Every hydropower stock is a bet on NEA's balance sheet

Nepal's listed hydropower companies are not bets on rivers-they are all claims on a single buyer, and every investment ultimately depends on the financial health of the Nepal Electricity Authority (NEA).

The Take

There is no such thing as a hydropower sector in Nepal. There is one customer, and there are ninety-odd companies that sell to it. Every megawatt on NEPSE is sold under a long-term power purchase agreement to the Nepal Electricity Authority (NEA) a state utility that sets the tariff, controls the transmission line and decides when it will take your power and when it will not. Last year NEA paid Rs 77.10 billion to independent producers. That number is not a line in someone's accounts; it is the entire revenue of the listed hydropower sector. And the entity writing that cheque just watched its pre-tax profit fall 37.32%, to Rs 9.06 billion while what it owes producers grew 11.73%. When you buy a hydropower stock, you are not buying a river. You are buying a receivable from NEA.

Ask a Nepali retail investor why they own a hydropower stock and you will hear about the river. The catchment, the head, the megawatts, the monsoon. It is a wonderfully physical story, and it is almost entirely beside the point.

A run-of-river plant in Nepal does not sell electricity into a market. There is no market. It signs a power purchase agreement with the Nepal Electricity Authority, a state monopoly that is the sole buyer of electricity in the country, the sole owner of the transmission grid and the sole party to the contract. The PPA fixes the tariff, typically for decades. It sets a dry-season rate and a wet-season rate. And it makes NEA the counterparty to every rupee that company will ever earn.

That is a monopoly, one buyer many sellers and it inverts everything you think you know about analysing a business. The producer has no pricing power, no customer diversification, no ability to walk away and sell elsewhere. Their revenue is not a function of demand or of management skill, or even really of hydrology beyond a point. Their revenue is a function of one thing: whether NEA can pay, and whether NEA will take the power.

So the correct first question about any hydropower stock is not "how many megawatts?" It is "how is NEA's balance sheet?" And the honest answer, on the most recent numbers, is: deteriorating fast.

Rs 77 billion, and where it comes from

Start with the scale of the dependency, because most investors have never seen it stated plainly.

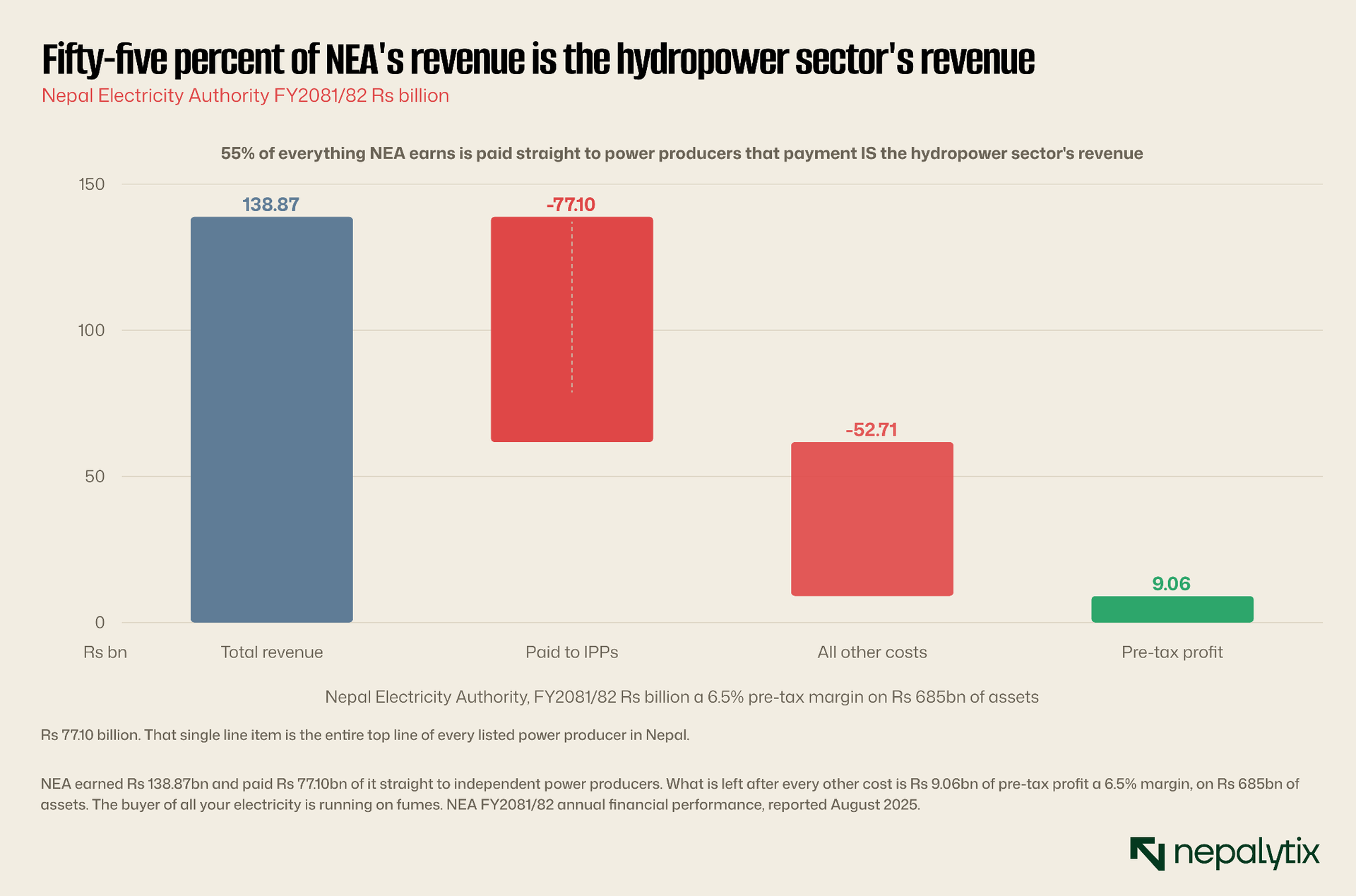

In FY2081/82, NEA's total revenue was Rs 138.87 billion of which Rs 125.27 billion came from selling electricity and Rs 17.47 billion from exporting it to India. Against that, it spent Rs 77.10 billion buying power from independent producers.

Stop and look at that ratio. Fifty-five percent of everything NEA earns is handed straight to power producers. And from the other side of the table, that Rs 77.10 billion is the revenue of Nepal's independent power sector, the pool from which every listed hydropower company's earnings, dividends and share price are ultimately drawn. There is no other source. The sector's top line is a line item in a state utility's cost base.

After paying producers and everything else, NEA was left with Rs 9.06 billion of pre-tax profit on total assets of Rs 684.91 billion. That is a 6.5% margin on a balance sheet carrying substantial debt, at a utility whose gearing sits around 1x and which relies on periodic equity injections from the government to stay comfortable.

The hydropower sector's revenue is a cost line at a state utility that just lost a third of its profit. That is not a sector. That is a concentration risk with a stock ticker.

The scissor

Now the part that should genuinely worry anyone holding these stocks because it is not a static risk. It is moving and it is moving the wrong way.

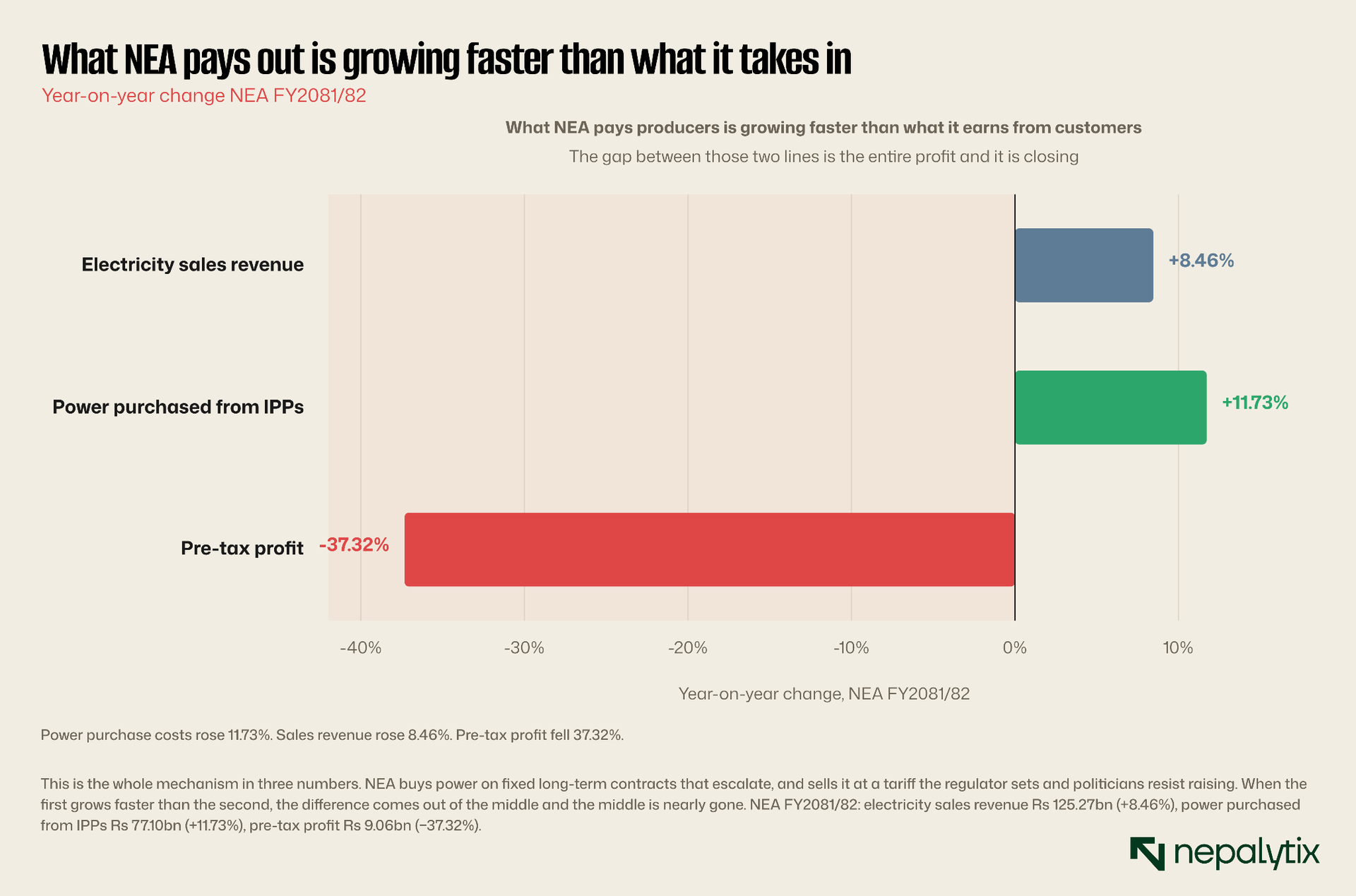

NEA's electricity sales revenue grew 8.46% last year. Its cost of buying power from IPPs grew 11.73%. Its pre-tax profit fell 37.32%.

Those three numbers describe a scissor, and the structure of the business guarantees it. On one blade, NEA buys power under long-term PPAs at contracted rates that escalate obligations it cannot renegotiate and cannot refuse. On the other hand, it sells electricity at a retail tariff that a regulator sets and that politicians are extremely reluctant to raise because electricity prices are a political commodity in every country on earth and Nepal is no exception. When the cost blade rises faster than the revenue blade, the profit in between is compressed. Last year it was compressed by more than a third.

And here is the uncomfortable implication for shareholders in the producers: the thing squeezing NEA is the thing paying you. The rising power-purchase cost that is destroying NEA's margin is, line for line, the growing revenue of the hydropower companies. Every new plant that reaches commercial operation and starts drawing on its PPA makes the utility's arithmetic worse. The sector's growth is the counterparty's problem and eventually the counterparty's problem becomes the sector's problem.

What gives when the utility cannot pay

Suppose the scissor keeps closing. What actually happens? A state utility does not simply default; it has a sovereign standing behind it and an AA+ domestic rating that reflects exactly that. But there are four pressure valves and every one of them is paid for by the producers.

The tariff rises. The cleanest fix and the one that keeps everyone whole. It is also politically hard which is why it has not kept pace so far. Do not build your investment case on it.

Payment slows. The utility keeps buying but pays later. Receivables lengthen at the producers, working capital tightens and dividends the entire reason retail owns these names get deferred. Note that NEA is already carrying Rs 22.8 billion of its own uncollected dues on trunk and dedicated lines. A utility with a collection problem passes it down the chain.

The power gets curtailed. This is the quiet one and the most damaging. NEA does not have to break the PPA to hurt you; it simply does not take your electricity. In the wet season when every run-of-river plant in the country is producing at once and demand is lower, the grid cannot absorb it and the power is spilled. Generated, and not paid for.

New PPAs stop. If NEA cannot afford the obligations it already has, it stops signing new ones which strand every company whose entire valuation rests on a project pipeline reaching commercial operation.

The grid is the real constraint

The curtailment risk is not hypothetical, and the energy balance shows exactly why.

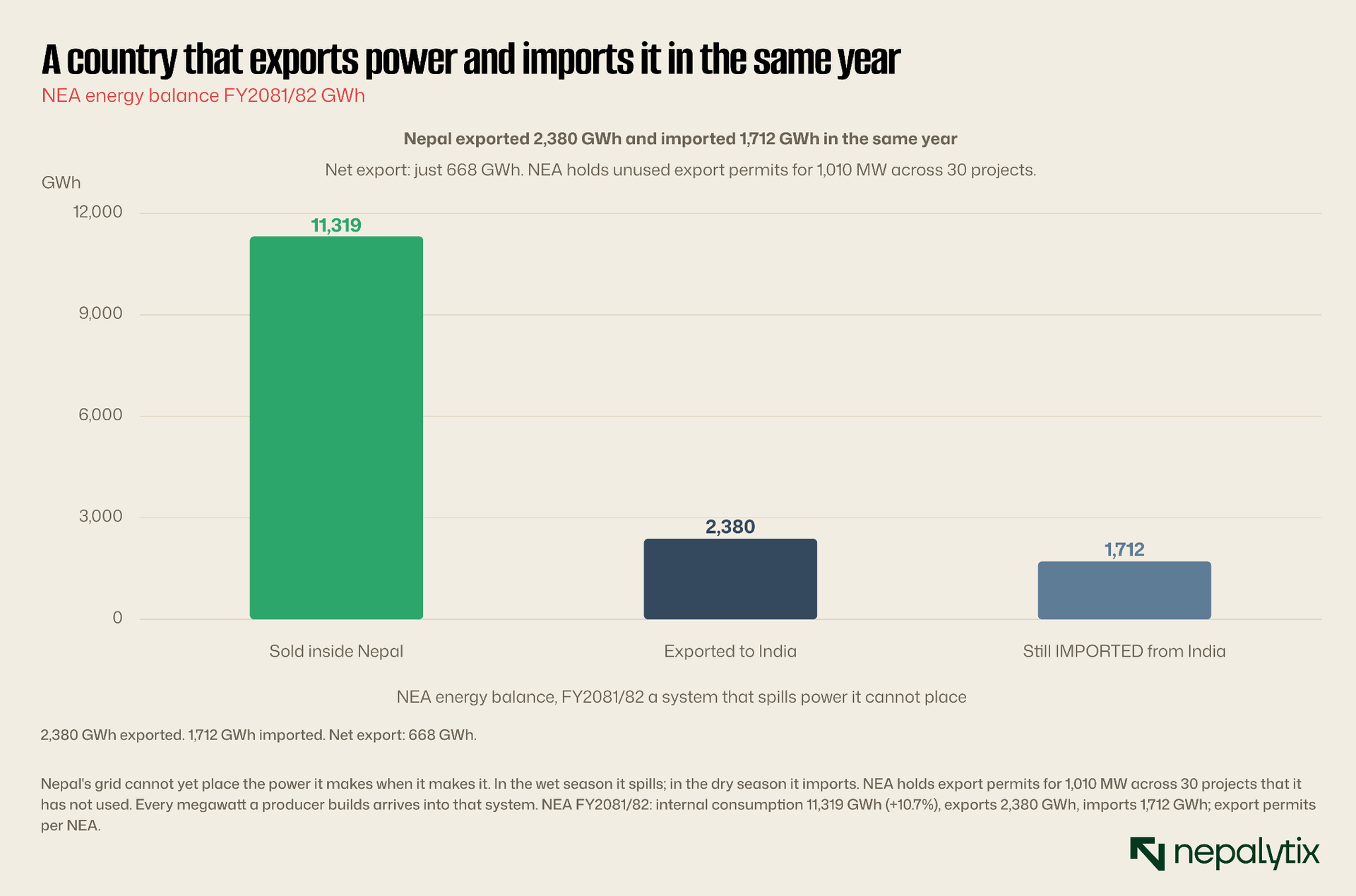

Last year Nepal exported 2,380 GWh of electricity to India and imported 1,712 GWh from India. The net export was 668 GWh. Read that twice. This is a country that is simultaneously a power exporter and a power importer because run-of-river hydro produces a flood in the monsoon and a trickle in the dry season, and the grid has to deal with both.

The consequence for a producer is brutal and specific. Your plant generates most of its annual energy in the wet months, which is precisely when the entire national fleet is also generating, demand is at its seasonal low and there is nowhere to put the power. If the transmission line to India is not there, or the export permit is not used, that electricity is spilled. NEA currently holds permits to export 1,010 MW across 30 projects capacity it has been criticised for failing to actually utilise. That unused permission is a direct, measurable haircut to producer revenue.

Which reframes what a hydropower investor is really underwriting. Not rainfall. Transmission. Your returns depend on whether NEA builds the line, gets the export deal signed, and takes your power when you make it. Those are all decisions made inside a state utility by people you cannot vote out and a board you do not sit on.

The take

None of this makes hydropower uninvestable. Nepal's electricity demand grew 10.7% last year and per-capita consumption is still tiny; the long-run demand story is real, the export opportunity to India is real and a producer with a signed PPA on a functioning grid connection earns a genuinely predictable, inflation-linked, utility-like cash flow. That is a decent asset.

But it means the analysis most people are doing is the wrong analysis. Comparing two hydropower stocks on their megawatts, their P/E or their catchment area is comparing two claims against the same counterparty and if that counterparty stumbles, both claims are impaired together, no matter how good the rivers are. There is far less diversification inside a portfolio of five hydropower stocks than the people holding them believe. It is one bet, held five times.

You are not diversified across five hydropower companies. You are concentrated in one state utility, five times over.

So the questions to actually ask, before you buy any of these names: Is the plant connected to a transmission line that exists today, or one that is promised? Is the PPA a take-or-pay contract, or does NEA get to refuse the power? What is the dry-season tariff, not the headline one? And above all: is NEA getting stronger or weaker?

On that last one, the most recent answer is unambiguous. Profit down 37%. Costs to producers up 11.73% against revenue up 8.46%. Rs 22.8 billion of its own dues uncollected. A grid that spills power in the wet season and imports it in the dry. And a political culture that fires the executive director when the numbers displease which is not a sign of an institution with a stable long-run plan.

Buy the river if you like. Just understand that the river is not an asset. The asset is a promise from a state utility whose margin is disappearing and the price of every hydropower stock on NEPSE is whether its holders know it or not, a bet on how long that promise holds.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.