Nepal’s banks have never had more money. They have no idea what to do with it.

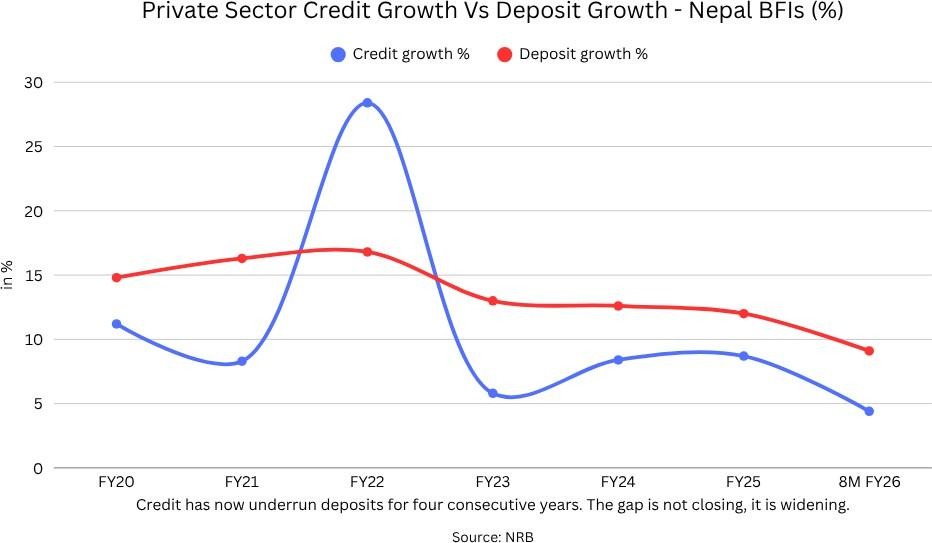

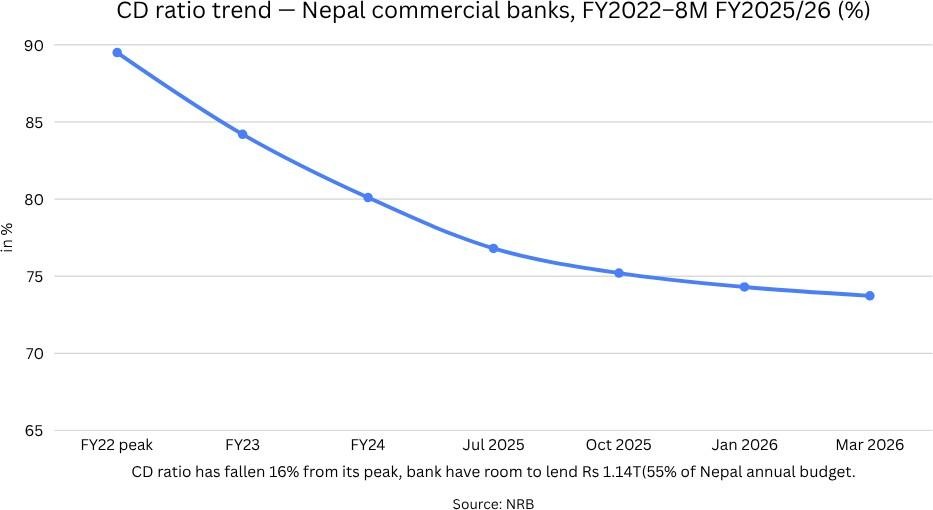

Credit grew 4.4% in the first eight months of FY 2025/26. Deposits grew three times faster. The CD ratio just hit 73.73%, the lowest in years. Banks could lend Rs 1.14 trillion more than they currently do. They aren

Nepal’s banks have never had more money. They have no idea what to do with it.

Credit grew 4.4% in the first eight months of FY 2025/26. Deposits grew three times faster. The CD ratio just hit 73.73%, the lowest in years. Banks could lend Rs 1.14 trillion more than they currently do. They aren’t.

On April 2, 2026, Nepal Rastra Bank(NRB) released its eight-month macroeconomic report for FY25/26. It landed quietly, as these reports usually do. No press conference, no prime-time coverage. But buried inside the numbers is a story that should be making more noise: Nepal’s banking system has now Rs 1.14 trillion in untapped lending capacity, inflation is at a multi-year low, interest rates have been cut four times, and credit is still growing at 4.4%. That is slower than last year.

Slower than the year before. The money is piling up. The economy is not absorbing it.

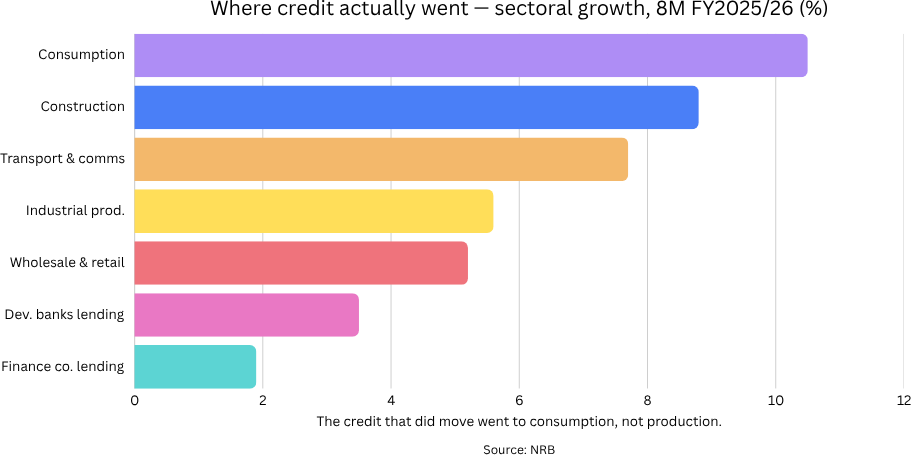

The deposit surge is being driven almost entirely by remittances. Nepal’s current account surplus hit Rs 552.85 billion in eight months, remittance inflows running hot, tourist arrivals up, and exports rising. The money is coming in. It is landing in bank accounts. And it is staying there, because the households receiving it, mostly in

remittance-dependent districts outside the Kathmandu valley, have no productive investment vehicle to put it into. Fixed deposits are earning 5-6%. Savings accounts are less. The alternative is nothing.

Why cutting rates isn’t working

The NRB has cut its policy rate to 4.5%, the bank rate to 6%, and the deposit collection rate to 2.75%. By textbook logic, cheaper money should stimulate borrowing. In Nepal’s case, the textbook isn’t working. Former banker Bhuvan Dahal put it plainly: “Lower interest rates do not necessarily guarantee increased investment. What matters more is a business environment that ensures better returns.” That is the real problem. Lending rates have fallen. But if you are a garment manufacturer in Birgunj or a cold storage operator in Dhangadi, the return on investment hasn’t improved because your power supply hasn’t improved, your road access hasn’t improved, and the regulatory environment hasn’t improved. Cheap credit into a structurally broken productive is still credit with nowhere to go.

“Lower interest rates do not necessarily guarantee increased investment. What matters more is a business environment that ensures better returns.”- Bhuvan Dahal, Former Banker, MyRepublica, March 2026

The number that makes this a structural problem rather than a cyclical one.

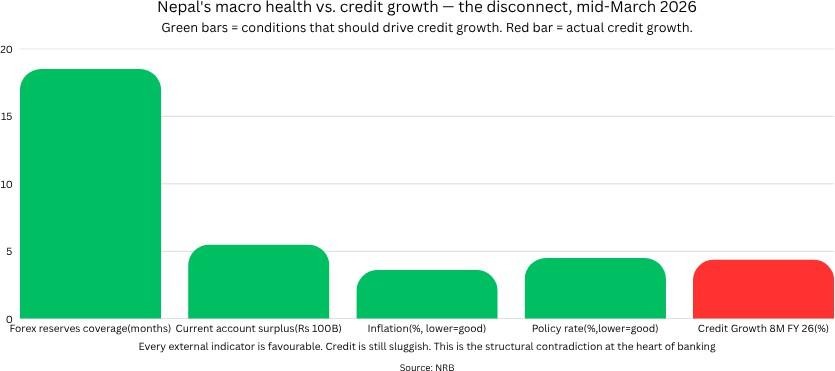

Here is the chart that closes the argument. Nepal’s foreign exchange reserves just hit Rs 3,413.77 billion, enough to cover 18.5 months of imports. Inflation is 3.62%, well within target. The current account is in surplus. By every external metric, Nepal’s economy is in its healthiest position in years, and yet domestic credit, the mechanism by which financial health translates into productive investment, is growing at 4.4%. If the conditions for credit growth were ever going to be right, they are right now. The fact that credit is still anaemic tells you that the problem is not monetary. It is structural. And no rate cut fixes that.

The NRB’s own report notes that with ample liquidity and low inflation, “the central bank can prioritise credit growth to agriculture, hydropower and SMEs without risking price stability.” That is the central bank telling you the conditions are perfect. The follow-up question, why isn’t it happening is the one Nepal’s financial press consistently fails to ask. Rs 1.14 trillion is sitting in Nepal’s banking system, looking for a productive home. Until the roads, power lines, and regulatory frameworks that make productive investment possible get built, it will keep sitting there. The banks will keep parking it at the NRB, The NRB will keep cutting rates. And the gap between Nepal’s financial health and it’s economic output wil keep widening.