Charts of The Week: The money is there. The willingness isn’t.

Nepal’s trade, markets, and liquidity data point to one reality: money is flowing, but not working. Despite rising remittances and excess liquidity, weak demand, low market participation, and import-heavy trade continue to stall productive growth.

Chart of The Week: The money is there. The willingness isn’t.

Three data releases dropped between Monday and Wednesday. Trade deficit. New market rules. Central bank liquidity. Read together they describe the same condition from three angles.

01. Trade: The deficit widened even though exports grew faster

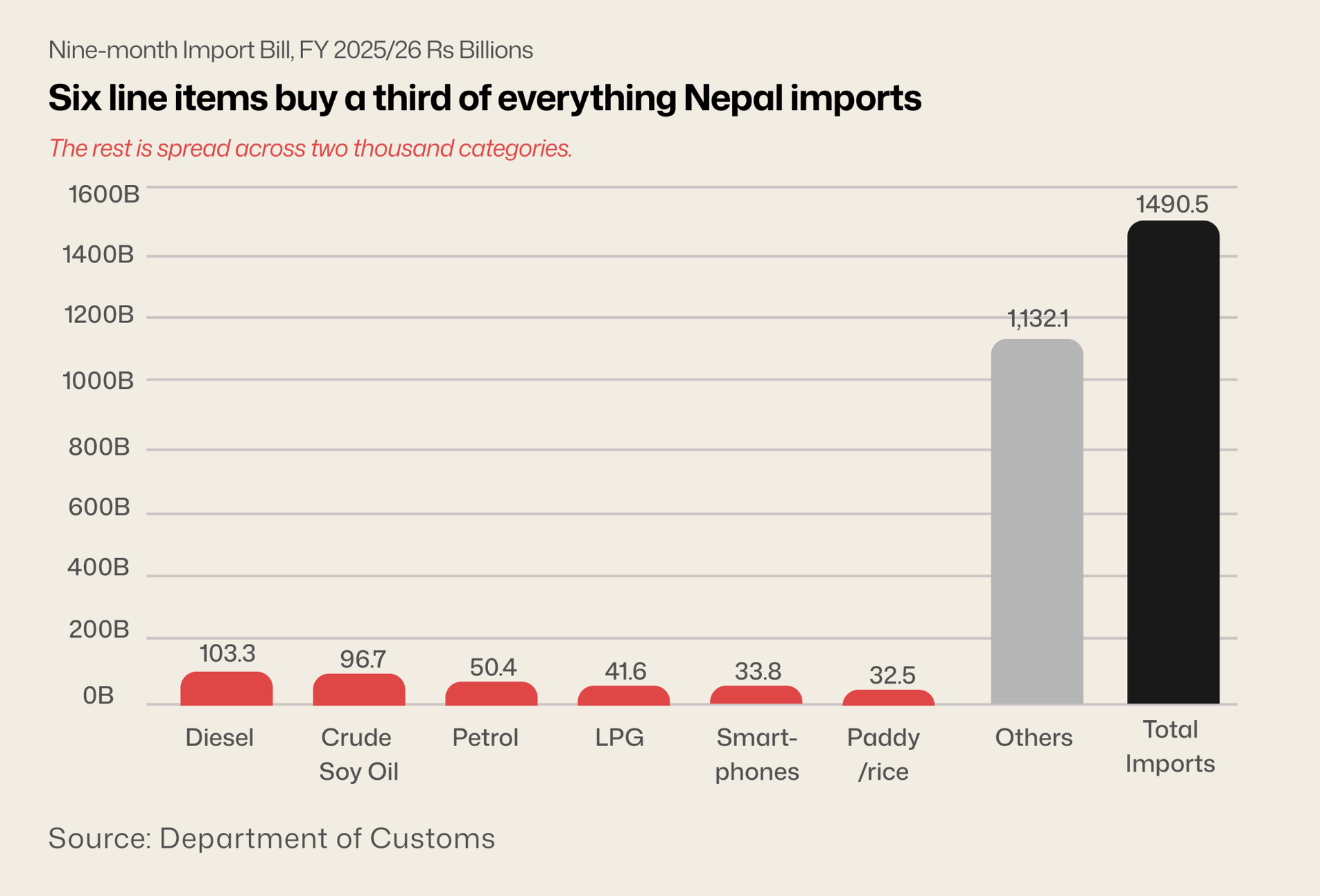

The Department of Customs nine-month trade data on Monday. Headline: Rs 1,267.56 billion. That’s the deficit from mid-July 2025 to mid-April 2026. The obvious reaction is that exports must have collapsed. They did the opposite. Exports grew 18.46% year-on-year. Imports grew 13.82%. Exports grew faster and the gap still widened by 13%. On a small enough base, growth rates don’t matter.

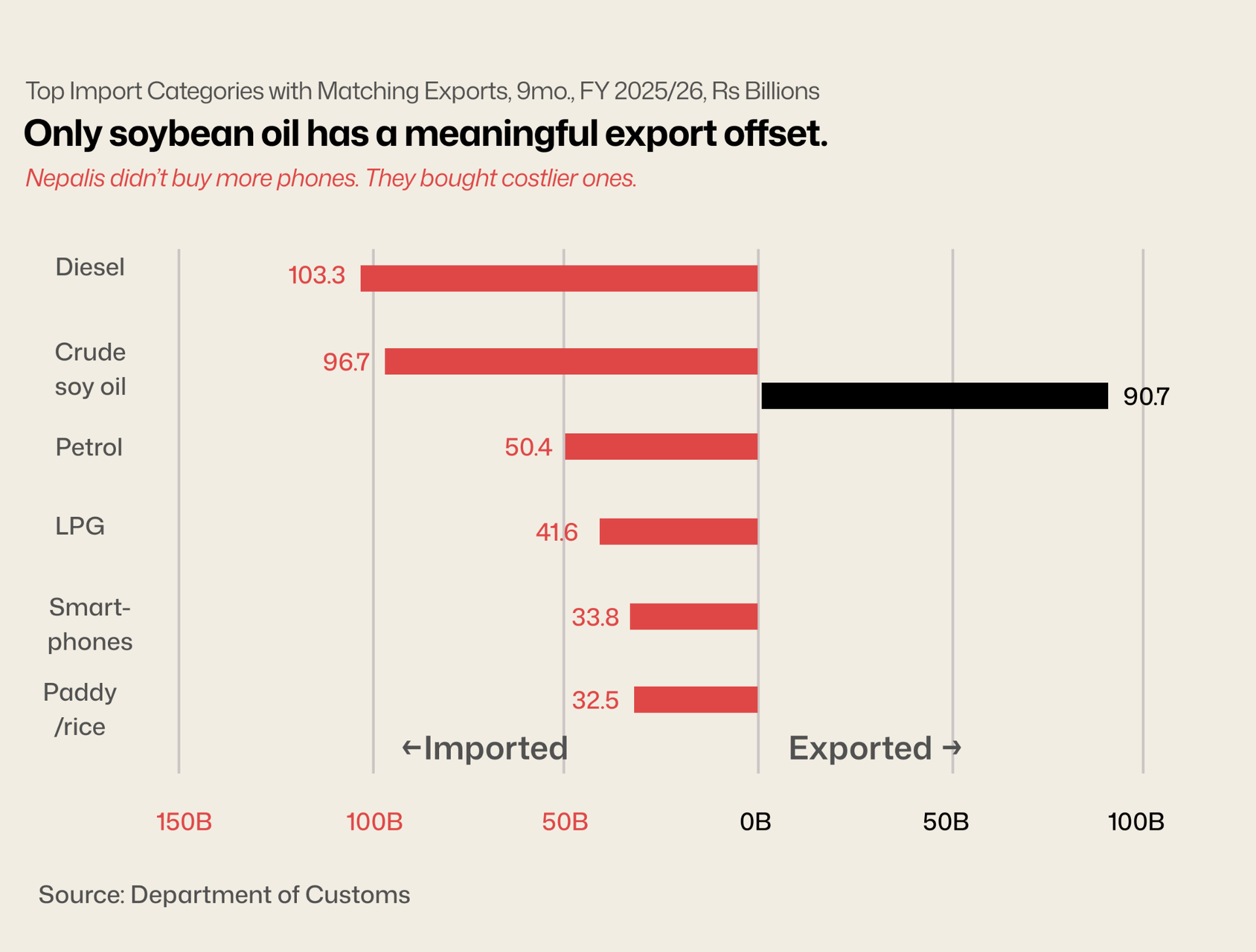

Diesel alone was Rs 103.31 billion. Add petrol and LPG and liquid energy tops Rs 195 billion, the price of not having an energy transition. Add crude soybean oil, paddy and smartphones and those six categories carry about a third of the nine-month bill. The top of this chart is the political economy of the country.

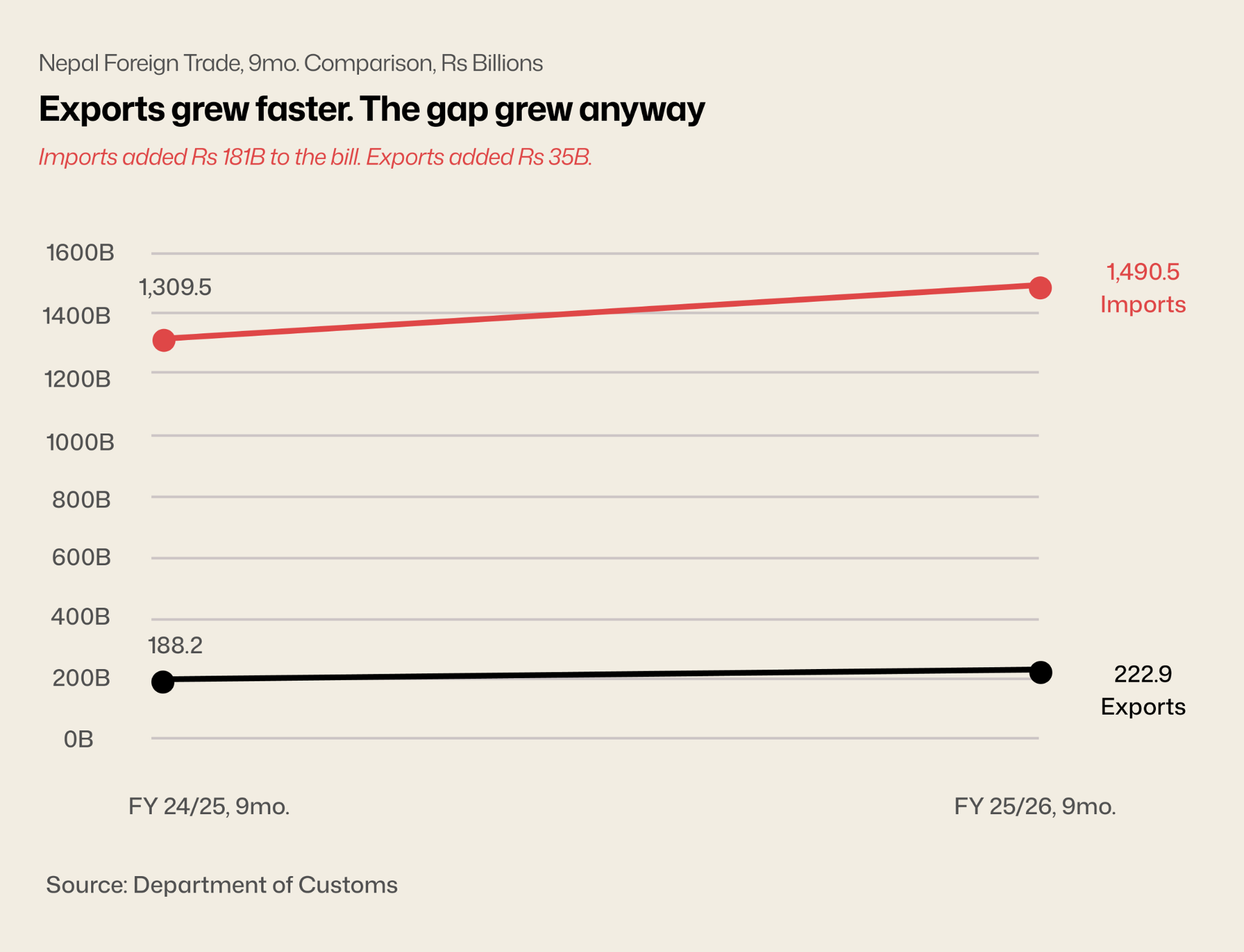

This is why “exports grew faster” is misleading. Exports went from Rs 188.19 billion to Rs 222.94 billion. Imports went from Rs 1,309.53 billion to Rs 1490.50 billion. In absolute terms, imports added Rs 181 billion. Exports added Rs 35 billion. The ratio can slip from 6.96x to 6.68x and it still feels like water behind a dam.

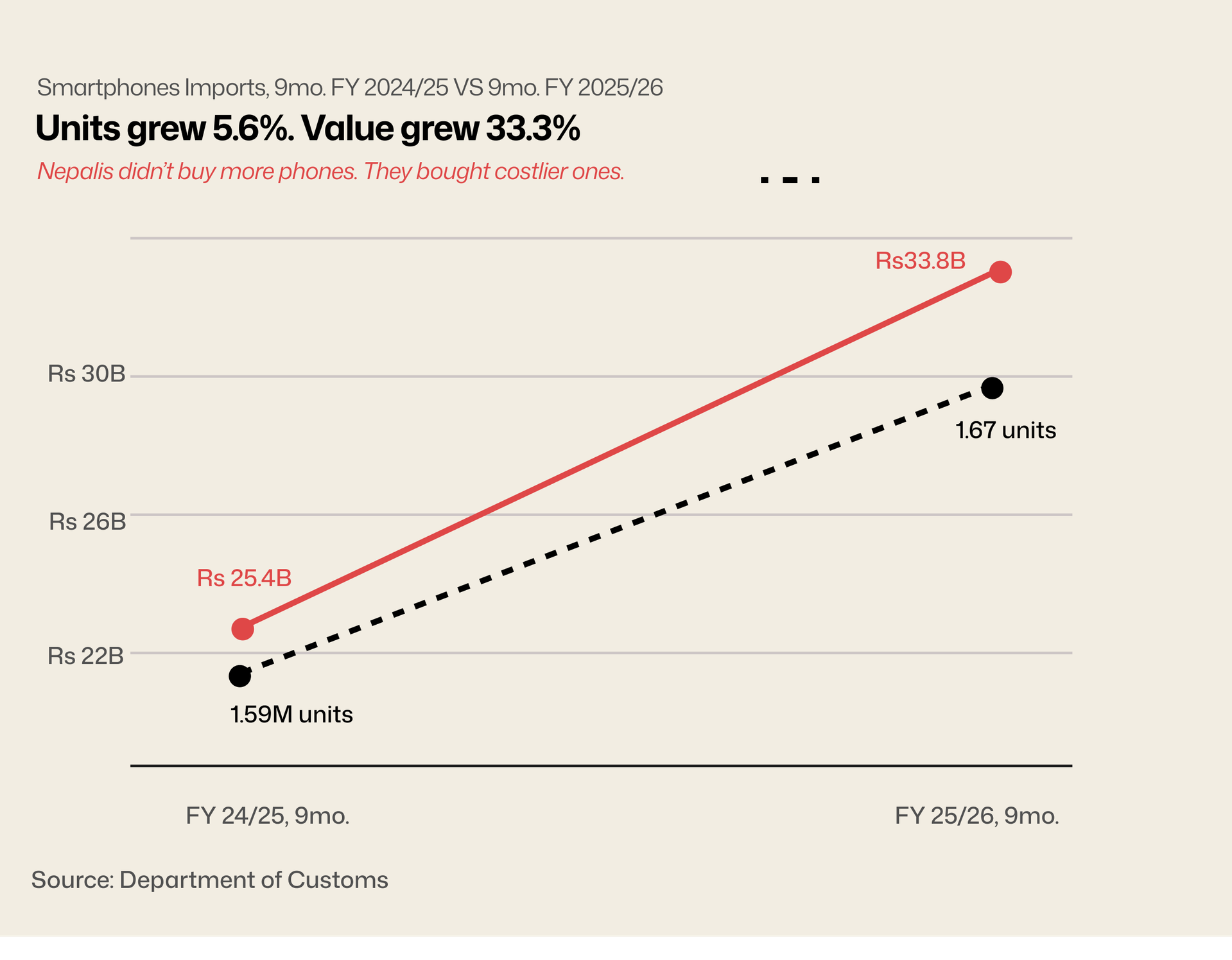

Smartphones cracked the top five imports for the first time. The story isn’t buying binge, volumes barely moved. The story is the rupee value per device: roughly sixteen thousand last year, twenty thousand this year. That’s either inflation, a mix shift towards premium models or both. Add custom duty to a higher landed value and revenue per import unit jumps, which is showing up at Birgunj where customs receipts are up 10% year-on-year on only 89% of target volume.

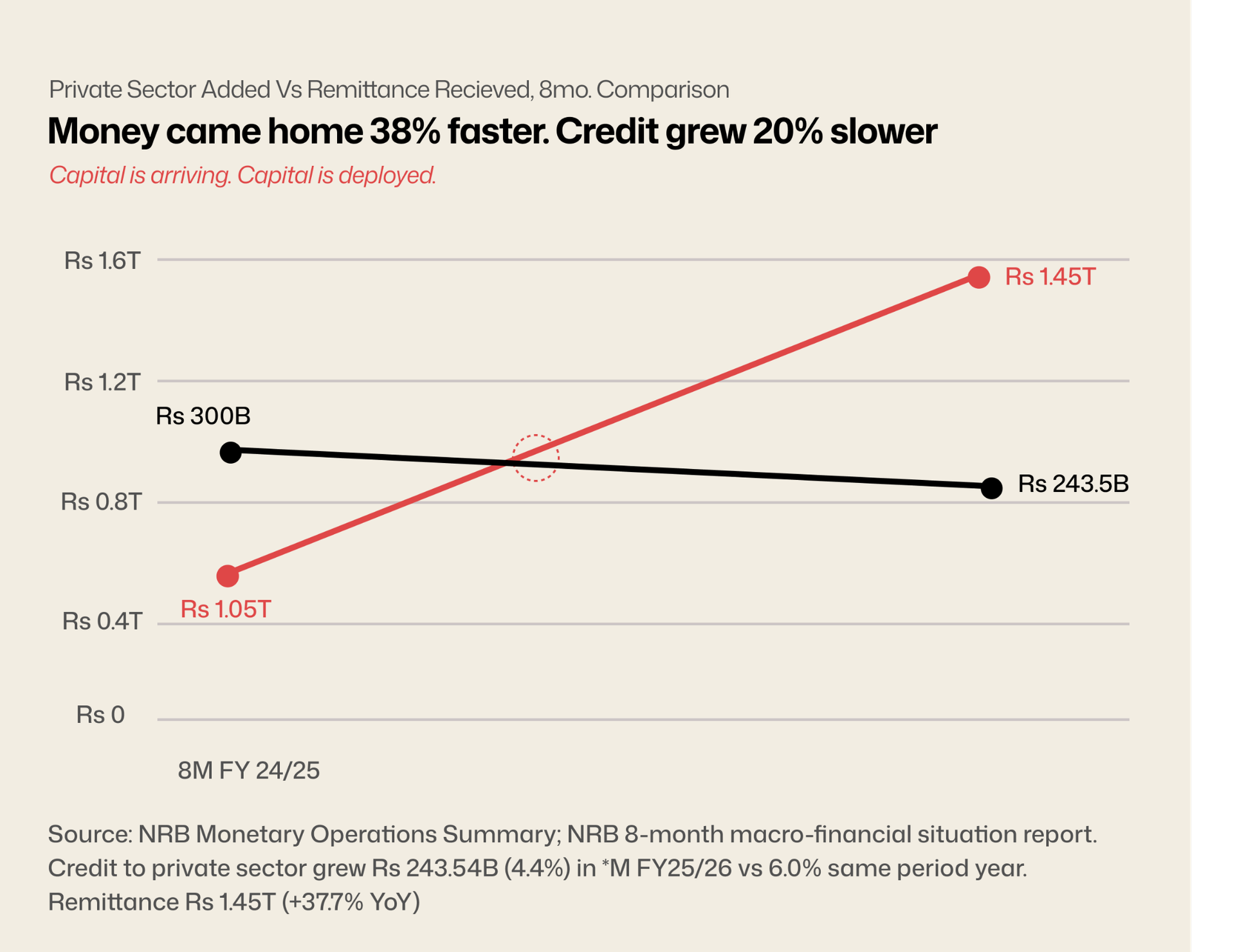

Refined soybean oil exports at Rs 90.71 billion are the headline of “Nepal exports oil.” The footnote is Rs 96.72 billion of crude soybean oil imported to make them. That’s a trading operation, not a manufacturing industry. Diesel has no matching export. Nor does rice. Nor LPG. Nor smartphones. The money leaving the country has to be financed by something, in Nepal’s case, remittances at Rs 1.45 trillion in eight months and up 37.7%. The capital is coming home. What it does after landing is the next story.

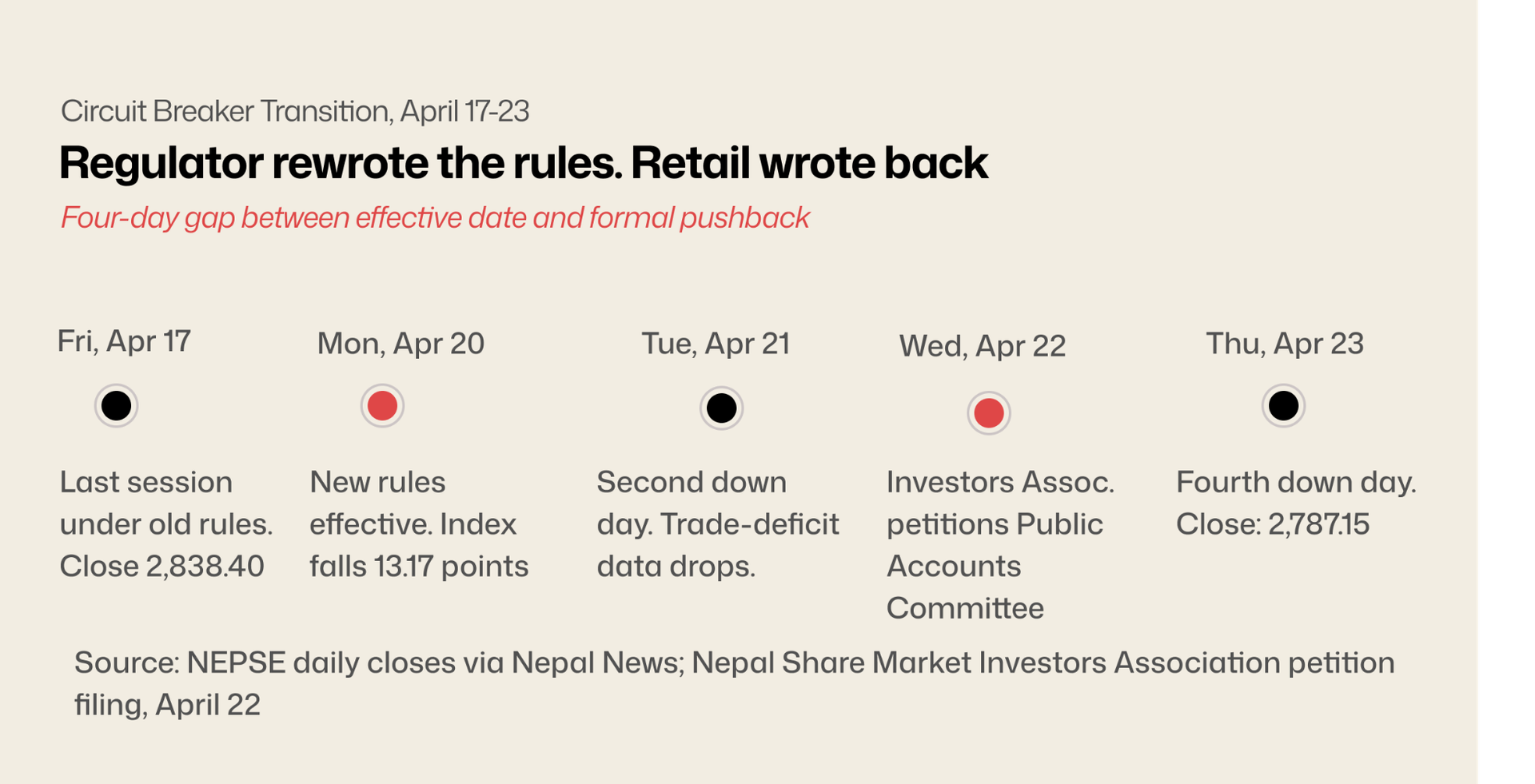

02. Markets: NEPSE got wider bands and went quieter

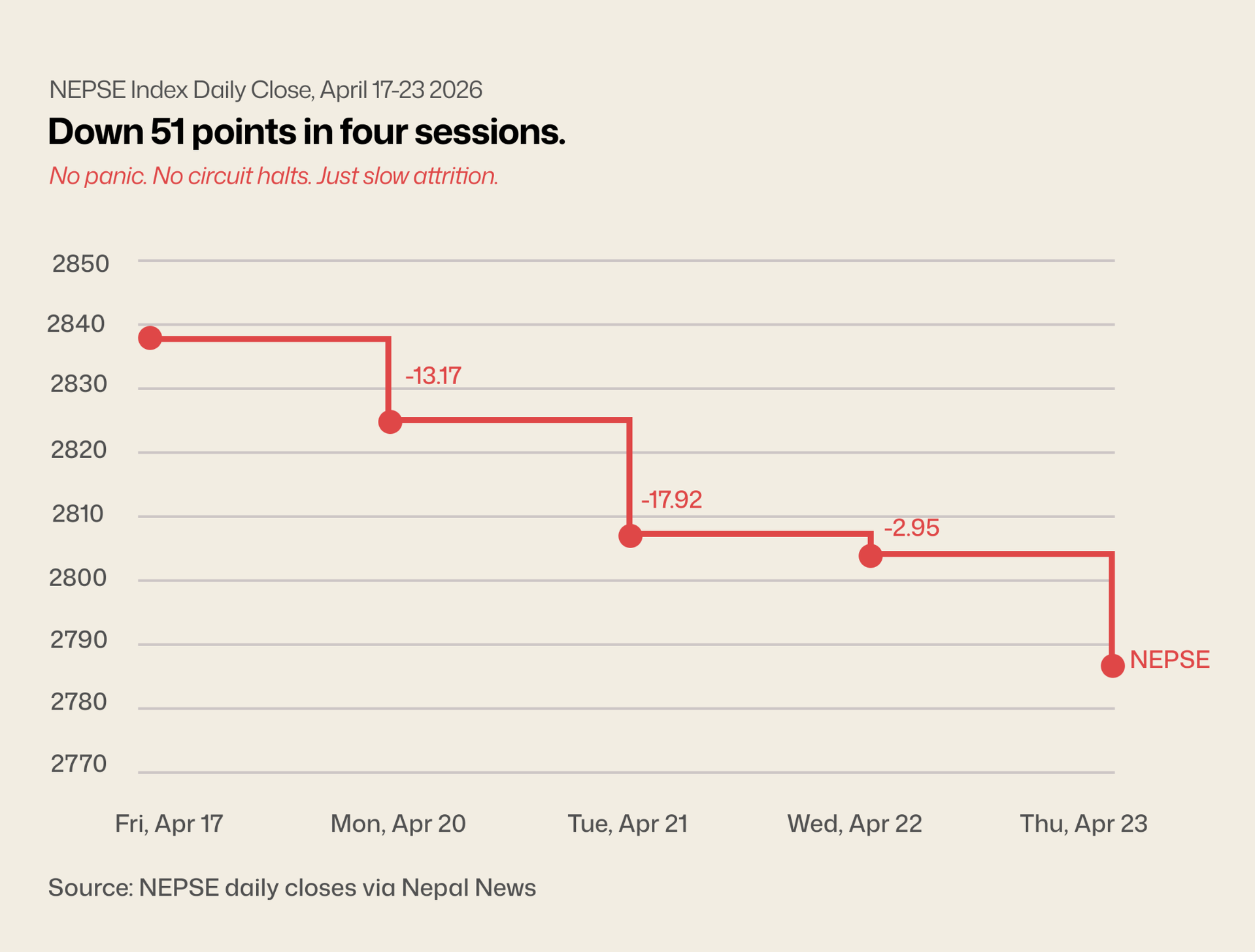

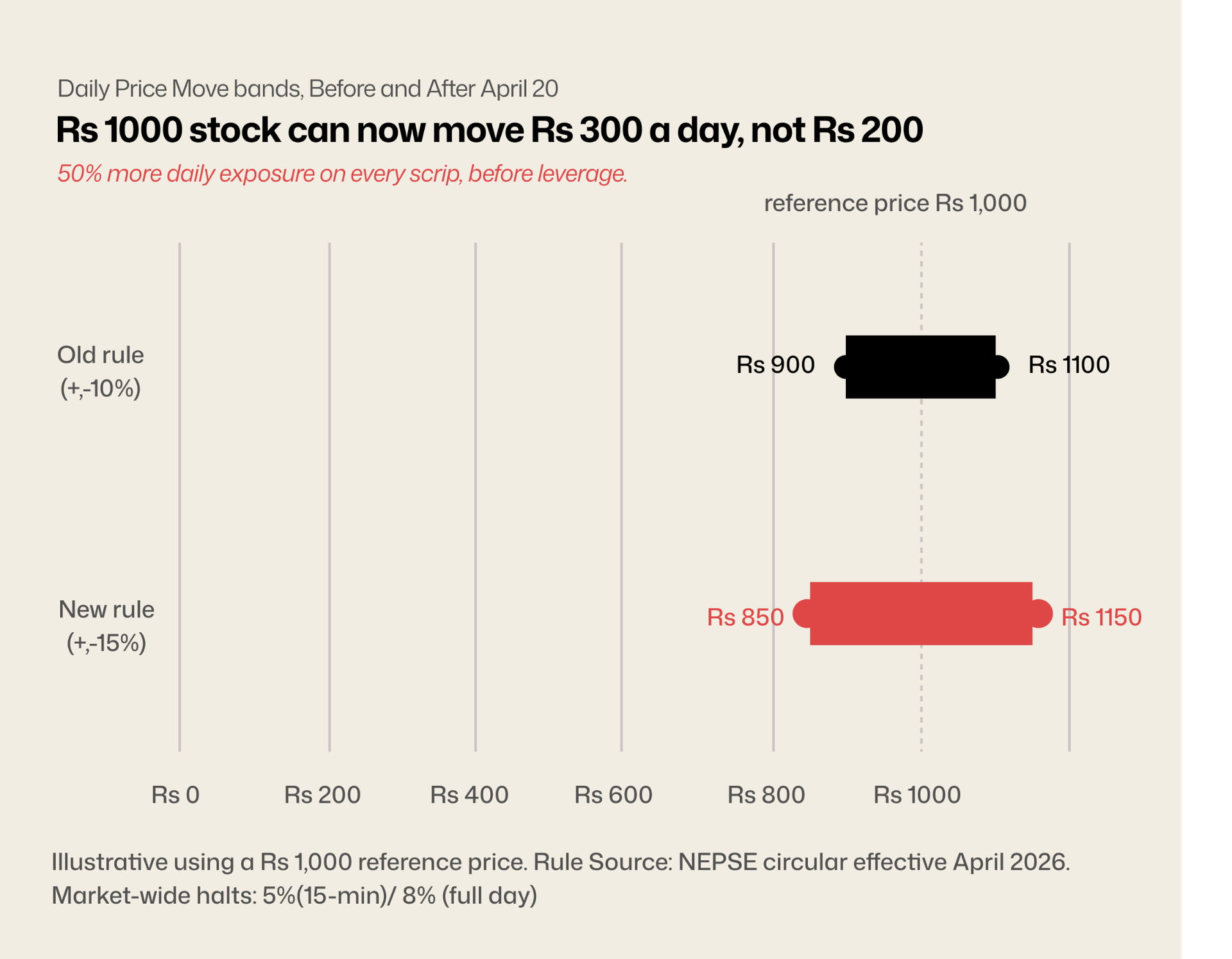

On APril 20, NEPSE activated new circuit breaker rules. Individual stocks can now swing 15% in a day, up from 10%. Market-wide halts trigger at 5% (15 minutes) and 8% (full day). The theory was that wider bands would let price discovery happen more freely. The practice was a market that drifted down every single day that week, on the smallest turnover in two months and a retail investor association petitioning Parliament by Wednesday.

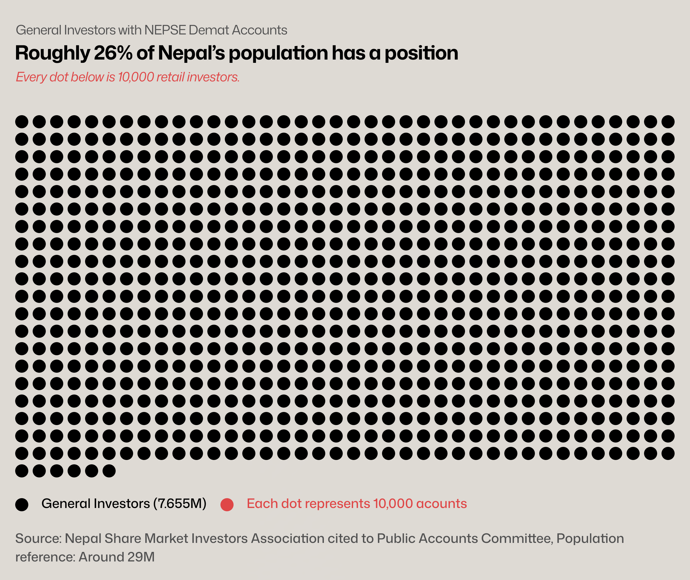

The Nepal Share Market Investors Association filed with the House of Representatives' Public Accounts Committee on April 22. Their argument: rules this consequential shouldn't pass without broader consultation. They claim changes passed "under the influence of interest groups." Whether that's true is unknowable. What's observable is that roughly 7.655 million demat account holders weren't asked, and most of them noticed.

This is not a circuit breaker week. No session came close to the new 5% threshold. The biggest single-day drop was -0.63% on Tuesday. Cumulative: -1.82% over four sessions. That's what a long, flat market looks like when nobody has conviction on either side. The bands exist. Nobody used them.

That 50% is what worries the association. A ten-lakh-rupee portfolio across five names saw its theoretical daily variance expand from Rs 100,000 to Rs 150,000, before margin trading which SEBON is also loosening. 7.655 million people have demat accounts. Most of them aren't using Greeks to size positions.

Total market capitalization: Rs 4.84 trillion as of mid-April, sits on those accounts. Banks are the heaviest weight in the index, and banks are sitting on a record cash pile they can't lend. SEBON widens the bands; NRB absorbs liquidity. Capital that can't find a borrower stops producing yield; the market that reflects bank earnings stops moving. That's where we go next.

03. Liquidity: Money everywhere. Credit nowhere.

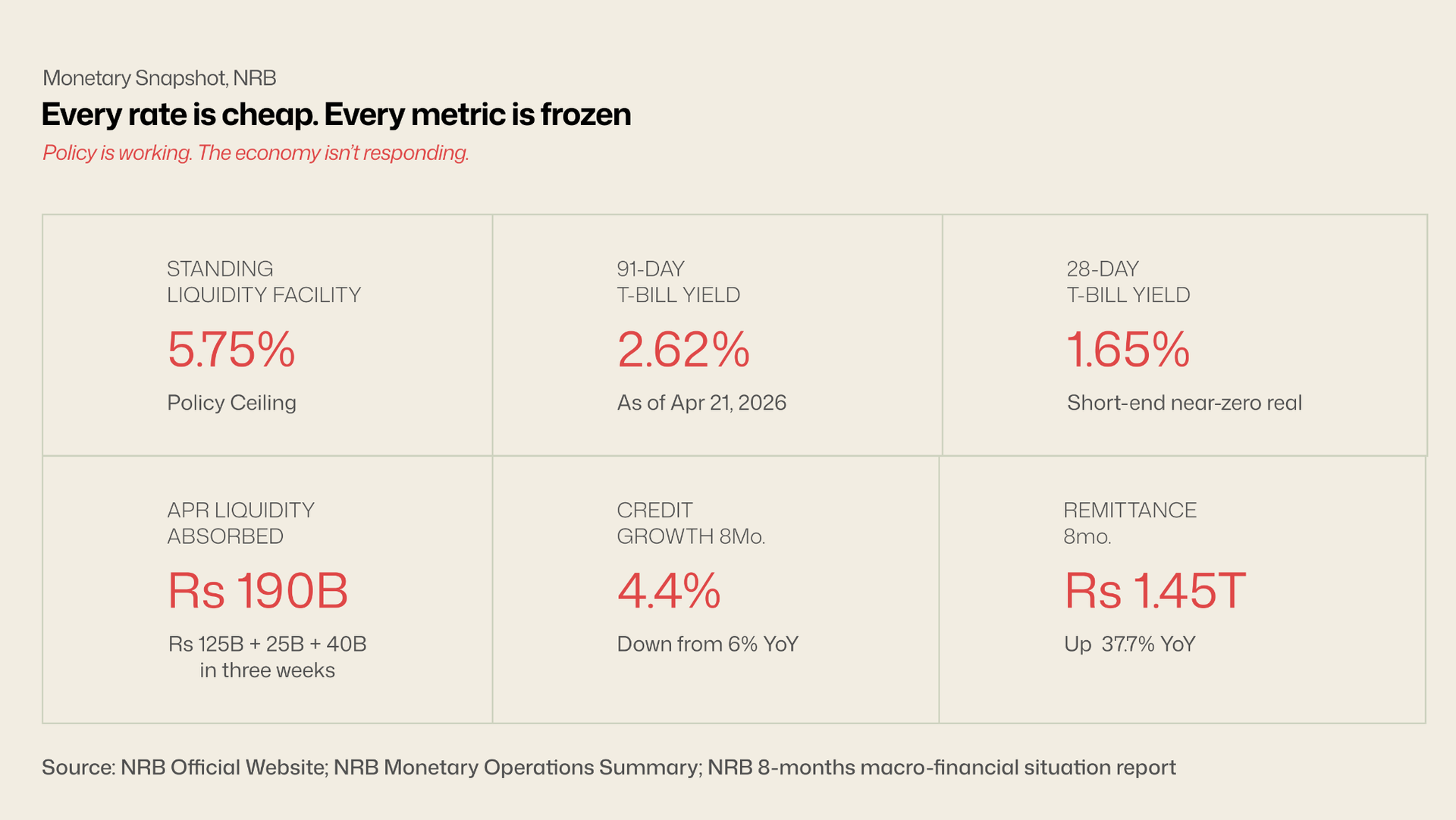

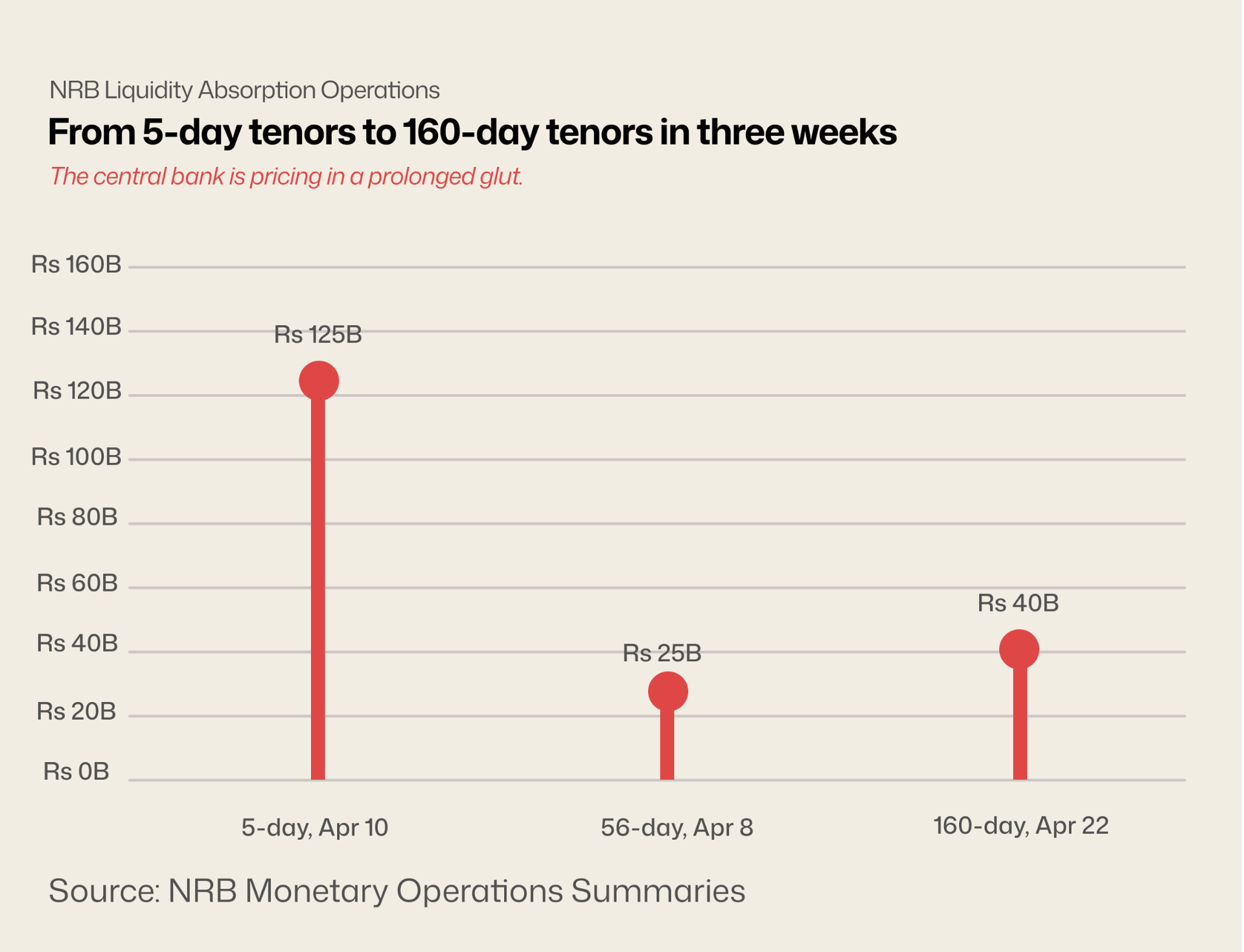

On April 22, Nepal Rastra Bank(NRB) announced a Rs 40 billion liquidity absorption via a 160 day deposit collection instrument, at a bid rate around 3%. Five months of parking, at a return that rounds to inflation. That is the longest-tenor pull of the year so far and the third major absorption operation in April alone. NRB does not pull money for months unless it expects the excess to persist for months.

Private sector credit grew by Rs 243.54 billion in the first eight months of FY 2025/26, a 4.4% expansion, down from 6% in the same period a year earlier. In absolute terms that's roughly Rs 60 billion less new credit than last year's comparable window. Festival season came and went. Credit demand should have peaked in November–December. It undershot. Bankers blame pre-election uncertainty, fuel prices up 70%, and the Middle East. Demand for working capital fell because the underlying activity didn't happen.

The 91-day T-bill yields 2.62%. The 28-day yields 1.65%. The interbank call rate is still lower. Short-term liquidity is priced at effectively zero and banks are paying depositors around the same. The transmission mechanism from rates to credit growth has broken or, more precisely, the rates are doing their job and the demand side isn't there. The real economy shows it next.

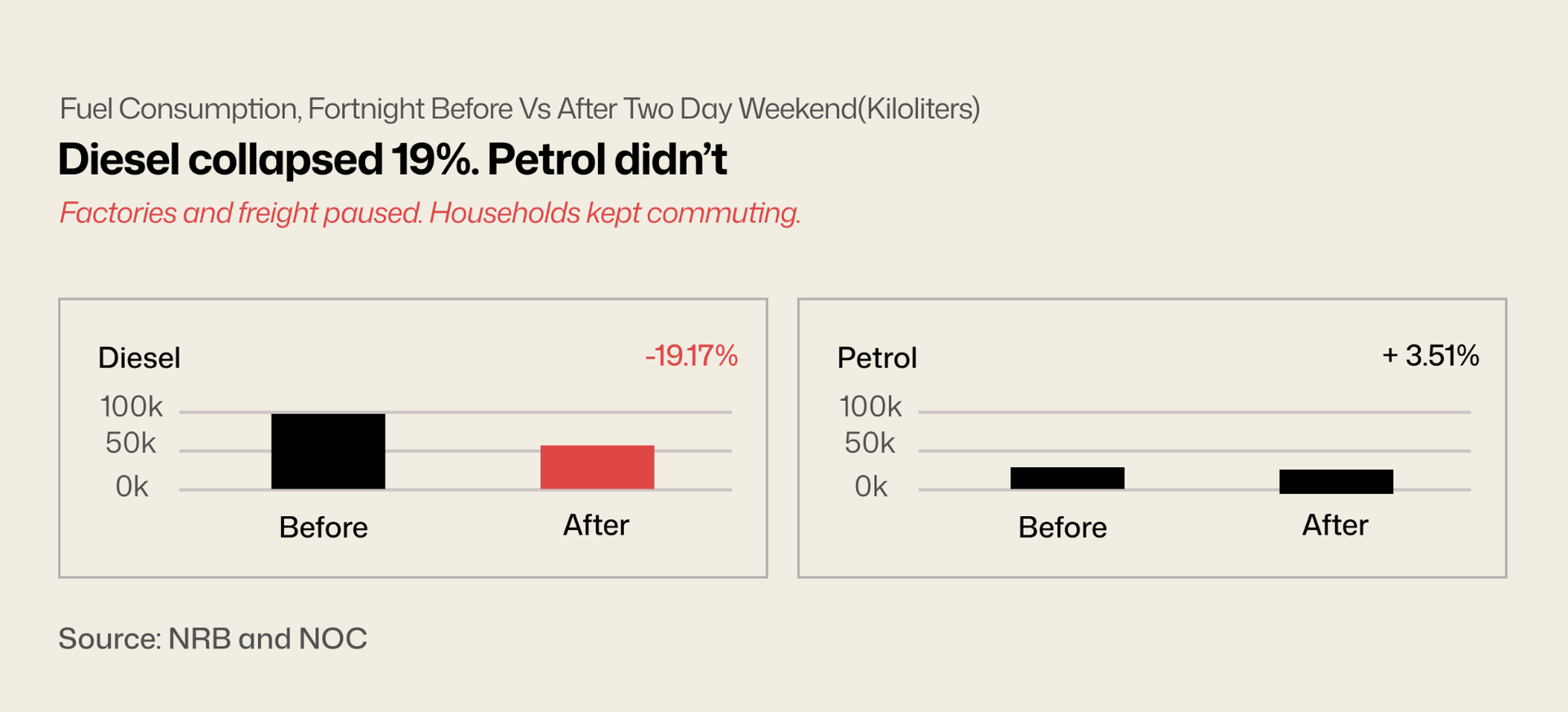

The government moved to a Saturday-Sunday weekend on April 5 specifically to cut fuel imports. The policy worked. Diesel sales fell from 96,566 kiloliters to 56,227. But diesel is what runs trucks, generators and industry. Petrol, which moves personal vehicles, actually rose. The collapse is not in consumption broadly. It's in productive, taxable, GDP-generating activity.

The three stories his week describe the same condition from three angles. The deficit says the money is spent on imports. The market says the capital that comes home has nowhere productive to go. The liquidity data says the banks holding it can't lend it out. Each fact was released in a different week, by a different institution;Customs, NEPSE, NRB. All three landed between Monday and Wednesday. Together they describe an economy where every loop is clogged. Demand is missing. Risk appetite is missing. The rules got looser and nothing moved. That is what "slow growth" looks like in real time.