Muktinath Bank is Winning Every Metric. So Why Isn't the Stock?

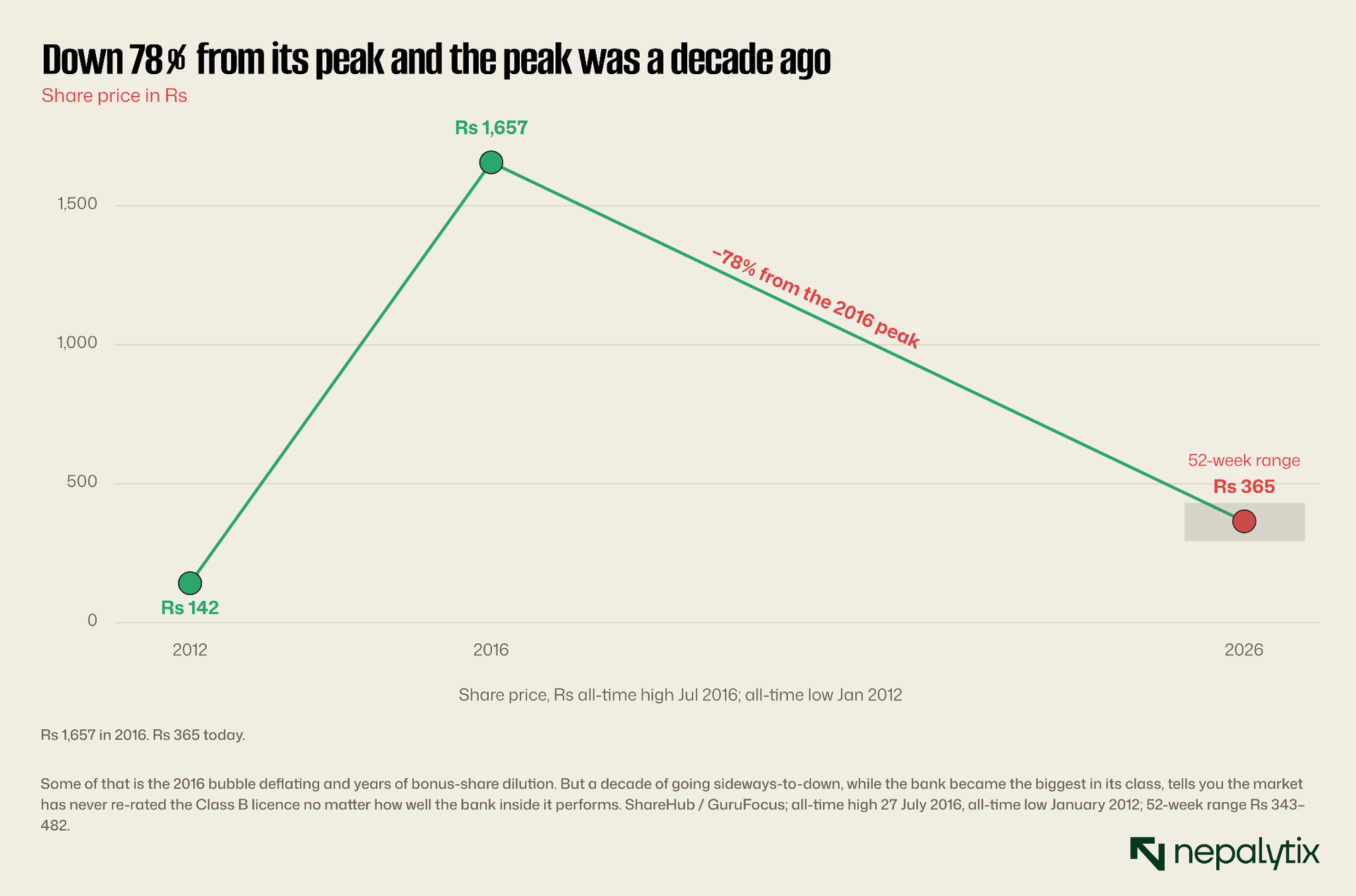

Muktinath Bikas Bank has become Nepal's largest and most profitable development bank, yet its share price remains nearly 78% below its 2016 peak.

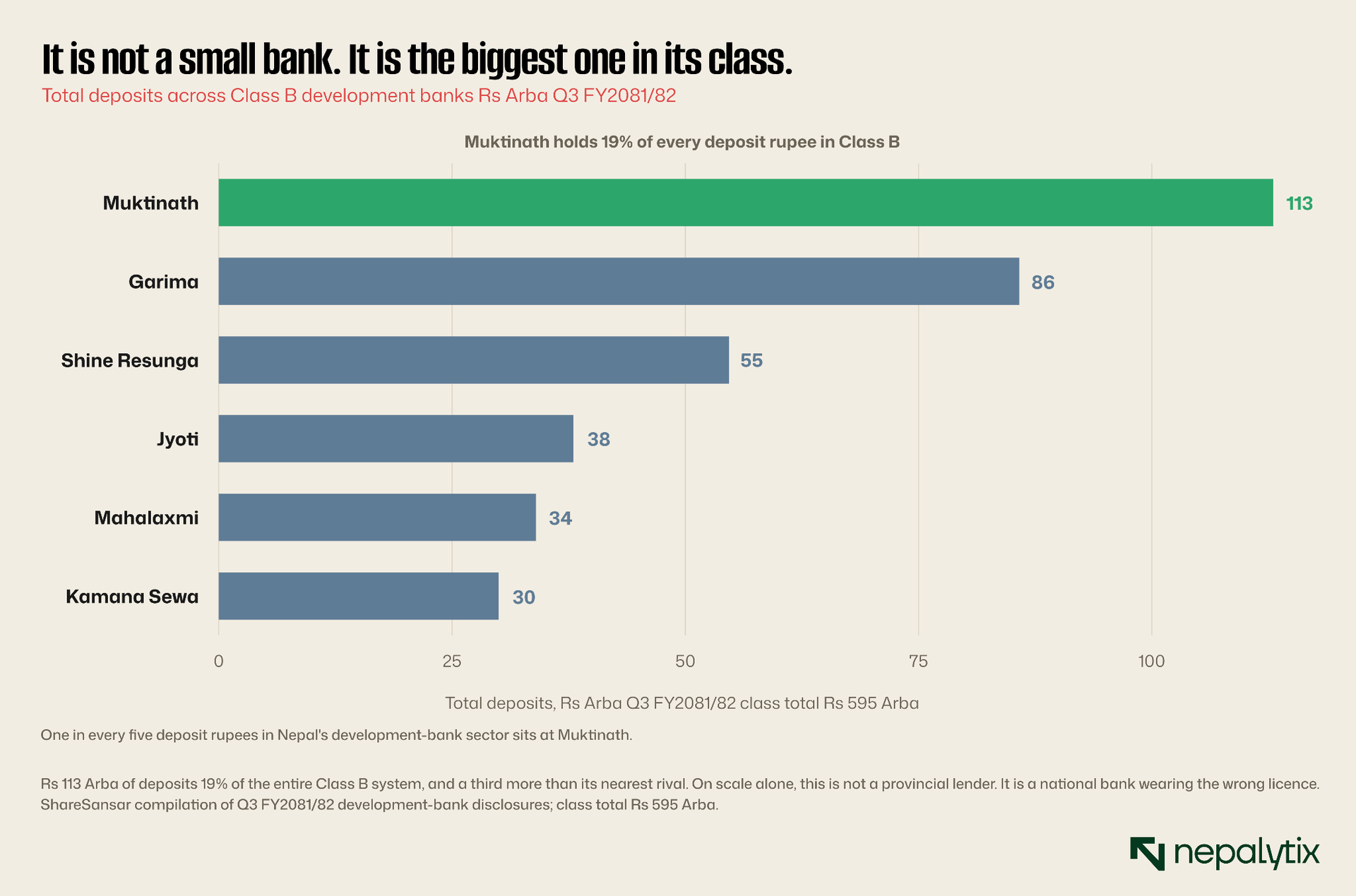

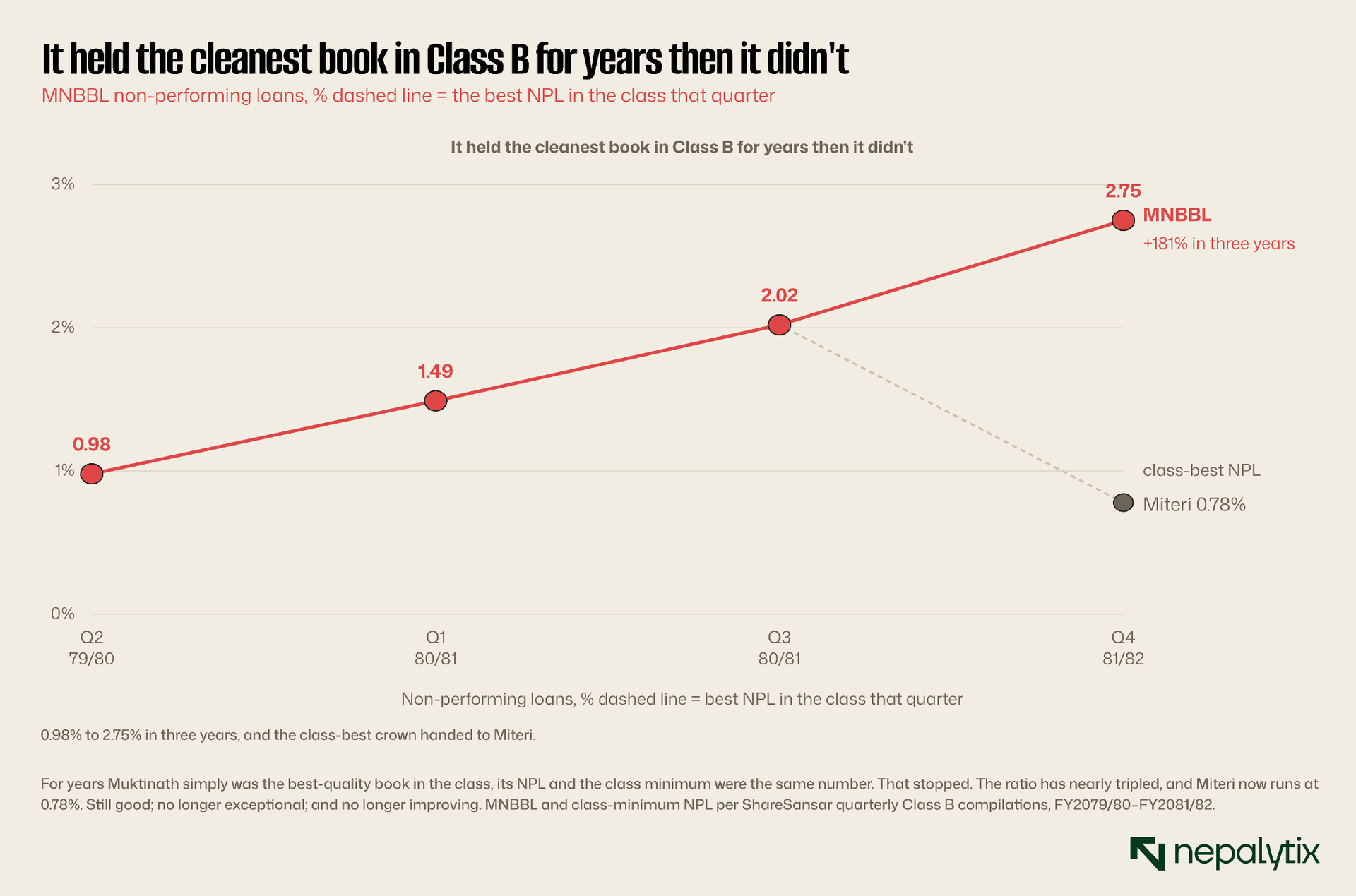

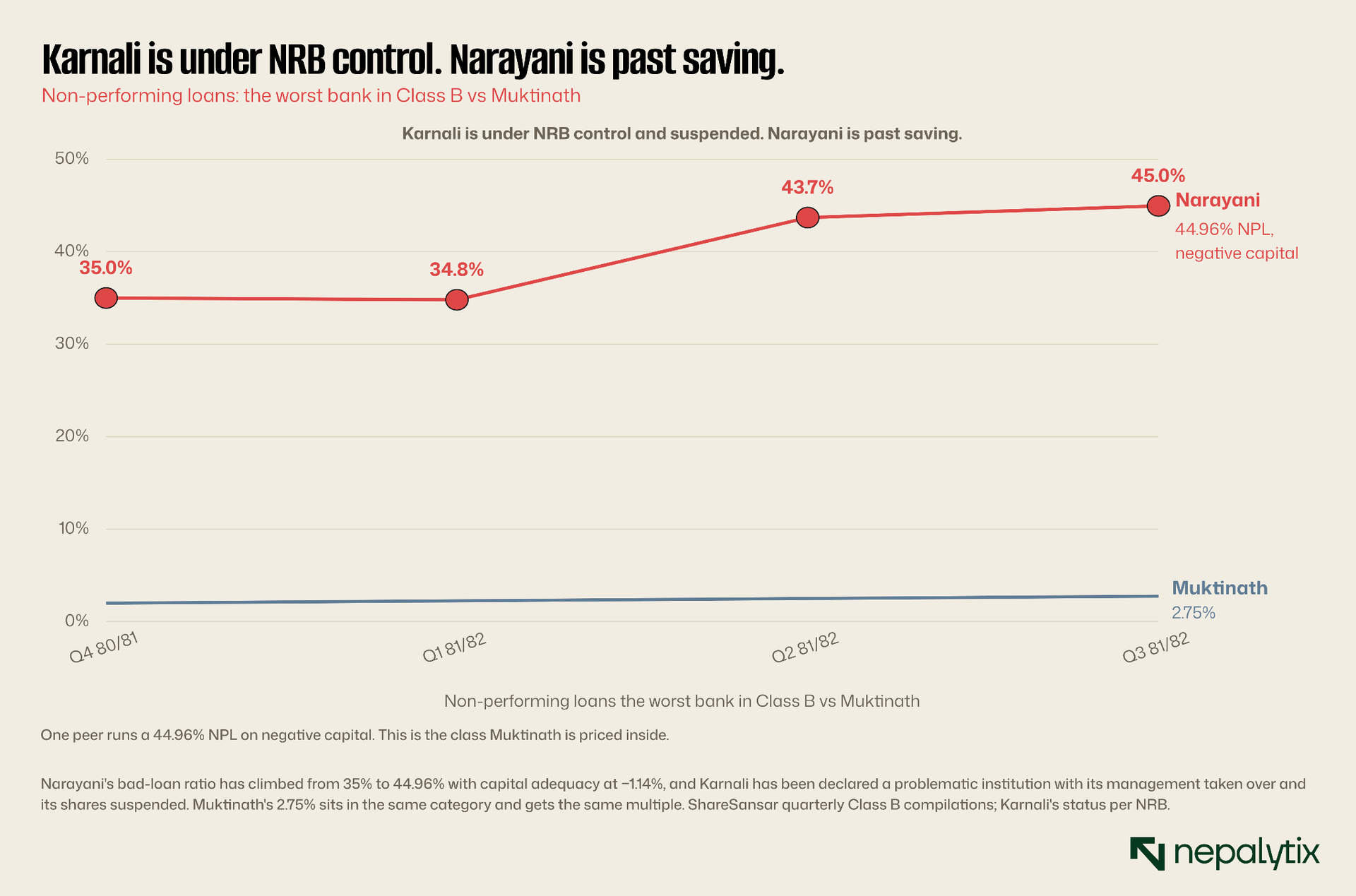

Muktinath Bikas Bank is, by almost every measure that matters, the finest institution in its category in Nepal. It holds more deposits than any other development bank Rs 1.17 Kharba, roughly one in every five rupees in the entire Class B system. It lends more. It earns more net interest income. It holds the largest paid-up capital. In FY2081/82 it became the first development bank in the country's history to post a net profit above Rs 1.5 Arba. Its non-performing loan ratio, at 2.75%, is among the cleanest in a class where one peer is running a 44.96% NPL on negative capital.

And the market pays 16.7 times earnings for it.

That is the puzzle this note exists to solve. A bank this dominant, this profitable and this clean should not be one of the cheapest names in its own sector. The stock trades at Rs 365, down 78% from the Rs 1,657 it touched in 2016, a decade in which the bank grew into the largest of its kind and the share price went nowhere. Something is being priced here, and it is not the bank's operating performance.

Our conclusion, stated up front: what the market is discounting is not Muktinath. It is the licence. Muktinath is a national bank trapped inside a Class B development-bank charter, a category that is being squeezed out of existence from both directions, and which the regulator has spent a decade consolidating away. The bank has outgrown its own legal box and until that box changes, no amount of operational excellence will get it re-rated. That makes this a stock about a structural event not a quarterly result and it means the analysis has to be about the licence not just the ledger.

How Muktinath actually makes money

Before the analysis, the business because Muktinath is not a generic bank and the shape of its franchise explains both its strengths and its ceiling.

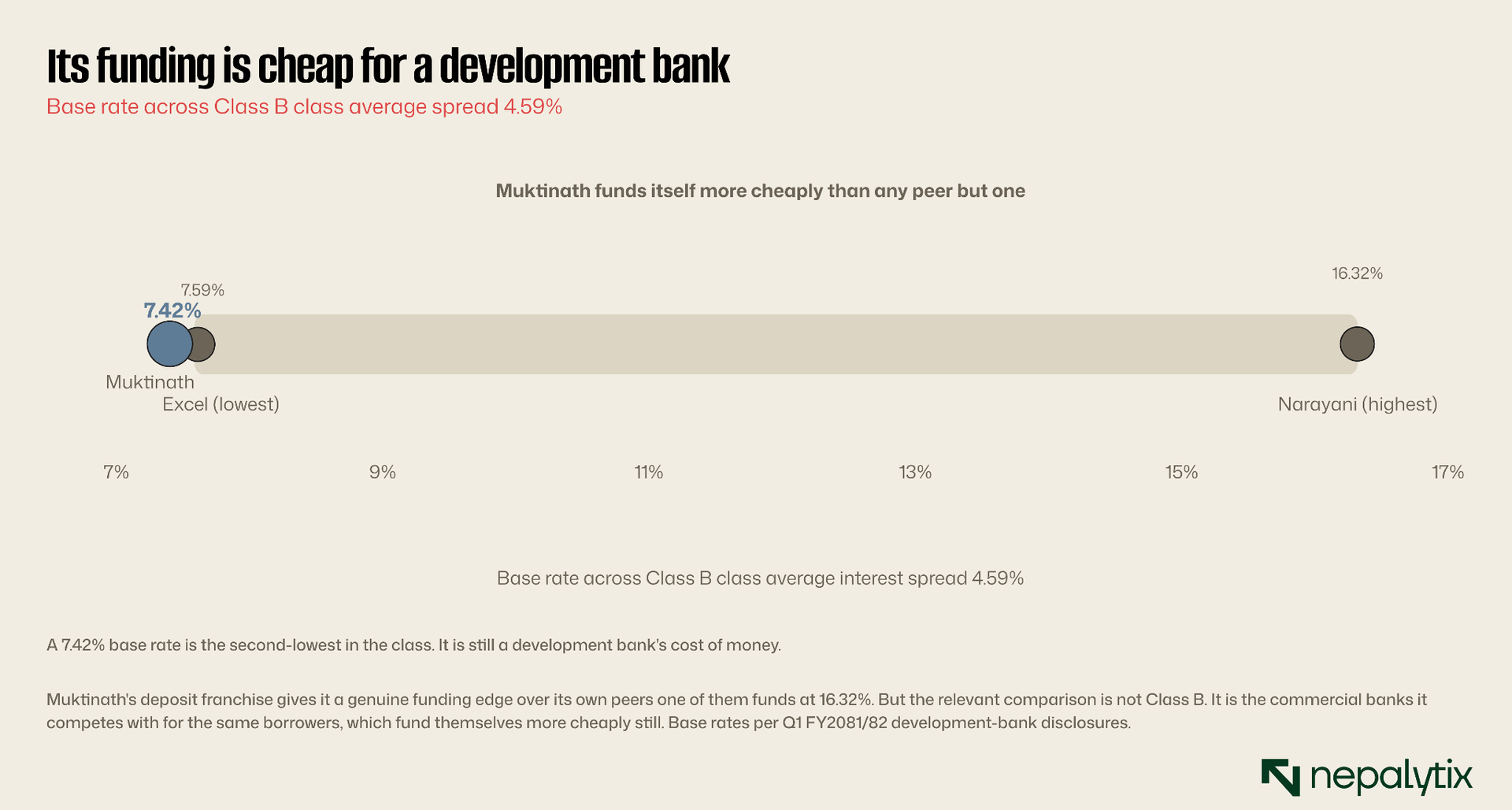

The bank was founded in Pokhara and grew out of the western hills and that origin still defines it. It reports through three segments: Modern Banking, Small and Micro Banking and Treasury Operations. The bulk of the revenue comes from the banking segments, the classic spread business of taking deposits at one rate and lending at a higher one. Muktinath's base rate is 7.42%, and the class-average interest spread is 4.59%; that spread, multiplied across a Rs 97.52 Arba loan book, is the engine.

What distinguishes it from a commercial bank is the customer. Muktinath's franchise is built on small-and-micro banking individual savers, small businesses, agriculture, hire-purchase and the semi-urban borrowers the big Kathmandu banks have historically ignored. This is a granular, high-touch, branch-heavy model. It is expensive to run and slow to build but it produces two things a commercial bank struggles to buy: sticky retail deposits and a borrower who is not being courted by five other lenders.

That is the whole basis of the bank's unusual position. Its deposits are stickier than a wholesale-funded lender's which is why it funds at 7.42% while a peer funds at 16.32%. And its borrowers are real which is why uniquely in a system with a liquidity glut, it has actually lent out 88% of what it holds. The franchise works.

The limit is equally structural. A granular retail bank grows deposits slowly, one customer and one branch at a time. Muktinath cannot conjure a Rs 20 Arba deposit inflow the way a commercial bank can by winning a single institutional mandate. So the thing that makes its funding good retail granularity is the same thing that makes its funding slow. Hold that thought, because it collides directly with the credit-to-deposit ceiling in the next chapter.

Muktinath also runs a capital-markets arm, Muktinath Capital, active as an issue and sales manager of a small, fee-based, capital-light income stream that does not depend on the interest cycle. It is not material to the valuation today, but it is the kind of business a bank builds when it is thinking about what it wants to be next.

The number that defines the bank

Before anything else, look at one ratio because it inverts everything you think you know about Nepali banking right now.

Nepal's banking system is drowning in money it cannot lend. The credit-to-deposit ratio across the system sits at 74.32% against a regulatory cap of 90%, nearly sixteen points of unused lending capacity because businesses have stopped borrowing. The interbank rate has fallen below the floor of the central bank's own corridor. This is a liquidity glut and we have written about it at length.

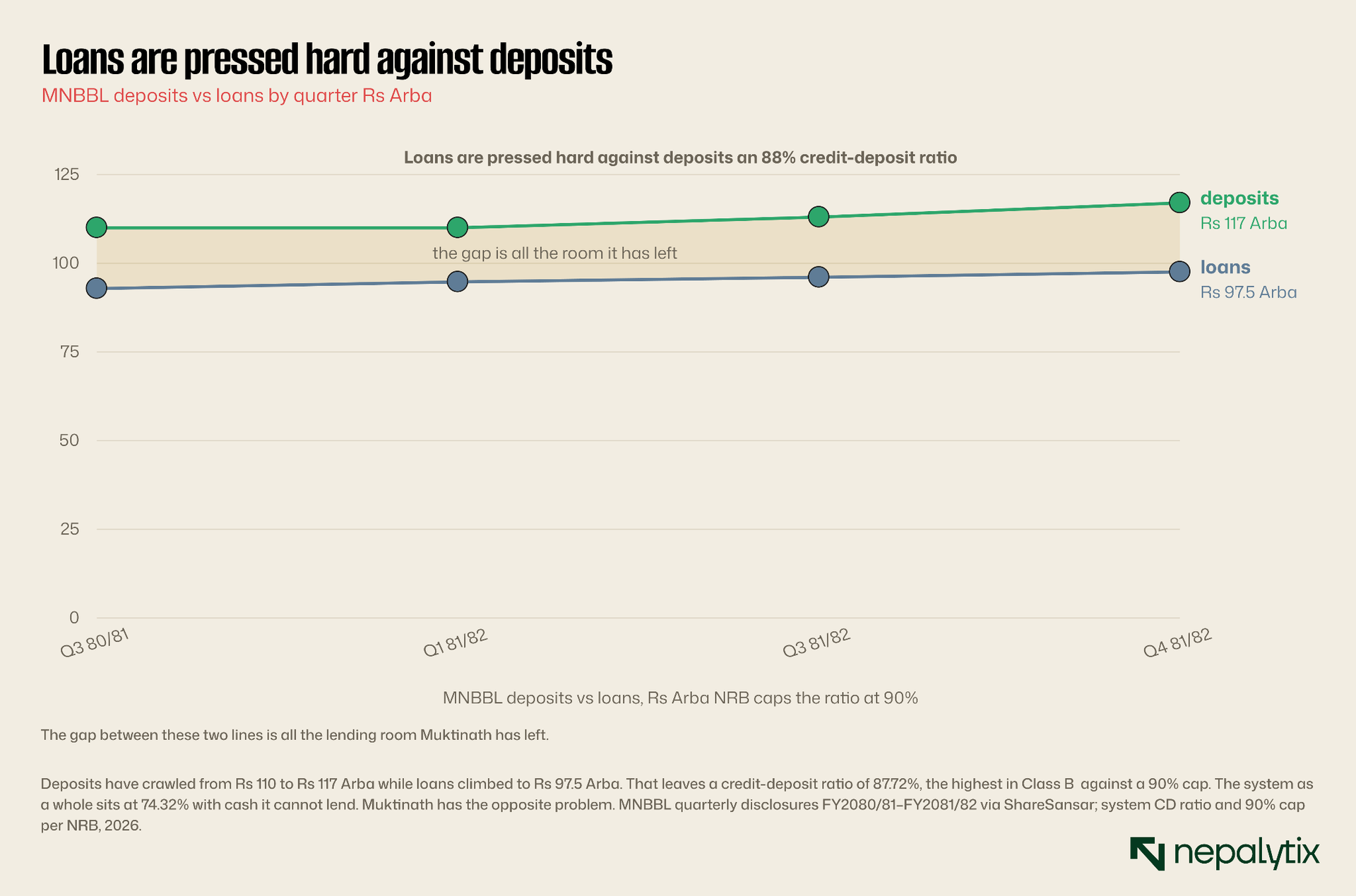

Muktinath's credit-to-deposit ratio is 87.72%, the highest of any development bank in the country.

Sit with that for a moment because it reframes the whole investment case. While the commercial banks are begging for borrowers and parking cash overnight at 2.75%, Muktinath has already lent out nearly everything it has. It has roughly 2.3 percentage points of headroom before it hits the cap. It is not suffering from an absence of demand. It is constrained by the supply of deposits.

The rest of the banking system cannot find borrowers. Muktinath cannot find deposits. Those are opposite problems, and they demand opposite solutions.

This tells you two things. The first is genuinely bullish: Muktinath's loan book is not the product of a desperate scramble for assets. Where the system has spare capacity and no demand, Muktinath has demand and no capacity for a lending franchise with real, live borrowers behind it. In a market where credit growth has stalled, that is a scarce and valuable thing.

The second is a hard constraint. A bank that has already lent 88% of its deposits cannot grow its loan book by lending more of what it has. To grow, it must gather deposits and deposits are the one thing a Class B development bank is structurally worse at raising than the commercial banks it competes with. Growth from here is not a decision management can simply take. It is gated.

The record year, and what actually produced it

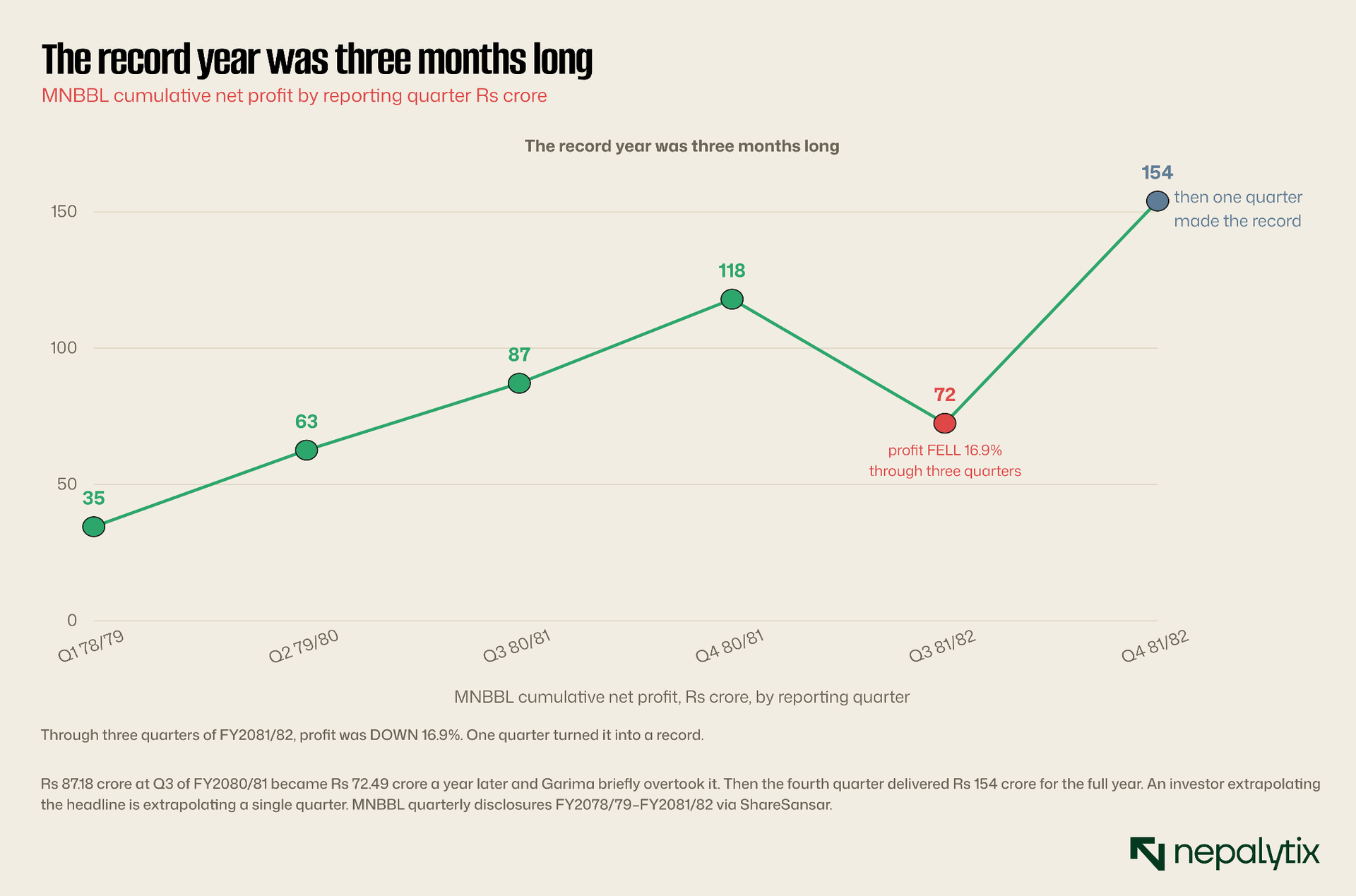

FY2081/82 was, by the headline, the best year any development bank in Nepal has ever had. Net profit of Rs 1.54 Arba, up 30.7%. Operating profit up 30.55%. Retained earnings up more than 650%. Deposits at Rs 1.17 Kharba, loans at Rs 97.52 Arba. EPS of Rs 21.82, net worth per share of Rs 169.95.

Now decompose it because the composition matters more than the total and because the same force is moving through every bank in the class at once.

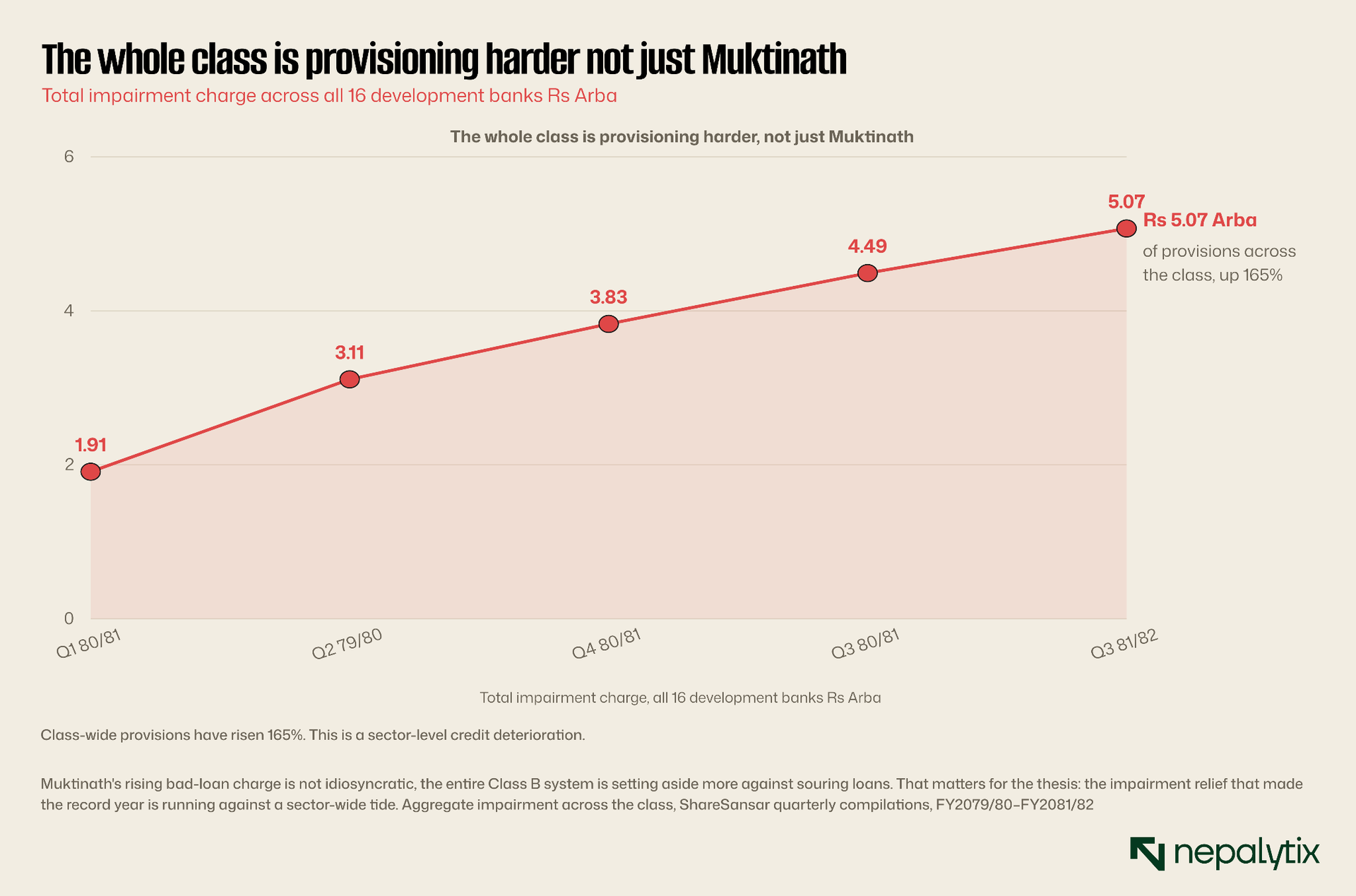

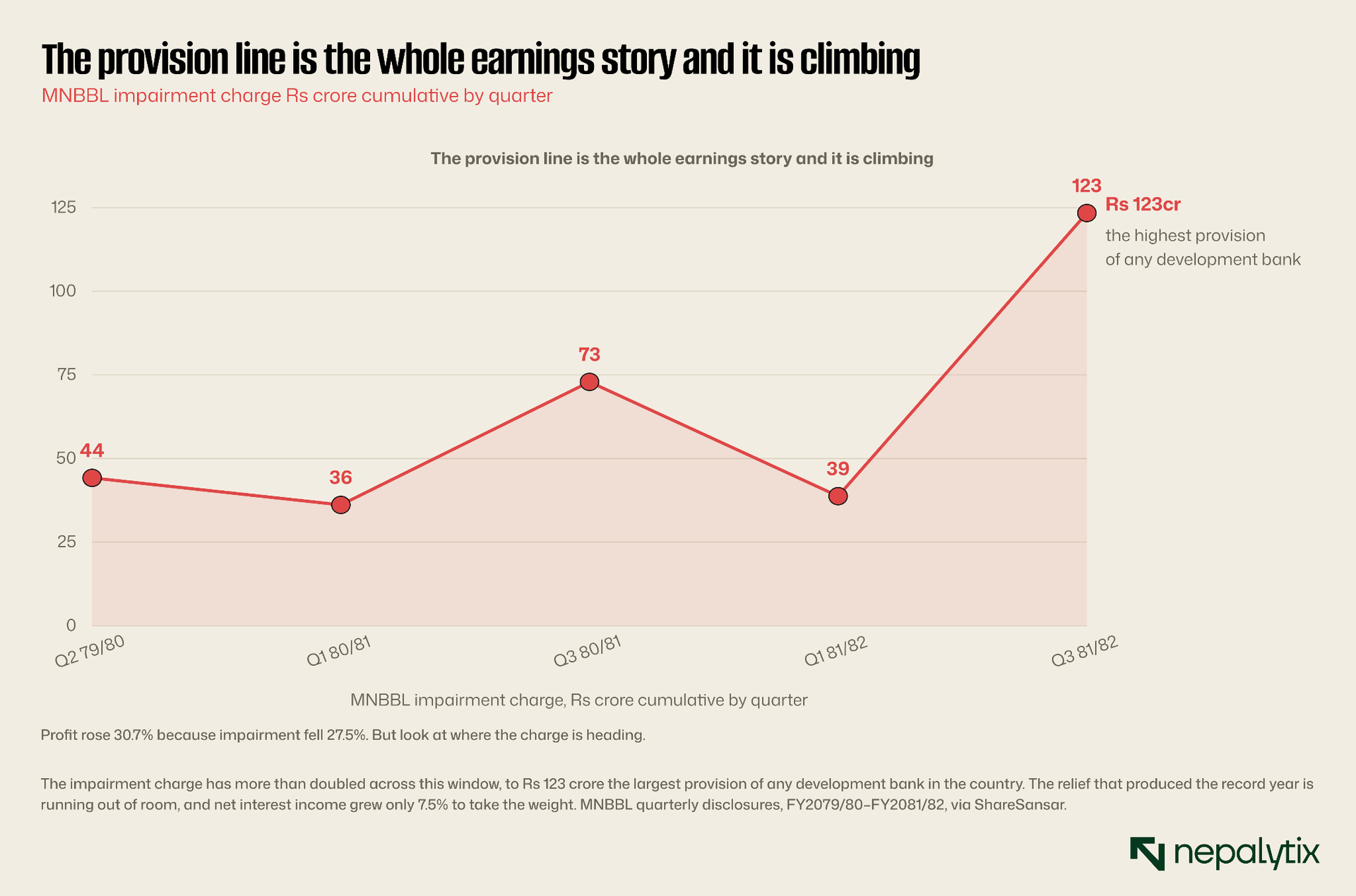

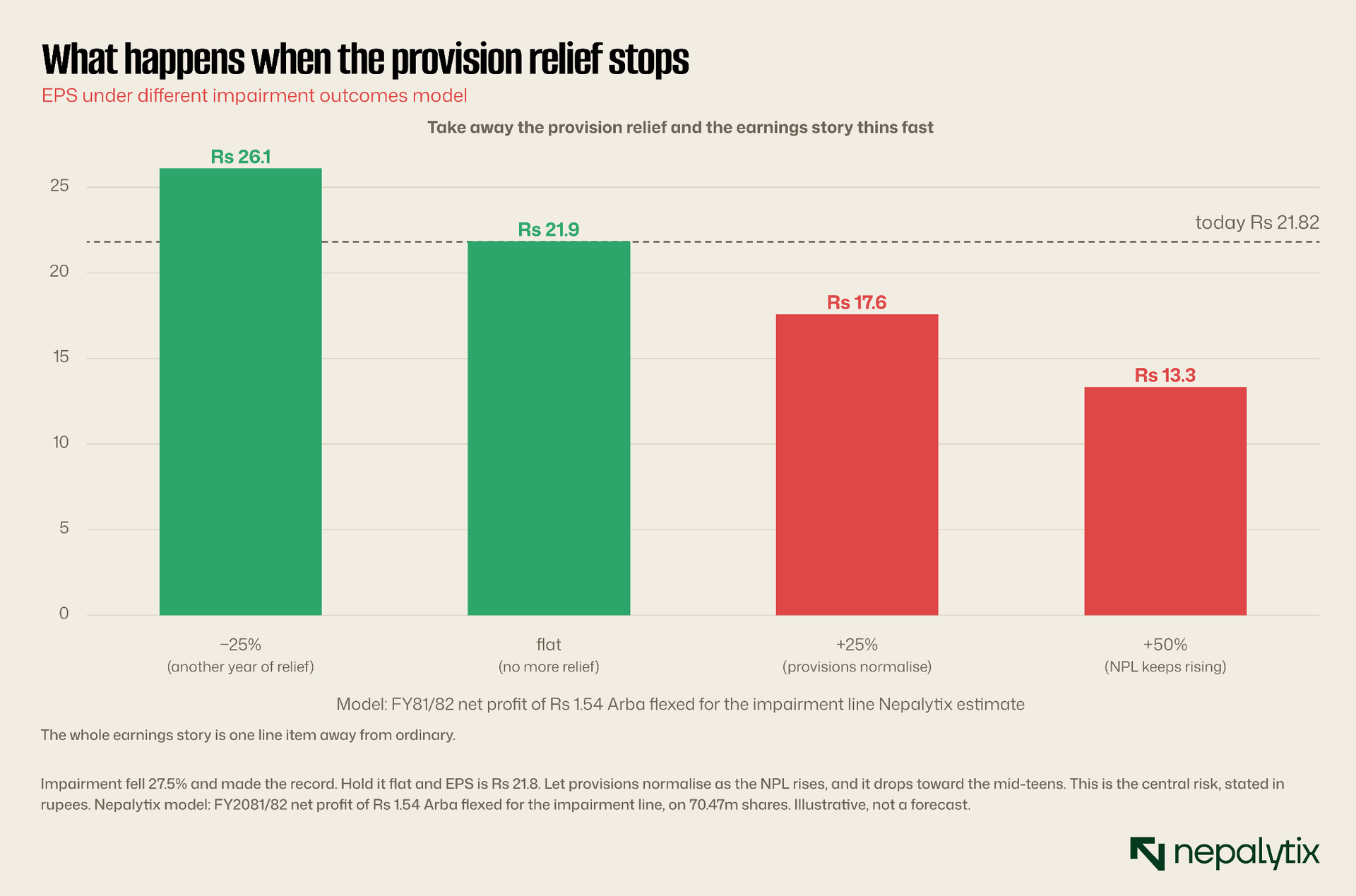

Net interest income which is what the bank actually earns from lending money grew 7.5%. Net profit grew 30.7%. The overwhelming majority of the growth came from the impairment charge falling 27.52%. That is not new lending, new customers or a wider margin. It is a smaller provision against bad loans, dropping straight to the bottom line.

To be clear, this is a legitimate result and not an accounting trick. Provisions fall when recoveries improve and the book behaves. But it is a one-off, in a way that net interest income is not. Impairment cannot fall 27% every year forever; at some point it hits a floor and then the bank's profit growth has to come from the 7.5% engine rather than the 27.5% tailwind.

And the quarterly path makes this uncomfortable rather than merely academic.

Through three quarters of FY2081/82, Muktinath's profit was not up 30%. It was down 16.9% from Rs 87.18 crore to Rs 72.49 crore and Garima Bikas Bank had briefly overtaken it as the sector's most profitable name. The entire record year was made in the final three months on the back of the provision release.

An investor buying today on the strength of a Rs 1.54 Arba headline should understand exactly what they are extrapolating: not a durable 30% growth engine but a strong fourth quarter powered by a line item that has already done most of its falling.

The credit book: genuinely good and turning

The asset quality is where Muktinath earns its reputation and it deserves the credit.

A 2.75% non-performing loan ratio, in a Nepali financial system where microfinance is running above 11% and one Class B peer is at 44.96% on negative capital, is a genuinely strong result. It reflects a real underwriting culture and a borrower base heavily rooted in the bank's Pokhara and western-region franchise, and in small-and-micro banking that has held up.

But the trend is the point. A year earlier that ratio was 2.02%. It has risen by more than a third. It is still the best in its class, and it is still moving in the wrong direction which matters enormously, because the impairment relief that produced the record year cannot coexist indefinitely with a rising bad-loan rate. Those two facts are in tension and the tension resolves in the provision line.

Capital is the caveat. A 12.99% capital-adequacy ratio clears the regulatory minimum comfortably but it is not a fortress. Smaller, more conservative peers hold far more. Combine an ordinary capital buffer with an 87.72% credit-to-deposit ratio and you have a bank that is running close to both of its constraints at once: little spare lending capacity and little spare capital to absorb a shock if the NPL keeps climbing.

One further observation about the credit book, because it is the bank's most defensible asset. A 2.75% NPL is not achieved by luck. It is the output of a lending culture, small tickets, local knowledge, relationship underwriting and a branch manager who knows the borrower. That culture is slow to build and almost impossible to buy which is why it is the single hardest thing for a commercial-bank acquirer to replicate and the single most valuable thing they would be paying for.

It also explains why the bank has borrowers when the rest of the system does not. The commercial banks' liquidity glut is, in part, a story about credit standards: they will not lend to the borrowers who want money, and the borrowers they want will not borrow. Muktinath's segment small business, agriculture, hire-purchase, the semi-urban middle never stopped needing capital. The bank is lent out at 88% because its customers still show up. In a stalled credit market, that is not a small thing; it is proof that the franchise is real rather than a legacy of easier times.

The funding edge and its limit

Muktinath's competitive advantage inside its class is its deposit franchise. It funds itself at a base rate of 7.42%, the second-lowest of any development bank against a peer that funds at 16.32%.

Within Class B, this is a decisive advantage and it explains much of the bank's dominance: cheaper deposits mean a wider spread, which means more profit per rupee lent, which funds the branch network that gathers more deposits. That flywheel is why Muktinath is the biggest.

But the flywheel has an outer wall. Muktinath does not primarily compete with other development banks for its best customers, it competes with commercial banks which fund themselves more cheaply still, carry bigger balance sheets and can offer products a Class B licence does not permit. As the bank grows into larger customers, it runs into rivals with a structurally lower cost of money. Its funding edge is real, and it is bound by the licence.

The licence is the whole story

Which brings us to what the market is actually pricing, and why a bank this good is this cheap.

Nepal's Class B development banks were created to fill a gap: regional, mid-market, semi-urban lending that commercial banks would not do. That gap has been closing from both sides for a decade. Commercial banks came down-market, armed with cheaper funding and bigger balance sheets. Microfinance came up-market, chasing yield. The development bank has been left in the middle worse funding than a Class A, worse margins than a Class D and the regulator has spent years merging the category down.

It is worth understanding how Class B got here because the trajectory is the argument.

The development-bank category was a creation of Nepal's financial liberalisation; dozens of institutions licensed to serve regions and customers the commercial banks would not. At its peak the class was crowded with small, thinly-capitalised regional lenders. Then the central bank began raising paid-up capital requirements and encouraging mergers and the category began to contract: dozens became a few tens and the survivors got bigger. Muktinath is what winning that contest looks like, the last institution standing at the top of a class that has been steadily shrinking beneath it.

But winning a shrinking category is a strange prize. The regulator's direction of travel has been consistent for a decade and is unambiguous today: fewer, stronger, larger institutions, with merger preferred to incremental capital. Every year the Class B licence looks less like a permanent category and more like a waiting room. And the market, which has watched this for ten years, prices it accordingly.

Muktinath has outgrown its own charter. Until the charter changes, the excellence does not get paid for.

Muktinath is the strongest possible version of an institution in a shrinking category. That is the paradox. It has a national deposit base, a Rs 1.5 Arba profit and 19% of its sector, the profile of a commercial bank sitting inside a licence class the system is steadily dismantling. This is precisely why the stock has gone nowhere for a decade while the bank got better and better: the market is not disbelieving the numbers, it is discounting the box they sit in.

So the entire investment case reduces to a question about the box and there are only three ways out.

It upgrades. Muktinath converts to a commercial bank, the outcome its scale most obviously justifies. It already has the deposits, the network and the profit of a Class A institution. The obstacle is capital: commercial-bank paid-up requirements are far above its Rs 7.05 Arba so an upgrade almost certainly means a large capital raise and that means dilution for existing shareholders before it means a re-rating.

It acquires. Muktinath consolidates the Class B tier absorbing smaller development banks to buy the deposits it cannot organically gather, solving its 87.72% CD-ratio problem with someone else's deposit base. This is the path its constraints most naturally point to and NRB's merger-first policy actively encourages it.

It gets acquired. A commercial bank buys Muktinath for exactly what makes it valuable, a Rs 1.17 Kharba deposit franchise, a clean book, and a branch network in regions the big banks are weak in. For shareholders this is likely the fastest re-rating, and the one they have least control over.

Note what all three have in common: none of them is "carry on as a development bank and wait for the market to notice." That path has been tried for ten years and produced a 78% drawdown.

Of the three, the acquisition path is the one the bank's own constraints point at most directly. A bank that is out of lending headroom and short of deposits does not need a bigger licence first, it needs deposits and its own class is full of institutions that have deposits and no future. Buying one solves the 87.72% problem immediately, adds scale toward the capital threshold an upgrade would eventually require, and does so in exactly the direction the regulator has been pushing for a decade. It is the move that is available today, rather than the one that requires permission.

The peer comparison sharpens this. Garima Bikas Bank the only development bank that has ever briefly outearned Muktinath, doing so at the third quarter of FY2081/82 with Rs 73.35 crore against Muktinath's Rs 72.49 crore is the obvious benchmark. It is roughly three-quarters of Muktinath's size on deposits (Rs 85.79 Arba against Rs 113 Arba) and carries a smaller paid-up capital. Shine Resunga sits third, at around half the scale. Below that, the class thins out quickly into small regional lenders several of which are in visible distress.

What that distribution means for an investor is important and often missed: Class B is not a sector with a range of investable options. It is one large, well-run bank, two credible mid-sized ones and a long tail of institutions that mostly should not exist. If you want exposure to development banking in Nepal, you are really choosing between Muktinath and Garima and Muktinath is a third larger, funds itself more cheaply and has a cleaner book. That concentration is precisely why it will be the consolidator rather than the consolidated, if the class consolidates at all.

Valuation: cheap, and the reason is legible

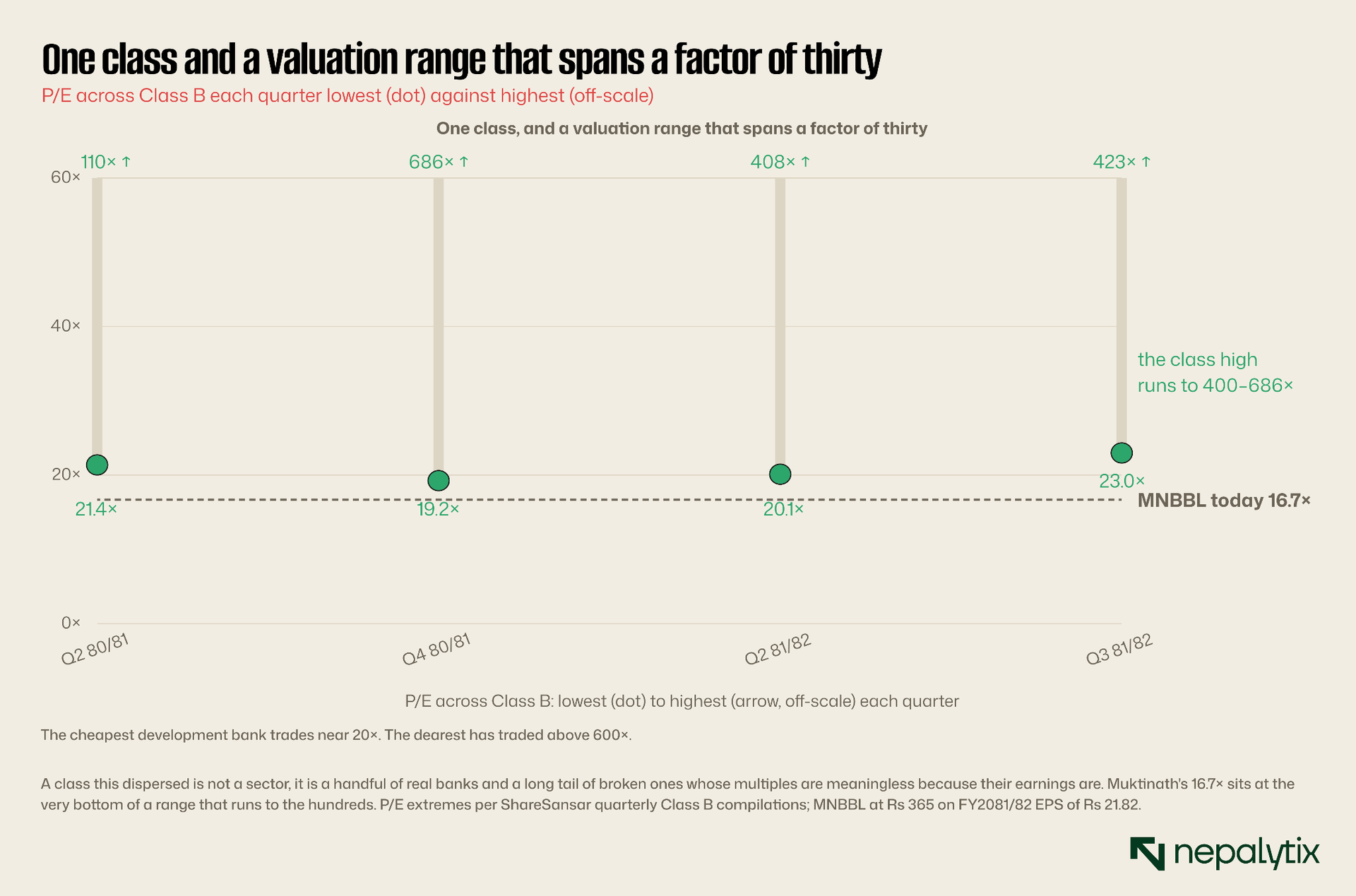

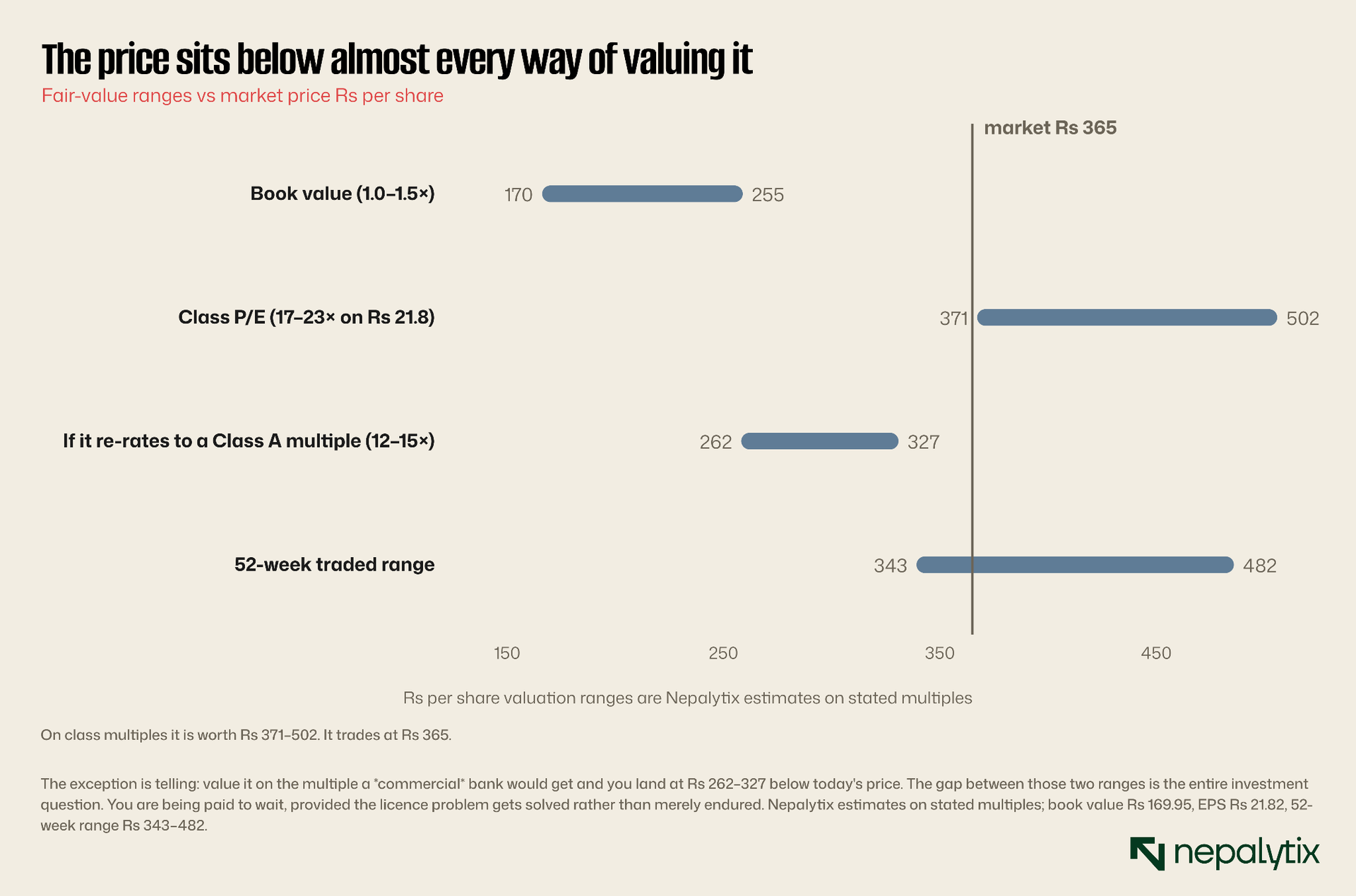

At Rs 365, Muktinath trades at 16.7 times FY2081/82 earnings and 2.15 times book. For the largest, most profitable and cleanest-lending bank in its class that is not a demanding price.

But cheapness is only interesting if you can name the catalyst that closes the gap and here the valuation itself tells you where the argument lives.

Value Muktinath as the best development bank in Nepal, on the multiples its own class trades at, and you get Rs 371 to Rs 502 meaningful upside from Rs 365. Value it on the earnings multiple a commercial bank typically commands, and you get Rs 262 to Rs 327 below today's price. Its book-value floor is Rs 170.

A note on what shareholders have actually received. Muktinath's retained earnings surged more than 650% in FY2081/82 to Rs 1.46 Arba, a large distributable pool by the standards of its class, and the raw material for either a meaningful dividend or the capital base for an acquisition. Which of those two it is used for will tell you more about management's intentions than any statement will. A large cash dividend says the bank is content in its class. Retention says it is preparing to do something. Watch that decision.

That divergence is the honest answer to "is it cheap?" It is cheap as a development bank. It is not obviously cheap as a bank in general. What you are buying, at Rs 365 is a claim on a structural resolution, an upgrade, a large acquisition or being acquired that turns a Class B asset into something the market will pay a Class A multiple for.

Finally, the ownership structure is worth a line, because it shapes what is possible. Muktinath's 70.47 million shares are split 51% promoter and 49% public, a genuinely liquid float worth about Rs 12.6 Arba at today's price which is large by development-bank standards and means an institutional buyer could actually build a position. The 51% promoter block, meanwhile, means any structural decision an upgrade, a merger, a sale is made by a coherent group rather than fought over. For a stock whose entire thesis rests on a corporate action, a decisive promoter block is a feature not a governance complaint. It also means minority holders will be told what is happening rather than consulted about it.

What breaks it

The risks are specific and worth naming precisely.

The provision of relief stops. This is the central near-term risk and it is measurable.

Muktinath's record year was built on a 27.5% fall in the impairment charge while the NPL ratio was simultaneously rising from 2.02% to 2.75%. Those two facts cannot both continue. If provisions normalise let alone rise with the bad-loan rate EPS compresses toward the mid-teens and a stock that looks cheap at 16.7 times a peak number looks ordinary at 20-plus times a normalised one.

The deposit constraint bites. At an 87.72% credit-to-deposit ratio, Muktinath cannot grow its loan book without growing deposits first and it is competing for those deposits against commercial banks with better brand reach and cheaper funding. Growth may simply stall and a stalled bank does not re-rate.

Dilution on the way to the upgrade. The most obvious happy ending conversion to a commercial bank very likely requires a capital raise to meet Class A paid-up requirements. Existing shareholders would be diluted before they were rewarded. The re-rating and the dilution arrive in that order and the market tends to price the second one first.

Nothing happens. The most underrated risk of all. Muktinath simply carries on being an excellent development bank, the licence question stays unresolved and the stock does for the next decade what it did for the last one. This is not a hypothetical, it is the base case if you extrapolate the past ten years.

Class B contagion. The development-bank category contains genuine wreckage and a peer with a 44.96% NPL on negative capital. A disorderly failure in the class or a forced merger on bad terms, taints every name in it including the good ones.

What to watch

The thesis turns on a small number of observable signals, and an investor can track them.

The impairment line, every quarter. Not the profit headline, the provision charge. If it stops falling while the NPL keeps rising, the earnings story deflates in real time and you will see it here first.

The credit-to-deposit ratio. If it stays pinned near 88%, growth is capped and the deposit constraint is real. If it falls because deposits are growing faster than loans, the bank has found room to run.

Any signal on licence class. A capital plan, a rights issue, an acquisition of a smaller development bank or the first credible noise about commercial-bank conversion. This is the catalyst that matters and it will not arrive gradually, it will arrive as an announcement.

Merger activity in Class B. Muktinath is the natural consolidator of its own class. A well-priced acquisition that adds deposits without straining capital would validate the entire thesis; a dilutive one would undercut it.

NPL prints. 2.75% and rising. The moment that ratio crosses meaningfully above 3.5%, the "cleanest book in the class" argument weakens and the provision cushion is gone.

Muktinath Bikas Bank is an outstanding institution and the market is not wrong to be unexcited about it. Both of those things are true and holding them together is the whole of the analysis.

The operational case is close to unimpeachable: the biggest deposit base in its class, the largest loan book, the highest net interest income, the first Rs 1.5 Arba profit in development-bank history and one of the cleanest credit books in Nepali finance. At 16.7 times earnings and 2.15 times book none of that is expensively priced.

The bear case is not an argument about the bank at all. It is an argument about the box. Muktinath's earnings quality is thinner than the headline implies, a record built on a provision release while the nine-month trend was negative and the NPL was rising. Its growth is gated by an 87.72% credit-to-deposit ratio in a system awash with idle cash. And its excellence has for ten straight years failed to translate into a share price, because the market prices the licence, not the ledger.

Stance. This is a structural-event stock, not a compounder. Owned as a bet that Muktinath resolves its licence problem by upgrading, by consolidating its class or by being bought it is attractively priced, with a book-value floor at Rs 170 and class-multiple fair value in the Rs 400s. Owned as a straightforward growth bank, it is a business running into two hard constraints with an earnings line that flatters itself. Buy the catalyst, not the quarter and if the catalyst never comes, understand that you have bought the last ten years again.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.