How To Read a Hydropower Company

Hydropower dominates NEPSE, but most investors misunderstand what they're buying. This guide explains how PPAs, tariffs, debt, hydrology and cash flows not megawatts determine what a hydropower company is actually worth.

Hydropower is the most-owned story on the Nepal Stock Exchange: nearly ninety listed companies, a tenth of the whole market and a retail following that buys the dam more than the share. But a hydropower company is not a dam. It is a thirty-year contract with a single buyer wrapped around a river that does as it pleases. Learn to read the contract and the share stops being a patriotic bet and starts being a business you can value.

Walk into any conversation about the Nepali share market and someone will be holding a hydropower stock usually because they have stood at the foot of the project, seen the penstock and the powerhouse and felt the megawatts. The sector is the most listed on the exchange with close to ninety companies and it carries something no other sector does: a sense of ownership in the country itself. People buy hydropower shares the way they might buy a brick in a temple. The trouble is that a brick in a temple does not have to earn a return and a hydropower share does.

To read one as an investment rather than a monument, you have to put the dam to one side and look at the thing that actually generates the money: the contract. Almost every listed hydropower company in Nepal sells its electricity to a single customer, the Nepal Electricity Authority under a power purchase agreement or PPA that runs for thirty years. The PPA fixes the price, the seasons, the escalation and the risk. It is, far more than the turbine, the asset you are buying. Everything that can make a hydropower share a good or a bad investment is written somewhere in that document and most retail buyers have never read a line of it.

This piece is a guide to reading the contract and through it, the company. We will go through it the way the money flows: when the plant earns, how the tariff changes, where the cash goes once it arrives, who carries the risk when the rivers misbehave and what return is left for the shareholder at the end. By the close you should be able to look at any hydropower company on the exchange and ask the six or seven questions that actually decide whether it is worth owning. None of them is about how big the dam is.

It is worth pausing on why the sector is so crowded with listings in the first place. Nepal's hydropower potential is genuinely vast, on the order of eighty-three thousand megawatts of which perhaps forty-two thousand are considered economically feasible. Yet only around three percent of that has been built. The gap between potential and reality is the runway that draws developers and investors alike, and after a five-year pause the NEA resumed signing new PPAs in 2023, opening the gates to a wave of new projects and the share issues that finance them. The result is a sector that now counts close to ninety listed companies and about an eighth of the entire market's value, more than any other single industry. That popularity is exactly why reading these companies properly matters: a great deal of ordinary Nepali savings is riding on them.

Start with the single most counter-intuitive fact about the business, the one that trips up nearly every first-time buyer.

The plant earns least when it runs hardest

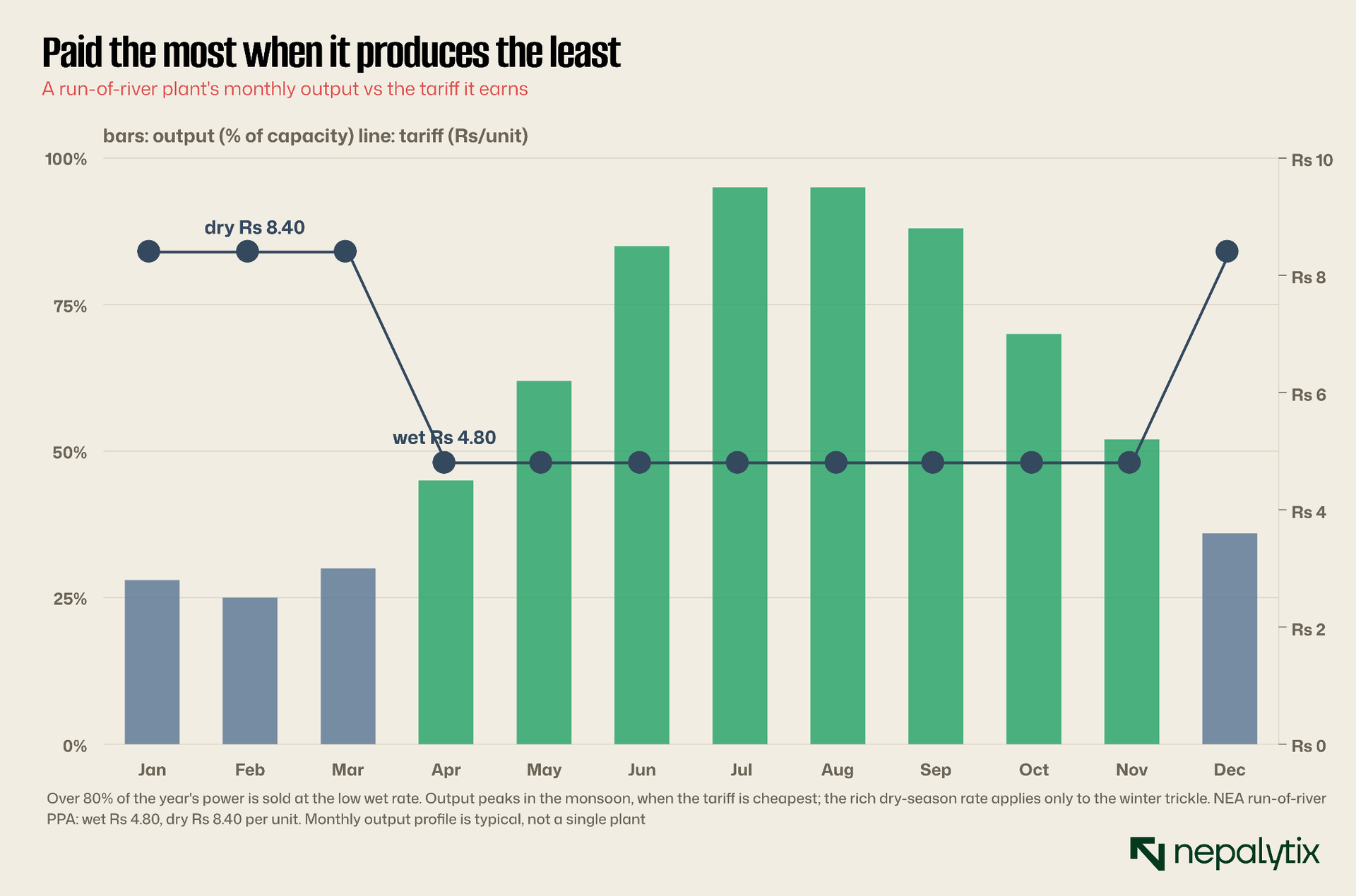

A run-of-river plant which is what most of Nepal's listed companies operate has no large reservoir. It generates from the river as the river flows which means it produces a flood of electricity during the monsoon and a trickle in the dry winter months. A typical plant runs at well over eighty percent of its capacity through the wet season and drops toward a quarter or a third in the depths of winter. Across the year it converts only about sixty-four percent of its nameplate capacity into actual energy. That number, the capacity factor or plant load factor is the first thing to look up about any hydropower company, because it tells you how much of the advertised megawattage ever turns into rupees.

Now lay the tariff on top of that output, and the cruelty of the contract appears. The PPA pays a run-of-river plant two different prices: a low wet-season rate of about 4.80 rupees per unit, and a high dry-season rate of about 8.40 rupees. You might assume the high rate is the important one. It is not because of when each applies. The wet season, when the plant generates most of its power runs roughly from mid-April to mid-December eight months. The dry season when the plant generates the least is the four months from mid-December to mid-April. So the rich 8.40 rate is paid precisely when there is barely any electricity to sell and the cheap 4.80 rate covers the monsoon torrent.

The chart makes the mismatch plain. The bars are monthly output, the line is the tariff and they move in opposite directions. Add it up and well over eighty percent of a plant's annual energy is sold at the low wet-season rate. The dry-season premium, which looks generous on paper, applies only to the winter dribble. This is why two plants with the same installed capacity can earn very different revenues: what matters is not the megawatts on the signboard but how much energy the river delivers, and at which season's price. A plant on a river with steadier year-round flow or one with even a little storage to shift output into the dry months is worth more than its nameplate suggests. A flashy monsoon-fed plant is worth less.

So the first question to ask of any hydropower company is not how many megawatts it has. It is: what is its capacity factor, how much of its energy falls in the dry season, and does it have any storage. The answer tells you how much real revenue sits behind the headline capacity.

The tariff rises for eight years then stops forever

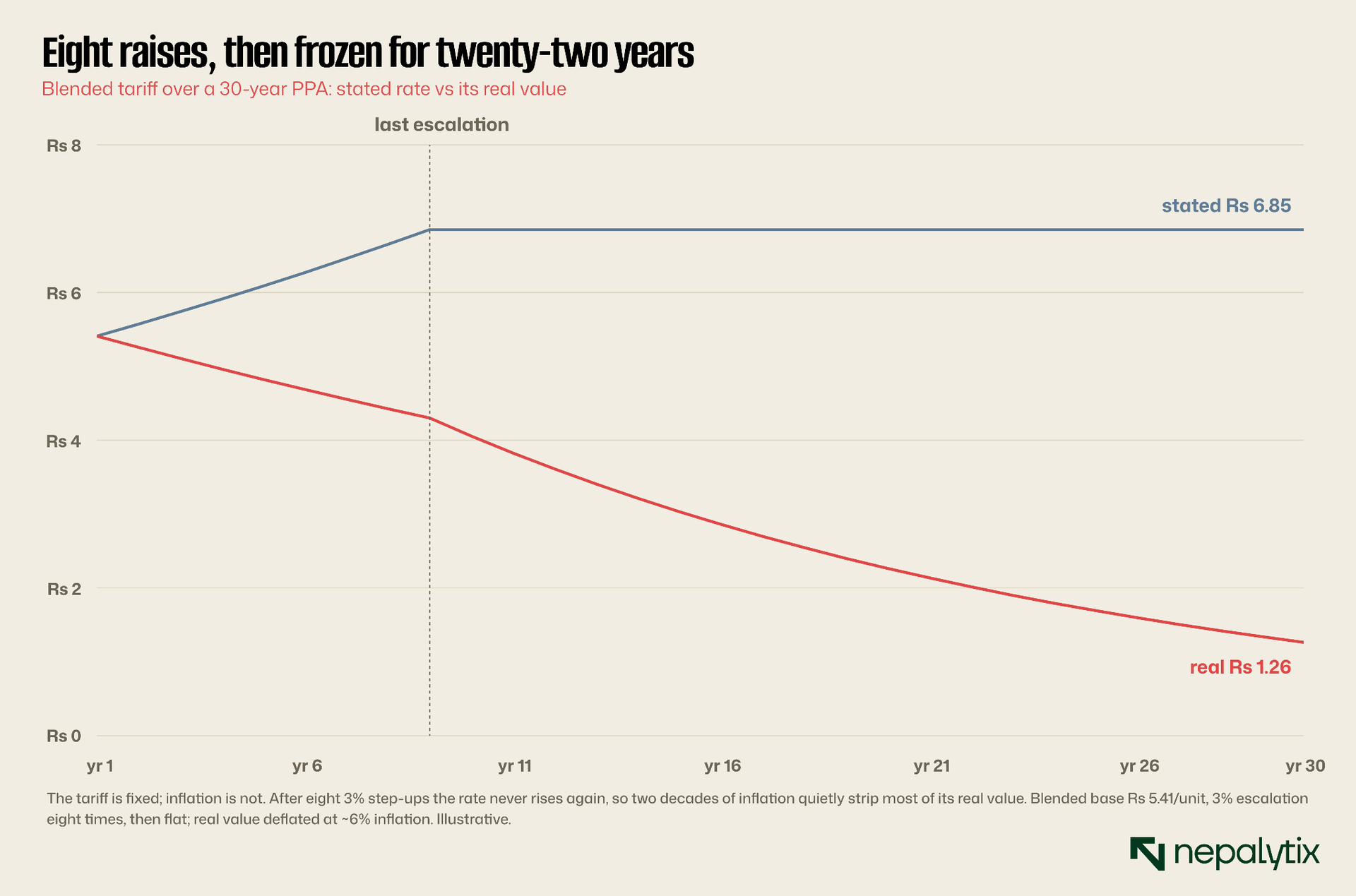

The second thing the contract does to the unwary is freeze. The PPA tariff is not fixed for all thirty years at the rate a plant starts with. It escalates by three percent a year but only about eight times. After the eighth step-up, the rate is locked for the remaining two decades of the contract. There is no further increase, no link to inflation, no adjustment for anything. Whatever the tariff is in year nine, that is the tariff in year twenty-nine.

This sounds minor and is not because inflation does not stop when the escalation does. The chart shows what happens. The stated tariff climbs for eight years and then runs flat, a straight line across the page. But the real value of that tariff, what it can actually buy, keeps falling for the next twenty-two years as prices rise around it. A rate that started near 5.40 rupees and climbed to about 6.85 is worth in real terms by the end of the contract barely over one rupee in the money of the first year. The company is selling the same electricity for the same nominal price while everything it pays for, salaries, spare parts, maintenance, climbs.

For an investor this has a sharp implication. A hydropower company's revenue per unit is highest, in real terms in its early-to-middle years, and erodes steadily thereafter. The business does not compound the way a bank or a manufacturer can because its core price is contractually prevented from rising. The way it grows is not by charging more but by building more and adding new plants under new PPAs which is why so many listed hydropower companies are perpetually raising money to develop the next project. A company with a single ageing plant and a frozen tariff is a slowly melting ice cube however solid the dam looks.

The question to ask: how many of the escalation steps are left and how many years remain on the PPA? A plant ten years into its contract has already passed its real-revenue peak. One that has just been commissioned has its best years ahead.

Follow the cash and mind the debt

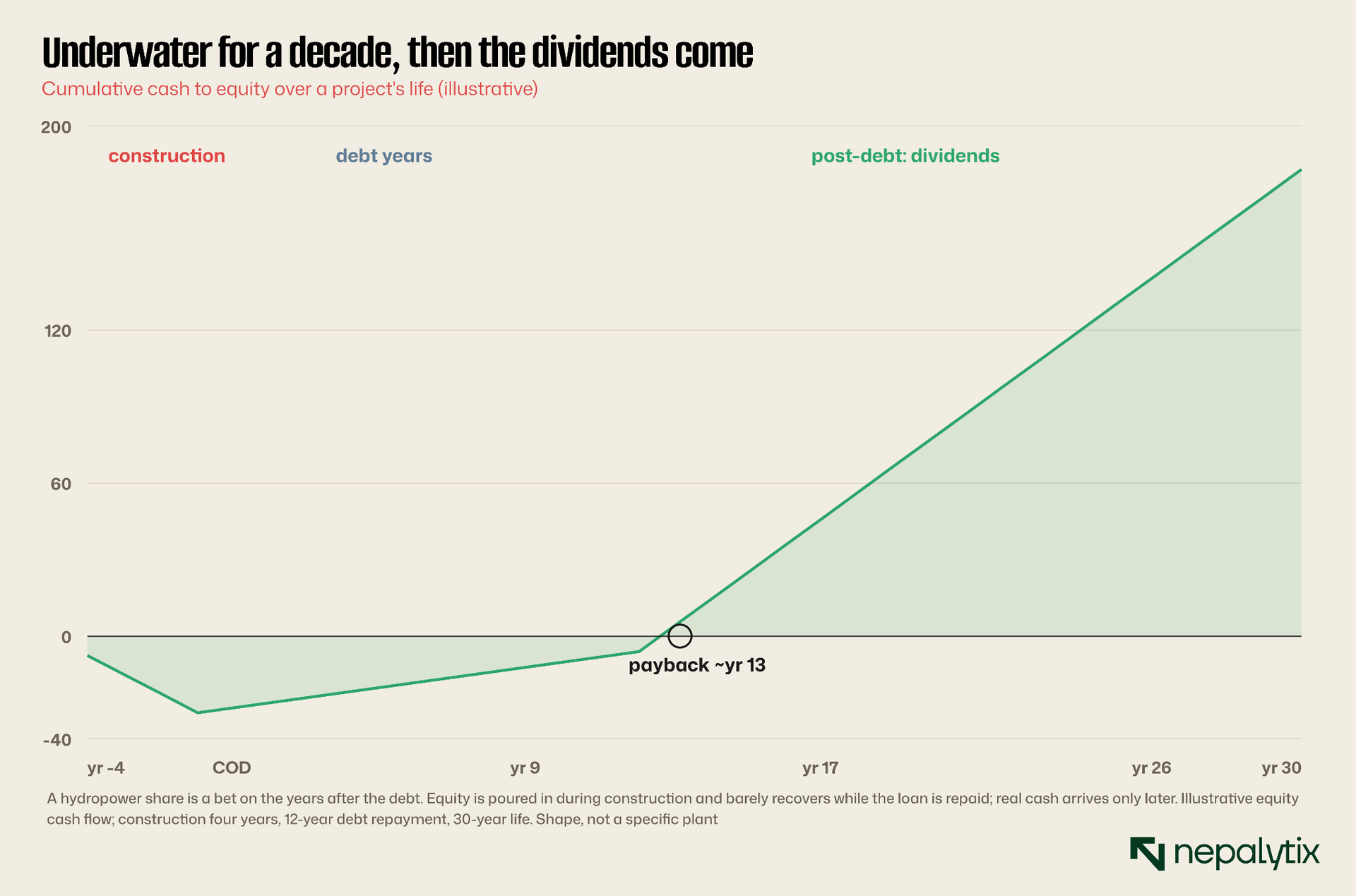

Knowing when a plant earns and at what price still does not tell you when a shareholder gets paid because between the revenue and the dividend sits a wall of debt. Nepali hydropower projects are built on roughly seventy percent borrowed money and thirty percent equity. The loans from local banks carry interest of around eleven percent and must be repaid over about twelve years after the plant starts running because that is the longest tenor Nepali banks typically offer. For the first dozen years of its operating life in other words, a plant's cash is spoken for.

Trace the whole life of a project and you get the shape in the chart, a deep J. During construction, which takes several years, equity holders pour money in and receive nothing; the cumulative cash to shareholders plunges. Then the plant is commissioned and revenue begins, but for the next decade most of the operating cash goes to the bank as interest and principal. Dividends in these years are thin, sometimes nominal even though the plant is running well. Only after the loan is cleared, often around year thirteen or fourteen, does the cash finally belong to shareholders and the curve climbs steeply into the years of real dividends.

This lifecycle is the single most misunderstood thing about hydropower investing. A retail buyer sees a fully operational, profitable-looking plant and expects a fat dividend, then is disappointed for years. The disappointment is not a sign of a bad company; it is the debt schedule working exactly as designed. The corollary is the opportunity: a well-run plant approaching the end of its debt repayment is about to transform its dividend and the market does not always price that transition in advance. A hydropower share is, in large part, a bet on the years after the loan is gone.

Watch the tax line here too because it flatters the early years in a way that can mislead. Hydropower enjoys a generous tax holiday: full exemption for the first ten years of operation and half for the next five, for run-of-river plants commissioned in time. So reported profit in the early years looks healthy but much of that profit is being handed to the bank, not the shareholder. Profit and cash to equity are not the same thing in this business and the gap between them is the debt.

One more risk belongs here, because it can interrupt the cash flow at any point: the river itself. Nepal's plants sit in steep, geologically young terrain and floods, landslides and glacial events regularly damage powerhouses, intakes and transmission lines. A single monsoon disaster can knock a plant offline for months, erasing a season's revenue and adding repair costs, all while the loan repayments fall due regardless. When reading about a hydropower company, its history of such disruptions and its insurance against them is not a footnote. It is part of the core risk and a plant on a flood-prone river deserves a more cautious valuation than one on a benign catchment.

Where a rupee of revenue actually goes

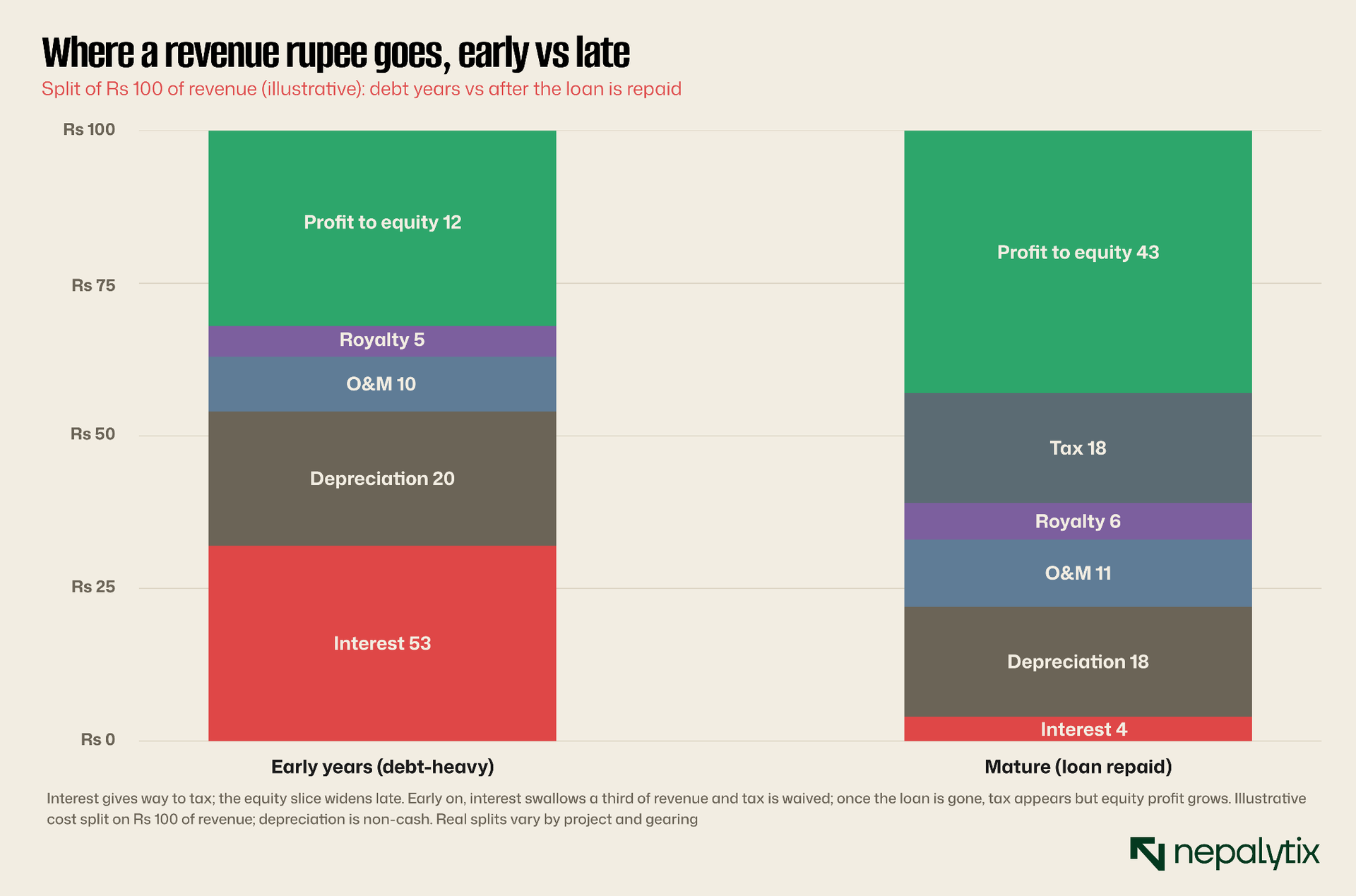

It helps to see a single rupee of revenue broken into its parts because the parts shift dramatically over a plant's life and the shift is the story. The chart shows two stacks: a typical early year when the loan is large and a mature year, after it is repaid.

In the early years, interest was the giant. It can swallow around a third of every revenue rupee on its own. Depreciation, a non-cash charge that nonetheless reduces reported profit, takes another fifth or so. Operations and maintenance, the cost of actually running the plant is modest because a hydropower plant has few moving parts and no fuel. Royalty to the government of two percent of energy sales plus a small capacity charge takes a few percent. Tax in these years is close to nothing thanks to the holiday. What is left as profit to equity looks reasonable but remember that a large part of it is immediately consumed by principal repayment which does not even show up on the profit line.

In the mature years the picture inverts. Interest shrinks toward nothing as the loan is cleared which frees up cash. But the tax holiday has expired so tax now takes a real bite. Operations and maintenance creep up as the plant ages. The profit to equity is larger and crucially it is now genuinely available to shareholders rather than pledged to lenders. The same company, the same dam, the same river produces a completely different financial profile depending on where in this arc it sits. Reading a hydropower company means knowing which stack you are looking at.

The depreciation line deserves a note of its own because it confuses many readers of these accounts. Depreciation is a large charge that reduces reported profit but involves no cash leaving the company; it is an accounting recognition that the plant is ageing. So a hydropower company's cash generation is typically much stronger than its reported profit suggests which is why some plants pay dividends that look high against their earnings. The flip side is principal repayment which is real cash leaving the company but appears nowhere as an expense on the profit line. To understand what a hydropower company can actually pay you follow the cash, not the profit and watch the two charges that pull in opposite directions: depreciation which understates the cash and principal repayment, which hides its drain.

The practical test: look at the interest expense relative to revenue and the years left on the loan. A company whose interest bill is shrinking and whose tax holiday still has years to run is in a sweet spot. One whose holiday has expired but whose debt is still heavy is in the squeeze.

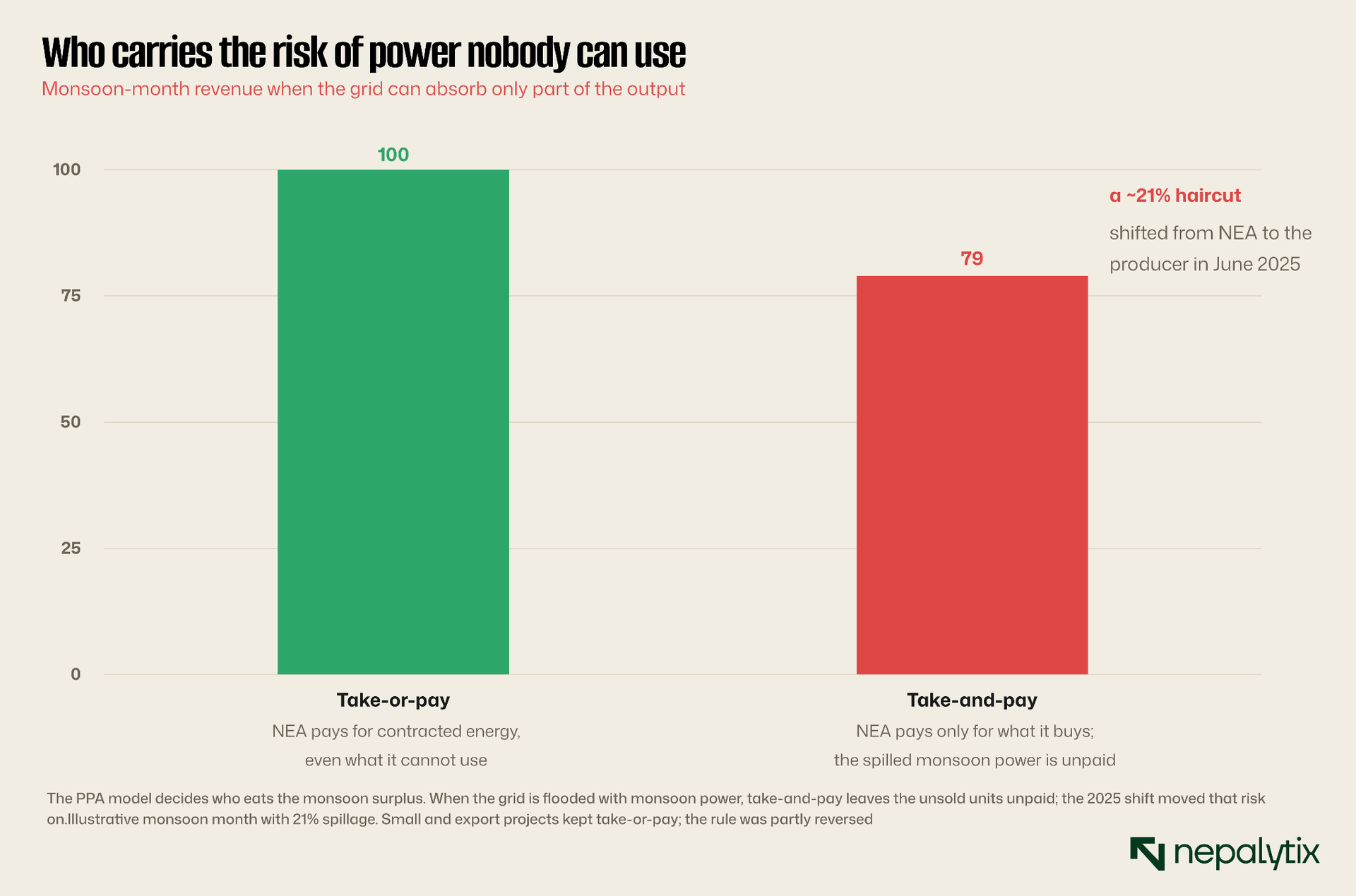

Who carries the risk of power nobody can use

For most of the sector's history, the PPA protected the producer from one large risk: that the country might not be able to use all the electricity a plant produced. Under the traditional take-or-pay contract, the NEA agreed to pay for the energy a plant was contracted to deliver whether or not it could actually absorb it. The producer was made whole; the risk of surplus sat with the buyer. This guarantee is what made the projects bankable in the first place, because no Nepali bank would have financed them otherwise.

That changed, at least in part in June 2025 when the government shifted new arrangements toward a take-and-pay model under which the NEA pays only for the electricity it actually buys. The chart shows why this matters. In the monsoon, when every run-of-river plant in the country is producing at once, the grid is frequently flooded with more power than it can use or export and some of that electricity is simply spilled. Under take-or-pay, the producer is paid for it anyway. Under take-and-pay, the spilled power is unpaid and in a heavy monsoon that can mean a meaningful haircut to a plant's most important revenue season.

The shift was controversial, was partly reversed after industry protests, and now applies unevenly: small plants of ten megawatts or less and export-oriented projects largely keep their take-or-pay terms, while others face the new model. For an investor this is now a question you must ask of each specific company because it changes the risk profile materially. A plant on take-or-pay has a contractually guaranteed offtake; a plant on take-and-pay is exposed to the grid's ability to absorb monsoon power, which Nepal's transmission system and export arrangements are still racing to expand. The same megawatts carry different risks depending on which model the contract specifies.

This is also where the much-discussed power-export story enters. Nepal aims to sell surplus monsoon power to India and Bangladesh, and to the extent it succeeds, the spillage problem shrinks and take-and-pay becomes less punishing. But export volumes remain modest relative to the ambition and depend on cross-border transmission and political agreements outside any single company's control. Treat export upside as a possibility to monitor, not a number to bank.

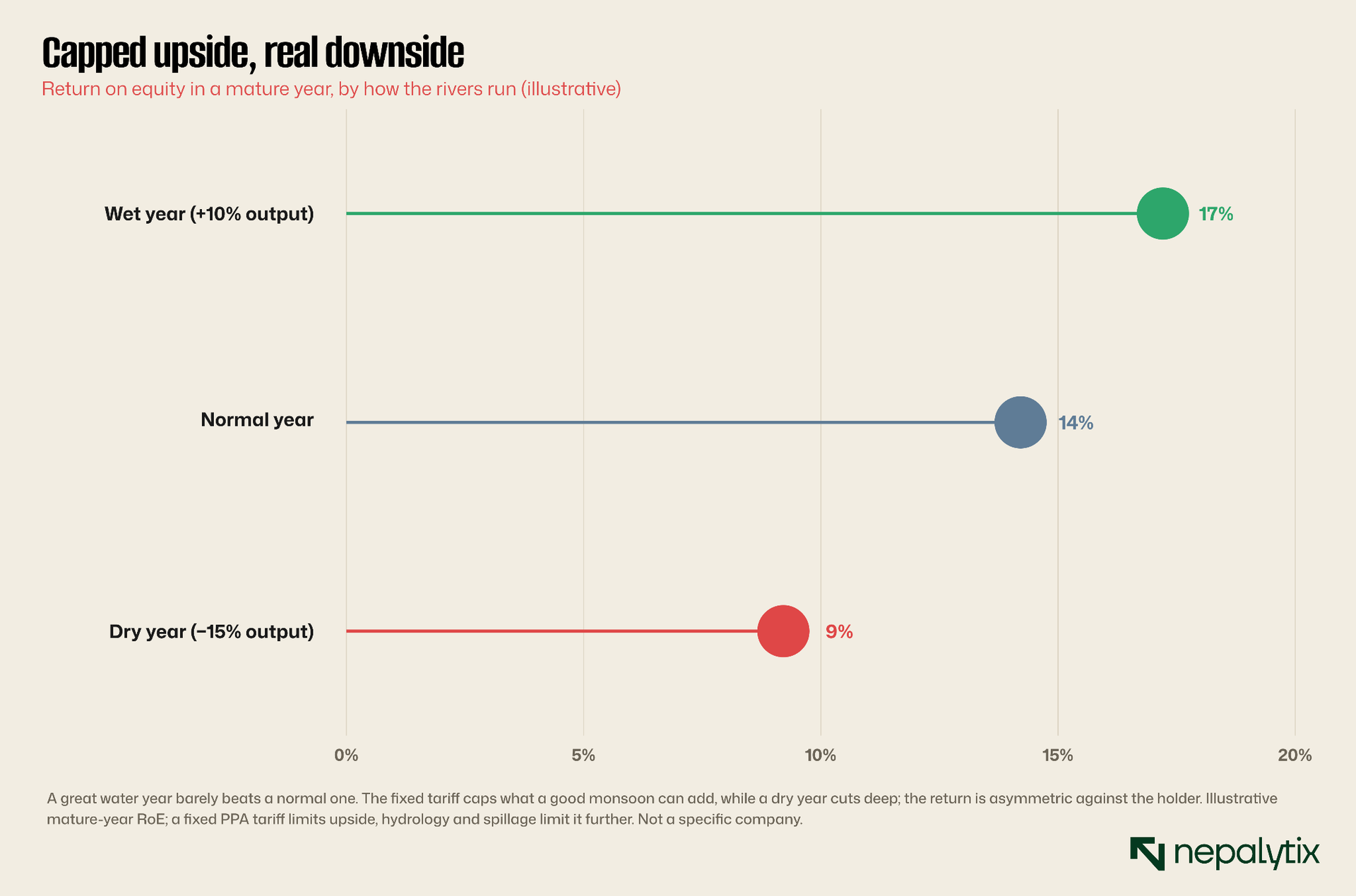

The return is capped on the way up

Put the pieces together and you arrive at the question that should have been first: what return does a hydropower share actually earn? The answer has an unusual shape and the shape is the reason a great dam can be a mediocre stock.

Because the tariff is fixed by contract there is a ceiling on how good any year can be. Even a spectacular monsoon with the river running high and the plant generating above its average, cannot earn more than the contracted rate per unit and if the grid cannot absorb the surplus under take-and-pay, the extra units may not be paid at all. So the upside of a wonderful water year is muted. The downside however is not symmetric. A dry year, with weak hydrology, cuts straight into the units generated and therefore into revenue, and there is no higher price to compensate. The chart sketches this: a good year lifts the return on equity only modestly above a normal one while a poor year drags it down sharply.

This asymmetry, capped upside and open downside is the defining financial characteristic of a Nepali run-of-river hydropower company and it should shape what you are willing to pay. A business whose best outcome is bounded but whose worst is not deserves a more cautious valuation than its steady appearance suggests. It is closer to a bond with hydrological risk than to a growth stock especially in its mature, post-debt years. The reliable dividend is real but the chance of a windfall is small and the chance of a poor year is always present.

It also explains why storage and reservoir projects, though far more expensive to build, command higher tariffs and higher strategic value. By holding water and releasing it in the dry season, they break the seasonality trap, earn the premium dry rate on real volume and provide the firm, dispatchable power the grid actually needs. As Nepal's market matures, the gap in quality between a flashy monsoon run-of-river plant and a steady reservoir project will become one of the most important distinctions an investor can draw.

A checklist for reading any hydropower share

None of this requires a spreadsheet to apply. It requires asking the right questions and the questions follow directly from the contract. Before buying any hydropower company on the exchange, work through roughly the following.

What is its capacity factor and how seasonal is its output? A higher, steadier figure means more real revenue behind the nameplate megawatts. How many years and escalation steps remain on its PPA? A young plant has its real-revenue peak ahead; an old one is sliding down the inflation slope. Where is it in its debt cycle? A plant nearing the end of its twelve-year repayment is about to see its dividend transform; one still deep in debt will disappoint despite healthy reported profit. Is the tax holiday still running, and how does that flatter the current profit line?

Then the risk questions. Is the plant on take-or-pay or take-and-pay, and how exposed is it to monsoon spillage? Is it run-of-river or does it have storage? What is its hydrology record, and has it suffered flood or landslide damage, which is common in Nepal's terrain? Who is the promoter, and do they have other projects that compete for capital and attention? And finally, the valuation question that ties it all together: given the capped upside, the fixed and eroding tariff, the debt cycle and the hydrology risk, is the price-to-book the market is asking reasonable for what is, in essence, a leveraged, seasonal, single-customer utility?

Two further questions catch common traps. First, was the plant completed on time and on budget? Delays past the required commercial operation date trigger penalties and, worse, reduce the number of tariff escalations the plant is entitled to, permanently lowering its revenue ceiling; a company with a troubled construction history may be quietly poorer than its capacity suggests. Second, who controls it and what else do they control? Many listed hydropower companies are one project among several owned by the same promoter group, and capital, management attention and the best opportunities do not always flow to the company whose shares you happen to hold. Related-party dealings, shared overheads and a pipeline of competing projects all belong in your reading.

Ask those and you will know more about a hydropower company than most of the people queuing to buy its shares on the strength of having seen the dam. The country's hydropower potential is genuinely enormous, only a few percent of it is built, and the sector will matter enormously to Nepal's future. But the future of the country and the return on a particular share are different questions and the contract, not the concrete, is where the second one is answered.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.