Nepal credit freeze is not a banking problem, its a production problem. Banks have money. Businesses don’t want it. The missing link is production.

Nepal’s banking system is flooded with liquidity, yet businesses are refusing to borrow.

Prior weeks at Nepalytix described banking sector earnings from the lender side, banks earning 19.3% more on a loan book growing only 4.4%, fee income substituting for interest income, the dispersion between the top three and bottom seventeen. The borrower side of that same fact has not been told. If banks are not lending, it is because Nepali businesses are not borrowing. And if Nepali businesses are not borrowing, the data on what they are actually doing, production levels, investment commitments, capacity utilization, sectoral output should show why. That is what this piece does. The structural diagnosis comes first; the policy implications follow.

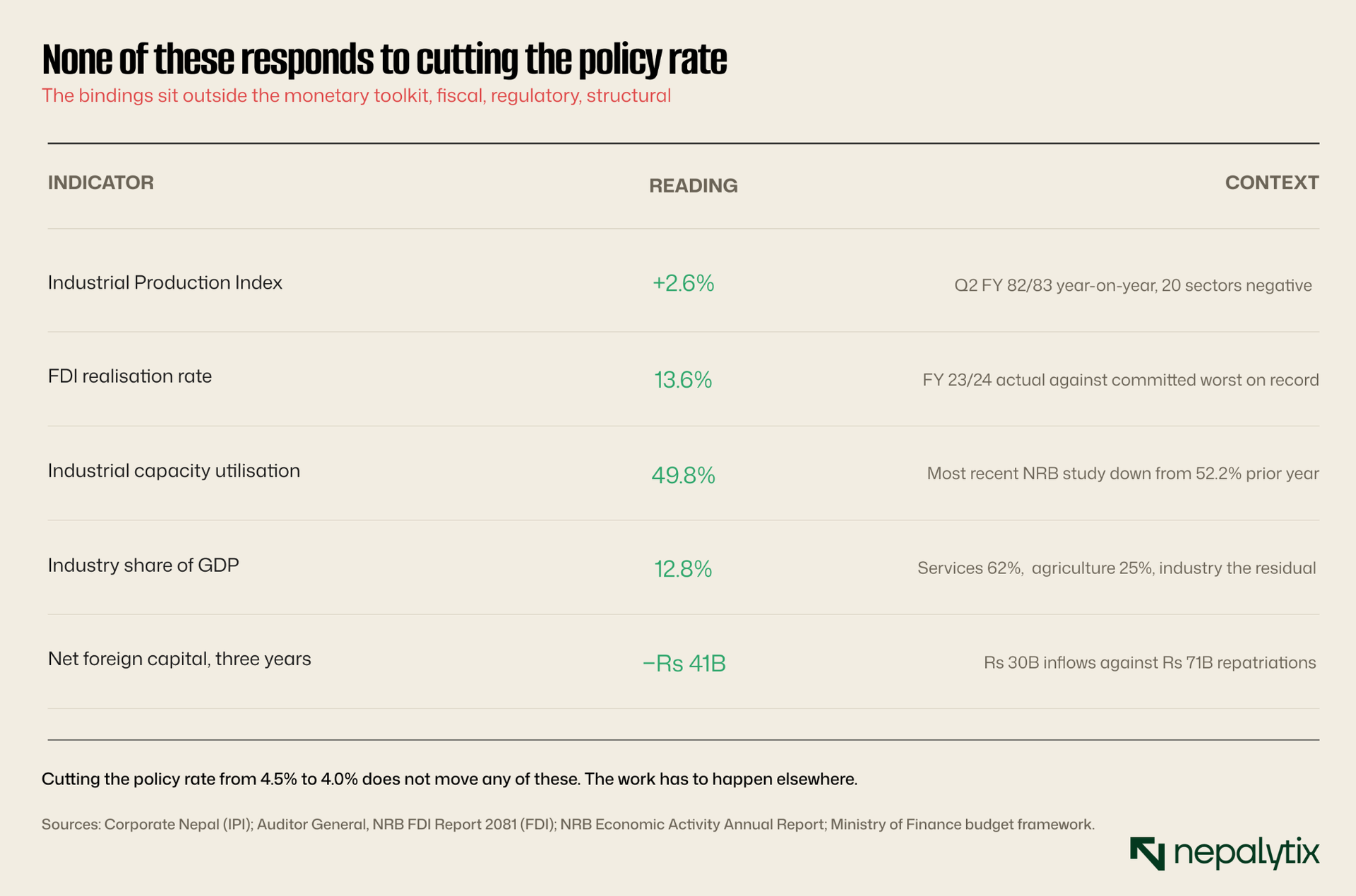

Industrial Production Index Q2 FY 2082/83 grew just 2.6 percent year-on-year, with 20 tracked sectors in negative growth. FDI realization rate has collapsed from 51.7 percent (FY 2019/20) to 13.57 percent (FY 2023/24) Rs 8.4 billion of actual inflow against Rs 61.9 billion of approved commitments. Industrial capacity utilization is below 50 percent. Industry is just 12.83 percent of GDP. These are the borrower-side facts. They explain why a 12 percent credit growth target cannot be hit by cutting rates.

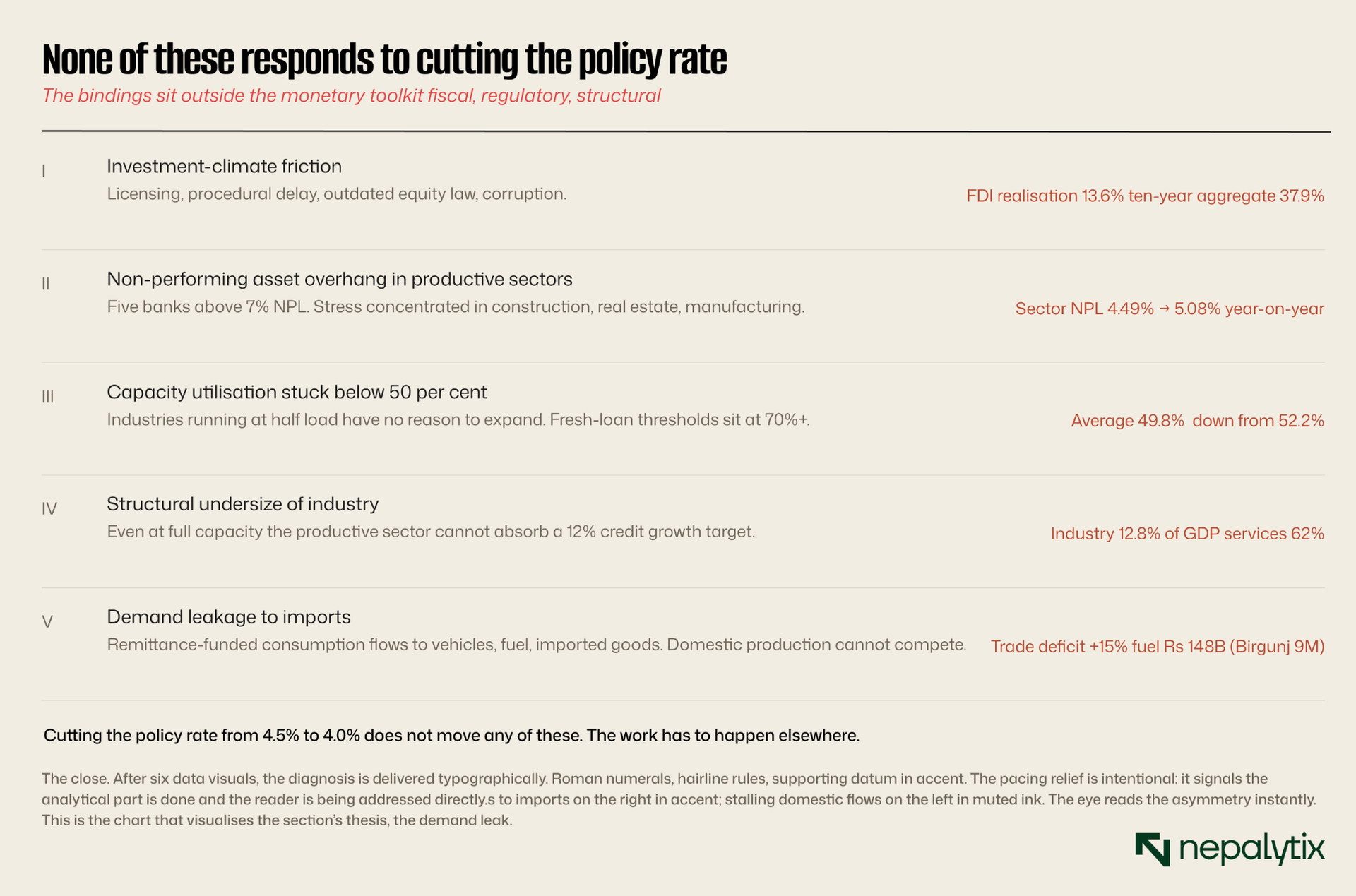

A sector contracting at 2.6 percent growth, with 20 sub-sectors negative and capacity utilization below half, does not borrow to expand. The Rs 838 billion in excess liquidity sitting at NRB is the mathematical consequence: banks have nowhere productive to lend. The constraints are structural: investment climate, NPA overhang, capacity, industrial undersize, demand leakage to imports. None responds to monetary policy.

From banks aren’t lending to business aren’t borrowing

The conventional analysis of Nepal's banking sector slowdown is a story about supply: banks have plenty of money, the central bank has cut rates, base rates are at multi-year lows yet credit growth remains stuck. Most commentary explains the gap by referring to bank risk aversion, NPL exposure, regulatory friction, or executive compensation incentives. These factors are real. They are not the whole story.

The complete story has two sides. On the supply side, banks are willing to lend at 4.5 percent above the base rate (which puts effective lending rates around 9 to 10 percent). On the demand side, Nepali businesses are not willing to borrow at those rates or any rates because the production opportunities those loans would fund are not generating returns that justify the borrowing. The 7.7 percent realized credit growth versus the 12 percent target is the equilibrium outcome of two forces meeting: bank supply at 9 percent rates and business demand at the existing production environment.

This piece is about that second side. What does the data say about Nepali business demand for credit? The Industrial Production Index, the FDI realization gap, the capacity utilization figures, the GDP composition and the trade flow data all tell parts of the same story. They suggest that the credit demand collapse is a structural condition of the Nepali productive economy in FY 2082/83 not a temporary stress response to high rates that monetary easing will reverse.

Industrial Production Index +2.6% Q2 FY 82/83

The most recent Industrial Production Index (IPI) data point is from Q2 of fiscal year 2082/83 (the period ending Magh, mid-February 2026) published by Corporate Nepal on April 7 2026 and reported by ShareHub Nepal. The headline figure: IPI grew 2.6 percent year-on-year. Underneath the headline, the more meaningful number: 20 tracked industrial sub-sectors registered negative growth against the prior year. The 2.6 percent headline is being carried by approximately ten or so sectors typically the ones that show up consistently in NRB Economic Activity Studies as positive performers (electricity generation, cement, vegetable oil, processed food, pharmaceuticals) while a broad swath of traditional industries (yarn, textiles, leather products, bricks, GI pipes, animal feed, soap, biscuits) contracted.

The implication for credit demand is direct. The simplest test of whether an industrial business will take a new loan is whether its output is growing fast enough to absorb the debt service. A yarn manufacturer that contracted 11.8 percent in Q2 is not in a position to borrow capital to expand; if anything, it is trying to refinance existing debt or extend amortization. A leather goods producer down 9.5 percent has the same problem. Across 20 sectors of the productive economy, the basic precondition for fresh credit demand output growth that justifies new borrowing is absent.

The pattern is not new. The same disaggregated structure showed up in NRB Economic Activity Studies for FY 2079/80 and FY 2078/79: a handful of sectors carrying the headline, with most traditional industries either flat or contracting. What is new is that the rate environment has changed dramatically (base rates from 10.03 percent in FY 2022/23 to 5.78 percent currently) without producing a meaningful response on the production side. If lower rates were going to revive industrial production, the response would already be visible. It is not.

The FDI realization gap

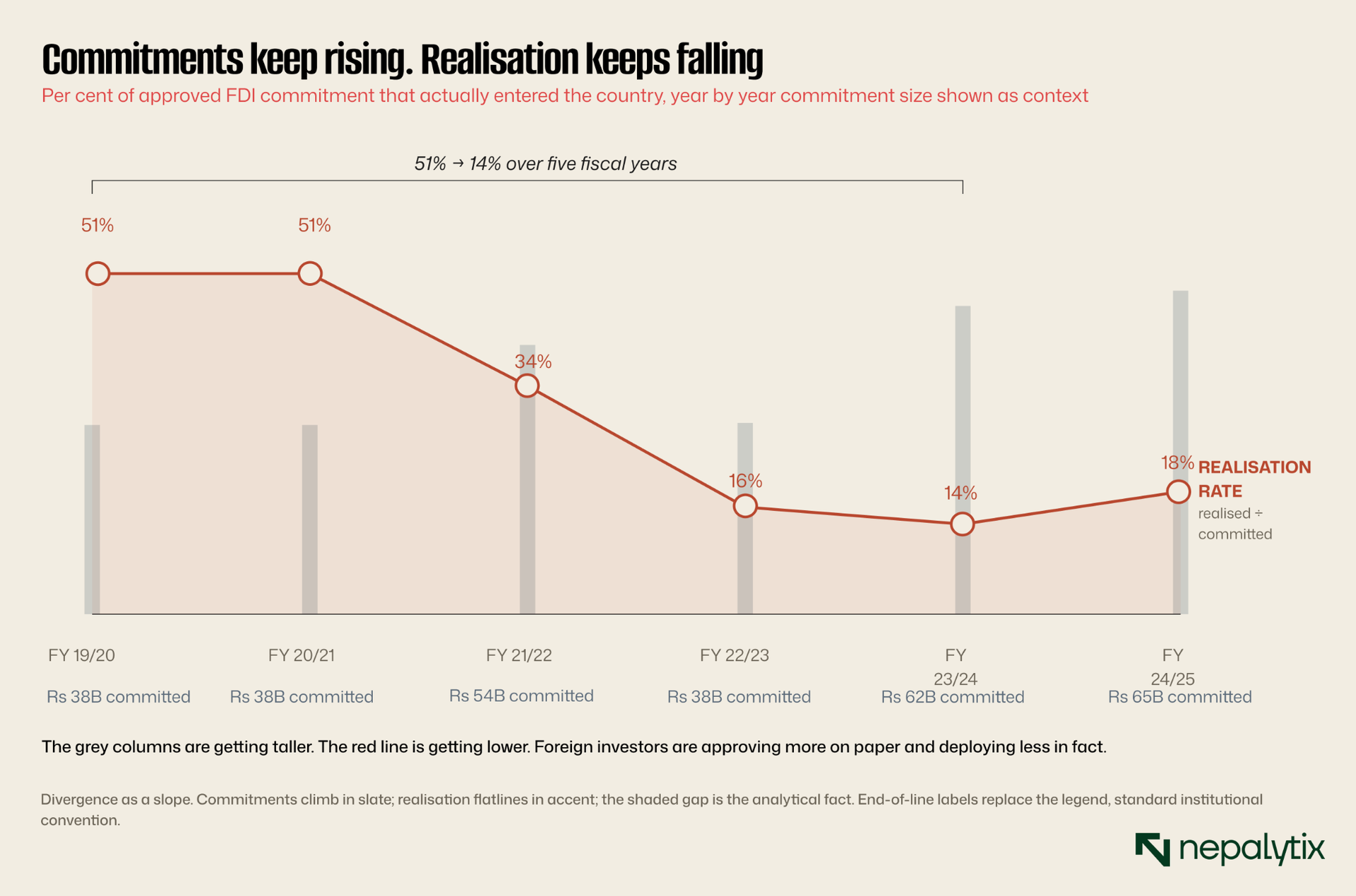

The most striking data point in Nepal's investment landscape is not the size of foreign direct investment commitments. It is the gap between commitments and actual realization. Across the past decade, Nepal received approved FDI commitments of approximately Rs 395.92 billion. Actual inflows totaled approximately Rs 126.29 billion. That is a 37.89 percent ten-year realization rate. For every Rs 1 of commitment, only 38 paisa of capital actually entered the country.

The trend is worse in recent years. FY 2019/20 realization: 51.7 percent. FY 2021/22: 34.27 percent. FY 2022/23: 16.06 percent. FY 2023/24: 13.57 percent, Rs 8.4 billion of actual inflow against Rs 61.9 billion of approved commitments. The Auditor General's most recent annual report quantified this directly: over the past three years, Nepal received Rs 30.34 billion in FDI inflows while seeing Rs 71.42 billion flow out of the country in repatriations and withdrawals. That is a net OUTFLOW of approximately Rs 41 billion of foreign capital from a country that is supposedly attracting record commitments.

Why is the gap so wide? The answer in nearly every primary-source analysis of the issue is the same: structural friction in the investment climate. Procedural delays in approvals. Outdated laws governing foreign equity participation. Licensing requirements that effectively gate market entry. Corruption in the approval chain. World Bank Doing Business indicators that consistently rank Nepal in the bottom quartile of comparable economies. Nara Bahadur Thapa, former executive director of Nepal Rastra Bank, framed the issue directly: "Foreign investors will no longer show interest unless Nepal's 'license rule' ends. Pre-approval does not mean much unless the investment process is genuinely simplified."

The implication for credit demand is consequential. If foreign investors who are far better positioned than Nepali domestic businesses to bring fresh capital to productive uses are choosing not to deploy 86 percent of what they commit, the domestic investment climate is the binding constraint. Nepali businesses face the same constraints with less leverage. The credit growth that Nepali banks are not producing is the same investment that foreign investors are not realizing.

The capacity utilization problem

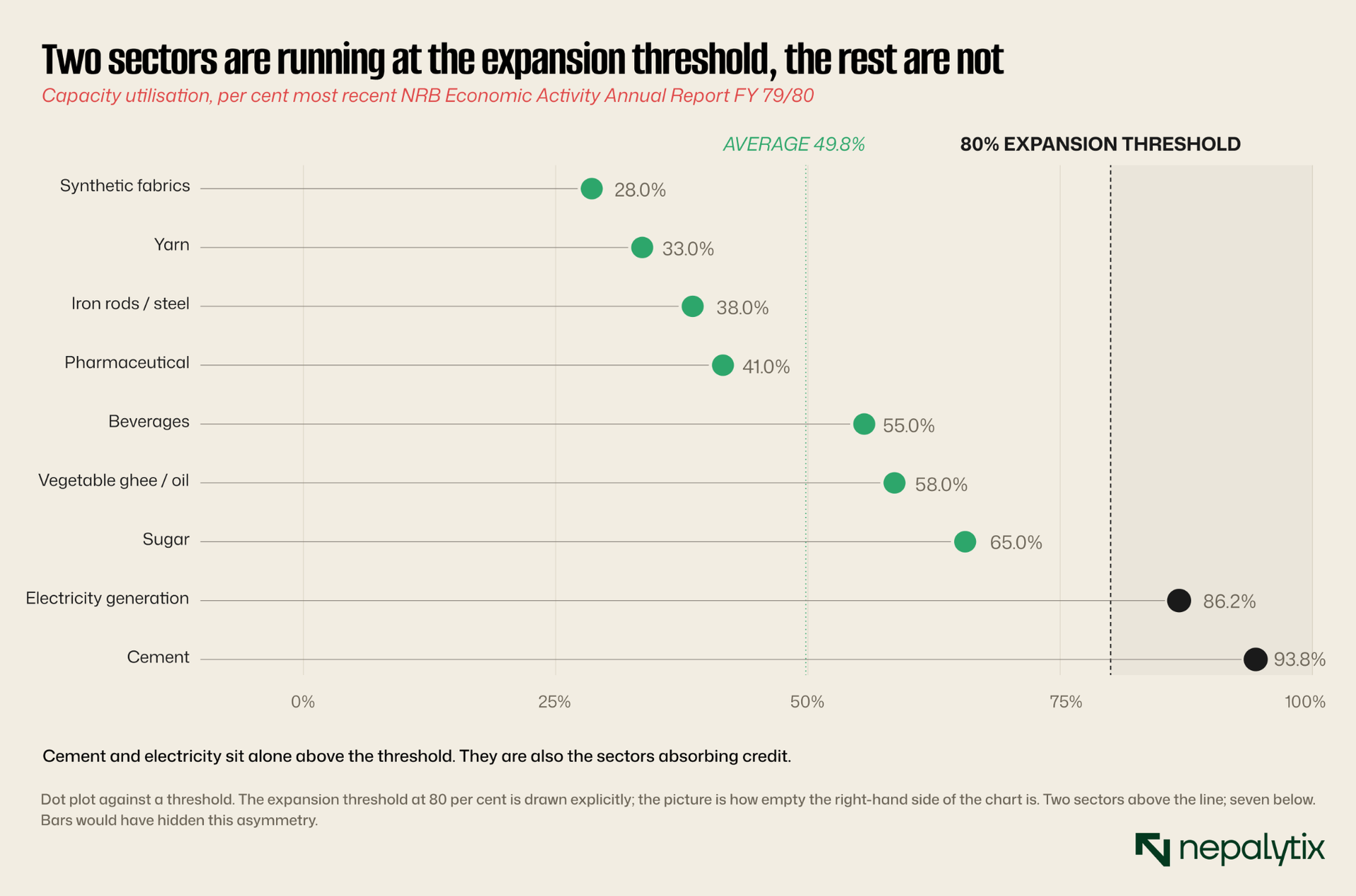

Even setting aside whether new investment is happening, existing industrial capacity in Nepal is being underutilized. The most recent NRB Economic Activity Annual Report (covering FY 2079/80) found average capacity utilization across tracked industries at 49.8 percent meaning Nepal's industrial base is producing less than half of what its installed equipment is capable of producing. That figure was down from 52.2 percent the prior year, indicating utilization is moving in the wrong direction even before the most recent macroeconomic stress.

The economics of capacity utilization for credit demand are simple. A business running at 30 percent capacity has 70 percent of its existing investment sitting idle. It has no reason to borrow new capital to expand capacity that it is already not using. The standard threshold for fresh expansion borrowing in industrial economics is roughly 80 percent capacity utilization above that level, the marginal returns to additional capacity are positive enough to justify the cost of capital. Below that threshold, the rational response is to wait for demand to absorb existing capacity before adding more.

Nepal's productive economy is below the expansion threshold across most sectors. The notable exceptions: cement and electricity generation are the sectors where bank credit has been growing fastest. That is not a coincidence. Cement is at 93.8 percent utilization because public infrastructure spending and hydropower construction have created persistent demand. Electricity at 86.2 percent reflects the secular growth in domestic and export power consumption. These are the sectors absorbing credit growth above the sector average. The rest of the industrial economy is not.

Industry is 12.83 percent of GDP, the maths doesn't close

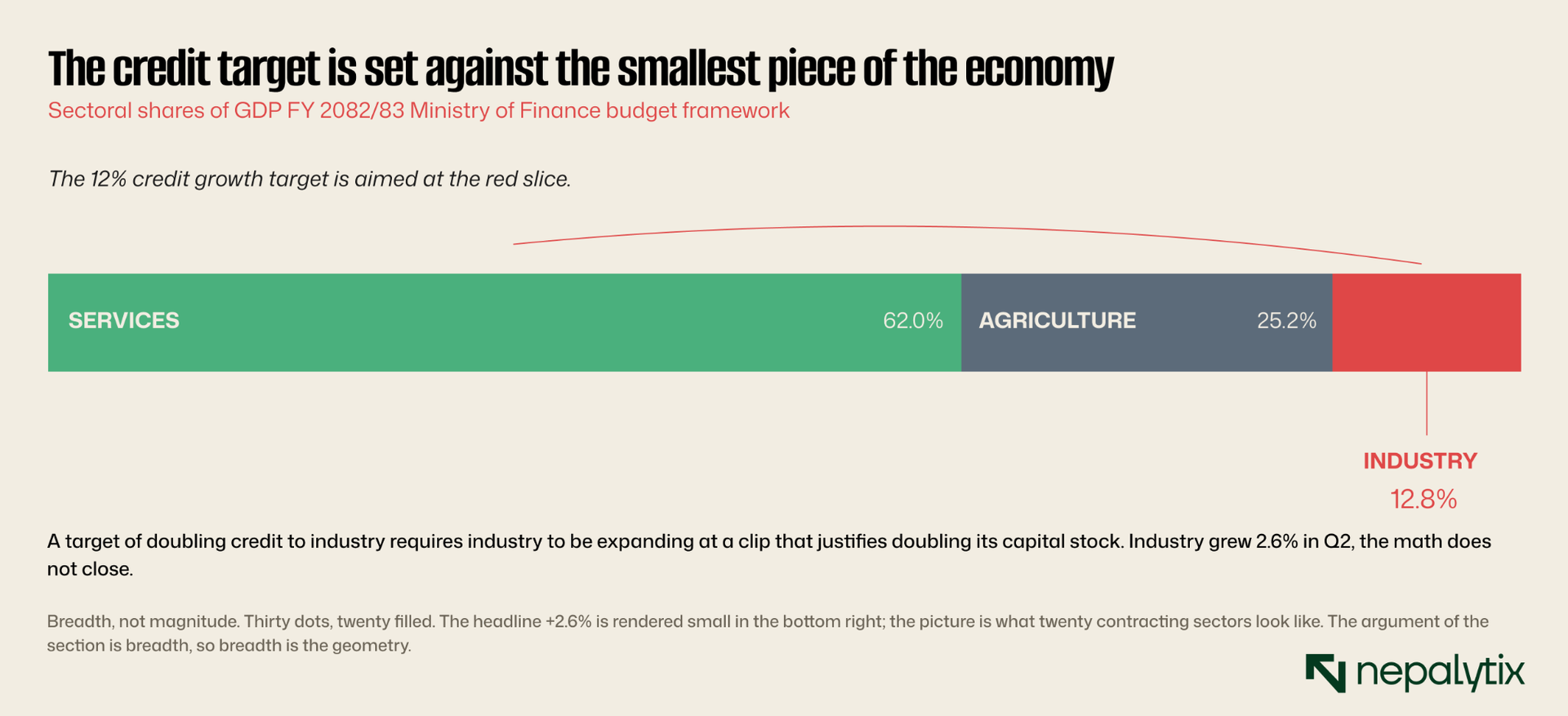

The most consequential structural fact about the Nepali economy is hidden in plain sight in the GDP composition. The sector that monetary policy targets when it sets a credit growth ambition like "12 percent expansion in private sector credit" is just 12.83 percent of total GDP. Services represent 62 percent. Agriculture represents 25 percent. The productive industrial sector that is supposed to absorb fresh credit and translate it into output expansion is the smallest piece of the economy.

Consider the arithmetic. If industry is 12.83 percent of GDP and the credit-absorbing share of that industry (excluding small-scale agriculture and cottage industries that don't typically use commercial bank credit) is perhaps 8 percent of GDP, then a 12 percent expansion of credit going to this sector would mean an effective doubling of bank credit-to-industry over a multi-year period. That requires industry to be expanding at a clip that justifies a doubling of its capital stock. Industry contracted in dollar terms in 2023, grew at 2.6 percent in IPI for Q2 FY 82/83 and is running at 49.8 percent capacity utilization. The math does not close.

This is the structural diagnosis that monetary policy alone cannot solve. The Nepali economy is service-dominant and remittance-driven. The fastest-growing demand categories are consumption goods (vehicles, electronics, fuel) that flow disproportionately to imports rather than to domestic production. Nepal does not have the productive industrial base to absorb a 12 percent credit expansion at any rate. The constraint is the size and competitiveness of the productive sector, not the cost of money.

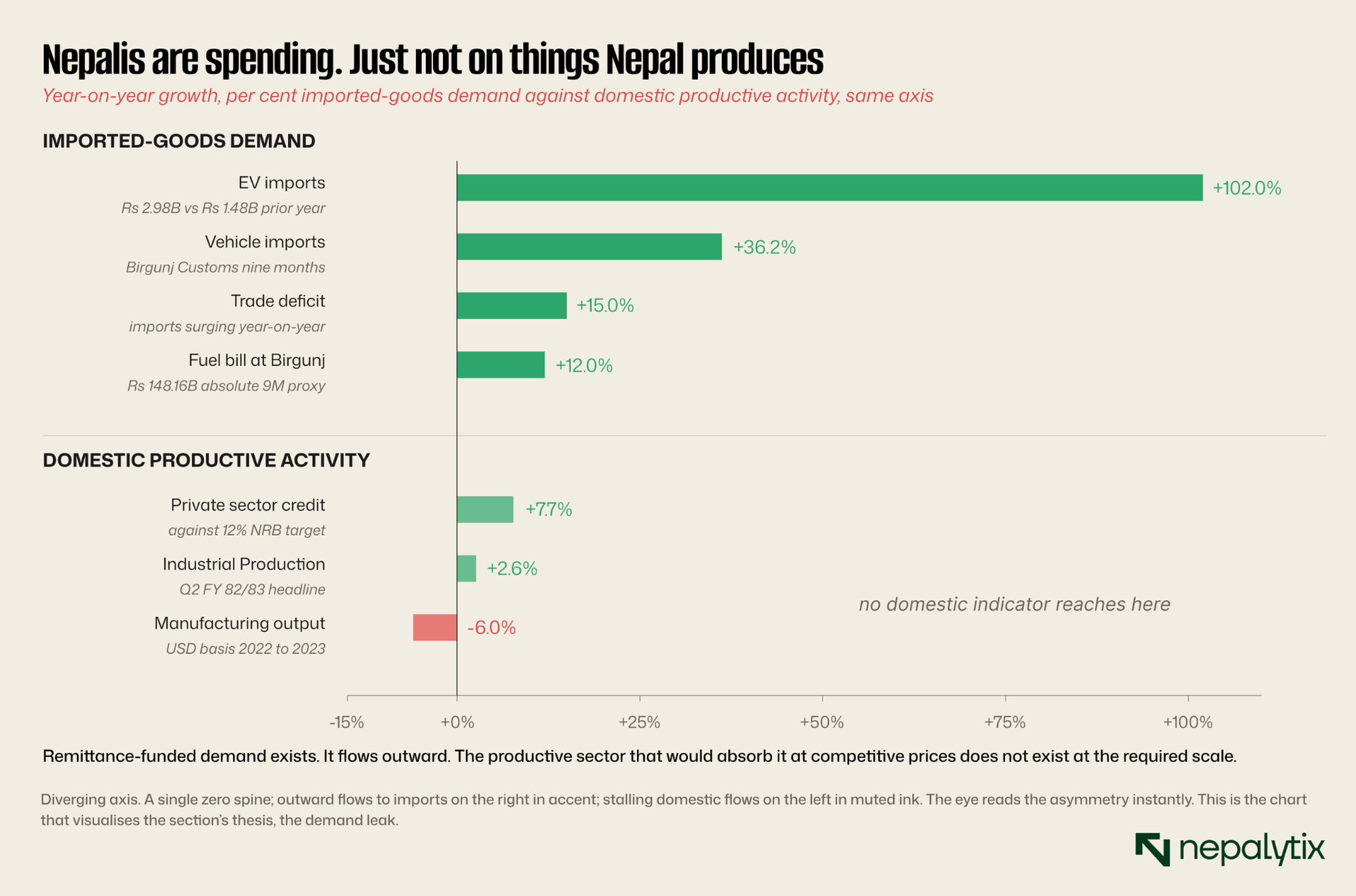

Imports surge while domestic production stalls

One temptation when reading credit growth data is to conclude that aggregate demand in Nepal is weak and that the credit slowdown reflects an absence of consumer or business spending appetite. The data contradicts this read. Aggregate Nepali demand for goods is alive and growing. It just does not flow to domestic production.

The details are informative. Vehicle imports through Birgunj Customs alone grew 36.19 percent in the first nine months of the recent reporting period. Electric vehicle imports specifically surged 102 percent year-on-year. Fuel imports through Birgunj reached Rs 148.16 billion over nine months generating roughly Rs 60 billion in customs revenue. The trade deficit widened by approximately 15 percent. Nepali consumers and businesses are absolutely spending money on tradable goods. The money is moving. It is just moving outward, to imports rather than recirculating through domestic production capacity.

This is the demand-leak. Remittance inflows fund household consumption. Household consumption translates into demand for goods. The goods come from India, China, third countries, rather than from Nepali factories operating at 49.8 percent of capacity. Nepali domestic production cannot compete on price, scale, or product quality with the imported alternatives. So the demand exists, but it does not generate the productive-sector credit growth that monetary policy is trying to engineer. The Rs 148 billion fuel bill is a Nepali demand fact; it produces zero Nepali productive credit growth because the production happens overseas.

Five non-monetary binding constraints

Pulling the data together, the credit demand collapse in FY 2082/83 is best understood as the surface manifestation of five structural binding constraints. None of them responds to monetary policy. All of them require coordinated action across fiscal policy, regulatory reform, and structural investment-climate initiatives.

The FY 83/84 Monetary Policy Statement from NRB, expected in mid-Shrawan (late July 2026), will face a difficult choice. Cutting the policy rate further from 4.5 percent to 4.25 percent or 4.0 percent is the action with the most institutional momentum. Setting another aspirational 12 percent credit growth target will continue the pattern of unmet expectations. Neither addresses the underlying constraints. What would be more consequential is direct NRB advocacy for the structural reforms that lie outside its mandate but determine the success of its policy: faster automatic FDI approval routes, an operational Asset Management Company for NPA resolution, simplified working capital loan guidelines for productive sectors, and explicit fiscal coordination on productive-sector investment.

The credit demand collapse is not a temporary cyclical phenomenon. It is the FY 2082/83 expression of long-running structural facts about the Nepali economy. The Industrial Production Index growth rate, the FDI realization rate, the capacity utilization figure, the GDP composition, and the trade flow data are all consistent with each other. They tell the same story from different angles. Banks lending to a productive sector that is contracting, foreign investors approving but not deploying capital, industries running at half capacity, services and imports absorbing the demand that domestic production cannot serve, these are facets of the same condition.

The most important implication for the next twelve months of Nepali financial markets: the binding constraint on banking sector earnings, listed equity sector growth, and macroeconomic recovery is not the cost of central bank funding. It is the productive-sector demand environment. Until the data on IPI, FDI realization, capacity utilization, and trade composition starts to move, the credit growth target will continue to be missed, banks will continue to earn through fee income rather than interest expansion, and the Rs 838 billion of excess liquidity at NRB will continue to grow rather than shrink. That is what nobody is borrowing to tell us. It is the most important piece of information about the Nepali economy in FY 2082/83.