Five recommendations for FY 2083/84 monetary policy

Five Structural Reforms Nepal Rastra Bank Should Prioritize in FY 2083/84 to Strengthen Nepal's Financial System.

Nepal enters the FY2083/84 cycle with inflation under control, reserves at a record and a policy rate that the market has stopped listening to. The binding problems are now structural, not cyclical. These are five recommendations the central bank can act on this year and two worth doing that can wait.

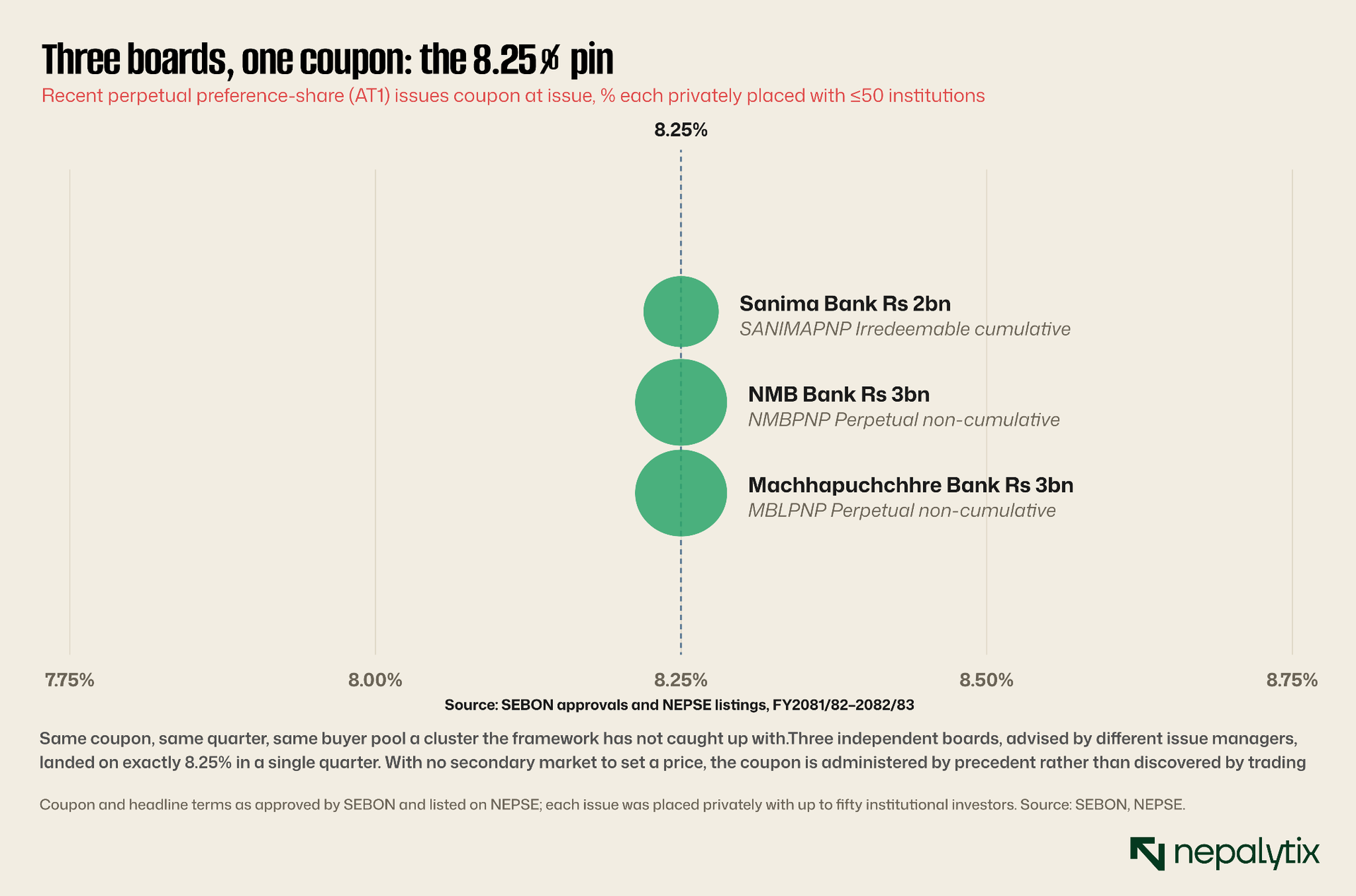

Start with a coincidence. In a single quarter of this fiscal year, three commercial banks, three boards, three issue managers priced perpetual capital at exactly the same coupon: 8.25 percent. Nobody ordered that number. It happened because the instrument these banks now lean on has no market to price it, only a precedent to copy. In the same months, the central bank cut its policy rate by 75 basis points and watched lending barely move. These are the same facts seen from two sides: Nepal's monetary problem is no longer the price of money, it is the plumbing that is supposed to carry it.

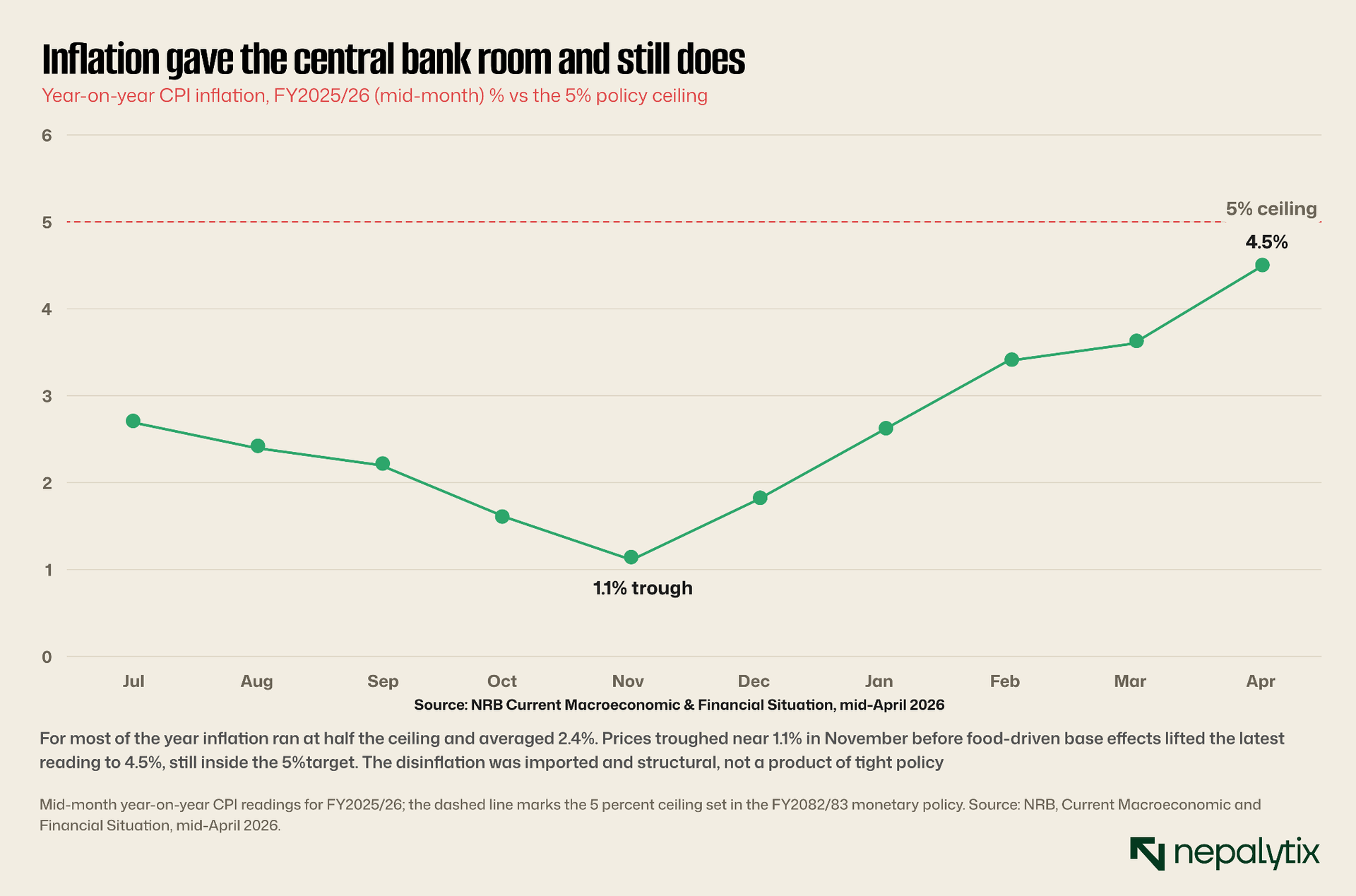

Everything this submission recommends follows from that. Nepal's macroeconomic position at the start of the FY2083/84 cycle is on the conventional indicators, enviable. Consumer-price inflation averaged 2.4 percent over the first nine months of the current fiscal year, troughing near 1.1 percent in November and even after a food-driven rebound to 4.5 percent in mid-April sits comfortably inside the 5 percent ceiling. The external account is not merely sound but cushioned to an unusual degree: gross foreign-exchange reserves stand at USD 23.6 billion equivalent to more than eighteen months of goods-and-services imports against a policy minimum of seven lifted by a remittance inflow that grew 39 percent year on year.

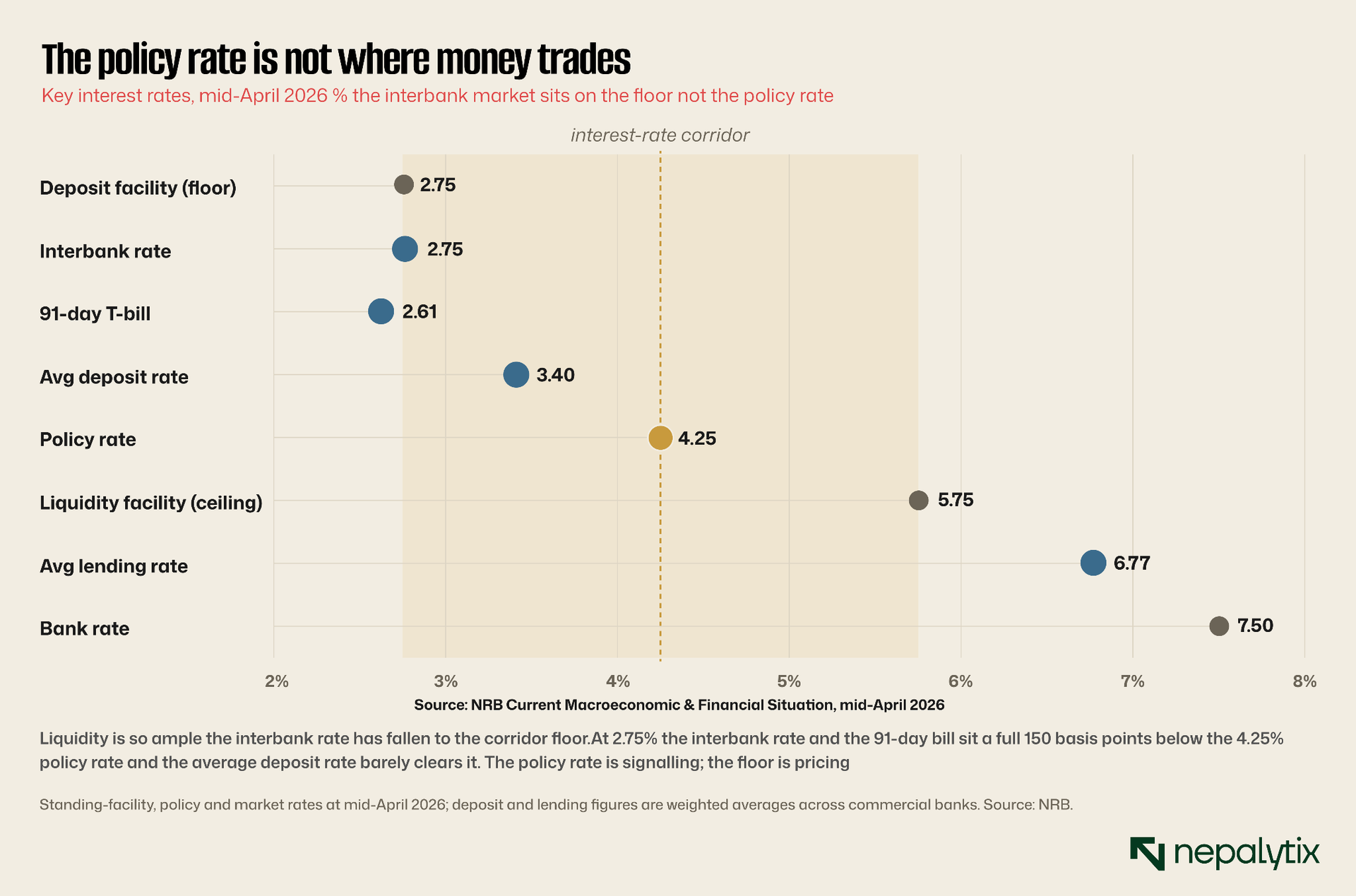

Against that backdrop the central bank has eased, cutting the policy rate by 75 basis points to 4.25 percent over the first half of the year and narrowing the interest-rate corridor and yet private credit has barely responded expanding just 6.6 percent year on year against broad-money growth of 14.5 percent, a gap that is itself a measure of how much of the new liquidity is bypassing domestic lending. This is the central fact that should orient the coming policy: the conventional tools are being deployed into an economy where they no longer transmit cleanly, where the constraints on credit and capital formation have migrated from the price of money to the plumbing that is supposed to carry it.

The puzzle is the weakness of credit itself. With inflation low and the policy rate cut, real lending rates have if anything risen yet borrowers have not come forward. Part of the explanation is demand: the disruption of September 2025 and a generally cautious investment climate have left firms reluctant to gear up and what broad-money growth the year has produced has been driven largely by the accumulation of net foreign assets rather than by domestic credit creation. Part is structural and it is the part monetary policy can address. A banking system that cannot move its cost of funds, an accounting transition taxing capital twice and a capital market sealed off from external savings together describe an economy whose financial plumbing, not its monetary stance, is the binding constraint.

This is why the recommendations that follow are weighted toward structure rather than stance. The cyclical task anchoring inflation, defending the rupee's peg to the Indian rupee, rebuilding reserves has largely been accomplished and accomplished well. The marginal return to a further rate cut is low when the last one did not transmit; the marginal return to repairing the channel through which any cut must travel is high, and rising. A central bank in Nepal's enviable cyclical position has the rare luxury of being able to turn to structural work and should.

One structural fact frames everything that follows: the rupee's peg to the Indian rupee. The peg has served Nepal well, importing a measure of price stability from a larger neighbour, but it also binds Nepal's monetary autonomy. Domestic rates cannot stray far from Indian rates for long without pressure on the parity or on reserves. That makes the quality of domestic transmission more important, not less. With limited room to set the level of rates independently, the central bank's leverage lies disproportionately in how effectively the rates it can set reach the real economy. A peg is itself an argument for fixing the plumbing, because the plumbing is where what discretion remains actually operates.

That diagnosis dictates the prioritisation that follows. We rank these recommendations not by their intellectual elegance but by the urgency of the operational gap each addresses and the speed with which the central bank can act unilaterally. Measures that close a live gap in the existing financial architecture, and that can be enacted by circular under powers the central bank already holds, come first. Measures that build desirable future architecture, or that require legislation and inter-agency coordination, come later — not because they matter less, but because the lead times are longer and the work to make them useful has to begin now precisely so that it is ready when it is needed. Five recommendations meet the first test well enough to be advanced this year. Two more are worth doing but can wait. Several fashionable ideas are, in our view, premature, and we say so at the close.

Recommendation 1: Bring the AT1 cluster inside a disclosure regime

Within a single quarter of the current fiscal year, three commercial banks Sanima, NMB and Machhapuchchhre issued perpetual preference shares and all three priced at exactly the same coupon of 8.25 percent. Sanima's was an irredeemable cumulative instrument of around Rs 2 billion; the other two were perpetual non-cumulative issues of Rs 3 billion each. Each was placed privately with no more than fifty institutional investors. They are in substance Additional Tier 1 capital: permanent, loss-absorbing and counted toward the Basel III capital stack the central bank itself requires.

The capital treatment of these instruments is, to be clear, already defined. The Unified Directives set a Basel III trigger: AT1 instruments must convert or be written down when a bank's common-equity Tier 1 ratio falls to 5.125 percent of risk-weighted exposures. What does not yet exist is the ongoing-disclosure and market architecture around a class of instruments that is now appearing faster than the framework governing its visibility. An investor or a supervisor scanning the system cannot today read off in one place and in real time how much AT1 is outstanding by the issuer on what terms and whether any dividend has been skipped. For a non-cumulative instrument, a skipped coupon is permanent and material yet it surfaces only in an annual report months later.

The coupon convergence is worth dwelling on because it is the clearest evidence that the instrument has outrun its market. Three independent boards advised by different issue managers arriving at precisely 8.25 percent in the same quarter is not coincidence; it reflects either informal guidance, the gravitational pull of the first approved issue as a precedent or most plausibly an institutional buyer pool that prices these placements as a bloc because there is no secondary market to price them otherwise. A cap of fifty investors per issue is at once cause and symptom: it keeps the instruments out of public price discovery which keeps the pool shallow which keeps the coupon administered rather than market-set. The difference between Sanima's cumulative structure and the non-cumulative issues of the other two, a material difference in how a skipped dividend is borne, is exactly the kind of term a functioning market would price into distinct yields, and that a uniform coupon conceals.

A secondary market is the missing piece that would make the rest cohere. Once these instruments can be bought and sold at observable prices, the buyer base widens beyond the handful willing to hold to perpetuity; the coupon on the next issue is set by the market rather than by precedent; and the supervisor gains a continuous, price-based read on how the system values bank capital an earlier warning than any quarterly return can give. The disclosure regime proposed here is the precondition for that market: instruments that cannot be seen clearly cannot be priced and instruments that cannot be priced will not trade.

The recommendation. We propose a standing AT1 disclosure and classification regime built on the existing capital rules rather than replacing them:

Mandatory quarterly disclosure of every AT1 instrument outstanding, by issuer face value, coupon, cumulative versus non-cumulative status and any conversion or write-down trigger.

Published NRB guidance clarifying what qualifies as AT1 versus Tier 2 to prevent instruments drifting into the more favourable capital bucket than their terms warrant.

Real-time disclosure of any dividend-skip or non-payment event, not deferral to the annual report

NRB–SEBON coordination on secondary-market mechanics so that institutional holders of these perpetual instruments can trade and price them rather than holding to a maturity that never comes.

Comparators. The reference points are well established. The Reserve Bank of India built a Basel III AT1 disclosure regime from 2013 onward after the instrument class grew ahead of its supervision; Bangladesh Bank operates a comparable framework and the Basel Committee's own Pillar 3 standards set the template for what continuous capital-instrument disclosure should contain. Nepal need not invent anything here, only adopt the disclosure layer that every comparable jurisdiction added once hybrid issuance began in earnest.

Implementation. This is the fastest of the five to enact. It requires a circular under the existing Unified Directives and a coordination memorandum with SEBON. No legislative change is needed, and the data the disclosure would require is already held by the issuers. It can be in force within the fiscal year.

Risks and counterarguments. Some issuers will argue that heavier disclosure discourages issuance at a moment when banks need the capital. The counter is that opacity is the greater deterrent to the very institutional buyers, provident and pension funds, insurers whose participation is the binding constraint on the market's depth. A buyer pool of fifty institutions per issue is small precisely because the instruments are hard to value and harder to exit. Disclosure widens that pool; it does not shrink it.

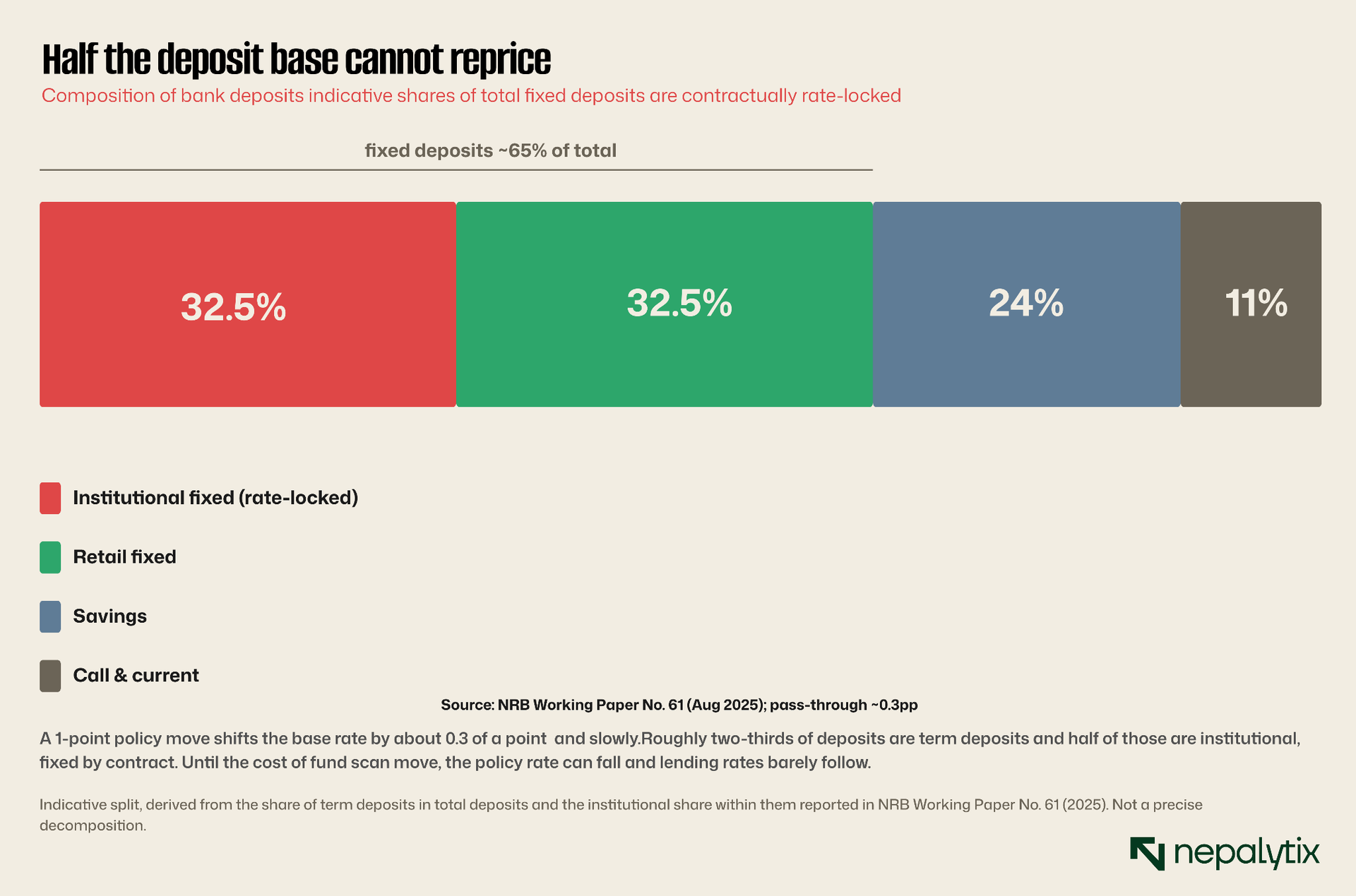

Recommendation 2: Make the policy rate transmit The central bank's own research has now documented, empirically, what practitioners have long suspected: in Nepal the price of money set by the central bank does not reliably reach the price of credit faced by borrowers. NRB Working Paper No. 61 published in August 2025 estimates a pass-through of roughly 0.3 of a percentage point from the policy rate to bank lending rates and finds that full transmission is not observed within the span of a year. When the central bank cannot dependably move the cost of credit, every other instrument in its kit weakens with it.

The mechanism is not mysterious and the same working paper identifies it. Term deposits make up around two-thirds of the banking system's deposit base and roughly half of those are institutional fixed deposits placed by the large provident and citizen-investment funds, insurers and similar bodies on contractual terms that fix the rate for the life of the deposit. When the policy rate falls, these contracts do not. The average cost of funds is therefore sticky almost by construction, and a bank whose funding cost will not move has little room to move its base rate, however much the policy rate signals.

The corridor itself tells the same story from the other side. With liquidity ample, the interbank rate has fallen to the standing-deposit-facility floor and stayed there which means the operative price of overnight money is the floor of the corridor, not its centre where the policy rate sits. A central bank steering from the middle of a corridor whose floor is doing the actual pricing is steering with a loose wheel. Pulling the operative rate back toward the policy rate would mean draining the structural surplus more actively using deposit auctions and the collection rate as the binding instrument so the interbank rate is lifted off the floor rather than left to settle beneath the policy rate.

The recommendation. Transmission cannot be legislated into existence, but several measures would materially tighten it:

Tighten the base-rate formula to narrow the discretionary spread banks may hold between the policy rate and their lending rates.

Introduce a published pass-through expectation, a stated share of any policy-rate change that should be reflected in base rates within a defined number of months and monitor against it.

Publish bank-by-bank transmission-lag metrics each quarter; transparency is itself an enforcement tool where formal compulsion is blunt.

Address the institutional deposit base directly working with the provident and citizen funds toward greater flexibility in their fixed-rate mandates which are a principal source of the rigidity.

The institutional deposit base is the deepest root and the hardest to pull. The large provident, citizen-investment and insurance funds place their money in long fixed deposits at administered rates because their own mandates reward certainty of return over responsiveness to policy and because there are few alternative instruments of comparable safety and tenor for them to hold. Loosening those mandates cannot be done by directive alone; it has to be paired with giving the funds somewhere else to go. The development of a tradable market in bank capital and in time in longer-dated government and corporate paper is therefore not a separate agenda from transmission but part of the same one.

Comparators. India confronted the identical problem and responded with a sequence of formula-based lending-rate regimes, culminating in the Marginal Cost of Funds-based Lending Rate framework introduced in 2016 which tied the lending rate mechanically to the marginal cost of funds and shortened the transmission lag. Bangladesh's interest-rate corridor implementation offers a second reference. Neither is a perfect template but both show that transmission improves when the regulator constrains the discretion banks have to absorb policy moves in their spread.

Implementation. The base-rate and disclosure measures sit within existing prudential powers and can be issued by directive within the year. The deeper work of loosening the fixed-rate mandates of the institutional funds is slower and reaches beyond the central bank alone, but it is the part that matters most and so should begin immediately.

Risks and counterarguments. Banks will argue that tighter transmission compresses their margins. It will. But the high, protected margin is itself what drives depositors toward AT1 instruments and informal channels in search of yield and what allows the cost of credit to stay high while the policy rate falls. A margin defended at the cost of a working transmission mechanism is a poor bargain for the financial system as a whole.

Recommendation 3: Finish NFRS 9 and end double provisioning Nepal's banks are midway through adopting NFRS 9, the forward-looking expected-credit-loss standard while still subject to the central bank's older, percentage-based loan-loss provisioning. For now they must satisfy both: the expected-loss model which anticipates impairment, and the regulatory reserve which is calculated mechanically on the stock of loans. The result is a double charge against capital for the same underlying risk and the squeeze falls hardest on the upper-tier commercial banks which is itself part of why AT1 issuance has accelerated. The capital strain that Recommendation 1 observes is, in part, manufactured by an unfinished accounting transition.

Transitions of this kind are damaging mainly when they drift. A half-adopted standard gives banks the worst of both regimes and gives supervisors a blurred view of asset quality, because two provisioning numbers that do not reconcile are in practice no clear number at all. The remedy is less a matter of choosing the right standard than of finishing the move to it on a fixed timetable.

The standardised-parameter point deserves emphasis, because it is where a frontier-market adoption most often goes wrong. Expected-loss modelling demands estimates of the probability of default and the loss given default for each asset class, and Nepal's principal exposures are precisely the ones for which generic parameters fail: hydropower lending, with its long gestation and concentrated construction-phase risk; microfinance with its high-frequency, low-value, socially collateralised book; and agriculture with its weather-driven clustering of defaults. Left to model these alone, twenty banks will produce twenty answers, none comparable and several self-serving. A central bank that publishes calibrated, sector-specific parameters turns expected-loss accounting from a source of supervisory fog into a source of clarity, and removes the excuse that the standard is too complex to apply honestly.

There is a procyclicality concern to manage in the timing. Expected-loss provisioning, by design, front-loads impairment as conditions deteriorate, which can deepen a downturn at exactly the moment the counter-cyclical buffer of Recommendation 5 is meant to cushion it. The two should be calibrated together: the transitional capital relief that smooths adoption and the buffer that releases capital in stress are the instruments that keep a more honest provisioning standard from becoming a more brittle one.

The recommendation. Bring the NFRS 9 transition to a definite close and resolve the double charge:

Set and hold to a firm date for full NFRS 9 compliance rather than allowing the deadline to slip year after year.

Resolve the double-provisioning trap explicitly: either expected-credit-loss provisions replace the regulatory percentage above a defined threshold or the regulatory percentage stands as a floor with the expected-loss charge taken above it but not both in full.

Provide a transitional capital-relief schedule, phased over a defined window for banks that take a one-time capital hit on full adoption.

Publish standardised expected-loss parameters probability of default, loss given default, exposure at default calibrated to Nepal-specific asset classes such as hydropower, microfinance and agriculture rather than leaving each bank to model frontier-market risks alone.

Comparators. India's own IFRS 9 adoption is instructive chiefly as a cautionary tale: repeatedly deferred and still only partial, it shows the cost of allowing a transition to drift. Bangladesh Bank's expected-credit-loss guidelines and the transitional capital reliefs granted across the European Union and United Kingdom at the point of IFRS 9 adoption are the more constructive models each smoothed the one-time capital impact rather than letting it deter adoption.

Implementation. This is a prudential directive coordinated with the accounting-standards body. It is more involved than a single circular but well within the central bank's authority, and the standardised parameter work can run in parallel with the compliance deadline rather than blocking it.

Risks and counterarguments. Faster, fuller provisioning means lower reported bank earnings in the near term and that will be unwelcome. But deferred loss recognition is precisely the mechanism by which the next non-performing-loan cycle is allowed to build unseen. Recognising impairment earlier is not a cost imposed on the banks; it is the cost of the risk they already carry, brought forward to when it can still be managed.

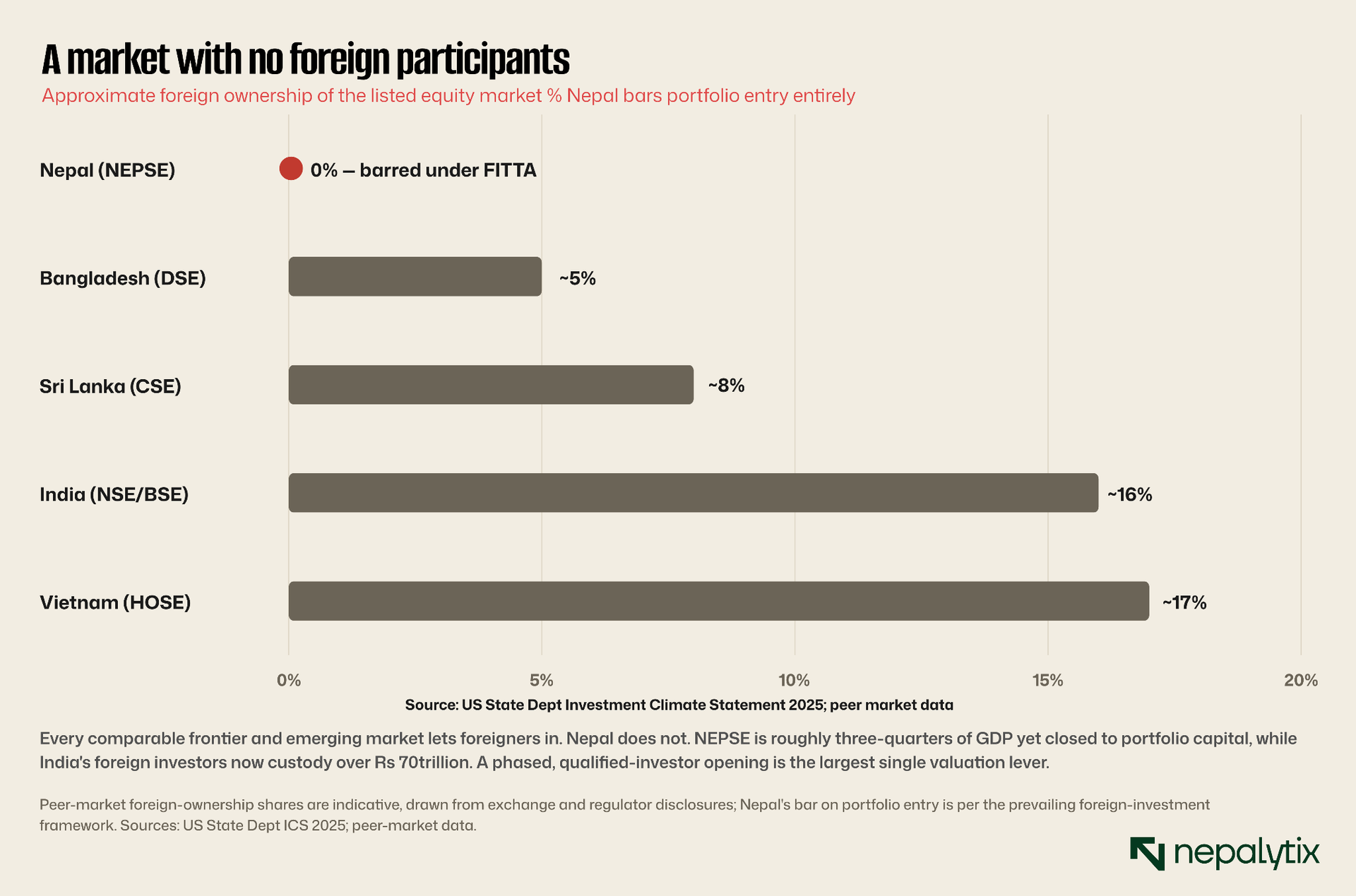

Recommendation 4: Open the market to qualified foreign investors Foreigners cannot invest in Nepal's stock market. Under the prevailing foreign-investment framework, portfolio entry to NEPSE is closed; the only route for foreign equity participation is a narrowly drawn venture-capital-fund provision that is, in practice, little used. The consequence is a national equity market worth roughly three-quarters of GDP that is financed almost entirely by domestic capital and a deposit-weary retail base. This is the single largest structural overhang on Nepali equity valuations, and it is self-imposed.

The contrast with the region is stark. India hosts thousands of registered foreign portfolio investors whose assets under custody now exceed Rs 70 trillion; Vietnam, Sri Lanka and Bangladesh all admit foreign participation within managed limits. Nepal already has the prerequisite that many of these markets lacked at the outset full current-account convertibility and has built a domestic institutional base deep enough as the AT1 issues show to absorb sizable placements. What it lacks is the legal and custodial architecture to let external capital in on terms that protect stability.

The mechanics matter as much as the decision and they are where earlier gestures toward opening have stalled. A foreign portfolio investor needs three things before a single rupee moves: a designated custodian to hold the assets and act as the interface with the exchange; clarity on tax, the rate of capital-gains and dividend withholding and an unambiguous right to repatriate proceeds; and a foreign-exchange framework that treats the inflow and its eventual outflow as a capital-account transaction distinct from the current account. India supplies all three through its designated-depository and custodian system, and its recent simplification of entry for low-risk categories shows the architecture can be made light without being made lax.

There is a genuine caveat on the other side of the ledger and it should be stated plainly. NEPSE is not yet deep or liquid enough to absorb the entry and exit of large positions without disturbance, and the influence of the finance ministry over both the exchange and the securities board has been cited as an impediment to the market's development. These are arguments for sequencing and for caps, not for closure. A phased opening that begins with long-horizon, low-turnover investors is the design that lets liquidity deepen as participation grows, rather than waiting for a depth that cannot arrive while the market is sealed.

The recommendation. Open NEPSE to qualified foreign investors in a phased, stability-first sequence:

Begin with the lowest-risk, longest-horizon investors sovereign wealth funds, multilateral institutions and regulated pension funds on the model of the simplified entry routes India has extended to precisely these categories.

Impose an initial aggregate cap on foreign ownership, on the order of 5 to 10 percent of each stock's free float, to contain volatility while the market learns the flow.

Establish tax clarity up front capital-gains treatment, dividend withholding and repatriation rules through the necessary amendment to the foreign-investment law.

Designate qualified custodians for foreign assets and coordinate with the central bank on the foreign-exchange treatment of these flows, so that portfolio capital is managed distinctly from the current account.

Comparators. India's foreign-portfolio framework, refined steadily since the early 1990s, is the obvious model and its recent move to streamline entry for sovereign and pension investors is exactly the qualified-investor approach proposed here. Vietnam's foreign-ownership limits on the Ho Chi Minh exchange and Sri Lanka's long-standing foreign participation show that managed openness is compatible with a frontier market's stability.

Implementation. This is the slowest of the five and the only one that reaches beyond the central bank's own authority: it requires an amendment to the foreign-investment law through Parliament, a central-bank foreign-exchange circular, securities-board regulation and changes to NEPSE's listing rules. That long lead time is the reason to begin now rather than the reason to defer.

Risks and counterarguments. The standard objection is hot money destabilising short-term inflows and sudden exits. The phased design answers it directly: an aggregate ownership cap and a qualified, long-horizon investor base are calibrated to limit exactly that behaviour. And the alternative is not stability but a permanent valuation discount and a market that cannot grow beyond the savings of a single, deposit-saturated economy.

Recommendation 5: Build a Nepal-specific counter-cyclical buffer The counter-cyclical capital buffer is the part of the Basel III architecture designed to make banks build capital in good times so they can absorb losses in bad ones. Nepal will need it before the next credit cycle turns. But the standard tool for deciding when to raise the buffer the gap between the credit-to-GDP ratio and its long-run trend is poorly suited to emerging and frontier economies, a point now well established in the academic literature. Activating a buffer on a bad indicator would be worse than having none. The work that makes this recommendation useful is therefore upstream of the buffer itself.

The case against the standard indicator is not academic fastidiousness. The credit-to-GDP gap assumes a long, stable history from which a meaningful trend can be extracted, and it assumes credit growth is the dominant signal of building risk. Neither holds in Nepal where the credit series is short and structurally rising as the economy financialises, and where the more telling signals of excess have historically been real-estate price momentum and the surge of remittance-funded liquidity into a narrow set of assets. An indicator built for Nepal would weigh these directly. Constructing it is a genuine research task, not a drafting exercise, which is exactly why it must be commissioned at the start of the cycle rather than reached for in haste when the next boom is already visible.

The recommendation. Prepare the framework now, and activate it only once the indicator is sound:

Mandate the central bank's research department to develop a Nepal-specific credit-cycle indicator, likely combining credit growth, real-estate price momentum, equity-market valuation and the remittance trajectory rather than relying on the credit-to-GDP gap alone.

Publish the counter-cyclical buffer framework with its indicator formula stated explicitly. Set the buffer initially at zero with rules-based activation triggers, so that the framework is preparation rather than immediate tightening.

Publish the indicator's readings quarterly, so that market discipline begins to operate well before the regulator ever activates the buffer.

Comparators. The Reserve Bank of India's work on an alternative buffer indicator, and the sustained critique of the standard Basel credit-to-GDP gap in the central-banking literature, both point the same way: the indicator must be built for the economy it governs. European activations of the buffer over the past decade provide a guide to the mechanics once a sound trigger is in place.

Implementation. This is a research programme of perhaps twelve to eighteen months followed by a framework circular. It is the least urgent of the five in the sense that nothing breaks if it is not ready this year but the research cannot be compressed and so it should be commissioned now.

Risks and counterarguments. The fear is premature activation that chokes off credit. A framework published with a zero initial buffer cannot do that: it is a standing readiness, not a tightening. The real risk is the opposite arriving at the next cycle's peak with no calibrated tool to lean against it.

Worth doing, but not this year's

Deposit-insurance reform. Nepal's deposit-insurance cap of Rs 500,000 is broadly in line with regional peers India's equivalent is also Rs 500,000, Bangladesh's somewhat lower so the cap is not the issue. The mechanism is. The Deposit and Credit Guarantee Fund operates as a pay-box: it reimburses insured depositors after a bank has already failed. A resolution authority, along the lines of India's deposit-insurance corporation, can act before failure transferring deposits and viable assets to a sound acquirer and winding down the rest without a disorderly run. The difference is the difference between compensation and continuity, and the move would also mean putting the Fund's finances on a risk-based footing, with premiums that reflect the risk each institution brings to the pool.

It is worth doing. But Nepal has not experienced a failure that exposed the present arrangement, and reforms of this kind are better designed in calm than improvised in crisis which is exactly why this one can wait a year, and exactly why it should not wait five.

Narrowing the productive-sector definition. Banks are required to direct a share of lending to the so-called productive sector, but the current classification sweeps in activities that are not productive in any economic sense. A credible tightening would start with measurement: the requirement only means something if "productive" is defined by economic contribution output, employment, export earnings, import substitution and if compliance is reported against that definition transparently enough to be checked.

The hard part is political. Every activity inside the present definition has a constituency that benefits from the directed credit it attracts, and narrowing the boundary takes something from each. That argues for careful sequencing and a transition period and for taking this up once the five primary recommendations are under way, not alongside them.

What to do first and what to leave

It is as important to say what this submission does not recommend. We deliberately leave aside three ideas that attract attention but do not, in our judgement, belong in this cycle. A central-bank digital currency is premature while the transmission of conventional policy is itself broken; building a new rail before the existing one carries a signal is a misordering of effort. A sovereign wealth fund is a serious idea, but it is a fiscal and reserve-management question deserving its own treatment, not a monetary-policy instrument. And cooperative-sector reform, urgent though it is, is a supervisory and legislative matter rather than one for monetary policy to carry.

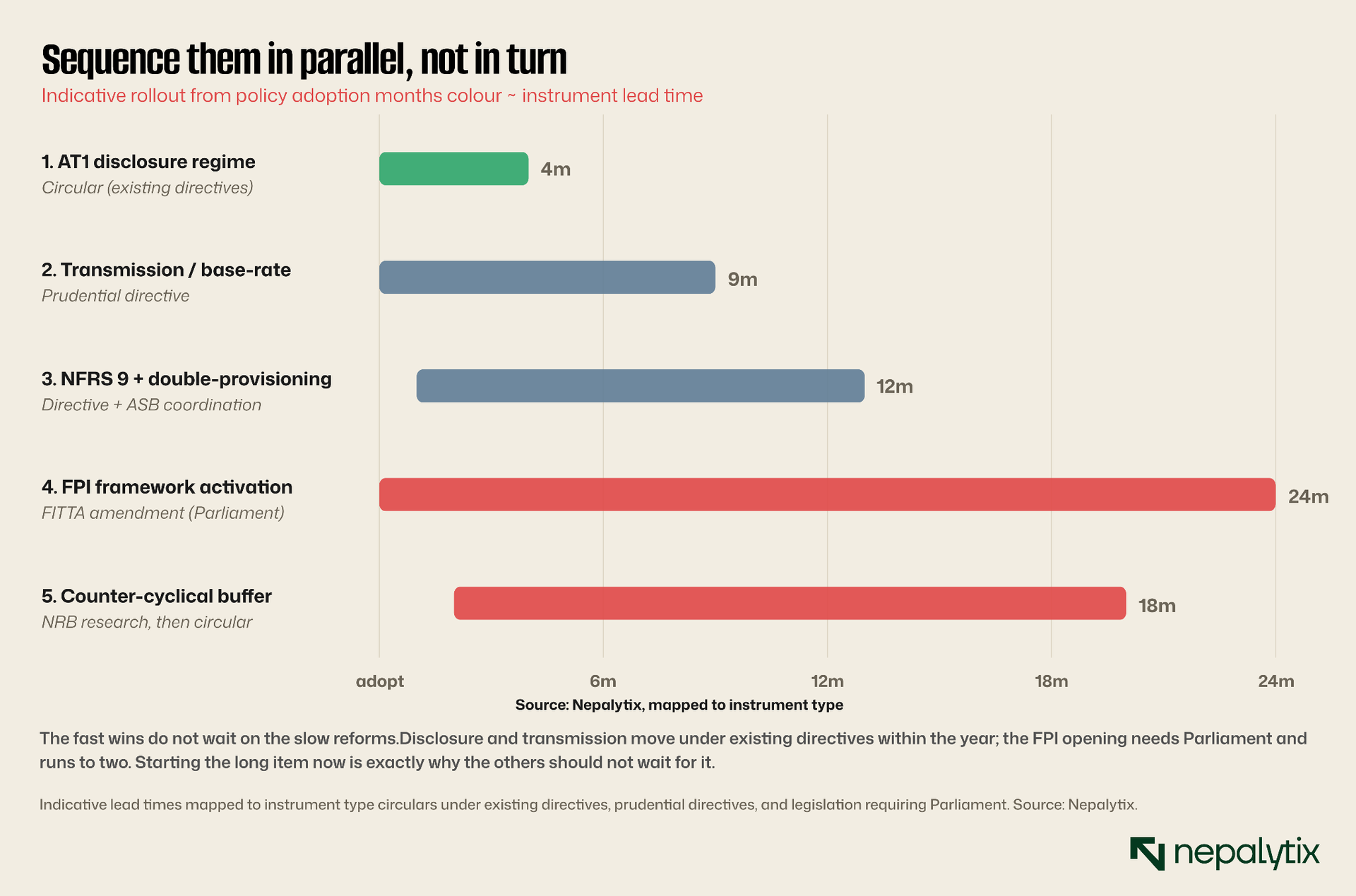

On sequencing, the essential point is that these five recommendations should be advanced in parallel, not in turn. The institutional capacity to work on several at once exists, and the lead times differ so widely that a serial approach would leave the slowest the foreign-investment opening, which needs Parliament perpetually last in a queue it can never clear. The disclosure and transmission measures can be in force within the year under existing powers; the accounting and buffer work runs over one to two years; the market opening runs to two and so must start first, not last.

The objection that the central bank cannot pursue five things at once underestimates both the institution and the nature of the tasks. Three of the five disclosure, transmission and the buffer framework are research-and-circular work that sits within existing departments and existing powers. One, the accounting transition, is already under way and needs finishing rather than starting. Only the foreign-investment requires the slow machinery of legislation, which is the argument for beginning it now, in parallel, so the drafting and inter-agency coordination mature while the faster measures are already in force. Sequenced in parallel, the full programme is the work of a single policy cycle. Sequenced in turn, it is the work of a decade and the binding constraints will not wait that long.

None of this is offered as criticism of a central bank that has, by the conventional measures, steered the economy to a position of genuine stability, low inflation, record reserves, an orderly exchange rate. The argument of this paper is precisely that the cyclical battle has largely been won, and that the returns to policy now lie in the structural work: making the rate transmit, bringing new instruments into the light, finishing the accounting transition, and opening a market that has outgrown the capital available to it. We submit these recommendations in that spirit, and publish them openly so that they can be argued with, refined, and improved.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.