Fixing SEBON won’t fix hydropower market

Nepal's hydropower IPO backlog is only part of the story. While attention remains focused on SEBON's approval delays, the bigger challenges lie in the NEA's 16,114 MW PPA queue, the enforcement of the Rs 90 net-worth rule.

The hydropower IPO queue is real. It is also a symptom. The actual binding constraint on Nepali hydropower financing sits upstream at NEA, where 16,114 MW of projects remain stranded in the PPA queue. The Rs 90 net-worth rule is not blocking good projects; it is identifying weak ones. And while regulators have been arguing about the visible problem, a worse one has scaled in the shadows: an unregulated pre-IPO market where retail investors are buying hydropower equity at fifteen to twenty-five times face value. Fix the IPO door alone, and capital still cannot flow.

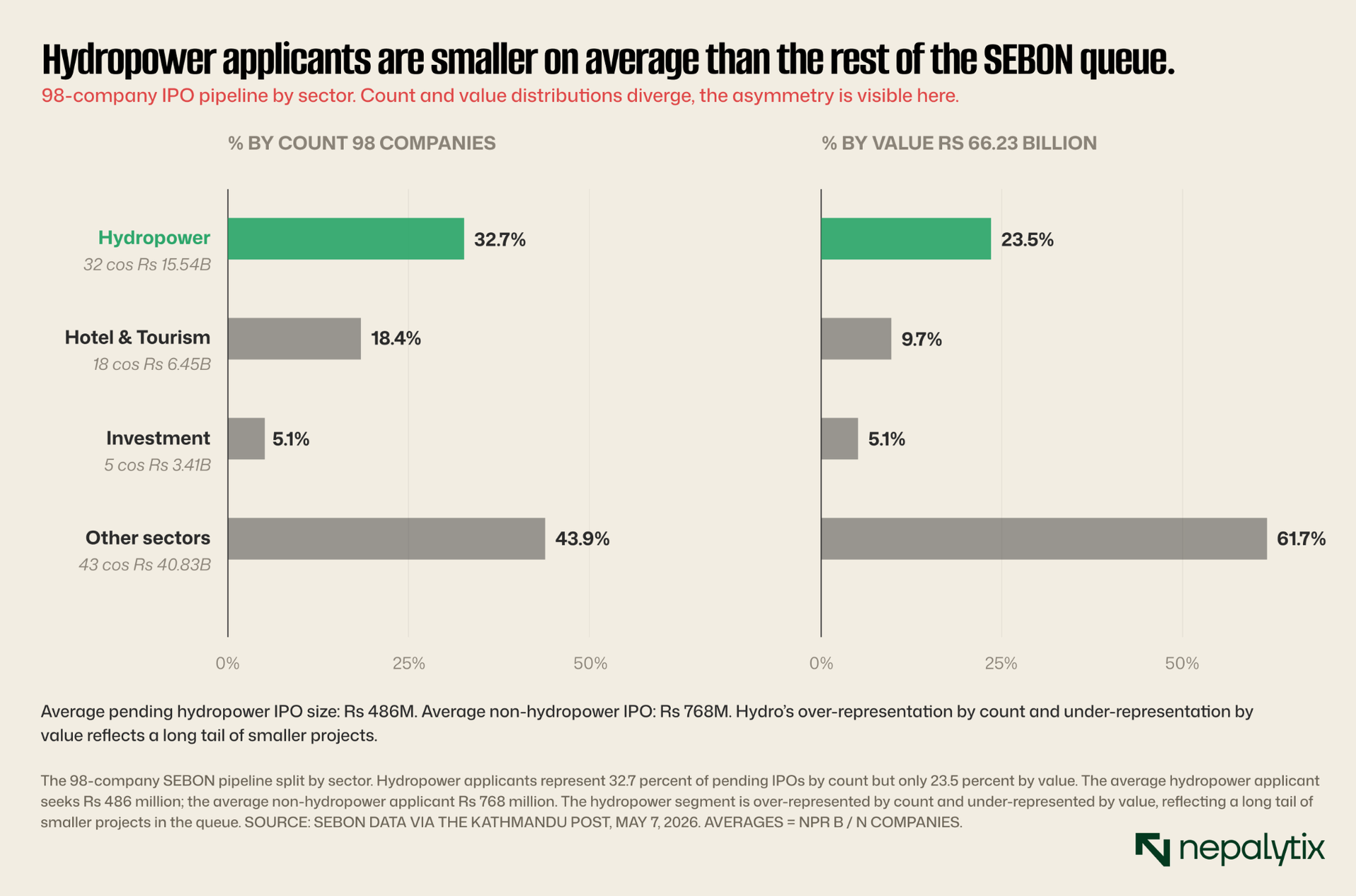

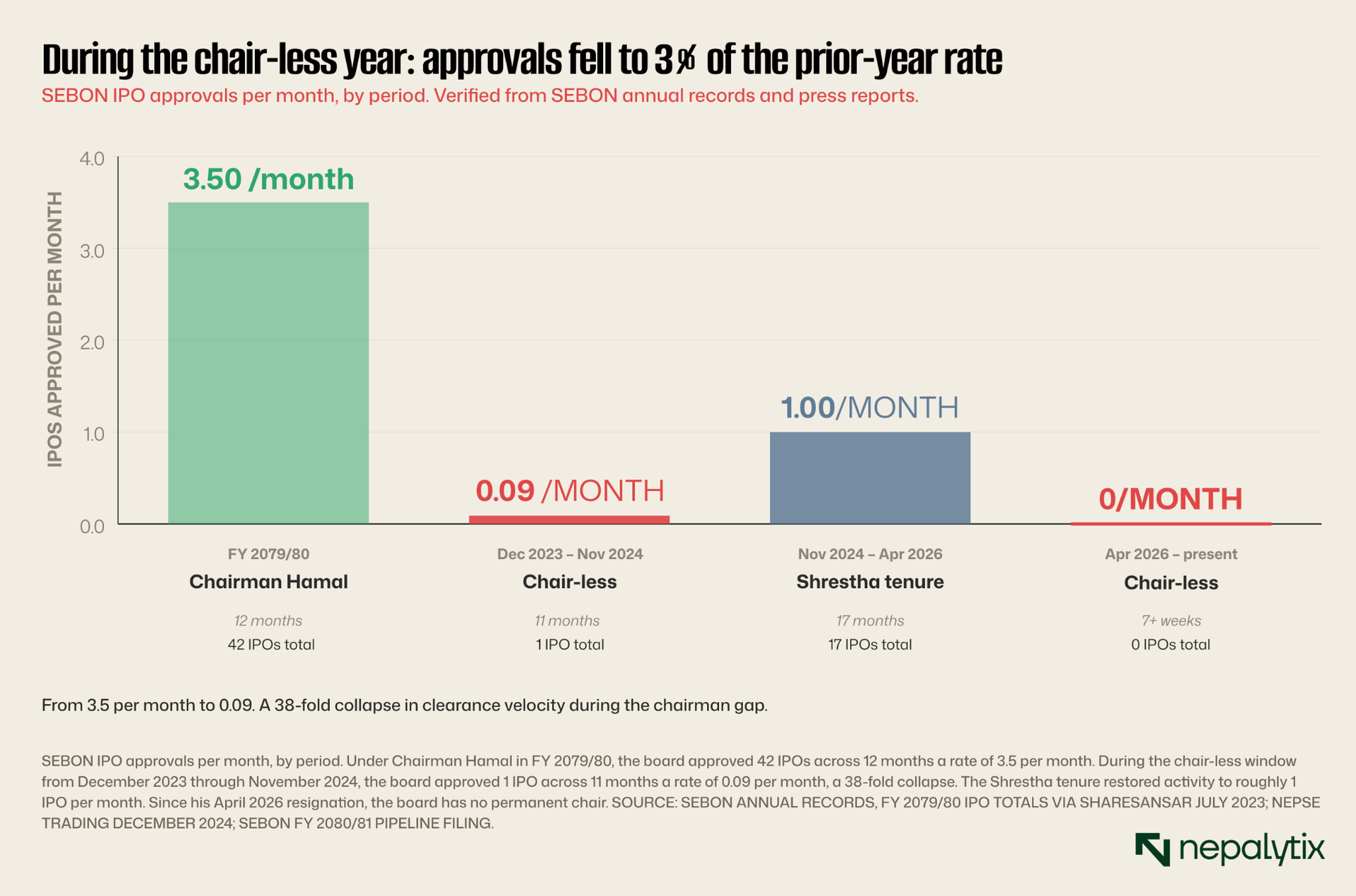

The current debate around Nepal's capital markets has a clear villain. As of May 2026, 98 companies have applied to the Securities Board of Nepal for IPO approval seeking to raise a combined Rs 66.23 billion. They have not received it. The board has been without a chair since April 17, 2026 when Santosh Narayan Shrestha resigned after seventeen months in the role and a Commission for the Investigation of Abuse of Authority probe that produced no formal charges. Before that SEBON had been without a chair for the eleven months leading up to Shrestha's November 2024 appointment. In that earlier window, the board approved one IPO. Guardian Microinsurance. That was the year's output.

The framing has hardened. Hydropower developers are being failed by regulatory paralysis; the IPO pipeline is choking the capital that the energy transition requires; SEBON's dysfunction is the bottleneck. Fix SEBON, the argument runs and Nepali hydropower can finally raise the equity it needs to build.

This is the wrong story. Or rather, it is the partly-true story that captures the noisiest piece of a deeper failure and obscures the rest of it. There is something wrong at SEBON. The board has demonstrably underperformed for nearly three years. But fixing SEBON's clearance velocity without fixing what sits upstream, downstream, and outside it would solve almost nothing. The real binding constraint on Nepali hydropower financing is the NEA PPA queue, where 16,114 MW of capacity is stranded waiting for the policy fight between Take-or-Pay and Take-and-Pay to resolve. The Rs 90 net-worth rule that has eliminated fourteen companies from the IPO pipeline is, on inspection, doing exactly what a net-worth rule is supposed to do. And the most damaging consequence of SEBON's slowness is not the projects that cannot list, it is the unregulated pre-IPO market that has filled the vacuum where retail money is being parked in hydropower equity at fifteen to twenty-five times face value with no audited statements and no exit.

To frame the IPO backlog as Nepal's primary hydropower-financing problem is to mistake the loudest crack in the wall for the building's structural defect. Below, three floors of the real argument.

Floor one: the queue that matters is upstream

Nepali hydropower equity does not become valuable because it lists. It becomes valuable because the underlying project signs a power purchase agreement with the Nepal Electricity Authority, builds, generates electricity and gets paid for that electricity at the contracted tariff over the contracted duration. A public listing is the financing event that allows external capital to participate in that economic engine. If the engine does not exist if there is no signed PPA the listing is a financing event in search of an asset. Public investors who buy into a pre-PPA hydropower IPO are buying a bet on regulatory decisions yet to be made.

This is where the consensus framing falls apart. Of the 32 hydropower companies in the SEBON queue, an unknown but material fraction do not have signed PPAs. SEBON itself has cited missing PPAs as one of the two reasons it has rejected eight hydropower applicants from the pipeline. The board did not invent this requirement; it is enforcing a sensible threshold. If a hydropower project has no buyer for its output, the question of whether it can issue equity to the public is a question Nepali regulators should be asking with considerable care.

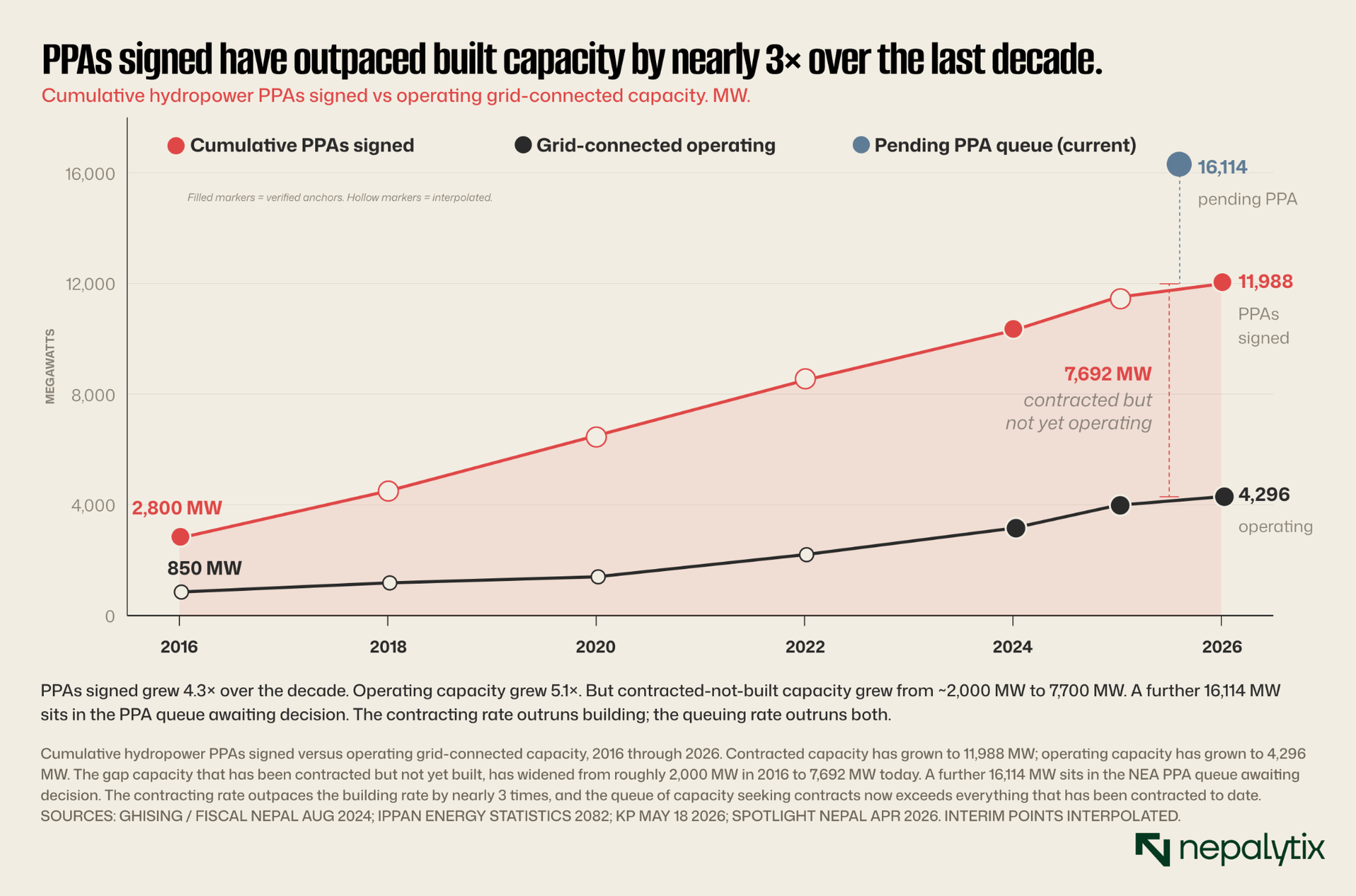

The reason the PPA gate exists is that the NEA queue itself is gigantic. According to data from the NEA Power Trade Department reported by Spotlight Nepal in April 2026, 261 hydropower projects representing 16,114 MW of capacity are stranded in the PPA queue. Of these, 124 have already secured connection agreements but are still waiting on PPA decisions. To calibrate that figure: Nepal currently has roughly 4,296 MW connected to the national grid. The PPA queue holds nearly four times the total installed capacity of the country's entire operating hydropower fleet.

The PPA queue did not back up because of regulatory absence. It backed up because of an unresolved policy fight. The FY 2082/83 budget introduced a "Take-and-Pay" provision for run-of-river projects shifting risk from the buyer (NEA) to the seller (the project developer). The previous regime had been "Take-or-Pay," under which NEA committed to pay for contracted electricity whether or not it was actually offtaken. The shift made the financial profile of new run-of-river projects substantially worse because lenders and equity investors had been pricing PPAs against the security of the take-or-pay commitment. The dispute has not been resolved. It has, in fits and starts, paralysed PPA signing for new projects. The new government has committed to clearing all pending PPA applications within 180 days. That commitment was made in March 2026. As of late May, the queue had not materially moved.

This is the binding constraint. If SEBON cleared all 32 hydropower IPOs in the queue tomorrow, the projects that depend on PPAs would still be unable to monetize. The retail investors who bought those IPOs would hold equity in companies whose only revenue line item remained contingent on a government decision that has not been made for three years. The IPO would be theatre: a clearance event without an underlying economic conclusion.

The consensus has noticed the loud part of the queue, the IPO half and missed the silent part. The silent part is bigger.

Floor two: the Rs 90 rule is doing exactly what it is supposed to do

The second piece of the consensus argument is that even where projects do have PPAs, SEBON is blocking IPO approvals on technical grounds. The technical ground most often cited is a directive from the parliamentary Public Accounts Committee that companies with a net worth below Rs 90 per share should not be permitted to issue an IPO. Industry critics have suggested this rule is mechanical, blunt, and inappropriate; that it penalises good projects with leveraged capital structures; that SEBON has hidden behind it to avoid making approval decisions.

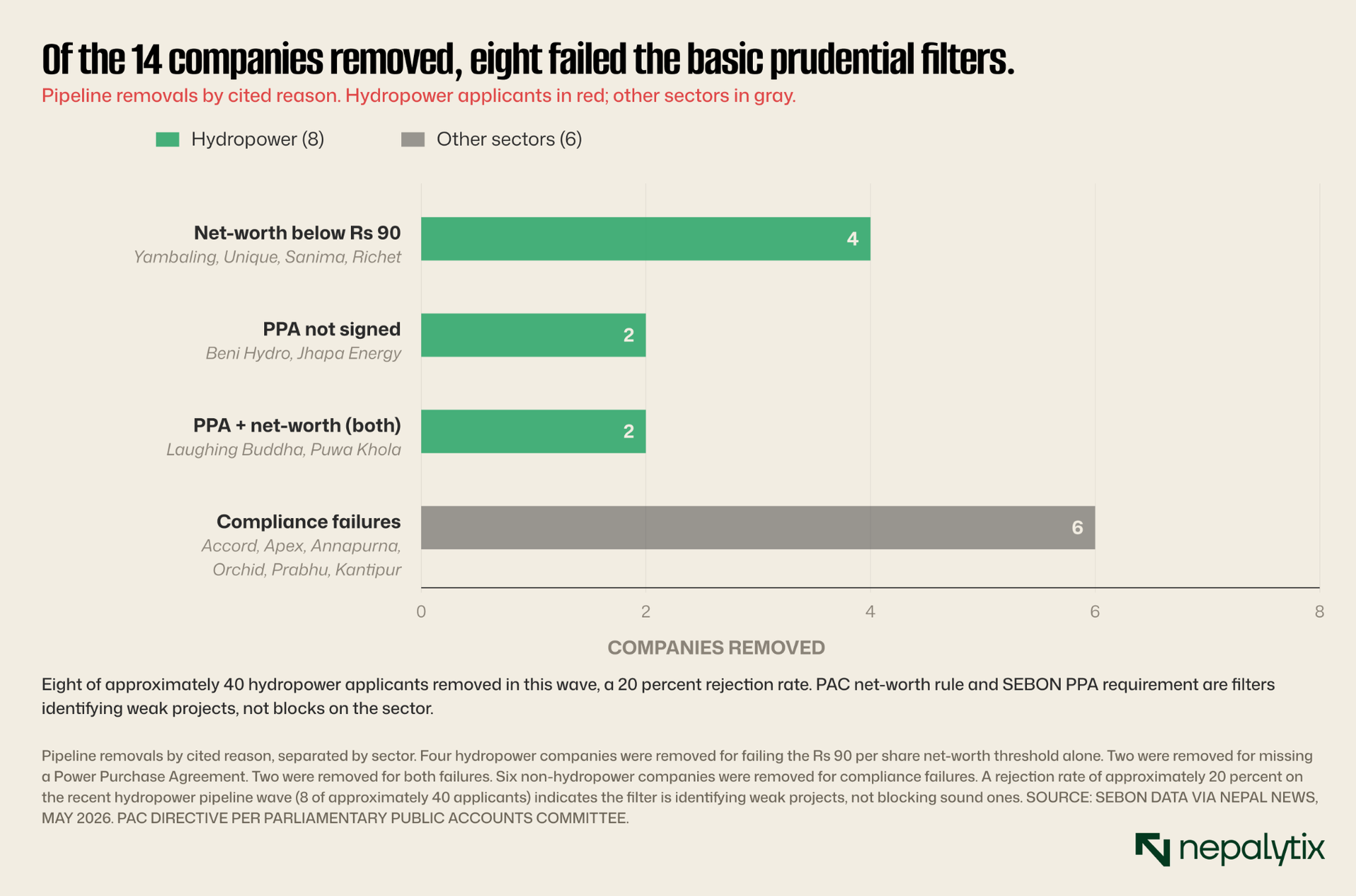

The data does not support that reading. In the most recent wave of pipeline cleanup, SEBON removed fourteen companies from the IPO queue, most of which were hydropower. The reasons were either failure to meet the Rs 90 net-worth threshold, absence of a signed PPA, or both. The eight hydropower companies removed: Laughing Buddha Power Nepal, Yambaling Hydropower, Unique Hydropower, Beni Hydro, Puwa Khola One Hydro, Sanima Hydro, Richet Hydropower, and Jhapa Energy. The six other companies: Accord Pharmaceuticals, Apex Hospitality, Annapurna Cable Car, Orchid Holdings, Prabhu Helicopter, and Kantipur Television all removed for compliance failures of various kinds.

Consider what a rejection rate of 20 percent on hydropower applicants actually implies. It does not imply that SEBON is being arbitrary. It implies that one in five hydropower companies that filed for an IPO did so without either a PPA in hand or a balance sheet strong enough to satisfy a fairly minimal net-worth threshold. The PAC directive is not a sophisticated economic test; it is the floor below which a company should not be selling equity to retail investors. A company below the floor is not a credit-worthy listing candidate. The fact that some hydropower developers regard this as an unreasonable obstacle says more about the applicant pool than it does about the regulation.

The filter is the point. A pipeline of 32 hydropower applicants from which eight had to be removed for failing basic prudential thresholds is not a pipeline that should be cleared faster. It is a pipeline that needs to be filtered more carefully. If anything, the relative ease with which weak balance sheets reached the SEBON queue suggests the upstream screening at the licensing and project-development stages has been inadequate. The IPO desk should not be the place where Nepal first asks whether a hydropower project is solvent enough to raise public equity.

The companies removed in this round can reapply once they meet the criteria. That is not a regulatory block. It is a regulatory function.

Floor three: the shadow market is the real retail harm

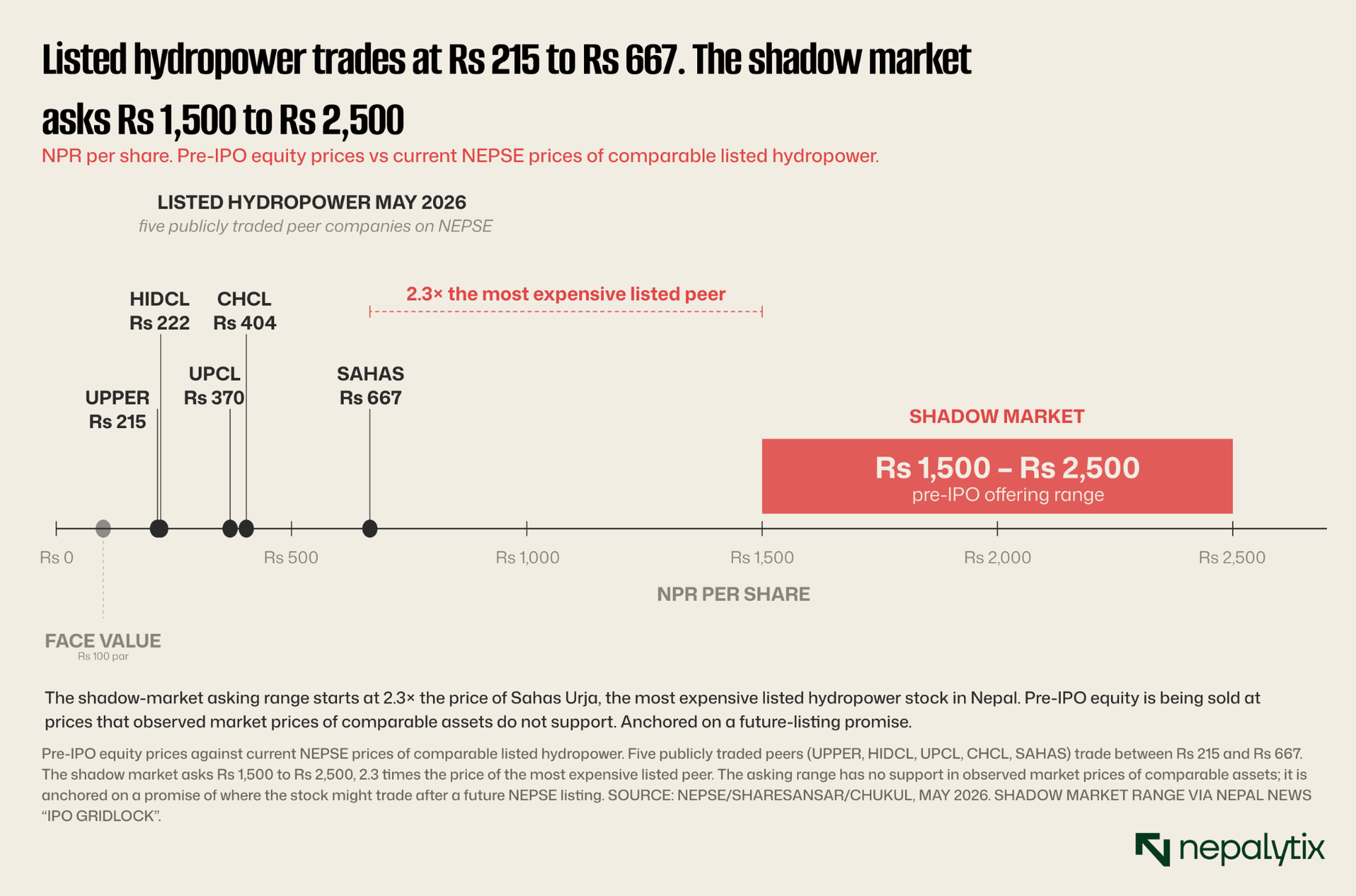

And then there is the floor underneath the floor. While SEBON has been processing applications slowly and rejecting weak ones, the front door of the Nepali capital market has been mostly shut for the better part of three years. Retail money does not stop seeking returns because the front door is shut. It finds the side door.

The side door has been a vigorous pre-IPO secondary market that has scaled significantly in the period of SEBON dysfunction. The mechanics are reported by Nepal News and corroborated across multiple merchant-bank channels: companies preparing to file for IPO and in many cases, companies still some distance from being eligible to file have sold equity stakes to retail investors at prices ranging from Rs 1,500 to Rs 2,500 per share. The face value of these shares is Rs 100. The implied multiple of face value is fifteen to twenty-five times. The marketing channels are merchant banks, WhatsApp groups, SMS networks, and personal referral chains. There is no prospectus. There is no audited financial statement. There is no liquid market in which a holder can exit. The pitch is that once the company eventually lists on NEPSE, the lock-in period expires, and trading begins, the listed price will be at or above the price paid in the shadow market.

The economic logic of these prices is fragile. To justify Rs 1,500 per Rs 100 face value, a hydropower project would need to be capable of generating something close to a fifteen-times return on initial paid-up capital after listing not as a long-run dividend stream, but as a tradeable price expectation within the lock-in horizon. The Nepali hydropower sector includes a small number of well-positioned operating companies that trade at substantial premiums to book value on NEPSE. Most of the projects being sold in the shadow market are not those companies. They are pre-construction or early-stage projects whose future cash flow is, at best, deeply contingent. The market is pricing a hope rather than an asset.

The harm to retail investors here is not theoretical. It is unfolding now, in real time, in transactions that SEBON does not see and cannot regulate. And it is being made worse by the very paralysis that the consensus argument identifies as the problem. The longer the IPO door stays closed, the more attractive the shadow door becomes because the implied arbitrage between the shadow-market price and the eventual NEPSE listing price gets larger the more pent-up demand accumulates. Speeding up SEBON's approval velocity might shrink that arbitrage; it might also, by validating the shadow-market thesis, draw more retail capital into it. The relationship is not obvious in either direction.

What is clear is that the regulatory architecture has been failing not only on the visible problem (IPO clearance) but on the invisible one (pre-IPO secondary trading). The latter is the more damaging failure because it operates entirely outside the disclosure regime that SEBON exists to enforce.

The counter-argument, treated fairly

The strongest case for the consensus framing that fixing SEBON is the priority runs as follows. The 28-month window during which SEBON has been substantively underperforming, including the 11-month chairman gap and the 17-month tenure that ended in resignation and a CIAA probe, is not a minor regulatory failure. It is the principal capital-formation institution of a frontier market failing to function. Companies that have followed the rules, secured their PPAs, met their net-worth thresholds, and submitted complete applications have nonetheless waited years for clearance. The cost of this delay is borne by the companies themselves, by the projects they were intending to finance, and by the broader sector that depends on a functioning equity market. Nepali hydropower needs equity capital. Equity capital needs a functioning regulator. The regulator has not been functioning. Fix the regulator first.

This is true. The 28-month window is a genuine regulatory failure. The CIAA probe is a genuine governance concern. The companies that have been waiting in queue have a genuine grievance, and not all of them are weak balance sheets or shell-PPAs. Some perhaps many are well-run hydropower developers with signed PPAs, adequate net worth, complete documentation, and no good reason to be in the queue for as long as they have been. Their projects are real, their need for equity capital is real, and their inability to access the public market is real.

Where the counter-argument doesn't hold

Consider the pipeline. A hydropower project moves from survey and licensing, through PPA negotiation with NEA, through construction and debt financing through SEBON IPO approval, and finally through NEPSE listing and public trading. Capital cannot reach the project until each stage has cleared. The binding constraint is whichever stage holds the longest queue. Fixing a non-binding constraint does not release more capital downstream; it shifts the queue without shortening it.

The asymmetry is visible across the pipeline. If SEBON cleared all 32 hydropower IPOs tomorrow, the projects that depend on yet-to-be-signed PPAs would still be unable to operate. The IPO would have raised capital against an asset that does not yet generate revenue. The retail investors who bought those IPOs would hold equity in companies waiting on a government decision that has been deferred for three years and may continue to be. The shadow market would not disappear; it would adapt, repricing against the new IPO-clearance velocity.

This is not an argument that SEBON should remain dysfunctional. It is an argument that the policy energy currently being directed at SEBON is on its own inadequate to the problem. Even a fully functional SEBON would not solve the upstream PPA queue, would not change the capital structure of the applicants who failed the Rs 90 rule, and would not shut down the unregulated pre-IPO market. Solving the visible problem in isolation may actively worsen the shadow market, by validating its core arbitrage thesis.

The institutional commentary so far has converged on a single demand: appoint a new SEBON chair, clear the backlog, restore IPO velocity. This is the visible solution to the visible problem. The visible problem is not the binding one.

Solving the visible problem in isolation may actively worsen the shadow market by validating its core arbitrage thesis.

What should change instead

Three policy adjustments would do more for Nepali hydropower financing than any improvement in SEBON's clearance velocity in isolation. They are listed in order of magnitude.

First, align SEBON timelines with NEA PPA decisions. An IPO approval that arrives before a PPA is signed is, for the marginal hydropower applicant, an empty document. Coordinate the two regulatory calendars so that IPO clearance is sequenced after PPA clearance, not parallel to it. This is partly a technical fix of interagency coordination on timelines and partly a substantive one: explicit recognition that the public-market IPO is the financing event for a contracted asset, not a discovery event for an uncertain one. The current Take-or-Pay versus Take-and-Pay deadlock at NEA is the real impediment to releasing capital into Nepali hydropower. Resolving it would do more for the sector than any number of additional IPO approvals.

Second, hold the Rs 90 line publicly and consistently. The PAC directive on minimum net worth is sound prudential policy. SEBON should not be embarrassed by its enforcement of that directive, and should not be pressured to make exceptions for individual hydropower developers who fail it. The rule is the filter. Companies that fail it should fix their balance sheets and reapply, not seek waivers. The signal that the Rs 90 floor will be held will, over time, improve the quality of the applicant pool which is the more durable solution to the IPO queue than any short-term clearance acceleration.

Third, regulate the pre-IPO secondary market explicitly. This is the policy gap that has done the most damage to retail investors over the past three years and is the least discussed. SEBON's current authority over merchant-bank-mediated pre-IPO transactions is limited and ambiguous. Clarifying it, requiring prospectus-level disclosure for pre-IPO equity sales above some threshold of investor count, and restricting the marketing of pre-IPO equity through unregulated channels (WhatsApp, SMS, personal referral networks) would address the part of the problem that the consensus framing has missed entirely. The shadow market exists because the regulatory perimeter has been drawn too narrowly. Redrawing it is harder than appointing a new chair, but it is the work that most directly protects the retail capital that the entire IPO debate is supposedly about.

None of these three changes is incompatible with appointing a new SEBON chair and improving the IPO clearance velocity. All three should happen alongside that appointment. But the sequence matters. A new chair who arrives, accelerates the queue, and validates the existing framing without addressing PPA timing, without holding the Rs 90 line, and without regulating the shadow market will have solved a small piece of a larger problem and may have made the larger problem worse. The IPO backlog is a real failure. It is also a useful distraction from three larger ones. The first task is to stop confusing visibility with importance.