Monopoly, Duopoly, and Dilution: Re-thinking Nepal Reinsurance Company

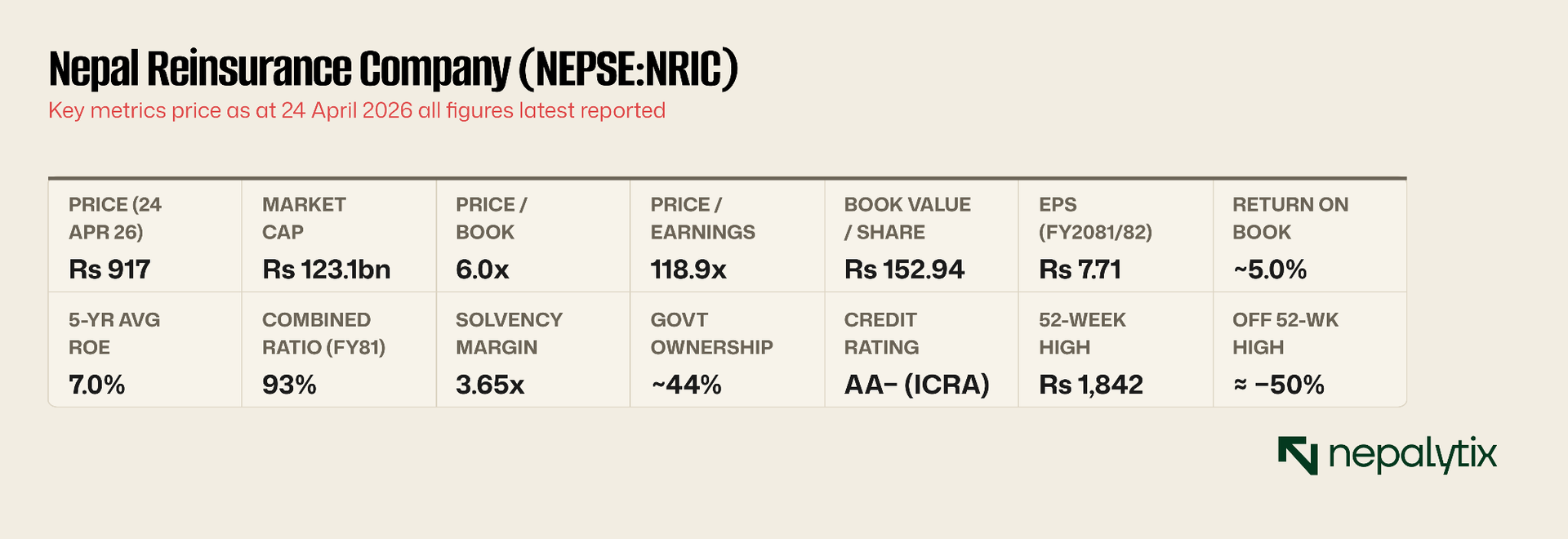

Nepal Reinsurance Company (NRIC) is often viewed as a government-backed monopoly with a strong balance sheet and guaranteed premium flows.

Nepal's first reinsurer is a sovereign-backed franchise with a fortress balance sheet, a captive flow of premium, and a genuine monopoly on one small line. It is also a sub-7%-return investment book whose regulatory subsidy is being legislated away, whose capital is being force-grown and whose shares trade at two to three times the multiple of the best reinsurers on Earth. This note lays out both halves and leaves the conclusion to the reader.

Nepal Reinsurance Company (NEPSE: NRIC) is routinely described, including by people who own it as a monopoly. The label is half a decade out of date. Nepal Re began life in 2003 as a state insurance pool covering riot, sabotage, terrorism and malicious-damage (RSMDST) risk during the Maoist insurgency was converted into the country’s first reinsurer in 2014 and listed on the Nepal Stock Exchange in June 2020. For its first years it was indeed the only domestic reinsurer and from 2018 the government handed it a captive revenue stream by making cession to it compulsory.

That exclusivity is gone. Since January 2024 a second, privately promoted reinsurer Himalayan Reinsurance (NEPSE: HRL), backed by the Shankar Group sits alongside it and the regulator splits mandatory cession between the two in equal shares. Nepal Re is a duopolist. What remains genuinely exclusive is narrow: under the Insurers Reinsurance Directive, Nepal Re is the sole legal beneficiary of RSMDST cession, a legacy of its insurgency-era origins. That single line grew to roughly 18% of gross premium in FY2080/81 from about 2% the year before after a profit-sharing renegotiation with cedants. It is the one place the word monopoly still applies.

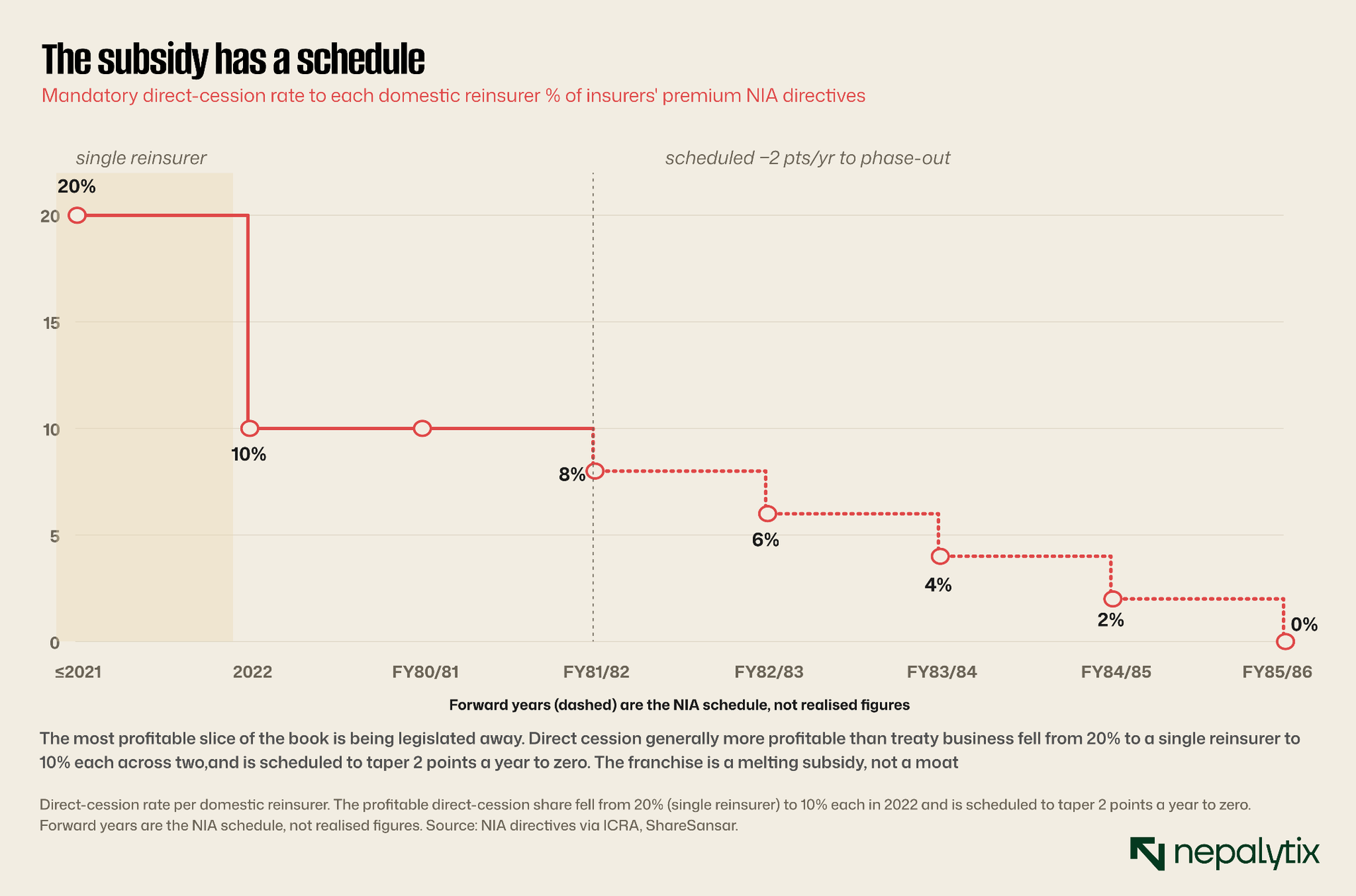

The rest of the franchise rests on mandatory cession and the terms are deteriorating. Under directives issued by the Nepal Insurance Authority (NIA, formerly the Beema Samiti) in May 2022 every domestic insurer must cede a fixed slice of premium and risk to each of the two reinsurers. The most lucrative slice direct cession was cut from 20% to a single reinsurer to 10% to each of two and is scheduled to fall a further two percentage points a year from FY2081/82 until it phases out by FY2085/86. Treaty cession, lower-margin, continues at regulated minimums on the remaining risk. The structure that built Nepal Re is being dismantled on a published timetable.

There is a second edge to the regulation. The 2080 directive also forces the entirety of several lines of life, motor third-party, agriculture, micro-insurance and RSMDST to be reinsured domestically and bars the two reinsurers from refusing any risk ceded to them. That is revenue but it is also concentration: a captive book of mandatory risk that cannot be declined, in a country exposed to one of the world’s most severe earthquake hazards. As of late 2025 the life-insurance industry was openly contesting the rule on risk-diversification grounds. The franchise, in other words, is not a quiet toll-road. It is a politically contingent arrangement that giveth and taketh away.

The international book deserves a moment because it is where the bull case looks for growth. Sovereign ownership has opened doors: Nepal Re has secured treaty participations across roughly a dozen Asian and African markets under the lead of established global reinsurers and holds a cross-border reinsurance certificate from India’s IRDAI. But this business is still a rounding error against the domestic book around 9% of gross premium and it is precisely the business where Nepal Re competes without a regulatory crutch against incumbents with decades of data and deeper balance sheets. Offshore expansion is a plausible long-term story; it is not yet a material earnings contributor, and the company’s 91%-domestic concentration is flagged by its own rating agency as a constraint rather than a strength.

It is worth dwelling on the one genuine monopoly because the bull case leans on it. RSMDST covers riot, strike, malicious damage, sabotage and terrorism is the line Nepal Re was born to carry, and the statute still names it the sole domestic home for that risk. The economics are attractive: the peril is episodic rather than chronic pricing references a state-backed pool rather than a competitive market and last year’s profit-sharing renegotiation lifted the line from roughly 2% of gross premium to about 18% in a single year. That is real, defensible, monopoly-grade business. But it is small in absolute terms, politically created and therefore politically revocable and concentrated in exactly the kind of correlated, headline-driven loss event that can turn a quiet line into a large claim overnight. The monopoly is a genuine asset; it is not a substitute for an underwriting franchise that earns its cost of capital.

Two reinsurers, one rulebook

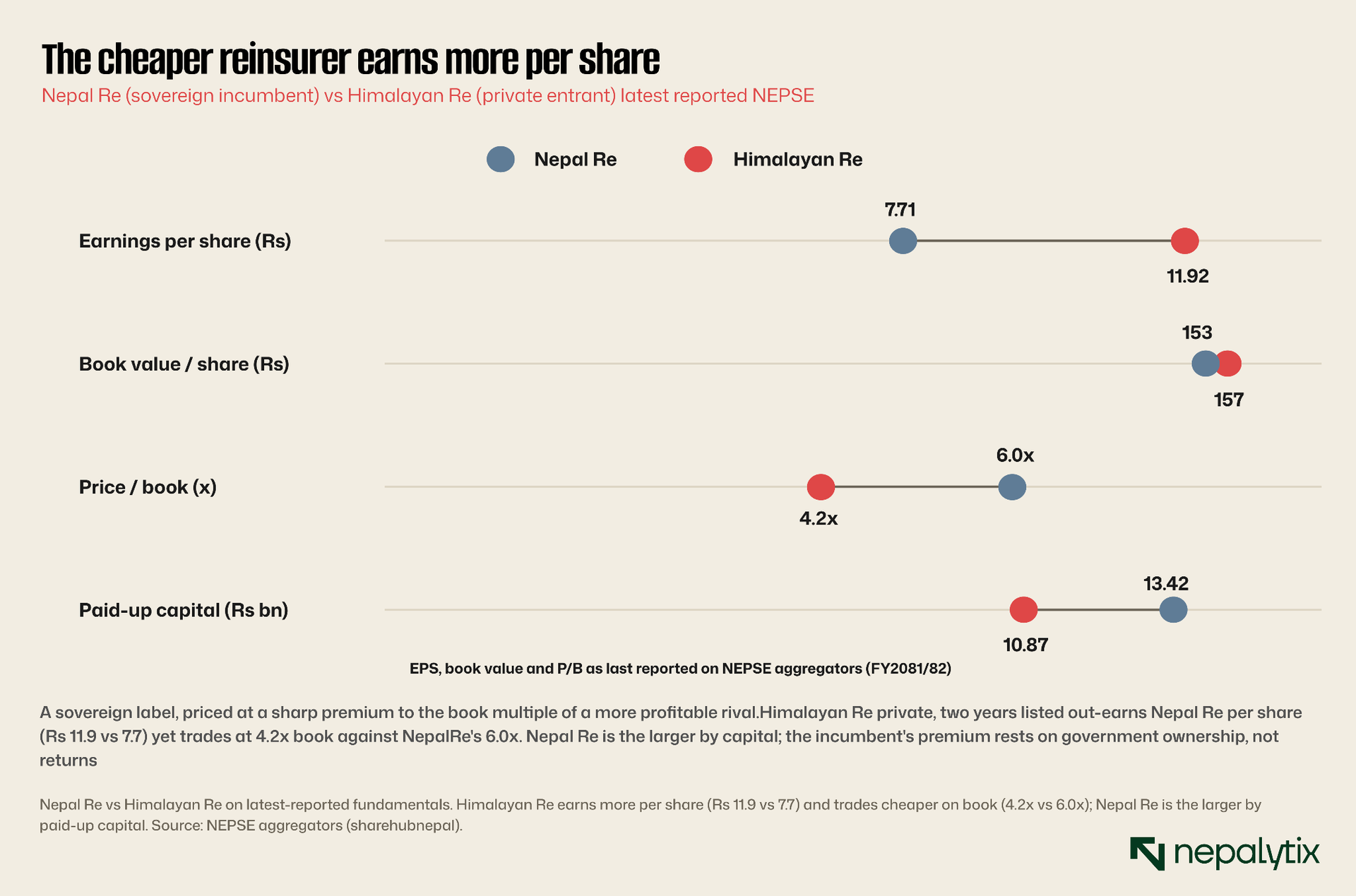

If mandatory cession defines the revenue, the competitive question is what Nepal Re does with it relative to the only peer that operates under the identical rulebook. Himalayan Re is two years listed, privately promoted, and roughly four-fifths Nepal Re’s size by paid-up capital (Rs 10.9bn against Rs 13.4bn). On the metrics that matter to an equity holder, the younger private entrant compares favourably uncomfortably so for the incumbent.

Himalayan Re earned Rs 11.9 per share against Nepal Re Rs 7.7 and changed hands at 4.2 times book against Nepal Re 6.0 times. The market in short, pays a large premium for the sovereign incumbent while the private rival earns more and costs less. Some of that premium is defensible: Nepal Re carries the implicit backing of a 44% government shareholder, the AA− domestic credit rating that follows from it, and the RSMDST monopoly. But none of those advantages has translated into superior per-share economics and the duopoly structure means the two firms increasingly chase the same mandated flow on the same terms.

The market pays a premium for the sovereign incumbent. The private rival earns more and costs less.

The competitive read is therefore neutral-to-negative for Nepal Re’s relative position. Equal cession shares cap its ability to out-grow Himalayan Re on the domestic book; its scale advantage in absolute premium is real but has not produced a return advantage; and its overseas ambitions treaty business across a reported thirteen countries and facultative cover across thirty-two remain small at roughly 9% of gross premium and unproven through a hard claims cycle.

It is worth being precise about why the comparison is awkward rather than damning. Himalayan Re carries a large IPO share premium of over Rs 3bn, which lifts its book and flatters some ratios, and its 70% promoter base includes two government-linked commercial banks so it is not a purely private animal either. As the newer entrant it has also built its book through benign claims years. None of that overturns the central point: on the numbers the market can see, the incumbent’s sovereign premium is not earning its keep against a rival operating under the identical mandate.

An investment book wearing a reinsurance licence

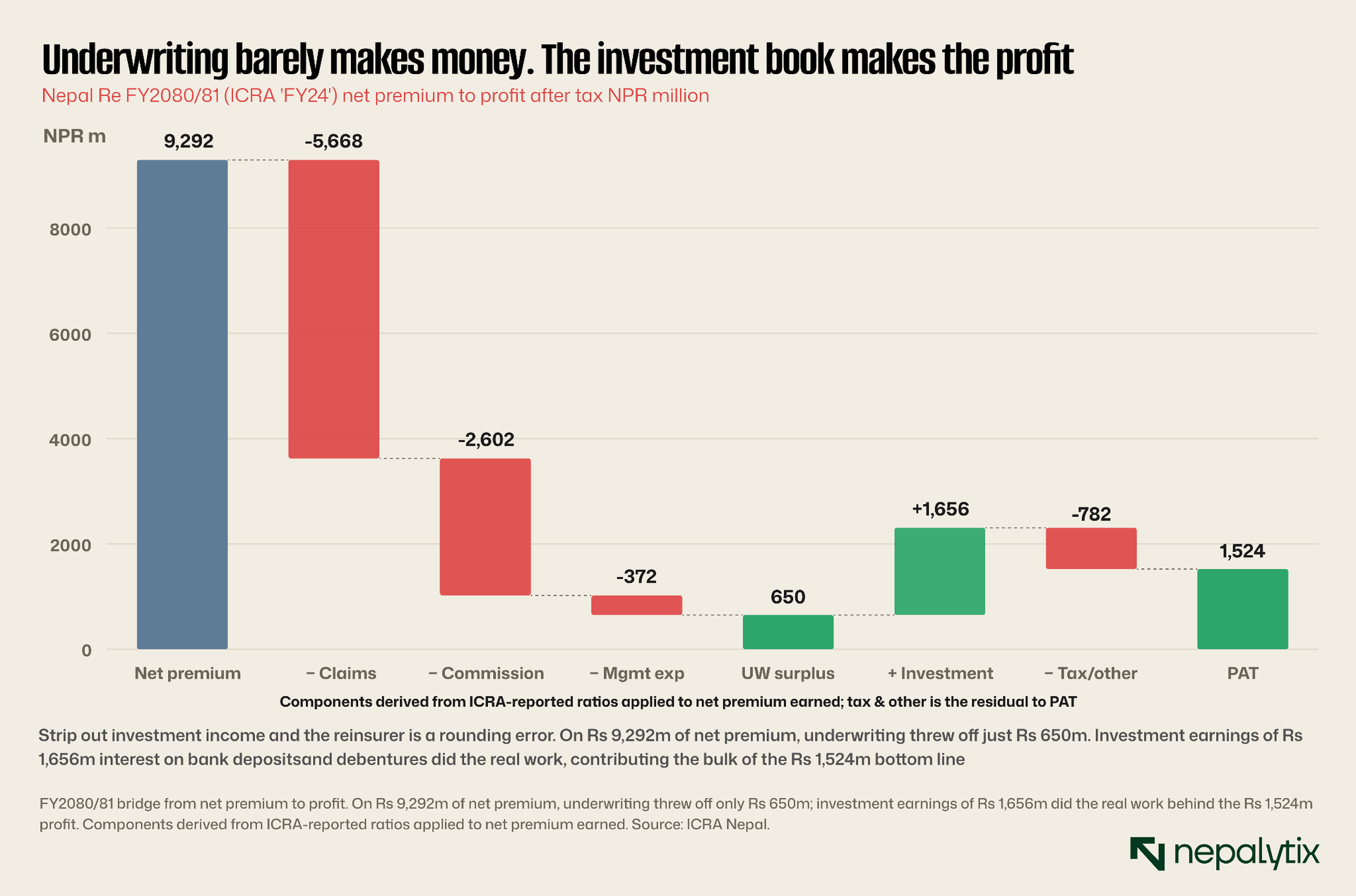

The single most important fact about Nepal Re is that it does not, in any meaningful sense, make its money from reinsurance. It makes its money from a Rs 32bn pile of bank fixed deposits and debentures, and the underwriting operation around that pile is close to break-even in a good year and loss-making in a bad one.

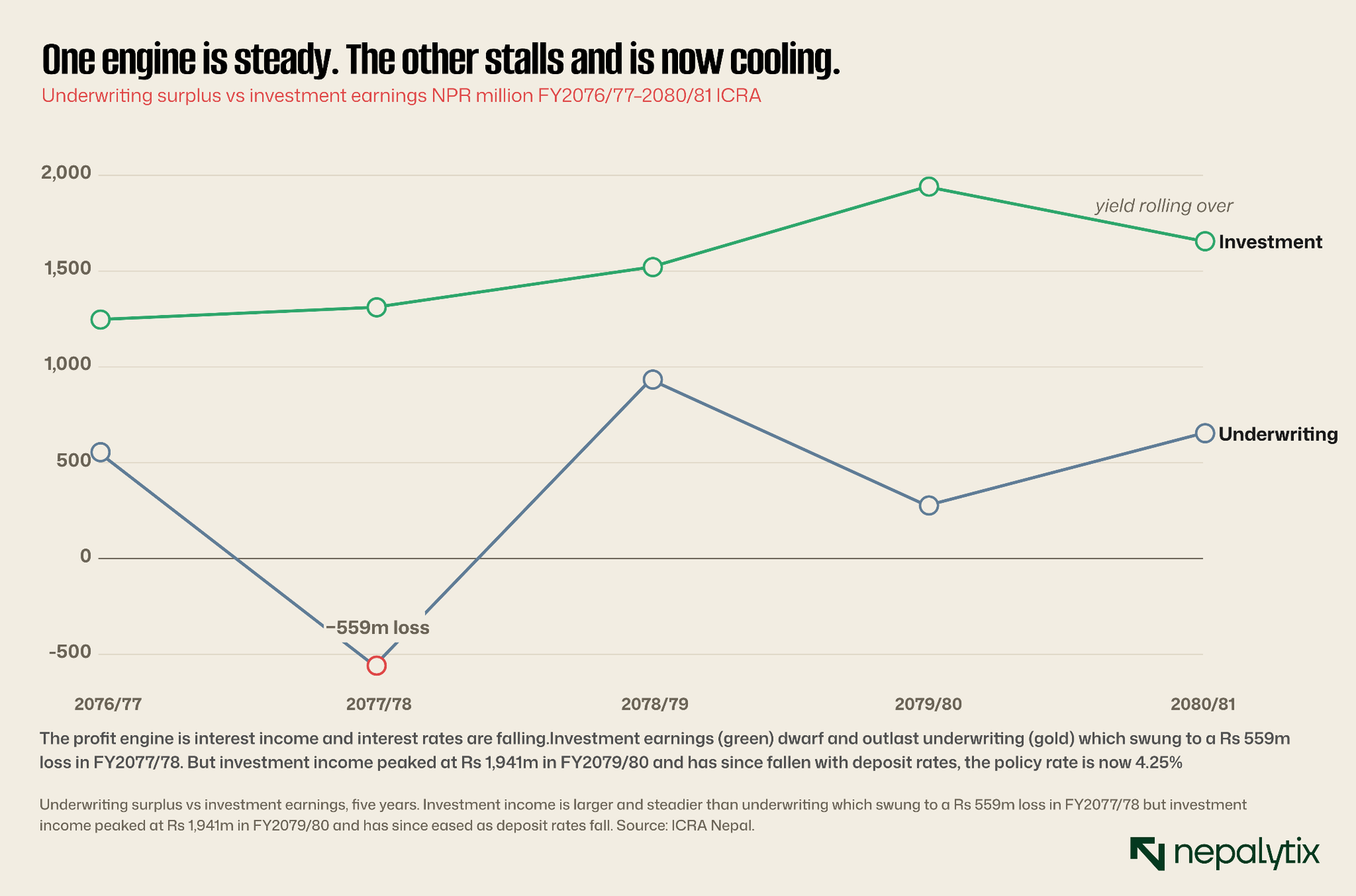

The bridge is stark. On Rs 9.3bn of net premium earned in FY2080/81, claims, commission and management expense consumed all but roughly Rs 650m. Investment earnings of Rs 1.66bn interest on deposits and bank paper then more than doubled the result before tax and reserves brought it to a Rs 1.52bn bottom line. Strip the investment income out and what remains is a thin, volatile underwriting margin on a captive book. This is not a quirk of one year; it is the model.

Over five years the two engines behave very differently. Underwriting surplus lurches Rs 555m, then a Rs 559m loss, then Rs 934m, Rs 277m, Rs 654m while investment income climbs steadily before rolling over. That roll-over matters. Investment earnings peaked at Rs 1.94bn in FY2079/80 and fell to Rs 1.66bn the following year as deposit rates softened; with Nepal’s policy rate now at 4.25% and the banking system awash in liquidity, the yield tailwind that has carried Nepal Re’s profits is turning into a headwind. A reinsurer whose earnings are a leveraged bet on Nepali deposit rates is a different and lower-quality proposition than the franchise label implies.

The composition of the book reinforces the reading. As of mid-2024 the portfolio was concentrated in fixed-deposit receipts and debentures of Nepali banks instruments whose yields move directly with the deposit-rate cycle the central bank is now easing, with little duration or credit diversification to cushion a falling-rate environment and regulatory limits on how far the company can reach for yield. The flip side, which the balance-sheet chapter returns to, is that this same conservatism makes the book genuinely low-risk in credit terms. But as an earnings engine, a portfolio of short bank paper in a 4.25%-policy-rate world is a structurally declining one.

The underwriting is a coin-toss

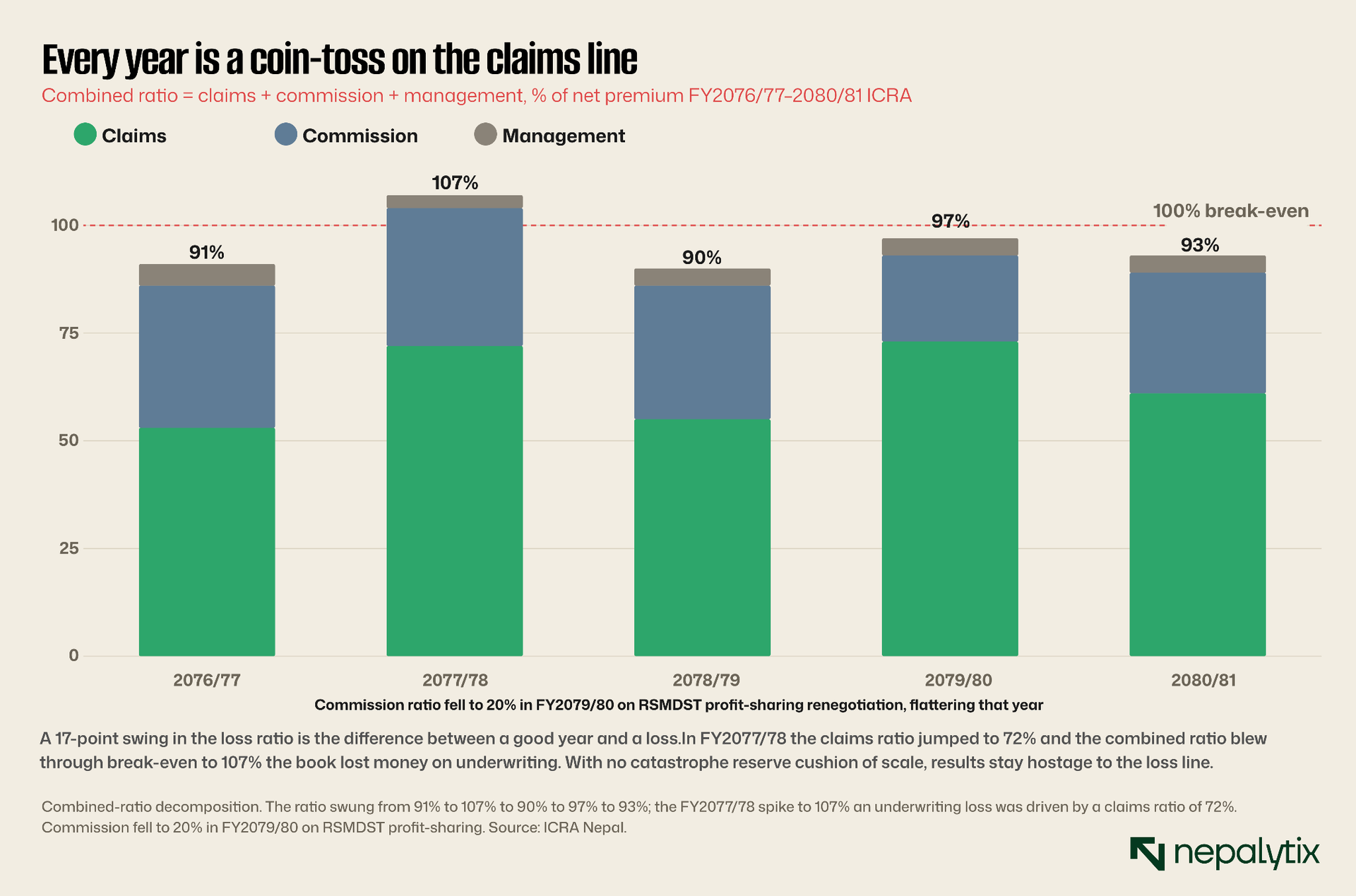

Because investment income flatters the headline, the quality of the underwriting is easy to miss. It should not be. A reinsurer’s combined ratio claims plus commission plus management expense, as a share of net premium is the cleanest read on whether the core business makes money, and Nepal Re’s has spent five years oscillating across the break-even line.

The combined ratio ran 91%, then 107%, then 90%, 97% and 93%. The 107% year was a genuine underwriting loss, driven by a claims ratio that jumped to 72%. The swing factor is almost entirely the loss line, a seventeen-point move between the best and worst years which is precisely what one would expect of a reinsurer that cannot decline mandated risk and lacks the scale of catastrophe reserves that global peers accumulate over decades. The commission line is noisier than it looks, too: the drop to 20% in FY2079/80 reflected a one-off renegotiation of RSMDST profit-sharing rather than a structural efficiency gain.

None of this is disastrous; a low-90s combined ratio is respectable for a young reinsurer. But it is not the picture of a dependable underwriter compounding a moat. It is a book whose annual result is hostage to the claims line, propped up by investment income and now facing the withdrawal of its most profitable cession category.

Two further points pull the underwriting picture in opposite directions. In Nepal Re’s favour, the rising RSMDST share is genuinely higher-margin and monopoly-protected and should lend the combined ratio more stability than the raw history suggests. Against it, the retrocession that caps catastrophe risk is itself a permanent cost: the premium ceded to Hannover Re and others drags on the net result and that cost tends to rise after heavy global catastrophe years regardless of Nepal Re’s own loss experience. The reinsurer is a price-taker on both sides; it cannot decline domestic risk, and it cannot dictate the cost of laying that risk off abroad.

Scale without returns

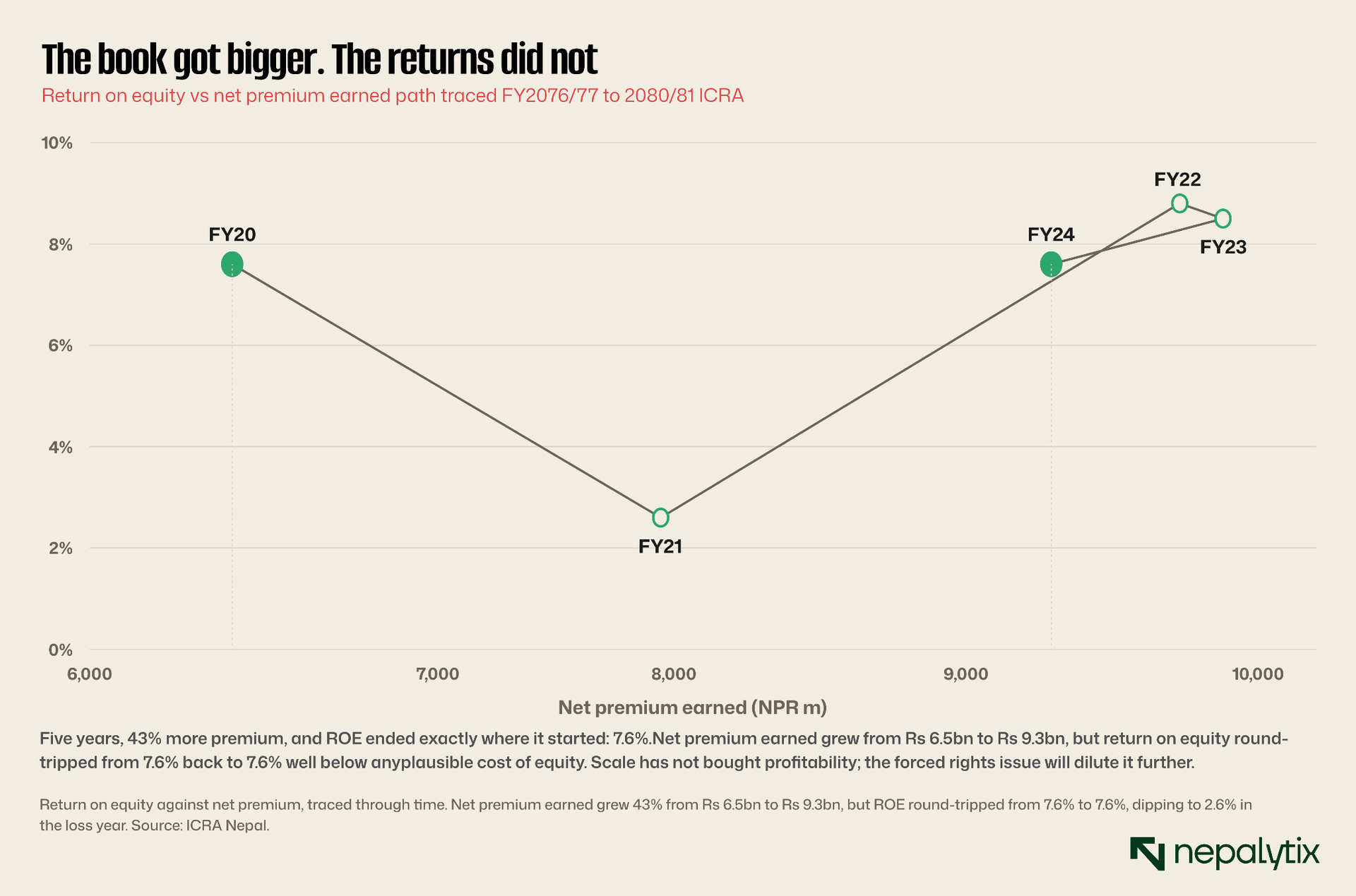

Put the five-year record together and a single chart tells the story that the franchise narrative obscures: Nepal Re has grown its premium base substantially and its returns not at all.

Net premium earned rose 43%, from Rs 6.5bn to Rs 9.3bn. Return on equity began the period at 7.6%, fell to 2.6% in the loss year, recovered to the high-8s, and ended exactly where it started: 7.6%. Five years of growth, a doubling of the captive cession base and the return on shareholder capital is unchanged and unchanged at a level well below any plausible cost of equity for a Nepali financial. The current-year picture is worse still: on FY2081/82 earnings of Rs 7.71 per share against book value of Rs 152.94, the return on book is roughly 5.0%.

Five years, 43% more premium and ROE ended exactly where it started: 7.6%.

The trajectory is about to bend the wrong way again. The NIA has directed Nepal Re to lift paid-up capital to Rs 20bn by Magh 2082 (January 2026); the company is executing a 1:1 rights issue to raise roughly Rs 7.2bn toward it. Issuing new equity into a business already earning sub-7% on equity is mechanically dilutive to return on equity unless the incremental capital is deployed at materially higher returns and there is no evidence in the record that it can be. More capital, on this book, means lower ROE.

The dividend record sharpens the question. Nepal Re’s most recent declared distribution was a token 4.75% bonus and 0.25% cash for FY2079/80 negligible against the capital it retains and the rights cash it is now calling. For the 44% government owner the equity has functioned more as a capital sink than an income stream and the rights issue asks minority holders to fund a regulatory capital target rather than a return-generating expansion. In a business already earning below its cost of equity, the burden of proof that incremental capital will be deployed productively sits with management and the five-year record does not discharge it.

The mechanics of the raise are worth spelling out. The 1:1 rights issue roughly doubles the share count, lifting paid-up capital from Rs 13.4bn toward the Rs 20bn the regulator demands by Magh 2082. New shares are issued at par against a book value of Rs 116 and a market price near Rs 917, so holders who take up their rights are averaging down hard and those who do not are diluted outright. Spreading a broadly unchanged stream of underwriting and investment earnings across nearly twice the equity base compresses both earnings per share and return on equity in the near term, before any benefit from the larger balance sheet can appear. Management will argue the bigger base unlocks retention and offshore growth; the arithmetic in the meantime is unambiguous, and it points down.

Against the world

Reinsurance is a global business with deep, liquid comparables, which makes Nepal Re unusually easy to benchmark for a frontier-market name. The comparison is not flattering and the most instructive peer is not a European giant but a regional one.

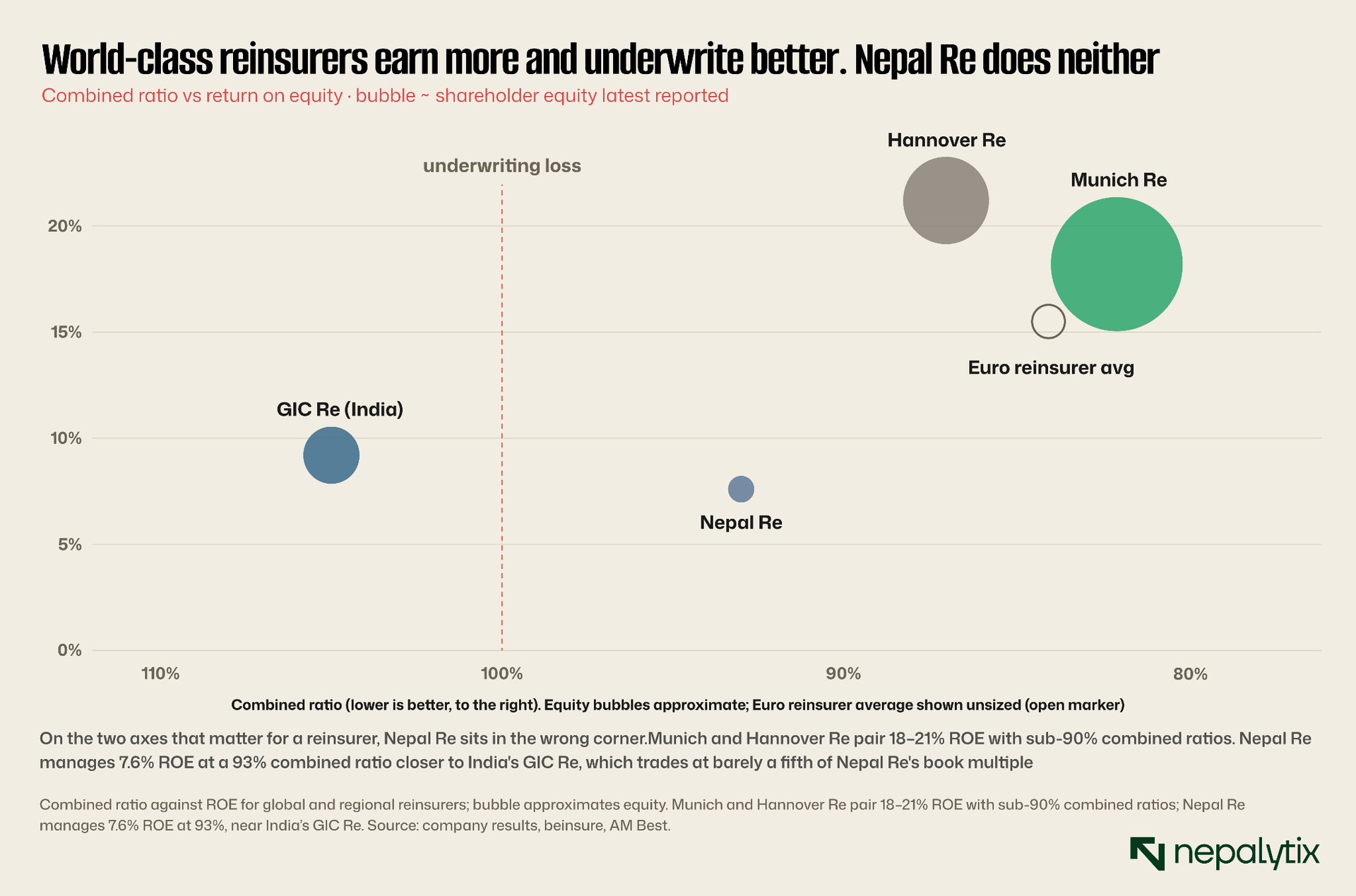

Munich Re earned an 18.2% return on equity in 2024 on a property-casualty combined ratio around 82%; Hannover Re earned an even higher 21% return at a combined ratio in the mid-80s; the European reinsurer average return was 15.5%. Nepal Re’s 7.6% ROE at a 93% combined ratio places it firmly in the wrong corner of the map with lower returns and weaker underwriting than the global complex. That gap is partly a frontier-market reality and partly the investment-led model showing through.

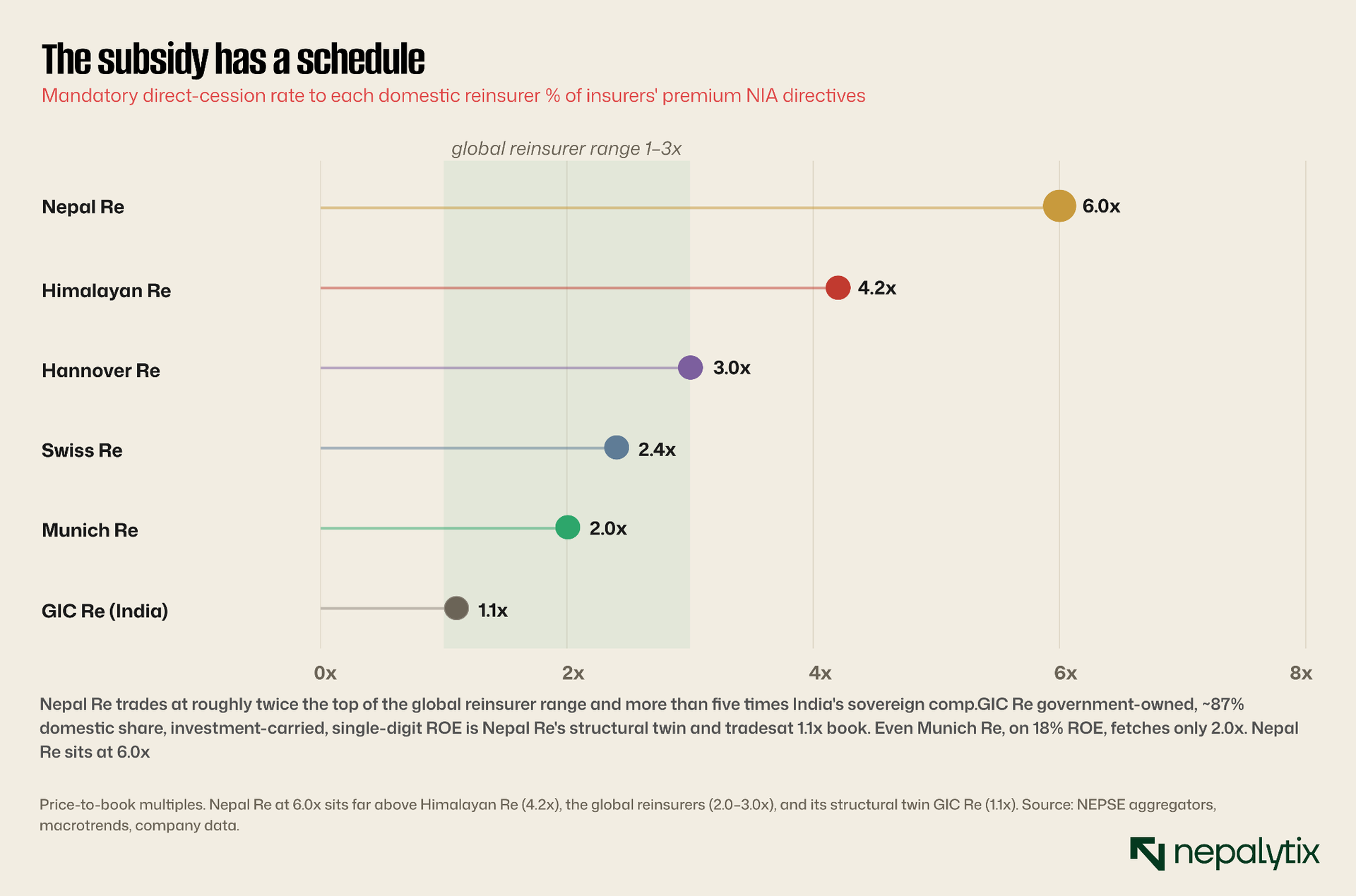

The sharper comparison is General Insurance Corporation of India GIC Re. It is the closest structural analogue Nepal Re has anywhere: government-controlled, dominant in its home market with roughly 87% share, an underwriting book that runs above a 100% combined ratio so that profits are carried by investment income, and a single-digit return on equity (a five-year average of 8.2%, 9.2% in FY2025). GIC Re is, in essence, what Nepal Re is a sovereign, investment-carried domestic reinsurer. It trades at 1.1 times book. Keep that figure in mind.

The natural objection is that NEPSE comparables trade richly across the board as a function of a small, largely closed market, limited free float, a deep domestic institutional bid and few alternatives for Nepali savings. That is true, and it means a literal 1.1x is the wrong target for a Kathmandu-listed reinsurer. But the scarcity premium is a feature of the market, not the company, and it applies equally to Himalayan Re, which still trades at little more than half Nepal Re’s multiple. Compare the two domestic names directly, same market, same rulebook and the conclusion survives: Nepal Re is expensively rated for what it earns.

The catastrophe nobody has priced

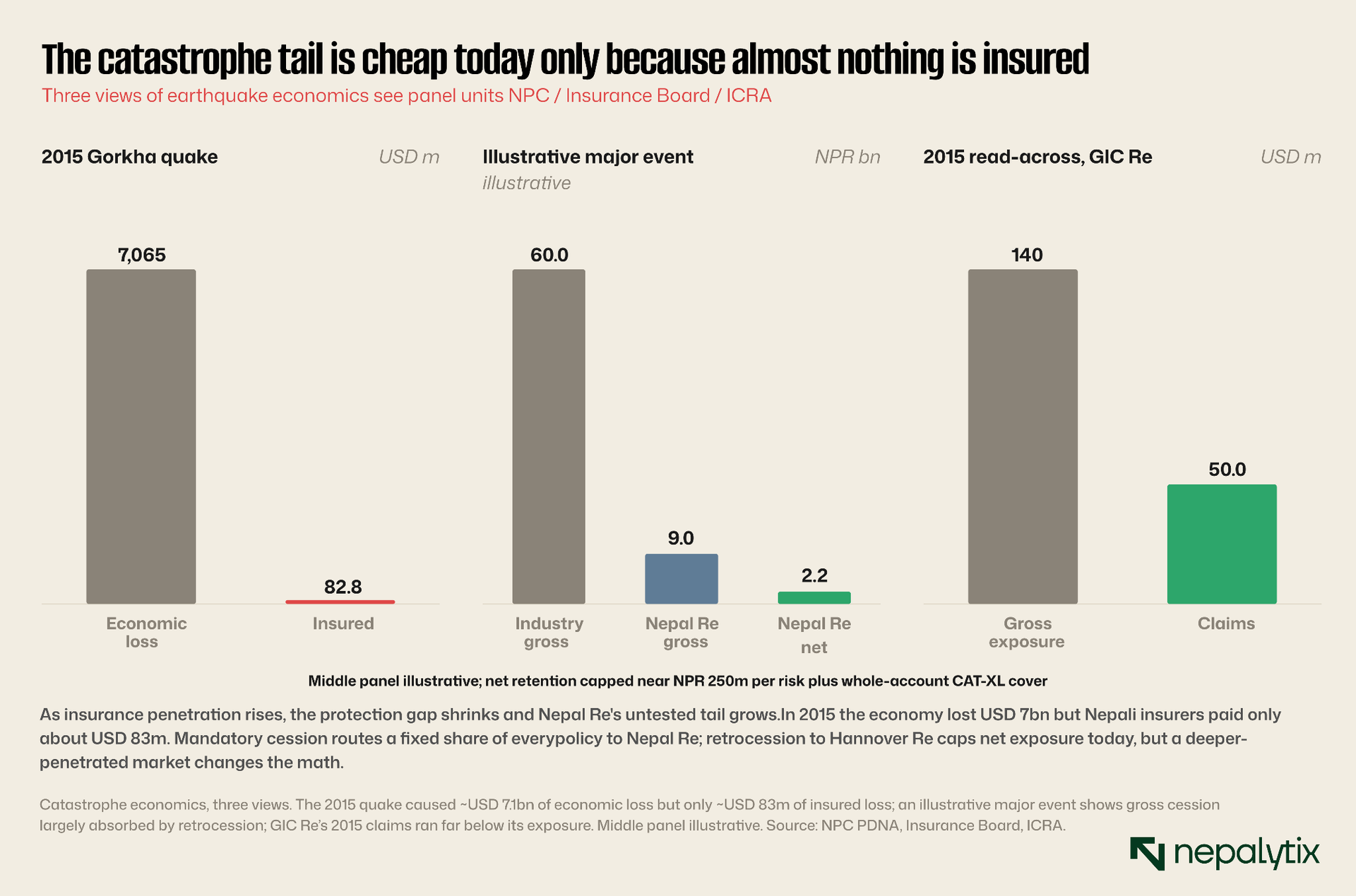

Every reinsurer is, at bottom, a bet that the catastrophe has not happened yet. For a Nepali reinsurer that bet is unusually live: the country sits on a major seismic boundary, and the 2015 Gorkha earthquake remains the reference event. What that event revealed about Nepal Re’s book is double-edged.

In 2015 the economy absorbed roughly USD 7.1bn of losses, of which Nepali insurers settled only about USD 83m of claims — barely 1%. Nepal’s insurance penetration was, and remains, low single digits of GDP. The paradox is that this protects Nepal Re today and threatens it tomorrow. Today, the mandated cession routes only a thin slice of a thinly-insured economy to the reinsurer, and a whole-account catastrophe excess-of-loss treaty with Hannover Re (AM Best A+) caps net retention at roughly Rs 250m per risk. The balance sheet is well shielded against a repeat of 2015 at 2015 penetration levels.

The catastrophe tail is cheap today only because almost nothing is insured. That will not stay true.

But the entire strategic logic of the sector and of the government’s mandatory-domestic-reinsurance push is to raise penetration. As more property is insured, more risk is ceded and the same earthquake produces a far larger claim against a reinsurer that is legally barred from declining the risk. Nepal Re’s catastrophe tail is untested, as ICRA repeatedly notes and its retrocession arrangements have not been stressed by a major domestic event since the company became a full-fledged reinsurer. The protection that looks comforting in today's book is a function of an under-insured economy that policy is explicitly trying to change.

Earthquake is the headline peril but not the only one. The 2024 monsoon brought severe flooding and landslides to the Kathmandu valley and beyond a reminder that climate-driven water risk is rising alongside seismic risk and that both feed the same mandatory-cession funnel. The variable that matters for valuation is penetration: Nepal’s premium-to-GDP ratio sits in the low single digits, far below regional peers, and every point of catch-up multiplies the absolute claims a fixed cession share routes to Nepal Re. The tail risk is paradoxically a direct function of the sector’s success. The better insurance does its job in Nepal, the more exposed its mandatory reinsurer becomes.

The retrocession architecture is the reason the tail looks manageable today, and it deserves description. Nepal Re lays off the top of its exposure through a whole-account catastrophe excess-of-loss programme led by Hannover Re, one of the strongest-rated reinsurers in the world, capping net retention per risk near Rs 250m. That structure converts an uncertain gross catastrophe loss into a bounded net number provided the programme holds, the limits are adequate to the event, and reinstatement cover is available after a first loss. Each proviso is a real risk in a severe, correlated event of the kind Nepal faces, and the cost of the cover ratchets higher after global catastrophe years regardless of Nepal Re’s own experience. The protection is genuine and well-placed; it is also a recurring expense and a dependency on counterparties whose appetite for Nepali risk is not guaranteed in perpetuity.

Capital, forced

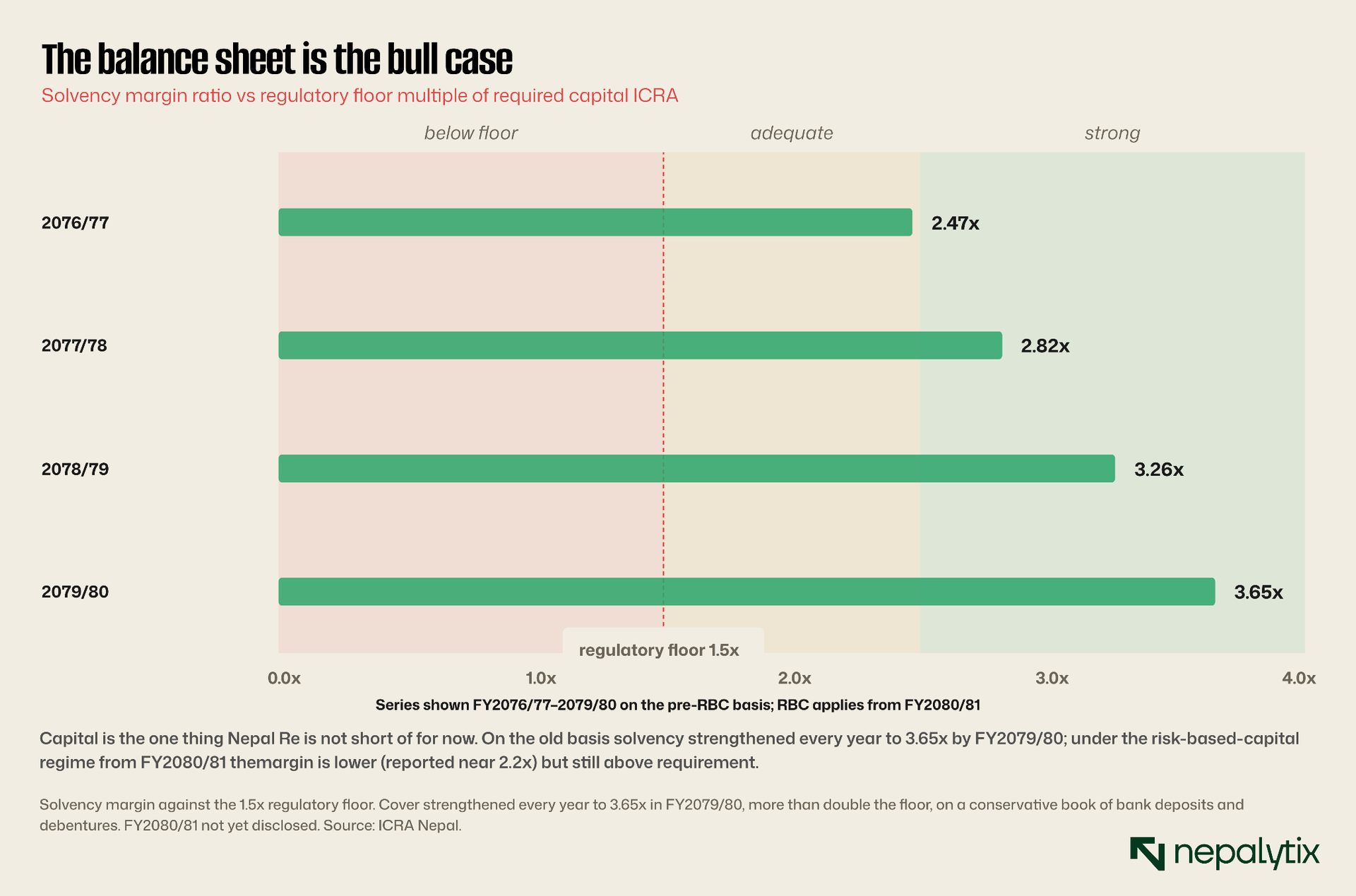

If the income statement is the bear case, the balance sheet is the bull case with an asterisk. Nepal Re is conservatively run and very well capitalised, and that is not a small thing in a frontier insurance market.

The solvency margin rose every year, reaching 3.65 times the regulatory requirement in FY2079/80 on the then-prevailing basis more than double the 1.5x floor, though under the risk-based-capital regime adopted from FY2080/81 the reported margin is lower, nearer 2.2x still above requirement. The investment book for all that it drives the earnings risk, is genuinely low-risk in credit terms: fixed deposits and debentures of Nepali banks, liquid and short with cash-to-technical-reserve cover above two times. There is no leverage problem here, no asset-quality time bomb, no aggressive reserving. For a creditor which is what the AA− rating speaks to Nepal Re is a comfortable credit.

The asterisk is that the strength is about to be enforced into a weakness for equity holders. The Rs 20bn paid-up mandate and the 1:1 rights issue will push capital well beyond what the current book can profitably employ. Solvency will rise further still toward levels that, for an equity investor, signal not prudence but trapped, under-earning capital. A balance sheet this strong on a return this low is capital looking for a use; the regulator’s answer is to add more of it.

There is a reading in which the capital build is value-accretive: a Rs 20bn base materially expands the net retention Nepal Re can prudently hold, lets it cede less premium abroad and gives the offshore ambitions the balance-sheet heft that wins mandates. That is the company’s case, and over a long horizon it is not unreasonable. The difficulty is timing and proof the capital arrives now, the returns on it are speculative and in the interim the larger denominator simply lowers ROE. The investor is being asked to pre-fund an option whose payoff depends on the same unproven offshore execution.

Government house

Governance at Nepal Re cannot be separated from its ownership. The Government of Nepal holds roughly 44%, with most of the remainder held by the domestic insurers that are required to cede to it, alongside life insurers, other public companies and the general public. Two of the six board seats, including the chair, are government nominees. This is the source of the franchise and of its conflicts.

The most obvious tension is structural: Nepal Re’s shareholders include the very insurers legally compelled to cede business to it. The cedants are also the owners. That alignment has worked in the company’s favour while cession terms were generous, but it places the board in the middle of every negotiation over cession rates, profit-sharing and the pace of the direct-cession phase-out negotiations in which the government’s interests as 44% owner, as fiscal beneficiary of dividends, and as regulator are not obviously the same.

The mandatory-domestic-reinsurance regime has itself become a governance question for the sector. Industry participants have publicly alleged that the 2080 directive which forces full domestic cession of several lines and bars reinsurers from refusing risk was shaped to benefit the newly-arrived private reinsurer and have warned that concentrating the nation’s catastrophe risk in two domestic balance sheets undermines diversification. Whatever the merits, the episode underlines the central fact for an equity holder: Nepal Re’s economics are set less in its underwriting room than in the regulator’s. Incremental regulatory change is the dominant variable, and it is outside the company’s control.

Related-party dynamics run through the everyday business, too. Nepal Re both reinsures and is part-owned by the same insurers, sets commission and profit-sharing terms with them, and negotiates the RSMDST arrangements that drove last year’s earnings mix all within a structure that blends regulator, owner and counterparty. Disclosure around these dealings is thinner than a global reinsurer’s, and board independence is structurally limited by the government’s nominee seats. For an equity holder this is less a red flag than a permanent discount factor: decisions that move earnings are taken in a room where the company’s interests and its owners’ are not cleanly separable.

The people and the process round out the picture. The board is chaired by a government nominee, with the chief executive running a lean organisation of roughly sixty-five staff against a Rs 123bn market capitalisation, a ratio that captures how much of the business is mandated flow rather than originated underwriting. A thin headcount is efficient but it also implies limited in-house catastrophe modelling, actuarial depth and offshore-underwriting capability relative to the global names Nepal Re meets abroad. For a company whose strategy increasingly depends on writing risk that is not handed by regulation, the institutional capacity to price that risk is itself a question mark.

What it’s worth

Which brings the analysis to the valuation, where the gap between what Nepal Re is and what it costs is at its widest. The relevant metric for a reinsurer is price-to-book, not price-to-earnings; on that measure Nepal Re trades at 6.0 times. The same number for its peers is the heart of the matter.

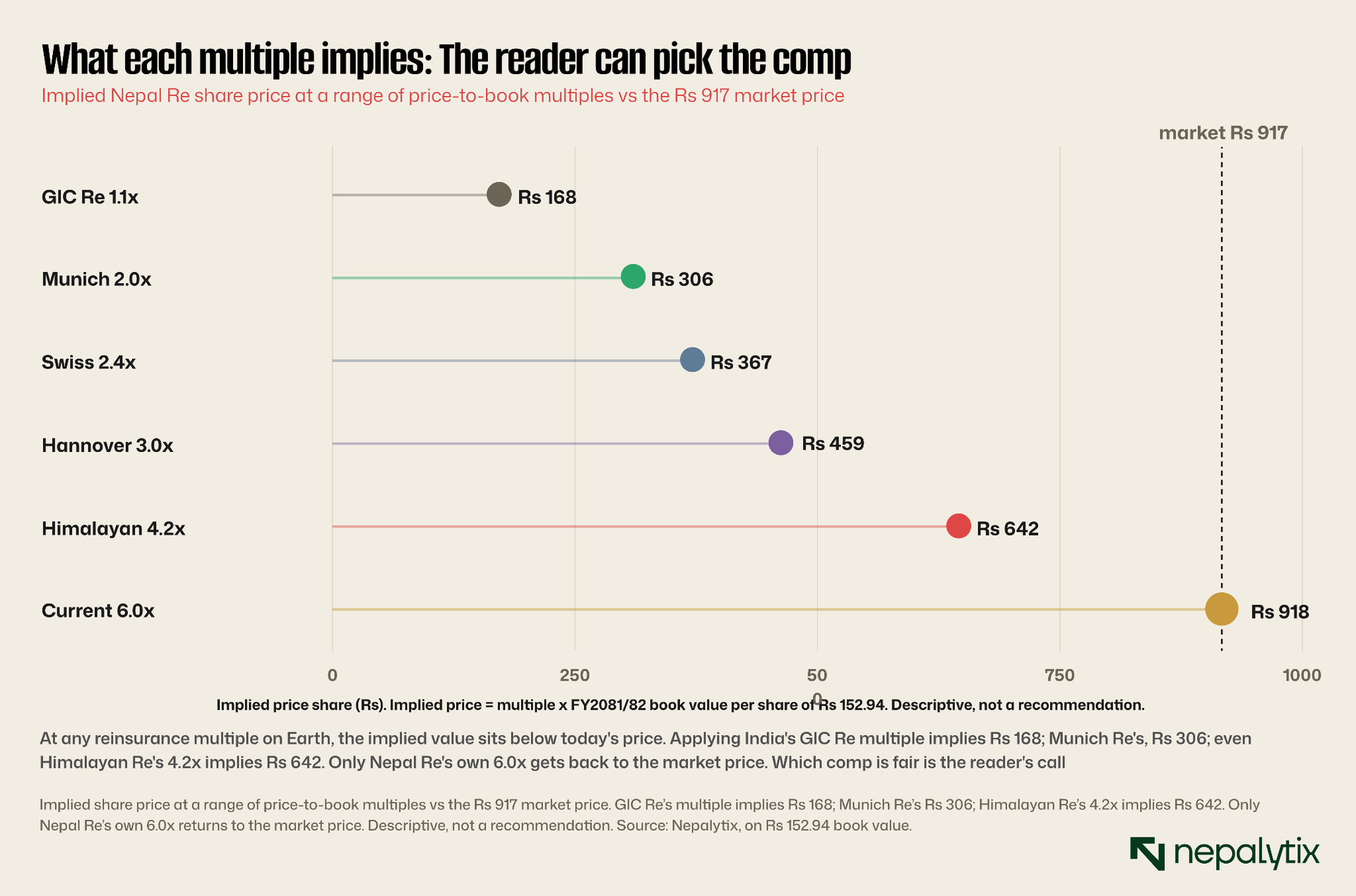

GIC Re the government-owned, investment-carried, single-digit-ROE Indian reinsurer that most closely mirrors Nepal Re’s actual business trades at 1.1 times book. Munich Re, with more than double Nepal Re’s ROE and a vastly superior combined ratio, fetches 2.0 times. Hannover Re, 3.0 times. Himalayan Re, the direct domestic equivalent of the identical rulebook, 4.2 times. Nepal Re sits at 6.0 times roughly twice the top of the global reinsurer range and more than five times its closest structural analogue. The premium is not explained by returns, underwriting quality, or growth, all of which are inferior to the peers trading at a fraction of the multiple.

Translating those multiples into a price on Nepal Re’s Rs 152.94 of book value per share is mechanical. India’s GIC Re multiple implies Rs 168 a share; Munich Re’s implies Rs 306; Hannover Re’s Rs 459 even Himalayan Re’s 4.2 times implies Rs 642. Only Nepal Re’s own 6.0 times returns to anything near the Rs 917 market price. Which of those comparables is the fair reference is a judgement the reader is better placed to make than we are but the ladder makes plain that the market is paying the single highest multiple in the peer set.

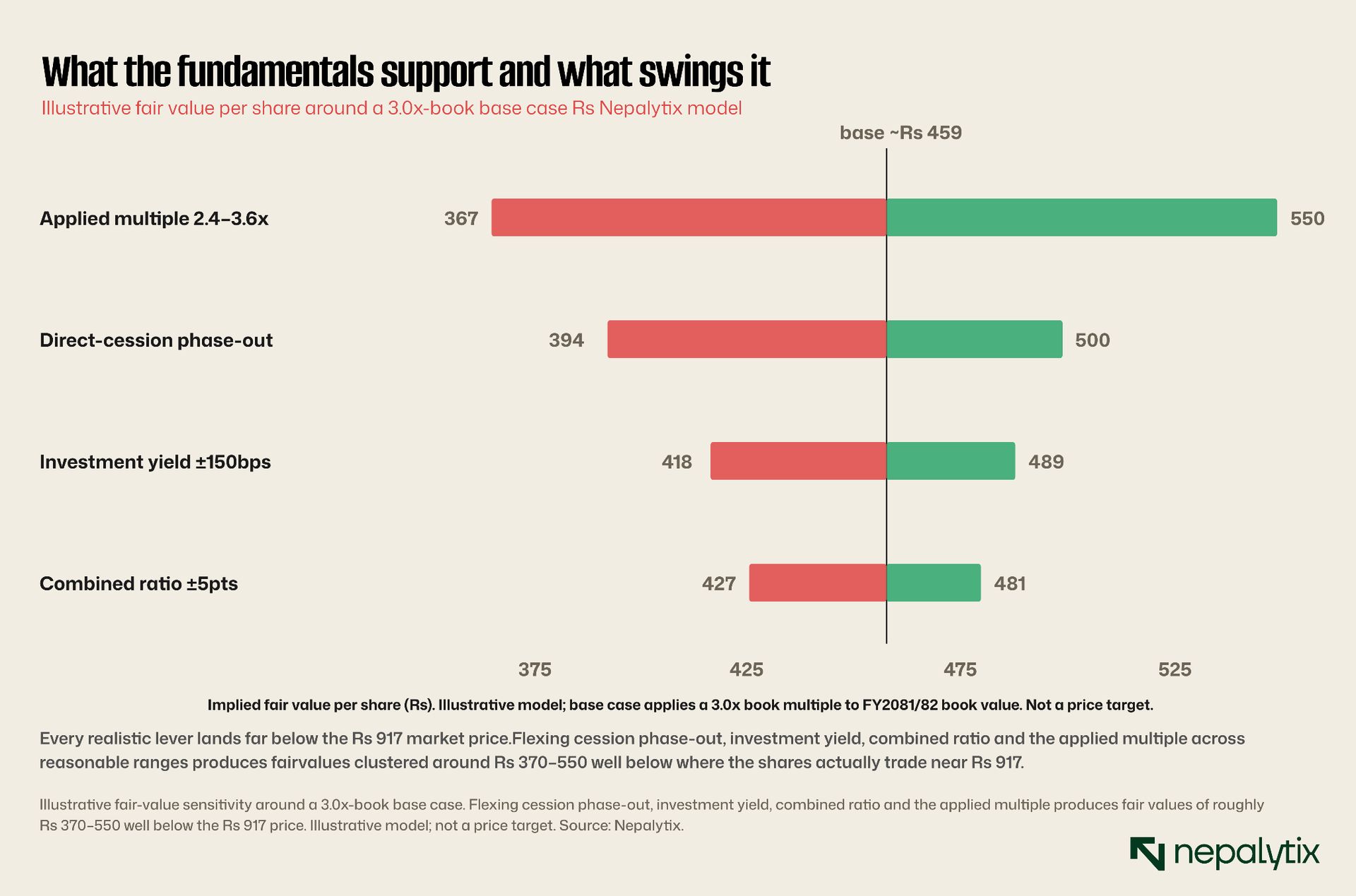

Sensitivity analysis does not rescue the gap. Anchoring to a 3.0x book multiple a premium to GIC Re for sovereignty and the RSMDST monopoly, in line with global reinsurers despite weaker fundamentals and flexing the cession phase-out, the investment yield, the combined ratio and the applied multiple across reasonable ranges produces fair values clustered between roughly Rs 280 and Rs 420. The market price sits at more than double the top of that range. For the valuation to be justified, one must believe either that the regulatory subsidy will be preserved rather than withdrawn, or that NEPSE’s structural scarcity premium on a small, retail-driven market with little float will persist indefinitely.

A word on why price-to-earnings is the wrong lens and why we lean on books. Nepal Re’s trailing P/E near 119 looks absurd, but it is distorted by a depressed-earnings year rather than informative; reinsurance earnings are too volatile and too tied to the investment cycle for an earnings multiple to carry much meaning. Book value is the disciplined anchor it is what the regulator capitalises, what solvency is measured against and what the peer set is consistently valued on. Embedded value, the other insurance yardstick, Nepal Re does not disclose, itself a gap against the global names. On the metric that travels across the peer set, the verdict holds before any argument about the right multiple.

The view

Our reading of Nepal Re is that it is two companies wearing one share price. The first is a sovereign-backed, fortress-capitalised institution with a real monopoly on RSMDST risk, an AA− credit profile, and a conservative balance sheet that would survive a repeat of 2015 comfortably. The second is a sub-7%-return investment vehicle whose underwriting is a coin-toss, whose most profitable regulatory subsidy is being legislated away on a published schedule, whose capital is being force-grown in a way that dilutes returns further, and whose catastrophe tail is untested and structurally growing as penetration rises.

The bull case is coherent: the RSMDST monopoly is durable and growing; sovereign ownership keeps the franchise and the rating intact; the balance sheet can absorb shocks; and a deepening, better-penetrated insurance market lifts the whole sector’s premium over time. The bear case is equally coherent and, on the current numbers, better supported: returns have not improved in five years and are about to be diluted, the subsidy is on a withdrawal timetable, the investment yield that carries the P&L is falling, and the shares trade at a multiple that no reinsurer’s fundamentals on the planet support least of all these.

Two companies wearing one share price: a fortress balance sheet, and a sub-7%-return book the market values like a compounder.

The base case sits between the two and closer to the bear: a serviceable, well-capitalised reinsurer earning a single-digit return on a captive book, worth a premium to GIC Re for its sovereignty and its one true monopoly, but nothing like the premium the market currently assigns. The key risks run in both directions a regulatory reprieve on cession or a hard reinsurance pricing cycle could lift returns; a major domestic catastrophe, a faster cession phase-out, or further forced capital would compress them. The catalysts to watch are concrete and near-dated: completion and pricing of the rights issue, the FY2081/82 audited results and any disclosure on the combined ratio and solvency post-raise, the NIA’s next move on the cession schedule, and the government’s dividend posture as 44% owner.

To put rough numbers on the three cases, without dignifying them as targets: a bear outcome accelerated cession phase-out, a soft investment cycle, dilution landing with no offsetting return leaves the fundamentals near the Rs 367—459 the model implies at 2.4—3.0x book. A base case that credits the sovereignty and RSMDST premium might stretch toward the Rs 459—642 Hannover-to-Himalayan range. A bull case in which the subsidy is preserved, offshore scales and the scarcity premium holds is the only path defending a price near today’s Rs 917 and it requires several independent things to go right at once. The asymmetry is the point.

For the reader tracking the name, the near-term calendar is concrete. The rights issue’s completion and take-up rate will set the post-raise share count and diluted book value. The FY2081/82 audited accounts in particular the combined ratio, the investment yield and the post-raise solvency margin will show whether the underwriting has stabilised or the loss line has swung again. The NIA’s next directive on the cession schedule is the single largest swing factor, capable of either extending the subsidy or accelerating its withdrawal. And the government’s dividend decision, as 44% owner balancing fiscal needs against the capital build, will signal how it intends to treat minority holders. None of these requires a rating to interpret; each moves the fundamentals the reader can already see.

We initiate coverage without a rating and without a recommendation, which is deliberate. The fundamentals are laid out in full above; so is the valuation. The distance between a 6.0-times-book price and a sub-7% return on equity is the entire investment question and it is one a reader can weigh as well as we can. Our job here is to make sure the gap is impossible to miss.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.