Nepali banking's third decade

Nepal's commercial banking sector has already shrunk from 32 banks to 20 over the past decade, but consolidation may not be over yet.

Nepal's commercial banks have halved in number in a dozen years, from thirty-two to twenty and the regulator is not done. This is a map of the consolidation still to come: who is buying, who is being bought, what forces the pairings and what it means for the people whose money sits inside.

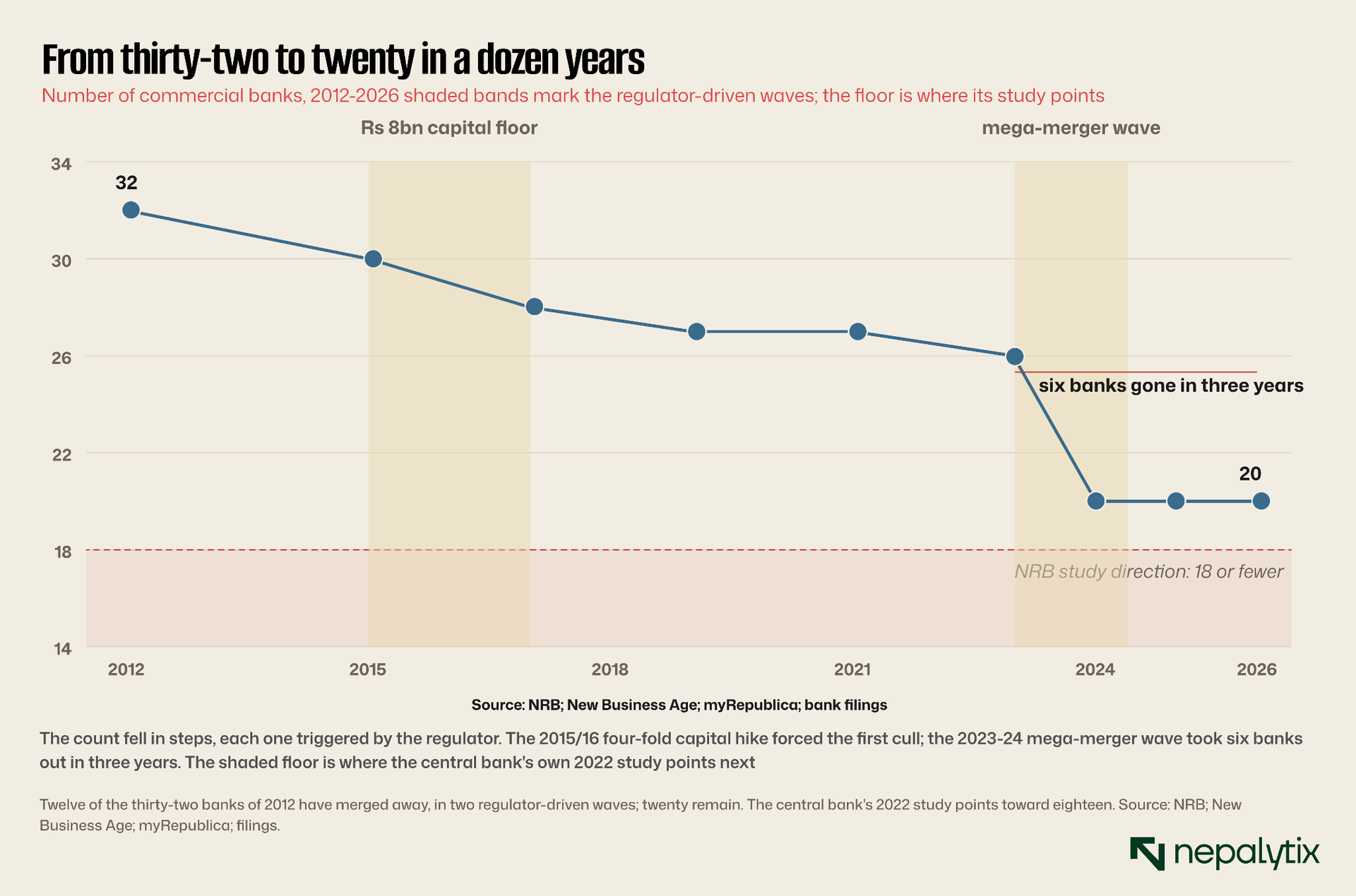

Begin with a number that has been falling for a decade. In 2012, Nepal had thirty-two commercial banks. Today it is twenty. The arithmetic of that decline is the story of modern Nepali banking and it is not finished: the central bank's own 2022 study on the optimal number of banks pointed lower still, toward eighteen or fewer and nothing in the sector's condition since has argued against it.

The cull came in waves, each triggered by the regulator rather than the market. The first followed the 2011 merger by law which for the first time gave banks and finance companies a legal path to combine. The second and decisive wave was set off by the 2015/16 monetary policy which raised the minimum paid-up capital of a commercial bank fourfold, to eight billion rupees and gave the industry barely two years to find it. A bank could raise that capital by issuing shares by retaining years of profit or by merging with another bank's balance sheet and for many, merger was the only route that arithmetic allowed. The third wave, the mega-merger spree of 2023 and 2024 was the one that reshaped the league table: eight banks combined in a single month of that season and the pairings were no longer weak-with-strong rescues but marriages of equals among the largest names in the country.

What remains is a sector that looks, on its headline aggregates, robust. The twenty surviving commercial banks together hold around 6.6 trillion rupees in deposits and have lent roughly 5.0 trillion, a credit-to-deposit ratio near 77 percent that leaves modest room to grow. The sector's capital-adequacy ratio at 12.78 percent sits comfortably above the eleven-percent regulatory minimum. By the measures a central banker reaches for first, this is a stable, well-capitalised system and a far cry from the fragmented field of more than two hundred deposit-taking institutions that existed a decade and a half ago.

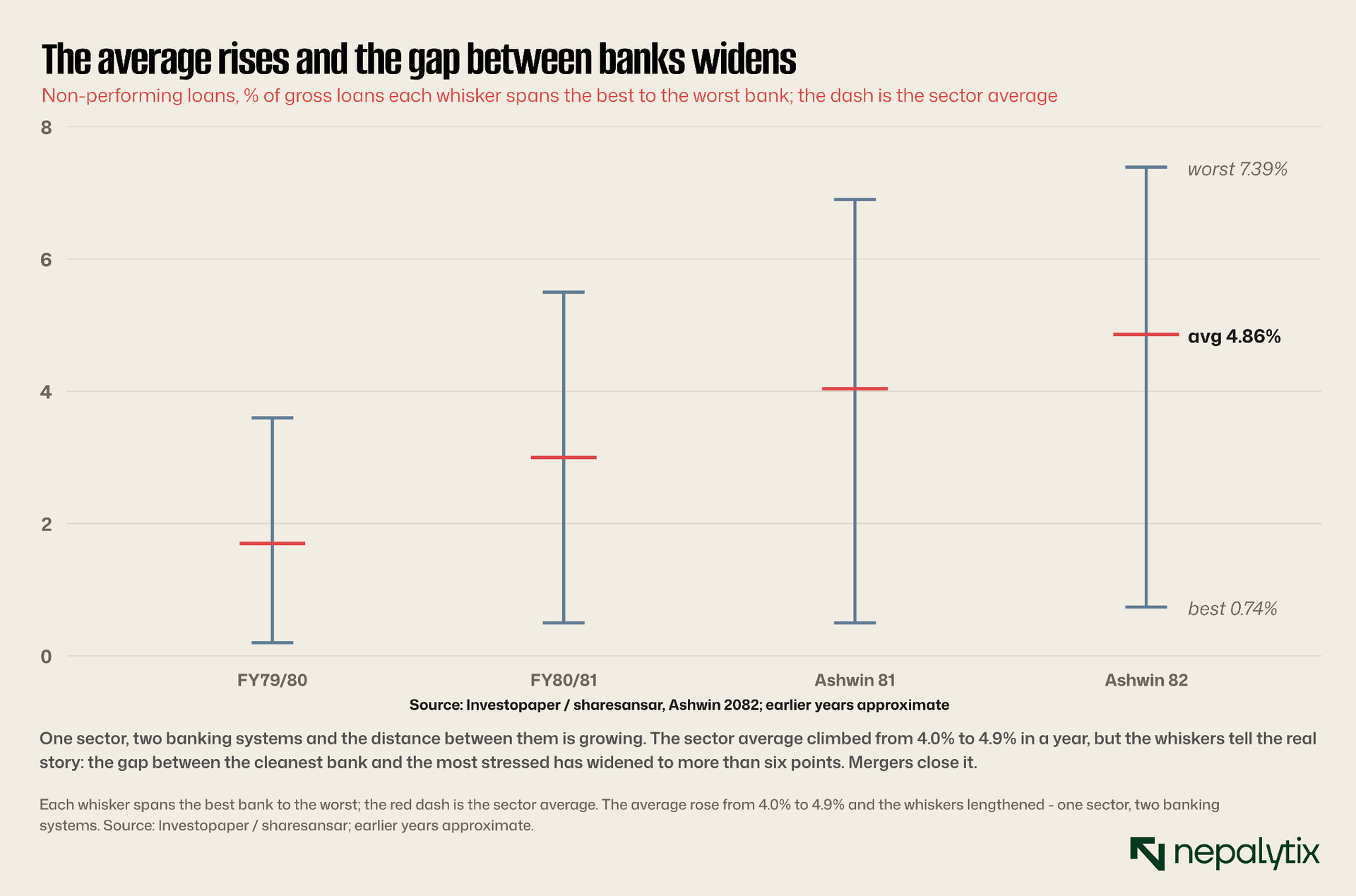

But aggregates conceal and two numbers underneath them are moving in the wrong direction. The first is asset quality. Non-performing loans across the sector have risen from 4.0 percent of gross lending a year ago to 4.9 percent today not yet a crisis but a clear drift and one concentrated in a handful of banks rather than spread evenly. The cleanest bank in the country carries bad loans below one percent; the most stressed carries above seven. That dispersion more than the average is what makes the next consolidation wave not merely likely but in the regulator's eyes, desirable.

The second number is capital and it connects this Long Read to the rest of the week's reporting. As Nepalytix has documented, the same banks that look adequately capitalised on the headline ratio have been issuing perpetual preference shares Additional Tier 1 capital at a remarkable clip, three of them at an identical 8.25 percent coupon within a single quarter. Banks do not reach for expensive permanent capital when ordinary equity is cheap and plentiful. They reach for it when the buffer is thin and the alternatives are worse. The AT1 cluster is the capital squeeze made visible, and the capital squeeze is the engine of consolidation.

The scale of the broader cleanup is easy to forget. Counting development banks, finance companies and microfinance institutions alongside the commercial banks, Nepal had well over two hundred deposit-taking institutions at the start of the last decade; today the figure is closer to one hundred and seven of which the twenty commercial banks form the well-capitalised core. The very first merger under the 2011 bylaw of a development bank and a finance company joining in Birgunj looks quaint beside the billion-rupee commercial-bank combinations that followed but it set the template. And one feature of the Nepali experience cuts against the usual fear that consolidation strands customers: because merged banks have kept the branches of both predecessors, the total commercial-bank branch network has grown even as the number of banks has shrunk. Fewer banks, in Nepal's case, has not meant fewer doors.

The sector looks stable on its averages and stressed in its distribution. Consolidation is how that distribution is usually resolved.

The capital squeeze, quantified

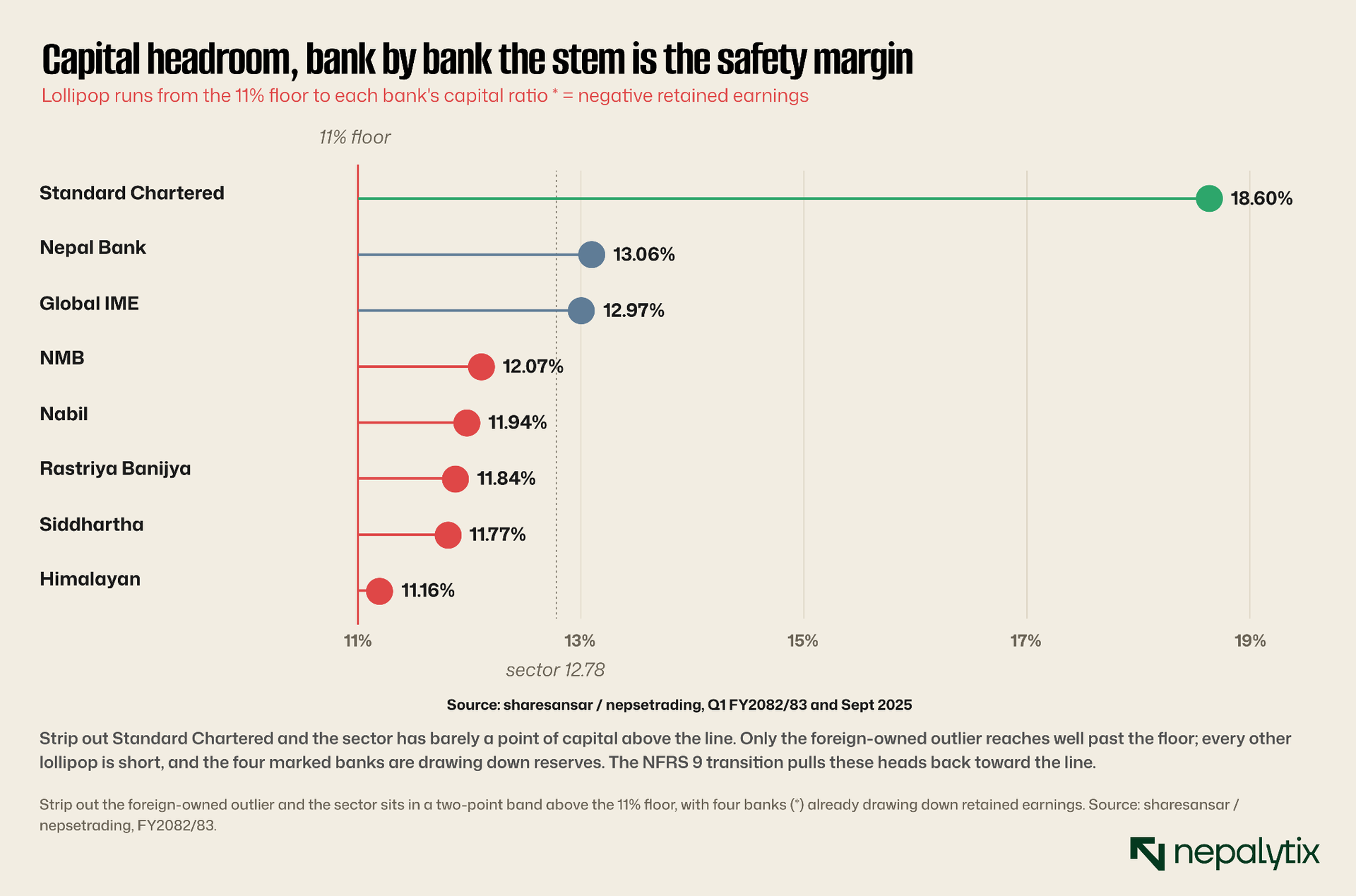

To see why mergers are coming, look at where each bank sits relative to the floor it cannot fall through. The regulatory minimum capital-adequacy ratio for a commercial bank is eleven percent. Cluster the twenty banks by their reported ratios and a striking picture emerges: with a single exception, the entire sector is bunched into a band barely two points wide above that minimum.

The exception is Standard Chartered whose ratio above eighteen percent reflects a foreign parent, a conservative loan book and a deliberate choice to stay small rather than chase market share. Every other bank including the largest and most profitable names in the country runs between roughly 11.2 and 13.1 percent. That is not a comfortable margin. It is a working margin, the kind a bank holds when it is lending as aggressively as its capital permits and no more and it leaves little absorbed buffer for a shock to asset quality of the sort the rising non-performing-loan trend threatens to deliver.

Two forces are pressing on that thin band at once. The first is the drift in bad loans already described: every rupee that migrates from performing to non-performing must be provisioned against and provisions come straight out of capital. The second is the accounting transition to NFRS 9, the forward-looking expected-credit-loss standard that Nepal's banks are midway through adopting. Under the transition they face what the industry calls double provisioning; they must satisfy both the new expected-loss model and the central bank's older, percentage-based loan-loss reserve at the same time. The two charges stack, and the stack falls hardest on exactly the upper-tier commercial banks that have lent most freely.

The clearest tell that the squeeze is real is not the capital ratio at all but the retained-earnings line. Four banks Himalayan, Kumari, Prabhu and NMB are reported to be carrying negative retained earnings, the accounting signature of a bank that has paid out or written off more than it has lately earned. A bank in that position cannot rebuild capital from profit quickly, cannot easily issue equity at a depressed share price without destroying book value, and is therefore left with two doors: issue costly AT1 paper or find a partner with capital to spare. Both doors lead toward consolidation.

This is the mechanism that turns a regulatory preference into a market inevitability. The central bank does not, in the main, order banks to merge. It sets the capital floor, tightens the provisioning rules, and lets arithmetic do the rest. A bank that cannot organically generate the capital to stay above the line, in a system where the line keeps effectively rising, will eventually present itself for sale and the banks with capital to spare know it and wait.

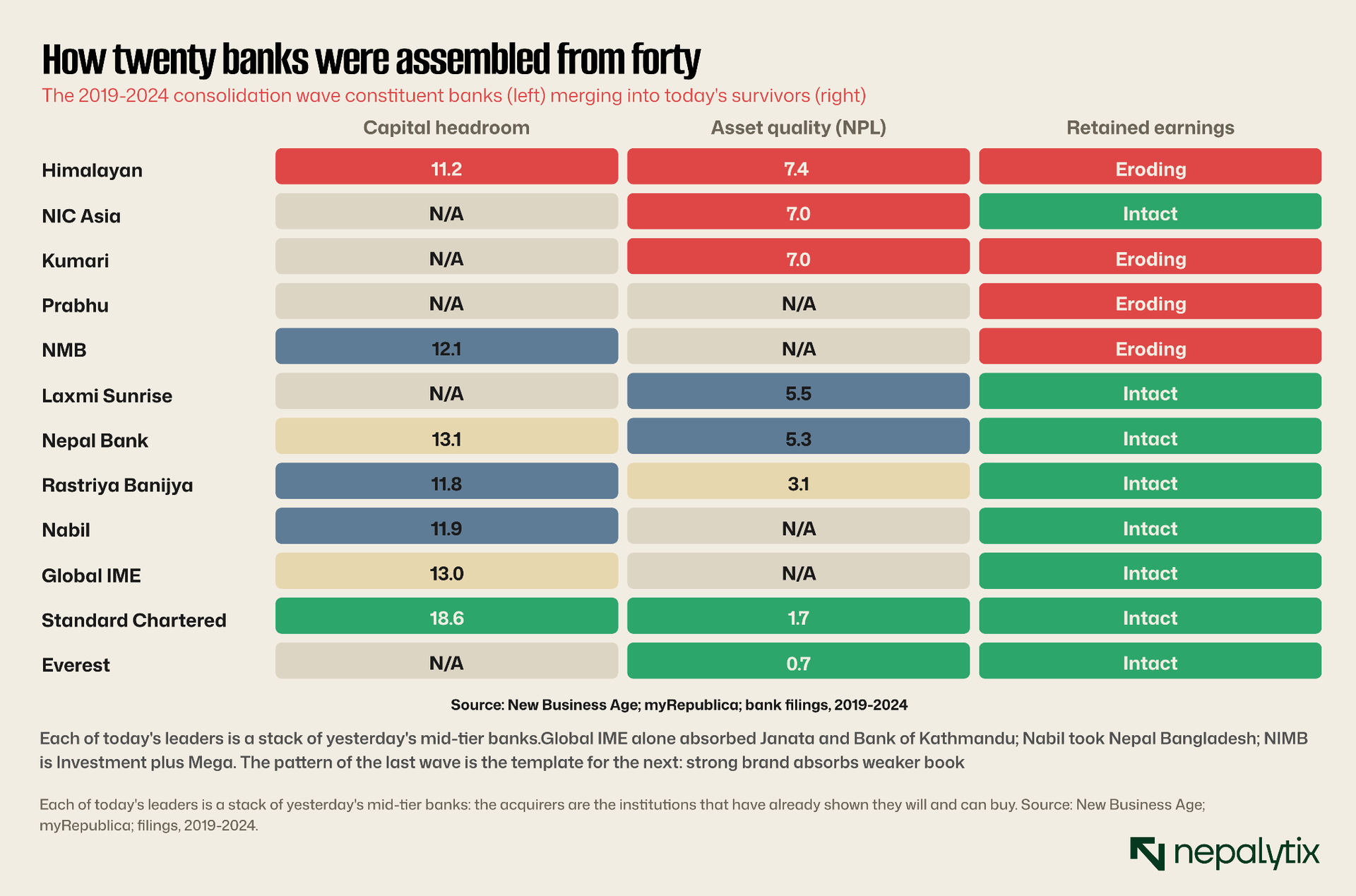

Put names to the band and the squeeze becomes concrete. Himalayan sits closest to the line at 11.16 percent, Siddhartha at 11.77, the state-owned Rastriya Banijya at 11.84, Nabil the most profitable bank in the country at 11.94, and NMB at 12.07. These are not troubled outliers; they are the mainstream of Nepali commercial banking, operating with one to two points of headroom above a floor that the provisioning cycle is steadily pushing up toward them. It is precisely this arithmetic that explains the rush into Additional Tier 1 paper documented elsewhere in this week's reporting: when a bank cannot lift its capital ratio out of retained profit and will not issue ordinary equity at a depressed price, an 8.25 percent perpetual preference share expensive, permanent, and counted as core capital becomes the path of least resistance. The coupon is the price of staying independent for another year.

The regulator rarely forces a merger. It sets the capital floor and lets arithmetic do the forcing.

The competitive map

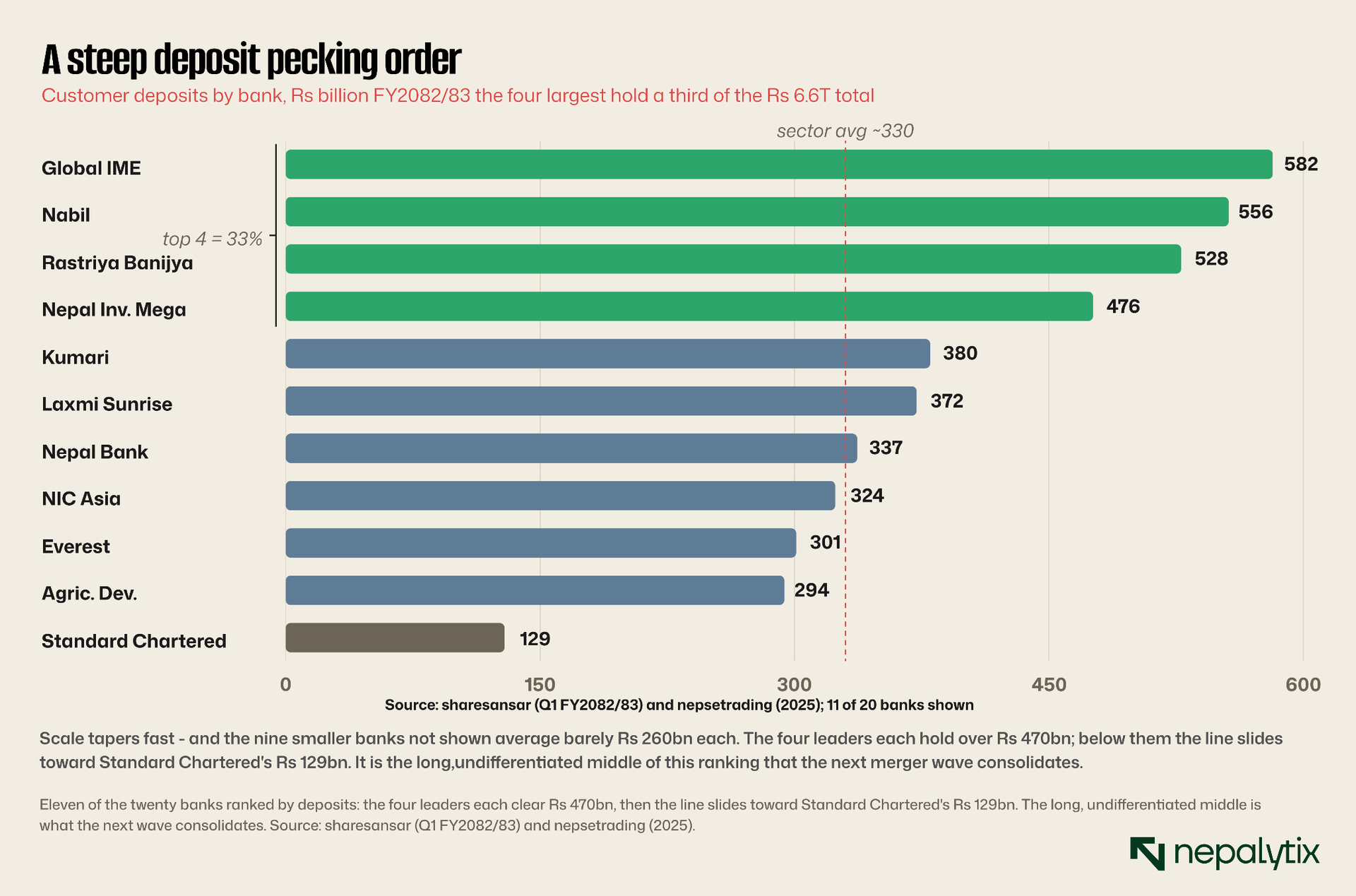

Before mapping who will buy whom, it helps to see how unevenly the field is already tilted. Rank the twenty banks by the deposits they hold and the concentration is immediate: three banks Global IME, Nabil and the state-owned Rastriya Banijya each command more than half a trillion rupees while the smallest listed commercial bank holds barely a fifth of that. The top of the table is not merely ahead; it operates at a different order of magnitude.

That concentration is itself the product of the last merger wave. Global IME reached the top of the deposit table by absorbing Janata in 2019 and Bank of Kathmandu in 2024; Nabil climbed by taking in Nepal Bangladesh Bank; Nepal Investment Mega Bank is, as its ungainly name records, the fusion of Nepal Investment and Mega. The institutions that sit at the top of the league did not grow there organically. They bought their way there, and the habit of buying does not easily fade.

Beneath the leaders the field sorts into recognisable tiers. There is a state-owned bloc Rastriya Banijya, Nepal Bank, the Agricultural Development Bank large by deposits, systemically important but structurally less nimble and less profitable than the private leaders, and unlikely to be either acquirer or acquired while majority government ownership holds. There is a small foreign-linked tier Standard Chartered, Nepal SBI, Everest with its Punjab National Bank parentage conservative, high-quality and largely insulated from the domestic merger pressure by patient foreign capital. And then there is the broad middle: a dozen private commercial banks of broadly similar size, similar products, similar branch footprints and similar margins, competing for the same urban deposits and the same creditworthy borrowers.

It is that middle tier that the next wave will consolidate. The strategic problem for a mid-table Nepali commercial bank is that it is differentiated from its rivals by almost nothing. It offers the same savings rates, the same digital app of roughly the same quality, the same corporate lending desk chasing the same conglomerates. In a market where scale lowers the cost of funds, of compliance and of technology, undifferentiated mid-scale is the worst place to stand. The banks caught there face a choice between a slow competitive decline and a merger that at least buys scale and in a thinning field, the number of available partners falls every year which is its own pressure to move sooner rather than later.

The lending table tells the same story of concentration from the asset side. Global IME tops it with a loan book above four trillion rupees out of the sector's five, with Nabil again second; the same handful of names that dominate deposits dominate credit, because in a relationship-banking market the two move together. The foreign-linked tier is the instructive counterpoint. Everest with Punjab National Bank of India among its founders runs the cleanest loan book in the country; Nepal SBI carries the discipline of its State Bank of India parentage; Standard Chartered pairs the highest capital ratio with the lowest cost of funds. These banks compete on quality rather than scale, and their patient foreign capital exempts them from the merger pressure that grips the domestic middle which is why paradoxically, the safest banks in Nepal are among the least likely to take part in the consolidation at all.

Undifferentiated mid-scale is the worst place to stand in a market where scale lowers every cost.

The predators

A consolidation wave has two cast lists and the shorter one is the acquirers. In Nepal the buyers are not hard to identify, because they have been buying for a decade and have left a paper trail of absorbed balance sheets behind them. The lineage of today's leaders is almost literally, a record of who hunts.

Global IME is the archetype. Built through a sequence of mergers and acquisitions that absorbed Janata, Bank of Kathmandu and others, it now sits atop the deposit, loan and paid-up-capital tables with a capital fund among the largest in the country. Its leadership has made consolidation a stated strategy rather than an opportunistic reflex and an institution that has integrated several banks already carries something rarer than capital: the operational muscle to merge core banking systems, rationalise branches and retain customers through the disruption. That integration capability is itself a competitive moat, and it makes Global IME the most likely buyer in almost any pairing it chooses to pursue.

Nabil and Nepal Investment Mega Bank are the other two natural acquirers, for related reasons. Both are large, both are profitable Nabil has at times led the sector in absolute net profit and both have recent merger experience fresh enough that the integration teams still exist. A profitable bank with a strong deposit franchise and a proven ability to absorb another institution is, in a consolidating market, a predator whether or not it thinks of itself in those terms.

What do the buyers want? Not, in the main, more of what they already have. The serial acquirer is hunting for specific assets that are cheaper to buy than to build: a deposit franchise in a region where the buyer is thin, a low-cost current-and-savings base that lowers the blended cost of funds, a branch network in districts the acquirer has not reached or simply the regulatory permission and the customer list that a banking licence represents. A clean enough loan book is a bonus, not a requirement. A well-capitalised buyer can digest a target's bad loans if the franchise underneath is worth having, and the central bank's merger incentives are designed precisely to make that digestion easier.

There is also a quieter category of buyer worth watching: the ambitious mid-tier bank that intends to acquire its way out of the dangerous middle. Laxmi Sunrise itself the product of a 2024 merger has signalled exactly this ambition to reach the top tier by combining again. In a thinning field, the banks that are neither clearly safe at the top nor clearly vulnerable at the bottom face a strategic fork and some will choose to be the consolidator rather than wait to be consolidated.

The numbers behind Global IME's position explain why it sets the pace. Its paid-up capital above thirty-eight billion rupees is the largest in the country; its total capital fund exceeds sixty billion; and its deposit base, near six hundred billion, gives it among the cheapest blended costs of funds of any large private bank. But capital is the smaller part of what makes it formidable. Having already merged Janata, Bank of Kathmandu and others onto a single core banking platform, it has done the genuinely hard work of consolidating migrating accounts, reconciling two risk cultures, choosing which of two overlapping branches to keep and keeping the muscle memory to do it again. That integration capability is the real moat. A bank can raise capital in a quarter; it cannot buy, in a quarter, the institutional experience of absorbing another bank without losing its customers and that experience is exactly what the next round of targets will need their acquirer to possess.

In a consolidating market a profitable bank with integration experience is a predator whether or not it thinks of itself as one.

The vulnerable

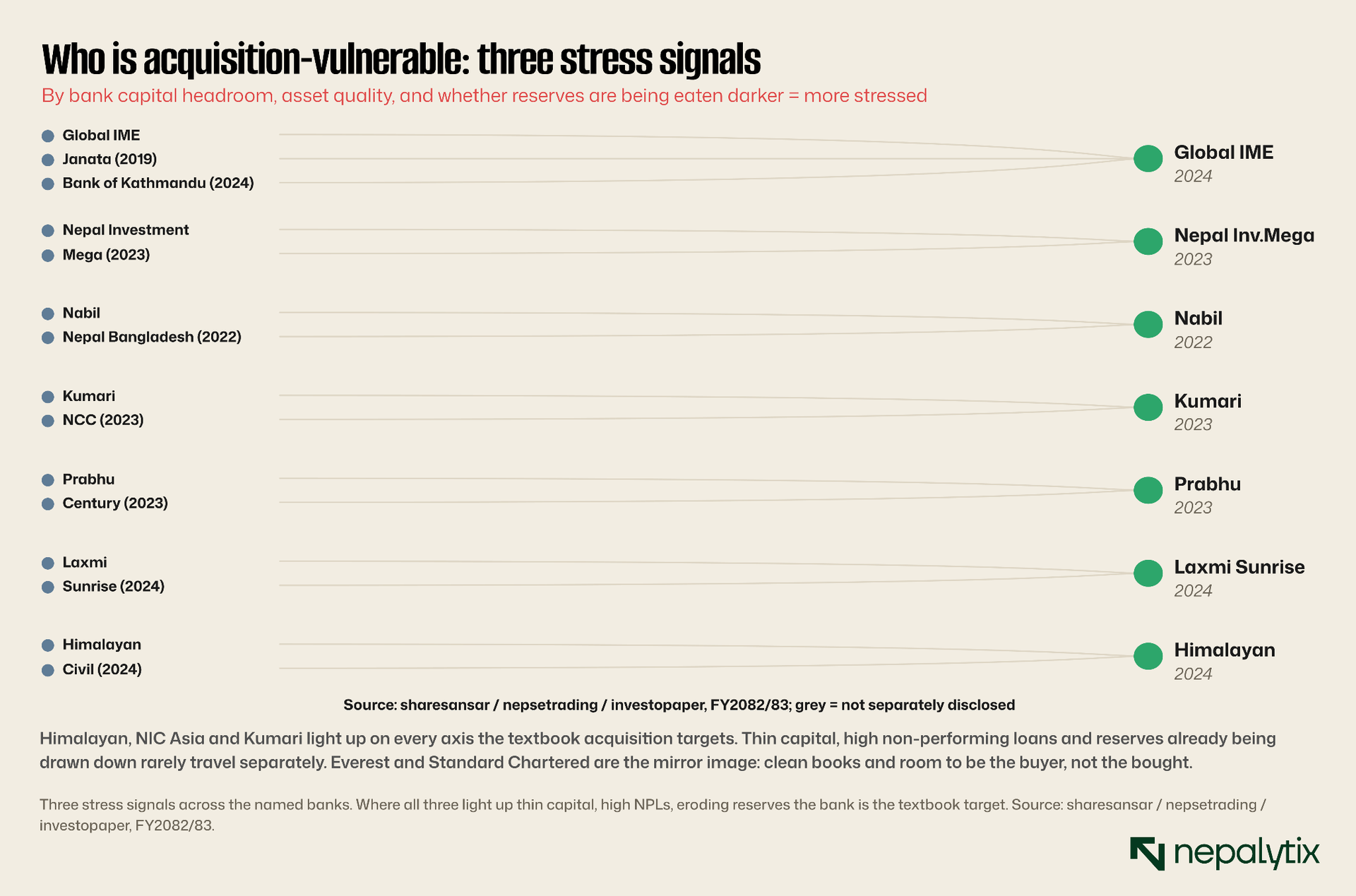

The longer cast list is the targets, and they can be identified with more precision than polite banking discourse usually allows because vulnerability in a bank has a consistent signature. It is rarely a single bad number. It is the coincidence of three: thin capital with little headroom above the floor, a high and rising stock of non-performing loans and a retained-earnings line that has turned negative. A bank with one of these can recover on its own. A bank with all three is, in the language of the market, in play.

Read across the rows and the most exposed names announce themselves. Himalayan Bank carries the highest non-performing-loan ratio in the sector, above seven percent, the thinnest capital ratio among the major private banks, and negative retained earnings all three signals at once. It is, on the numbers, the single most acquisition-ready large bank in the country, and its recent absorption of Civil Bank did not resolve the underlying strain. NIC Asia, once among the most aggressive lenders in the market, now sits with the second-highest non-performing-loan ratio, the legacy of that aggression coming due. Kumari combines high bad loans with eroding reserves; Prabhu and NMB each show the capital-and-reserves signature that marks a bank short of room to manoeuvre.

It is worth being precise about what vulnerability means here, because it is not the same as failure. None of these banks is in danger of collapse; Nepal's deposit base is loyal, its banks are liquid and the central bank has shown neither appetite nor need for a disorderly resolution. Vulnerability means something narrower and more commercial: that the bank's board, facing a capital wall it cannot climb organically and a share price too low to issue equity against will eventually conclude that merging into a stronger partner is the least-bad option for shareholders and that the stronger partners know this and can afford to wait for the terms to improve.

The mirror image of the vulnerable bank is instructive too. Everest carries the lowest non-performing-loan ratio in the country, below one percent, and the patient backing of an Indian parent; Standard Chartered pairs the highest capital ratio with a clean book. These are the banks with the room to be the buyer rather than the bought and tellingly, the least pressure to do either. Health in this market buys the luxury of choice. Stress removes it.

Between the clear predators and the clear targets sits the largest group of all: the mid-tier banks whose numbers are not alarming but not comfortable either clustered just above the capital floor with bad loans near the sector average. These are the banks whose fate the next twenty-four months will decide. Some will be pulled upward by an acquirer; some will combine defensively with a peer; a few will issue enough AT1 paper to buy another year of independence. But the direction is one-way. The field will be smaller a year from now than it is today.

The figures put the vulnerability beyond impression. Himalayan's non-performing-loan ratio stands at 7.39 percent, the highest in the sector; NIC Asia's at 6.99; Kumari's at 6.98. Laxmi Sunrise, itself a recent merger, carries 5.49 percent and the state-owned Nepal Bank 5.34 both elevated, both reminders that a merger does not by itself cleanse a loan book. Set against these the cleanest names: Everest at 0.74 percent, the only bank below one and Standard Chartered at 1.71. The distance between a bank carrying roughly three rupees of bad loans in every forty and one carrying barely seven in a thousand is the distance between being the buyer and being the bought and in a consolidating market that distance only widens because the stressed banks must keep lending to grow out of their problem even as the strong ones can afford to be selective.

Vulnerability is not failure. It is the moment a board concludes that selling is the least-bad option for its shareholders and the buyers know it.

What the regulator's levers point toward

None of this happens without the central bank which has spent fifteen years building the machinery of consolidation and shows every sign of intending to use it again. Understanding the next wave means understanding the levers Nepal Rastra Bank holds because in this market the regulator is less a referee than a choreographer.

The most powerful lever is the one that began the whole process: the minimum paid-up capital requirement. Raising it is the bluntest and most effective tool the central bank has because it converts a policy preference into an arithmetic compulsion. The fourfold hike to eight billion rupees in 2015/16 did more to shrink the sector than any direct merger order ever could, and another increase long rumoured, never confirmed, would have the same effect, forcing under-capitalised banks to either raise capital they cannot raise or find a partner who can. Every board in the country watches the monetary policy statement each July for exactly this signal.

The second lever is the provisioning and accounting regime. The pace at which the central bank pushes NFRS 9 to full adoption, and the way it resolves the double-provisioning overlap, directly determines how much capital the weaker banks must find and how fast. A hard deadline accelerates the squeeze; a generous transition relieves it. The regulator has, in effect, a throttle on the speed of consolidation, calibrated through accounting rules that look technical but are anything but.

The third lever is incentive rather than pressure. For years the central bank has dangled regulatory carrots in front of banks willing to merge relaxation of the cash-reserve and credit-to-deposit requirements, easier treatment of overlapping exposures, breathing room on capital during integration. These incentives lower the cost of a merger for the acquirer and make digesting a weaker target's bad loans more palatable. They are the velvet glove around the capital-requirement fist.

Behind all three sits the central bank's own stated view of where the sector should end up. Its 2022 study on the optimal number of banks canvassed opinion that ranged from as few as five well-capitalised institutions to a more moderate fifteen-to-twenty and the institution's revealed preference, expressed through a decade of policy, has been steadily downward. A regulator that believes the country has too many banks, and that holds the capital lever, will get fewer banks. The only open questions are the pace and the pairings.

The incentives have a documented history worth recalling. The central bank introduced an acquisition bylaw in 2013, folded it into a broader merger-and-acquisition bylaw in 2016, and has since attached to every merger a package of relaxations easier cash-reserve and credit-to-deposit treatment, room on overlapping exposures, transitional capital forbearance designed to ease the acquirer through the disruptive integration period. These are not trivial: liquidity relief alone can be worth more to a merging bank in its first year than the eventual cost savings of the deal. As for the destination, the 2022 study did not settle on a single number so much as reveal a spectrum of opinion, some favouring as few as five to ten commercial banks, others fifteen to twenty, others a more conservative twenty to twenty-five. The midpoint of that range still sits below today's twenty, which tells its own story about which way the institution leans.

There is a counter-pressure worth naming, because it complicates the timing. The very ease of the current macro environment, abundant liquidity, low policy rates, reserves at a record removes some of the urgency that a tighter cycle would impose. A bank that can fund itself cheaply and roll its problem loans for another year feels less pressure to sell at a weak valuation. Easy money, paradoxically can slow consolidation by relieving the very squeeze that drives it. That is why the regulator's deliberate levers on the capital floor, the NFRS 9 deadline matter so much: they supply the pressure that a benign cycle withholds.

What the precedents teach

Nepal is not the first frontier or emerging market to drive its banking sector through a regulator-led consolidation, and the precedents are worth studying both for what they promise and for what they warn against. Two episodes are especially instructive because in each the central bank or government did deliberately what Nepal Rastra Bank is doing gradually.

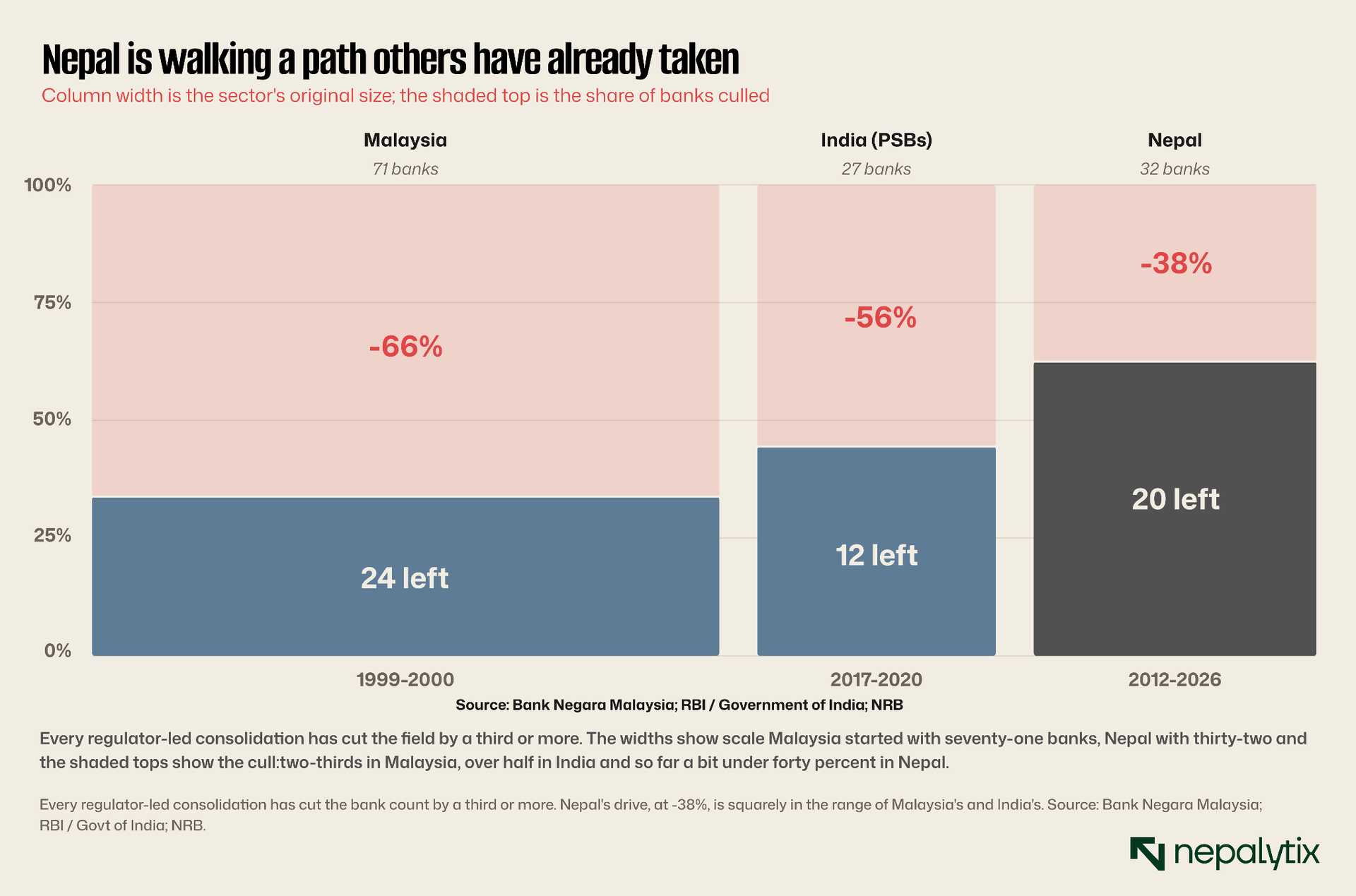

Malaysia is a dramatic case. In the wake of the 1997-98 Asian financial crisis, with a fragmented sector of seventy-one institutions competing destructively for a small market, Bank Negara Malaysia forced the entire industry into ten later six anchor groups, collapsing seventy-one banks into twenty-four in barely a year. It was consolidated by fiat, swift and total, and it produced a sector of larger, better-capitalised banks. It also produced a generation of resentment about the heavy hand of the state and the winners and losers it picked. Nepal's model is gentler and slower but the end state Bank Negara engineered is recognisably the one Nepal Rastra Bank has in mind.

India is the more apt comparison, because it consolidated not through crisis but through deliberate policy and because its banks faced the same affliction of bad loans that troubles Nepal's today. Between 2017 and 2020 the Indian government merged twenty-seven public-sector banks into twelve, folding ten weaker state lenders into four larger anchors in a single 2020 step. The stated goals were Nepal's goals exactly: stronger capital, better risk management, banks large enough to fund national growth.

And here the Indian precedent delivers its warning. The most careful assessments of that consolidation found that while it created larger banks with stronger capital buffers on paper, the underlying non-performing-loan problem did not vanish; it was merged and not resolved. A weak loan book absorbed into a larger balance sheet is a smaller percentage of a bigger number, but it is the same bad debt and the borrowers behind it are no more able to pay. Consolidation can recapitalise a sector and rationalise its costs; it cannot, by itself, make bad loans good. For Nepal, where rising non-performing loans are part of what drives the merger logic, this is the essential caution: a wave of mergers will produce fewer, larger, better-capitalised banks, and it will not, on its own, fix the asset quality that helped make them merge.

The Indian episode is worth unpacking a step further because its sequencing rhymes with Nepal's. It opened in 2017 with the State Bank of India absorbing its five associate banks to create a lender of global scale, then proceeded in 2019-2020 to the mega-merger of ten weaker public-sector banks into four anchors Punjab National Bank taking in Oriental Bank and United Bank, Canara absorbing Syndicate and so on. The trigger was an asset-quality crisis: public-sector non-performing assets had climbed toward eleven percent, a level that made consolidation feel less like strategy than triage. And the story has a sequel that should interest Nepal by late 2025 the Indian government was reported to be weighing a 'Merger 2.0' to shrink twelve public-sector banks toward four, even while publicly denying any active proposal. A consolidation drive, once begun, develops a momentum of its own that is hard to declare finished.

Consolidation can recapitalise a sector and cut its costs. It cannot, by itself, make a bad loan good.

Three ways the next two years could run

Forecasting specific pairings is a fool's errand merger talks collapse over board egos as often as over balance sheets but the range of plausible outcomes can be bounded and the variable that moves the sector between them is not the banks but the regulator. Here are three scenarios for the twenty-four months ahead, distinguished less by which banks combine than by how hard the central bank presses.

In the base case, the count falls from twenty to about seventeen. The central bank nudges rather than shoves: no dramatic capital-floor hike, a measured NFRS 9 timetable, and two or three voluntary pairings among mid-tier banks that read the direction of travel and choose to combine on their own terms while they still can. The most stressed names a Himalayan, perhaps a Kumari find partners or buyers; one or two ambitious mid-tier banks combine to climb. This is the path of least resistance, and the most likely single outcome.

In the accelerated case, the count falls to fourteen or fewer. The trigger is a deliberate regulatory push: a meaningful increase in the minimum paid-up capital, or a hard NFRS 9 deadline that crystallises the capital shortfall at the weaker banks all at once. In that environment the vulnerable banks cannot wait for favourable terms; they must merge from weakness, quickly, and the predators acquire on buyers' terms. This is the scenario the central bank can engineer at will, and the one its 2022 study suggests it would not mind seeing. It compresses years of gradual attrition into a single forced season.

In the stalled case, the count barely moves, to nineteen. Here the benign macro cycle does the regulator a disservice: abundant liquidity and cheap funding let even the weaker banks roll their problems for another year, share prices stay too low for anyone to want to merge at the implied valuations, and boards resist the dilution and loss of control that any combination entails. Consolidation does not reverse it never has but it pauses, waiting for the next tightening or the next regulatory shove to resume.

It is worth resisting the temptation to name the pairings too confidently, but the logic does narrow the field. The clearest targets Himalayan, NIC Asia, Kumari will each need a partner with the capital to absorb their bad loans, which points toward the three established acquirers. A defensive combination among mid-tier peers, two roughly equal banks merging to reach escape velocity is the other recurring pattern and Laxmi Sunrise has already signalled the appetite for it. What is least likely is the status quo: a bank sitting in the stressed middle, declining to act, hoping the cycle rescues it. That is the one strategy the arithmetic does not reward.

The striking thing about the three paths is what they share. In none of them does the number of banks rise or even hold for long. The disagreement is entirely about speed. That is the surest sign that the consolidation is structural rather than cyclical: when every plausible scenario points the same direction and differs only in pace, the destination is no longer in question.

What it means for shareholders

For the investor, a merger is not an abstraction but a transaction with a price and the price falls differently on different holders. The first distinction that matters is between the shareholders of the acquirer and those of the acquired, and the hinge between them is the swap ratio the number of the buyer's shares each seller's share converts into set by the relative valuations the two boards and their advisers negotiate.

For the shareholders of a strong acquirer, a well-judged merger is usually accretive over time: the combined bank lowers its cost of funds, strips out duplicated branches and back-office systems, and spreads fixed compliance and technology costs across a larger base. But the gains are gradual and the costs are immediate. Integration is expensive and disruptive, customer attrition is real in the first year, and if the acquirer overpays for a target or underestimates the bad loans it is absorbing the deal can dilute book value for years before it accretes. The Indian precedent is again the warning: bigger did not automatically mean better for the anchor banks' shareholders, because the bad loans came with the franchise.

For the shareholders of a weak target, the calculus is starker and more immediate. A bank merging from strength can command a swap ratio that rewards its holders; a bank merging from weakness thin capital, high bad loans, negative reserves merges on the buyer's terms and its shareholders typically accept a ratio that crystallises the discount the market has already applied. The cruel arithmetic of consolidation is that the moment a bank most needs to sell is the moment it can extract the least for its owners. There is, however, a counter-current worth noting: several mid-tier banks trade below their book value precisely because the market doubts their independent future. For a fundamentally sound bank in that position, a merger that removes the doubt can re-rate the shares upward; the discount was the franchise's stand-alone risk, and consolidation retires it.

The second distinction is newer to Nepal and sharper in its consequences: the gap between equity holders and the holders of Additional Tier 1 capital. The perpetual preference shares that Nepali banks have rushed to issue sit above common equity in the capital structure but their protection is conditional. In a merger of healthy banks the distinction is academic. In a distressed combination it is anything but: AT1 instruments carry write-down or conversion triggers, and a non-cumulative instrument that skips its dividend does so permanently. An investor who bought an 8.25 percent perpetual on the assumption that it behaves like a bond may discover, in exactly the consolidation scenarios this Long Read describes, that it behaves like the riskiest slice of equity at the worst possible moment.

The practical lesson for the shareholder is to read the direction of travel into the position today. The predators large, profitable, capital-rich are where the durable value sits, because they will buy well and integrate competently. The clearly vulnerable are a speculative bet on takeover terms that, merging from weakness, are unlikely to be generous. And the AT1 paper that yields so temptingly should be held with a clear eye on the fact that its safety is a function of the issuer's health, in a sector whose weakest members are precisely the ones most likely to test it.

What it means for everyone else

A bank is not only a security; it is the place a family keeps its savings, the institution a business borrows from and the employer of tens of thousands. Consolidation reaches all three, and its effects on them are more mixed than the tidy logic of capital ratios suggests.

For depositors, the news is mostly good and a little constraining. A larger, better-capitalised bank is a safer home for savings and the merged institutions inherit the combined branch and ATM networks of both predecessors, so physical access typically improves rather than shrinks. Deposit insurance, capped at five hundred thousand rupees, covers the ordinary saver in any case. What the depositor loses is choice and, at the margin, pricing power: a sector of twenty banks competes a little less hard for deposits than a sector of thirty-two did, and a sector of fifteen will compete less still. The deposit rate a saver is offered is, in part, a function of how many banks are bidding for the money.

For borrowers, the trade-offs are sharper. Fewer banks mean fewer doors to knock on when a loan is refused and a borrower whose relationship manager and credit history sit with a bank that is absorbed must rebuild that relationship inside a larger, more standardised institution that may view the loan differently. Concentration also concentrates credit decisions: when three banks hold a third of the system's deposits, their risk appetite shapes who in the economy can borrow and on what terms. The offsetting benefit is that a better-capitalised bank can lend in larger tickets and fund the bigger infrastructure and hydropower projects that a thinly capitalised sector could not underwrite the central bank's stated rationale for wanting larger banks in the first place.

For employees, consolidation is where the human cost lands, and it is rarely discussed honestly. The single largest source of merger savings is the elimination of duplication: two head offices become one, overlapping branches close, redundant back-office and technology teams are cut. The branch network may grow in total, but the staff per rupee of assets falls, and in a country where a bank job is a coveted, stable, middle-class livelihood, that contraction is felt in households far from the trading screens. Past Nepali mergers have managed this through attrition and redeployment more than outright dismissal, and the cultural friction of combining two institutions' staff, different systems, different pay scales, and different ways of working is often the hardest part of any integration. The capital ratios improve on the spreadsheet long before the merged organisation actually works as one.

The deposit-insurance backdrop softens the depositor's risk through any of this. Nepal's Deposit and Credit Guarantee Fund covers balances up to five hundred thousand rupees per depositor per bank, which protects the overwhelming majority of ordinary savers regardless of which bank holds their money or which larger bank eventually absorbs it. The saver with more than that on deposit has reason to prefer the stronger, larger institution a merger creates and in practice, the quiet flight of large depositors toward safety is one of the pressures that pushes a weakening bank toward the negotiating table in the first place.

These distributional effects are the part of consolidation that the regulator's framing tends to underweight. A stronger, safer, larger-scale banking system is a genuine public good and Nepal's is demonstrably more resilient than the fragmented field of fifteen years ago. But resilience is bought, in part, with reduced competition, concentrated credit power and real disruption to the people inside the institutions. A consolidation done well delivers the first and manages the second. A consolidation done carelessly delivers fewer, larger banks that are no better at lending and a good deal less hungry for the customer's business.

The consolidation decade

Step back from the bank-by-bank detail and the shape of the thing is clear. Nepali commercial banking entered its first decade as a liberalised free-for-all, licences handed out freely until the field had swollen past what a small economy could support. It spent its second decade being pruned of the capital hikes, the merger bylaw, the first waves of combination that took the count from thirty-two toward twenty. It is now entering its third decade, and the evidence of this Long Read is that the third decade will be the consolidation decade in earnest: the one in which the field settles toward the fifteen or the dozen or the regulator's hinted-at eighteen, and the question of how many banks Nepal should have is finally answered in practice rather than in study papers.

The forces are aligned and mutually reinforcing. Asset quality is drifting and concentrated in the weakest hands. Capital is thin across almost the entire sector and being pressed from two sides at once by rising bad loans and the NFRS 9 transition. The rush into perpetual preference shares is the audible alarm of banks reaching for capital wherever they can find it. The regulator holds the decisive lever on the capital floor and has signalled for a decade that it intends to keep using it. The predators are identified, capitalised and experienced. The targets are identifiable on three coincident stress signals. And every plausible scenario for the next two years points the count downward, differing only in speed.

What remains genuinely uncertain is not the direction but the pace and the pairings and the answer to both lies in the central bank's hands more than the banks' own. A benign macro cycle has, for now, loosened the squeeze and bought the weaker banks time; a capital-floor hike or a hard accounting deadline would tighten it again and turn a gradual attrition into a forced season. The boards that read this correctly will choose their partners while they still can choose; the boards that wait will have partners chosen for them.

For the reader watching this unfold, three signals will mark the pace. The first is the July monetary policy statement: any move on the minimum paid-up capital requirement is the starting gun, and every board in the country will be reading that page first. The second is the NFRS 9 timetable, whose deadline tightens the screw on the thinnest balance sheets. The third is the preference-share pipeline. Every new perpetual issue is a bank buying another year of independence, and a slowdown in issuance would signal either that the squeeze has eased or more ominously, that the banks have run out of institutional buyers and must turn to a partner instead. Watch those three, and the shape of the wave will announce itself well before the merger headlines do.

And underneath it all sits the caution the Indian precedent supplies and that no Nepali enthusiasm for scale should be allowed to drown out. Consolidation will deliver fewer, larger, better-capitalised banks. It will lower costs, fund bigger projects and produce a sector that looks stronger on every headline ratio. It will not, on its own, make a single bad loan good nor teach a merged bank to lend more wisely than its constituents did. The bad debt that helped drive the wave will still be there the morning after, merged into a bigger balance sheet, waiting. A consolidation wave is a recapitalisation and a rationalisation. Whether it is also a genuine improvement in how Nepal's banks allocate the country's savings is the harder question and the one worth watching through the decade to come.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.