Nepal's Matribhumi Fund

Nepal's proposed Matribhumi Fund could become one of the country's most important economic institutions-or one of its biggest governance failures.

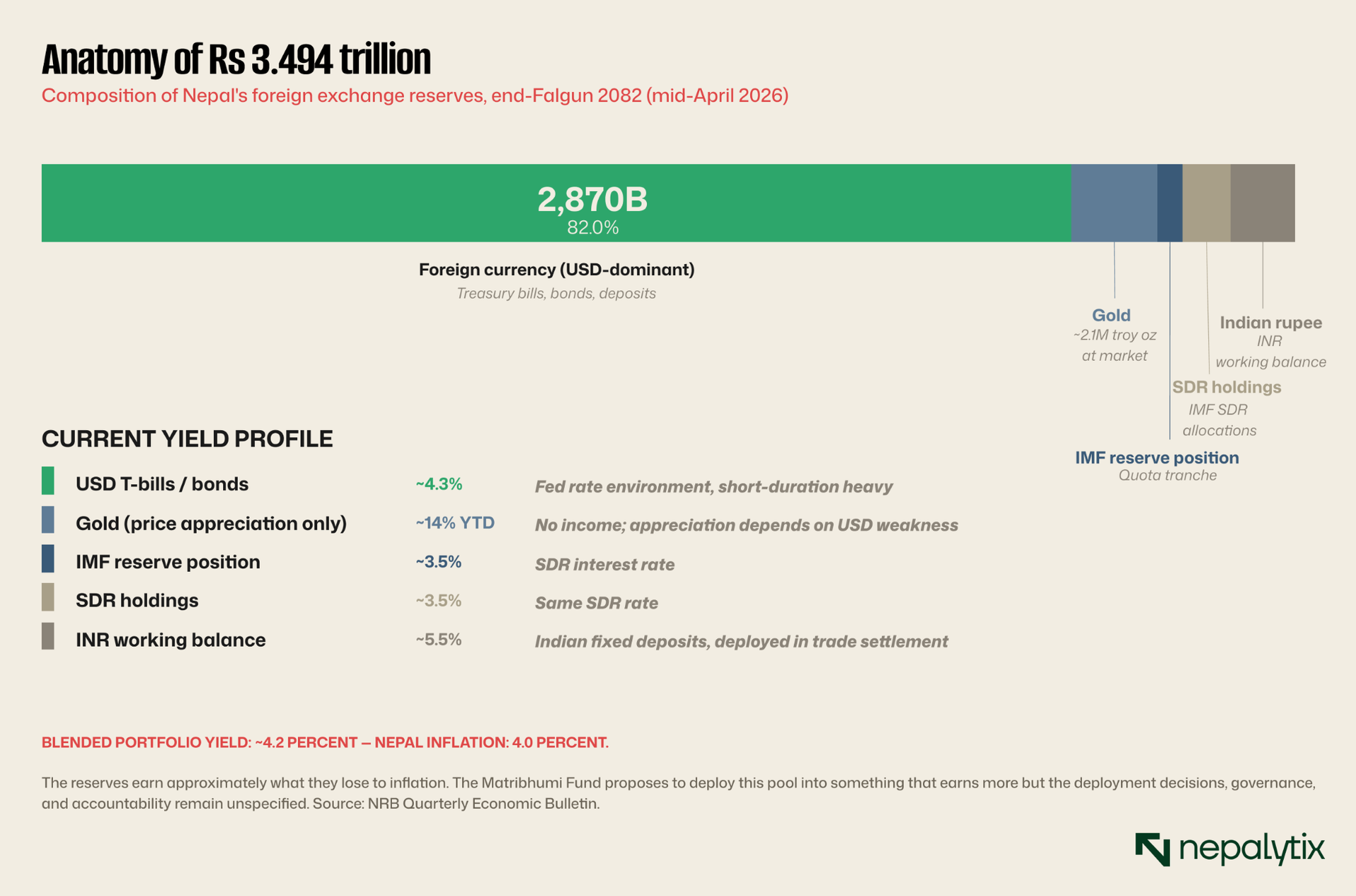

Friday's budget proposed a sovereign wealth fund the Matribhumi Fund to deploy a portion of Nepal's Rs 3.494 trillion in foreign exchange reserves. The market is treating it as a future-tense announcement. It is actually a present-tense governance test and the answer is being written in the next eight months whether anyone is watching or not.

The Matribhumi Fund got fewer than fifty words in Friday's budget speech. Finance Minister Swarnim Wagle announced that the government would mobilise a portion of Nepal's foreign exchange reserves through a newly envisioned Sovereign Wealth Fund to be activated when the reserve position remains comfortable. The stated initial use cases were strategic assets including an "AI factory," fuel storage, and clean-energy infrastructure. That was substantially the entire announcement.

Three things the announcement did not specify and each one matters more than what it did say. First, how much. The reserves are Rs 3.494 trillion; the fund is "a portion." A portion can mean 5 percent or 50 percent and the implications for the country's external position are completely different at those two values. Second, the governance architecture. Who sits on the board. How members are appointed. Whether they can be removed by the executive. What investment mandate is published and binding versus discretionary. Third, the oversight mechanism. Whether parliament gets real review authority or formal-only review. Whether independent audit is mandated or optional. Whether transparency disclosures are required or recommended.

None of these three were addressed in the budget speech. None of them appear in the supporting policy and program document. They will be addressed instead, in the implementing legislation that will be drafted, tabled, and debated in the next several months. That legislation is where the Matribhumi Fund actually gets built. The budget announced an empty box. The contents of the box are still being decided.

Sovereign wealth funds end up in wildly different places

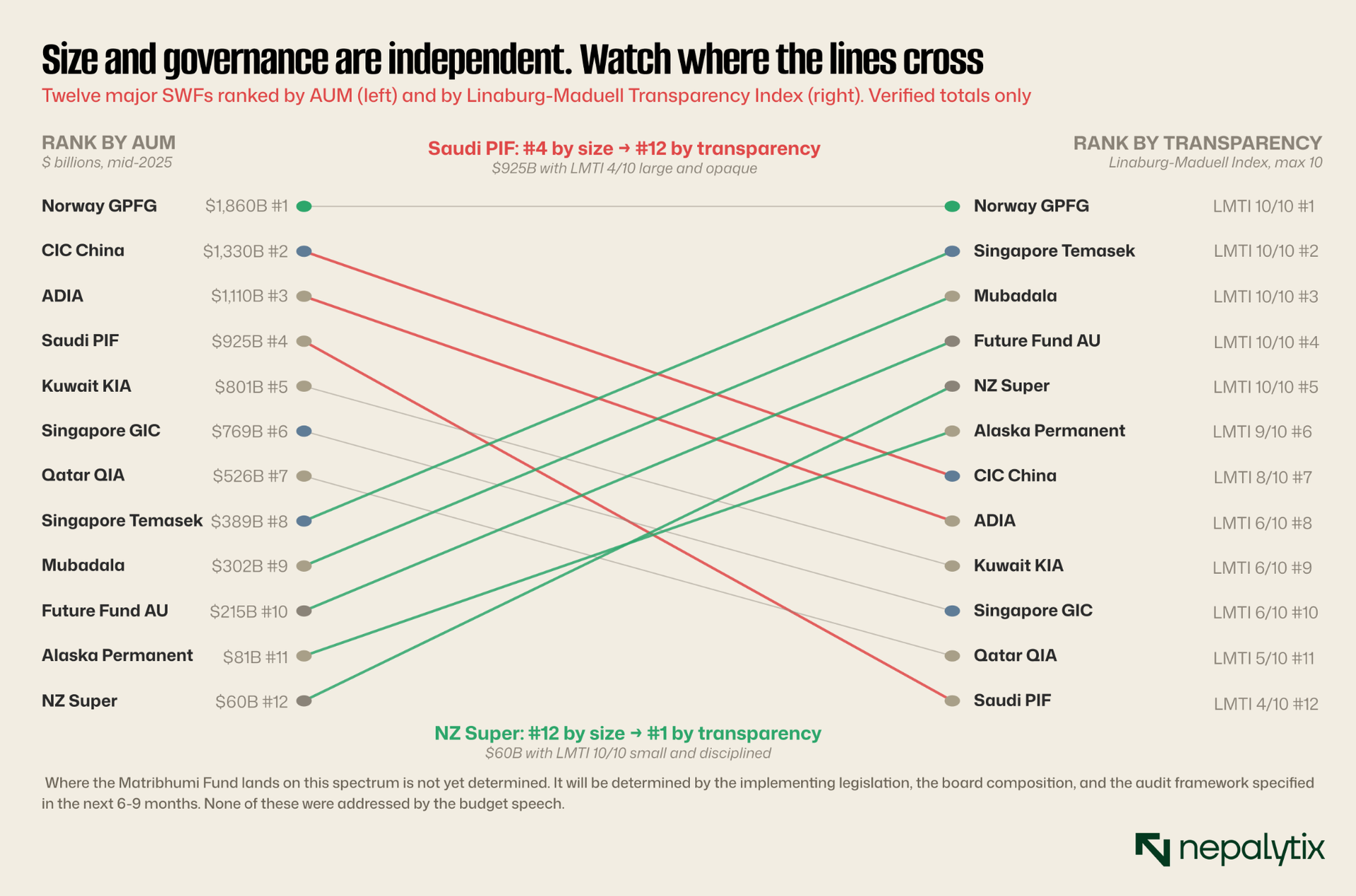

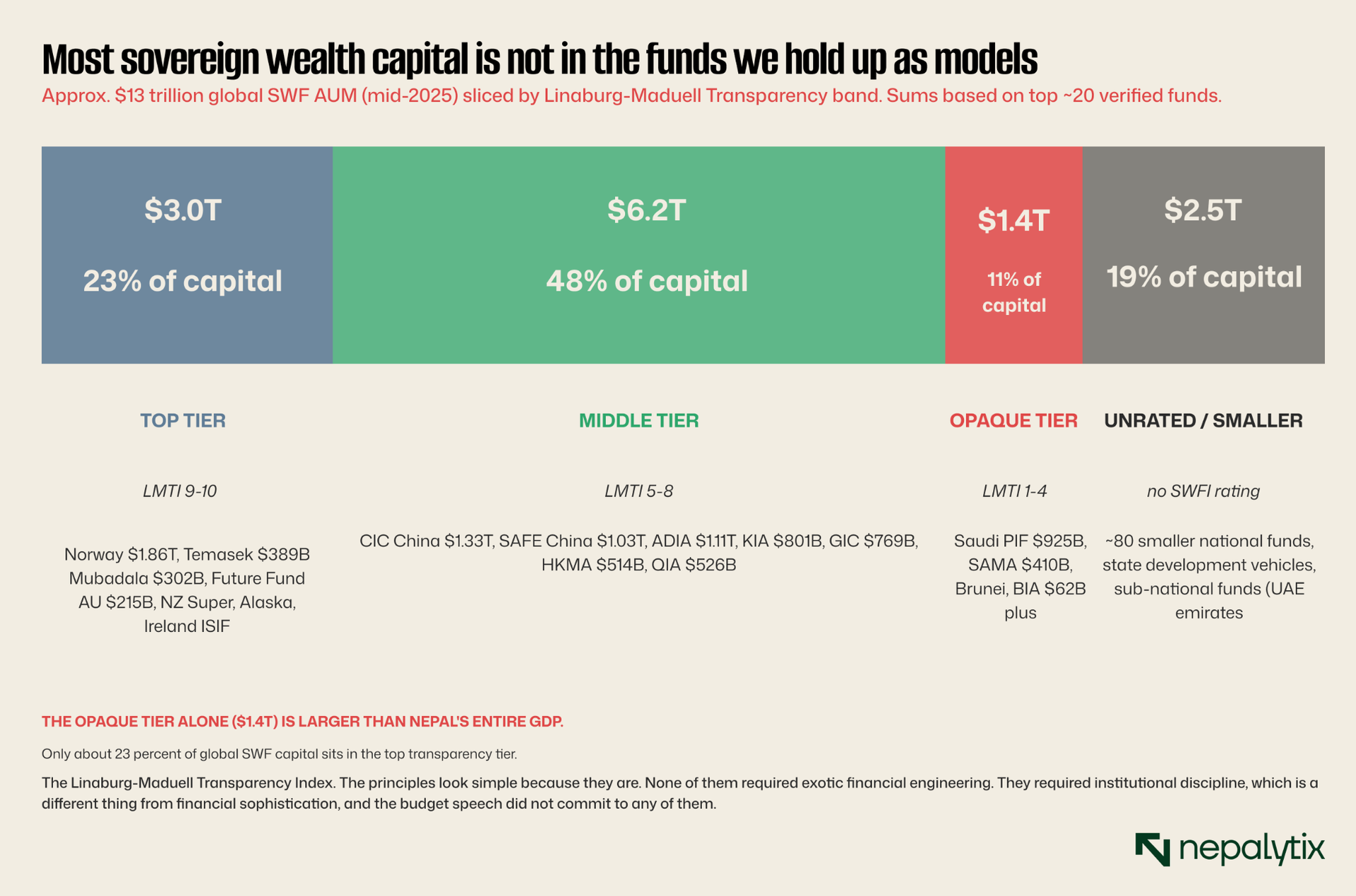

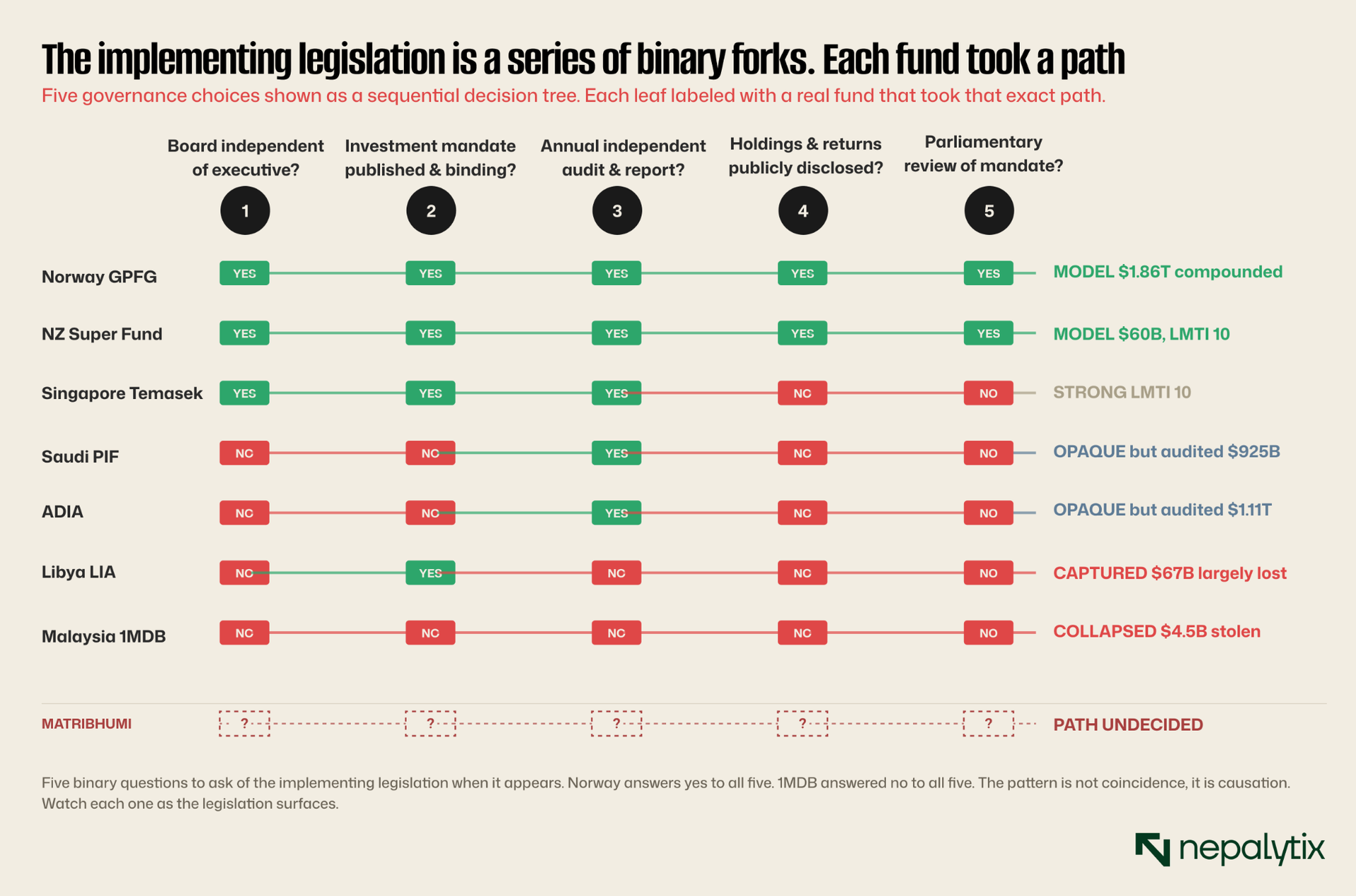

Worldwide, more than 100 sovereign wealth funds manage roughly $13 trillion in assets. They look superficially similar to government-owned investment vehicles mostly funded from reserves or commodity revenues. But their outcomes diverge enormously. Norway's Government Pension Fund Global has grown from oil revenues to $2.2 trillion equivalent to more than $390,000 per Norwegian citizen scoring a perfect 10 on the Linaburg-Maduell Transparency Index, the global benchmark for SWF governance quality. Singapore's Temasek with roughly $300 billion under management scores the same 10. Norway's GPFG and Temasek are the two most-studied success cases in the SWF literature.

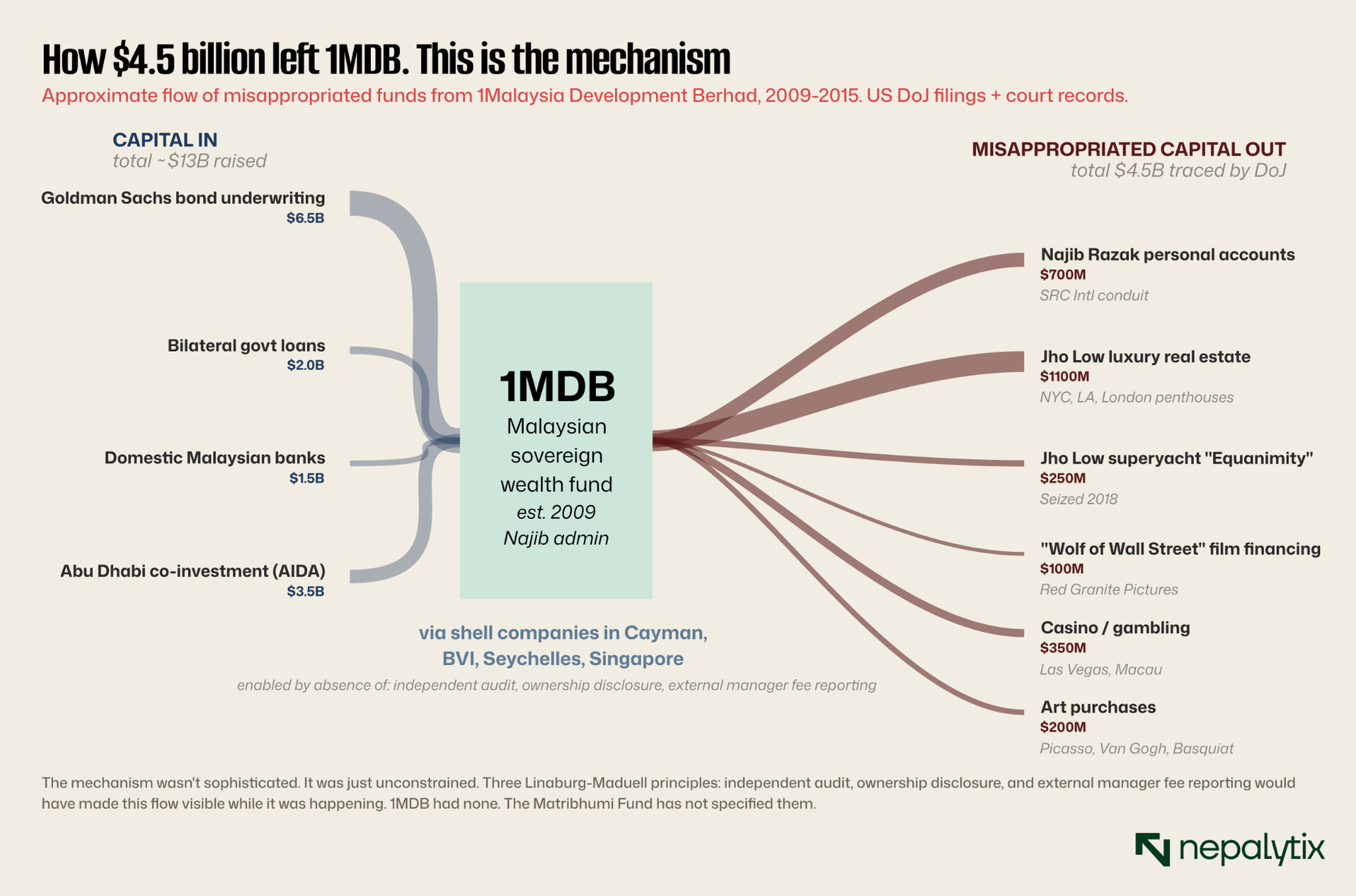

At the other end of the same spectrum sit cases that should be required reading for every minister considering creating a sovereign wealth fund. Malaysia's 1MDB, established in 2009 with strategic-development rhetoric and AI-equivalent technological ambitions for the time, was used between 2009 and 2015 to systematically embezzle more than $4.5 billion. The US Department of Justice in 2016 called it "the largest kleptocracy case to date." Prime Minister Najib Razak was sentenced to twelve years in prison. Libya's Investment Authority, established in 2006 with $67 billion in oil wealth, scored 2 out of 10 on transparency and lost an estimated 98 percent of its value through a combination of poor investments, fraud, and political appropriation. The same vehicle type, very different outcomes.

What separates Norway from 1MDB is not the founding rhetoric. Both funds launched with strategic-development language. Both promised to mobilise national wealth for productive long-term investment. The difference is what came after the announcement, the institutional architecture that surrounded the fund. Norway built that architecture deliberately over years. 1MDB never built it, and the consequence was foreseeable.

Ten questions the budget did not answer

The Linaburg-Maduell Transparency Index developed at the Sovereign Wealth Fund Institute in 2008 scores SWFs against ten specific principles. Each principle is binary; either the fund does it or it does not. Norway scores 10 out of 10. The Matribhumi Fund, as announced on Friday, addresses zero of the ten.

This is not, in itself, fatal. The budget speech is not the place where governance principles are laid out, that is what the implementing legislation is for. But the absence of any signal about which of these ten the fund will adopt is itself a signal. A government serious about Norway-style discipline would have used the budget speech to commit, even at a level of principle, to independent audit, to disclosure standards, to ethical guidelines, to parliamentary oversight. The budget speech committed to none of these.

The opportunity cost everyone is understating

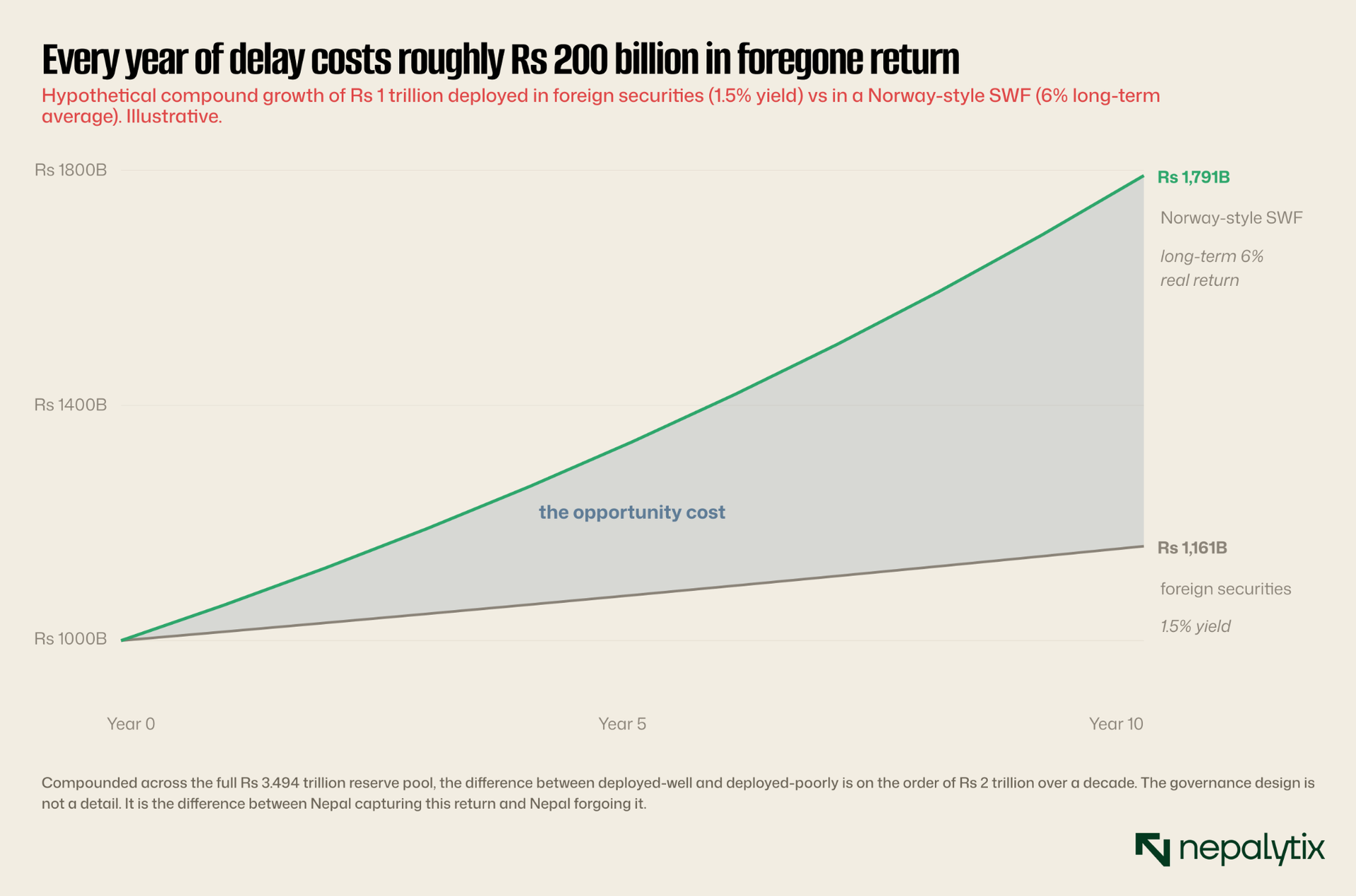

The conventional reading of the Matribhumi Fund is that it is a long-term structural project. Set it up properly, take the time to design the governance, and the fund can compound returns for generations. That reading is correct. It also obscures how expensive every year of suboptimal deployment actually is.

Nepal's FX reserves currently earn roughly 1-2 percent in yield from foreign sovereign securities. A Norway-style SWF, deployed across a balanced portfolio of equities, fixed income, and alternatives, has delivered approximately 6 percent long-term real returns. The compounding difference between the two over a decade is approximately 80 percent of the deployed capital. Applied to even one trillion of Nepal's reserves, that gap is on the order of Rs 800 billion over ten year.

The political timeline matters here. A reformist government and the budget signals an unusually reformist agenda has roughly two to four years to lock in the institutional architecture before the political incentives that produced it dissipate. Locking in governance now, while the legitimacy and political room exist, is materially easier than locking it in later under any future configuration. Every month spent on draft legislation that does not include real audit, real board independence, real transparency, is a month in which the default option informal political control of the fund gets closer to becoming the institutional reality.

The 1MDB parallel that Nepal policymakers should study

Of all the cautionary cases in the SWF literature, Malaysia's 1MDB is the most directly relevant to Nepal. The fund was established in 2009 with a stated mission of strategic national development. Its founding rhetoric about transforming the country into a high-income nation, mobilising state resources for productive investment, projecting Malaysia onto the global financial stage is indistinguishable from the rhetoric currently surrounding the Matribhumi Fund. Goldman Sachs raised $6.5 billion for 1MDB in the early years, with the Abu Dhabi Investment Authority as a co-investor. International institutional credibility was attached to the project. The fund looked, from the outside, like Malaysia's answer to Singapore's Temasek.

What 1MDB lacked, structurally, was every one of the safeguards that Norway had. The board was not independent , it was chaired by the prime minister himself Najib Razak. The investment mandate was vague enough to permit, in practice, almost any deployment. The audits were delayed, modified, and ultimately withdrawn. The transparency standards were nonexistent and the public did not learn the scale of the looting until journalist Clare Rewcastle Brown's Sarawak Report leak in 2015. Parliament was not allowed to access the records. By the time the scandal broke, $4.5 billion had been moved through a network of shell companies and offshore accounts, with $700 million flowing directly into Najib Razak's personal bank accounts.

The lesson is not that all SWFs in developing countries fail. Botswana's Pula Fund, established in 1994, has run cleanly for over thirty years on a fraction of Norway's resources. Timor-Leste's Petroleum Fund has been managed transparently since 2005. The lesson is that governance is a choice that is made early, in the implementing legislation. Nothing about Malaysia's national character made 1MDB inevitable. Nothing about Norway made GPFG inevitable. The institutional architecture was the variable.

What to watch between now and mid-January 2027

The implementing legislation for the Matribhumi Fund will be drafted, tabled, and debated over the coming months. The actual structural choices will become public as that legislation moves. Five specific questions will, between them, answer where on the disaster-to-model spectrum the fund actually lands.

The first is the board. Is it independent of executive control, with majority non-political members and protections against political removal? Or is it a politically-controlled board where the executive can appoint and dismiss at discretion? The second is the mandate. Is the investment policy written, published, and binding before the fund operates? Or is it left to the board's discretion to define as it goes? The third is the audit. Is there a mandatory annual external audit by a recognised firm, with the audit report tabled in parliament? Or are audits internal and confidential? The fourth is transparency. Are holdings, returns, fees, and management compensation publicly disclosed at a defined frequency? Or are these treated as commercially sensitive? The fifth is oversight. Does parliament have real binding review authority over the mandate and the leadership? Or is its role advisory only?

The legislation will answer each of these. When it does, score it against this five-question framework. The answers will tell you, with reasonable confidence, where Nepal's Matribhumi Fund is going to end up.

What the market is missing

The coverage of the budget over the weekend has treated the Matribhumi Fund as a positive structural announcement, a long-overdue commitment to deploy Nepal's reserves productively, comparable in spirit to Norway and Singapore. That framing is not wrong, but it is incomplete. The fund as announced is a possibility, not yet a reality, and the realities that emerge from announcements of this kind span an enormous range. The public conversation is fixed on whether the fund will exist. The harder question, on what kind of fund, is not yet being asked.

The variance is the signal. Between Norway's $2.2 trillion of compounding national wealth and 1MDB's $4.5 billion of theft is a range of outcomes that the next eight months of implementing legislation will determine. The eight months matter more than the next eight years, because architecture established in foundational legislation is extraordinarily difficult to retrofit. Get it right now and the fund compounds national wealth for generations. Get it wrong now and the corrective cost will be measured in decades and trillions of rupees.

What readers and observers should be doing this week is not celebrating the announcement. It is watching the legislative drafting. Anything the implementing committee produces, anything that surfaces from the Ministry of Finance regarding governance design, anything that hints at board composition or audit framework or parliamentary review authority, is more consequential than the announcement itself. The signal nobody is pricing in is that the most important question about the Matribhumi Fund is one whose answer is being written right now, by people whose names most readers do not know, in a process that has not yet attracted public attention. By the time the public attention arrives, the architecture will mostly be settled.

This is the budget signal that matters. Not the Rs 2.124 trillion headline. Not the tax exemption. Not the IT incentives. The single decision that will determine whether Nepal's post-2025 reformist moment produces a Norwegian-style generational asset or a Malaysian-style cautionary tale. The window is open. The window will not stay open.