Nepal Built a NPR 4.8 Trillion Stock Market. It Still Can't Reliably Price a Stock.

Nepal’s stock market has grown into a NPR 4.8 trillion exchange with nearly seven million investors, but size does not necessarily mean efficiency.

The Nepal Stock Exchange now carries the market capitalisation of a serious bourse and the liquidity of a seasonal bazaar. Inside the machinery of price discovery on NEPSE and why a NPR 4.8 trillion market still struggles to tell you what a share is worth.

There is a comforting story Nepali investors tell about their stock market, and it goes like this: a frontier exchange, once a sleepy government appendage has matured into a NPR 4.8 trillion machine equal to four-fifths of national output with nearly seven million account-holders and a screen that lights up green most mornings. The story is true in its particulars and misleading in its conclusion. Size is not depth. A market can be enormous and still be unable to do the one job a market exists for: turn the scattered opinions of buyers and sellers into a price that means something.

Price discovery is that job. In a deep market, a share's quote is a dense, continuously updated summary of everything known about the company: earnings, rates, risk, sentiment compressed by thousands of competing trades into a single number that moves smoothly and resists being pushed around. In a thin market, the same quote is a rumour with a decimal point. It is set by whoever traded last, on volume that would not register on a serious exchange, inside rules that stop the price the moment it tries to move with conviction. NEPSE, for all its growth, sits much closer to the second description than the first. This piece is an attempt to show with the exchange's own numbers exactly how its prices are made, and why the quality of those prices has not kept pace with the size of the market printing them.

The scale illusion

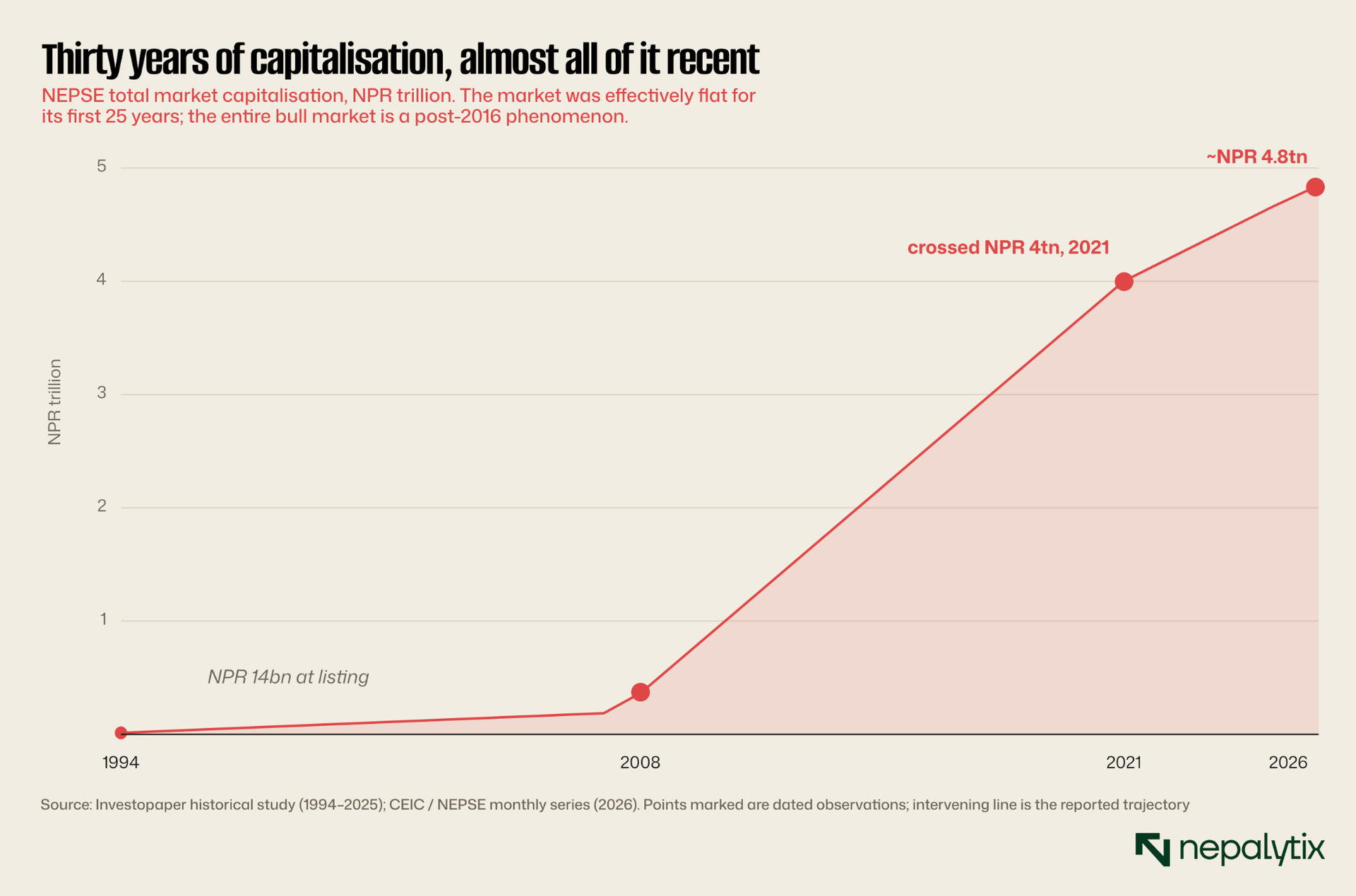

Begin with the headline that everyone repeats because it is genuinely remarkable. When NEPSE opened its floor in 1994 it listed 66 companies worth in aggregate under NPR 14 billion. Three decades later the listed universe is past 260 names and the market is worth roughly NPR 4.8 trillion, a 336-fold expansion in capitalisation against a roughly four-fold rise in the number of companies. The exchange now stands at around 82 percent of GDP, a ratio that would not embarrass a mid-tier emerging market. Capitalisation crossed NPR 5 trillion for the first time in the summer of 2025 before the political turbulence of the autumn pulled it back toward NPR 4.5 trillion and then by spring 2026 back up again.

What the trajectory hides is that almost all of it is recent and almost none of it is liquidity. For the market's first quarter-century the line barely lifts off the floor; the entire move is compressed into the years after 2016 and especially after 2020. That shape matters. A market that quadruples its capitalisation in four years has not slowly accreted depth the way a mature exchange does, it has been inflated, fast by a wave of new listings and a flood of new money, while the plumbing that is supposed to price all that paper has stayed roughly the same width.

The composition of all that paper matters as much as its quantity. The listed roster past 260 names is dominated by the financial sector: commercial banks, development banks, finance and microfinance companies and insurers alongside a lengthening tail of hydropower developers. Industrials, consumer names and the rest of the real economy are thinly represented. The practical consequence is that the headline index, and the capitalization it tracks, prices the fortunes of the banking system and the credit cycle far more than it prices the broad Nepali economy. When investors say "the market," they are largely saying "the banks" which is also why the same monetary conditions that drive lending drive the index.

The distinction between size and depth is not pedantry. It is the whole argument. A share price is only as informative as the volume of disagreement behind it. When NEPSE's capitalisation balloons but the trading that prices it does not deepen in proportion, the result is a market where the quoted value of the country's corporate sector rests on a remarkably thin layer of actual transactions. To see how thin, you have to stop looking at the stock of wealth and start looking at the flow.

Liquidity that arrives in spasms

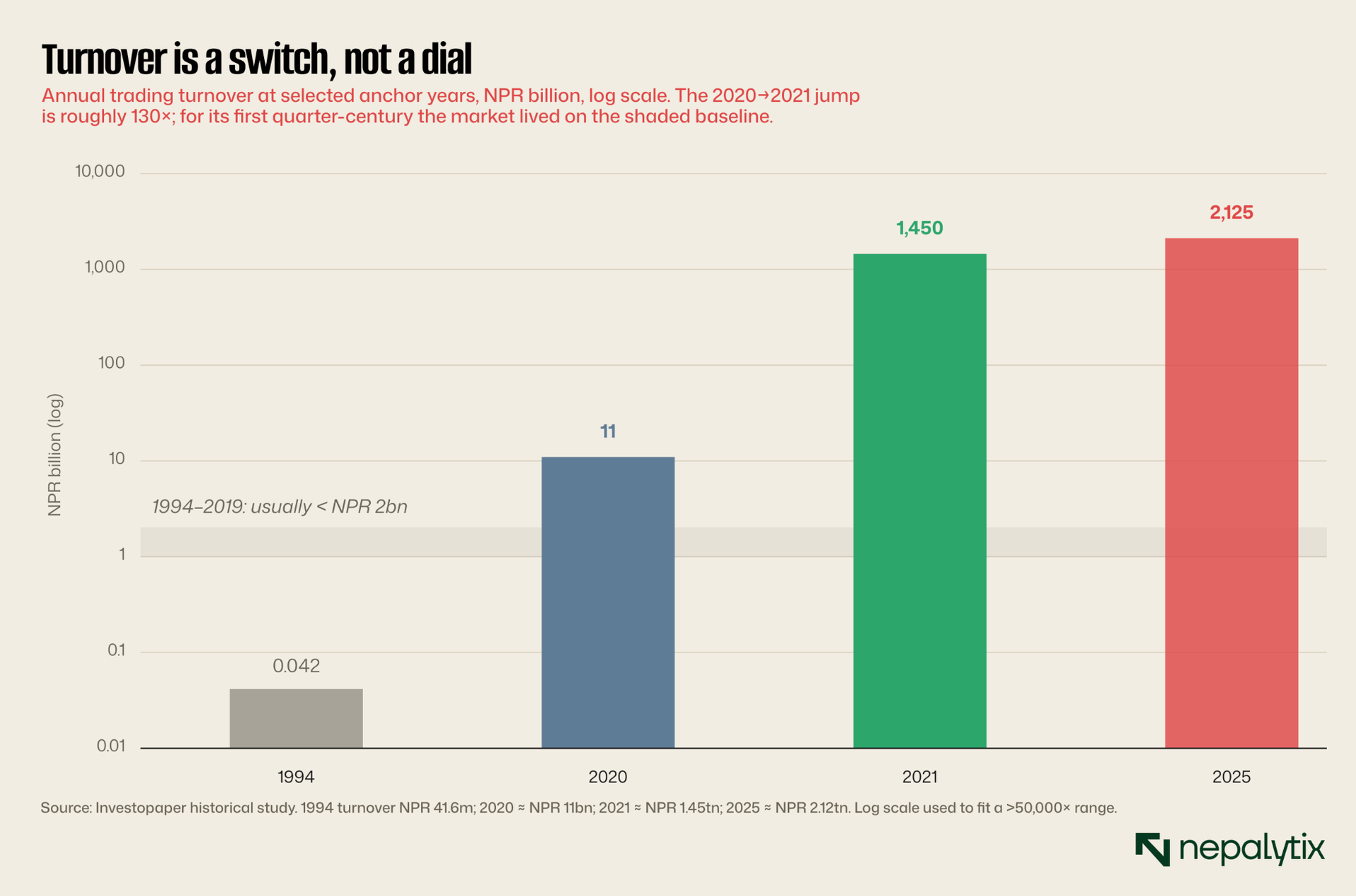

Turnover is the flow, the value of shares that actually change hands. And NEPSE's turnover does not behave like the turnover of a deepening market, which tends to rise gradually and steadily as more participants and instruments come on. It behaves like a switch. For the better part of three decades, annual turnover rarely cleared NPR 1–2 billion. Then, in the span of a single year, it did not double or triple; it multiplied roughly 130-fold from around NPR 11 billion in 2020 to about NPR 1.45 trillion in 2021, before settling near an all-time-high NPR 2.1 trillion in 2025. The turnover of the 2021–2025 window dwarfs the combined turnover of the previous 26 years.

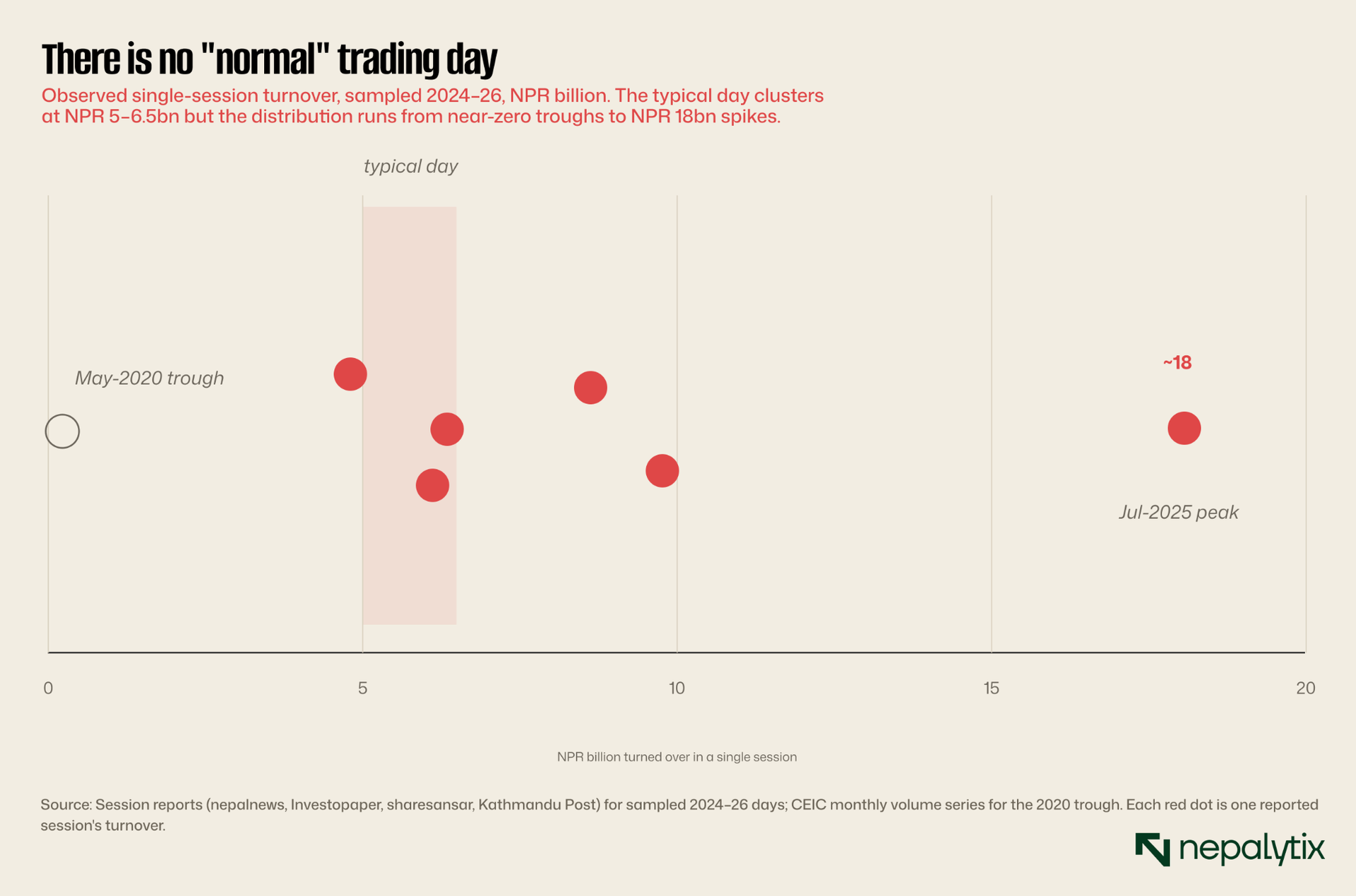

A market that switches on like this is not discovering prices in any continuous sense; it is being repriced in bursts. The bursts coincide with credit cycles and sentiment, not with the arrival of new information about companies. When liquidity is present, prices move fast and far; when it withdraws, the same shares can sit for sessions on stale quotes. The daily picture confirms the instability. On an ordinary recent session the exchange turns over something like NPR 5–6 billion; on the hot days of mid-2025 it pushed toward NPR 18 billion; and the monthly volume series has swung between a 2024 peak and a May-2020 trough that was lower by a factor of several thousand. "Normal" is not a number on NEPSE. It is a wide, unstable band.

A market that switches on 130-fold in a year and then withdraws to a trickle is not pricing companies. It is pricing the appetite of whoever happens to be in the room.

Thin by the measure that counts

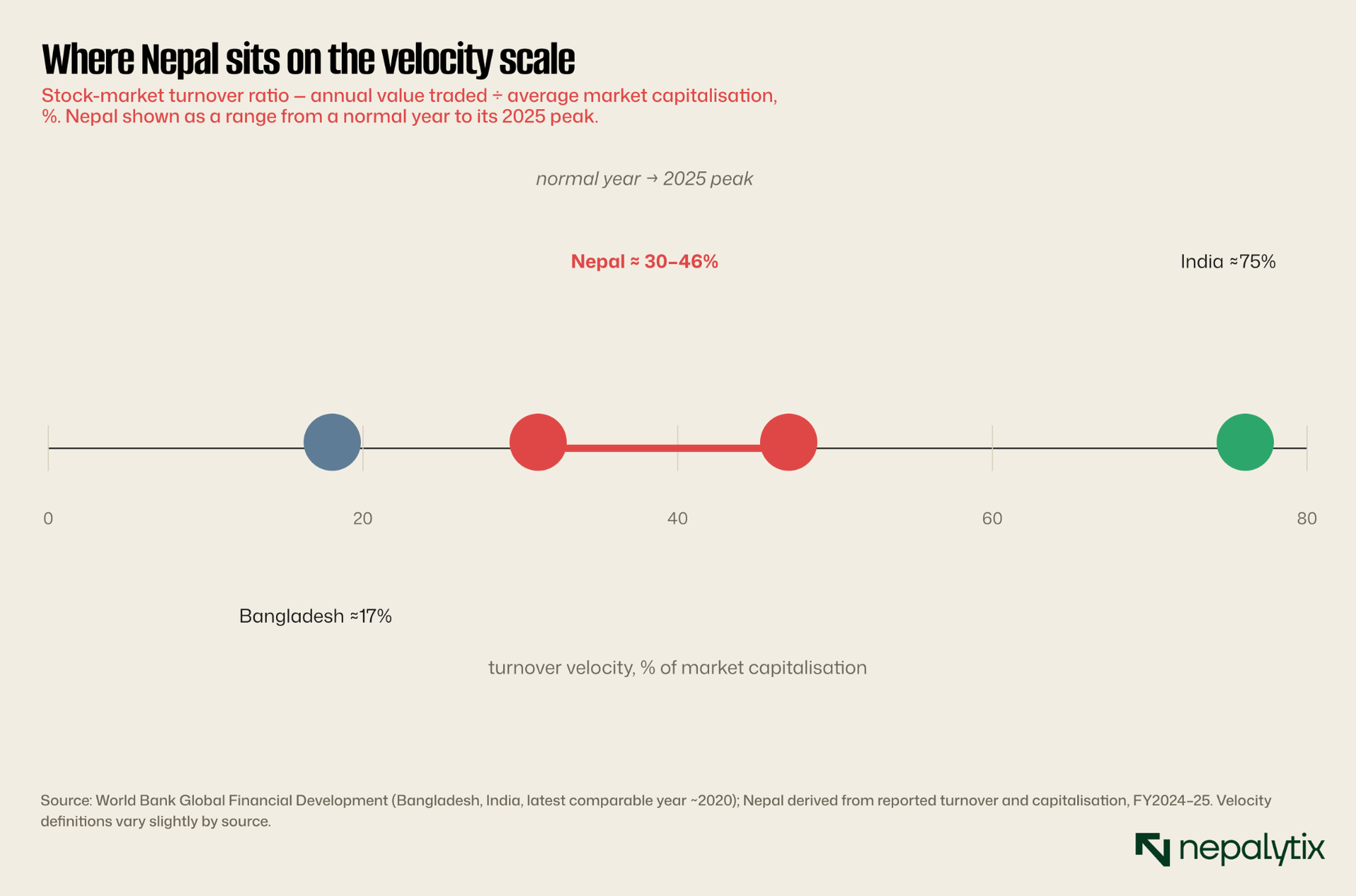

The cleanest way to compare liquidity across markets is velocity: the value traded in a year divided by the average market capitalisation. It strips out size and currency and answers a single question: how many times does the market turn its own float over in a year? A deep market churns its capitalisation once or more annually. India's exchanges have run velocity in the region of three-quarters of capitalisation. Bangladesh's Dhaka exchange, a closer peer, has spent recent years between roughly 17 and 30 percent. Nepal, even in its hottest year on record, churned somewhere between a third and a half of its capitalisation and in a normal year, less.

Read that carefully, because it cuts both ways against the bullish story. On one hand, NEPSE's peak-year velocity is not embarrassing by frontier standards; the 2025 turnover boom genuinely lifted it toward the middle of the regional pack. On the other hand, that velocity is the peak, the product of a credit-fuelled mania, not the steady state. The steady state is thinner, and it is the steady state that determines the quality of prices on the other 300 days of the year. A market that only achieves respectable velocity when it is on a leverage-driven tear has not solved its liquidity problem; it has rented a temporary solution from the banking system.

Velocity is an annual average and averages flatter a market whose activity is wildly uneven across names. On any given session a small group of liquid large-caps, the dominant commercial banks, a few insurers, the hydropower favourite of the moment absorbs the bulk of turnover, while the long tail of listed scrips trades in a few hundred shares or does not trade at all. For those names the order book is shallow at the touch and the gap between the best bid and the best offer is wide; a single modest order can walk the price several percent before it is filled. A closing price quoted off two or three small trades is a price in name only; it records what one buyer paid one seller for a sliver of stock, not what the market would bear at any size. The aggregate velocity number, respectable as it looks on the peer chart, is the average of a handful of genuinely liquid names and a few hundred that barely have prices at all.

The peer comparison also reframes what "frontier" means here. Nepal is not unusually small in capitalisation relative to its economy, quite the opposite. It is unusual in how unstable its liquidity is around that large base. That instability is the signature of a market whose marginal buyer is not a patient institution recycling savings, but a leveraged retail investor whose presence depends on the price of credit. Which raises the question that organises the rest of this piece: who, exactly, is setting the price?

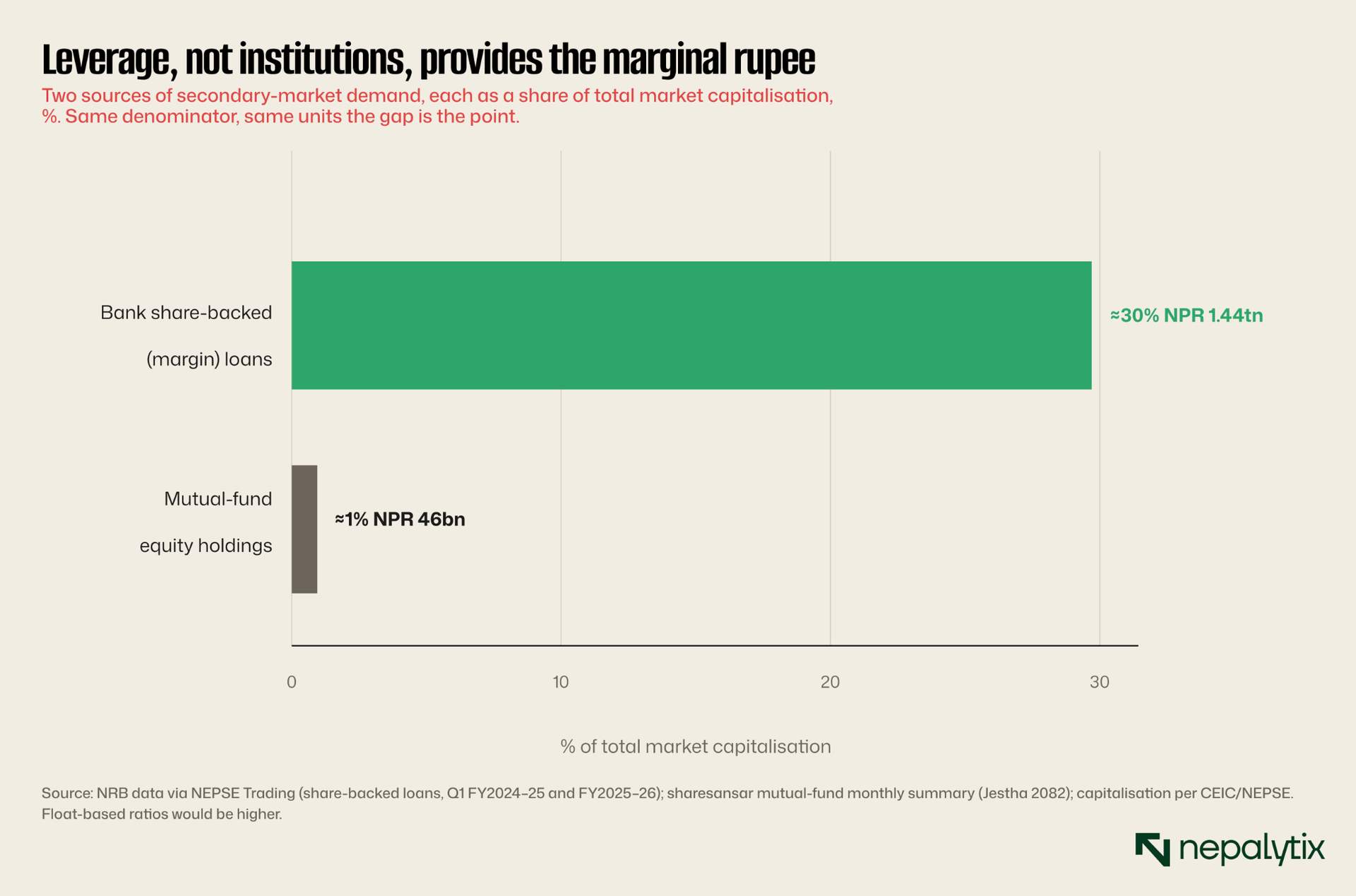

The marginal rupee is borrowed

Every market has a marginal price-setter, the participant whose next order tips the quote. In a developed market it is overwhelmingly institutional: pension funds, insurers, mutual funds and foreign investors, deploying long-duration savings with a mandate to value companies. On NEPSE that buffer barely exists. The entire domestic mutual-fund industry, some forty-odd open- and closed-end schemes held equity investments of roughly NPR 46 billion in mid-2025. Against a market capitalisation near NPR 4.8 trillion, that is on the order of one percent. The funds that retail investors imagine as price stabilisers could not stabilise a single mid-cap on a busy afternoon.

And the mutual-fund gap is only the visible part of a wider absence. The institutional investors that anchor mature markets, pension funds deploying retirement savings, life insurers matching long-dated liabilities, foreign portfolio money arbitraging mispricings are effectively missing from NEPSE's order flow. Foreign investment in listed equity has long been tightly restricted; the contractual-savings pools that do exist are not meaningfully mandated into stocks; and what passes for the buy-side is, in practice, the same retail crowd routed through different labels. The account base has swelled from roughly 5.35 million demat accounts in 2022 to about 6.75 million by mid-2025, nearly 22 percent of the population but that growth measures enthusiasm for opening accounts, not depth in trading them. There is no patient, valuation-driven counterweight to lean against a momentum move: no natural buyer at the other side of a panic, no natural seller at the top.

Now set that against the other source of marginal demand. Banks' share-collateral, or margin, lending stood at roughly NPR 1.05 trillion at the close of the first quarter of FY2024–25 and had climbed about 37 percent to around NPR 1.44 trillion a year later. Measured against total capitalization, share-backed credit is on the order of thirty percent of the entire market's value and measured against the far smaller tradable float, the proportion is materially higher still. The arithmetic is stark: for every rupee of equity the mutual-fund industry owns, the banking system has lent something like thirty against shares.

This is the engine of NEPSE's price formation and it is reflexive in the most dangerous way. The collateral for the loans is the same paper the loans are used to buy. Banks lend up to 70 percent of the lower of a 180-day average price or the last trade, with a margin call triggered if the value falls roughly 40 percent. So when prices rise, collateral values rise, lending capacity expands, and more credit chases the same shares higher, the mechanism behind the 2021 turnover explosion. When prices fall, the loop runs in reverse: margin calls force selling, which lowers collateral values, which forces more selling. The regulator has spent years alternately loosening and tightening this tap most recently lifting the cap on institutional share-collateral loans while keeping individuals capped precisely because it understands that the tap, not corporate earnings, is what moves the market.

When the collateral for a loan is the same share the loan buys, rising prices manufacture their own demand until they don't.

A market priced by leveraged retail flow, with no institutional ballast, will overshoot in both directions. That is not a moral failing of Nepali investors; it is a structural feature of a market that built its capitalisation before it built its buy-side. And it explains why the prices NEPSE produces are so often momentum rather than valuation, why a stock can triple and round-trip within a year on no change in fundamentals. The marginal opinion being expressed is not "what is this company worth" but "can I still borrow against it."

When the band does the discovering

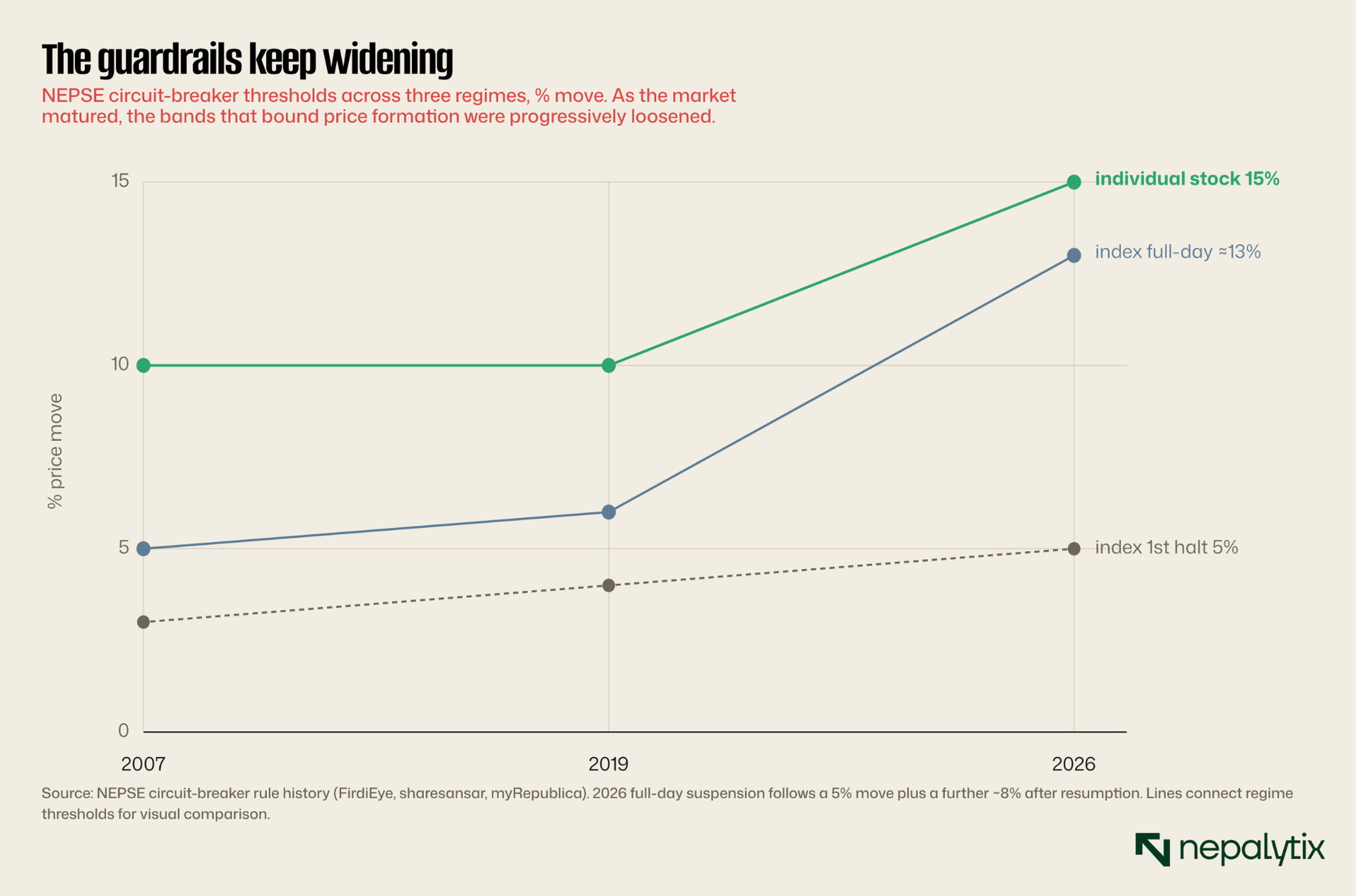

Layered on top of thin, leveraged flow is a set of mechanical limits that further blunt price formation: circuit breakers. NEPSE caps how far an individual stock can move in a day, and how far the index can move before trading halts. The intent to slow panic and curb manipulation is reasonable. The effect, in a thin market, is more ambiguous. When a stock can move only a fixed percentage per session regardless of news, the limit itself becomes the price. A piece of information worth, say, a 40 percent revaluation cannot be expressed in one day; it is rationed out over many sessions of stocks "hitting circuit," each day's close set not by where buyers and sellers agree but by where the rulebook stops them.

The bands have also been moving and the direction is loosening. The individual-stock daily limit sat at 10 percent for nearly two decades before being widened to 15 percent in the 2026 rule revision. The index-level halts have stepped up twice: from 3/4/5 percent triggers at their 2007 introduction, to 4/5/6 percent in 2019, to a 2026 regime in which a 5 percent move triggers a short halt and a further 8 percent suspends the day. Each loosening lets prices travel further before the rulebook intervenes a tacit admission that the old bands were doing too much of the discovering.

Notice what the rules do not change: depth. A wider band lets a thinly traded stock gap further on the same handful of orders; it does not summon more orders. In a recent ordinary session, three stocks rode the new 15 percent ceiling to a positive circuit — not on a flood of conviction-led buying, but on the modest volume it takes to move a thin name to its limit. The band did not contain a wave of information; it framed the absence of one. This is the quiet truth about circuit breakers in a shallow market: they spend most of their time not stopping mobs, but disguising how little it takes to move a price.

A tape written by politicians

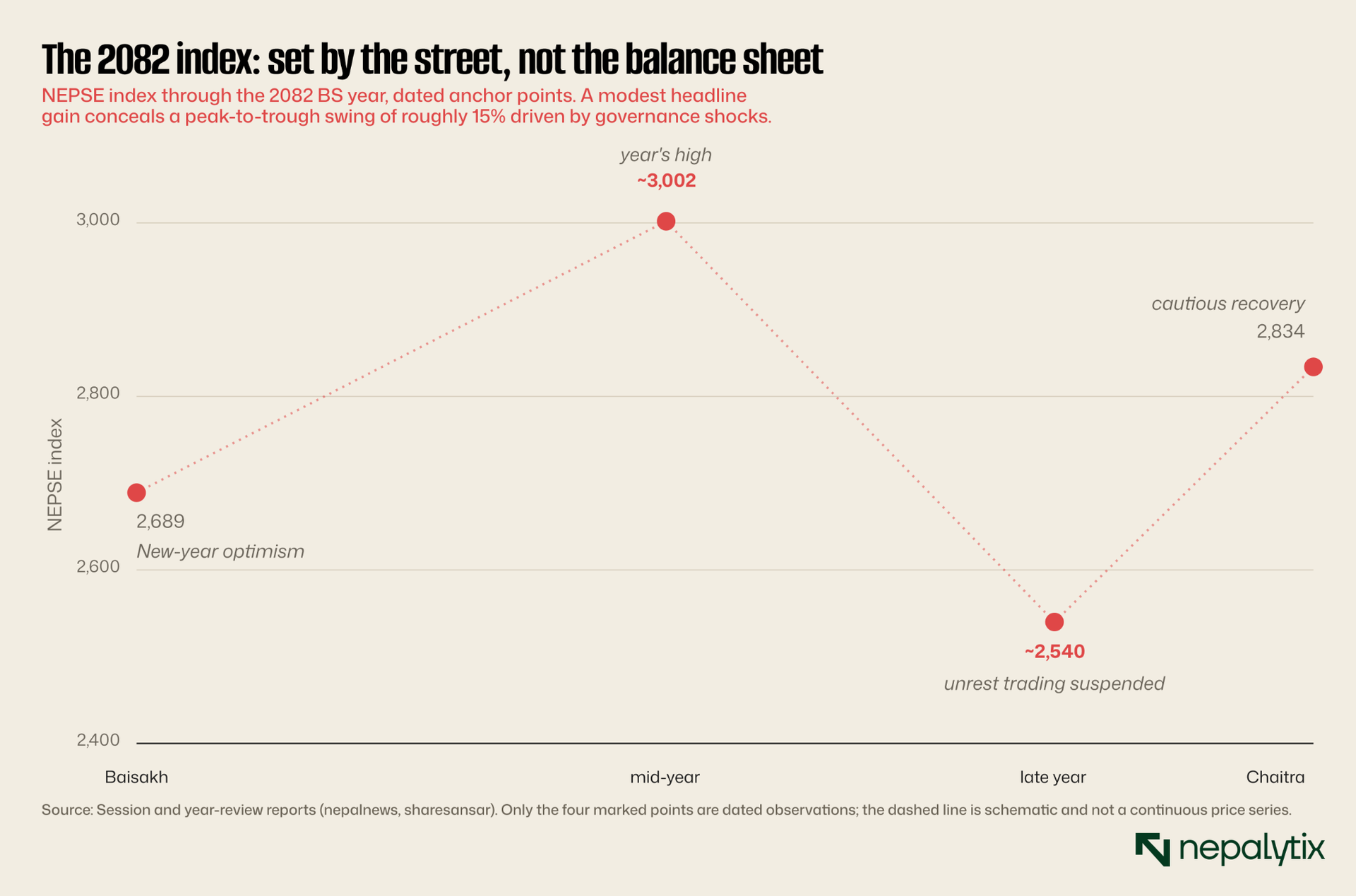

If thin, leveraged, limit-bounded flow is the mechanism, the autumn of 2082 BS was the demonstration. The Nepali trading year opened in renewed optimism, the index lifting off a stable close into the high 2,600s on the back of cheap money and remittance liquidity. By mid-year it had climbed back above 3,000, its strongest level in years, though still short of the 3,199 record set in 2021. Then the country's politics intervened. Anti-corruption unrest swept the streets, the market endured repeated circuit halts and an outright trading suspension tied to the crisis and the index cratered toward the mid-2,500s before clawing back to close the year near 2,834 a modest net gain that flatters a year of violent intraday swings.

No earnings season explains that path. The companies behind the index did not lose and regained a sixth of their fundamental value in a few months. What moved was the willingness of leveraged retail money to stay in the market, and that willingness is a function of confidence in the state, not of discounted cash flows. A market that prices political risk this violently, and corporate performance this faintly, is telling you where its price discovery actually happens: in the headlines, transmitted through the margin account, and out through the daily limit. The recent budget's decision to make capital-gains tax a final tax while raising the rates is the kind of policy variable that, here, moves prices more reliably than a results announcement.

Anatomy of a single session

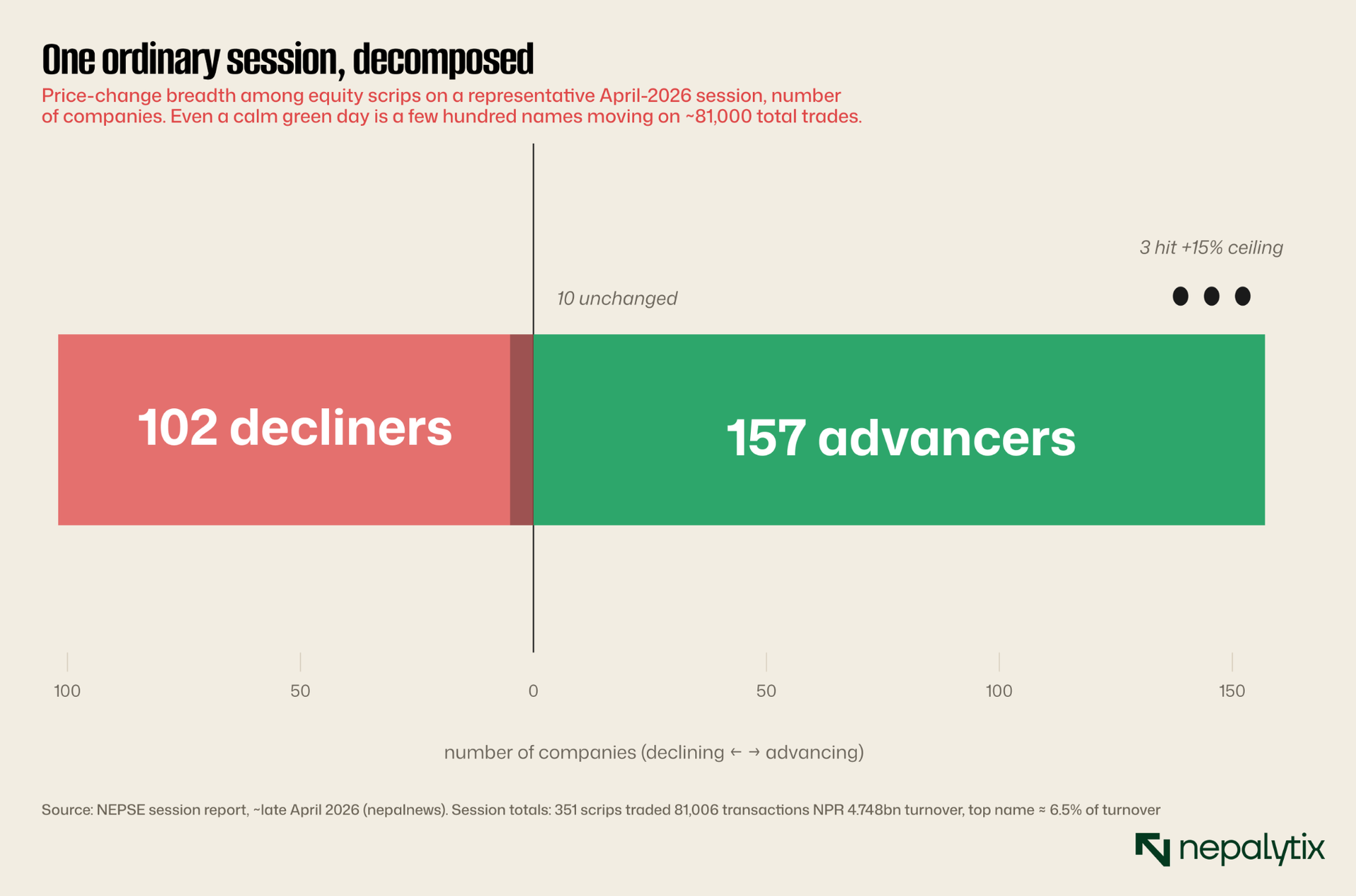

Step inside one ordinary day and the abstractions become concrete. In a representative recent session the index rose a quiet seven points to close near 2,796. Beneath that placid headline, 351 securities traded but through only about 81,000 transactions across the entire exchange. A serious market processes many trades in seconds; NEPSE takes a full session, and even then the flow is lopsided. The single most-traded name by value, a spinning mill, accounted for roughly 6.5 percent of the whole market's turnover by itself. Breadth, such as it is, sat at 157 advancers against 102 decliners and a handful unchanged with three names riding the freshly widened 15 percent ceiling to a positive circuit.

The machinery that produces that day is, for what it is worth, modern. NEPSE retired its open-outcry floor for a semi-automated screen system in 2007 and moved to a fully online order-routing platform the NEPSE Online Trading System in 2018. Orders now flow from investors through the terminals of fewer than a hundred licensed brokers into a central matching engine; a pre-open auction collects orders and sets the day's opening price before continuous trading runs from late morning to mid-afternoon, five sessions a week. Holdings are dematerialised, and clearing passes through the Central Depository System and Clearing on a T+2 cycle two business days from trade to settlement, a calendar that India and the United States have since shortened to T+1. There is nothing primitive about the plumbing. What is missing sits upstream of it, in the thinness of the orders the plumbing has to carry.

Hold the day's numbers together and the structure of the market resolves into focus. Nearly seven million demat accounts exist about 22 percent of the population yet the entire country's appetite to trade resolves into tens of thousands of transactions, concentrated in a few names, on a few billion rupees, much of it borrowed. The breadth of the account base is nominal; the depth of the order book is not. The accounts were opened, in large part, to chase the lottery odds of an IPO that tends to pop on listing not to trade the secondary market. The result is a register of millions and a market of a few thousand active hands.

It also explains the curious divorce between Nepal's primary and secondary markets. Millions of accounts were opened, overwhelmingly, to enter the lottery for initial public offerings priced by regulation at or near par and with a long history of jumping on their first day of trading. Winning an allotment is close to free money; trading the resulting shares afterward is a different and far less popular pursuit. So capital floods in at the IPO window through the depository's blocked-amount system and then goes dormant, and a stock that popped on listing can drift sideways on negligible volume for years afterward. The primary market manufactures shareholders by the million; the secondary market struggles to keep a few thousand of them active on any given afternoon. A register that is wide attached to an order book that is narrow is the clearest single symptom of the gap between size and depth.

What price discovery means here

Pull the threads together and a coherent picture emerges, one that is neither the bull's triumph nor the bear's dismissal. NEPSE is a large market, genuinely large, relative to Nepal's economy that has not yet built the apparatus a market needs to price things well. Its capitalisation outran its liquidity; its liquidity arrives in credit-driven spasms rather than a steady institutional tide; its marginal buyer is a leveraged household rather than a valuing institution; its prices are bounded by limits that, in a thin market do as much disguising as protecting; and its sharpest moves track the political weather, not the earnings calendar. Each of these is a feature of price discovery that is present in form and weak in function.

None of this is a verdict on direction. A structurally shallow market can rise for years, and Nepal's has rewarded patient holders handsomely. The point is narrower and more durable: the price NEPSE prints is a lower-quality signal than its size implies. It carries more noise, more reflexivity, and more politics per rupee of information than a casual look at the capitalisation would suggest. For an investor, that is not a reason to stay away; it is a reason to treat the quote as the beginning of analysis rather than the end of it to assume that the last trade reflects who could borrow, who was forced to sell, and what the headlines said, at least as much as what the company is worth.

There is an irony worth sitting with. On the infrastructure that is easy to import electronic order matching, dematerialised holdings, online IPO applications, a working central depository Nepal has moved quickly and competently. A retail investor in Kathmandu can open a demat account, win an IPO allotment and trade from a phone with much the same ease as one in Mumbai. The piece that cannot be imported, because it has to be grown at home, is the one still conspicuously missing: a domestic pool of patient capital with a mandate to value companies and the size to act on it. The market laid the pipes before it grew the water to run through them.

The fixes are not mysterious, and most are already being attempted in fits and starts: a genuine institutional buy-side, which means pension and insurance money and a mutual-fund industry an order of magnitude larger than today's one-percent footprint; market-making and securities lending to put two-sided quotes on the long tail of names that barely trade; and a steadier hand on the margin tap so that liquidity stops switching on and off. Until then, the honest description of how Nepali equity trades is the one the data keeps returning. The market got big before it got liquid. It learned to print prices before it learned to discover them. And it still, most days, sets the value of a country's listed companies on a handful of borrowed, limit-bounded, politically charged trades and calls the result a closing price.