Nepal hydropower sector is mispriced by anyone reading it as a recovery play

The country has transitioned from a net electricity importer to a net exporter, backed by long-term export agreements with India and Bangladesh, accelerating capacity additions, and rapidly rising earnings among well-positioned IPPs like Sahas Urja.

The earnings strength visible in Nepali hydropower stocks through FY 2082/83 is not a cyclical recovery from a temporary downturn. It is the first quarterly evidence of a structural inversion. Nepal stopped being a net importer of electricity in 2024 and started being a net exporter. The 25-year India PPA has been signed. The tripartite Bangladesh agreement has been signed. The addressable market for Nepali hydropower output has expanded by an order of magnitude in three years. The market is still pricing the sector against the old reality.

Most published commentary on the recent strength in Nepali hydropower stocks frames it the same way. The sector had a couple of difficult fiscal years, the framing goes: monsoon variability, transmission constraints, delayed PPAs, NEA dispute backlog. Now the difficulties are easing. Earnings are recovering. The stocks are recovering. Buy the recovery story. This is the wrong story.

It is the story you tell when the underlying numbers fit the cyclical-recovery template and you have not bothered to check whether the template applies. Look at the actual data, and what you see is not a sector recovering from problems. You see a sector reorganizing itself around a structural fact that did not exist three years ago: Nepal has electricity to sell, and the buyers have signed contracts to buy it.

Three pieces of evidence make this case. The first is the export trajectory. The second is the rate at which Nepal is adding installed capacity. The third is the cluster of long-term power purchase agreements that have actually been signed since January 2024. None of these is consistent with a cyclical-recovery framing. All of them are consistent with a structural-shift framing. The earnings numbers from individual listed hydropower stocks Sahas Urja Q3 9M FY 2082/83 net profit of Rs 1.18 billion versus Rs 834 million the prior year, up 41.5 percent are not anomalous data points to explain. They are the predictable output of the structural shift, working its way through the income statements of the well-positioned players.

Nepal stopped being a net importer of electricity

For the entire post-independence history of the Nepali electricity system, the country has been a net importer of power from India. The arithmetic was simple. Nepal's installed generation capacity was insufficient to meet peak demand. The deficit was covered by import from the Indian grid. As recently as the 2018-19 peak demand of 1,320 megawatts, Nepal's installed capacity sat at 1,182 megawatts and the country was importing roughly 38 percent of total electricity consumption from India.

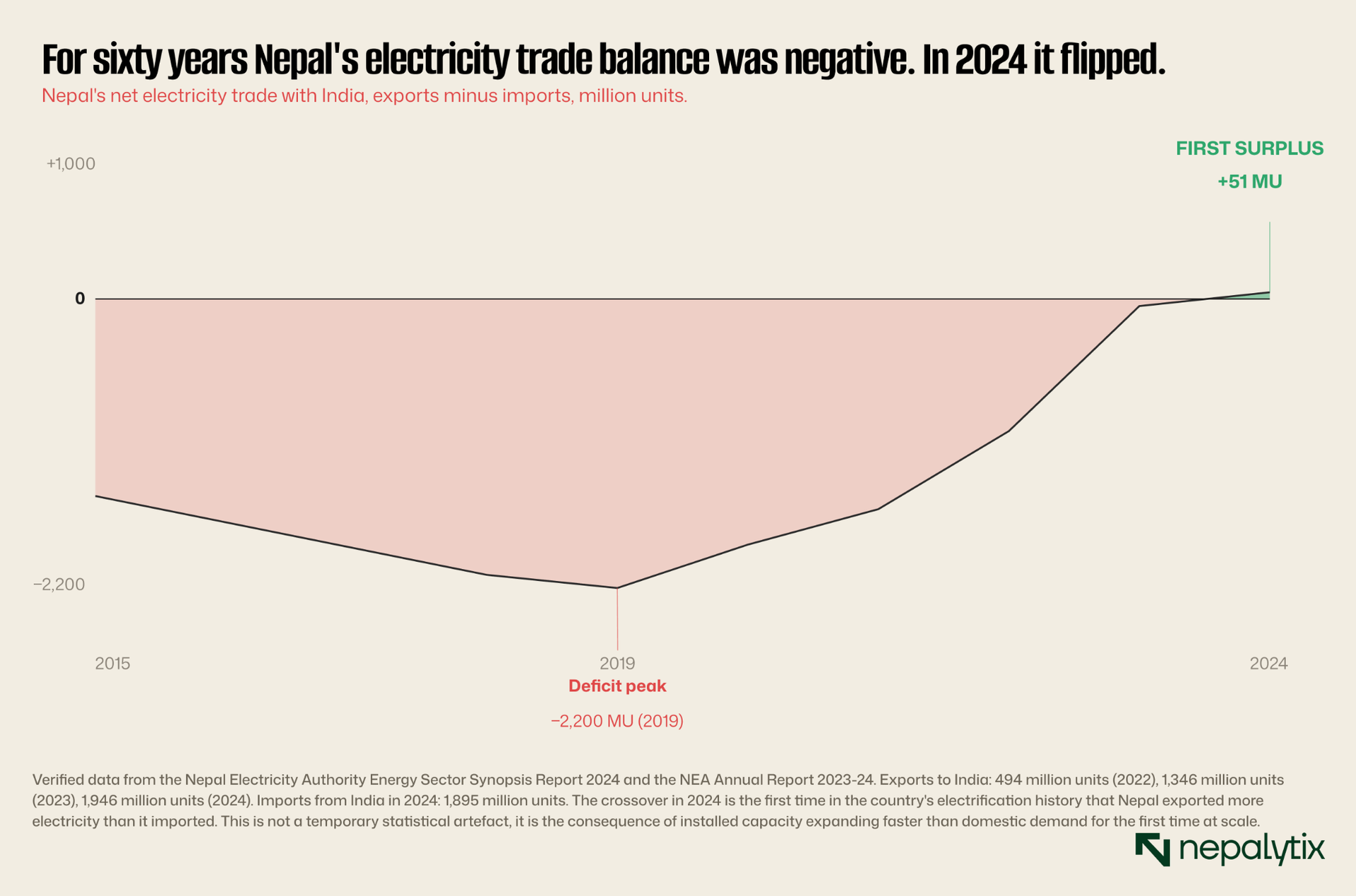

That was the structural condition that defined the sector for sixty years. That structural condition ended in 2024.

Read the numbers as a sequence. Exports to India in 2020: approximately 30 million units. 2021: approximately 100 million units. 2022: 494 million units. 2023: 1,346 million units. 2024: 1,946 million units. That is roughly a 4-times increase in just two years (2022 to 2024). Over the same period, imports from India trended down from a 2018-19 peak above 2,000 million units to 1,895 million units in 2024. In a system where exports and imports converge from opposite directions, the result is exactly what 2024 produced: a net exporter outcome that did not exist before.

This is not a number that turns back around on its own. The capacity behind the export figure has been built. It is operational. It is connected to the grid. The transmission infrastructure to India has been commissioned. The Day-Ahead Market arrangement with the Indian Energy Exchange has been operational since November 2021. None of these conditions reverses if the next monsoon is normal or if the next NEA general manager changes. The trajectory of the export figure may fluctuate around its trend line. The trend line itself is structural.

The capacity buildout is accelerating, not recovering

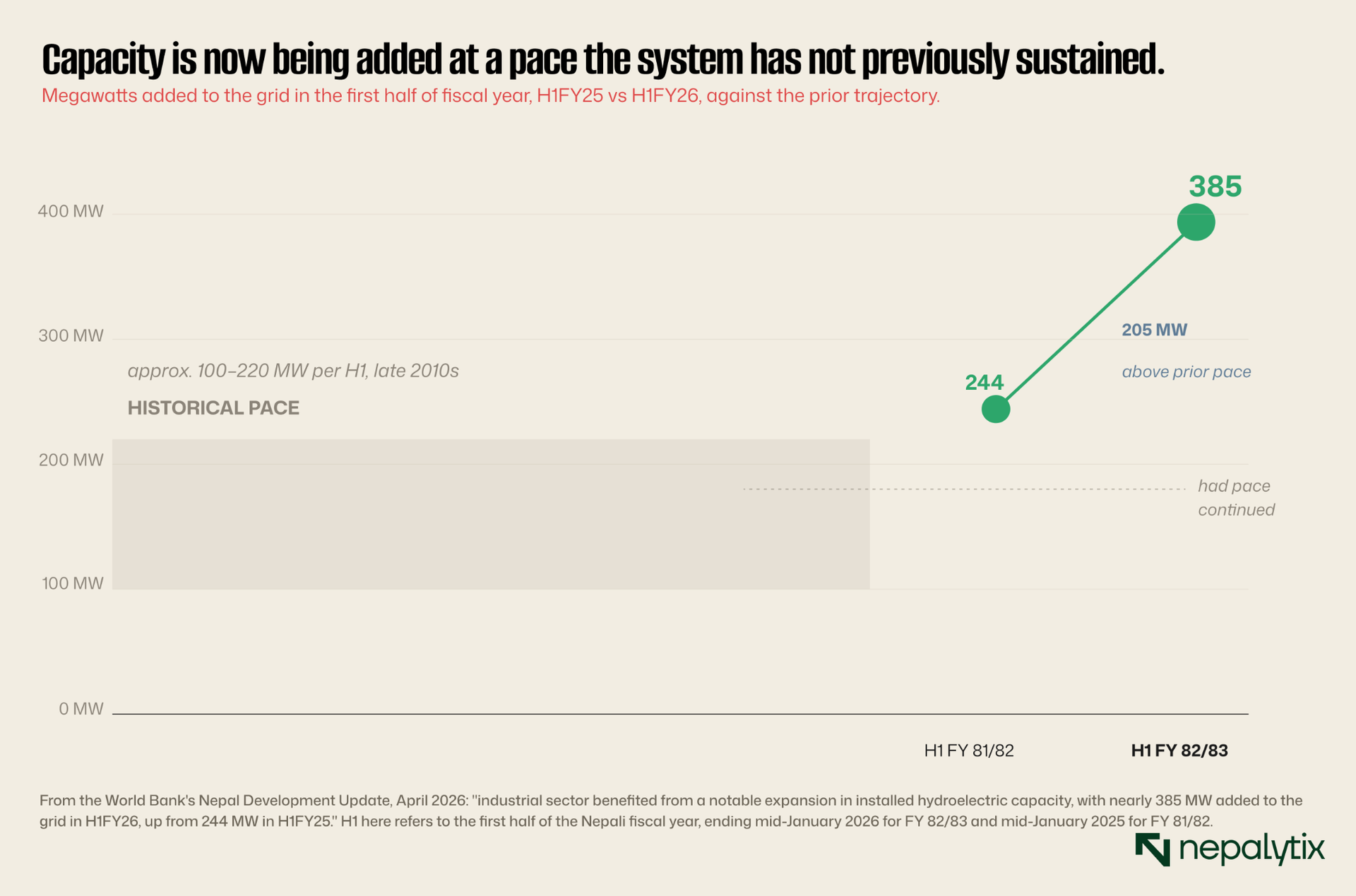

A recovery framing assumes that the system is returning to a prior equilibrium after a temporary disruption. What the capacity data actually shows is that the system is moving faster, not catching up. The World Bank's Nepal Development Update for April 2026 documents this directly. In the first half of fiscal year 2082/83 (mid-July 2025 to mid-January 2026), Nepal added approximately 385 megawatts of installed hydroelectric capacity to the national grid. In the comparable period of fiscal year 2081/82, the figure was 244 megawatts. That is a 58 percent year-on-year acceleration in the rate at which new capacity is coming online.

This is not what a recovering system looks like. A recovering system gradually returns to its prior pace of capacity addition. An accelerating system passes through its prior pace on the way to a higher one. Nepal is doing the second thing. The pipeline supports continued acceleration: roughly 5,809 megawatts of installed capacity is currently under construction across active projects, with a further 3,572 megawatts in the project development pipeline. The government's stated target of 28,000 megawatts of installed capacity by 2035 implies a sustained capacity addition rate that is substantially higher than anything the country has achieved historically.

Whether that 28,000 megawatt target is achieved on schedule is a separate question. What matters for the thesis of this piece is the direction of travel and the rate of acceleration. Both of those are pointing the same way. The sector is not returning to where it was. It is moving past it.

The addressable market has been contractualized

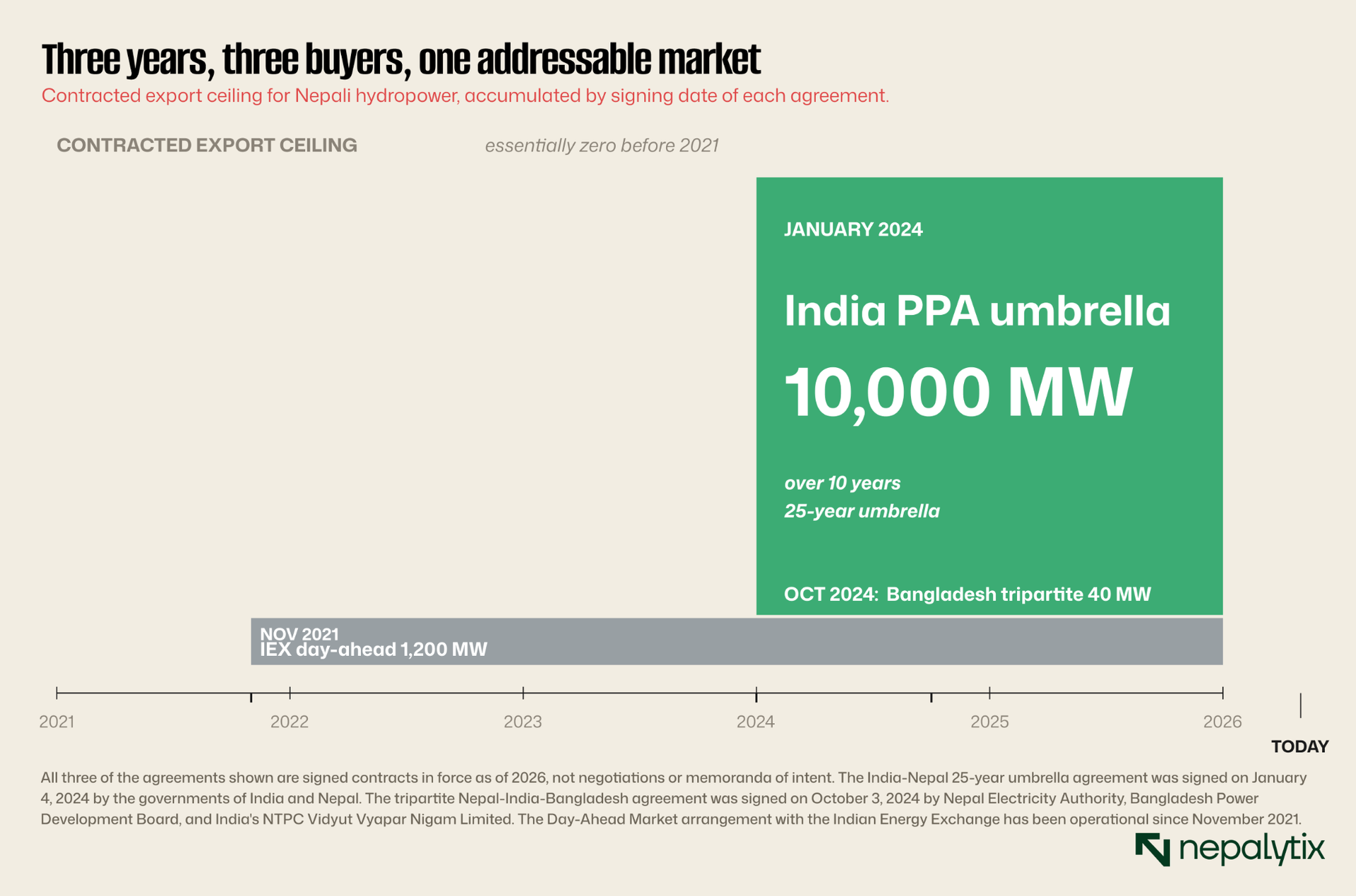

Capacity without buyers is generation without revenue. The third piece of evidence is the most consequential because it removes the demand-side uncertainty that has historically constrained Nepali hydropower investment. The structural fact is this: the long-term power purchase agreements have been signed.

The most consequential of the three is the India-Nepal 25-year umbrella agreement signed on January 4, 2024. The agreement targets 10,000 megawatts of Nepali electricity export to India over the next ten years and auto-renews every ten years thereafter. The agreement is an umbrella framework that enables medium-term and long-term sub-PPAs of 5 to 10 years to be signed under it. Nepal Electricity Authority and India's NVVN are now signing those sub-PPAs. Already, roughly 6,000 megawatts of PPAs have been signed with private power developers downstream of the umbrella agreement, and 3,000 megawatts of new project capacity is under construction post-signature.

The Bangladesh tripartite agreement signed in October 2024 is smaller in initial volume (40 megawatts) but structurally similar in import. The electricity flows through Indian transmission infrastructure (the Baharampur-Bheramara cross-border line) from Nepali producers to Bangladeshi buyers, at a contracted tariff of 6.40 US cents per kilowatt-hour. The initial volume is symbolic. The Bangladesh stated target is 9,000 megawatts of import by 2040. The architecture has been built. The volume can scale into it.

And the day-ahead market arrangement with the Indian Energy Exchange, operational since November 2021, provides the residual outlet for wet-season surplus electricity that the long-term PPAs do not absorb. NEA has been targeting 1,200 megawatts of wet-season export to India through this channel. The combination of long-term PPAs and day-ahead market access means that for the first time, the binding constraint on Nepali hydropower revenue is generation capacity rather than buyer availability.

Three years ago, the binding constraint was the reverse. Plenty of hydropower projects had been built, and they were generating, but their wet-season output was being spilled because there was no market to absorb it. The agreements signed between 2021 and 2024 changed that. The data on hydropower company earnings is now reflecting what changed.

The earnings are starting to show it

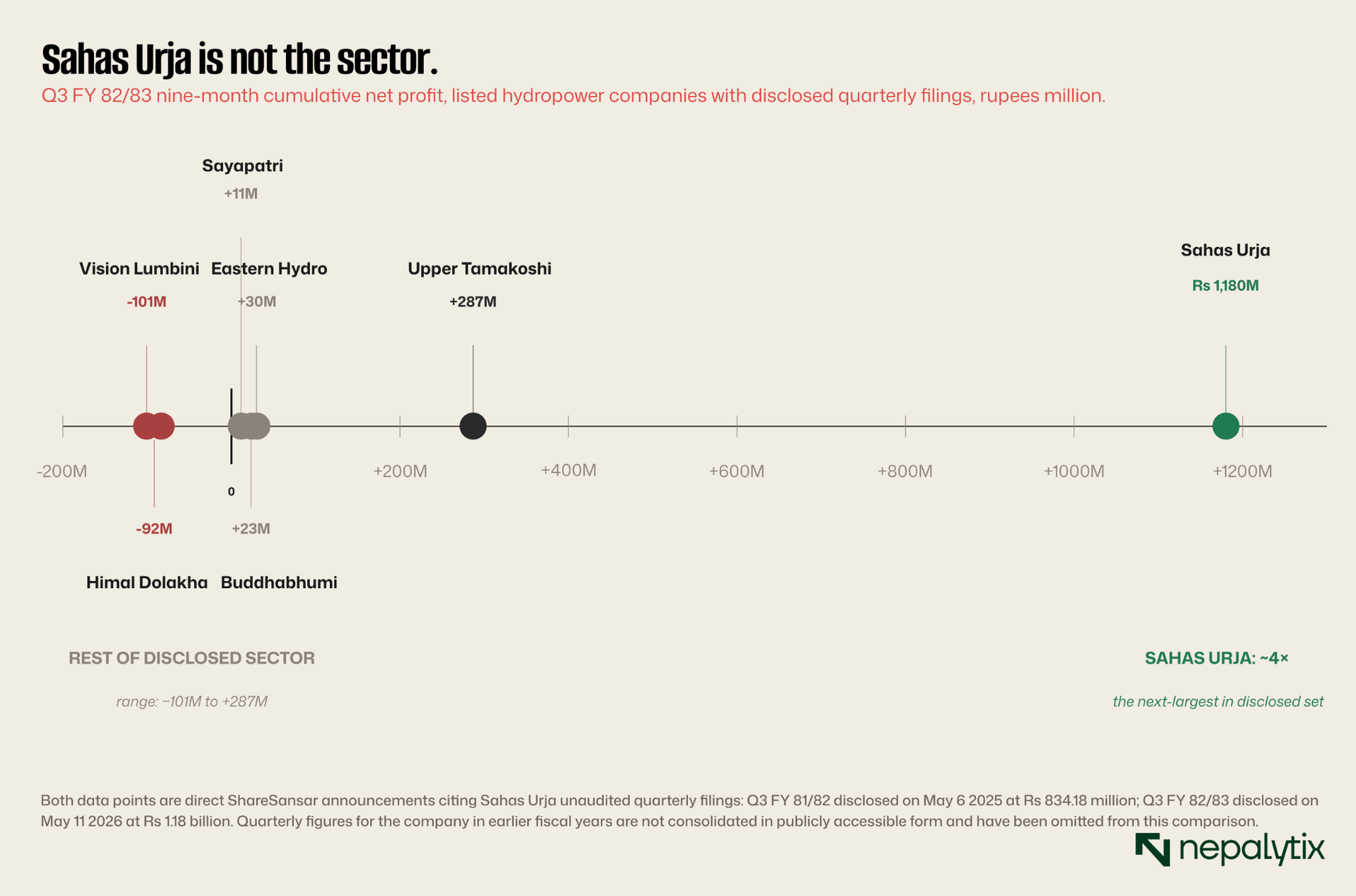

Look at Sahas Urja Limited, the listed independent power producer behind the 86-megawatt Solukhola Dudhkoshi project commissioned in 2023. The company's Q3 nine-month net profit through FY 2081/82 (mid-April 2025) was Rs 834 million. The equivalent figure for FY 2082/83 (mid-April 2026) was Rs 1.18 billion. That is a 41.5 percent year-on-year increase in cumulative nine-month net profit. The company declared a 22.1 percent dividend on FY 2082/83 profits, the highest in the listed hydropower sector.

Sahas Urja is not the largest listed hydropower stock by market capitalization. Upper Tamakoshi (456 megawatts, NEA-owned, market cap Rs 43.8 billion) and Chilime (the umbrella for several NEA-affiliated projects, market cap Rs 46.2 billion) are larger. But Sahas Urja is structurally the most interesting because it is a private-sector independent power producer whose commercial operations are entirely exposed to the structural shift. Its asset (Solukhola Dudhkoshi) was commissioned in 2023, the year before the India PPA was signed. Its operational track record is therefore short enough that no part of its earnings can be attributed to pre-shift operational normalization. The 41.5 percent year-on-year growth in Q3 nine-month profit is, in its entirety, the company benefiting from the post-shift environment.

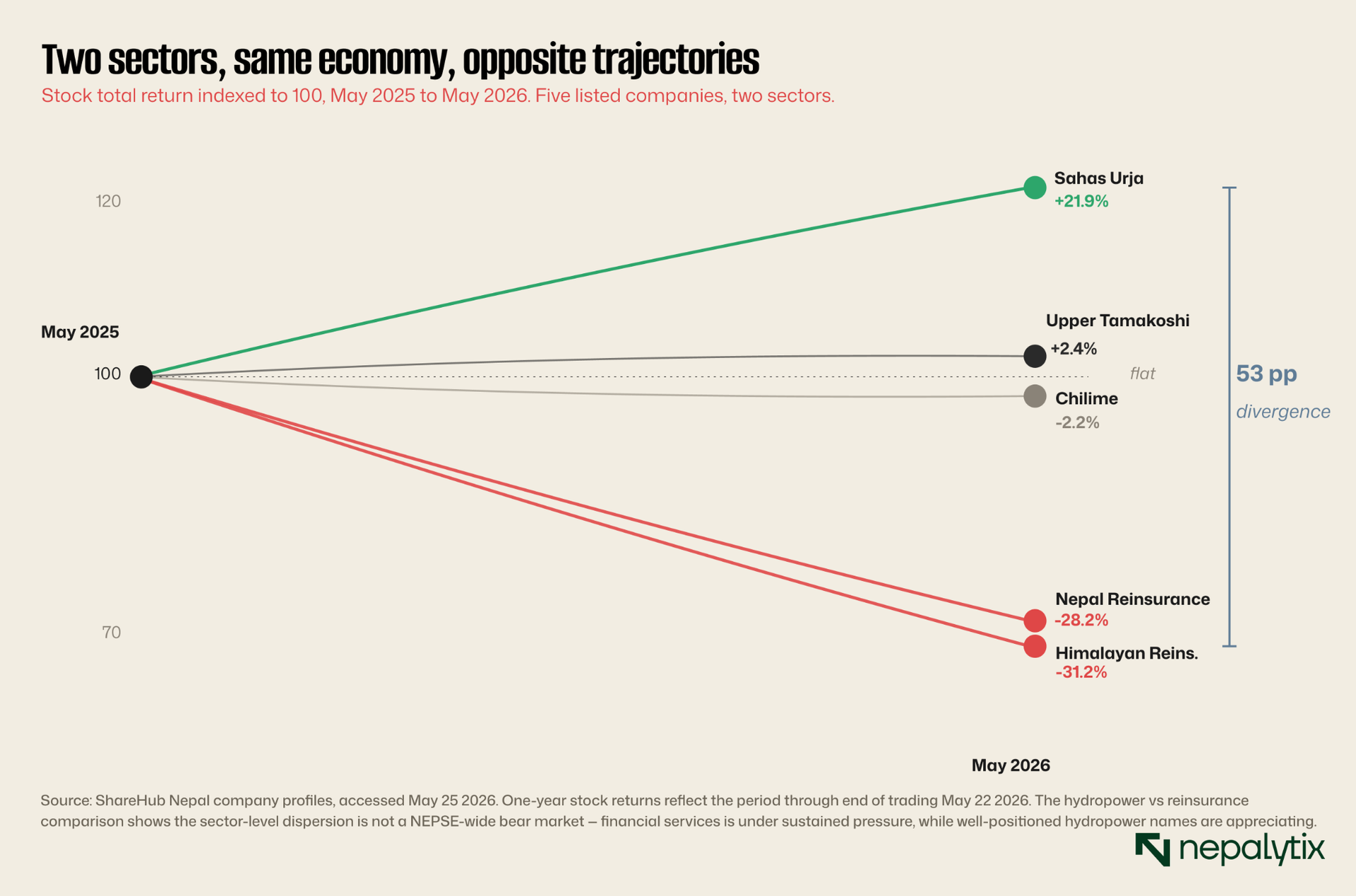

The dispersion is the signal. Sahas Urja is up 21.91 percent over the past year. Upper Tamakoshi is up 2.39 percent. Chilime is down 2.22 percent. The sector is not moving as a block.

Compared to the broader sector. Some listed hydropower companies are still posting Q3 9M FY 2082/83 losses (Vision Lumbini Urja Rs 100.56 million loss, Himal Dolakha Hydropower Rs 91.60 million loss). Some are flat. Sahas Urja's 41.5 percent surge is not representative of the sector. It is representative of the sub-set of the sector that is well-positioned for the structural shift IPPs with operational assets sized appropriately for the export market, located near transmission infrastructure to India, with PPAs that capture the wet-season surplus pricing dynamic.

That dispersion is itself part of the thesis. The structural shift does not benefit the sector uniformly. It benefits the companies whose assets are positioned to monetize the new addressable market. The market is currently pricing the sector as if all hydropower names move together. Sahas Urja's 22 percent one-year return alongside Chilime's -2 percent suggests the market is starting to differentiate. But the broader sector P/E multiples (Sahas Urja at 15.5x, Upper Tamakoshi at 114x, Chilime at 58x) still reflect company-specific operational metrics more than the structural sector tailwind. That gap is the mispricing.

What changes in the analysis

Three implications follow from reading hydropower as a structural shift rather than a cyclical recovery.

For investors in Nepali hydropower equity, the most important consequence is that historical price-to-earnings ratios for the sector are no longer the right comparison. The earnings power of well-positioned listed hydropower companies is structurally higher than it was three years ago, and it is going to remain structurally higher. Valuation multiples that look elevated against five-year historical averages may look reasonable against forward earnings power that reflects the addressable-market expansion. The relevant comparison is not whether Sahas Urja trades cheaply for its own history. It is whether listed Nepali hydropower trades cheap to the cash flow it will generate from contracts that have already been signed.

For policymakers and regulators, the most important consequence is that the sector's binding constraints have moved. They are no longer on the demand side. They are on the supply side transmission infrastructure to enable the contracted export volumes, project execution discipline to commission new capacity on schedule, regulatory simplification of the PPA process to keep the pipeline moving. The Ministry of Energy, Water Resources and Irrigation has roughly Rs 6.2 trillion of estimated infrastructure investment required to reach the 2035 capacity target. That investment must happen on the supply side of the equation, not on the demand side. The demand side has already been solved.

For the broader macroeconomic picture, the most important consequence is that Nepali hydropower has become one of the few visible sources of structural foreign exchange earnings for the country in an environment where the rest of the financial services sector is constrained by a low-rate, low-credit-demand environment. The Rs 1.22 billion of annual export revenue from the initial 40-megawatt Bangladesh tripartite agreement is small. The Rs 12 to 15 billion per year that would flow from the targeted 1,200-megawatt wet-season export to India at prevailing pricing is not small. The 10,000-megawatt PPA target, if realized over its ten-year horizon at current pricing, generates foreign exchange earnings of a different order of magnitude. None of this is in the consensus macro projection because the consensus macro projection treats hydropower as a recovery story rather than a structural one.

The recovery framing is convenient because it does not require updating priors. The structural framing is uncomfortable because it does. But the data exports up 4x, capacity adding 58 percent faster year-over-year, agreements signed that did not exist three years ago, earnings expanding at 40 percent for the well-positioned names is the data. The data does not fit the recovery template. It fits the structural-shift template.

Reading it as recovery is mispricing.