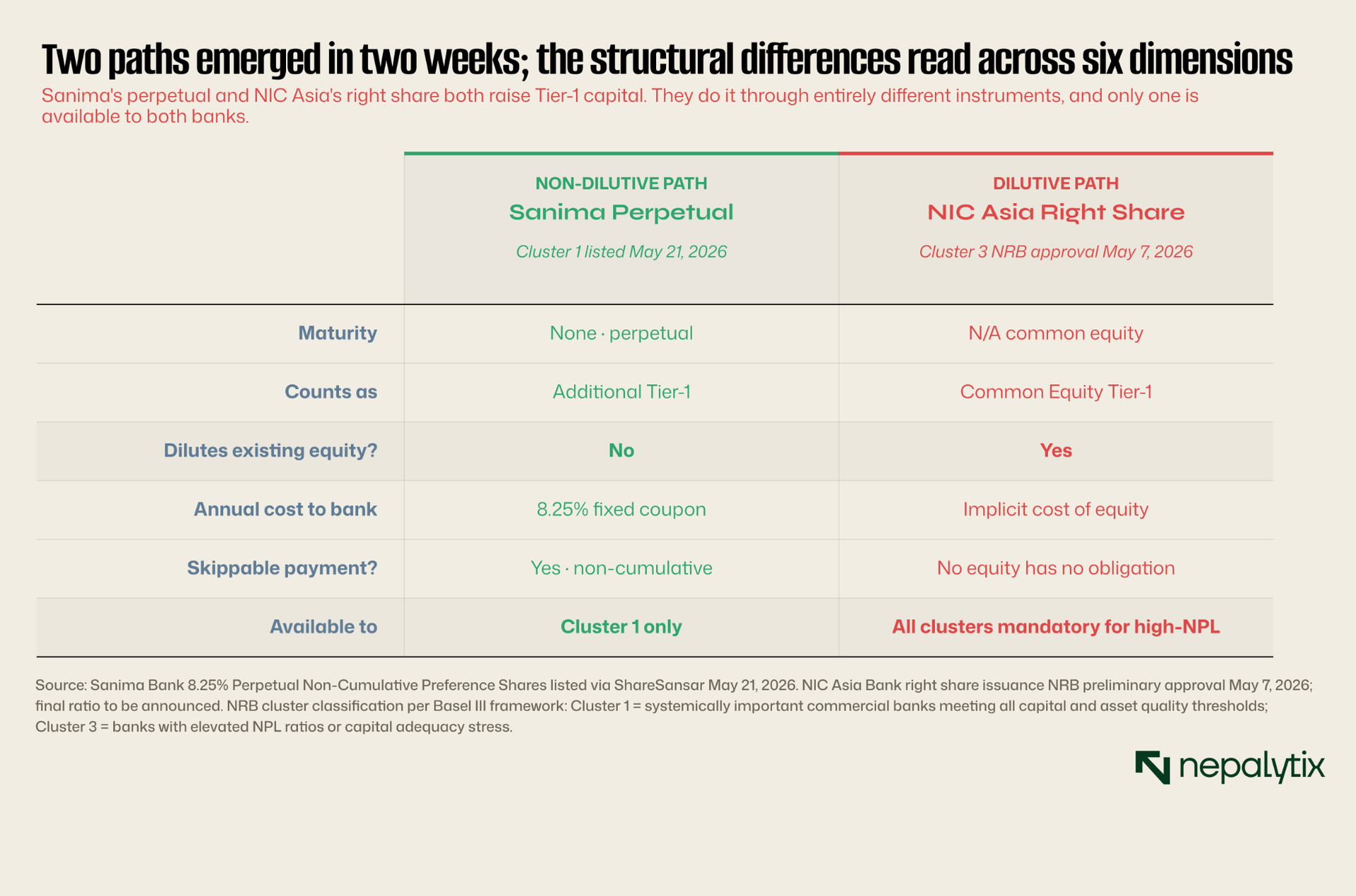

On May 21, NEPSE listed Sanima Bank's "8.25% Sanima Perpetual Non-Cumulative Preference Shares." Two words in that name are doing the analytical work: perpetual (no maturity, no obligation to return principal) and non-cumulative (if Sanima skips a coupon payment, holders don't accumulate the missed amount as a claim). The instrument sits between debt and equity. For accounting purposes it counts as Additional Tier-1 capital meaning it improves Sanima's capital adequacy ratio without diluting existing shareholders. For investors it pays a fixed 8.25% indefinitely as long as the bank stays solvent and willing to pay. Until this listing, NEPSE had essentially no comparable instrument trading. This is a new asset class.

The 8.25% coupon is not arbitrary. Place it on a yield ladder against the actual rates retail capital is choosing between right now and the logic becomes immediately visible. Fixed deposits post-1 Jestha are landing around 5.3%. Sovereign T-bill yields are in the 4.5–5.5% range. Bank debentures vary widely. Equity ROEs at strong Cluster 1 banks range 16–22%. The 8.25% perpetual sits in the middle of those meaningfully above any deposit option meaningfully below the return profile of common bank equity and offering something neither alternative does: a fixed contractual yield with no maturity risk.

The structural significance is bigger than the single instrument. Until this week, the only ways for retail capital to capture bank earnings were either to take equity risk (full ROE participation, including downside) or to lend the bank money short-term through deposits or fixed-maturity debentures. The perpetual creates a third option: fixed-yield bank exposure with no maturity, no upside participation but no dilution risk and no rollover risk. This is the first time NEPSE has effectively traded a hybrid capital instrument at meaningful scale. The price discovery on the secondary market over the next four weeks will tell us how the local market values that hybrid risk.

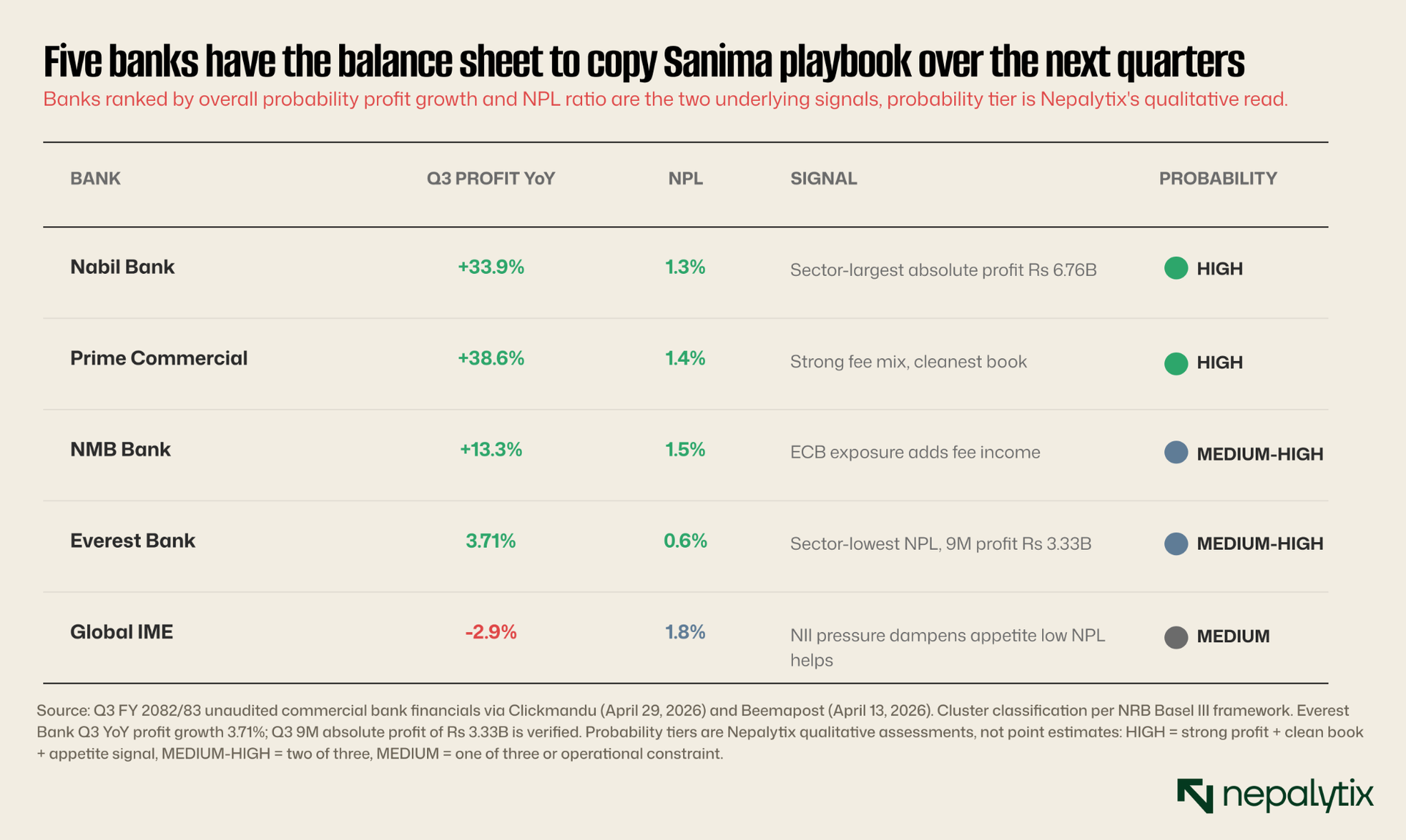

Who comes next? Sanima's successful issuance creates an implicit template that other Cluster 1 banks can read. The candidates with both the balance-sheet strength and the existing fee-income mix to support a fixed 8.25%-area perpetual coupon are Nabil, Prime, NMB, Everest, and Global IME roughly the same names last week’s cluster map placed in the top quadrant. Three (Nabil +33.9%, Prime +38.6%, NMB +13.3%) are still posting profit growth; two (Everest −3.71%, Global IME −2.9%) have Q3 declines driven by impairment surges and NII compression respectively but balance-sheet quality remains intact in both cases. What matters for a perpetual issuance is durable capital, not last-quarter EPS direction and all five have it. The Cluster 3 names cannot follow this path; they would need to price closer to 11-13% to attract demand, at which point right shares (with ownership dilution but no fixed coupon obligation) become cheaper. The Sanima listing has effectively created a two-tier capital market for Nepali banks.

The pricing of Sanima's perpetual in the secondary market over the next four weeks is itself one of the more interesting forward observations available to anyone watching NEPSE. If it trades flat to issue price (par), the 8.25% is the right clearing yield for Nepali bank perpetuals. If it trades up (yield compresses below 8.25%), the next issuer can come cheaper. If it trades down (yield expands above 8.25%), the next issuer either has to pay more or shelves the plan. Section IV picks up the related deposit-yield story.

IV. Rates are live: 1 Jestha reality check

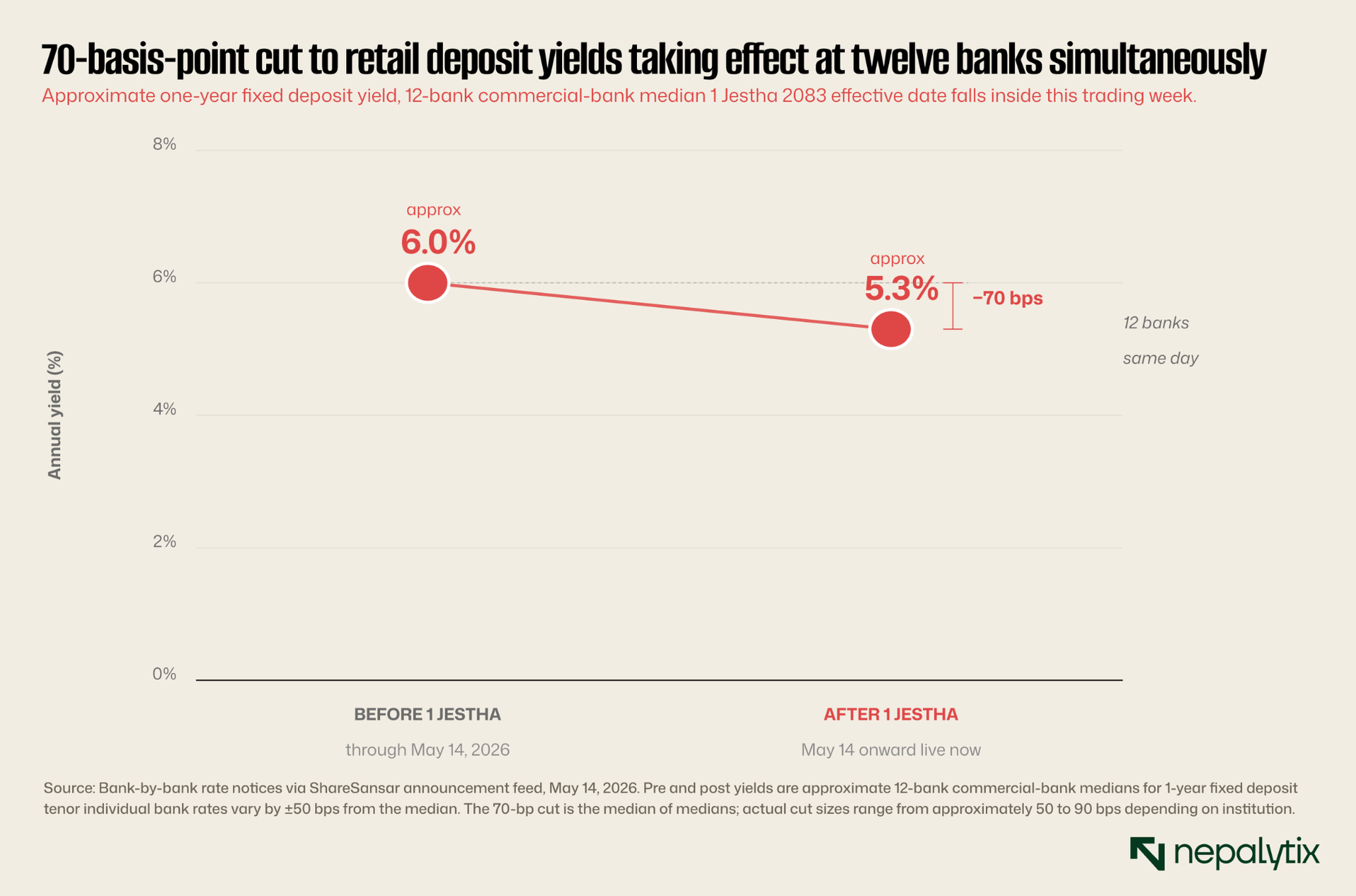

Last week covered the rate-notice announcements. This week, those notices are actively in force. The May 14 rate filings from twelve banks and finance companies all cited 1 Jestha 2083 as the effective date, which falls inside this trading week. The deposit yields retail savers earned last Monday no longer exist. The new yields are what they earn now and what they earn now is meaningfully lower than what they earned last week.

The actual cut size varies by institution and tenor, but the median commercial-bank one-year fixed deposit has reset from roughly 6.0% pre-1 Jestha to ~5.3% post-1 Jestha, a 70 basis-point cut. Loan rates have moved by similar magnitudes. For a household choosing between parking Rs 100,000 in a fixed deposit and rotating it into NEPSE small caps, this week is when the opportunity cost calculation flipped. Rs 700 per year of foregone deposit yield is no longer a hypothetical; it is the actual difference.

The same cut on the asset side lower loan rates compresses bank net interest margin. NII grew just 2.09% sector-wide in Q3 (per Clickmandu's April 29 sector compilation), and this rate cut likely takes another 30-40 basis points off that already-thin margin number over Q4. Cluster 1 banks with strong fee-income franchises absorb that compression more easily than Cluster 3 banks with weak fee mixes. The Sanima perpetual issued this week is partly a hedge against exactly this margin pressure non-dilutive Tier-1 capital raised before NIM compression eats into capital adequacy ratios next quarter.

The five-step chain: NRB liquidity absorption → bank deposit rate cuts → household yield search → wider daily band → speculation in information-vacuum sectors is now end-to-end live. Last week described the first three links as theory because Household yield search didn't exist yet and wider yield band was still attached to microfinance. This week added the missing structural links and rotated the venue. The hydropower concentration in Section II, the Sanima perpetual in Section III and the deposit cut in this section are three views of the same flow.

V. Q3 endgame + IPO pipeline running hot

Two parallel earnings stories closed this week. Manufacturing Q3 is materially done, Sharesansar's May 19 sector compilation confirmed Sarbottam Cement and Himalayan Distillery as the sector profit leaders, with Reliance Spinning Mills (Rs 266.89M 9M profit confirmed May 6) anchoring the post-IPO cohort. Hydropower Q3 is still mostly pending; perhaps 10% of names have filed. That asymmetry is exactly the information vacuum Section II identified as one of the three conditions making hydropower the speculation venue. The question this week added is when the asymmetry closes.

On the primary market side, this week was unusually active. Snow Rivers Limited closed its IPO oversubscribed 31.66 times meaning Rs 31.66 of applications came in for every Rs 1 of shares on offer. Taksar Pikhuwa Khola Hydropower allotted 2.51 lakh applicants 10 units each via lottery on May 20. Kalanga Hydro Limited opened its 28.7 lakh-unit IPO on Friday May 22, running through May 27. Sanigad Hydro opens May 28 with 46.74 lakh units. Three of those four are hydropower, exactly the sector that took 45% of Thursday's secondary turnover. Primary and secondary enthusiasm in the same sector is reinforcing.

A 31.66× oversubscription on Snow Rivers is the cleanest available evidence of how much capital wants exposure to listed hydropower. A retail investor putting in Rs 5,000 to buy IPO shares of a hydropower company they have done zero fundamental work on is the same retail behavior that produces a 45% sector turnover share on Thursday in the secondary market. Both are bets on a sector with 90% of Q3 financials still unfiled. The discipline of waiting for Q3 anchors before deploying capital is structurally not what the market is doing right now. The forward catalyst stacks the events that will resolve which way the open threads from this edition land unusually dense for the next two to three weeks.