Markets Weekly June 05: The Budget's Winners and Losers

The market sold the capital gains tax hike, failed to hold its rebound, and rotated sharply into insurance and finance while hydropower dragged the index lower.

The market's first answer to the budget was a 233-stock sell-off then it stopped panicking and started sorting. Insurance up, hydropower down, capital-gains tax the dividing line. Four sessions on the index is roughly where it began, but underneath it's a different market.

I. The week in three sessions

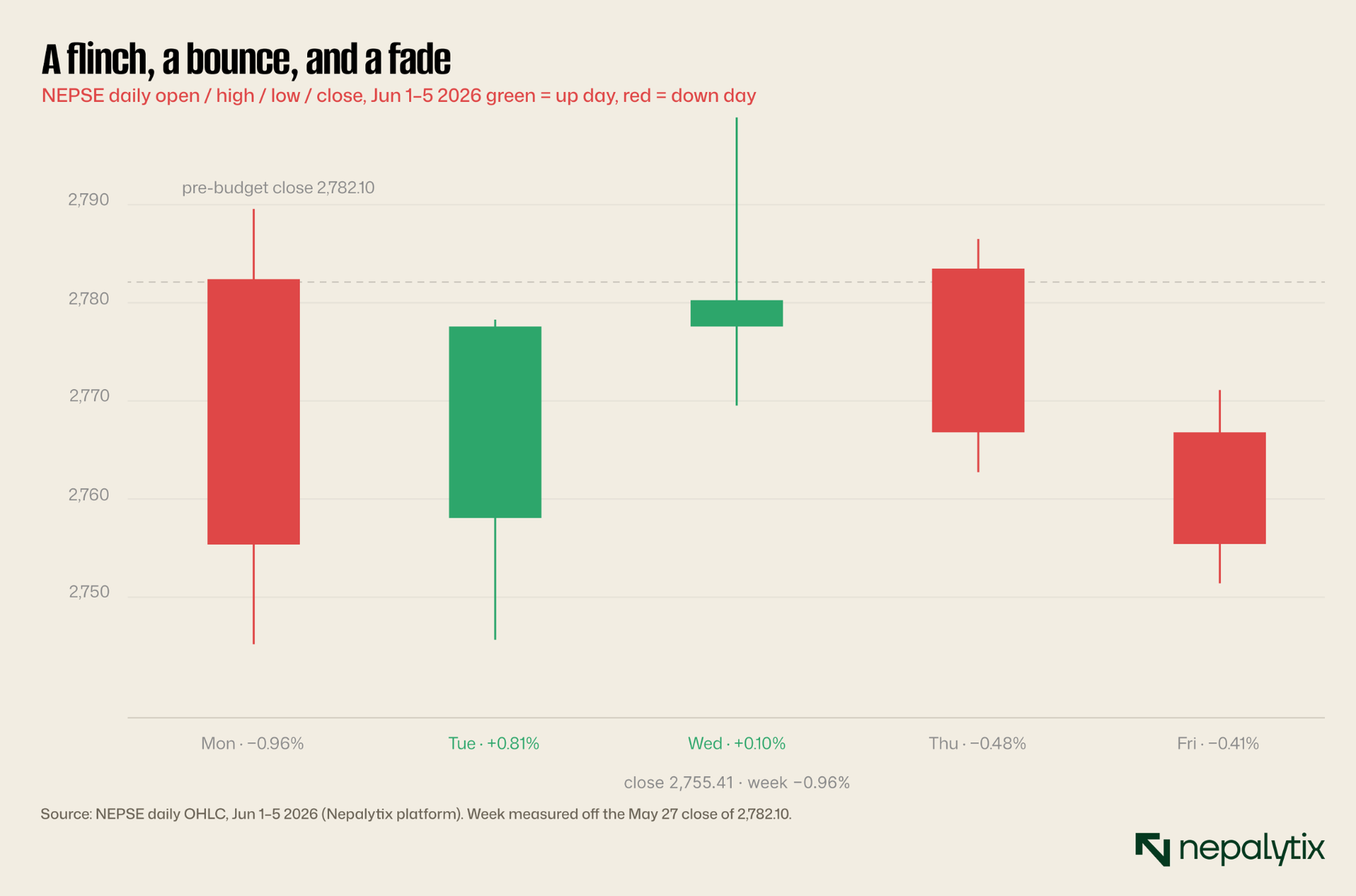

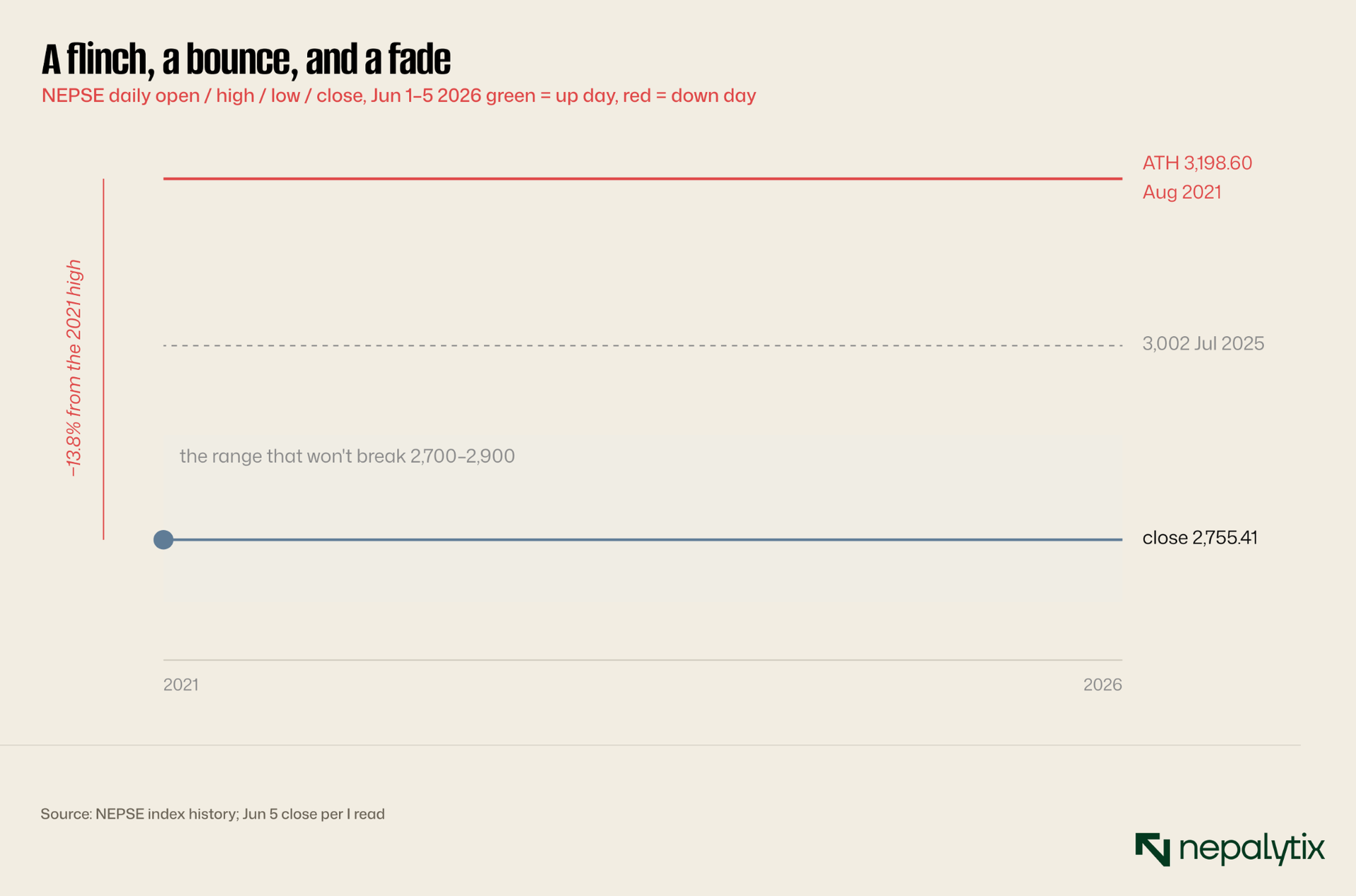

The market's first word on the budget was no and its last word, five sessions later, was the same. NEPSE closed the first full post-budget week at 2,755.41, down 26.69 points (0.96%) from where it sat before Wagle stood up. In between it staged a near-perfect round trip and then gave the whole thing back.

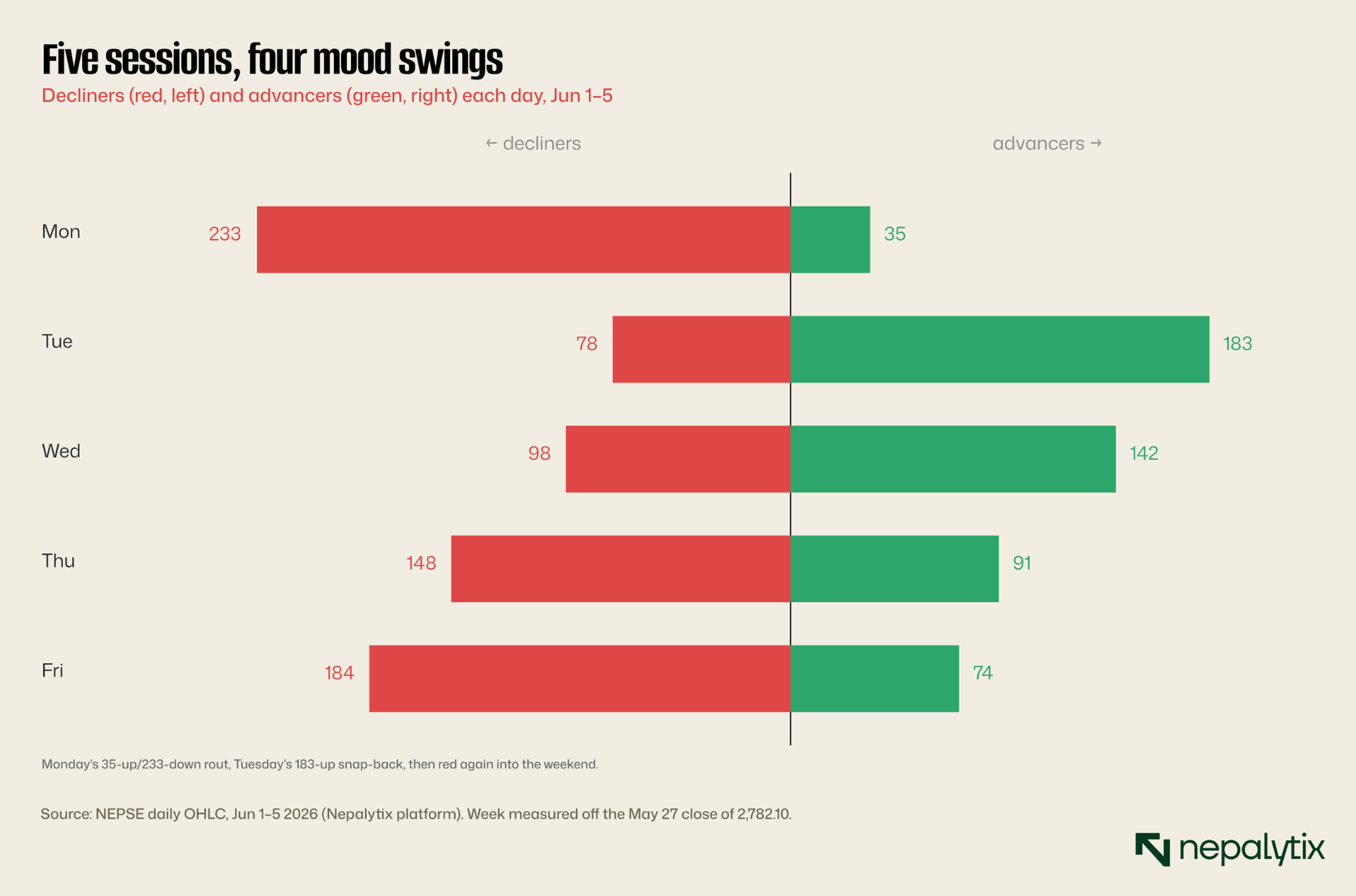

The candles carry the whole arc. Monday gapped lower and sank to 2,745 intraday investors read "10% and 7.5%" on capital gains and bolted. Tuesday and Wednesday clawed almost all of it back, Wednesday even poking at 2,799 before fading. Then Thursday and Friday rolled over again. The bounce was real; it just didn't hold. If the index looks merely soft, the breadth underneath shows how violent the week actually was.

Monday's 35-up against 233-down was a stampede; Tuesday's 183-up against 78-down an equally violent reversal; then the red returned, 148 and 184 decliners into Thursday and Friday. This was a market reacting in spasms, not deciding. And it did it on real volume, not holiday drift.

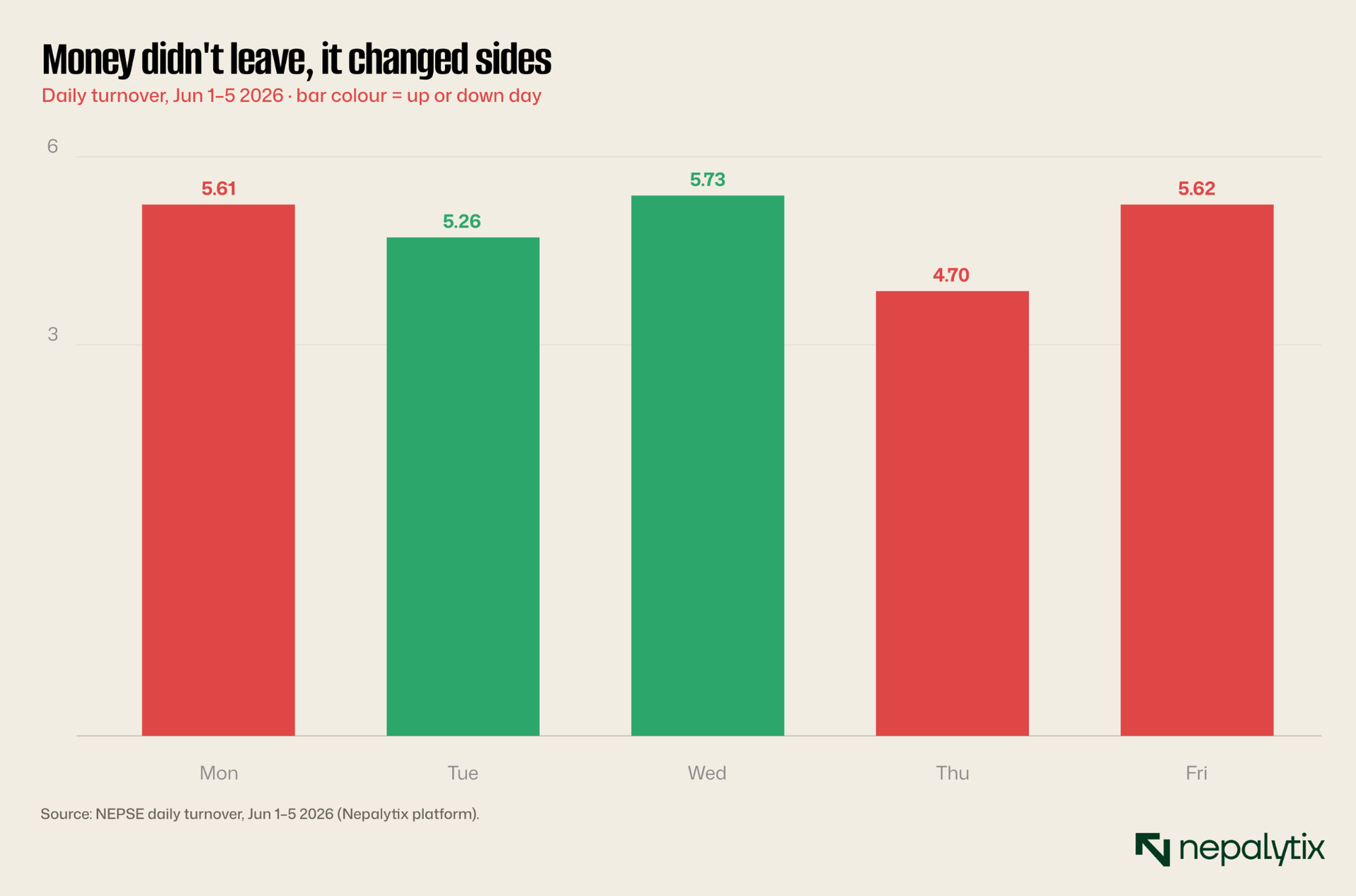

Turnover held between Rs 4.7bn and Rs 5.7bn all week, dipping only Thursday before Friday's Rs 5.62bn sell. The money didn't leave the market; it changed sides. Which is the real story of the week not the index level, but the rotation underneath it. Friday's sector tape is the clearest snapshot of where it went.

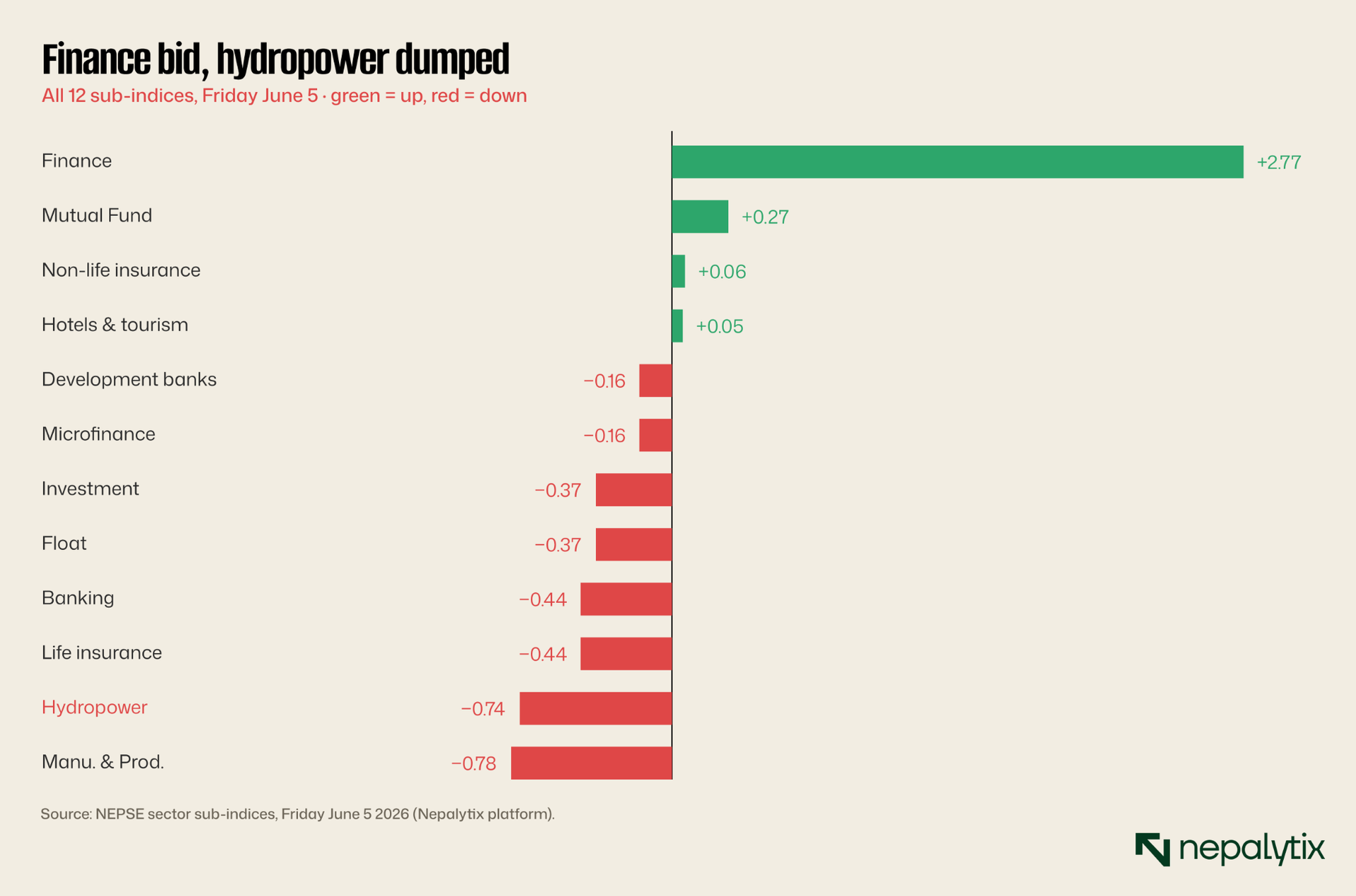

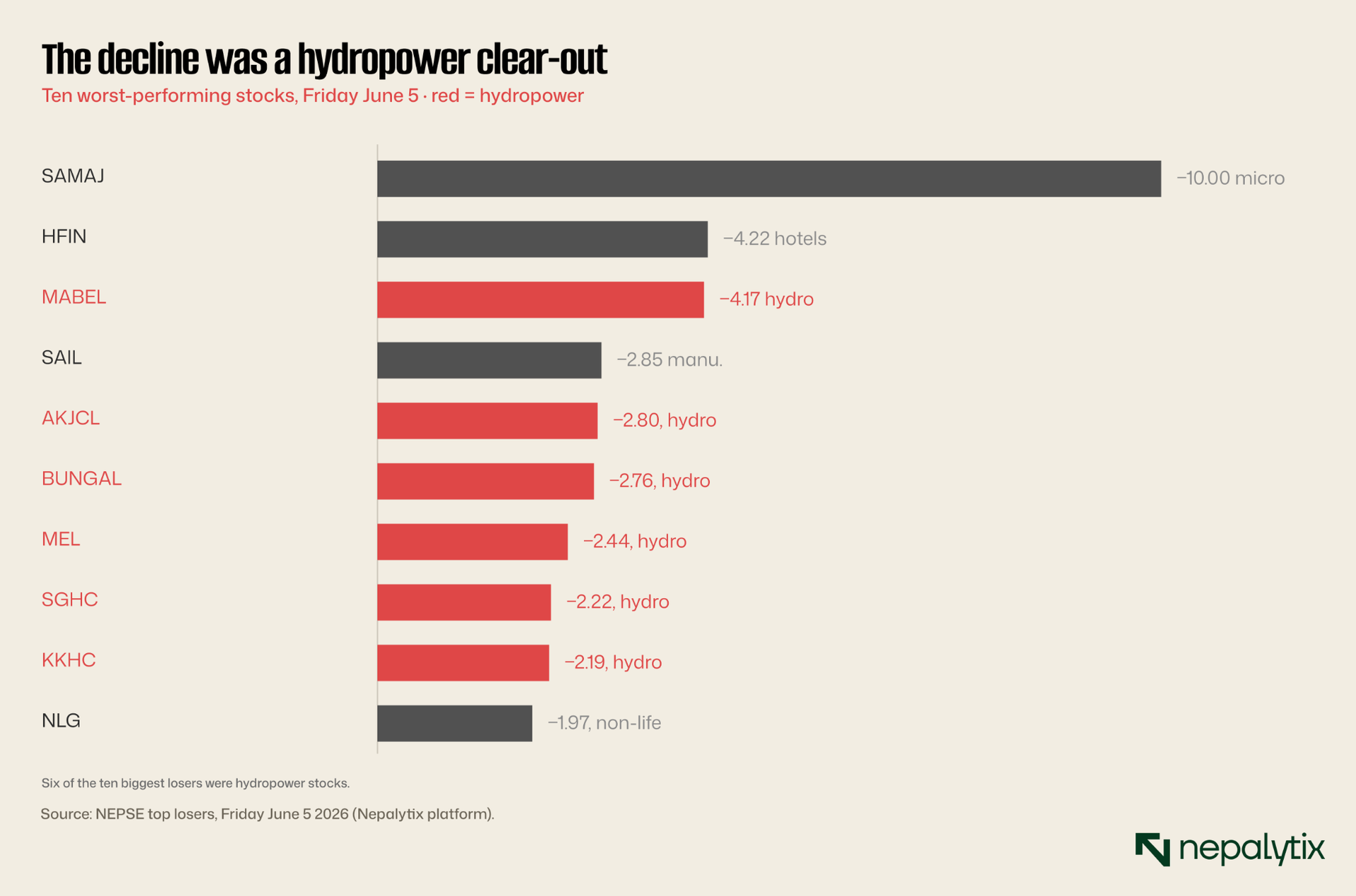

Finance led Friday (+2.77%) and the gainer board was a wall of finance and microfinance names ULBSL +9.71%, BFC +7.55%, CITY +7.06%. The bottom was a hydropower row: of the ten biggest losers, six were power stocks — MABEL −4.17%, AKJCL −2.80%, BUNGAL −2.76%, MEL, SGHC, KKHC alongside Samaj Laghubitta pinned to its −10% floor. The damage was concentrated; the strength rotated. On secondary estimates the week trimmed roughly Rs 45bn off market value, to about Rs 4.66tn an index-derived approximation, not a reported figure.

So the verdict is a guarded no, with a re-sort underneath: the market sold the tax, couldn't hold the bounce, and rotated toward what the budget feeds and away from what it taxes. The next three stories are that rotation. Start with the one sector that stayed green when everything else bled.

II. The one sector the budget bought

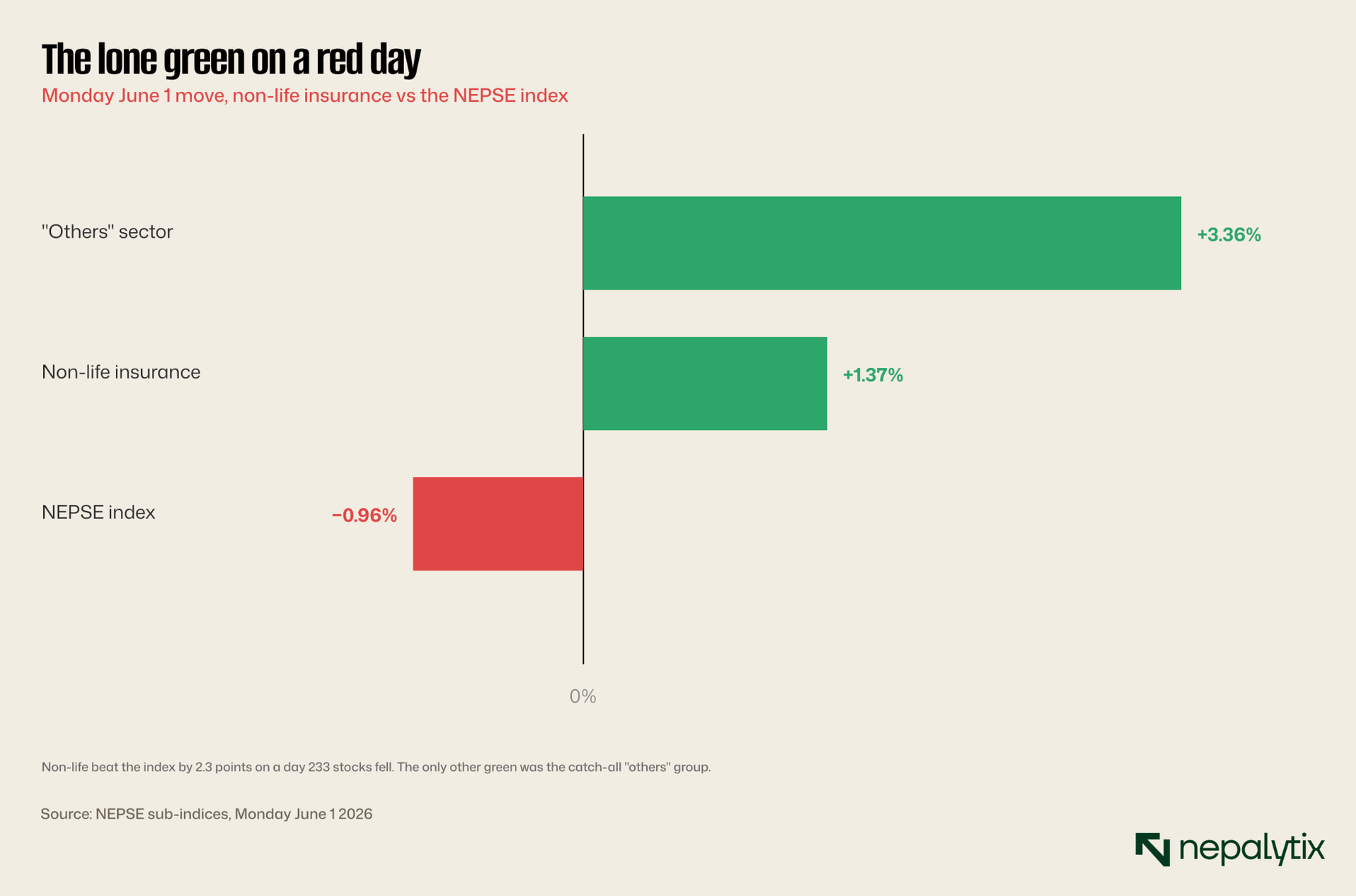

When 233 stocks fell on Monday, non-life insurance went up the only large sector to do so, +1.37% on the worst day of the week. It wasn't bargain-hunting or defensiveness. The budget had just written the sector a demand cheque, and the market cashed it the same morning.

Why? Three lines in the Finance Bill explain it. The budget made insurance mandatory on residential building construction, raised compulsory third-party motor cover to Rs 1 million, and put National Life Insurance up for its first-ever public share sale. That isn't a forecast of demand, it's legislated demand and it lands on the single most underdeveloped corner of Nepali finance.

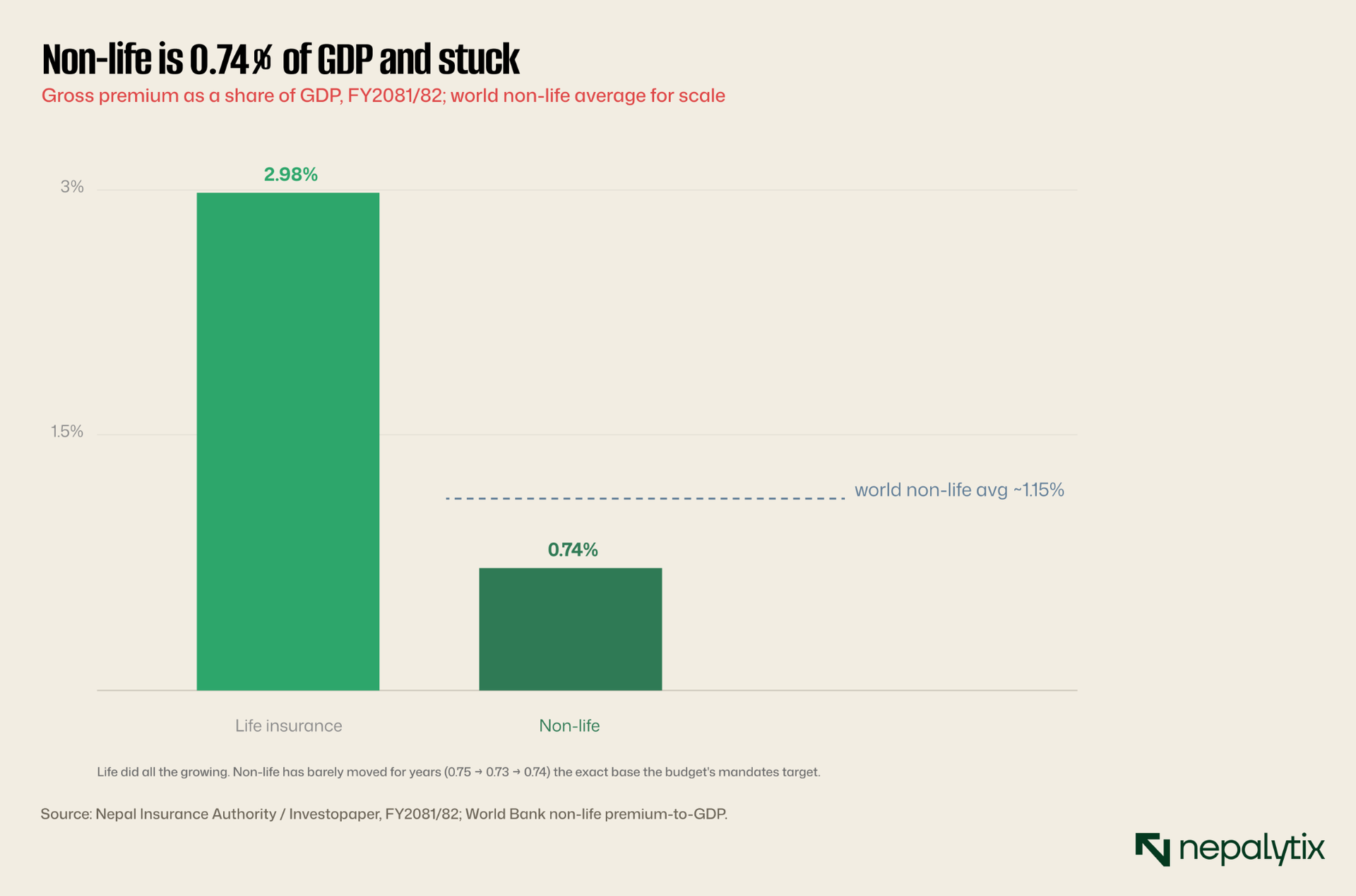

Non-life sits at three-quarters of one percent of GDP barely a third of the world average, and flat for years while life insurance did all the growing. So the budget didn't sprinkle incentives on a healthy sector; it pointed to a legislative fire-hose at the part of the market with the most room and the least momentum. The tape understood that immediately.

There's a second engine under the bid worth naming because it shapes the whole market right now. With bank deposits paying under 5% and property frozen, Nepali savers have almost nowhere left to chase a return the banking system is sitting on more than a trillion rupees it cannot lend. That wall of idle money is why a sector suddenly handed legislated growth doesn't just get bought, it gets mobbed. It's the same backdrop that will decide how every other budget lever lands: when cash has nowhere to go, the market reacts hard to anything that changes the after-tax math of holding shares which is exactly the fight in IV.

III. The sector that pulled NEPSE down

Now the red. Hydropower is the heaviest thing on this exchange, the most-listed sector, a perennial leader of turnover, the engine that usually drives the index. This week it ran in reverse, and because of its weight, it took the market with it. Every session after Monday, hydropower underperformed the index.

Set Samaj Laghubitta aside pinned to its 10% circuit floor for stock-specific reasons and the loser board is almost all hydropower: MABEL, AKJCL, BUNGAL, MEL, SGHC, KKHC, six of the worst ten. Hydropower is also where the market's volume lives, so when it sells, the index feels it. The weakness wasn't a one-day quirk; it tightened all week, and the budget is why.

The drag isn't a mood, it's a squeeze, and the budget tightened two of its three jaws. Hydropower is where Nepal's retail traders churn hardest, so the CGT hike to 10%/7.5% bites it harder than any other sector: a tax that punishes turnover lands heaviest on the most-traded names. Then the budget quietly rewired how the sector's biggest projects get built and that traces back to a number the government can no longer ignore.

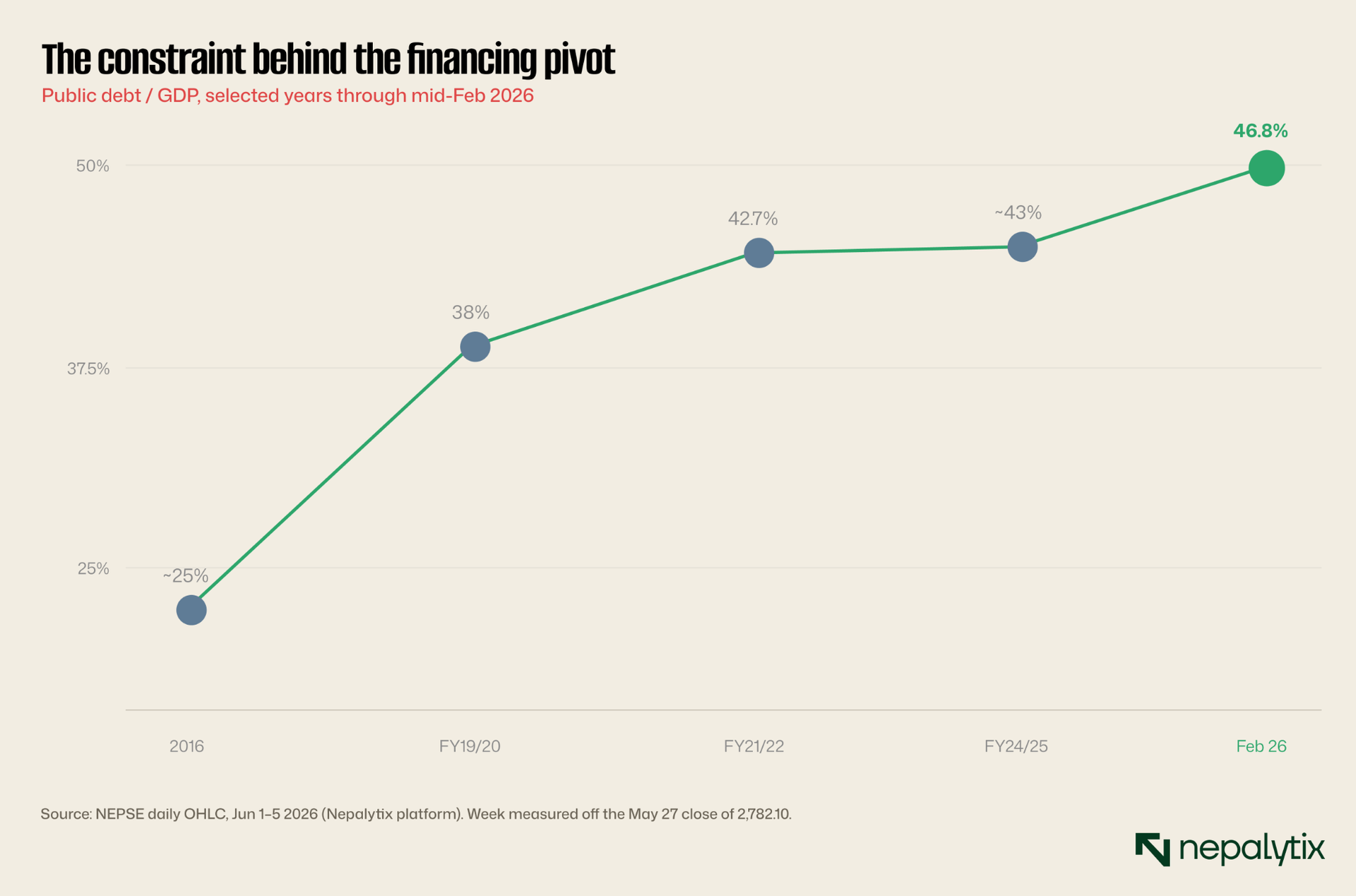

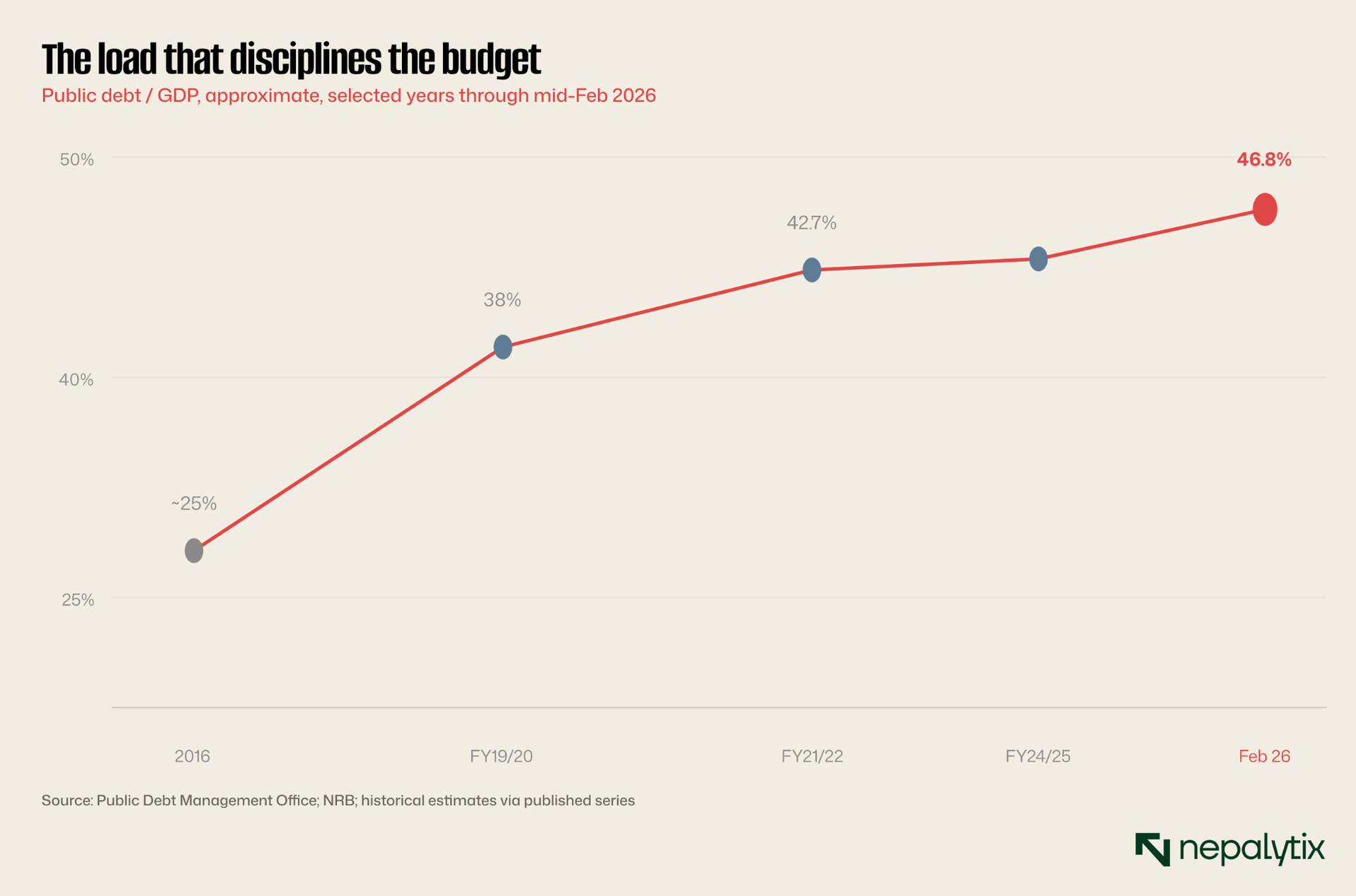

Public debt has nearly doubled in six years, to 46.81% of GDP Rs 2.858tn. With the balance sheet that stretched, debt-financed mega-projects are off the table, and Wagle signalled that the flagship builds Nijgadh Airport, the Budhi Gandaki hydropower project shift onto PPP and FDI instead. For a market where hydropower is the dominant weight, that is not a financing footnote; it is a live question about future listed supply and the sector's earnings base. Until the government puts a mechanism and numbers behind the rhetoric, that question stays open and the sector that usually leads NEPSE keeps trading like the one holding it back.

IV. The line that did the sorting

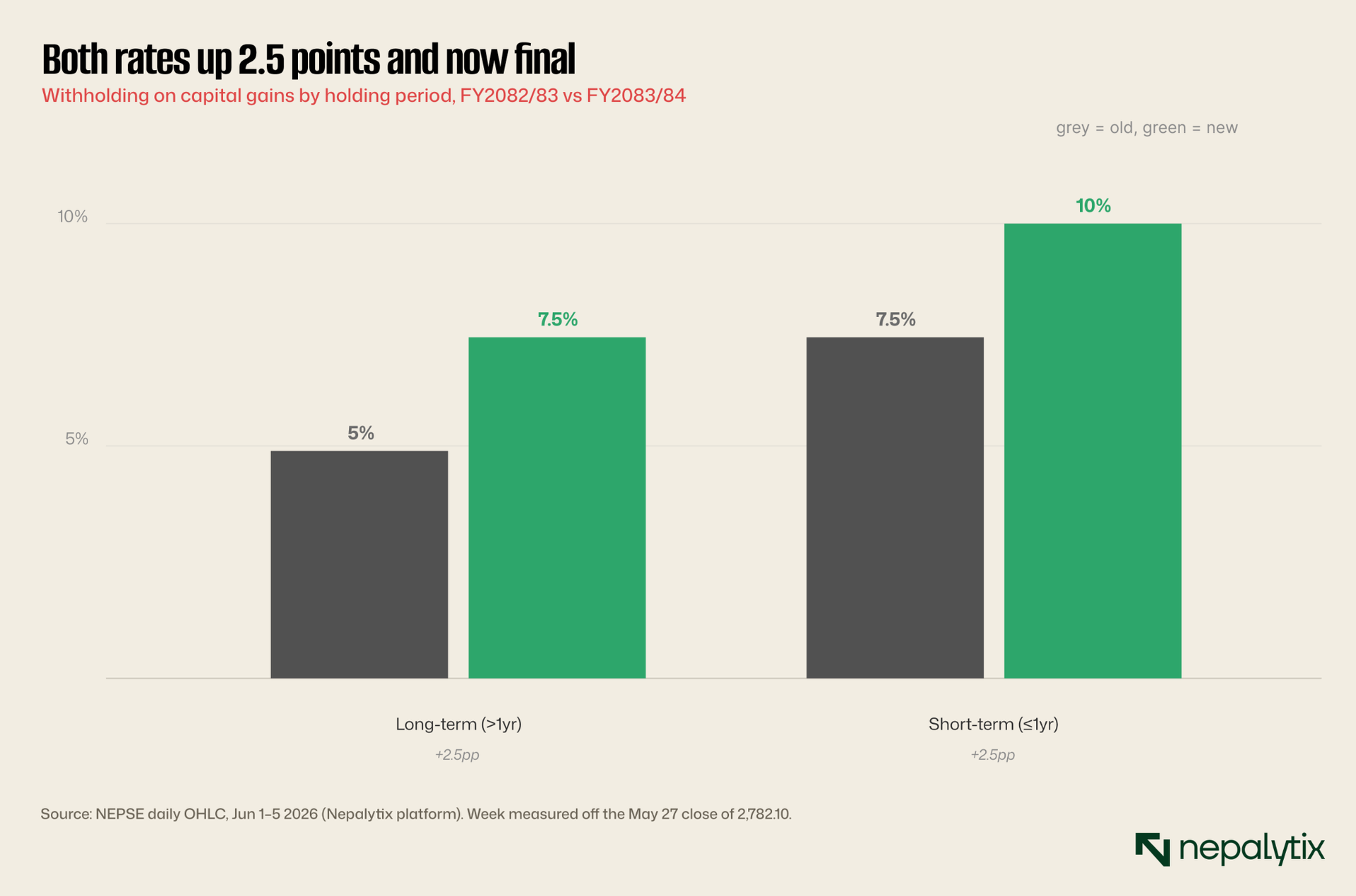

Both stories above run through one number: the capital-gains tax. The budget finally made it a final tax the certainty investors had asked for since 2023 and, on the same page, raised the rate. Short-term gains go from 7.5% to 10%, long-term from 5% to 7.5%. That hike is what they sold on Monday, and it's the dividing line between the green sectors and the red.

The bulls have a fair counter: even hiked, Nepal still taxes a gain well below India's 12.5%/20%, and finality ends a three-year limbo. But the floor's objection is sharper and structural Nepal taxes transactions, not portfolios. Lose money on the year and you can still owe tax.

So the level isn't the grievance the structure is.

Because losses can't offset gains and there's no carry-forward, the tax lands on gross winning trades, not net performance, an effective 37.5% on what our example investor actually made. As one analyst put it, the change is "headline positive but structurally incomplete." Finality settled the old argument; it didn't touch this one. And it's this structure, sitting on top of a high-churn market, that made the hike hurt hydropower most and spared the sectors the budget was feeding.

V. What to Watch

The reaction isn't finished, Friday is still open, and the budget's bigger levers haven't even switched on. Here's the short list that decides whether this week's sorting becomes a trend.

Step back and the whole budget-week drama: the flinch, the bounce, the fade happened inside a band NEPSE has been stuck in for four and a half years, still 13.8% below its 2021 peak. That's the real tell: a CGT change and a fistful of reforms shuffle sectors around within the range; they don't break it. What breaks 2,900 is earnings, and earnings need the economy to actually grow. The budget is betting on 7%, against a recent run-rate nearer 3–4%. That gap, not the tax rate, is the number that decides the next leg.

So the short list to watch: July 16, when the new 10%/7.5% CGT rates switch on and the high-churn trade gets its real test; whether the government puts a financing mechanism behind the hydropower PPP rhetoric or leaves it at intention; and whether the mandated insurance demand keeps bidding non-life as the National Life IPO supply approaches. The honest verdict on the week is a guarded no: the market sold the tax on sight, failed to hold its own bounce, and closed down 0.96% but the louder story is what it did underneath, rotating hard out of hydropower and into finance, microfinance and insurance. It didn't reject the budget so much as re-price the market around it. Whether that re-pricing becomes a trend is next week's question; this week, the budget moved the tape, and the tape moved exactly where the budget pointed it.