Nepal built a mass stock market before it built a mature one

In a single decade, Nepal’s stock market transformed from an elite financial niche into one of the most retail-dominated markets in the world, with over seven million Demat accounts and ownership spread across roughly a quarter of the population.

In a single decade, a frontier economy of thirty million people built one of the most retail-dominated stock markets on earth: seven million share-holding accounts around 85% of the market in private hands and a capitalisation worth nearly three-quarters of GDP. It is a genuine democratisation of ownership and a market that retailised far faster than it matured.

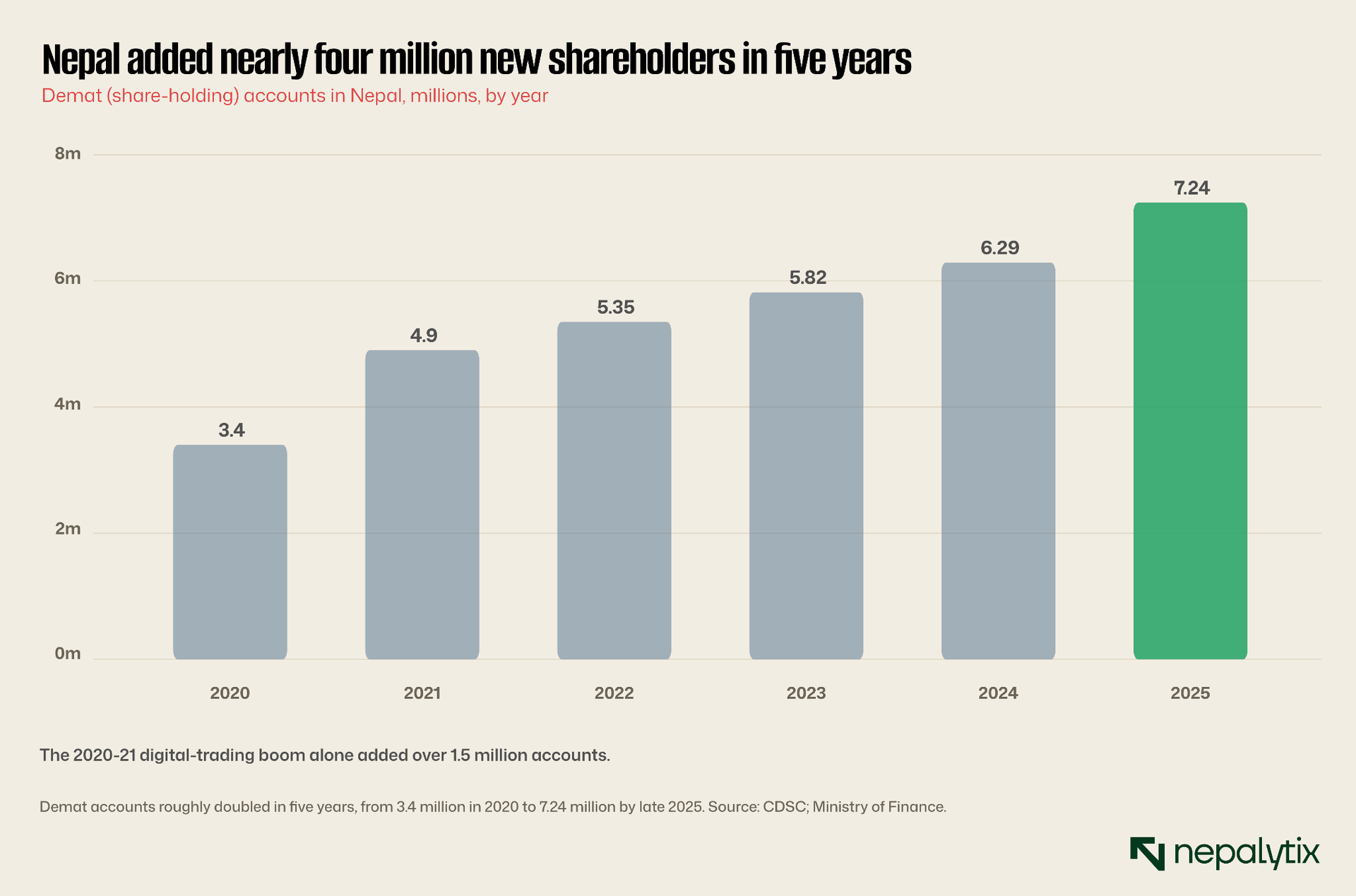

On any weekday between Sunday and Thursday, a few minutes before eleven in the morning, several hundred thousand Nepalis open an app on their phones and prepare to trade shares. They are schoolteachers in Pokhara, shopkeepers in Biratnagar, migrant workers checking prices from a labour camp in the Gulf and students in Kathmandu who opened an account before they had a salary. A decade ago almost none of them owned a single listed share. Today, by the count of the country's central depository there are more than seven million share-holding accounts in a nation of around thirty million people roughly one for every four citizens, infants included.

This is, on its face, a remarkable democratisation of financial ownership and one of the genuine economic stories of contemporary Nepal. A capital market that for its first quarter-century was the preserve of a thin Kathmandu elite has, in the space of a few years, gone mass. But the same figures that describe a triumph also describe a risk. A market grows healthily when its institutions, its liquidity, its disclosure and its investor base mature together. Nepal has not done that. It has acquired a vast retail investor base at frontier-market speed while keeping the depth, the breadth and the safeguards of a frontier market. The result is a system that is at once impressively inclusive and structurally fragile and understanding both halves of that sentence is the purpose of this piece.

To grasp how unusual this is, set it against other markets. India, in the middle of a celebrated retail boom of its own, has on the order of a tenth of its population holding share accounts; Nepal is at roughly a quarter. Even allowing for the dormant-account inflation discussed below, the depth of retail penetration relative to population is among the highest anywhere in a frontier economy with the participation rate of a rich one. That inversion, a poor country with a wealthy country's breadth of ownership, is the single most distinctive fact about Nepal's market and the source of both its promise and its peril.

Seven Million Owners. Three Million Participants

The Nepal Stock Exchange opened its trading floor in January 1994, a single room in Kathmandu where brokers shouted orders across a hall. For its first fifteen years it was a small, slow, paper-based market. The transformation that produced today's seven million accounts was not driven by a sudden national enthusiasm for equity analysis; it was driven, overwhelmingly, by technology and access. Each leap in participation tracks a leap in the plumbing: the move from open-outcry to automated screen-based trading in 2007, the creation of the central depository in 2011 that allowed shares to be held electronically, the first fully electronic trading in 2013-14 and the decisive one the NEPSE Online Trading System that, from 2020, let anyone with a smartphone place an order without ever visiting a broker.

For most of its history the market gave ordinary Nepalis little reason or means to take part. Trading meant a physical visit to a broker in Kathmandu; settlement was slow and paper-based; information was scarce and unevenly shared. Ownership was correspondingly narrow, concentrated among the capital's business families and the institutions close to them. Each piece of infrastructure that arrived chipped at those barriers but it was the combination of a depository that made shares electronic, a settlement cycle that shrank to two days, and finally a trading app in every pocket that removed them. The barriers fell in sequence; when the last one went, the dam broke.

That last change collided with the pandemic and the two together produced an explosion. Lockdowns kept people at home with their phones and, often, with remittance income that could not be spent on travel or events. Opening a Demat account became a ten-minute task done from a sofa. In the single fiscal year of 2020-21, the number of accounts jumped by more than 1.5 million.

The shift represents a profound change in how Nepali households think about saving. For generations, surplus income went into gold, land, or a fixed deposit at the local bank - tangible, illiquid, low-return stores of value suited to an economy with shallow financial markets. Easy equity access offered, for the first time, a liquid claim on corporate growth that an ordinary family could buy in small amounts from a phone. That is a structural advance in financial inclusion, whatever its risks; the question Nepal now faces is not whether to reverse it; it cannot, and should not but how to make it safe.

The growth did not stop when the lockdowns lifted. From around 3.4 million accounts in 2020, the count climbed to 4.9 million in 2021, past 5.8 million by 2023, and to 7.24 million by late 2025 more than doubling in five years and rising every single year regardless of what the market itself was doing. By the government's own reckoning, the number of citizens holding a Demat account passed a fifth of the entire population in 2024 and has kept climbing since.

Two deeper forces sit beneath the technology. The first is remittances, which are equivalent to roughly a quarter of Nepal's GDP and which deposit, every month, a flood of cash into the bank accounts of households with few other places to put it. With fixed-deposit rates low and property expensive and illiquid, the stock market became the obvious home for that money and the same digital rails that move remittances now move share orders. The second is a culture of primary-market participation so widespread it has become a national habit, to which this piece will return. Together they turned a niche pursuit into a mass one, and the activity data shows it vividly.

The remittance channel makes Nepal's case structurally different from a pure speculative mania. Money earned abroad arrives every month into millions of household bank accounts and in an economy with thin domestic investment options the listed share is the most accessible store of value with any prospect of a return. The stock market is, in part, simply the destination of choice for a remittance economy with nowhere else to put its savings. That gives the boom a durable foundation a fad would lack but it also means a remittance slowdown, or a shock to the migration economy on which Nepal depends, would knock away a pillar the market now quietly leans on.

As online access spread, the number of transactions on the exchange did not grow; it detonated, rising more than sevenfold in the year that online trading became mainstream. A market that had processed under two million trades in a year was suddenly handling more than fifteen million. The infrastructure of a sleepy, elite market was, almost overnight, carrying the order flow of a mass-participation one.

Who are these new owners? The crowd skews young, male and urban, though all three edges are blurring as access spreads. The first wave of online investors was disproportionately students and early-career professionals in Kathmandu and the larger towns, the people most comfortable with a trading app. But the remittance economy has pushed participation outward and abroad: a large and growing share of accounts belong to migrant workers in Malaysia and the Gulf who send money home and increasingly direct part of it into shares from thousands of kilometres away, and to their families managing portfolios on their behalf. For a diaspora that cannot easily buy property at home, a Demat account is a way to own a piece of Nepal from a labour camp.

The supply side of access expanded to meet the demand. The number of depository participants the banks and brokers licensed to open Demat accounts rose past a hundred, and the count of stockbrokers offering online trading roughly doubled, many of them advertising free account-opening and slick mobile apps to capture the wave. Opening an account, once a bureaucratic errand, became a customer-acquisition battle fought with promotions. Non-resident Nepalis were brought formally into the market with dedicated foreign-currency investment routes. Every institutional barrier to entry that could be lowered was lowered which is precisely why entry, rather than informed participation, became the defining feature of the boom.

The Market Behind The Headline

Before drawing conclusions from the seven-million figure, it is worth being precise about what it does and does not mean because the headline number flatters the reality. A Demat account is simply an electronic container for shares. Having one is not the same as actively investing, and the gap between the two is large and important.

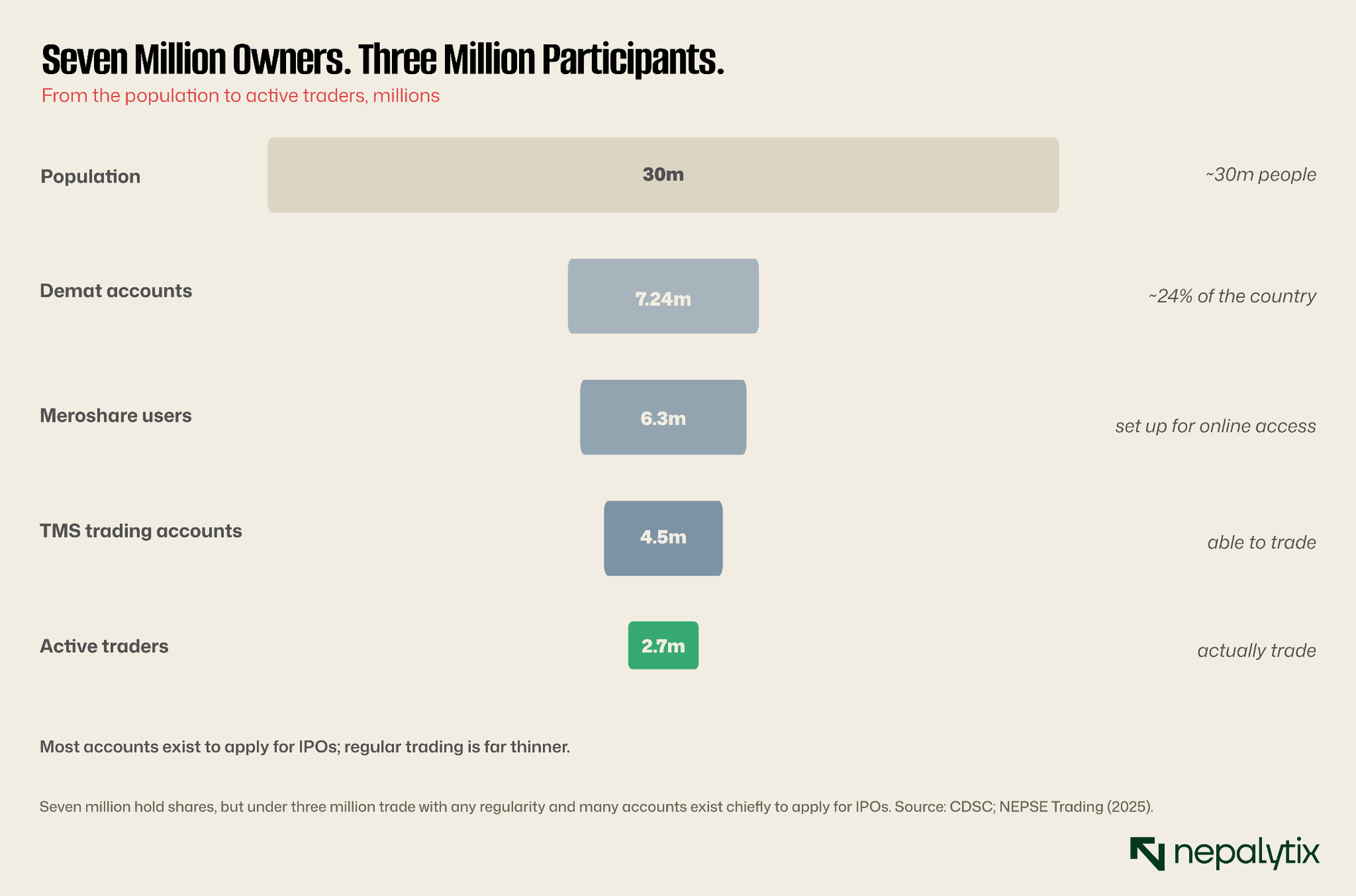

Of the 7.24 million Demat accounts, around 6.3 million are linked to Meroshare, the online portal used to apply for new share issues and view holdings. About 4.5 million have a trading account with a broker, the additional step required to buy and sell on the secondary market. And of those, only around 2.7 million are active traders in any given period. The funnel narrows sharply at every stage. The true scale of regular secondary-market participation is therefore closer to two and a half or three million than to seven, still an enormous number for a country this size, but a long way from the headline.

The gap exists for a specific and revealing reason: a very large share of accounts are opened not to invest but to play the IPO lottery. Because new shares are almost always sold at par value and allotted by a computerised draw that gives each application an equal chance, the rational move for a household is to open accounts for every eligible family member and apply to everything, maximising the number of tickets in the draw. Millions of accounts are, in effect, lottery tickets that rarely trade. That single design choice to which we will return shapes the entire participation picture.

Stripped to its core, the participation story has two layers. The outer layer has seven million accounts, a quarter of the population measures reach, and it is genuinely historic. The inner layer under three million active traders, a smaller core setting prices measures engagement and it is far more modest. Both are true at once, and most commentary on Nepal's market goes wrong by quoting one and implying the other. The market has the reach of a mass phenomenon and the trading depth of a niche one, and the distance between those two facts is where its risks live.

A very large share of the seven million accounts are not really investors. They are lottery tickets that rarely trade.

The dormant-account problem is therefore not a quirk; it is baked into the market's incentive structure. Because every additional application is an additional lottery ticket with an independent chance of winning a near-guaranteed listing gain, a household maximises its odds by opening an account for every member who qualifies spouse, adult children, parents - and applying to every issue. The seven-million figure is inflated by this arithmetic of the draw. It means the market has fewer genuine investors than it appears to and that a meaningful slice of the participation statistics measures appetite for free listing-day money rather than any engagement with the companies being bought.

Even among those who do trade the secondary market, activity is concentrated. The 2.7 million active figure itself masks a smaller core of frequent traders who account for a disproportionate share of volume, while the long tail logs in occasionally to check a holding or flip an allotment. This is normal for any market, but in Nepal it sharpens the central paradox: a market described in the language of mass participation is, in its day-to-day price-setting, the work of a far smaller and more concentrated group than seven million or even three million would suggest.

The boom and the bust

The market into which all these new participants poured is not a steady compounder. It is one of the more volatile equity markets in the region, prone to violent cycles that a mature market of its nominal size would rarely experience. The new investors of the past five years have already lived through one full cycle, and many learned the hard way what the index can do.

This is not the first time NEPSE has done this. The market has a long history of sharp boom-and-bust episodes, a celebrated bubble and collapse around 2008-09 another run-up and decline in the mid-2010s each driven by the same combination of loose credit, a surge of inexperienced money and a subsequent monetary tightening. What changed in the most recent cycle was scale: the crowd caught in the 2022 downturn was several times larger than in any previous one, because the online-account boom had multiplied the number of participants. The pattern is old; the number of people exposed to it is new.

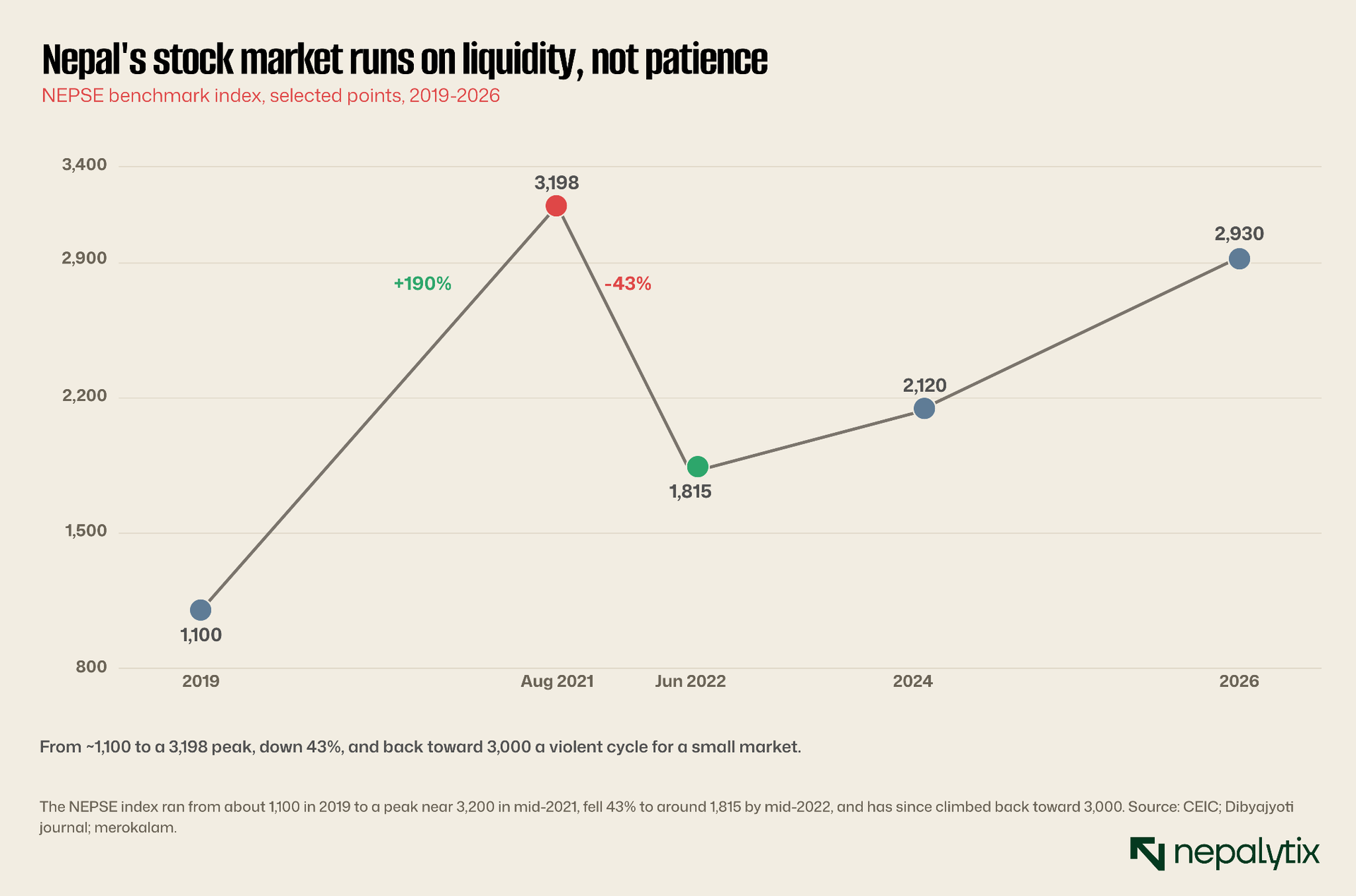

From a level around 1,100 in early 2019, the benchmark NEPSE index surged to a peak just short of 3,200 in August 2021 a gain of roughly 190% in little over two years, much of it fuelled by the same pandemic-era liquidity and new-account boom described above. Then it reversed. Over the following year the index lost some 43% of its value, bottoming near 1,815 in mid-2022, and the broader bear market that ran into 2023 erased a great deal of the paper wealth created on the way up. Drops of 30 to 50% from peak to trough are not anomalies in NEPSE's history; they are a recurring feature. The market has since recovered, climbing back toward 3,000 by early 2026, but the round trip left a generation of new investors with a vivid education in downside risk.

The human cost of that cycle was not evenly shared. Those who arrived earliest and sold near the top did well; the millions who opened accounts in 2021 near the peak buying because the market only seemed to rise were left holding the losses when it fell by nearly half. The bear market that followed was not an abstraction on a chart, it was real savings, often remittance savings, marked down by forty per cent or more for people who had been told, implicitly, that shares were a one-way bet. That experience seeded caution in some and, remarkably, did nothing to deter the millions who kept arriving behind them.

Why is a market of this size so cyclical?

Part of the answer is structural thinness, which the later sections address. But part is monetary. Nepal's stock market has historically been extraordinarily sensitive to the central bank's stance, and in particular to its rules on lending against shares as collateral. When money is loose and margin credit is freely available, liquidity floods into a small pool of stocks and prices run far ahead of fundamentals; when the central bank tightens to defend the currency peg, or to cool an import-driven balance-of-payments problem that same leverage reverses and the market falls as fast as it rose. The cycle is, to a substantial degree, a credit cycle wearing an equity costume.

The 2021 mania had all the hallmarks of a classic liquidity bubble. Pandemic-era monetary easing left the banking system awash with cash; margin lending against shares was cheap and abundant; and the flood of new online accounts supplied a steady stream of fresh buyers. Prices detached from earnings, hydropower and smaller speculative names ran hardest, and the familiar logic of every bubble that it would keep rising because it had kept rising took hold among investors with no memory of a downturn. The market did not so much grow as inflate.

When the central bank tightened, it deflated just as fast. Nepal runs a currency pegged to the Indian rupee and that peg sets a hard limit on how loose monetary policy can be: when imports surge and foreign-exchange reserves come under pressure, the central bank must raise rates and rein in credit to defend the peg, whatever the stock market is doing. In 2022 it did exactly that. The margin credit that had inflated the market reversed, forcing selling fed on itself in a thin market, and the index gave back most of its gains. The lesson that the Nepali stock cycle is ultimately governed by the balance of payments and the central bank's response to it not by corporate earnings is one every investor in this market should learn and few have.

Buying The Crash Without Knowing It

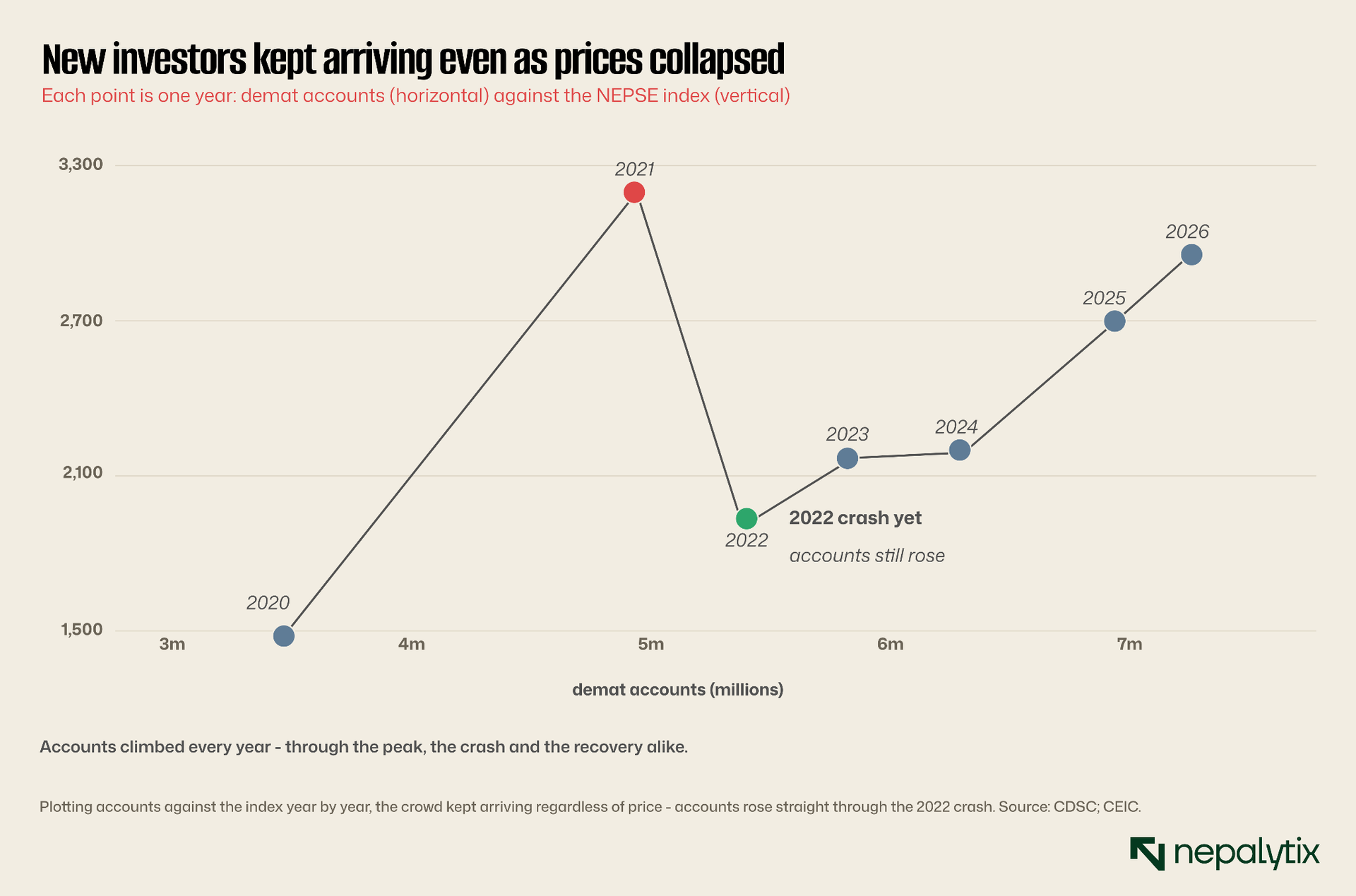

Here the story takes its most striking turn and the data reveals something that ought to worry policymakers more than it appears to. One might expect new investors to arrive during a bull market and retreat after a crash, as happens in most markets. In Nepal, they did not retreat. The account numbers rose every single year through the euphoria of 2021, through the 43% collapse of 2022 and through the slow recovery since.

Read the chart as a path traced over time and the behaviour is unmistakable. In 2021 accounts and the index rose together, the familiar pattern of a bull market drawing in the crowd. But in 2022, as the index fell by nearly half, the account count did not fall with it; it kept climbing, from 4.9 million to 5.35 million and onward. New investors arrived in the teeth of the crash and have continued arriving ever since, through every subsequent twist of the index. The crowd in other words is not responding to price in the way an experienced investor base would. It is arriving on a secular wave driven by access, remittances and the IPO lottery that runs largely independent of whether the market is cheap or dear.

That is a double-edged finding. On the optimistic reading, it means Nepal is building a structural, long-term equity culture that does not evaporate at the first downturn the patient base every developing market wants. On the pessimistic reading, it means millions are entering with little reference to valuation, buying because everyone is buying and because the account is easy to open, which is precisely the condition in which a future bubble and bust would do the most damage to the most people. Both readings are consistent with the evidence; which one proves correct depends on how the market and its regulator behave from here.

For policymakers, the price-insensitivity of the crowd carries a specific systemic danger. A market that keeps drawing in new money regardless of valuation can sustain elevated prices for longer than fundamentals justify which sounds benign until one remembers that the longer and higher the build-up, the more participants are exposed when it finally turns, and the more of them are recent, leveraged and inexperienced. A price-insensitive inflow is not a floor under the market; it is a larger crowd standing in the same room when the exit is needed.

Big On Paper

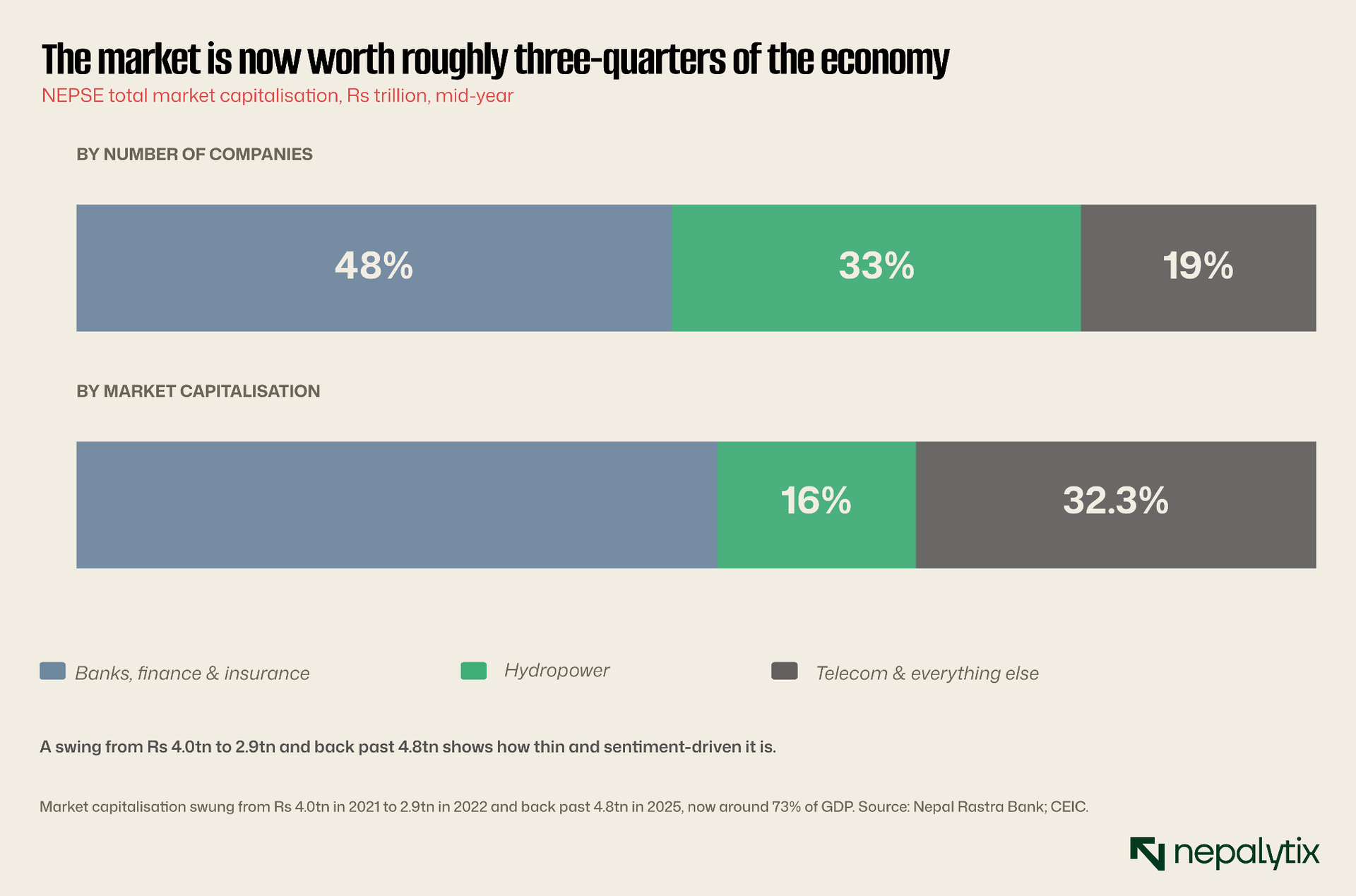

The sums involved are no longer small relative to the economy, which is what makes the market's fragility a matter of public, not merely private, concern. The total value of all listed companies on NEPSE has swung dramatically over the cycle, and now sits at a level that would be high even for a far richer and deeper market.

In mid-2021, near the market top, the capitalization of NEPSE stood at about Rs 4.0 trillion. A year later, after the crash, it had fallen to Rs 2.9 trillion more than a trillion rupees of nominal wealth erased in twelve months. It then recovered through Rs 3.1 trillion and Rs 3.6 trillion to a high above Rs 4.8 trillion in 2025, before easing to around Rs 4.5 trillion in early 2026. At that level the market is worth roughly 73% of Nepal's entire annual economic output. For comparison, that ratio is in the range of large, deep, developed markets, an extraordinary figure for a low-income economy whose listed sector is dominated by banks, and a sign that the market is richly valued relative to the real economy beneath it rather than that the real economy has been transformed.

A swing of that magnitude up a trillion, down a trillion, up nearly two in a market whose daily turnover is only a few billion rupees tells you how thin and sentiment-driven the whole structure is. The capitalisation figure is large; the volume of actual trading that sets those prices is small. That mismatch between the wealth nominally at stake and the trading that underpins it is the central vulnerability of the Nepali market, and it runs through everything that follows.

The size relative to the economy invites an international comparison that is genuinely startling. A market-capitalisation-to-GDP ratio in the seventies is typical of deep, developed markets the United States, Japan, the wealthier economies of East Asia not of low-income frontier markets which usually sit far lower because their formal corporate sectors are small relative to informal and agricultural activity. Nepal's high ratio does not signal that its economy has been transformed into a corporate powerhouse; it signals that a narrow band of listed companies, banks above all, is richly valued relative to a real economy that remains largely informal. The market is big relative to the economy not because the economy grew into it but because the market ran ahead.

The paradox sharpens when set against turnover. A market worth more than four trillion rupees trades only a few billion on a typical day, a turnover velocity so low that the vast majority of that nominal wealth is never tested by an actual transaction. Prices are set at the margin by a thin sliver of trading, and the four-trillion headline is what those marginal prices imply if applied to every share, most of which are not for sale at any given moment. It is wealth on paper in the most literal sense, and it can compress with frightening speed when the marginal buyer steps back.

The Diversification Mirage

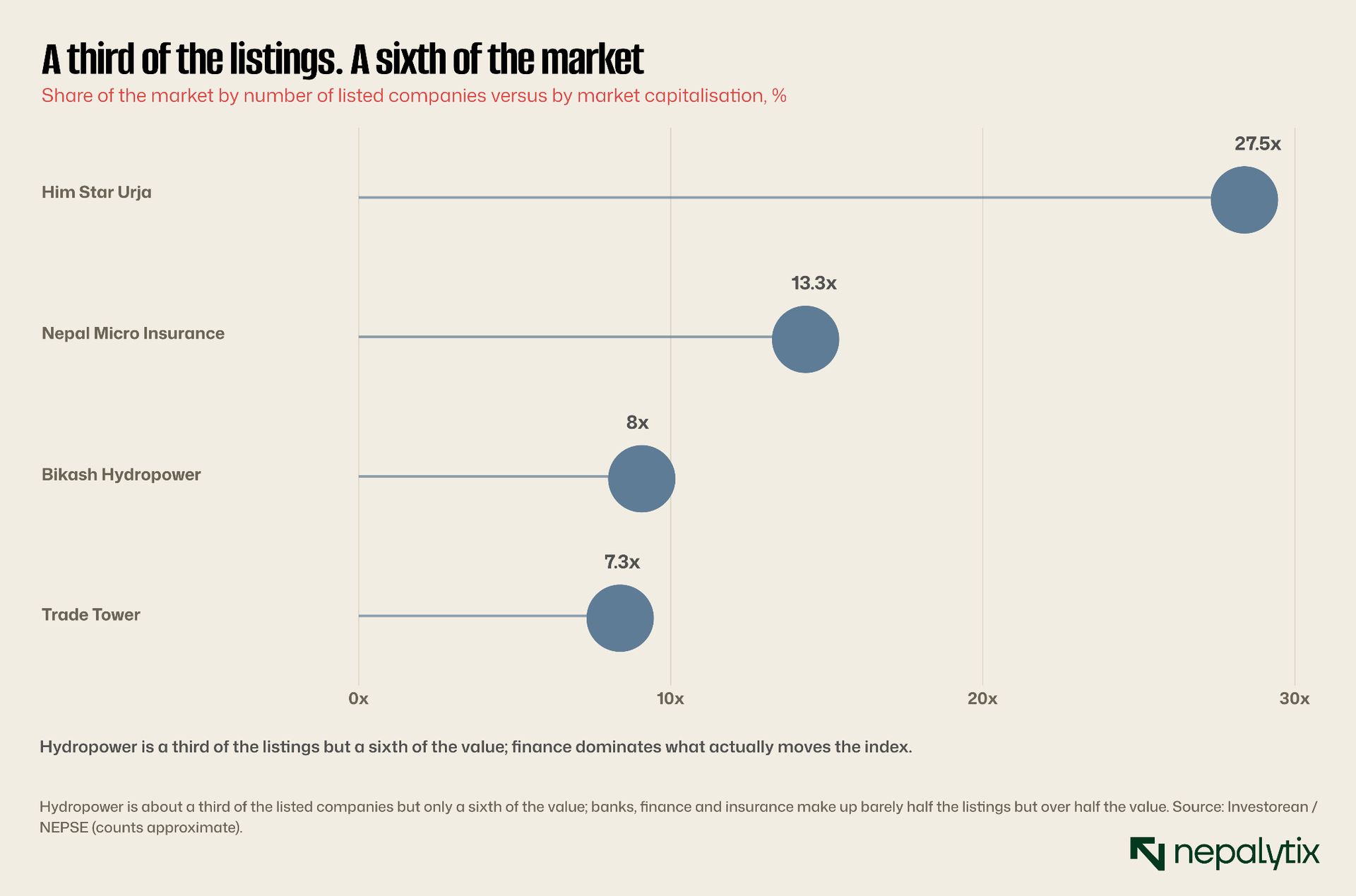

To a newcomer scrolling through the list of nearly three hundred listed companies, NEPSE looks at diversified banks, insurers, hydropower developers, microfinance firms, hotels, manufacturers, and telecom giants. The appearance is misleading. The market is far more concentrated than the company count suggests and the concentration matters because it determines what actually moves the index that seven million people are watching.

Diversification is the promise an equity market makes to a small investor: that by owning many companies, no single failure can ruin them. NEPSE makes that promise and only partly keeps it because beneath the long list of names sits a short list of risks. Understanding what the market actually contains as opposed to how many tickers it lists - is among the first things a new investor should learn, and among the last things the market's own structure makes it easy to see.

Banks, other financial institutions and insurers together account for more than half of total market capitalization around 52% while making up under half the listed companies. Hydropower presents the opposite picture and the clearest example of what might be called the breadth illusion: it is the single largest sector by number of companies, roughly a third of all listings, yet it accounts for only about 16% of market value. The remaining third of the market's value sits in a small number of large non-financial names, the telecom company Nepal Telecom above all that dwarf most of the hydropower sector despite being a handful of stocks.

For the ordinary investor this concentration quietly defeats the diversification they believe they are getting. A portfolio of a dozen NEPSE stocks picked across sectors will, on inspection, often prove to be a dozen variations on the same bet because the banks lend to the hydropower developers, hold one another's paper, and rise and fall together with the central bank's liquidity stance. Genuine diversification requires uncorrelated assets, and a market this concentrated and this governed by a single monetary lever offers fewer of them than its three hundred tickers suggest. The investor diversifies across names and stays undiversified across risks.

The practical consequence is that the NEPSE index is, to a first approximation, a bet on Nepal's banks. When a few large financial stocks move, the index moves; a regulatory change or a credit squeeze in the banking sector drags the whole market with it regardless of how the hundred-odd hydropower companies are faring. The retail investor who believes they are buying a diversified slice of Nepal's growth economy is far more often than they realise buying the fortunes of a dozen banks. And as a companion analysis this week has argued the largest of those banks have themselves grown enormously without growing more profitable so the ballast of the entire index is a sector whose returns have been compressing not expanding.

Look at which names actually carry the index and the concentration becomes concrete. The heavyweights that move NEPSE are a familiar and short list: the state telecom operator Nepal Telecom, the largest commercial banks such as Nabil and Global IME, the Citizen Investment Trust, the national reinsurer, a few large insurers and a hydropower flagship or two. Because the index is weighted by market value, these giants dominate it, and the daily direction of a seven-million-investor market is effectively decided by sentiment toward a couple of dozen stocks - most of them financial.

Hydropower is the clearest case of the breadth illusion, and a companion analysis this week made the point in detail: more than ninety listed hydropower companies give the market its appearance of breadth and its speculative energy yet because almost all are small and many are still building their plants, the entire sector is barely a sixth of market value. Investors who pile into hydropower issues believing they are buying the future of Nepal's economy are buying a great many small, correlated, monsoon-dependent bets that together move the index far less than a single large bank does. The breadth of listings is not the breadth of risk.

Everything Starts With IPO Lottery

Returns now to the IPO because it is impossible to understand Nepal's retail market without it. The new issue of the IPO is not a peripheral feature of this market; it is the gateway drug, the single most important reason millions of accounts exist, and the clearest illustration of how a well-meaning design choice can distort an entire system.

The overwhelming majority of Nepali IPOs are sold at a fixed price of Rs 100 the par value regardless of what the issuing company is actually worth. Because that price is almost always far below what the market will pay, the share reliably jumps to a multiple of its issue price on listing day, handing an immediate, near-guaranteed profit to anyone allotted stock. Allotment is by computerised lottery, with each application given an equal chance. The combination is potent: a near-risk-free windfall, distributed by lucky draw. Popular issues are routinely oversubscribed seven, thirteen, even twenty-seven times over.

The arithmetic of the listing pop is worth dwelling on. A company that issues shares at a par value of Rs 100 which then list at Rs 300 has, in effect, sold its equity at a third of what the market would have paid and the missing two-thirds did not vanish, it was handed to whoever the lottery favoured. Multiply that across dozens of issues a year and the par-value system becomes a vast, continuous redistribution from issuing companies, and the projects they would have funded, to the lucky winners of allotment draws. It is popular precisely because the winners are numerous and visible while the cost of underfunded companies mispriced capital is diffuse and invisible.

This arrangement has done real good; it is the mechanism through which equity ownership reached the masses and it spread listing-day gains widely rather than concentrating them among institutions. But its costs are steep and largely invisible to the public. It teaches an entire investing generation that the way to make money in shares is to win an allotment, not to value a business that the market is a lottery rather than a place to assess risk and reward. It floods the system with millions of dormant accounts opened solely to buy tickets. And it systematically underprices the capital that companies raise, handing value that should have funded a dam or a factory to whichever applicants the draw favoured. A market whose front door is a lottery should not be surprised when its participants behave like lottery players.

The mechanics of the IPO deserve to be spelled out because they are unusually consequential here. An applicant blocks money in their bank account through the ASBA system, applies through Meroshare and waits for the computerised draw; if allotted, the shares are credited and can be sold from the first listing day often at two to four times the issue price subject to a modest capital-gains tax. With more than two dozen issues in a typical year and allotment by equal-chance lottery, the optimal strategy for a household is mechanical and well understood: apply to everything, with as many accounts as possible. The primary market has in effect been gamified and the secondary market inherits the habits it teaches.

The bottleneck in that primary market has, as this week's coverage has documented, produced a dangerous side effect: with dozens of companies stuck for years in the approval queue, an unregulated pre-IPO market has grown up in which shares are sold to the public at steep premiums before any oversight applies. The same retail appetite that the lottery cultivates is now being channelled into instruments with none of the lottery's protections. The cultural force is the same: the conviction that getting in early on a new issue is a sure thing but the safety net has been removed which is precisely how a speculative habit becomes a scandal.

The Fault Lines

Gather the threads and a clear picture emerges of where this market is vulnerable. The first fragility is depth or its absence. Daily turnover runs at only a few billion rupees against a capitalisation of more than four trillion; many smaller stocks trade rarely and an investor wanting to sell a meaningful position in a falling market may find no buyer at anything near the last price. Thin markets go up easily on light volume and fall just as easily, and the wealth that appears on a screen can evaporate faster than it can be sold.

The second fragility is leverage. Nepal's market has always run on credit with the central bank's rules on lending against share collateral acting as the effective accelerator and brake of the whole cycle. New margin-trading rules introduced in 2026 allow investors to borrow against their portfolios more formally than before. Used carefully, margin deepens a market; used by millions of inexperienced investors in a thin and cyclical one, it is petrol near a flame, amplifying both the rallies and the crashes and turning ordinary corrections into forced-selling spirals.

The third fragility is concentration already described: an index that is effectively a leveraged bet on a dozen banks so that a problem in one sector becomes a problem for every portfolio in the country. The fourth is literacy. A market that added millions of participants in a few years did not, and could not, add financial education at the same pace. Investment decisions are widely driven by social-media tips, rumour and herd behaviour rather than analysis; the regulator's own investor-education efforts, though real, reach a fraction of the new crowd. And the fifth is the human cost of combining all of the above: when a thin, concentrated, leveraged market driven by an under-informed crowd turns down, the losses do not fall on institutions that can absorb them but on schoolteachers and shopkeepers and migrant workers who often cannot.

Used by millions of inexperienced investors in a thin, cyclical market, margin lending is petrol near a flame.

The literacy gap is the thread that ties the others into danger. A deep, well-informed investor base can live with thinness, leverage and concentration because it understands and prices them. A base assembled in five years from people whose investment information comes largely from social-media tip channels and the confident assertions of strangers cannot. The point is not that Nepali investors are foolish, they are responding rationally to the incentives the market hands them, the lottery above all but that the market has equipped millions to participate without equipping them to assess risk. Inclusion without education is not empowerment; it is exposure.

None of these fragilities is hypothetical. Each was visible in the 2021-22 cycle when leverage drove the rally, thinness and forced selling deepened the crash, banking weakness dragged the index and the heaviest losses fell on the newest and least-prepared investors. The market survived, recovered, and kept adding accounts. But it survived a relatively mild macroeconomic shock. A more severe one, a balance-of-payments crisis, a serious episode of banking stress, a political rupture of the kind Nepal experienced as recently as 2025 would test a far larger and more leveraged crowd than the last downturn did.

Two further fragilities are political and systemic rather than structural. Nepal's recent history is punctuated by episodes of acute political instability including serious unrest in 2025 and a market driven by sentiment and leverage is exquisitely sensitive to such shocks; the technology itself adds operational risk, with trading platforms known to freeze under the heavy load of a volatile session locking investors out at exactly the moment they most want to act. Neither is a tail risk in Nepal. Both are recurring features of the environment in which seven million people now hold shares.

Sitting above all of this is a regulator stretched thin. The Securities Board of Nepal oversees a market that added millions of participants and dozens of new intermediaries in a handful of years, with resources scaled to the far smaller market of a decade ago. Supervision, enforcement, investor education and the primary-market approval pipeline have all struggled to keep pace as this week's coverage of the IPO gridlock documented. A market this large and this retail needs a regulator with the capacity to match it; closing that gap is as important as any single rule change.

The deepest systemic danger though, is the loop between the banks and the market. Because banks both dominate the index and lend against shares as collateral, a falling market and a stressed banking sector can feed each other: share prices fall, the collateral behind margin loans erodes, banks call those loans, the forced selling drives prices lower still and the losses circle back onto the balance sheets of the very institutions that anchor the index. In a market this concentrated and this leveraged, a banking problem and a market problem are not two risks but one, and the retail investor sits at the centre of the loop.

The Maturation Challenge

It would be wrong to end on alarm, because the underlying achievement is real and worth defending. Seven million share-holding accounts represent a genuine broadening of economic ownership in a country where for generations financial wealth was the preserve of a narrow elite. Millions of ordinary Nepalis now have a direct stake in the formal economy, a reason to follow company results and central-bank decisions and a savings vehicle that over the long run and despite its cycles, has outperformed the bank deposits and idle cash that were their only prior options. That is a public good, and the digital and remittance forces driving it are not going to reverse.

The danger in celebrating the headline figure is that it invites complacency about everything else. Seven million accounts is the kind of number that makes for a proud ministerial speech, and it deserves to: it represents millions of citizens with a direct stake in the formal economy for the first time. But reach is the easy part and it was delivered largely by private technology and the remittance economy almost as a by-product of forces no one designed. Depth, resilience, fair pricing and real protection are the hard parts, and they will not arrive on their own; they require deliberate institution-building that no trading app will do for the country. The boom was, in a large sense, the gift of circumstance; what gets built on top of it will have to be a choice and the window for making that choice well is open now, while the last crash is still recent enough to focus minds.

But a mass market demands mass-market institutions and that is where Nepal has fallen behind its own success. The reforms that would make this market match its participation are not mysterious, and several have been argued elsewhere in this week's coverage: price discovery through book-building instead of the par-value lottery, so that issues are priced honestly and the crowd learns to value rather than to gamble; a transparent, time-bound primary market that does not bottleneck capital and breed an unregulated shadow market beside it; deeper liquidity through market-making and a broader, less bank-heavy roster of listings; cautious, well-supervised margin rules that deepen the market without detonating it; and an investor-education effort scaled to the size of the crowd rather than to the budget of a small division of the regulator.

The models for what comes next are visible across the region. Some frontier markets that broadened ownership quickly went on to build the depth and supervision to match, and turned a retail boom into a durable domestic capital base. Others let the boom outrun the institutions and suffered a crash severe enough to drive a generation of small investors out of the market for good, setting financial development back by years. Nepal stands at exactly that fork now with a larger and more leveraged crowd than it had at the last downturn, and a reform agenda that is well understood but only partly enacted.

If there is a priority among these reforms, it is price discovery. Almost every distortion in this market traces back to the par-value lottery: the dormant accounts, the gambling mentality, the mispriced capital, the unregulated pre-IPO market the bottleneck spawned. Change how new shares are priced, move to genuine book-building, let issues clear at something near fair value and the incentives that shaped the retail crowd begin to shift with it. Liquidity, supervision and education all matter, but pricing is the keystone: pull it and much of the rest follows.

The central fact of Nepal's stock market in 2026 is that its investor base has run far ahead of its institutions. Seven million people have been invited into a market that still trades like a small one thin, concentrated, leveraged and lightly regulated. The democratisation is done; the maturation has barely begun. Whether the retail republic becomes the foundation of a deep, resilient capital market or the setting for a painful reckoning depends entirely on whether the institutions are now built to match the crowd that has already arrived. The crowd, as this week's data shows, is not waiting.

What would success look like?

It would look like the maturation catching up to the participation: a market where new issues are priced by demand rather than handed out by lottery, so the crowd learns valuation; where liquidity is deep enough that an ordinary investor can exit a position without moving the price against themselves where the roster of listings extends well beyond banks into a genuinely diversified real economy where leverage is available but supervised; and where the regulator's investor-education effort is funded and scaled to the millions it must reach. None of that is beyond Nepal's capacity, and parts of it are already being attempted. The optimistic case is real and should not be dismissed. Markets that broaden ownership early can build over a generation, the deep domestic capital base that lets an economy fund its own development rather than depending on foreign money and a population that has lived through a cycle and stayed invested is exactly the patient base that makes such a market resilient. Nepal has almost by accident, assembled the raw material of a formidable capital market: a vast, engaged, growing body of retail owners. The question is whether the country now builds the institutions worthy of them, or leaves them exposed in a market that trades like the small one it used to be.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.