How an IPO actually works in Nepal

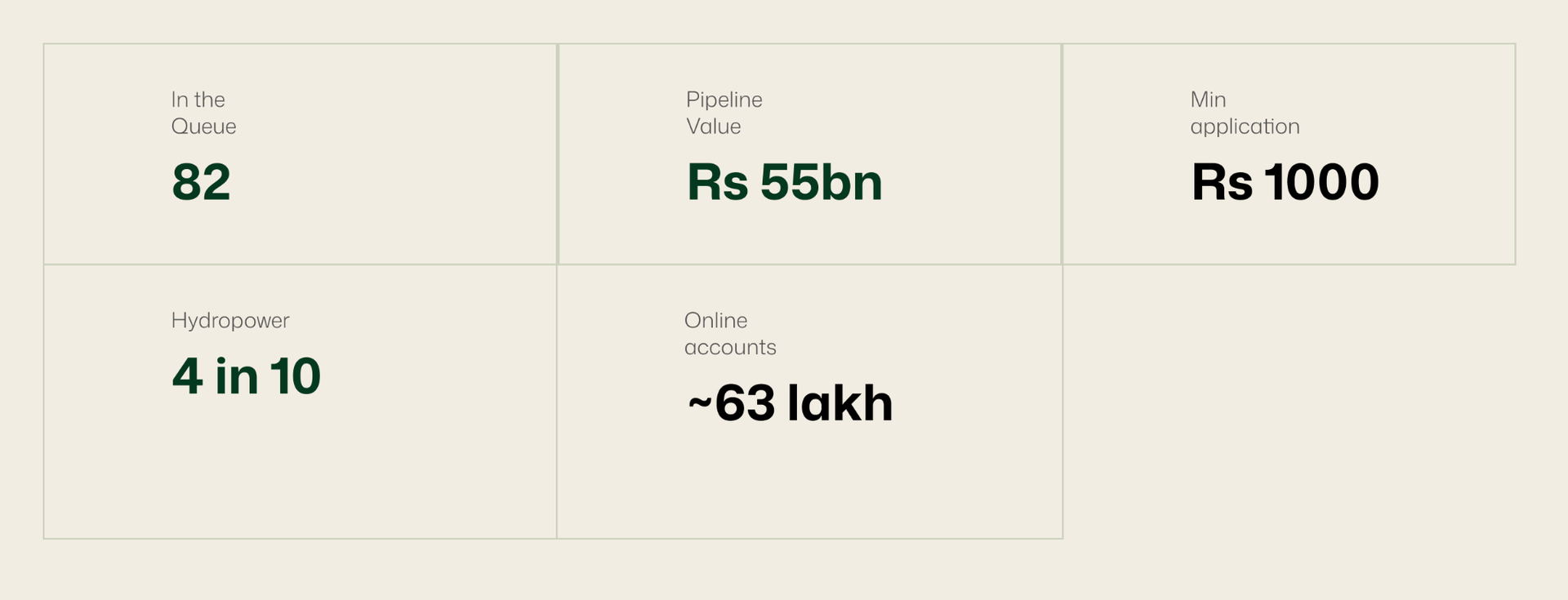

Nepal's IPO market is witnessing unprecedented growth, with 82 companies seeking to raise nearly Rs 55 billion from the public.

Eighty-two companies are queued up to sell shares to the public, worth about Rs 55 billion, one of the busiest stretches in NEPSE's history. Here is what an IPO actually is, how the shares get handed out, and why your odds of landing any are slimmer than they feel.

If you have a Demat account and the MeroShare app, you have probably applied for an IPO and probably been told, a fortnight later, that you were not allotted. You are not alone. Nepal's primary market is in the middle of a boom: roughly eighty-two companies are waiting in the Securities Board of Nepal's queue to go public together hoping to raise around Rs 55 billion and more than six million online trading accounts now exist to chase them. This is a plain-English guide to what is actually happening when a company “does an IPO” and why the whole thing works the way it does.

So what is an IPO, really?

IPO stands for initial public offering. It is the first time a privately owned company sells a slice of itself to ordinary people. Until that point the company is owned by its founders, a few large investors, maybe a bank or two. When it needs more money to build a hydropower plant, expand a factory, strengthen an insurer's capital it can borrow or it can sell ownership. An IPO is the second option: the company prints new shares and offers them to the public and in return the public's money flows into the company.

In Nepal almost all of this happens at a par value of Rs 100 a share. A few stronger companies are allowed to charge a premium above Rs 100 but most issues are plain par-value offerings. The whole process is licensed and policed by the Securities Board of Nepal (SEBON), and once the shares are handed out, the company is listed on the Nepal Stock Exchange (NEPSE), where its shares can then be bought and sold every trading day.

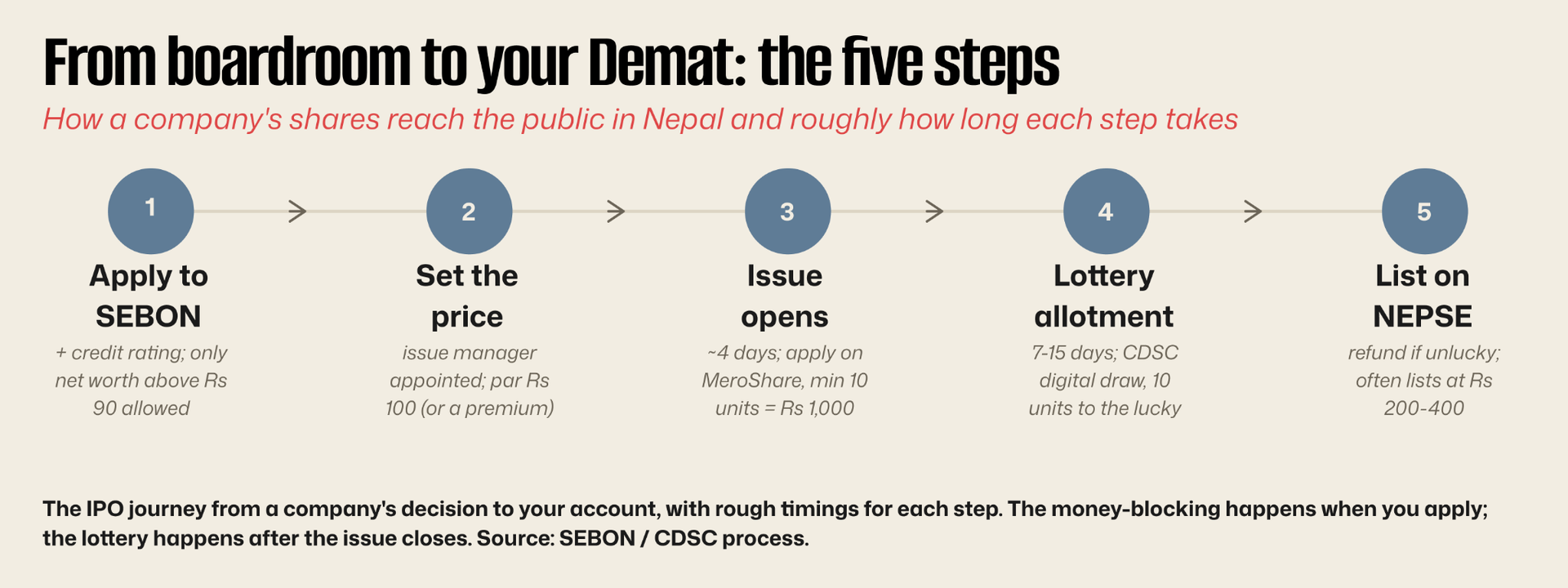

The journey has five recognisable stops.

First, the company applies to SEBON for permission, with audited accounts and a credit rating attached. SEBON has tightened this gate: following a directive from Parliament's Public Accounts Committee, only firms whose net worth is above Rs 90 a share are now allowed to proceed with a filter meant to keep the weakest companies out of the public's pockets.

Second, the company appoints an issue manager (usually a merchant bank or capital company) who sets the price and the dates.

Third, the issue opens for about four days and you apply through MeroShare for a minimum of ten units that is Rs 1,000 using the ASBA system which simply blocks the money in your own bank account rather than taking it.

Fourth, after the issue closes, the shares are handed out. If more people applied than there are shares which is almost always a computerised lottery run by CDS and Clearing decides who wins. Fifth and last, the lucky applicants see the shares appear in their Demat accounts, everyone else has their blocked money released within a few days, and the company lists on NEPSE where trading and the famous listing-day jump begins.

Why are eighty-two companies all queuing at once?

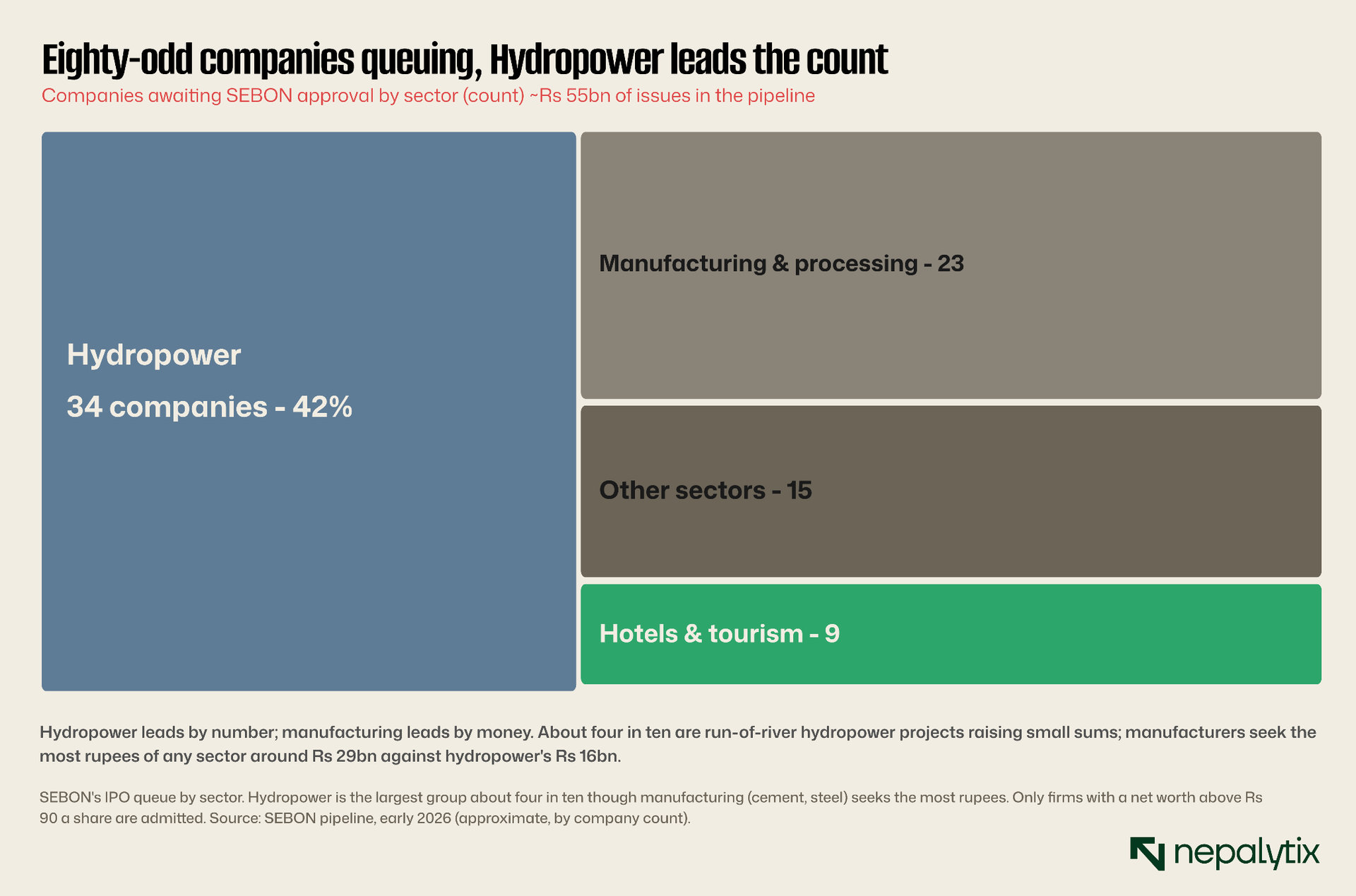

Two things are pulling companies toward the public market at the same time. The first is that money has rarely been cheaper to raise this way: bank deposit rates are low, the property market is soft and savers are looking for somewhere to put their money so demand for new shares is enormous. The second is the make-up of Nepal's economy. The single biggest group in the queue is hydropower: run-of-river projects that need large amounts of construction capital and have learned that an IPO is a cheaper, equity-based way to get it than piling on bank loans. More than four in ten of the companies in line are hydropower.

A useful nuance hides inside that chart. Hydropower dominates by the number of companies, but by rupees raised the manufacturers cement and steel makers issuing billions at a time are actually the largest sector of all, seeking around Rs 29 billion against hydropower's Rs 16 billion. So the queue is at once very crowded with small power projects and anchored by a few large industrial names. For an investor, that mix matters: a small hydropower IPO and a large cement IPO are very different propositions wearing the same Rs 100 sticker.

The lottery: why you probably won't get the shares

Here is the part that surprises newcomers. Because so many people apply for so few shares, getting an IPO is mostly a matter of luck, not size. Everyone applies for roughly the same small amount, and a transparent CDSC lottery drawn with numbered balls in front of the company, NEPSE and the media hands out a minimum of ten units to as many applicants as the shares will stretch to. The rest get nothing but their money back.

The numbers are stark. When Nepal Micro Insurance went public in early 2025, it received 1.8 million applications for its public shares thirteen times more than were on offer. Only about 184,500 applicants, roughly one in ten were allotted ten units each. Everyone else, more than 1.6 million people, was refunded. And that was a relatively generous issue: smaller, hotter offerings are far stingier. Him Star Urja, a tiny hydropower issue, was oversubscribed more than twenty-seven times so barely one applicant in twenty-five came away with shares. Across recent IPOs the win rate has run somewhere between one-in-six and one-in-twenty-five.

A quiet feature of the system worth knowing: separate slices are carved out before the public lottery typically 10% for Nepalis working abroad, around 3% for the company's own employees, and 5% for mutual funds, with a small share sometimes reserved for people living near a project. What is left is what the general-public lottery draws from.

The pop and the catch

So why does anyone bother if the odds are this long? Because when you do win, the reward has often been immediate. A share bought at Rs 100 in an IPO has frequently listed at Rs 200 to Rs 400 on its first days of trading a doubling or trebling for a Rs 1,000 outlay with almost no downside if you simply do not get allotted (your money comes straight back). For a retail investor that asymmetry feels close to a free lottery ticket and it is exactly why more than six million accounts now pile into every issue.

But the catch deserves equal billing. The listing pop is not guaranteed; it depends on how the wider market is feeling and on how richly the company is valued and weaker listings have drifted back toward par. The Rs-90 net-worth gate exists precisely because not every company in the queue is sound; a credit rating of “BB” or below, common among smaller issuers, signals real risk. And the very enthusiasm that drives the pop can leave a stock expensive the day it lists, so that the early buyers in the secondary market, the people who did not get the IPO and chase it afterwards are the ones most likely to be left holding an overpriced share. The excitement is real; so is the speculation inside it.

If you are going to apply, the practical bits

A few rules will save you grief. Apply once, with one PAN multiple applications from the same PAN get all of them rejected. Double-check your BOID and bank details because a small error makes the whole application invalid. The minimum is ten units or Rs 1,000 and ASBA blocks that money in your account rather than debiting it, so you keep the interest until allotment. Results land seven to fifteen working days after the issue closes; you can check them on the CDSC portal or MeroShare, and a refund for a non-allotment arrives within days.

None of this is advice to chase every issue that opens. The honest summary is that an IPO in Nepal is a low-stakes lottery with a genuinely attractive prize and genuinely long odds, attached to companies whose quality varies more than the uniform Rs 100 price suggests. Knowing how the machine works: the gate, the lottery, the reserved slices, the pop and its limits is what separates an informed applicant from someone buying a ticket in the dark. Next time the result reads not allotted, at least you will know exactly why.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.