Long Read: Mutual Funds Trade Below Their Own Value

Nepal's closed-end mutual funds consistently trade well below their net asset value (NAV), allowing investors to buy a diversified portfolio of blue-chip stocks at a significant discount.

On the Nepal Stock Exchange you can buy a professionally managed basket of the country's blue chips for around 80 paisa on the rupee and have done so for years. The gap between what these funds own and what they sell for is one of the most stubborn anomalies in Nepali finance. It is also a near-perfect X-ray of an asset-management industry that took in the money and never quite earned the trust.

Somewhere in a brokerage account in Kathmandu sits a small puzzle that ought not to exist. A unit of a Nepali closed-end mutual fund, a fund that holds nothing but shares of Nabil, of NIC Asia, of the hydropower and insurance names every investor in the country knows can be bought today for meaningfully less than the value of those very shares. The fund's own managers publish the number every month: this is what a unit is worth, they say, this is the net asset value. And every trading day the market replies, in effect, no it is not and marks the unit down by a tenth, a fifth, sometimes more than a quarter.

This is not a fire sale or a moment of panic. It is the ordinary, settled state of affairs. Of the roughly forty closed-end mutual funds listed on the Nepal Stock Exchange almost every one trades below the value of the assets it holds and many have done so for the better part of their existence. An investor with the patience to hold could, on paper, buy a rupee of diversified, professionally selected Nepali equity for around eighty paisa, wait for the fund to mature and collect the difference. Almost nobody does.

That gap, between price and value, between what a fund owns and what its units fetch is the subject of this piece. It is a small anomaly in absolute terms; the entire mutual fund industry in Nepal manages only around twenty billion rupees, a rounding error against the banking system. But it is a revealing one. The persistence of the discount, through bull markets and bear, says something uncomfortable about how Nepal's young asset-management industry is built, who runs it,and why the people it was meant to serve do not quite believe in it. The discount is the industry's report card, and it has been failing for a while.

The puzzle has a respectable pedigree which makes Nepal's version no less striking. Closed-end funds trade at discounts in rich markets too; the phenomenon is well enough known to have a name in the finance literature, the closed-end fund puzzle, and economists have argued about its causes for decades. But the discounts in deep markets are usually modest, a few percent, kept in check by arbitrageurs and the occasional activist who forces a fund to buy back units or convert. Nepal's discounts are an order of magnitude larger and far more durable because the forces that discipline them elsewhere, liquidity, arbitrage capital, activist pressure are largely absent. The puzzle is universal; the scale is local.

Start with the scale of it.

What you are actually buying

To see why the discount is strange you have to understand what a closed-end mutual fund is because the structure is the whole story. When one of these funds launches, it sells a fixed number of units to the public usually at a par value of ten rupees each, and raises a fixed pool of money. It then invests that money, mostly in listed Nepali shares under a manager's discretion. The number of units never changes. The fund has a fixed lifespan, typically seven to ten years, at the end of which it is wound up: the holdings are sold and the proceeds are handed back to unit holders in proportion to what they own.

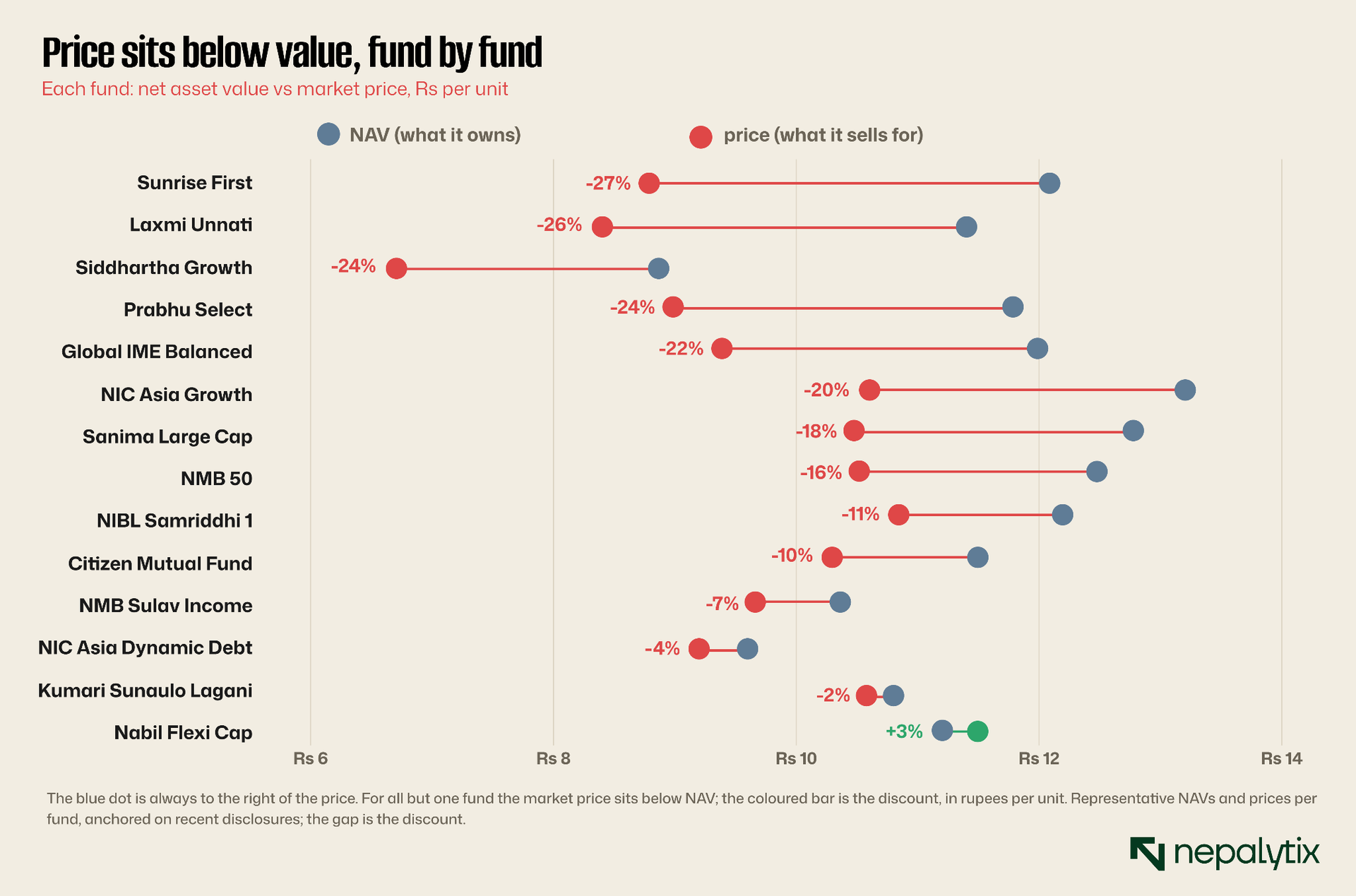

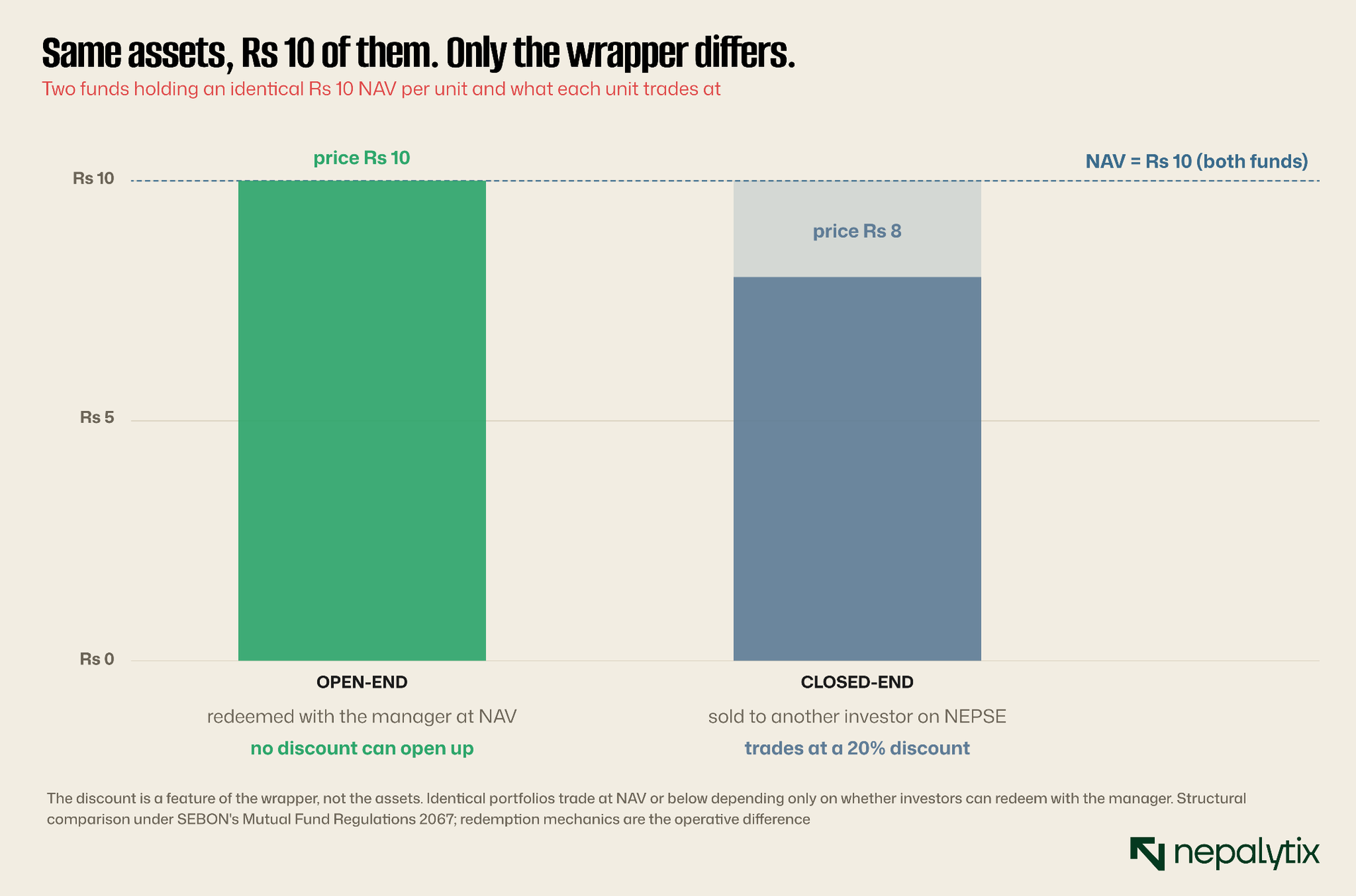

Two numbers describe such a fund at any moment. The first is its net asset value, or NAV: the market value of everything the fund holds, divided by the number of units, published monthly by the manager. If a fund's shares are worth a billion rupees and it has issued a hundred million units, the NAV is ten rupees a unit. The second number is the market price: what a unit actually changes hands for on the NEPSE, where the units are listed and traded like any share. In a rational world these two numbers would be close because a unit is simply a claim on the underlying assets and the assets have a known value.

They are not close. The market price is set, like any share price, by supply and demand among investors and in Nepal that price has settled persistently below the NAV the managers report. The difference, expressed as a percentage, is the discount. A unit with a NAV of ten rupees trading at eight is at a twenty percent discount. The fund owns ten rupees of stock per unit; the market will pay eight.

There is an important contrast lurking here, and it is worth drawing early because it frames everything that follows. Nepal's other kind of mutual fund, the open-end fund, does not have this problem at all. An open-end fund is not listed on the exchange; instead, investors buy and sell units directly with the manager, who creates new units for buyers and redeems units from sellers, always at the prevailing NAV. Because you can always redeem at NAV, the price simply is the NAV. No discount can open up because the moment one tried to, an investor would redeem rather than sell cheap. The discount, in other words, is not a feature of the assets. It is a feature of the closed-end wrapper and that distinction is the key to the entire puzzle.

One practical note before moving on, because it matters for how investors read these funds. The NAV is not a market quote; it is calculated by the manager, typically once a month, by valuing the fund's holdings at their market prices, subtracting liabilities and accrued fees and dividing by the number of units. It is as close to an objective measure of what a unit is worth as exists. The market price, by contrast, updates continuously as units change hands. So when a fund reports a NAV of twelve rupees and its units trade at ten, the twelve is the considered monthly judgement of the people who manage the assets and the ten is the live verdict of the people who trade them. The discount is the daily argument between the two.

A short history of the discount

The discount has a history and it begins with an exception. For more than a decade, Nepal's only open-end mutual fund was the Citizen Unit Scheme run by the state-owned Citizen Investment Trust. It was a quiet, conservative vehicle, popular with government employees paying a steady dividend of around eight percent and offering a buyback facility that let holders exit near fair value. Because it was open-end, it never traded at a discount; there was nothing to trade it against. For years it was effectively the whole industry and it worked.

The modern industry, the one with the discount problem, was created by regulation. The Mutual Fund Regulations of 2067, issued in 2010 and the supplementary guidelines of 2012 built the legal scaffolding for a new kind of fund: closed-end schemes, sponsored by commercial banks, managed by their merchant-banking subsidiaries and listed on the NEPSE. The framework was sensible on its face. It required a fund sponsor, a fund manager and an independent fund supervisor, imposed investment limits, and mandated that equity-oriented funds keep at least seventy percent of their assets in listed securities. It was designed to be safe and in the narrow sense of protecting investors from outright fraud, it largely has been.

What it was not designed to prevent was the discount, because the discount is a property of the listed, closed-end structure the regulations encouraged. Through the 2010s and into the 2020s, bank after bank launched closed-end funds, each sold to the public at the ritual par value of ten rupees a unit, each promising professional management and diversification, each listing on the exchange a few weeks later. The IPOs were popular, often heavily oversubscribed, because Nepali retail investors will buy almost any new listing at par. And then, almost without exception, the units would drift below NAV in the secondary market and stay there.

So the discount was not a bug that crept in. It was built into the industry's founding design, the predictable consequence of choosing a closed-end, exchange-listed structure in a thin market with no arbitrage capital. The one fund type that never had the problem, the open-end scheme, was for years the road not taken and only recently have the capital companies begun to return to it. The history in other words, is of an industry that solved a problem it did not really have, accessibility and created one it did, the discount and then spent a decade growing on top of it.

The par-value ritual deserves a moment, because it quietly shapes everything. Every closed-end fund launches at ten rupees a unit, a round number with no analytical meaning, and Nepali investors have been trained by the IPO market to treat ten rupees as the natural price of a new thing. When the unit later trades at eight, the investor's reference point is not the NAV, which he may never have computed but the ten rupees he paid against which eight is simply a loss. The par convention plants the seed of the discount's misreading at the moment of issue. A fund that launched at, and was always discussed in terms of, its NAV might be understood very differently. The number on the IPO form does more harm than anyone intends.

The arbitrage that looks free

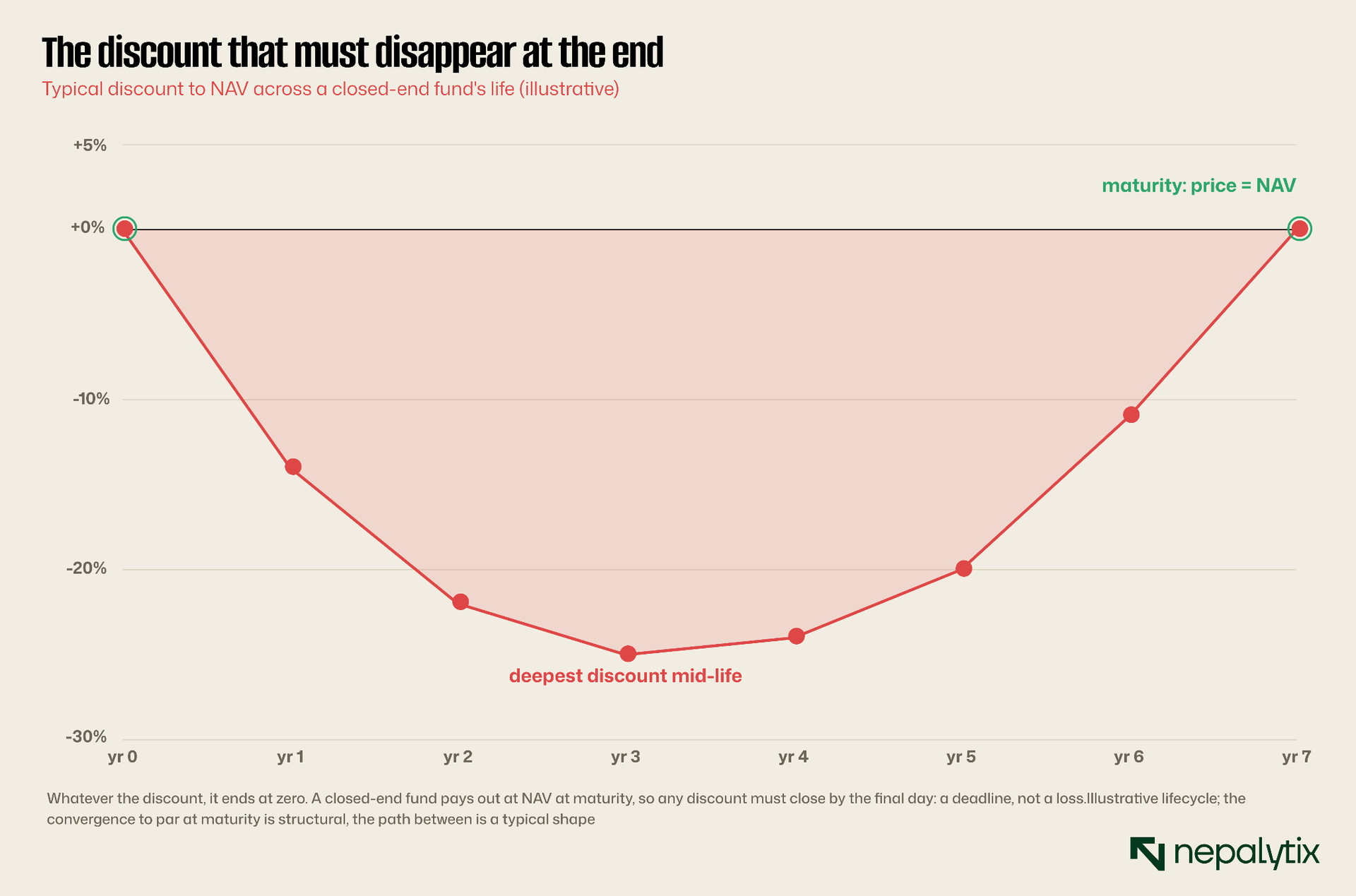

Here is what makes the discount genuinely odd, as opposed to merely unfortunate. A closed-end fund is not a permanent vehicle. It has a maturity date and on that date it is liquidated and pays out at NAV. Which means the discount is not a permanent feature an investor must live with. It is a temporary gap with a hard deadline. Whatever the discount on the day you buy, it must, by the structure of the thing, close to zero by the day the fund winds up.

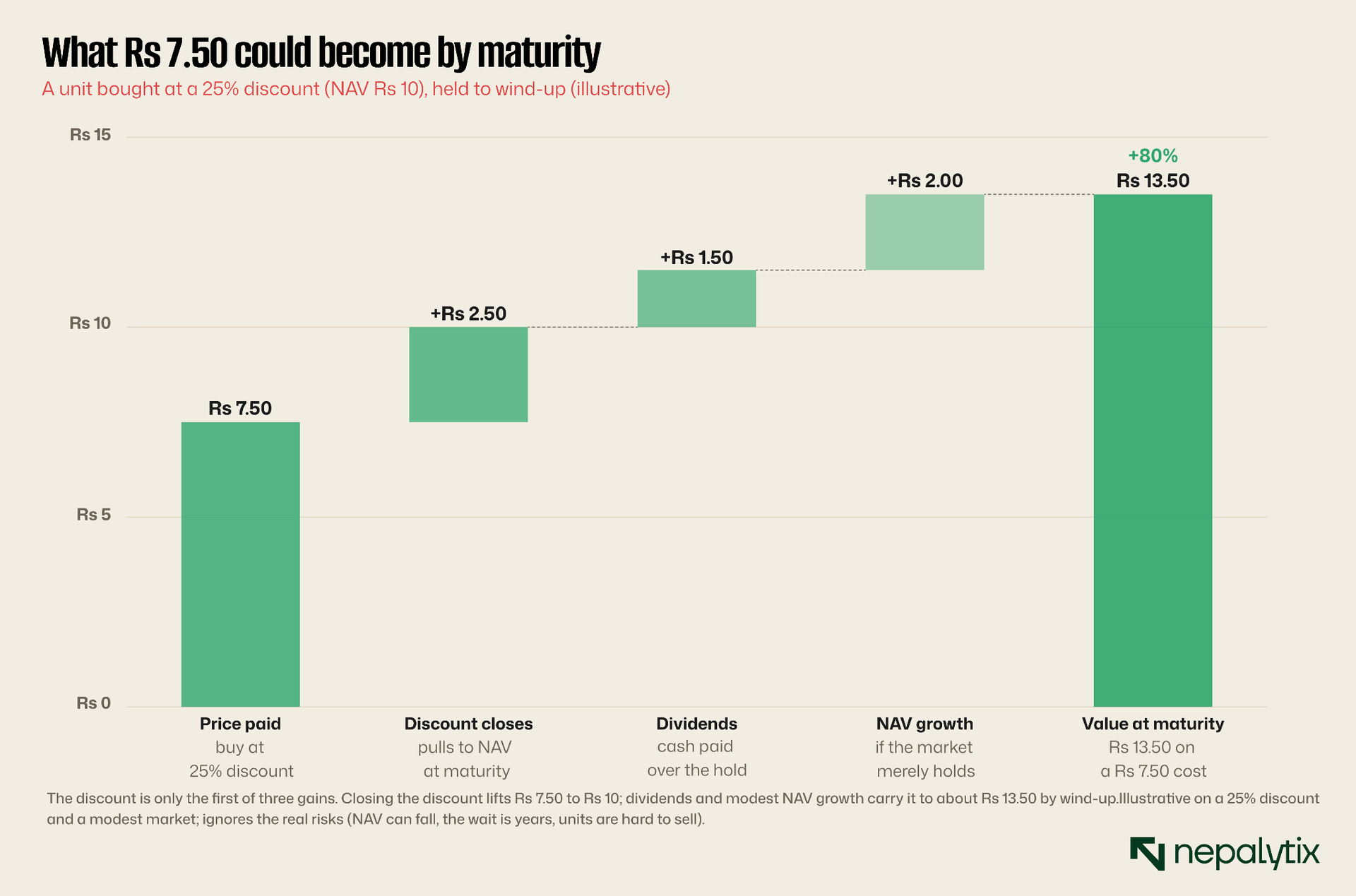

Follow the arithmetic, because it is striking. Suppose you buy a unit at a twenty-five percent discount: NAV ten rupees, price seven and a half. If you simply hold to maturity and the fund liquidates at NAV, your seven and a half rupees becomes ten, a gain of one third, purely from the discount closing. That is before anything else happens. Along the way, the fund pays cash dividends out of its income, which on a unit bought cheap represents a high yield on your actual cost. And if the underlying NAV itself grows because the Nepali market rises even modestly over the years you hold, you capture that too, on top of the discount you have already pocketed.

Stack those together and the numbers look almost embarrassing. The discount closing, the dividends collected and a few years of modest NAV growth can compound into a return of seventy percent or more by maturity on an investment whose chief risk, on this telling, is that you have to be patient. This is the kind of opportunity that, in a deep and sophisticated market, would not survive a week. Arbitrageurs would buy the discounted units, the buying would push the price up toward NAV and the gap would close. The fact that it has not closed, year after year, is the real mystery. A market that leaves seventy percent on the table is telling you something about itself.

The dividend leg of the return deserves a closer look because it is the part retail investors most often miss. A fund pays cash dividends out of the income its holdings generate, per unit, on the NAV basis not on the discounted price you paid. So if you buy a unit at seven and a half rupees and the fund pays a dividend worth, say, eight percent of its ten-rupee NAV, you are earning that eight percent on assets that cost you only seven and a half. Your yield on actual cost is higher than the headline, and it accrues every year you hold, separately from whether the discount ever closes. For a patient holder, the dividends alone can repay a meaningful slice of the discounted purchase price over the life of the fund.

The lifecycle chart shows the deadline at work: whatever the discount in the middle years, it is pulled back to zero as maturity approaches because the payout at NAV is a certainty written into the fund's deed. The closer a fund gets to winding up, the narrower its discount tends to be precisely because the arbitrage becomes harder to ignore as the clock runs down. Which raises the obvious question. If the money is so plainly there, why does almost nobody reach for it?

The money stays on the table

The answer is that the arbitrage is free only on paper and the gap between paper and practice is exactly where Nepal's market reveals itself. Several real frictions stand between the investor and that seventy percent and together they explain why the discount survives.

The first is that the NAV is not a floor. The arithmetic above assumes the fund's assets at least hold their value but a closed-end fund in Nepal is overwhelmingly invested in Nepali equities and the Nepali market is volatile and has spent five years below its 2021 peak. If the NAV falls, the discount you bought can close not because the price rose to meet the NAV but because the NAV fell to meet the price. You can be perfectly right about the discount and still lose money, because the thing you are discounting is itself sinking. For a retail investor, that is not an arbitrage. It is a leveraged bet on a flat market with extra steps.

The second friction is time and it is underrated. The discount only reliably closes at maturity and maturity can be years away. A twenty-five percent discount that closes in one year is a wonderful return; the same discount that closes in seven years is a pedestrian one, easily beaten by a fixed deposit once you account for the risk. The longer the wait, the more the annualised return shrinks and the more can go wrong. Money locked in a discounted fund for half a decade is money not compounding elsewhere and Nepali investors, with bank deposits and the lure of the next IPO in front of them, are not a patient constituency.

The third friction is the one that does the most quiet damage: liquidity, or the lack of it. These funds barely trade. A serious investor who wanted to put real money to work buying discounted units would struggle to do so without pushing the price up against themselves and would struggle even more to get out if they changed their mind. The thin float that helps cause the discount also prevents the arbitrage that would close it. There is no pool of patient arbitrage capital in Nepal standing ready to buy mispriced units at scale because the market is too shallow to absorb it. The discount persists not because investors are foolish but because the trade that would erase it is, in practice, very hard to execute.

Underneath all three frictions sits a deeper absence: Nepal has almost no institutional arbitrage capital. In a developed market, the job of closing discounts falls to hedge funds, value funds and activist investors who exist precisely to find mispricings, buy them at scale, and if necessary agitate for the fund to be wound up or converted. Nepal has none of this in size. The investor base is overwhelmingly retail, the few institutions are banks and insurers with their own mandates and there is no pool of professional, patient, opportunistic money whose business is to hunt anomalies like this one. The discount is not closed because there is, quite literally, almost no one in the market whose job it is to close it.

The discount is not a mispricing waiting to be corrected. It is a verdict, renewed every trading day, on the wrapper the industry chose to sell.

A tale of two investors

To feel why the discount persists, picture the two investors who meet across it. The first is a patient, NAV-aware value investor, the kind the textbook says should exist. She sees a fund trading at a twenty-five percent discount, calculates the pull to par, judges the manager competent and the maturity not too distant and buys, intending to hold to the end. She is doing exactly what an efficient market is supposed to reward, and on a long enough horizon she probably will be rewarded.

The second is the typical retail participant and there are vastly more of him. He came to the market in the IPO boom, opened a demat account to flip new listings for a quick premium and thinks in days and weeks, not years. To him a mutual fund unit trading below its issue price of ten rupees is simply a loser, a position in the red, something to avoid or to sell, not a discounted claim on real assets. He does not compute NAV. He sees a falling price and reads it as a falling value, which for him it effectively is because he will never hold to the maturity at which the distinction would pay off.

The market price is set at the margin by whoever is most active, and in Nepal that is overwhelmingly the second investor. There are simply not enough of the first with enough capital and enough patience to move the price toward NAV against the weight of the second. So the discount the value investor sees as an opportunity is the same discount the retail flipper creates by avoiding it. The two are looking at the identical number and seeing opposite things and the one who sees it wrong is the one who sets the price. That, in a sentence, is why the eighty-paisa rupee stays eighty paisa.

It would be easy, and a little unfair, to blame the retail investor for this. He is behaving rationally given what he knows and the horizon he can afford. The failure is upstream: an industry that never taught its buyers what NAV means, a regulator that never required the discount to be shown plainly and a market structure that gave the impatient majority no reason to think beyond the next listing. The retail investor's misreading of the discount is not the cause of the problem so much as its most visible symptom.

What the market is really discounting

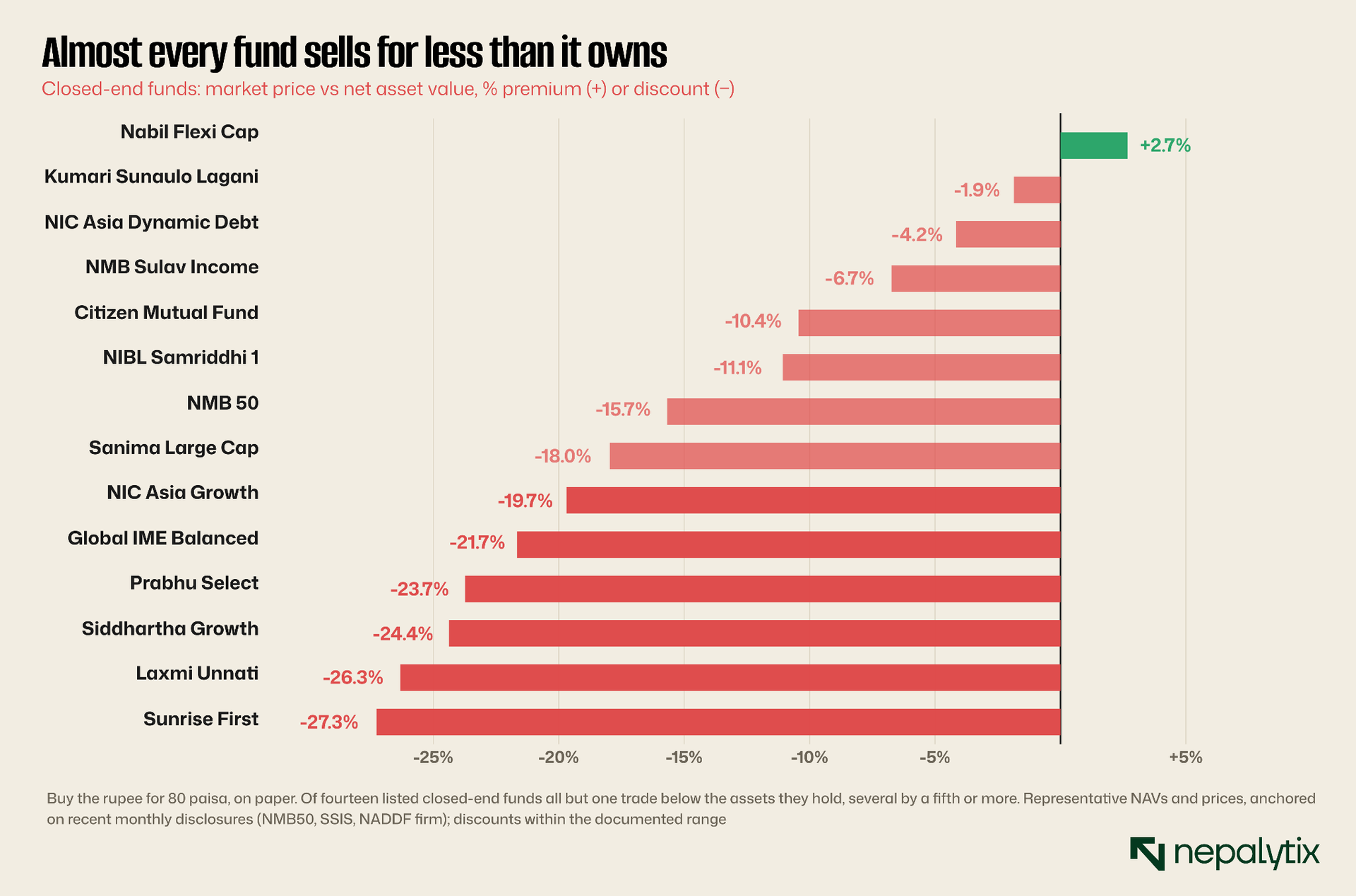

If the frictions explain why the discount is not arbitraged away, they do not fully explain why some funds trade at a few percent below NAV while others languish at thirty. For that you have to look at what the deepest-discounted funds have in common and the pattern is instructive.

The funds that trade closest to, or even above, their NAV tend to be the ones with a track record of actually beating the market: a Nabil Flexi Cap or a Kumari fund whose managers have, over time, generated returns good enough that investors trust the next rupee they manage. Trust, here, is literal. When investors believe a manager will keep compounding their money, they will pay close to NAV or occasionally a premium, for the privilege of staying invested. The discount narrows toward zero as confidence rises.

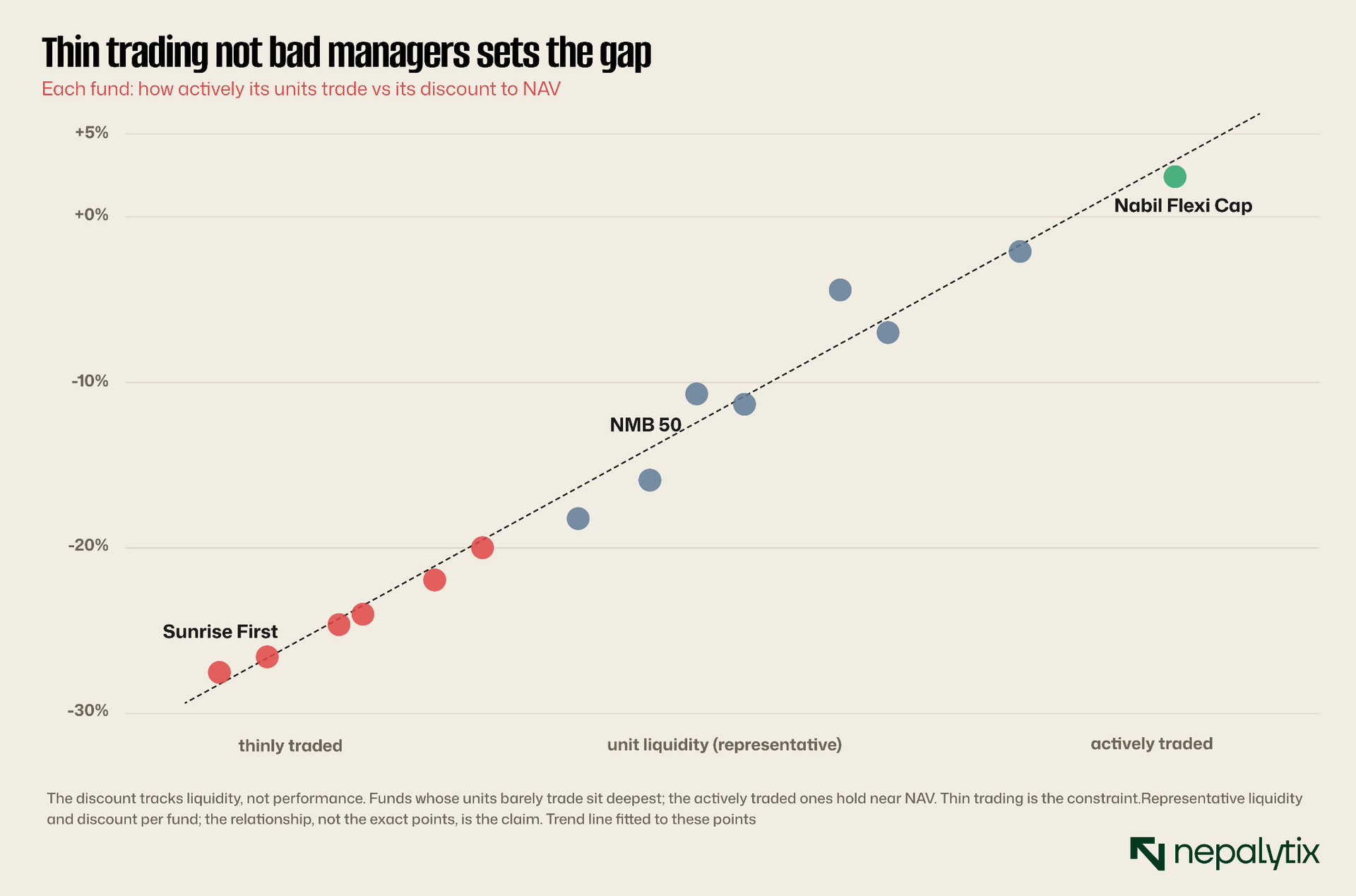

The funds at the bottom of the table share the opposite traits. They are heavily weighted toward equities which makes their NAV swing violently with the market and frightens off the very long-term holders who might otherwise close the discount. They have years left to run so the maturity backstop is distant. And they trade thinly so the discount has no natural corrective. The scatter makes the strongest of these relationships visible: plot each fund's discount against how actively its units trade and the pattern is hard to miss, the thinly traded funds sitting at the deepest discounts while the actively traded ones hold near NAV. The single strongest force pulling a fund toward fair value is simply whether its units trade enough for the market to price them properly. Where they do not, the discount festers.

This is worth dwelling on because it reframes the discount. It is not a uniform tax on all closed-end funds. It is a market verdict, fund by fund on manager quality, portfolio risk and tradability and the funds it punishes most harshly are the illiquid, equity-heavy, long-dated ones run by managers investors do not yet trust. The discount, read this way, is doing a job. It is just doing it to an industry that would rather it did not.

The funds that escape the discount are worth studying precisely because they prove it is escapable. A Nabil Flexi Cap at a small premium, a Kumari fund near par, are not exceptions to some iron law; they are demonstrations that when a manager earns enough trust and runs a portfolio investors are willing to hold, the gap closes on its own with no buyback, no regulation, no arbitrage required. That is the encouraging half of the message buried in the discount. The gap is not a curse laid on the asset class. It is a deficit of trust, and trust can be earned. The funds at the top of the ladder earned it; most of the industry has not.

The industry that grew anyway

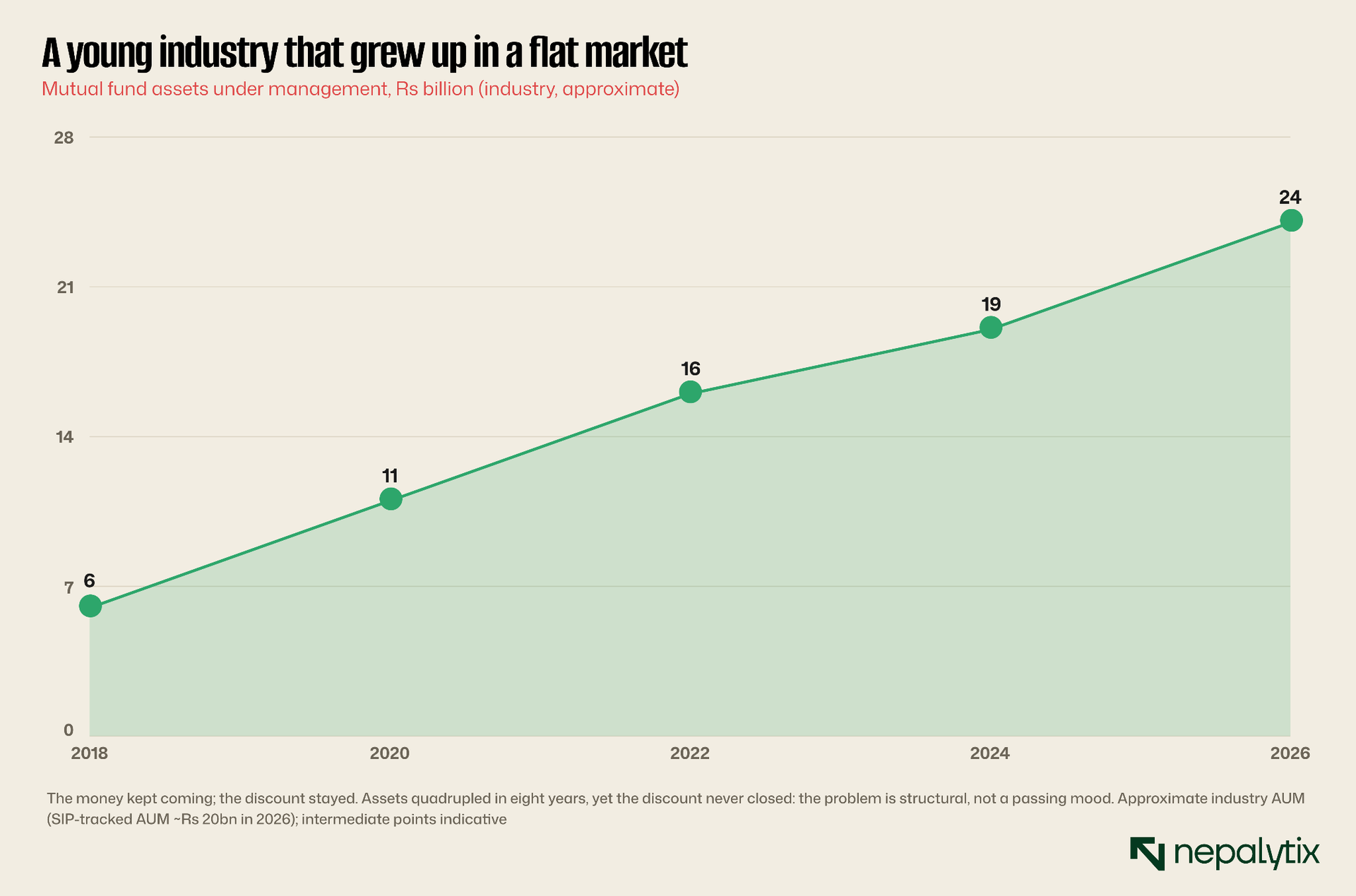

You might expect an instrument that persistently disappoints its buyers to wither. The striking thing about Nepal's mutual fund industry is that it did the opposite. It grew and quickly, right through the years the discount refused to close.

From a standing start little more than a decade ago, the industry now counts more than fifty tracked funds, around forty of them closed-end managing something on the order of twenty billion rupees between them. The trajectory has been steadily upward: more funds, more units, more assets, a new launch every few months as another bank's capital subsidiary brings another closed-end scheme to market. Measured by money raised, the industry is a success story, a genuine broadening of how Nepalis can access the stock market without picking individual shares.

And yet the discount never closed. That combination, rising assets and a persistent discount is the most telling fact in the whole story because it rules out the easy explanation. If the discount were just a passing mood, a temporary bout of pessimism, it would have lifted as money flooded in and the market recovered from its 2022 lows. It did not. The funds kept launching, the assets kept growing and the units kept trading below NAV. A problem that survives a quadrupling of the industry around it is not a mood. It is structural, baked into the design of the product and the behaviour of the people who buy and sell it.

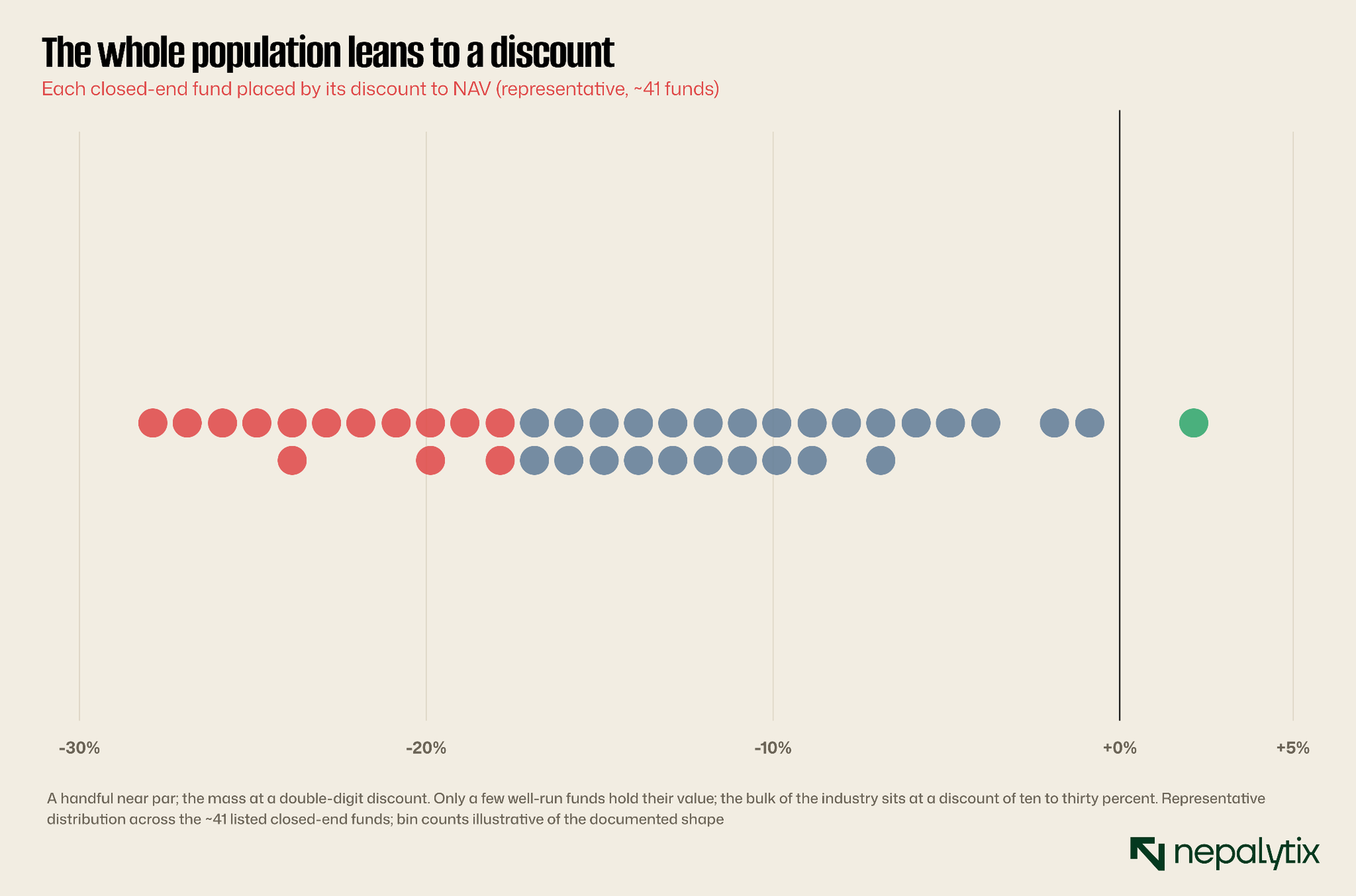

The distribution of discounts across the industry makes the point visually. This is not a handful of troubled funds dragging down an otherwise healthy average. The whole population leans to one side. A small cluster of well-run funds sits near par, and then the mass of the industry stretches out across a discount of ten, fifteen, twenty, thirty percent. The typical Nepali closed-end fund is not a borderline case. It is a discounted one, and the industry's growth was built on top of that fact rather than in spite of it.

There is a worrying circularity in this. The industry grows by launching new closed-end funds, each sold at par to retail investors who do not fully understand what they are buying. Those funds then drift to a discount confirming the next cohort's suspicion that mutual funds are a way to lose money slowly. And yet the IPOs keep selling, because the par-value launch resets the cycle before the discount can teach its lesson. The primary market, where units are sold at ten rupees, and the secondary market, where they settle below it, are almost two different products wearing the same name. Growth is measured in the first; credibility in the second; and the two have moved in opposite directions.

Who runs the money and why it matters

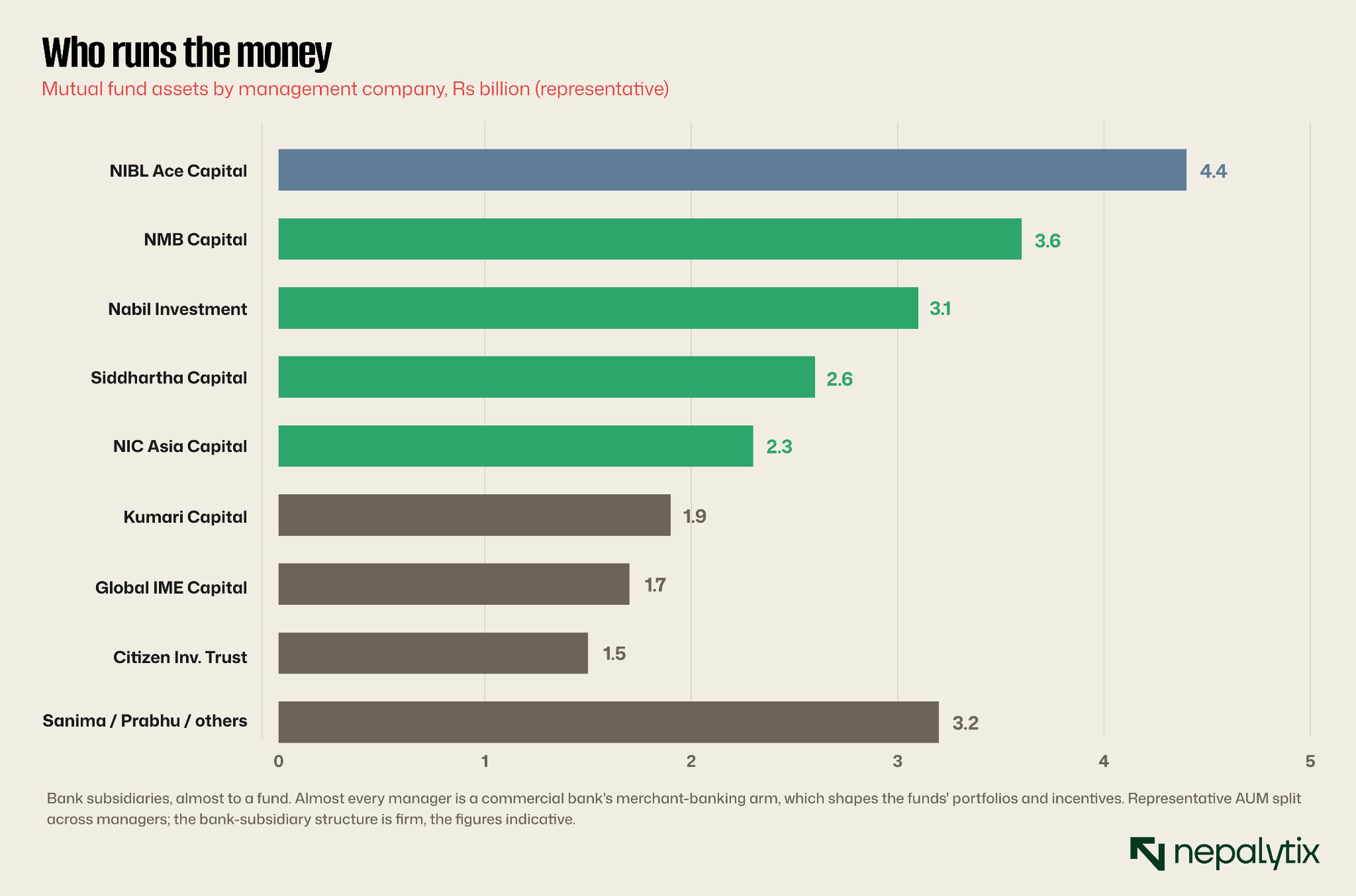

To understand why the product is built the way it is, look at who builds it. Almost every mutual fund in Nepal is run not by an independent asset manager but by the merchant-banking subsidiary of a commercial bank. NIBL Ace Capital belongs to Nepal Investment Bank. NMB Capital to NMB. Nabil Investment to Nabil. NIC Asia Capital, Siddhartha Capital, Kumari Capital, Global IME Capital, Sanima, Prabhu: the league table of fund managers reads, almost line for line, as a league table of the banks that own them.

This matters for incentives in ways that are easy to miss. A bank's capital subsidiary is not, in the main, in the business of maximising returns for fund unit holders. It is in the business of generating fee income for the bank and of giving the bank's customers another product to be sold. The fund manager earns an annual fee of up to one and a half percent of net asset value and a fund supervisor takes another fifth of a percent on top. So the management complex collects on the order of one and three-quarter percent of assets every year, regardless of whether the fund beats the market or trails it. The fee is charged on NAV not on the discounted market price the investor actually paid which means the investor pays a full freight management fee on assets the market values at a discount.

Stack that fee against the performance and the discount starts to look less mysterious. An industry whose managers are rewarded for gathering assets rather than for closing the gap to NAV has little reason to do the things that would close it: buy back units when they trade cheap, return capital aggressively or convert closed-end funds to open-end ones that would trade at NAV by construction. Each of those would shrink the asset base the fee is charged on. The structure that produces the discount is, not coincidentally, the structure that pays the people who could fix it. That is not a conspiracy. It is just incentives doing what incentives do, in an industry young enough that nobody has yet been forced to choose the investor over the fee.

It also shapes the portfolios. Bank-owned managers, staffed and supervised by bankers tend toward the same crowded trades: the big banks, the established hydropower names, the blue chips everyone already owns. The funds are diversified in the narrow sense of holding many shares, but concentrated in the broader sense of all holding the same shares, the ones their parent institutions know best. That concentration is part of why their NAVs move so tightly with the index which feeds the volatility that feeds the discount.

There is a conflict of interest in the structure that deserves naming. A fund run by a bank's subsidiary often holds among its largest positions, the shares of other banks. The manager selecting those positions is an employee of an institution with its own relationships, its own listed stock and its own view of which names should be supported. None of this need be corrupt to be distorting. It is enough that the people choosing the fund's investments are embedded in the banking system whose shares dominate the market which tilts the funds toward the same familiar names and away from the independent, contrarian positioning that might generate the outperformance that would close their discounts.

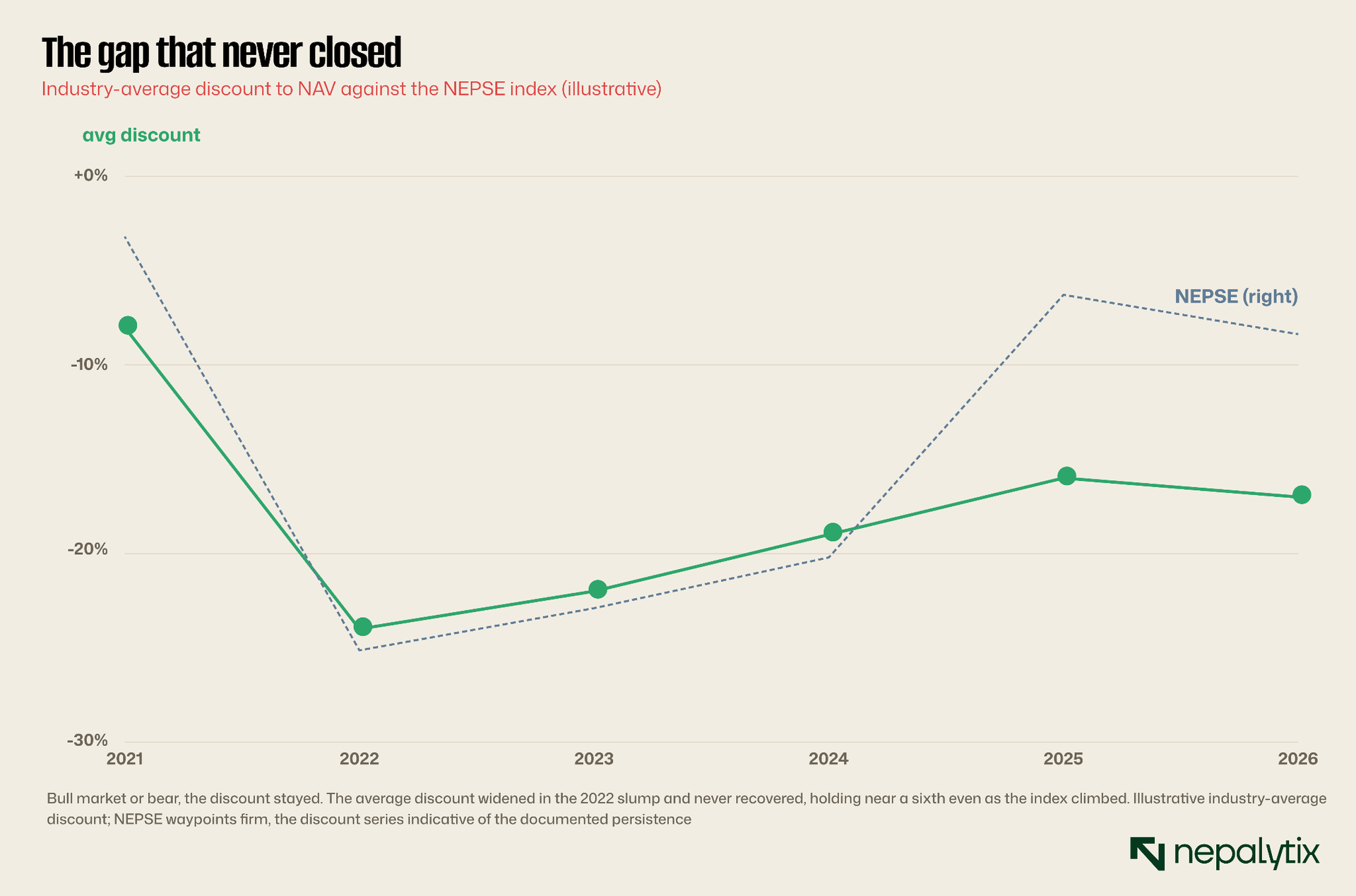

Bull market or bear, the gap held

It is worth confronting the most obvious objection to everything above: maybe the discount is just what happens in a bad market and a good one would fix it. The evidence says otherwise and the evidence is the most damning part of the case.

The Nepali market has not been uniformly grim over the life of these funds. It crashed in 2022, recovered through 2024 and 2025 and touched three thousand on the index again before settling back. If the discount were simply a function of market sentiment, it would have breathed with that cycle widening in the slump and closing in the recovery. Instead it widened in the 2022 crash as you would expect and then stayed wide. The average discount across the industry never returned to where it had been before the crash even as the index climbed back toward its old highs and new money poured into the funds.

That persistence through a market recovery is the clinching evidence that the discount is structural rather than sentimental. A discount that survives good news is not waiting for better news to close it. It is held open by the mechanics we have walked through: the illiquidity, the fee drag, the absence of arbitrage capital, the misalignment between managers and unit holders and the simple fact that retail investors who dominate this market often do not understand what NAV means or why a unit trading below it might be cheap. You cannot arbitrage a gap that most participants cannot see.

Retail misunderstanding deserves its own mention because it is both a cause and a symptom. Surveys and the behaviour of the market both suggest that many Nepali mutual fund buyers do not distinguish sharply between a fund's NAV and its market price, do not grasp that a discount represents value and treat the units as just another speculative chip in the IPO-and-flip culture that defines much of the retail market. A fund trading at a discount to such a buyer is not a bargain. It is a loser, to be avoided which depresses demand further and deepens the very discount that ought to attract them. The discount is sustained, in part, by the financial illiteracy it ought to reward.

The wrapper is the flaw

All of which points to a structural fix that the industry has been slow to embrace even though it sits in plain sight and Nepal already has working examples of it. The fix is to stop selling closed-end funds and start selling open-end ones.

Recall the contrast from the beginning. An open-end fund redeems units with the manager at NAV so its price is the NAV, and no discount can ever open up. The same portfolio of Nepali shares, wrapped in an open-end structure instead of a closed-end one, would trade at fair value automatically. The discount is not a property of the assets or even of the managers. It is a property of the closed-end wrapper, and the proof is that the identical assets in an open-end fund do not suffer from it. Nepal's open-end funds from the long-running Citizen Unit Scheme that served government employees for years to the newer systematic investment schemes the capital companies have begun to launch, simply do not trade at discounts because there is nothing to trade against NAV.

So why does the industry keep launching closed-end funds? Because the closed-end structure is better for the manager and worse for the investor which is the same misalignment in a different guise. A closed-end fund gives the manager a fixed pool of money locked up for years, immune to redemptions on which the fee is guaranteed regardless of performance. An open-end fund must stand ready to redeem at NAV which disciplines the manager: perform poorly and investors walk, shrinking the fee base. Closed-end is comfortable for the people running the money. Open-end is comfortable for the people whose money it is. The industry has, predictably, preferred its own comfort and the discount is the bill it quietly passes to investors for the privilege.

It is worth being precise about what conversion to open-end would and would not solve. Turning a closed-end fund open would abolish the discount on that fund overnight, because redemption at NAV makes a discount impossible. It would not, by itself, make the manager any better or the underlying Nepali equities any less volatile; an open-end fund holding the same shares would still rise and fall with the market. What it would do is stop charging investors a second penalty, the discount, on top of the ordinary risk of owning equities. The closed-end wrapper does not add return; it only adds a way to lose. Removing it is pure gain for the investor and pure discipline for the manager, which is exactly why it has been resisted.

The encouraging development is that this is beginning to change. The newer wave of open-end schemes, the systematic investment plans that let investors drip money in monthly and redeem at NAV, points to where a healthier industry would go: more open-end funds, fewer closed-end ones, and for the closed-end funds that remain, mechanisms like unit buybacks and shorter lifespans that keep the price honest. None of this is exotic. It is standard practice in deeper markets. Nepal's asset managers know it perfectly well. They have simply not yet had a strong enough reason from regulators or from investors to give up the comfortable structure for the fair one.

What the regulator could do

If the discount is structural, the obvious question is what the regulator intends to do about it and the honest answer is, so far, not much. The Securities Board of Nepal has the authority to reshape the industry and several of the levers it could pull are neither radical nor untested elsewhere.

The most direct would be to require closed-end funds to defend their own NAV. A mandatory buyback mechanism, triggered when a fund's discount exceeds some threshold, would force managers to repurchase units in the market when they trade too cheaply, putting a floor under the price and returning capital to the investors who want out. Several markets use exactly this device to keep closed-end discounts in check. Nepal does not require it and few managers volunteer it because buying back units shrinks the asset base on which their fee is charged. The tool exists; the incentive to use it does not.

A second lever would be to tie the management fee to performance or at least to charge it on the market price rather than the reported NAV, so that managers share in the discount from which they are currently insulated. A third would be to nudge the industry toward open-end structures, easing the path for new open-end launches or encouraging maturing closed-end funds to convert rather than simply wind up. A fourth, simplest of all would be to improve disclosure: more frequent NAV publication, the discount itself shown plainly on trading screens and investor education that explains what a discount means so that the retail buyers who currently shun discounted units might learn to read them as the value they represent.

None of this is exotic and none of it has happened at scale. The regulator has been content, for the most part, to license funds, approve their documents and let the market sort out the price which it has duly done by marking the units down. A more activist board, one that treated the persistent discount as a sign of a product flaw rather than a market quirk, could close much of the gap with a handful of rule changes. That it has not is itself part of the story: the discount survives partly because no one with the power to end it has yet decided it is a problem worth ending. With a new chair recently installed at the board, that calculation may change but the burden of a decade's inertia sits against it.

What the discount says about Nepal

Step back from the mechanics and the discount becomes a kind of mirror, and what it reflects is not flattering. A persistent, industry-wide discount to NAV is, at bottom, a measure of trust and the Nepali mutual fund industry has not earned much.

Think about what it means for a market to price a basket of assets below the sum of its parts, year after year. It means investors do not believe the manager will add enough value to justify even fair value let alone a premium. It means they fear being trapped by illiquidity or by a long maturity more than they covet the discount. It means there is no class of sophisticated, patient capital large enough to enforce fair pricing. And it means the people who could close the gap, the managers are paid not to. Every one of those is a statement about the maturity of an asset-management industry and Nepal's are the statements of a young one that grew its assets faster than it grew its credibility.

The contrast with what these funds could be is the saddest part. Mutual funds are, in principle, exactly what a market like Nepal's needs: a way for small savers to own a diversified, professionally managed slice of the economy without the knowledge or the time to pick stocks themselves, a counterweight to the speculative IPO-flipping that dominates retail behaviour, a source of patient institutional capital that could stabilise a volatile market. A well-run mutual fund industry would be one of the better things that could happen to Nepali capital markets. The discount is the measure of how far the actual industry sits from that ideal.

It is also, for the patient and clear-eyed investor, an opportunity and it would be dishonest to end without saying so. The discount is real, the pull to par at maturity is structural and an investor who understands the risks who can tolerate the illiquidity and the wait and the possibility that the NAV itself falls is genuinely being offered Nepali equity below its market value. The reasons the discount persists are also the reasons it is available: most participants cannot see it, cannot execute it or are paid not to close it. That is precisely the condition under which a real opportunity hides in plain sight.

It is tempting to read the discount as simply the sign of an immature market that will fix itself with time, and there is something to that. But maturity is not automatic; it is built by regulators who demand better products, by managers who choose alignment over fees and by an investor base that learns to read what it is buying. None of those is guaranteed to arrive. Markets can stay shallow and discounts wide for a very long time if the people with the power to change them find the status quo comfortable enough. The discount will close when Nepal's asset-management industry decides to earn it shut and not a day before.

The verdict renewed daily

The closed-end discount will probably narrow over time but not for the reasons an optimist would hope. It will narrow as the oldest funds reach maturity and pay out at NAV mechanically closing their own gaps. It will narrow if the open-end structure gradually displaces the closed-end one, as it should. It will narrow if liquidity deepens enough that arbitrage capital can finally do its work. What will not close it is the market suddenly deciding to trust an industry that has not yet given it reason to.

Until then, the discount stands as the most honest number the Nepali mutual fund industry produces. The managers publish their NAVs, their glossy fact sheets, their performance claims. The market reads all of it and renders its own verdict every trading day, in the only language that cannot be massaged: the price. And the price says, with remarkable consistency, that a rupee of these funds is worth about eighty paisa. The industry can call that a mispricing if it likes. It is closer to the truth to call it a grade.

For the investor, the lesson is twofold. Treat the discount as a signal, not a glitch: it is telling you something real about liquidity, about trust, about the alignment between the manager and you. And if you choose to buy it anyway, do so with your eyes open, knowing exactly which of the discount's many causes you are betting will reverse, and over what horizon. The eighty-paisa rupee is real. So for every reason it costs only eighty paisa. The whole of Nepali asset management, in the end, is written in that gap.

And it is, finally, a fixable gap which is the note worth ending on. Nothing about the discount is a law of nature. It is the sum of choices, by managers who preferred the locked-up fee by a regulator who preferred to be watched by investors who never learned to look. Change any of those and the gap narrows. A market gets the discount it tolerates and Nepal has tolerated this one for a decade. The day it stops will be the day its asset-management industry finally grows up.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.