How to Read a Manufacturing Company

Learn how to value Nepal's manufacturing stocks the right way. Why bank metrics fail, what matters instead, and how to read companies like Shivam Cement.

Reliance Spinning Mills, a spinning mill, was the second most-traded stock on the Nepal Stock Exchange this week with roughly Rs 649 million changing hands. It outran every commercial bank on the board in a week when the whole market was half-asleep, turnover down 8.45 percent and the index parked at 2,653. A cotton-yarn factory beating the banks. Most investors who saw that number had no framework to explain it, because the Nepali market teaches you exactly one way to read a company and it is the wrong way for this one.

Seventy percent of NEPSE is banks, insurers and the financial machinery around them. So the mental model every retail investor absorbs is the bank model. You learn to reach for price-to-book. You learn that a stock "below book" is cheap. You learn that dividends come out of a distributable-profit reserve after the regulator takes its cut. That model is correct for a bank. Point it at a factory and it returns nonsense.

The type error

A bank is worth a multiple of its book value because for a bank, book value is the business. Equity is the buffer that backs risk-weighted assets. Regulators measure it, cap growth against it and force you to raise more of it. When you pay 1.5 times book for a bank you are paying for the earning power that regulated equity is permitted to generate.

A factory is not worth its book. Its book is a pile of depreciating machinery, a warehouse of inventory and a plot of land carried at some historical number. None of that is what you are buying. You are buying the cash the plant throws off this year, next year, across a cycle. A cement kiln carried at Rs 4 billion on the balance sheet might generate Rs 1.5 billion of cash a year or might generate nothing depending on whether anyone is building anything. Same book, wildly different worth. Applying price-to-book to a manufacturer is a category error, like measuring a runner's speed in kilograms.

Take the number literally for a second. Shivam Cement carries a book value near Rs 190 a share and trades around Rs 612 more than three times book. On the bank reflex, that screams "expensive." But that book is a cement plant and a limestone quarry, and the Rs 612 is a claim on the cash the plant throws off; in a good year it earns more than enough to justify a large premium to book. Price-to-book did not tell you the stock was cheap or dear. It told you nothing at all.

So put the bank lens down. Here is the lens that actually works five things, in order.

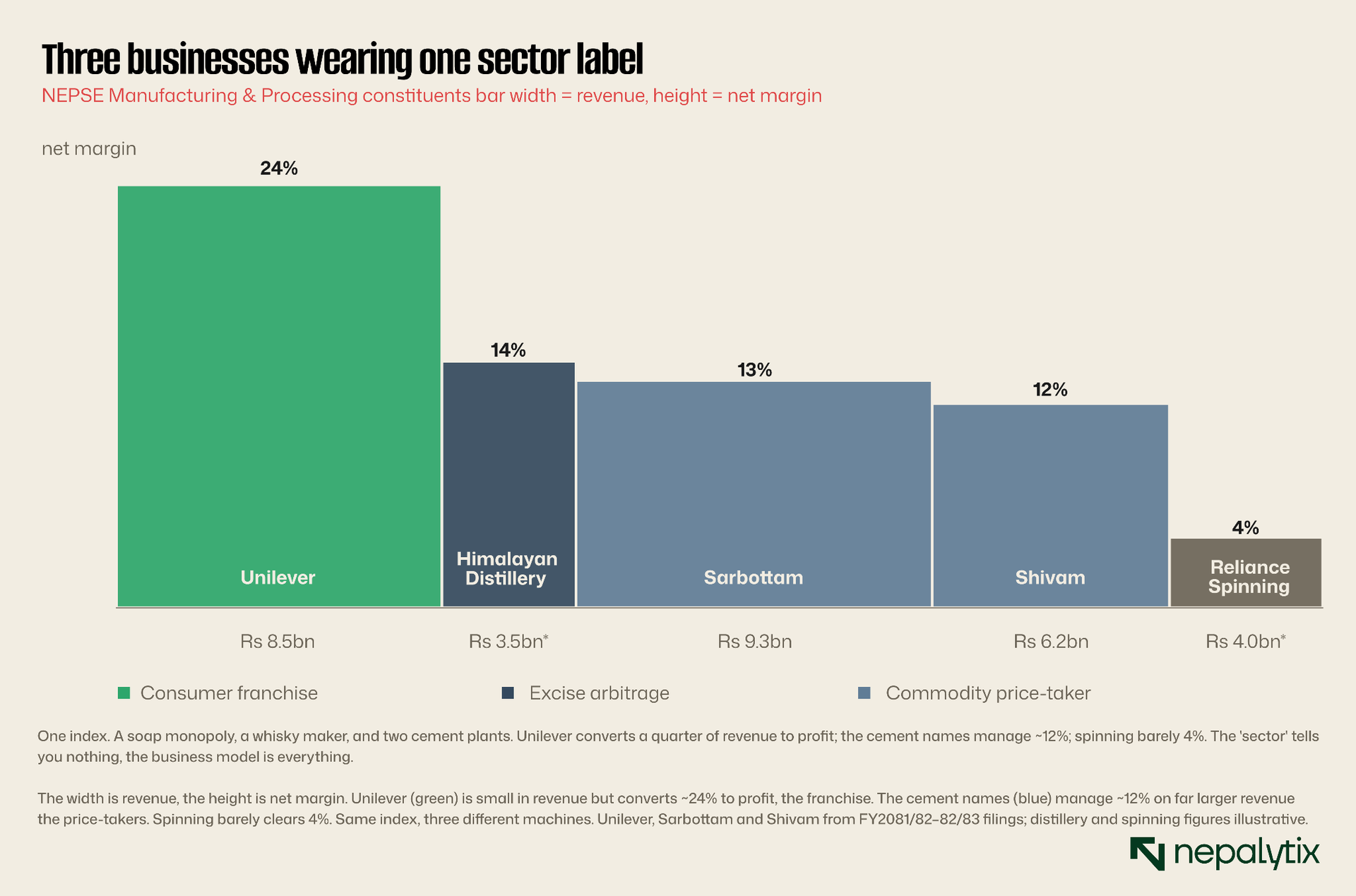

One: it is not one sector, it is three

NEPSE files everything from soap to whisky to cement under a single index called Manufacturing & Processing. Treat that label as information and you will misprice everything inside it. Under that one heading sit three completely different businesses and the only thing they share is that they run a factory.

The first is a consumer franchise. Unilever Nepal converts about 24 rupees of every 100 in revenue into net profit on a return on equity near 39 percent because it owns brands and shelf space that no competitor can cheaply replicate. That margin is a moat.

The second is a commodity price-taker. The cement makers Sarbottam, Shivam run at roughly 12 to 13 percent net margin in a good year and the margin is not theirs. It is the spread between the cost of clinker, coal, and power and a bag price set by the market. When construction slows or a rival adds a kiln, that spread compresses and the margin evaporates. A spinning mill is the same story with thinner numbers.

The third is an excise arbitrage. A distillery's economics are dominated by the government's excise structure. The margin is real, but it lives or dies on a line in the budget not on anything the company does.

Read the margin and you know which of the three you are holding. A 24-percent business and a 4-percent business should never trade on the same logic, yet in Nepal they trade under the same one-word label. That is the first edge: the sector tells you nothing; the business model tells you everything.

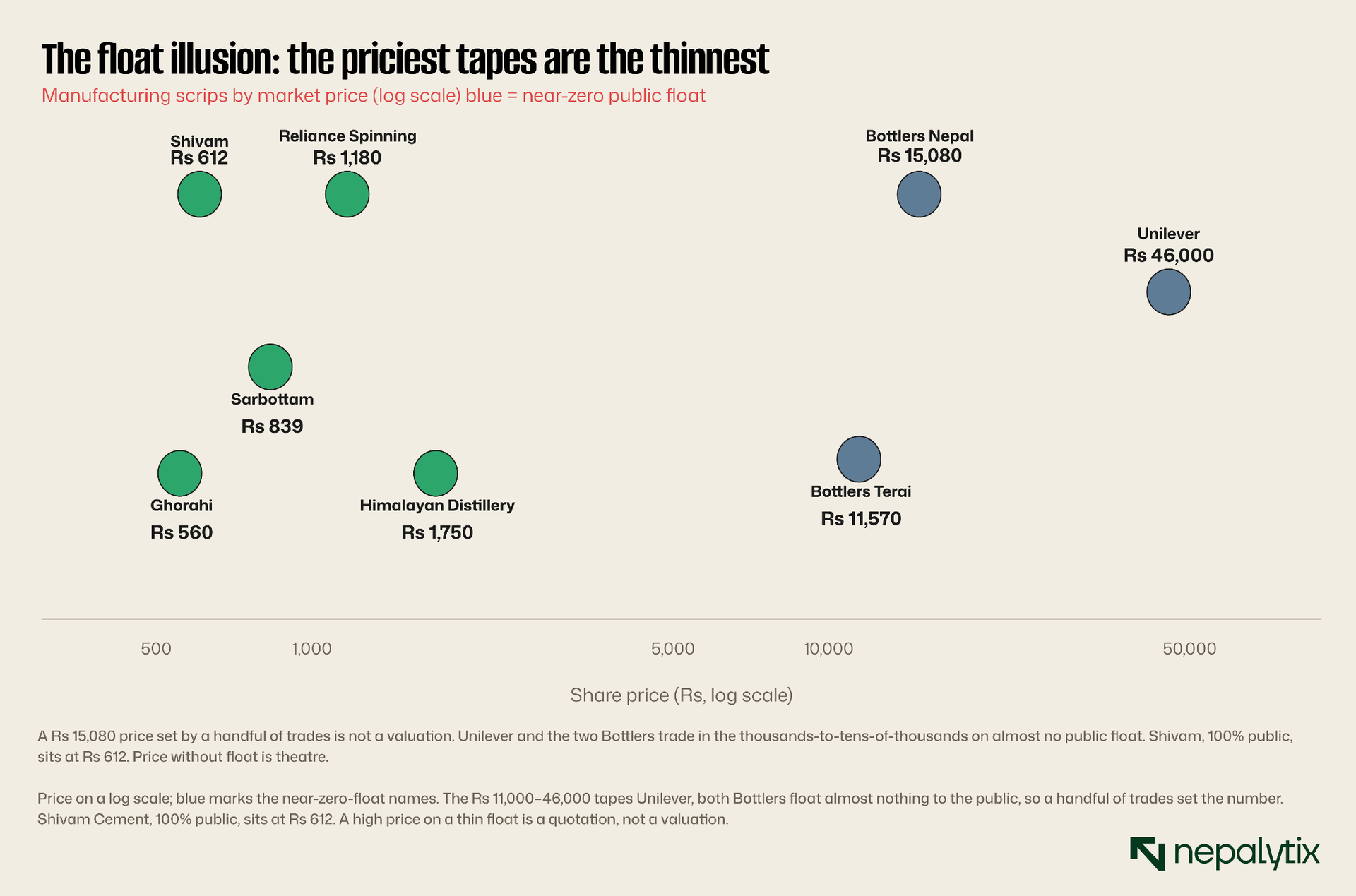

Two: the price is not the price

Now look at the tape and you hit the second trap immediately. Bottlers Nepal the Coca-Cola bottler trades around Rs 15,080. Its sister company in Terai trades at Rs 11,570. Unilever changes hands in the tens of thousands. These look like the most valuable companies on the exchange. They are not. They are the ones with almost no shares in public hands.

When 90-odd percent of a company's shares are locked with promoters, the "market price" is set by whoever trades the sliver that floats sometimes a few hundred shares a day. That price can be anything. It tells you what the last buyer paid, not what the business is worth. Nepal Lube Oil has zero public shares; its quote is essentially decorative. Compare that with Shivam Cement which is 100 percent public: its Rs 612 is a real, contested, market-cleared price. Before you are impressed by a five-figure share price, check the float. Usually the price is high because the float is thin, not because the business is extraordinary.

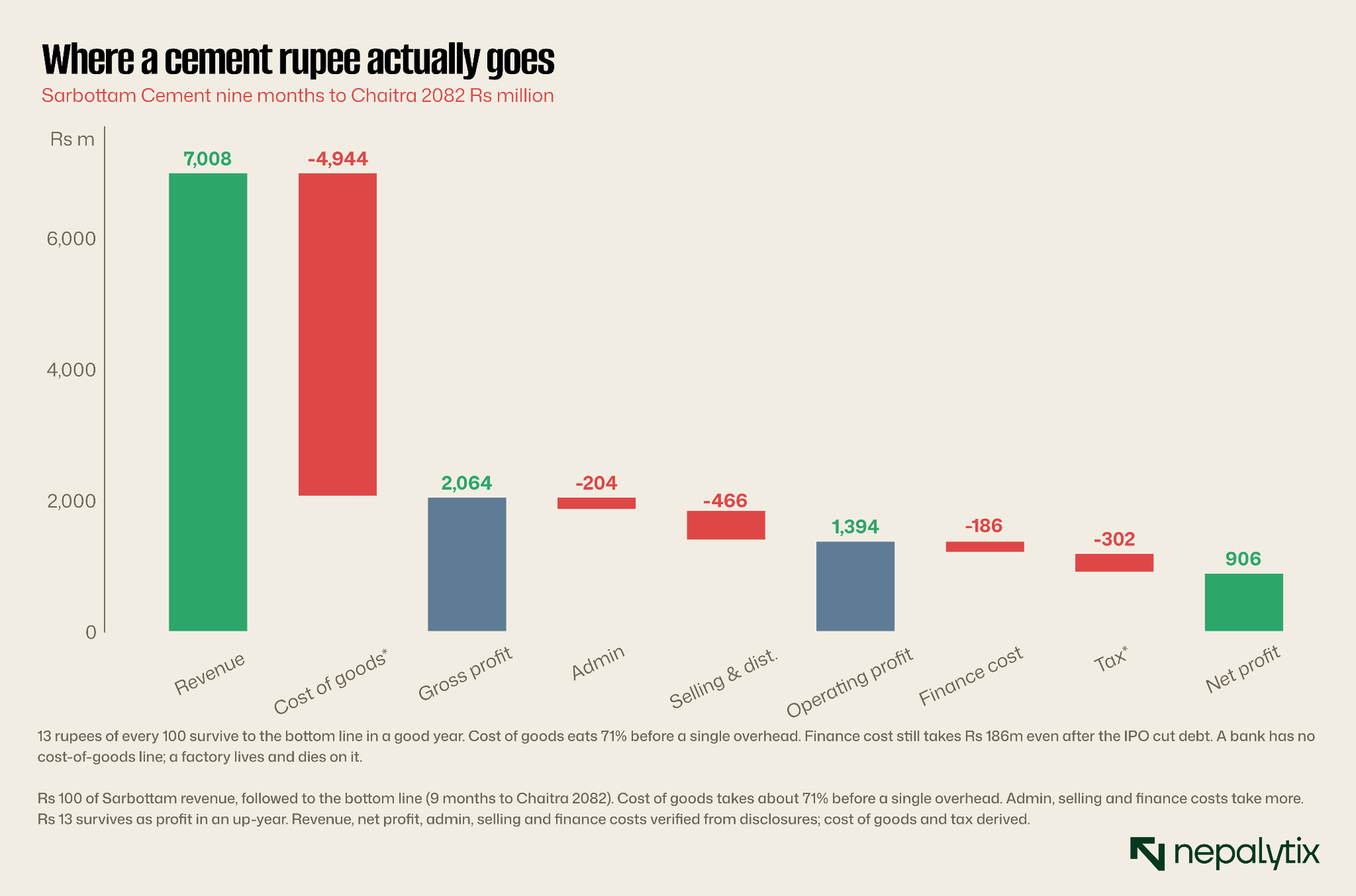

Three: read the rupee not the multiple

The single line that separates a manufacturer from a bank is the one at the very top of a factory's income statement and absent entirely from a bank's: cost of goods sold. A bank has no warehouse of raw material. A factory's whole game is the gap between what it pays for inputs and what it sells the output for and that gap is narrower than beginners think.

Trace a single rupee of cement revenue and the lesson is blunt. The cost of goods eats roughly 71 percent of it before the company pays a single salary or a rupee of interest. Selling and distribution cement is heavy and shipping it is expensive takes another slug. Finance cost still claims Rs 186 million even after Sarbottam's IPO paid down most of its debt. What survives is about 13 rupees of profit for every 100 of sales, and that is a good outcome. This is why a manufacturer's earnings can collapse on a small move in input costs or selling price: there is very little cushion between the top line and the bottom. A bank's spread does not swing like this. A factory does.

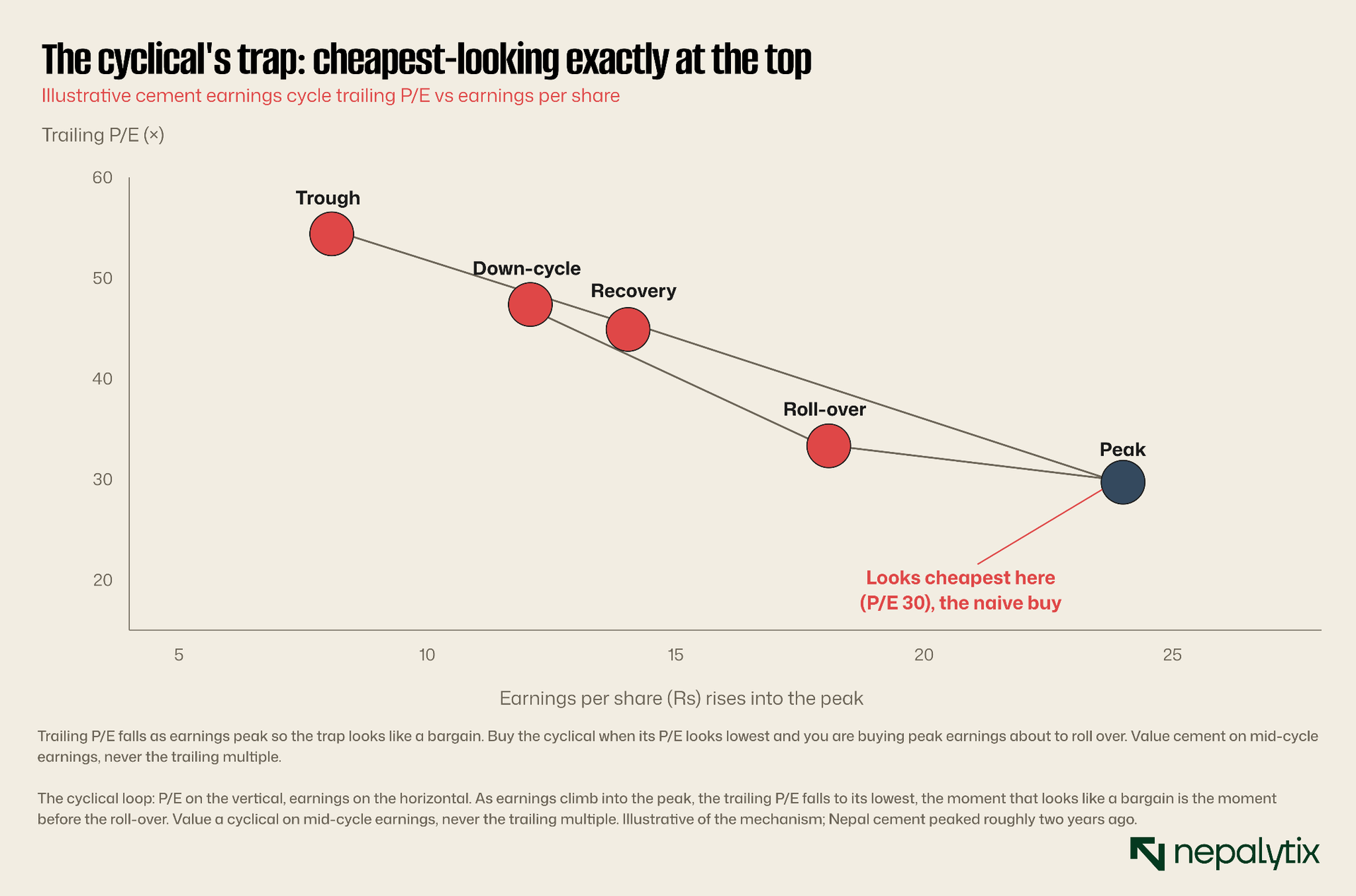

Four: the cheapest-looking moment is the trap

Because these earnings swing, the multiple you were taught to trust will actively mislead you. A trailing price-to-earnings ratio divides today's price by the last year's profit. For a cyclical, the last year's profit is highest exactly at the top of the cycle so the P/E looks lowest precisely when the stock is most dangerous.

Follow the arrows. At the peak, earnings are high and the P/E reads 30 cheap says the screener and the naive buyer buys. Then construction demand softens, the spread compresses, earnings roll over and the "cheap" stock re-rates downward on falling profits. The investor who bought the low trailing P/E bought peak earnings about to reverse. The fix is not complicated: value a cyclical on its mid-cycle or normalised earnings what it makes across good years and bad not on the last twelve months. Nepal's cement sector, by most readings, peaked around two years ago. A trailing P/E today is measuring a different animal than the one you would own next year.

Five: the sub-sector is not the stock

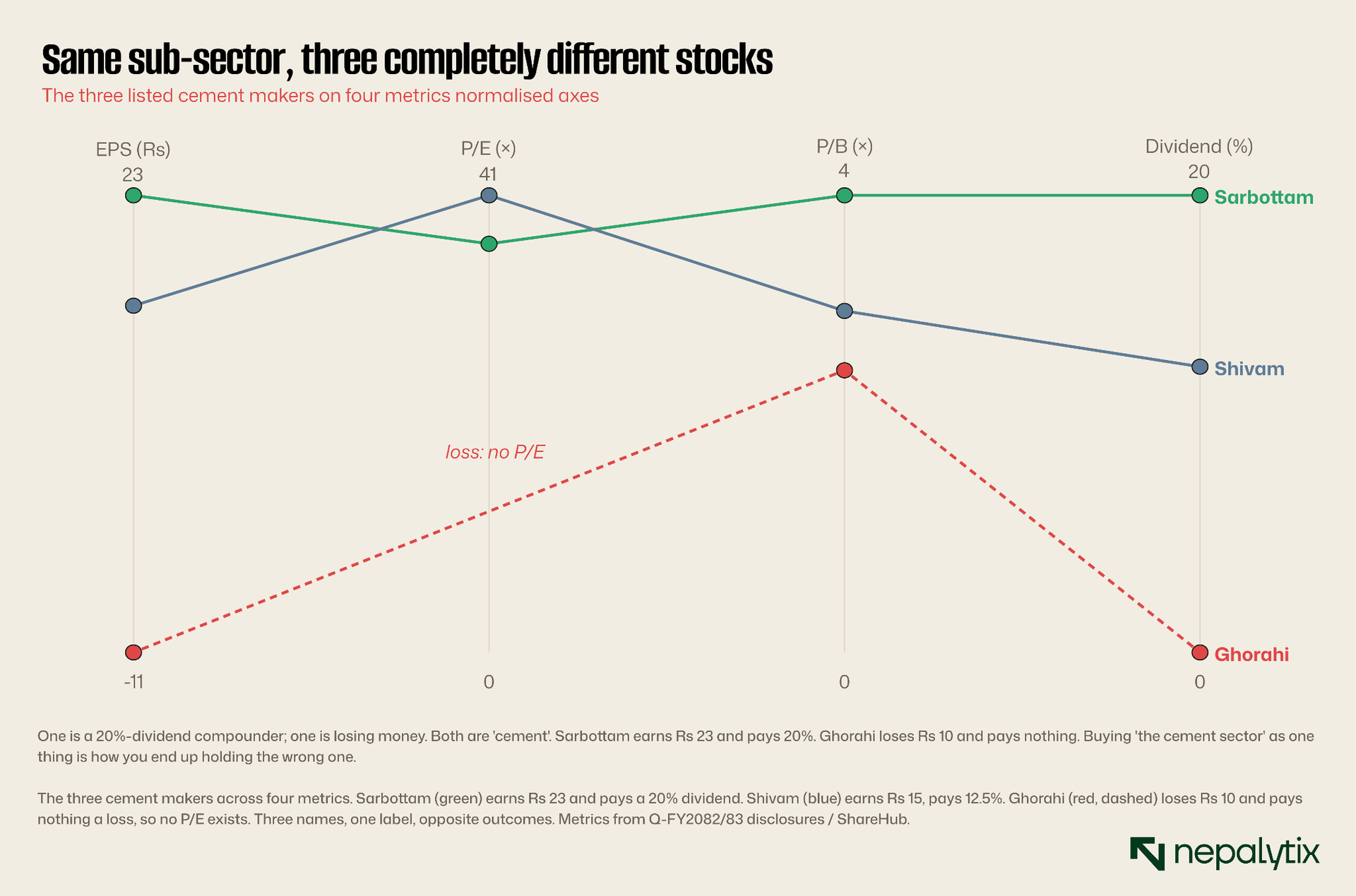

Even inside a single sub-sector, the companies diverge violently and this is where "buy the cement story" gets people hurt. There are three listed cement makers. They do not move together.

Sarbottam is a 20-percent-dividend payer trading on real, growing earnings. Ghorahi is losing money sliding about 16 percent over the past year with a promoter lock-up unwinding into a weak market. Shivam sits between them, and interestingly trades at a discount to Sarbottam on book while paying a smaller dividend a puzzle the peer reads exists to surface. "Cement is doing well" is not a thesis. Which cement, at what point in its own cycle with what float overhang, is the thesis. Buying the sub-sector as one thing is how you end up holding the wrong one.

Part of that spread is not about cement at all, it is about shares. Shivam's promoter lock-up expired back in 2022 so its float is fully cleared and the market no longer discounts a wall of future supply. Ghorahi is the mirror image: roughly 80 percent promoter-held, with a lock-up unwinding into a weak tape right about now, an overhang that sits on the price regardless of what the kilns do. Same product, same island of limestone but one stock has already absorbed its supply and the other has not. Reading the company means reading its share register, not just its plant.

The tell you can check in one number

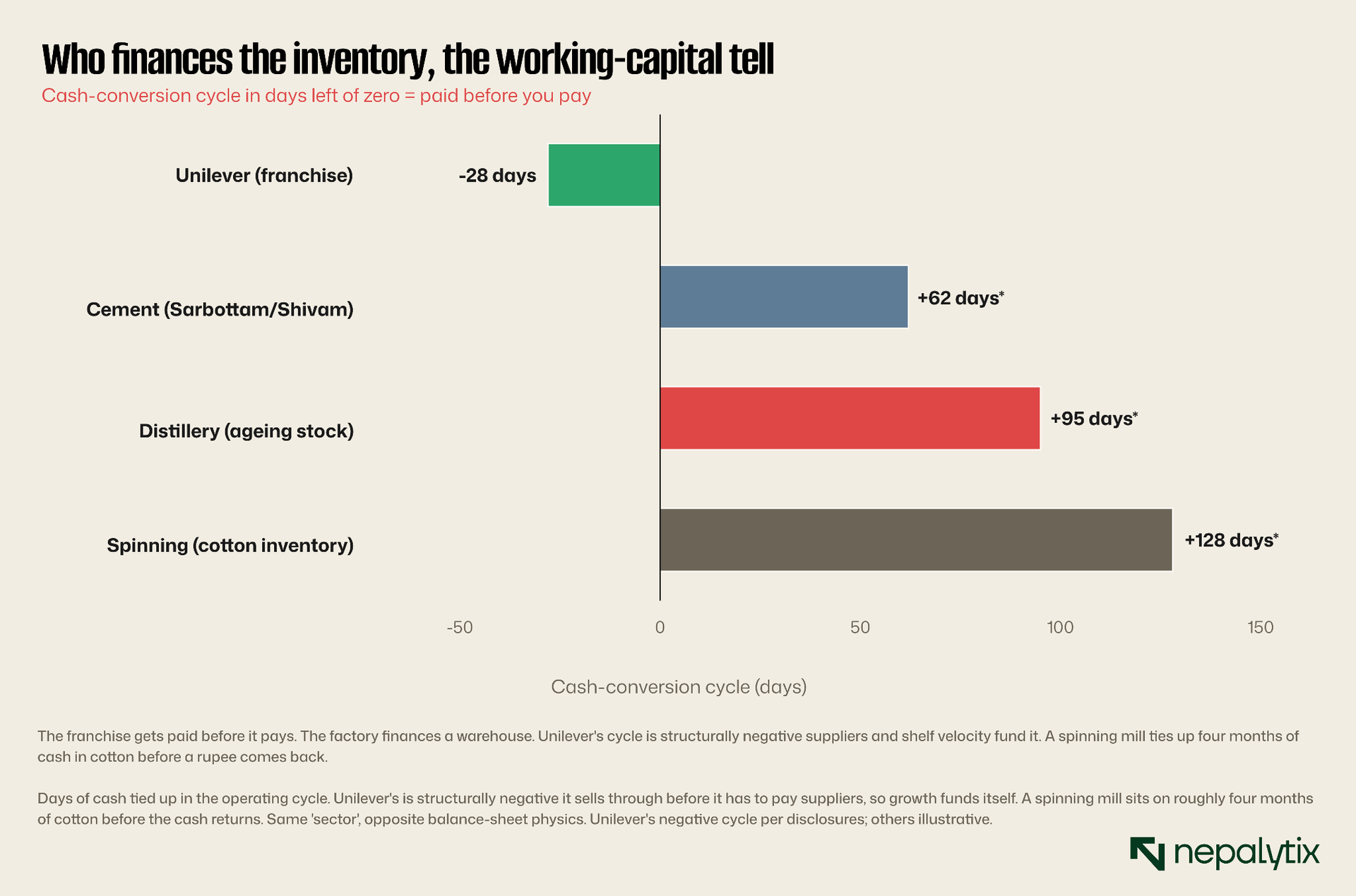

There is one more number that instantly separates a great manufacturer from a mediocre one and almost nobody looks at it: the cash-conversion cycle, how many days pass between paying for inputs and collecting from customers.

A great consumer franchise runs a negative cash-conversion cycle: shelf velocity and supplier terms mean the customer pays before the supplier does, and the business funds its own growth. Unilever's cycle is structurally negative, one of the quiet reasons it can be debt-free and still pay out most of its earnings. A cement plant or a spinning mill runs the opposite way: it finances a warehouse. Cotton, clinker, and finished stock sit for months tying up cash that has to be borrowed or retained. When you read a manufacturer's balance sheet, find the working-capital cycle. It tells you whether the customer funds the business or the business funds the customer.

The margin you don't control

Return to margin, because there is a layer beneath it the income statement never shows: who set the margin in the first place. For a Nepali manufacturer the answer is often the government not the company and a margin the state grants, the state can withdraw.

Cement is the clearest case. Nepal built itself from a net importer into a producer that now meets most of its own demand and even ships to India, on the back of abundant domestic limestone and value addition above 80 percent. But the economics rests on policy scaffolding. Producers are shielded by a customs duty of Rs 2,400 a tonne plus 13 percent VAT on imported clinker which props up the domestic price it reached around Rs 950 a bag once imports were squeezed. Exporters are dangling an 8 percent cash subsidy for cement made with Nepali raw materials. Strip those two supports out and the margins in the waterfall above look very different.

And the supports are unreliable. Exporters report waiting two years for subsidies they were promised. India periodically blocks Nepali cement at the border most recently by stalling the IS-mark certification products needed to sell there so the export margin hangs on a foreign regulator's goodwill. Meanwhile Nepal has built roughly 22 million tonnes of capacity against domestic demand of 8 to 9 million and that glut is a permanent thumb on price: when everyone can make more than the country can absorb, the biggest plants cut prices to keep their kilns full and squeeze the smaller grinders out. Even the state plants that sit directly on limestone Hetauda, Udayapur shut down repeatedly which tells you raw material was never the binding constraint. Management and money were.

So when you read a manufacturer ask where the margin comes from and how durable the source is. A distillery's profit is a function of the excise regime. A spinning mill is a function of cotton prices and duty protection. A cement maker's is a function of import duties, an export subsidy, an Indian certification stamp and a capacity cycle. None of it appears in the P/E and all of it decides whether the P/E means anything. A single line in the Jestha budget can reprice the entire sector before one plant changes a thing it does.

Put the lens on one company

Run the six moves on Shivam Cement and you get a reading in five minutes. Margin: about 12 percent net a commodity price-taker, not a franchise so do not expect Unilever economics. Float: 100 percent public so its Rs 612 is a real, contested price rather than a thin-float quotation unusually clean for this market. The rupee: cost of goods dominates, and its recent profit surge came from cost control on flat revenue, which says the operating leverage is real but the top line is not growing. Cycle: a trailing P/E in the low 40s looks rich, and against a sector two years past its peak you should be pricing mid-cycle earnings not last year's. Peers: it trades below Sarbottam on book while paying a smaller dividend which is the market asking a question about earnings quality you should answer before you buy. Working capital and policy: it finances its inventory like every cement maker and its margin ultimately leans on the same duties, subsidies, and demand cycle as the rest of the sector. None of that is a verdict. It is a reading which is the entire job of the six moves.

So how do you actually read one

Six moves and you can do them in the order they appeared here. Start with the margin because it tells you which of the three animals you are looking at, franchise, price-taker or exercise play. Check the float before you trust the price, because a five-figure quote on a locked-up register is theatre. Trace the rupee down the income statement because the cost-of-goods line is where a factory lives and a bank does not exist. Never value a cyclical on its trailing multiple; use mid-cycle earnings. Read the specific company against its listed peers because the sub-sector average hides the spread between a compounder and a loss-maker. And find the cash-conversion cycle because it silently tells you who is financing whom.

Now go back to Reliance Spinning at the top of the tape. A spinning mill outrunning the banks in a dead week is not a mystery once you have the lens. It is a thin-margin, long-cash-cycle, commodity price-taker whose stock moved on something as a result, a rumour, a squeeze on its slim float that has nothing to do with the banks it briefly out-traded. Whether that move is worth chasing is a different question. But you can now ask it properly, which is the entire point. The bank lens would have left you staring at a number you could not explain. The factory lens lets you read the machine.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.