How to read a Mutual Fund

Nepali investors obsess over NAV, discounts, and dividends. They're often looking at the wrong numbers. The real question is much simpler: what does the fund actually own? Once you answer that, most of the industry starts to look very different.

A mutual fund is the only instrument on NEPSE that tells you in public, every day, exactly what it is worth. It publishes a number the net asset value that is computed from the market price of everything it owns. No other listed security offers you that. When you buy a bank you are guessing at the value of its loan book. When you buy a hydropower company, you are guessing at hydrology and a tariff. When you buy a fund, the value is disclosed.

And yet mutual funds are the most misunderstood thing retail investors in Nepal own. They are bought at issue because Rs 10 "feels cheap." They are held without anyone ever opening the portfolio to see what is inside. They are judged on the dividend they pay, which is not a return at all. And they are treated as diversification when, in a market this concentrated, most of them own almost exactly the same stocks as each other and as you.

This is a guide to reading one properly. Not to argue about whether funds trade below their NAV that argument is settled and we made it at length in a separate long read. This is the layer underneath: what a fund actually is, what its numbers actually mean and the four or five things to check before you put money into one.

The structure decides everything

Before you look at a single number, establish what kind of fund you are looking at because there are two and they behave nothing alike.

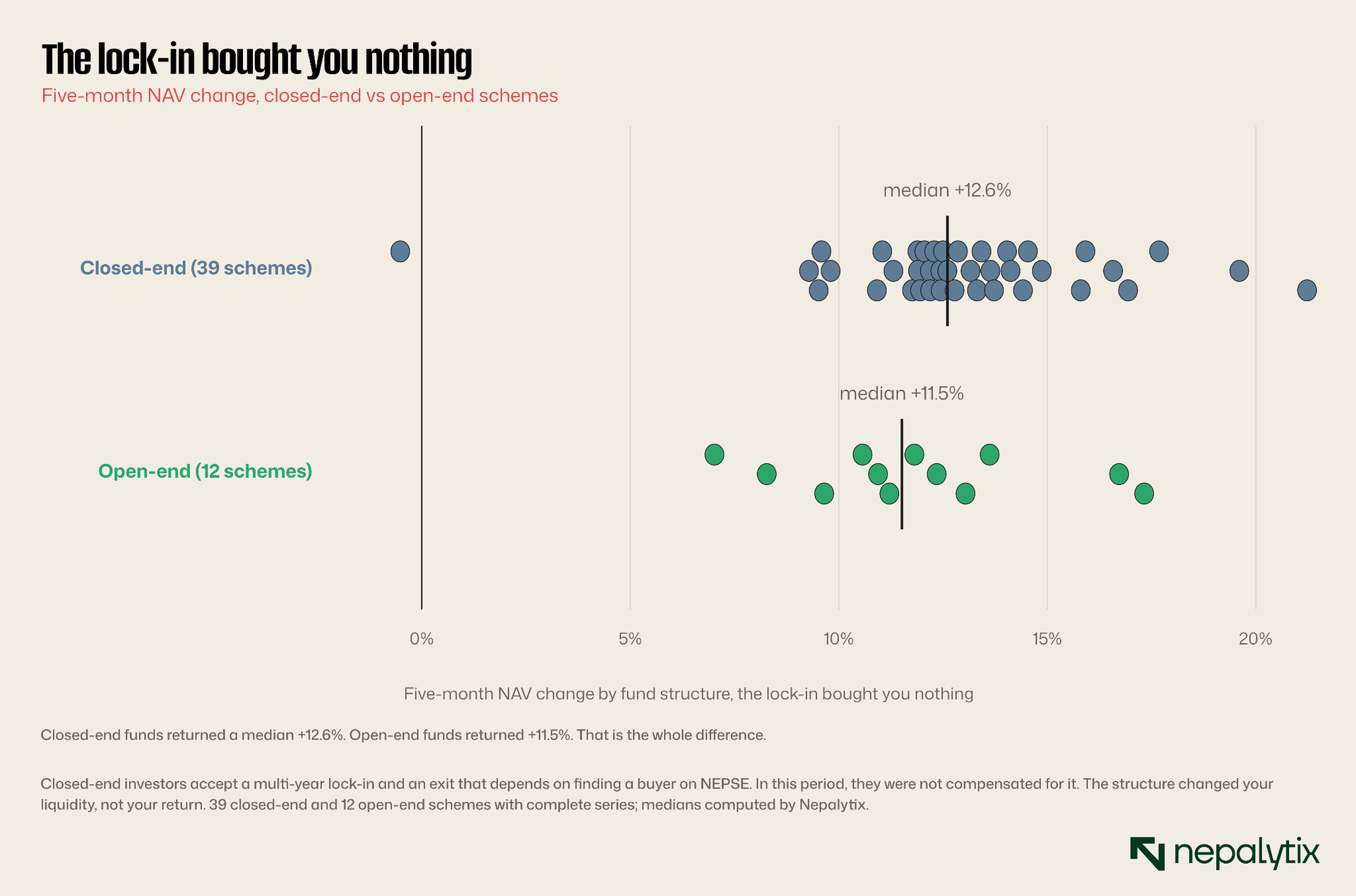

A closed-end fund raises a fixed pot of money once issues a fixed number of units and then closes. It has a maturity date typically five to ten years out and on that date it sells everything it owns and pays unit holders their share of the NAV. Between launch and maturity, you cannot redeem. Your money is in. The units are listed on NEPSE so the only way out is to find another buyer on the exchange at whatever price the market is offering that day.

An open-end fund is the opposite. It has no fixed size and no maturity. It issues new units to anyone who wants them and buys them back from anyone who wants out at NAV on demand. It does not list on NEPSE because it does not need to; the fund itself is your counterparty. You can invest a fixed amount every month which is impossible in a closed-end scheme.That single fork determines your entry, your exit, whether you can run a monthly plan and what price you transact at. Forty-eight of the sixty-five registered schemes are closed-end which means most Nepali investors are without quite realising it, holding a locked instrument they must sell to a stranger to escape.

What NAV actually is and what it is not

NAV is arithmetic, not opinion. Take the market value of everything the fund owns its shares, bonds, cash, dividends it is owed. Subtract everything it owes management fees, expenses payable. Divide by the number of units outstanding. That is NAV per unit.

Two consequences follow and both matter.

The first: NAV is a scorecard, not a valuation. It tells you what the fund's holdings are worth right now. It does not tell you whether they are good holdings or whether the manager is skilled or whether the price you are being asked to pay is sensible. A fund whose NAV has fallen from Rs 10 to Rs 9 has lost money. That is all NAV says. Why it lost money, bad stock picking, or a falling market that dragged everything down is a question NAV cannot answer.

The second and this is the one that traps people: the Rs 10 par value is not a price. Every Nepali scheme launches at a par of Rs 10 per unit and that number feels official, fair, fixed. It is none of those things. On the day a fund launches it owns nothing but the cash you just gave it. NAV is Rs 10 because Rs 10 is what you handed over. You have not bought a portfolio at a bargain; you have bought your own money back and hired someone to invest it. Whether that was a good idea depends entirely on what they do next.

Par value is not cheap. On day one, a fund is just a pile of your cash with a fee attached.

Open the bonnet: this is the step everyone skips

Here is the number that matters more than NAV more than the dividend, more than the manager's name: what does the fund actually own?

Every equity-oriented scheme in Nepal must, by SEBON rule, hold at least 70% of its assets in listed securities. That sounds like a prudent diversification requirement. Look at what it means in a market like NEPSE and it becomes something else entirely. Nepal's exchange has a few hundred listed companies, but liquidity is savagely concentrated in a small handful of large commercial banks and a few blue chips account for the overwhelming majority of what actually trades. A fund manager with a hundred crore to deploy cannot meaningfully buy the illiquid tail. They have to buy what is liquid enough to buy.

So they all buy the same things.

And we can prove it, rather than assert it.

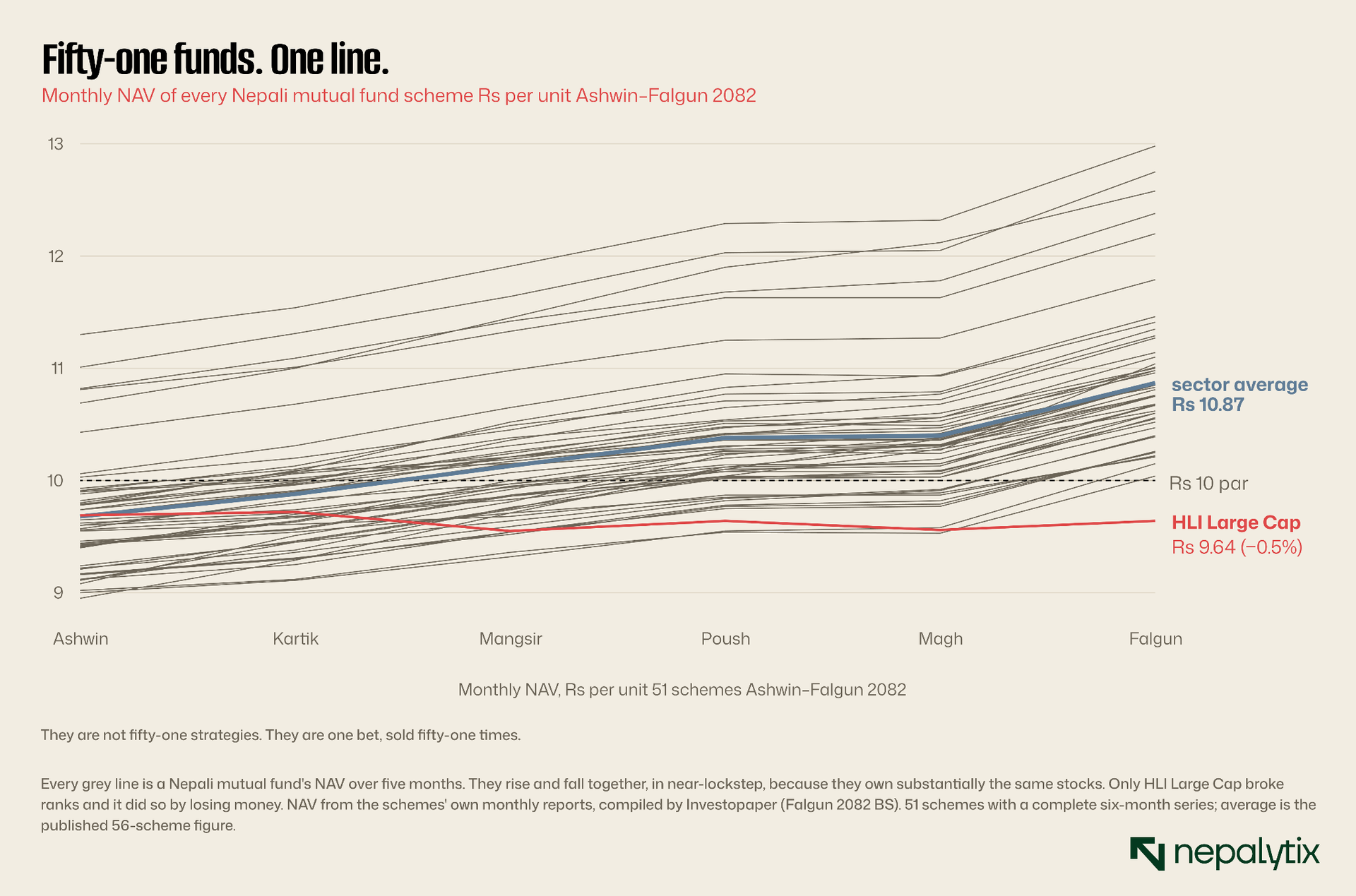

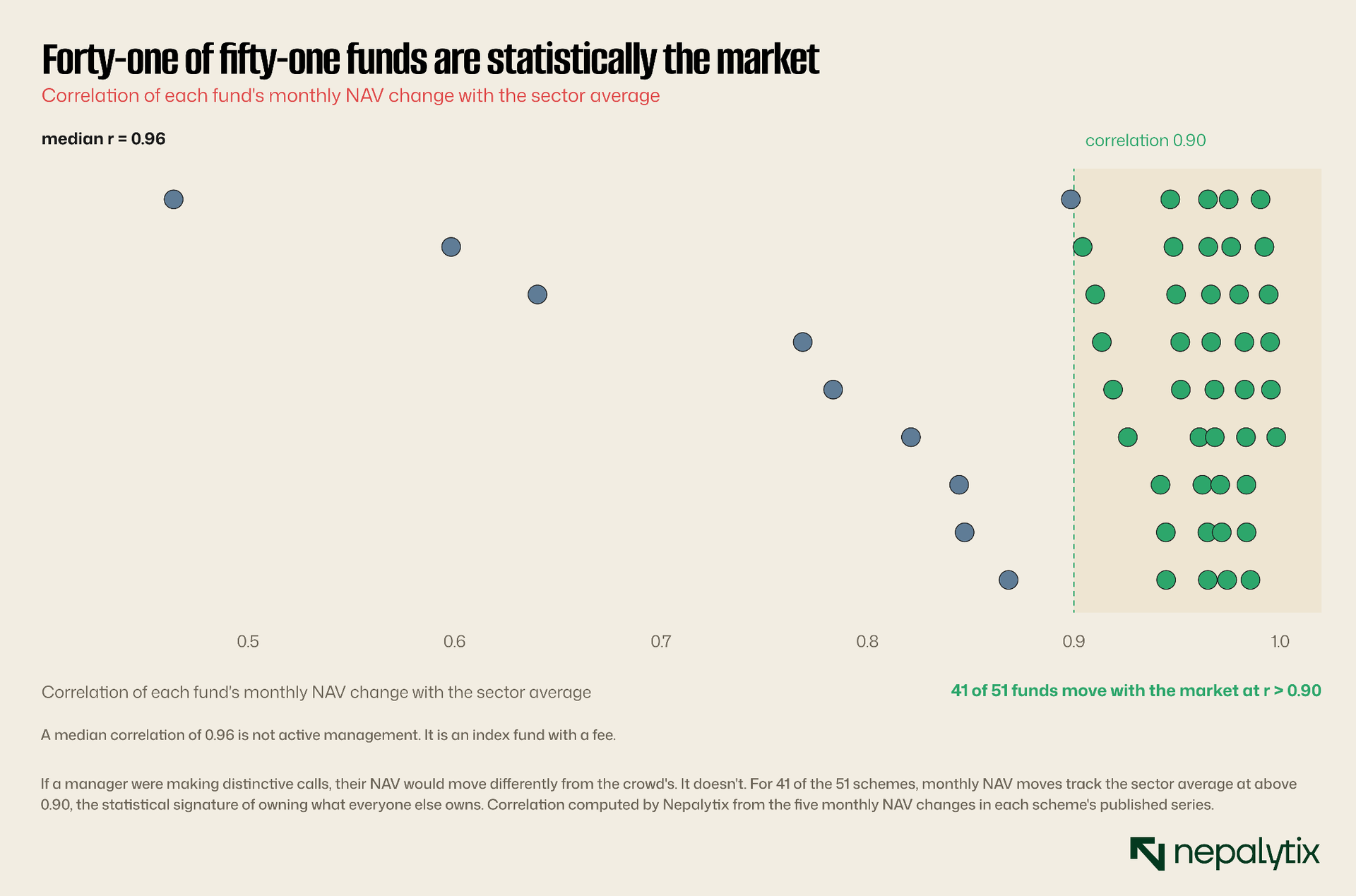

Take the published monthly NAV of every scheme in the country over the last five months and compute a simple statistic: how closely does each fund's NAV move with the sector average? If a manager is making distinctive calls overweighting one sector, avoiding another, holding cash when others don't, their NAV should wander away from the pack. If they are all holding the same names, their NAVs will move in lockstep.

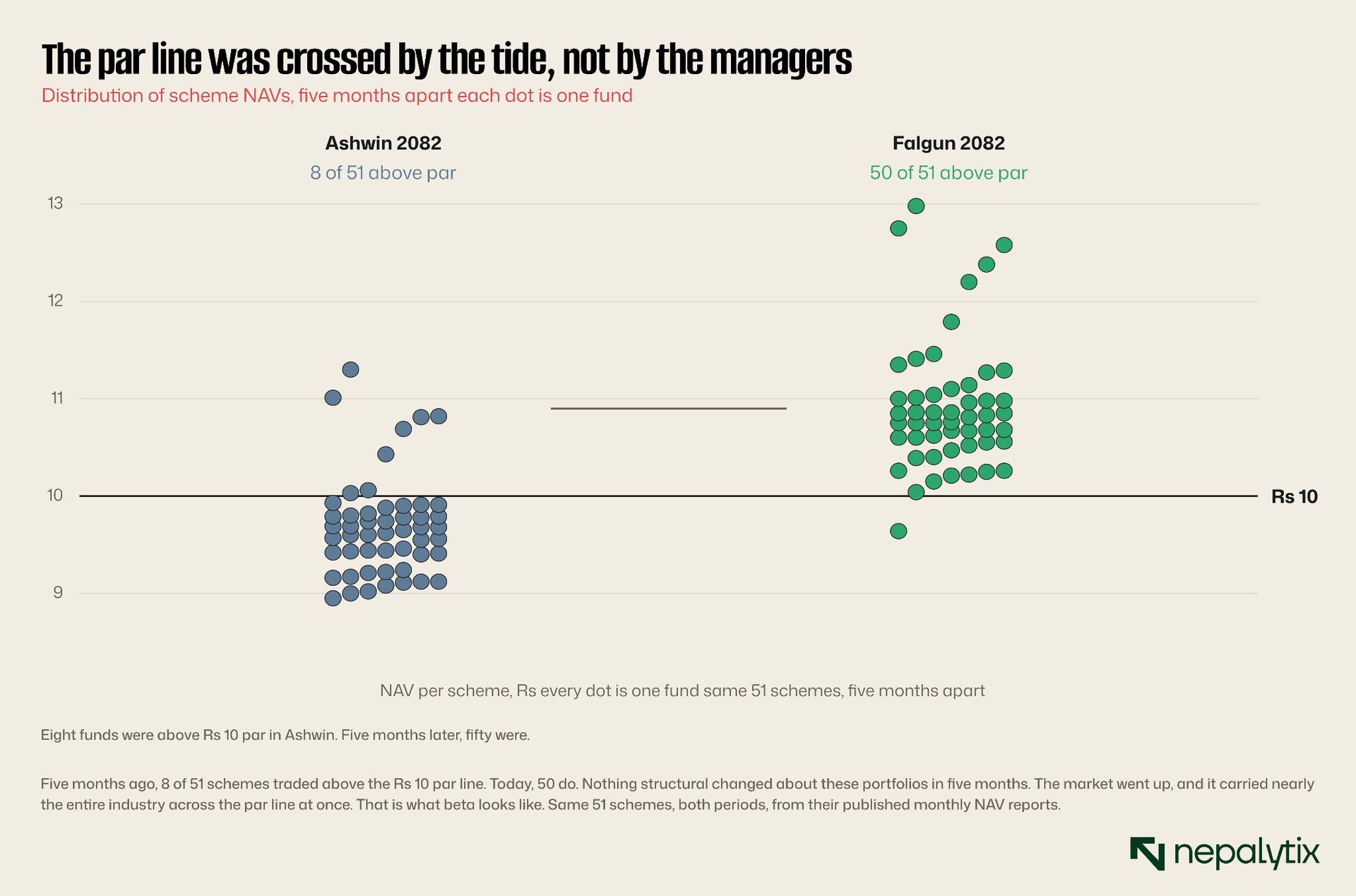

The median correlation across the industry is 0.96. Forty-one of the fifty-one schemes sit above 0.90.

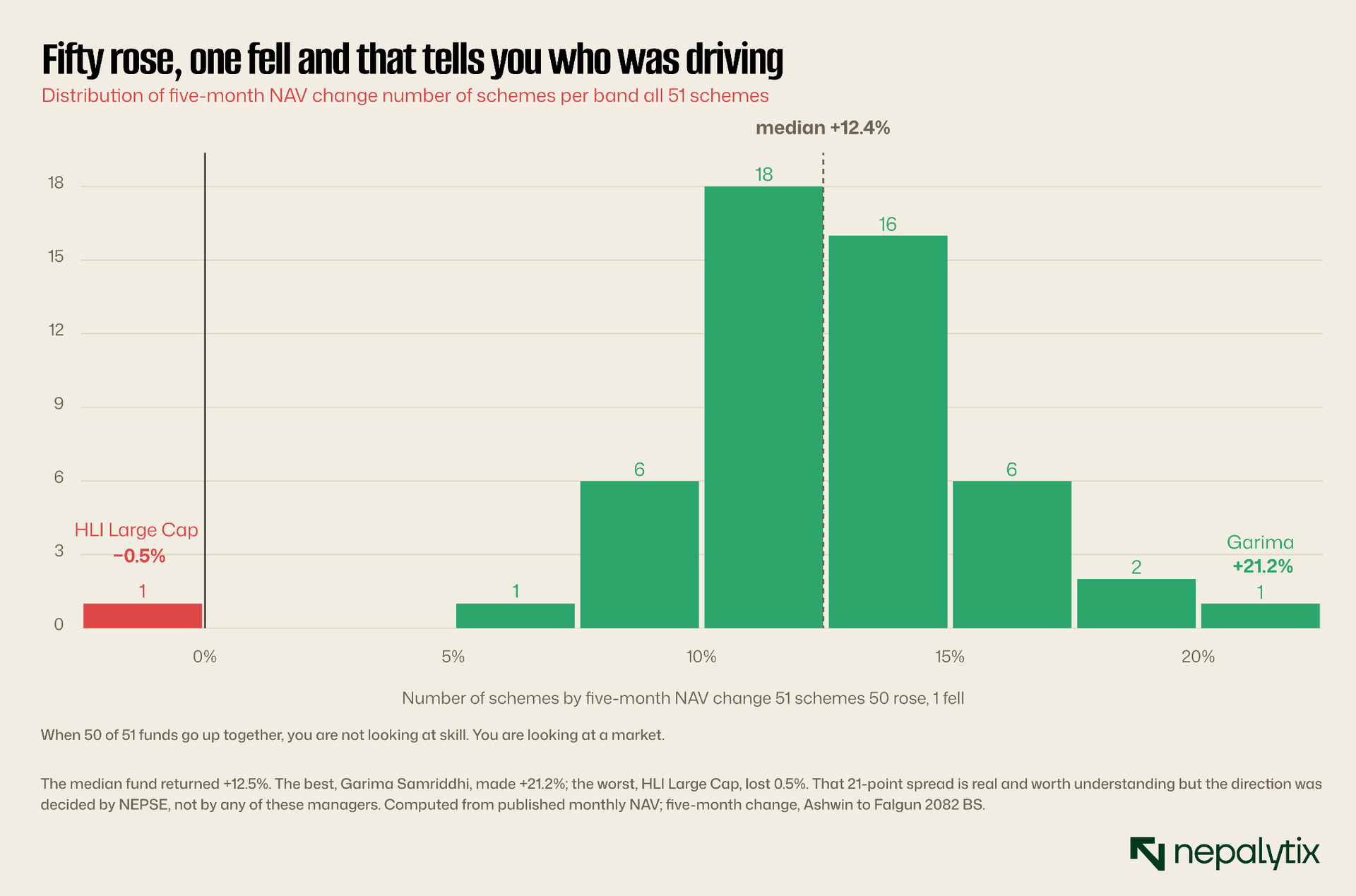

That number is the whole argument. A correlation of 0.96 with the average is not active management; it is an index fund, sold with an active management fee. And the return data says the same thing from the other direction: over those five months, 50 of the 51 schemes went up. Not most. Not the good ones. Fifty out of fifty-one, in near-unison. The only fund that fell, HLI Large Cap, lost half a percent.

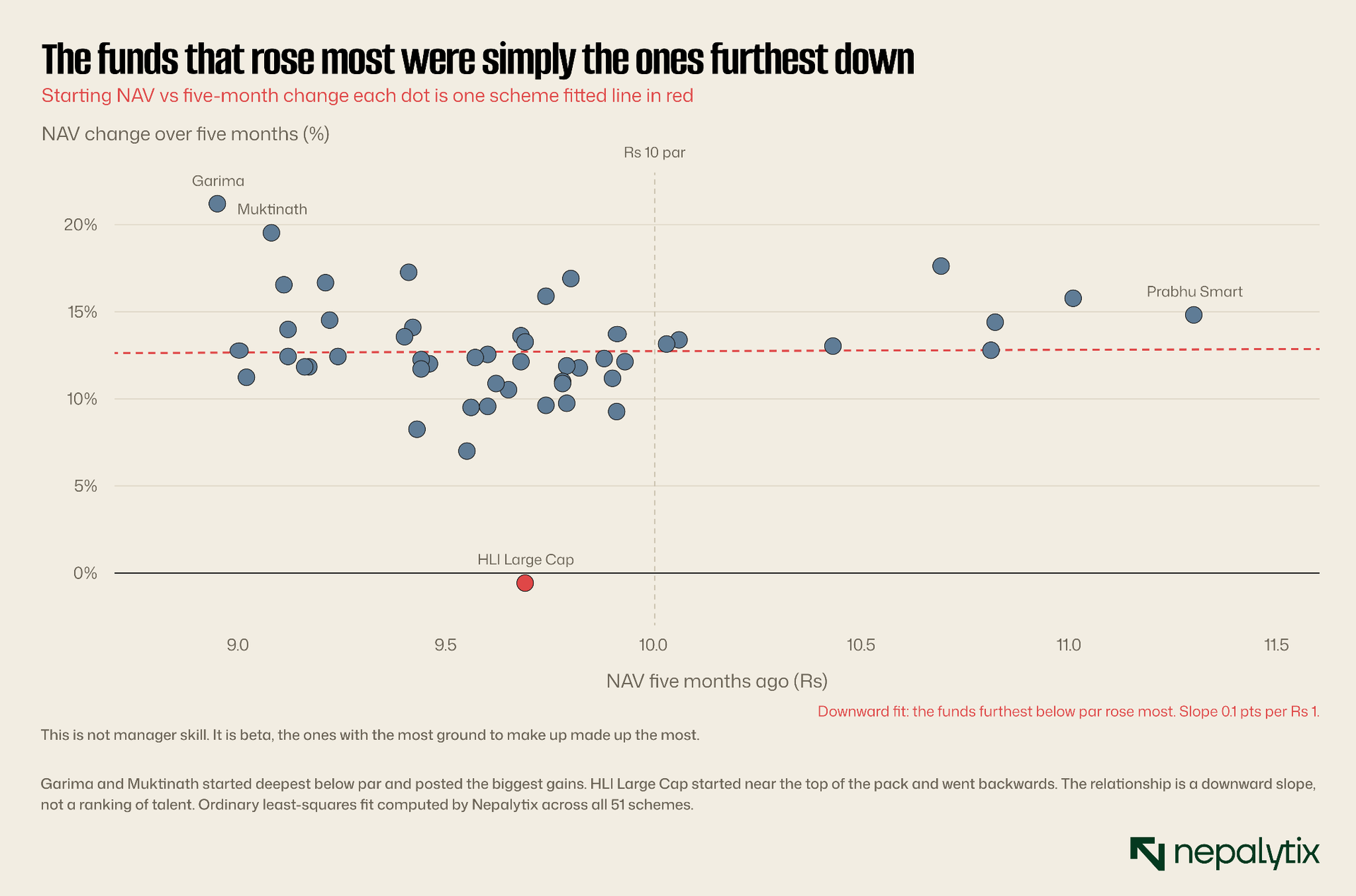

There is real dispersion there and it is worth respecting: the best fund, Garima Samriddhi, returned +21.2%, and the worst was flat. Twenty-one points is not nothing. But look at where that dispersion came from before you credit anyone with genius.

Plot each fund's starting NAV against what it earned and the picture resolves into something uncomfortable: the funds that gained the most were simply the ones that had fallen the furthest. Garima and Muktinath began the period deepest below par, at Rs 8.95 and Rs 9.08, and posted the biggest recoveries. The fitted line slopes down. That is not a ranking of skill. It is beta, the mechanical bounce of the most beaten-down portfolios in a rising market.

The final piece of evidence is the par line itself. Five months ago, 8 of the 51 schemes had an NAV above Rs 10. Today, 50 do.

Nothing about these portfolios changed in five months. No manager suddenly learned to pick stocks. NEPSE went up and it carried the entire industry across the par line together, like boats on a tide.

You are very likely not buying diversification. You are buying NEPSE with a management fee attached.

The practical consequence is the same as before but now it rests on evidence rather than intuition: before you buy any fund, download its portfolio disclosure and read the top ten holdings. Compare that list against what you already own directly. If your personal portfolio is Nabil, NIMB and NTC, and the fund's top holdings are Nabil, NIMB and NTC, you have not spread your risk, you have concentrated it and paid someone to do it.

The funds worth paying for are the ones whose portfolio you could not have assembled yourself and whose NAV therefore does not move in lockstep with the average. On this data, they are rare. Go looking for them, and be honest about how few you find.

There is a fair counter-argument and it deserves stating. For an investor with a small amount to deploy someone who cannot buy meaningful positions in fifteen companies without brokerage eating them alive, a fund does provide real breadth they could not otherwise afford. That is a genuine service. But it is a service for the investor who owns nothing else. The moment you already hold the same large banks directly, the fund stops adding breadth and starts adding duplication.

The fee is real, it compounds and it does not care how you did

A fund charges a management fee, plus expenses. It is deducted from the fund's assets which means it is already inside the NAV you see. You never write a cheque for it; it simply reduces your NAV, quietly, every year, forever.

Two properties of the fee are worth sitting with. First, it is charged on assets under management not on gains. In a year the fund is down 12%, the manager is still paid. That is the deal and it is not scandalous running a fund costs money whether markets cooperate or not but it means the manager's incentive is to gather assets and yours is to earn returns and those are not the same incentive.

Second, it compounds against you. Over a seven-year closed-end life, a fee that looks trivial in any single year quietly removes a meaningful slice of your terminal wealth. Which brings the previous section into sharp focus: if the fund is holding the same ten stocks you could have bought yourself on TMS then the fee is the entire product. You are paying an annual charge for a portfolio you did not need help constructing.

So find the expense ratio. It is in the factsheet. Divide the return you expect by what you are being charged for it and ask whether the manager is being paid for skill or for showing up.

A dividend is not a return

This one costs Nepali investors real money every year and it is the easiest to fix.

When a fund distributes a cash dividend, it is not generating new wealth. It is handing you back a piece of the fund's own assets and NAV falls by exactly that amount on the day of distribution. A fund with an NAV of Rs 11 that pays a Rs 1 dividend has an NAV of Rs 10 the next morning. You have Rs 1 in your account and Rs 10 in the fund and you are precisely where you were minus the 5% withholding tax on the distribution.

Chasing the fund with the biggest dividend is therefore not a strategy. It is a preference about the timing and tax treatment of money that is already yours. The only true measure of a fund's performance is the change in NAV, plus dividends paid, over the period you held it. That total, not the headline payout, is what the manager actually earned you. Compute it, and compare it to what NEPSE did over the same window. If the fund lagged the index, you paid a fee to underperform a market you could have bought for nothing.

Total return = change in NAV, plus dividends. Anything else is a distraction dressed up as a yield.

Do it with real numbers once and it sticks. Suppose you bought units of a closed-end scheme two years ago at Rs 9.20 on the exchange. Today the NAV is Rs 9.60 and over those two years the fund paid you dividends totalling Rs 1.10 per unit. Your gross gain is the Rs 0.40 of NAV appreciation plus the Rs 1.10 distributed Rs 1.50 on an outlay of Rs 9.20, or roughly 16% over two years, before tax. Notice what that calculation does not use: the par value, which is irrelevant to you; and the headline dividend percentage, which tells you nothing until you divide it by what you actually paid.

Then subtract the tax because it is not trivial. Distributions to individuals are subject to a 5% withholding at source (15% for institutions) deducted before the money reaches you. And if you sell your units on NEPSE rather than holding to maturity, the gain is taxed like a listed share. Neither rate will ruin the trade but both belong in the arithmetic and neither appears anywhere in the marketing material.

Know the expiry date

If you hold a closed-end fund, you own something with a life span and where you are in that life span changes the entire proposition.

At maturity, the fund liquidates its holdings and pays out NAV. That is the contract, and it is the one moment the market price and the true value must meet. A fund with one year left is a fundamentally different instrument from a fund with eight years left even though both trade on the same board and look identical on the ticker. In the first, the reckoning is close. In the second you are agreeing to be locked in for most of a decade, exposed to a manager you cannot fire, in a market you cannot exit except by finding someone else to take your place.

So before you buy: find the maturity date. Then ask yourself, honestly, whether you are prepared to hold for that long because if the answer is no, the exchange is the only door, and it does not always open at a price you like.

Check whether the manager has skin in the game

One more thing and it changed recently in a way most investors have not registered.

The fund manager and sponsor are required to put their own money into the scheme alongside your "seed capital." For years the rule was a straightforward 15% of the scheme's size, which is a meaningful alignment: if the fund does badly, the manager bleeds with you. In early 2026, SEBON relaxed it. A manager that meets certain experience and performance criteria may now post as little as 10%, or even 5%, with 15% remaining the default only for those who do not qualify.

Read that carefully, because it cuts both ways. The managers permitted to post less are, by construction, the ones with a track record so a low seed is partly a badge of experience. But it also means the manager of a fund you are considering may now have a third as much of their own money at risk as they would have had two years ago. It is not a scandal. It is a fact worth knowing, and it belongs on your checklist next to the fee and the portfolio.

The order of operations

Put it together and the sequence to follow is short and it is not the sequence most people use.

First, the structure. Do you need to be able to redeem on a date you choose, or to invest a fixed sum monthly? Then you need an open-end fund, and the closed-end universe 48 of the 65 schemes is simply not for you however good the manager. Get this wrong and nothing downstream fixes it.

Second, the holdings. Pull the portfolio disclosure. Read the top ten. If it is the same ten large banks you already own, you are not buying diversification and you should either look elsewhere or accept that you are buying the market with a fee attached.

Third, the cost. Find the expense ratio. Ask what you are getting for it. If the answer is "a portfolio I could have built on TMS in an afternoon," the answer is no.

Fourth, the record is measured properly. Not the dividend. Change in NAV plus distributions, over years against what NEPSE did in the same window. A manager who lagged the index over a full cycle is not managing your money; they are storing it, at a charge.

Fifth and only if it is closed-end, the clock and the price. How many years to maturity, and what discount to NAV is the market offering you today? That last question is a long story in itself, and we have told it separately but note that it is the last question, not the first. The discount is only a bargain if the thing being discounted is worth owning.

Which is the whole lesson, really. A mutual fund is not a magic diversifier and it is not a savings account with a better rate. It is a portfolio of Nepali listed companies chosen by someone else that you rent for a fee and usually cannot leave when you like. Judge it as exactly that. Open the bonnet and look at what is inside before you ever look at the price. Almost nobody does, which is precisely why it is worth doing.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.