Equity Research: Global IME Bank: The cost of getting big

Global IME Bank (GBIME) became Nepal’s largest commercial bank through an aggressive merger strategy that absorbed roughly twenty-one financial institutions.

Global IME absorbed roughly twenty-one institutions to become the largest bank in Nepal. This note asks a narrower question than whether that was good strategy: What does a shareholder own at around 1.3 times book a scale champion or a low-return aggregator still digesting its acquisitions? We take no view on the price; we lay out the evidence.

Global IME Bank (NEPSE: GBIME) is the largest commercial bank in Nepal by deposits, paid-up capital, branch network and net interest income. It reached that position not by out-growing its rivals but by absorbing roughly twenty-one banks and financial institutions folded into one balance sheet over a decade. The strategy succeeded on its own terms: GBIME is unambiguously the biggest. This note examines a different question, the one a buyer of the shares actually faces whether being the biggest has made it a good bank to own. The short answer the numbers give is: solid, but not superior, and priced accordingly. We assign no rating; the chapters below set out the case on both sides.

I. A Banking Empire Built on Deposits

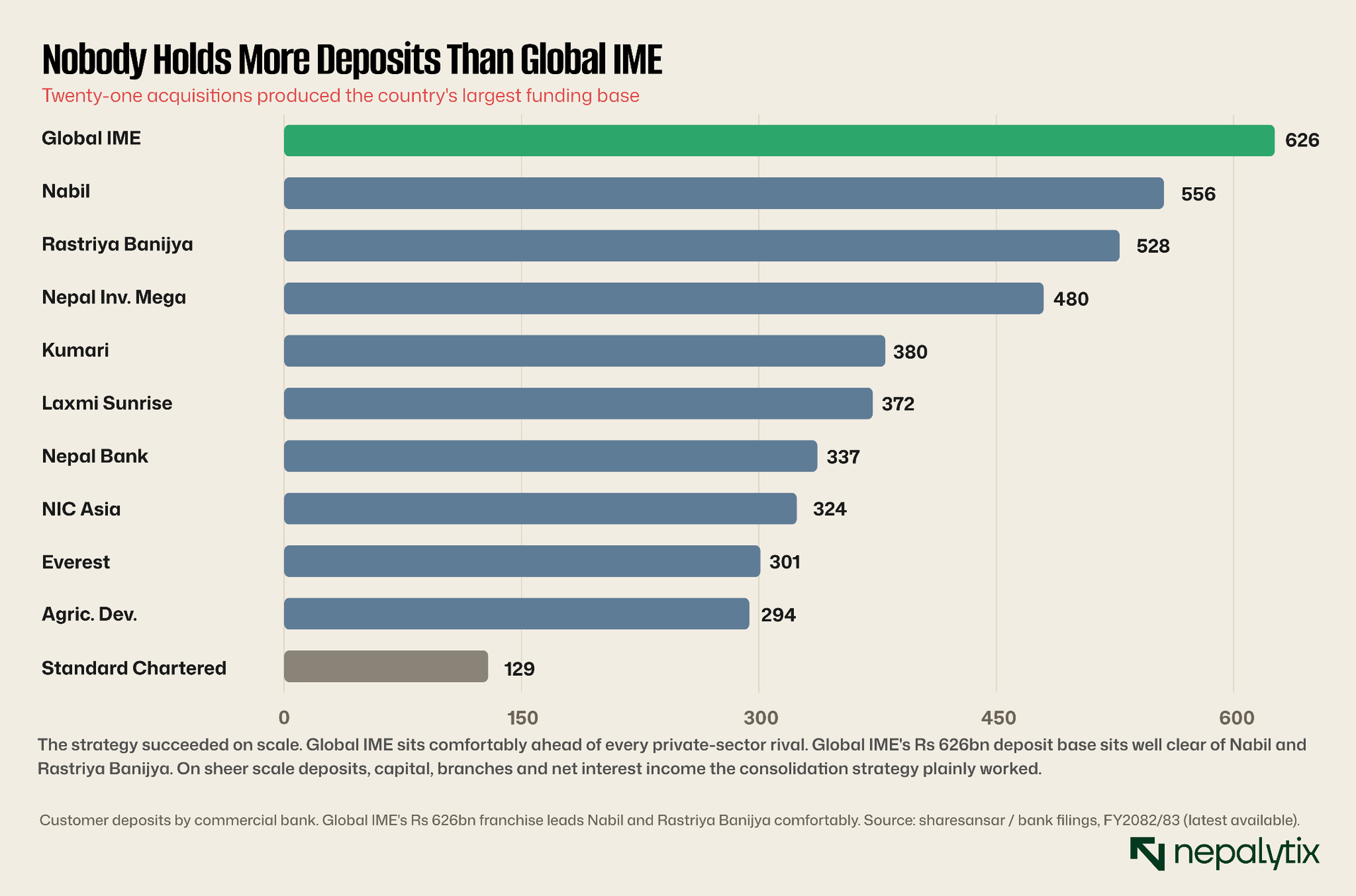

Starts with what the shareholder is buying. At the end of the third quarter of fiscal year 2082/83, Global IME held about Rs 626 billion in customer deposits and roughly Rs 439 billion in loans, the largest book in the country. Its paid-up capital of Rs 38.1 billion is the highest of any Nepali bank, its branch network of around 440 outlets is among the widest and in the first quarter of the year its net interest income led the entire commercial-banking sector. By every measure of size, this is the anchor institution of the Nepali banking system.

What the franchise looks like on the ground is a network of roughly 440 branches and extension counters reaching well beyond the Kathmandu valley, paired with one of the larger mobile- and internet-banking user bases in the country, the infrastructure behind the 'Bank for All' positioning the bank has long used. That reach is expensive to run, but it is also the moat: it gathers the low-cost deposits, distributes the remittances that flow through the IME network, and makes the institution genuinely national rather than a valley bank. The cost of maintaining it, however, is one more claim on the returns that never quite arrive.

The deposit league table is worth dwelling on because it is the single clearest piece of evidence for the bull case. Customer deposits are a bank's raw material and the institution that controls the most of them, most cheaply, starts every contest a step ahead. Global IME's Rs 626 billion base is not merely first; it is first by a margin over Nabil and the state-owned Rastriya Banijya and it dwarfs the focused high-return operators that beat it on profitability. If the funding scale alone determined the value, this chapter would be the whole note.

Scales of this kind are not cosmetic. A larger deposit base lowers the average cost of funding, a wider branch and digital network deepens the low-cost current and savings balances that protect a bank's margin and sheer size confers a systemic importance that shapes how the central bank and the market treat the institution in a stress. The deposit franchise visible above is the asset the entire merger programme was built to assemble and on that narrow test the programme worked. The question is what came attached to it.

The economics of that scale run through the cost of money. A bank's profit begins with the spread between what it pays for deposits and what it earns on loans and the cheapest deposits are the current and savings balances customers leave largely idle. A franchise of Global IME's reach 440 branches, a large remittance business inherited from its IME parentage, one of the country's bigger digital footprints is built to gather exactly those low-cost balances at volume. In principle that confers a structural funding advantage over smaller rivals, and in net interest income where the bank leads the sector, the advantage is visible.

Scale carries a less quantifiable benefit too: systemic weight. As the largest deposit-taker in the country, Global IME is the kind of institution a central bank cannot let fail, and that implicit backstop steadies its funding when smaller banks face runs. For a depositor this is reassurance; for a shareholder it is double-edged, since the same importance invites closer scrutiny, higher capital expectations and a seat at the front of every policy-driven merger. The franchise is genuinely valuable. Whether that value reaches the bottom line is the question the returns must answer.

II. Twenty-One Institutions Became One Bank

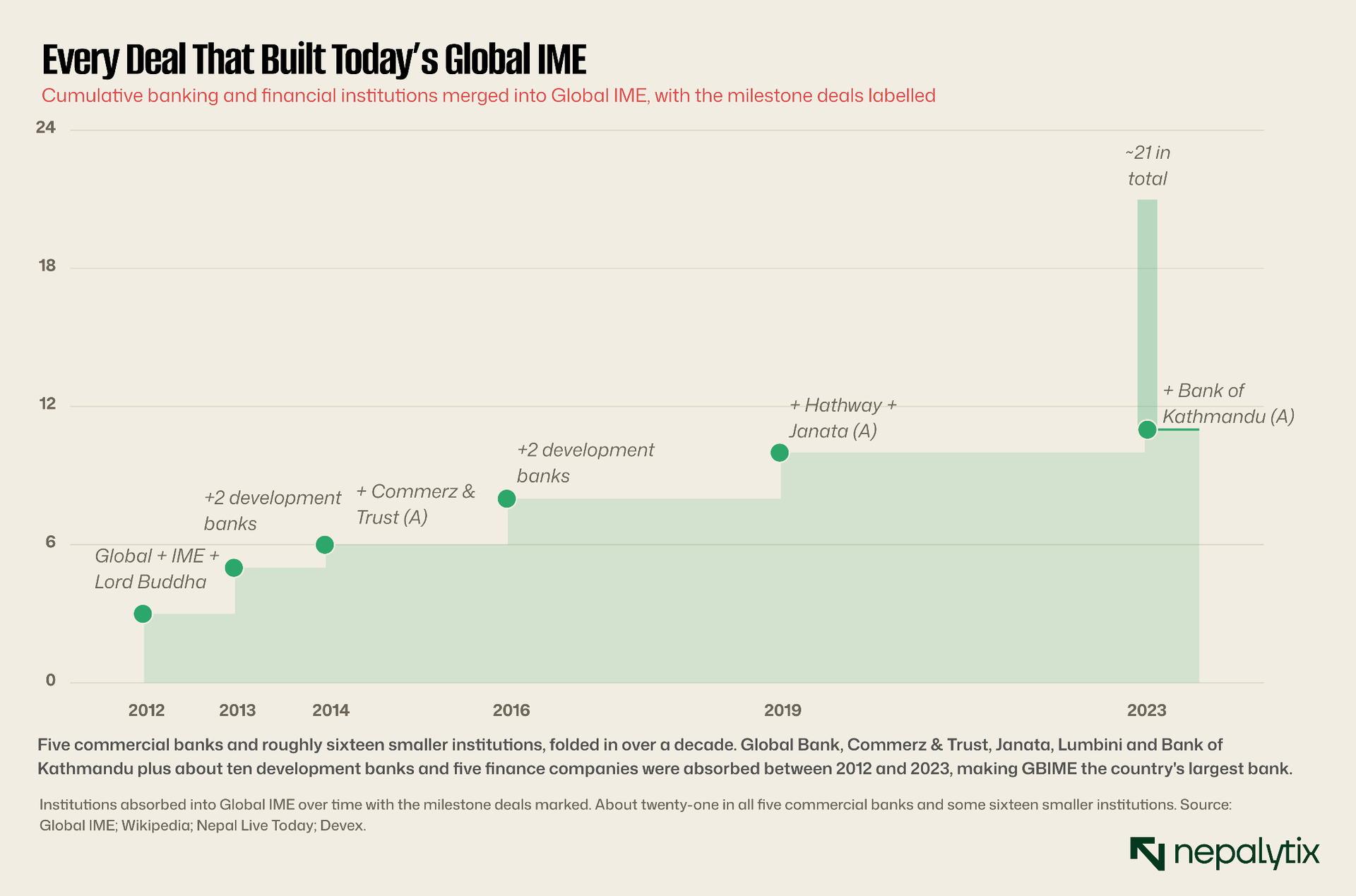

Global IME's size is the residue of the most aggressive consolidation strategy in Nepali banking. The bank that trades today as GBIME began as Global Bank an 'A'-class commercial bank licensed in 2007. In 2012 it merged with IME Financial and Lord Buddha Finance and took its current name; from there the acquisitions came almost yearly.

Two development banks followed in 2013; Commerz and Trust Bank, an 'A'-class commercial bank, in 2014; two more development banks in 2015-16; Hathway Finance and Janata Bank, another commercial bank in 2019; and finally Bank of Kathmandu in January 2023, the deal that made GBIME the largest bank in the country. In total the group has folded in roughly twenty-one banking and financial institutions, five of them commercial banks (Global, Commerz & Trust, Janata, Lumbini and Bank of Kathmandu), alongside about ten development banks and five finance companies.

This was, in large part, policy working as intended. Nepal Rastra Bank spent the past decade pushing the sector to consolidate through capital requirements and merger incentives and Global IME was the most willing participant. But a merger is not free and the costs do not all appear in the year the deal closes. Integrating twenty-one institutions means reconciling that many loan books, cultures, branch overlaps and information systems; it means inheriting the weakest assets of the acquired alongside the best; and, crucially for the shareholder, it means paying for the targets overwhelmingly in newly issued shares. The franchise in Chapter I was assembled. The bill arrives in the chapters that follow.

On the narrow test of scale, the merger programme worked. The question is what came attached to the size.

This was not empire-building for its own sake. Nepal Rastra Bank spent the 2010s deliberately shrinking the number of banks raising minimum paid-up capital roughly four-fold in 2015 and offering tax and regulatory incentives to merge precisely to forge fewer, sturdier institutions from a crowded field. Global IME chaired by Chandra Prasad Dhakal of the IME remittance group, read that direction earlier and more aggressively than anyone and turned it into a growth engine. In that sense the bank is the clearest single expression of a decade of national banking policy.

But serial acquisition is among the hardest strategies to execute and the difficulties compound with each deal. Every target brings a core-banking system to reconcile, a credit culture to harmonise, overlapping branches to rationalise, staff to integrate and, less visibly, a legacy of weaker loans inherited in full. A bank that has done this twenty-one times carries twenty-one layers of integration and the benefits that justify a merger cost synergies, cross-selling, a cleaner combined book tend to arrive slowly and partially, while the costs land at once. The returns are where one tests whether the synergies ever showed up.

III. Biggest Bank. Average Economics

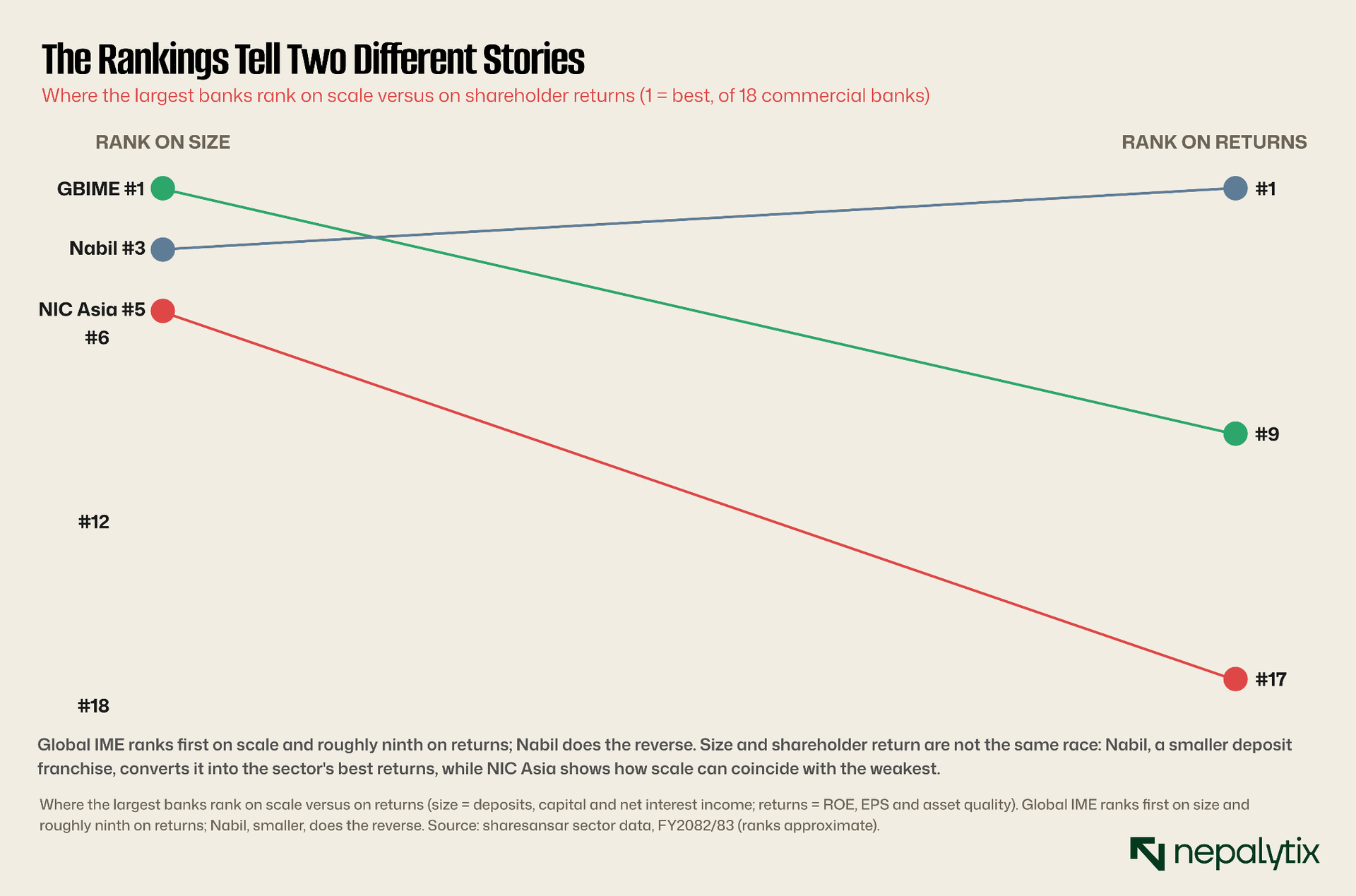

If consolidation created value for shareholders, it should show up as superior returns on the capital they have invested. It does not. On the metrics that matter to an owner return on equity, earnings per share, asset quality Global IME ranks far lower than it does on size.

Set the franchise against the book it sits on. Global IME's net worth per share, at roughly Rs 178 is close to the industry average of about Rs 200 middling and a long way below the Rs 340 of Rastriya Banijya or the Rs 260 of Nepal Bank, whose decades of retained earnings have built far thicker per-share capital. A bank that grew by issuing shares rather than by compounding retained profit ends up almost by definition with more shares each backed by less book. That is the structural starting point for the return gap that follows.

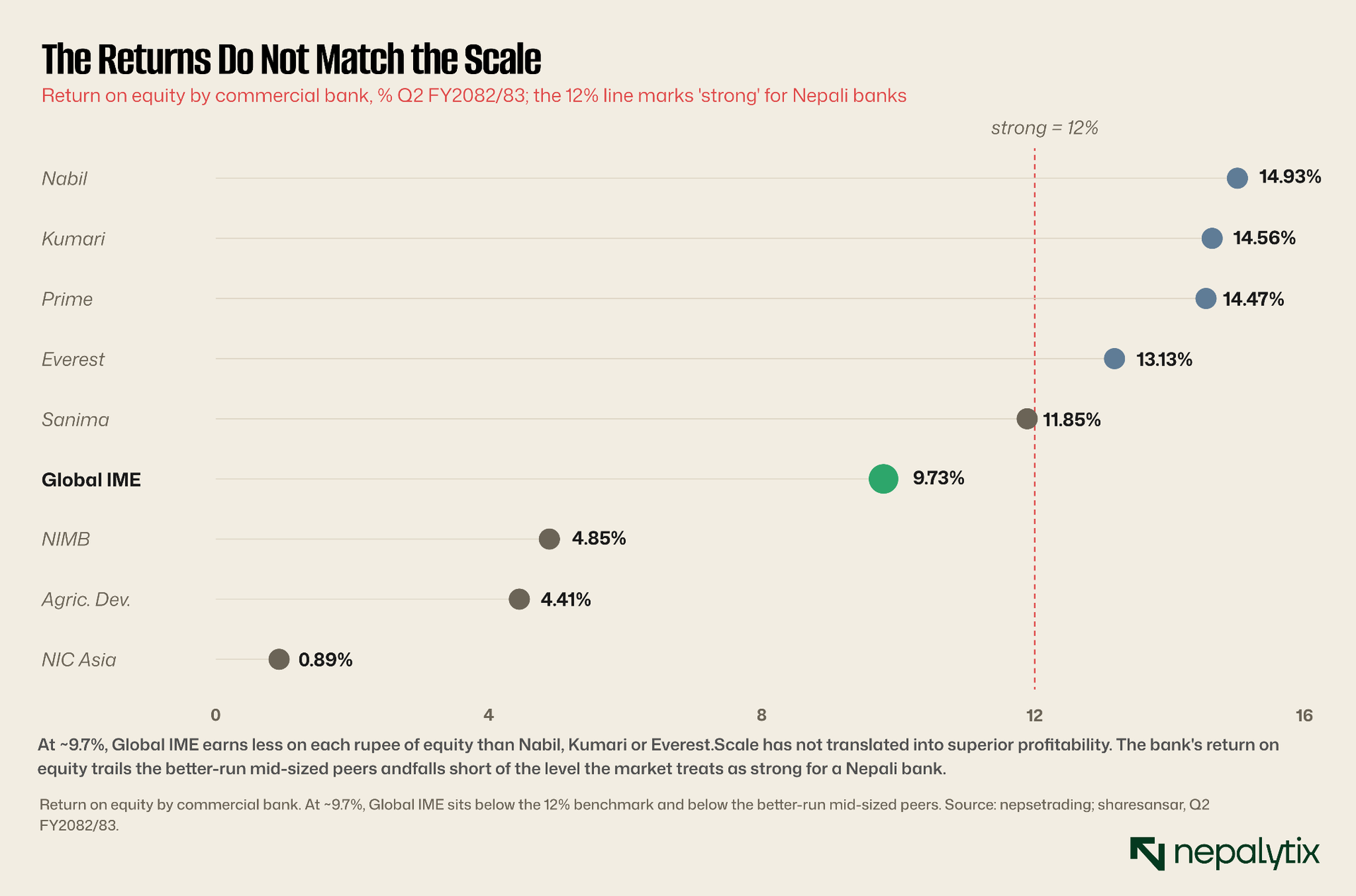

The clearest single statement of the problem is the bank's return on equity. In the second quarter of 2082/83 Global IME earned about 9.7% on its equity. That is below the roughly 12% the market treats as the mark of a strong Nepali bank and well below the 13-15% that Nabil, Kumari, Prime and Everest were generating in the same quarter. A rupee of equity entrusted to Global IME simply produced less profit than the same rupee at several smaller, more focused competitors.

Part of what Global IME inherited from its IME lineage is a remittance franchise unusual among Nepali banks. IME is one of the country's largest money-transfer networks and remittances equivalent to roughly a quarter of Nepal's GDP flow through it into deposit balances and fee income in a way few competitors can match. In principle this is a structural advantage: a low-cost, sticky source of both funding and non-interest revenue tied to the single largest external inflow into the economy. That it has not lifted returns above the pack suggests the advantage is being competed away in deposit pricing or absorbed by the cost of the sprawling network that captures it, the recurring theme of this note, in which genuine franchise strengths keep failing to reach the bottom line.

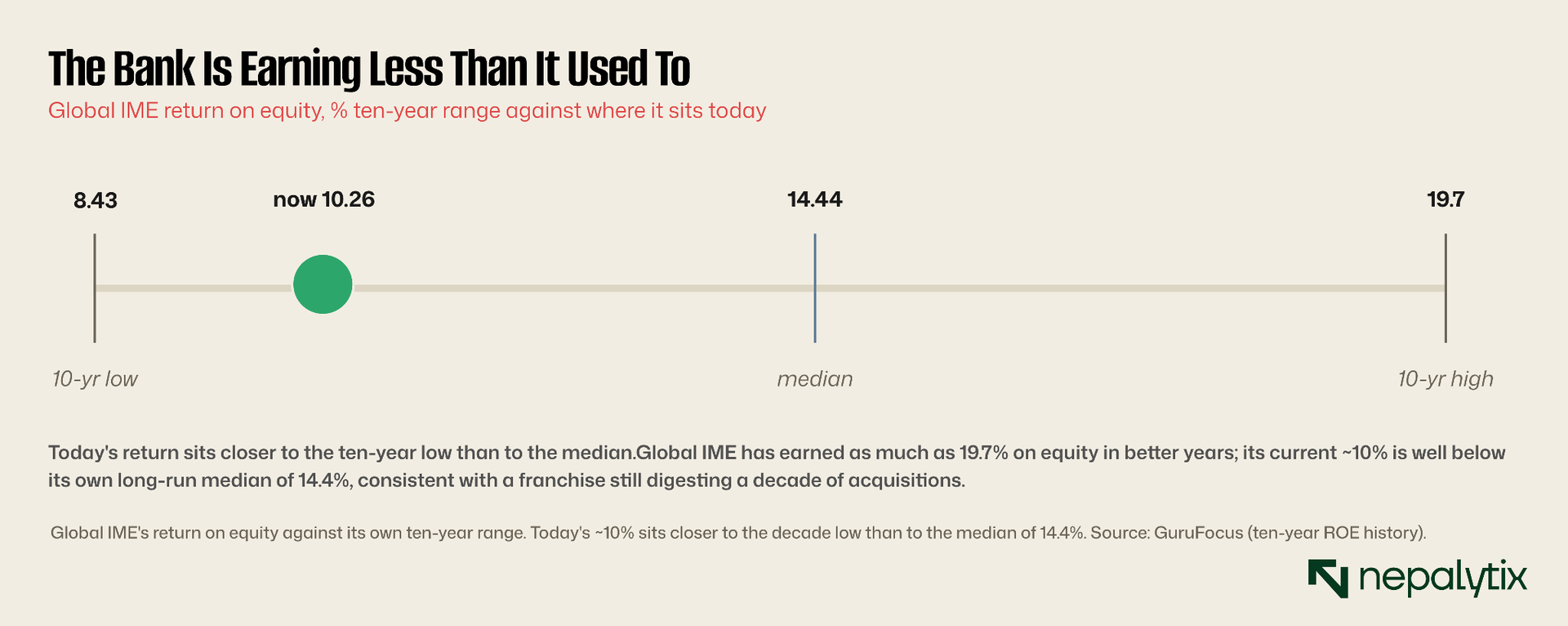

Nor is this a single weak quarter. Measured against its own decade, Global IME's current return sits close to the bottom of its range; it has earned as much as 19.7% on equity in stronger years and a long-run median near 14.4%. The compression to roughly 10% is consistent with a bank still absorbing the dilution and the weaker assets of its acquisitions rather than one hitting a temporary air pocket.

The integration record is the natural place to look for the missing returns, and it is mixed. A well-executed merger should, within two or three years, lower the combined cost-to-income ratio as duplicate branches, systems and back-office functions are stripped out, so the acquirer emerges leaner than the sum of its parts. Global IME's persistent mid-pack returns through a decade of deals suggest those efficiencies have been partial at best; each new acquisition appears to have reset the integration clock before the previous one fully delivered. Whether the Bank of Kathmandu merger, the largest and most recent, finally breaks that pattern is the single most important operational question for the next two years.

The pattern first on size, mid-pack on return is the central fact of the investment case. It is not unique to Global IME; large, serially acquisitive institutions the world over tend to trade growth in assets for discipline in returns. But it does mean that an investor buying GBIME for its scale should be clear that scale and profitability have, so far, pulled in different directions.

It helps to take the return apart. Return on equity is the product of how much a bank earns on its assets and how heavily those assets are leveraged over its equity, and Global IME's problem sits on the asset side. Its net interest margin squeezed by the cost of chasing deposits and by interest it cannot collect on non-performing loans is unexceptional; its fee income is solid but not transformative and provisioning takes a further bite before profit reaches shareholders. Layered on top is an equity base swollen by years of merger-funding share issuance, which enlarges the denominator of the calculation. A bigger bottom on the fraction, a squeezed top: a return that has settled near 10%.

The pattern is familiar internationally. Banks that grow chiefly by acquisition tend to trade returns for size the acquirer pays a premium, dilutes its own holders to fund the deal and spends years absorbing the target before efficiencies show by which point the next deal has begun the cycle again. The most valuable banks in most markets are rarely the largest; they are the disciplined mid-sized operators with the highest returns on capital exactly the place Nabil, Kumari and Everest occupy in the Nepali data. Global IME chose the other path; whether that served shareholders, as opposed to the bank's standing and the sector's structure, is the crux of this note.

IV. The Hidden Cost of Endless Mergers

Why has size not produced per-share value? The answer lies in how the size was paid for. Almost every acquisition was settled in stock, so each deal that added deposits and branches also added shares and earnings, however much they grew in absolute terms had to be divided across an ever-larger count.

Capital adequacy frames the same story from the regulator's side. Global IME runs a capital-adequacy ratio around 13% comfortably above the 11% regulatory floor but well short of the 18.6% that Standard Chartered, the sector's most conservatively run bank, carries. That gap is telling: the largest bank holds among the thinner capital buffers relative to its risk-weighted assets, which is part of why it has leaned so heavily on bonus shares to stay compliant as it grew. Adequate capital and abundant capital are different things, and for the systemic anchor of the system the distinction is not trivial.

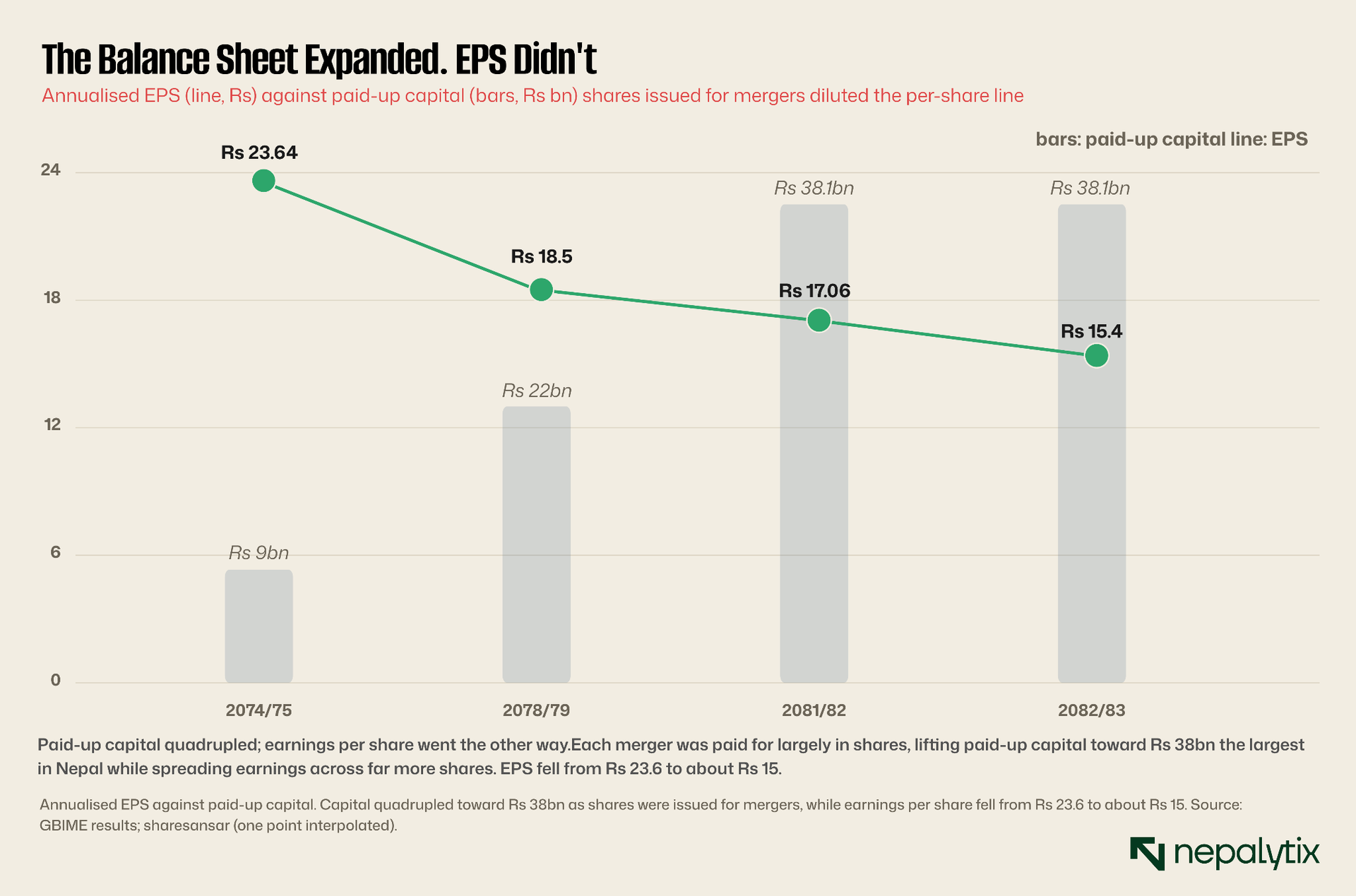

The picture is stark. Global IME's paid-up capital has risen toward Rs 38 billion, the largest in Nepal while its annualised earnings per share have fallen from about Rs 23.6 in 2074/75 to roughly Rs 15.4 by the third quarter of 2082/83. The bank earns more total profit than it used to; each share simply owns a thinner slice of it. For a shareholder, this is the mechanism that turns an impressive growth story into an ordinary holding: the company gets bigger, the stock does not necessarily get more valuable. Bonus shares and rights issued to fund and capitalise the mergers are the unglamorous arithmetic behind the return gap in Chapter III.

The bank earns more total profit than it used to. Each share simply owns a thinner slice of it. \

The contrast between total profit and per-share profit is the cleanest way to see the cost. Global IME earned around Rs 6 billion in net profit in fiscal 2080/81 a large absolute figure, among the biggest in the sector and exactly what a press release leads with. Spread across the Rs 38 billion of paid-up capital the mergers required, it translates into ordinary per-share earnings and a sub-par return. Bonus shares, the favoured tool for both capitalising mergers and meeting the regulator's capital floor are the quiet agents: each one issued enlarges the share count without putting new cash to work at a high return, so headline profit and per-share value drift apart. A shareholder is paid in the latter.

V. Scale Also Means Bigger Mistakes

The second drag on returns is credit. Like most of the sector, Global IME has seen its non-performing loan ratio climb steeply through the post-pandemic credit cycle but as the largest lender, it carries the largest absolute book of problem loans, and the provisions against them flow straight through the income statement.

Two technical points qualify the headline NPL number in opposite directions. On the reassuring side, a rising ratio is partly a denominator effect: as loan growth slows in a tight cycle even a stable stock of bad loans rises as a percentage and a portion of the increase reflects stricter classification rather than fresh defaults. On the cautious side, the ratio captures only loans already recognised as non-performing; the more telling questions for the largest lender are how fully those loans are provisioned, how concentrated the book is in the stressed real-estate and construction sectors, and how much restructured credit sits one reclassification away from the non-performing column. Those details, buried in the notes to the accounts, matter more than the single ratio on the cover.

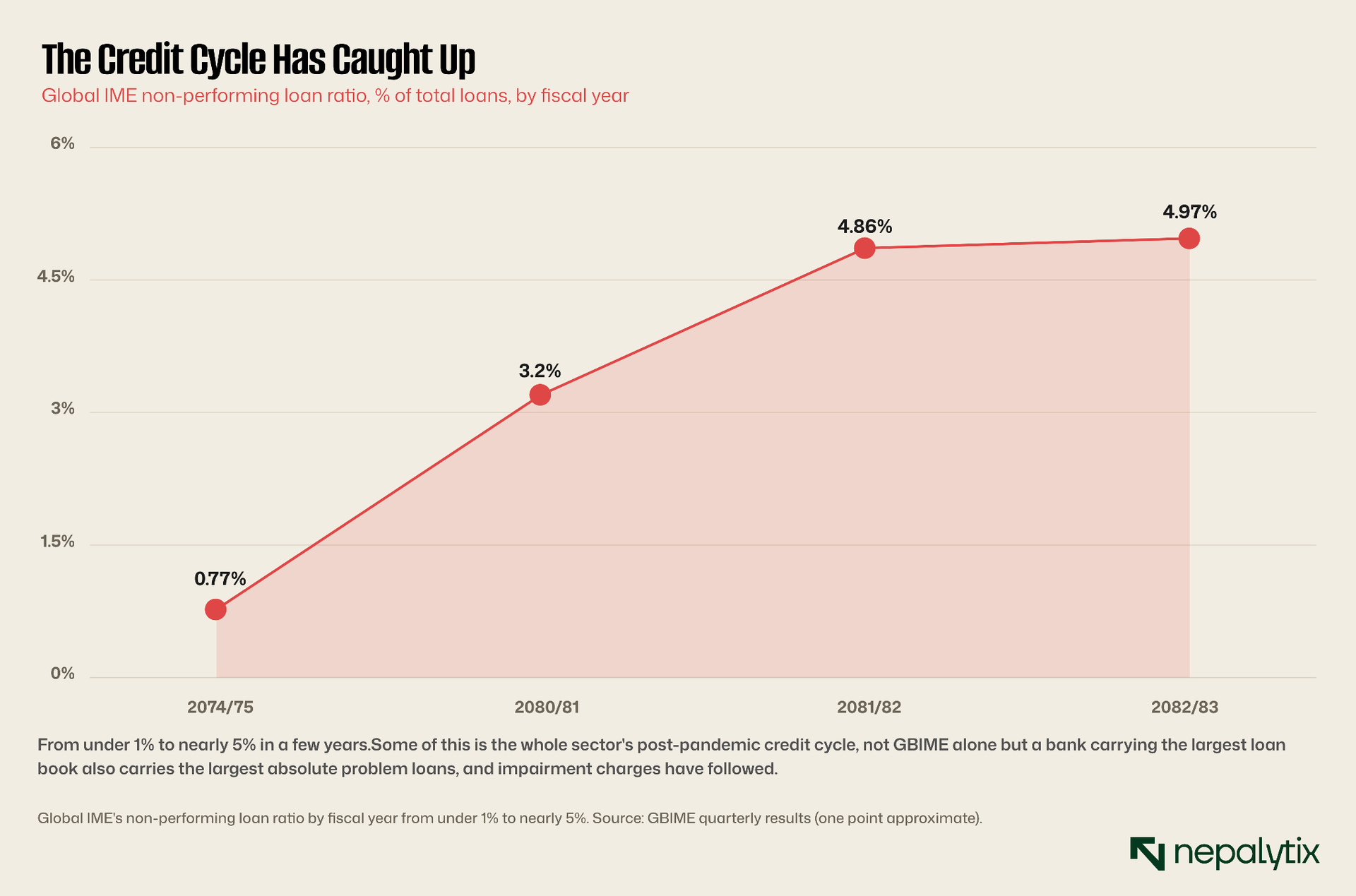

The ratio has moved from under 1% a few years ago to 4.97% in the third quarter of 2082/83. Part of that is industry-wide: a construction and real-estate slowdown, stretched borrowers and tighter classification have pushed bad loans up across nearly every Nepali bank. But the level matters, and on a Rs 439 billion loan book a 5% NPL ratio represents a very large absolute sum of impaired credit.

It is worth converting the ratio into a number. Roughly 5% of a Rs 439 billion loan book is on the order of Rs 22 billion of non-performing credit, a sum larger than the entire loan book of several smaller commercial banks. The percentage places Global IME in the middle of the pack; the rupee figure places it, unavoidably, at the top, because it lends more than anyone else. This is the recurring asymmetry of being the largest: average ratios produce systemic absolute exposures, and the bank that anchors the system is the one whose problem loans would matter most to it.

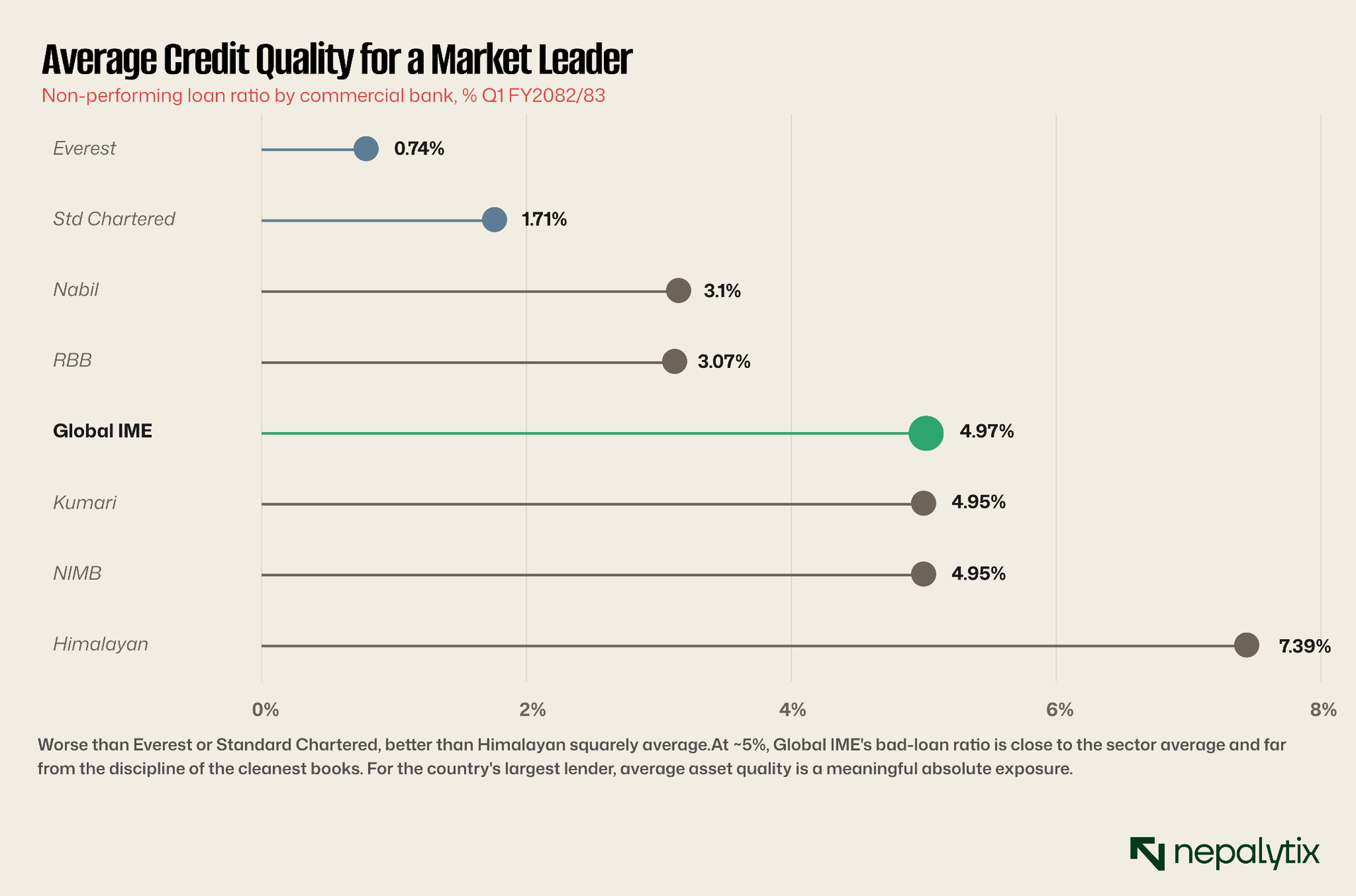

Against peers, Global IME is squarely average on asset quality a long way from the sub-1% discipline of Everest, but well clear of the most troubled books such as Himalayan's 7.4%. Average, however, is an uncomfortable place for the country's largest lender to sit: it means the systemic institution is carrying systemic-sized problem loans not setting the standard for the sector it anchors.

The margin tells the same story from the funding side. Nepal's competitive deposit market and the regulator's cap on the interest spread leave little room for any bank to earn an outsized margin and Global IME, for all its low-cost remittance balances, runs a net interest spread broadly in line with the sector's roughly 3.8-4%. Its advantage such as it is, comes from volume rather than price earning a thin sector margin on the largest asset base. That is a perfectly viable model but a low-return one by construction and it explains why leading the sector on net interest income does not translate into leading it on profitability.

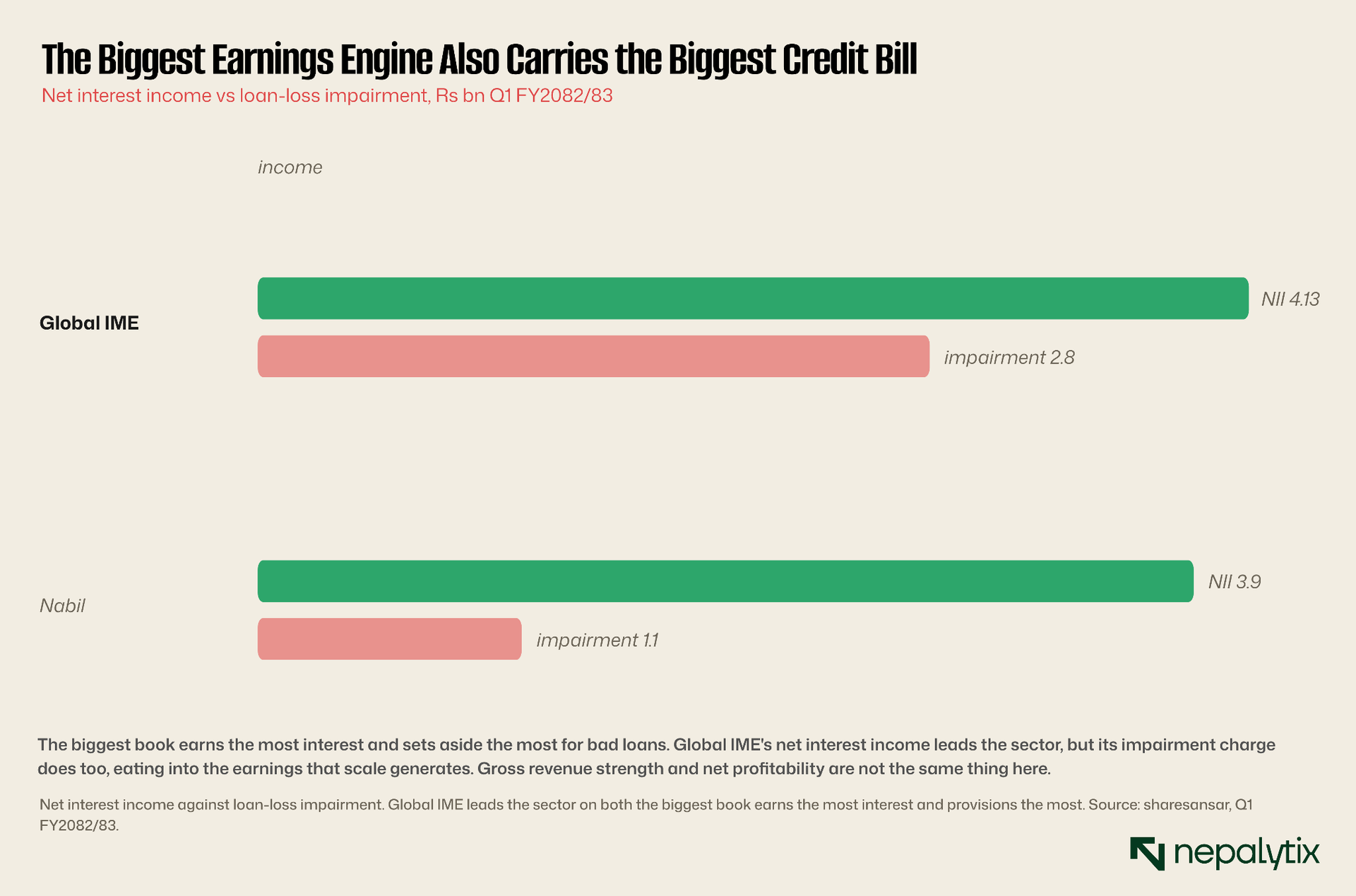

The income statement shows the tension directly. Global IME generates more net interest income than any other bank the reward for its scale but it also booked the sector's largest impairment charge around Rs 2.8 billion in a single quarter. Strong gross revenue and modest net profitability can coexist when provisions are this heavy, and that is precisely the combination Global IME has been running: a powerful top line, eroded on the way down.

The drivers of the deterioration are largely the sector's, not the bank's alone. Nepal's post-pandemic years brought a sharp real-estate and construction slowdown, an import-driven liquidity squeeze, stretched borrowers and tighter loan-classification rules - a combination that pushed bad loans up across nearly every commercial bank. Global IME sits inside that cycle rather than apart from it, and its ~5% ratio is close to the sector mean rather than an outlier.

What singles the bank out is scale and inheritance. A 5% ratio on a Rs 439 billion book is a very large absolute sum of impaired credit well over Rs 20 billion and the provisions against it are correspondingly heavy, which is why GBIME booked the sector's single largest impairment charge in the quarter examined. Some of those problem loans, moreover, were not originated by Global IME at all but inherited through acquisition: absorb twenty-one institutions and you absorb their weakest credits along with their deposits and the clean-up runs through the acquirer's income statement for years. The asset-quality drag, like the dilution, is partly the bill for the growth.

VI. A Fair Price for a Fair Business

A below-average return need not make a bad investment if the price is low enough. So the final question is whether the market is discounting Global IME for its modest returns or charging full freight for its size. The evidence points to the latter: the stock is priced fairly, not cheaply.

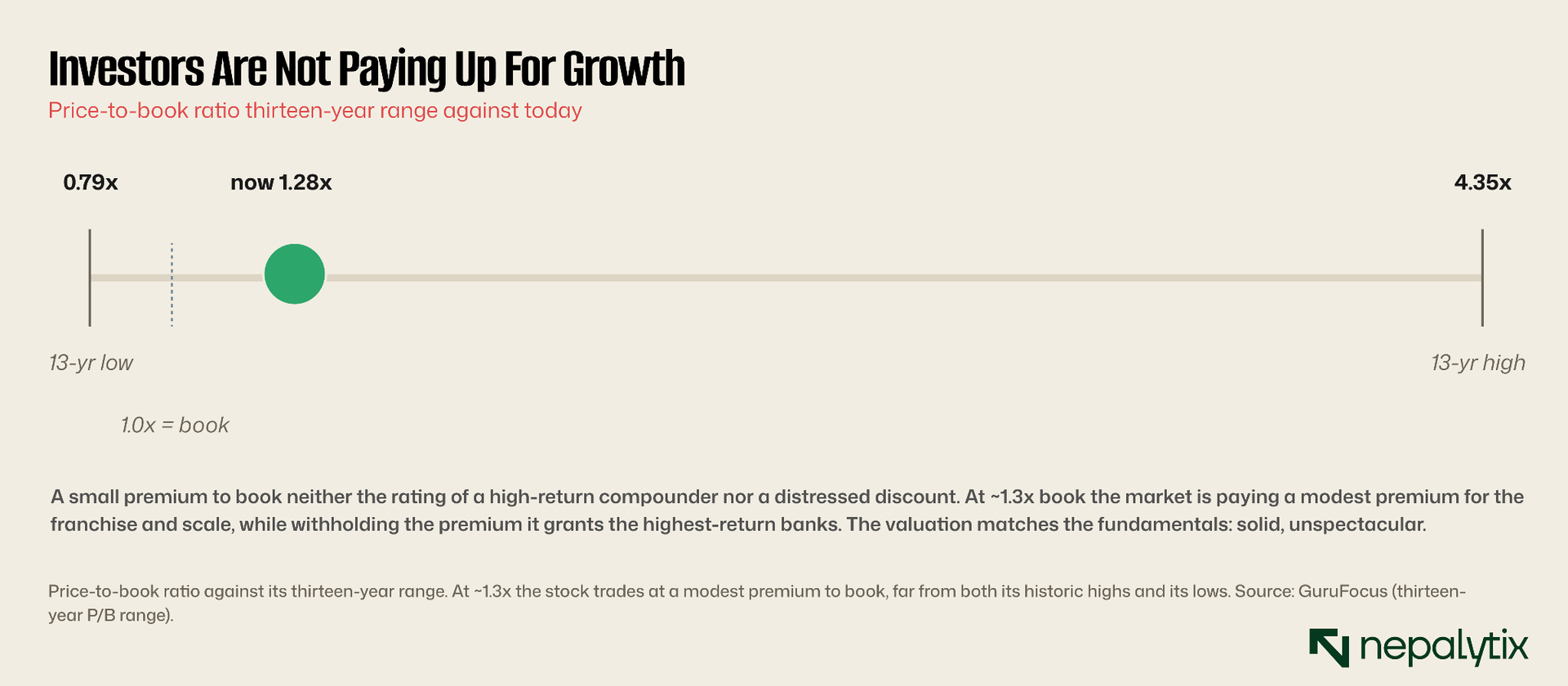

The honest way to value a bank like this is against the book it is compounding, not the earnings of a single soft quarter. At about Rs 178 of net assets per share and a price near Rs 227, the market is paying roughly a quarter more than liquidation value for the franchise, the deposit base and whatever recovery in returns the future holds. The relevant comparison is dynamic: if the bank can grow that book value at, say, low-double-digit rates while paying a modest distribution, the premium is recovered over a few years even if the multiple never expands. If book value stalls because returns stay depressed, the premium is dead money. The valuation, once again, reduces to the same unresolved question about returns

At about 1.28 times book value, Global IME trades at a small premium to the Rs 178 of net assets behind each share neither the rich multiple the market awards its highest-return peers nor the discount it applies to distressed names. Over thirteen years the stock has commanded as much as 4.35 times book and as little as 0.79; today's level is unremarkable which is itself the point. The market is paying for a solid, systemic franchise and no more.

Step back, and Global IME is the living test of the consolidation thesis the whole sector has been pursuing. The regulator's decade-long push to merge Nepal's banks into fewer, larger institutions rested on an assumption that scale would make banks safer and more efficient and that efficiency would reward both the system and shareholders. Global IME took that assumption further than anyone. Its results so far validate the first half and complicate the second: the bank is unquestionably larger and systemically safer but its shareholders have not been rewarded with superior returns. For a sector still being steered toward consolidation that is a result worth sitting with.

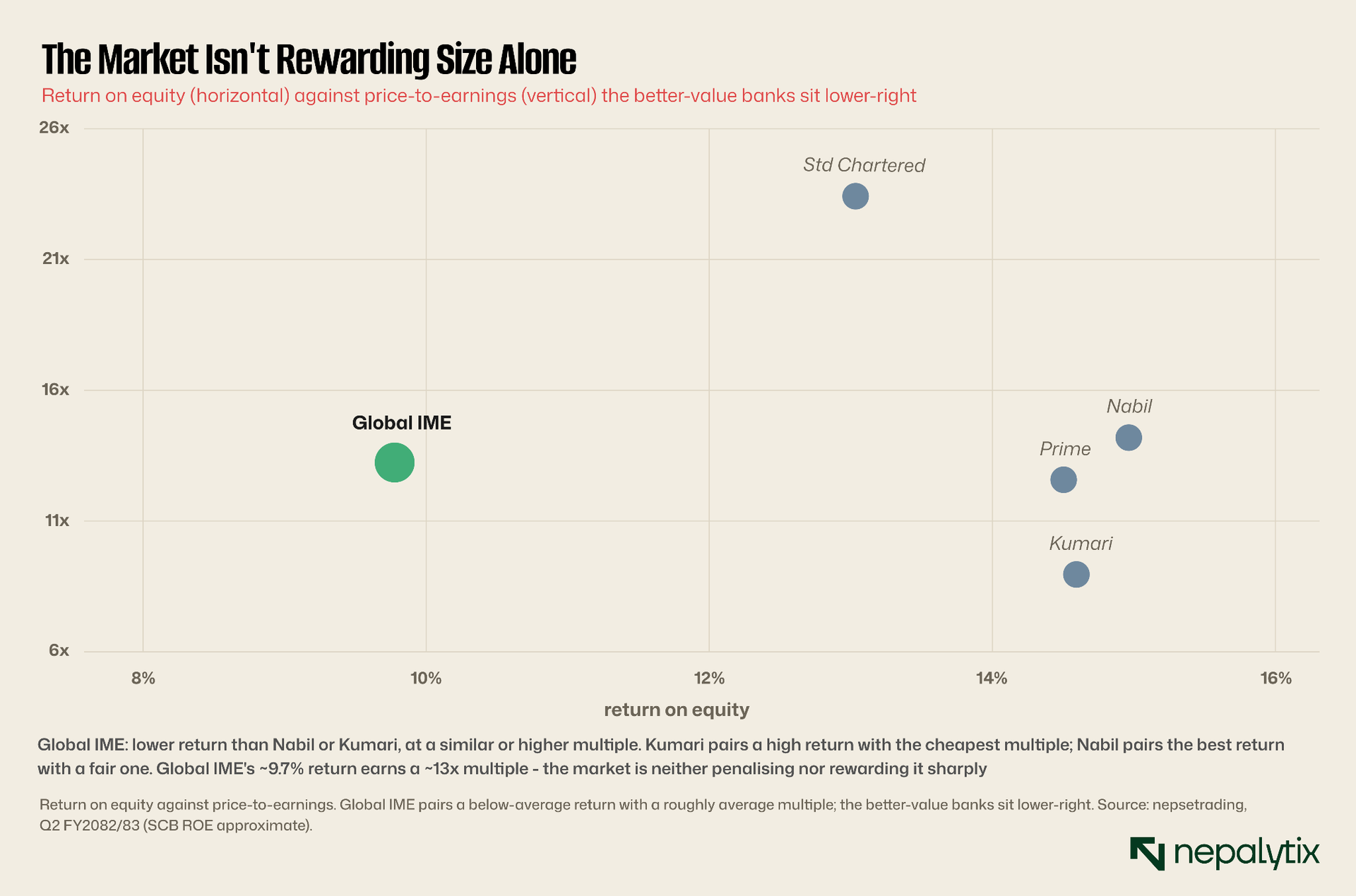

On earnings the same conclusion holds, with a sharper edge. Global IME trades at roughly 13 times earnings but Kumari, with a materially higher return on equity trades at under 9 times and Prime at around 12. An investor paying up for GBIME is paying for size and stability not for a bargain and not for superior profitability. The clearest way to see this is to plot return against multiple directly.

For the prospective shareholder, the choice of the chart below frames is finally quite concrete. Buying Global IME means buying the largest, most systemic, most acquisitive bank in the country at a fair price, in the expectation that a decade of digestion eventually yields the returns the scale ought to produce. Declining it means concluding that the better-run mid-sized banks already deliver those returns, more cheaply and without the integration risk and that size, in banking, is not the same as quality. Neither choice is obviously wrong; the data only insists that the buyer know which bet they are making.

In that map the better-value banks higher return, lower multiple sit toward the bottom right. Global IME sits to the left, with one of the lower returns in the group, at a multiple no cheaper than peers earning far more. The market, in other words, has it about right. There is no obvious mispricing to exploit here in either direction; the valuation simply reflects the fundamentals the earlier chapters laid out.

Two further points round out the valuation. The first is income: Global IME has been a steady, if unspectacular, distributor, favouring bonus shares over cash to keep building capital, and at the current price the yield is reasonable rather than rich. For an investor who values the systemic franchise and accepts mid-single-digit returns plus that distribution, the stock is a defensible income holding even without a re-rating.

The second is what would actually move the multiple. A bank re-rates from a fair multiple to a premium one when the market becomes convinced its returns are durably higher not when it simply grows larger. Global IME has already grown larger, and the multiple has not followed. The catalysts that matter are therefore all on the return side: a recovery in ROE toward the sector's mid-teens, a fall in the NPL ratio and impairment, and evidence the latest integration is delivering the efficiencies earlier ones did not. Absent those, paying above book is paying for size the market has already declined to reward.

VII. The Case For Owning Global IME

The constructive view does not dispute the numbers; it reads them differently. Global IME is the systemic anchor of a banking sector that the regulator is steering toward fewer, larger institutions exactly the kind of bank built to survive and consolidate further. Its funding base is the deepest in the country, which in a rising-rate or stressed environment is a powerful defensive asset; its net interest income already leads the sector. The depressed return on equity, on this reading, is a cyclical and integration trough rather than a structural ceiling: as the post-pandemic credit cycle turns, provisions normalise and the Bank of Kathmandu integration matures, the bank's own history of mid-teens returns suggests meaningful recovery potential. At 1.3 times book, a buyer is not paying a demanding price for the option on that recovery and the bank's scale and dividend capacity provide a floor while waiting.

The macro backdrop supports the constructive case. Nepal's banking penetration remains low by regional standards, remittance inflows continue to swell deposits and a falling-interest-rate environment tends to lift bank margins and revive credit demand at once. As the institution with the broadest reach and the deepest funding, Global IME is positioned to capture a disproportionate share of any cyclical upswing in lending and operating leverage means incremental loan growth on an already-built branch and capital base flows efficiently to profit. A buyer at 1.3 times book is paying an undemanding price for that upside. There is also a reinvestment-and-optionality argument. A bank earning 10% on equity and retaining most of it still compounds book value at a respectable clip so even without a re-rating the patient holder accrues value as net assets per share grow and buys, at 1.3 times book, a cheap option on the integration eventually working. In a sector the regulator still wants to consolidate, the largest, best-capitalised player is also the most likely acquirer on favourable terms and the least likely to be forced into a defensive merger itself. For an investor who believes Nepali banking will keep concentrating, owning the consolidator rather than a consolidation candidate is a coherent way to play it.

VIII. The Case Against The Stock

The skeptical view is that the return gap is the structure, not the cycle. A decade of stock-funded acquisitions has left Global IME with diluted per-share earnings an average-quality loan book carrying the sector's largest absolute provisions, and a return on equity that has spent years below both its own median and its peers a track record more consistent with a low-return aggregator than a temporarily depressed compounder. Integration synergies that were promised with each deal are hard to find in the returns. The very size that the bull case prizes brings diseconomies too: a sprawling branch network, the complexity of reconciling twenty-one institutions, and a loan book large enough that its credit problems are systemic. And because the stock is already priced fairly rather than cheaply, the shareholder has limited margin of safety if returns do not recover. On this reading, an investor seeking quality could find higher returns and lower multiples elsewhere in the sector.

The skeptic would add that the burden of proof has shifted. A decade is long enough for integration synergies to appear, and the persistence of mid-pack returns through multiple cycles suggests the problem is the model, not the moment. Each merger was sold on the promise of efficiency; the aggregate result is a bank that earns less on equity than focused peers a fraction of its size. At some point a pattern of unrealised synergies stops being bad luck and starts being evidence, and a shareholder is entitled to weigh a ten-year record more heavily than a two-year forecast of recovery.

The governance dimension sharpens the skeptical case. A bank this large, closely associated with a single business group and built through a long chain of acquisitions, warrants a level of disclosure and board independence that minority shareholders should scrutinise rather than assume related-party exposures, the pricing of past deals and the independence of provisioning decisions all matter more, not less, at the system's anchor. None of this implies wrongdoing; it implies that the margin of safety a minority investor needs is wider here and yet the price, at a premium to book, supplies a thinner cushion than several higher-return, cleaner-booked peers offer at lower multiples.

IX. So What Does A Shareholder Actually Own?

The two cases turn on a single empirical question that the next several quarters will answer: is Global IME's ~10% return on equity a trough or a plateau? If provisions ease and the latest integration delivers, the history of mid-teens returns makes the current price look reasonable for a systemic franchise. If the return stays near 10%, the shareholder owns the biggest bank in Nepal at a full price for ordinary profitability scale without the return that should justify it.

A reader can resolve the question with a simple frame. Decide, first whether the post-pandemic credit cycle and the Bank of Kathmandu integration are temporary headwinds or permanent features; second, what return on equity the bank can sustain through a normal cycle the bulls mid-teens or the bears' low double digits; and third, what multiple that sustainable return deserves. Plug in mid-teens returns and 1.3 times book looks undemanding; plug in a structural 10% and it looks full. The data here cannot settle that judgement, because it turns on a forecast rather than a fact but it can ensure the judgement is made with the right numbers in view.

Our own reading of the evidence is deliberately limited to what it can support. Global IME has, beyond dispute, won the size race; it has not, on the record so far, converted that size into superior shareholder returns and the market is not pricing it as though it had. That is neither a recommendation to buy nor to sell; it is the frame within which a reader can apply their own view on whether the integration finally pays off. The signals to watch are concrete: the trajectory of the NPL ratio and impairment charges over the next two or three quarters, any recovery in return on equity back toward the sector benchmark, and whether the bank now pauses to digest rather than pursuing the next merger. Those, more than the size that is already settled will decide what the shares are worth.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.