Nepal’s Banks Post Record Profits, But Core Lending Remains Weak

Commercial banks in Nepal reported a 19.3% rise in profits in Q3 FY 2082/83, yet core income grew only 2.09%. The gap reveals that much of the growth came from provisioning relief rather than real business expansion.

Commercial banks reported record profits. Their core business is still weak.

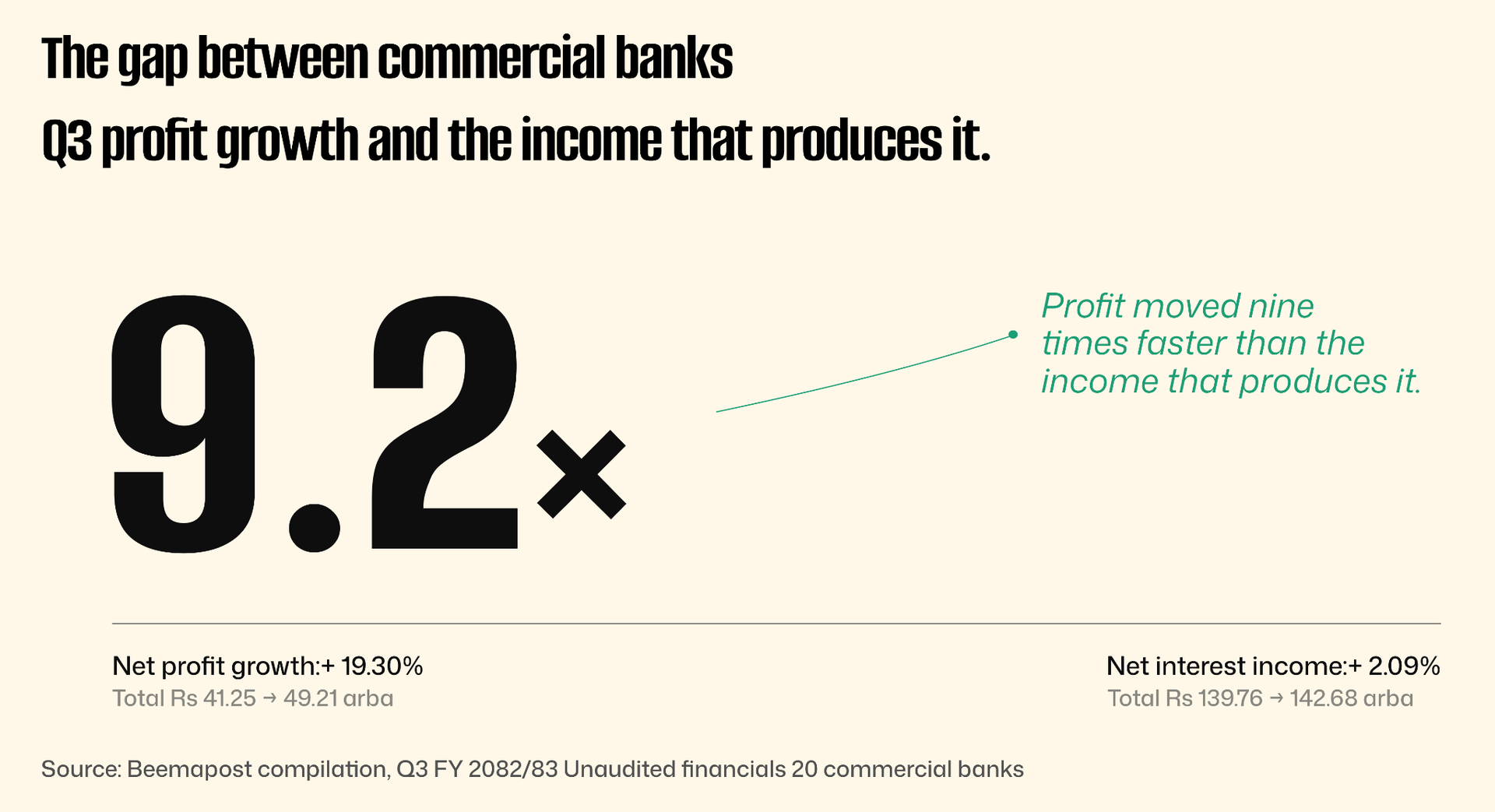

Net profit grew 19.30% across twenty banks. Net interest income grew 2.09%. The 9x multiplier between them is the regulatory accommodation in plain sight and the most underreported number of the Q3 cycle.

When Nabil released its Q3 numbers on April 28, the headline wrote itself. Operating profit up 26%. Net profit up 33.91%. Earnings per share climbed nearly Rs 8 in a single quarter, to Rs 33.02. The bellwether of Nepal's commercial banking sector, the bank everyone benchmarks against, had just delivered what looked like its strongest quarter since the pandemic recovery began.

The maths of that quarter if you sit with it, doesn't quite work.

Nabil's net interest income (NII), the cash a bank earns from the elementary act of lending money out and paying depositors less for it, grew exactly Rs 405 crore over the same nine months last year. A 3.36% bump. Real growth, but modest. Then came the line that did the actual work. Impairment charges: the money banks set aside against loans they expect to recover poorly fell from Rs 2.29 arba to Rs 47.87 crore, a 79% drop. Roughly Rs 1.81 arba in cash that the bank no longer had to flag as a buffer against bad loans. That money didn't disappear. It walked up the income statement and landed in operating profit.

That’s where the 26% operating profit growth came from. Not the income. The Nabil pattern wasn’t the exception. It was the pattern.

Profits grew 9x faster than core income.

Nepal's twenty commercial banks closed Q3 FY 2082/83 with collective net profit of Rs 49.21 arba, up 19.30% from Rs 41.25 arba a year ago. That's the number that got circulated. The number that didn't: collective NII across the same twenty banks grew 2.09% to Rs 142.68 arba. Profit moved nine times faster than the income that produces profit.

The 9x multiplier should be implausible. Banks earn money two ways. They lend it out and capture a spread (NII) and they earn fees from forex, treasury, and other activities. NII is the dominant revenue source for Nepali commercial banks, typically 65% to 75% of total income. If NII grows 2%, total revenue grows somewhere similar. After operating costs, taxes, and provisions, profit growth should track. Nineteen percent profit growth on two percent income growth means something well below the income line did the work.

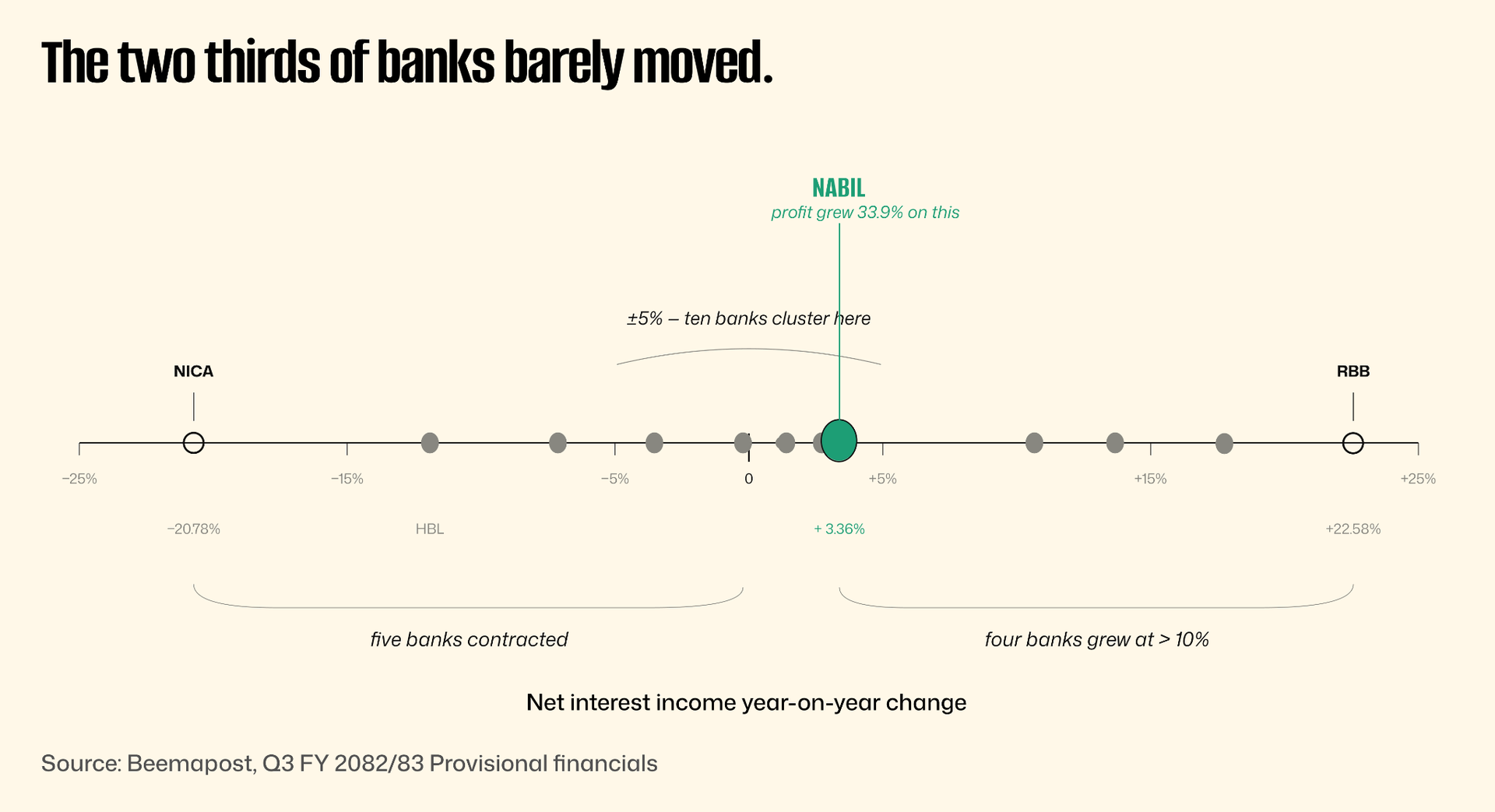

Not every bank is actually improving. A third of banks are still going backwards.

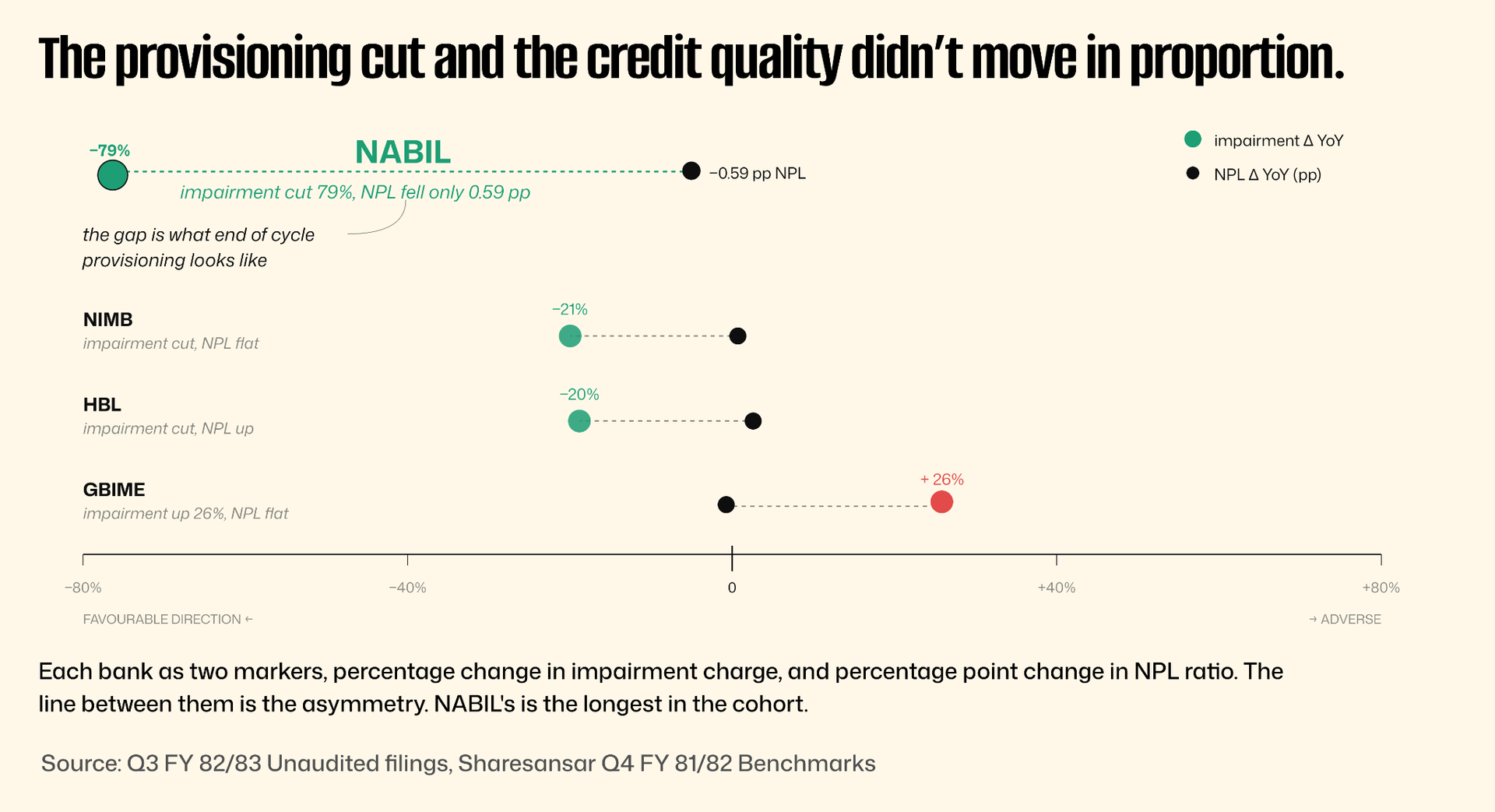

The 9x multiplier isn't an outlier dragging an average. It's the average of three populations. Some banks did grow their core lending business meaningfully. Rastriya Banijya Bank's NII jumped 22.58%, the strongest organic growth in the sector. Kumari Bank up 17.80%. NMB up 13.68%. Agricultural Development Bank up 10.69%. A meaningful cluster of banks ran flat, Nabil at +3.36%, Siddhartha at +3.04%, Nepal Bank at +2.99%, Prime at +2.70%, Prabhu at +1.36%, Everest at +1.33%. And then the cohort that lost ground. Laxmi Sunrise basically flat at −0.22%. Global IME −3.51%. Nepal Investment Mega −7.13%. Himalayan Bank −11.87%. And NIC Asia, the sharpest core decline of any commercial bank in the country, fell 20.78% year-on-year.

That dispersion is the actual state of Nepal's banking sector in Q3 FY 82/83. About a third growing, about a third flat, about a third in genuine NII decline.

If the headline is "banks reported strong Q3," the truth is that some banks reported strong Q3 numbers because their core business is genuinely healthy and a substantial group reported strong Q3 numbers despite their core business being in active decline. Both groups got there. Only one earned it.

To see how the second group got there, you need to understand what an impairment charge is and what NRB changed.

How the impairment walks straight into the income statement

When a Nepali commercial bank lends Rs 100 to a borrower, accounting rules require the bank to set aside a portion as a loan loss provision. The amount depends on the loan's classification. A performing loan needs a small provision, call it Rs 5. A loan overdue by a few months requires more Rs 25, sometimes more. A loan that's been formally restructured, where the borrower's payment terms have been adjusted because they couldn't keep up with the original schedule, historically required Rs 50 or more. The provision is the impairment charge. It hits the income statement immediately, before the loan has actually defaulted. The logic is conservative, book the expected loss now so that reported profit reflects realistic earning power, not optimistic accounting.

Banks book impairment in waves. When loan stress rises, provisions go up sharply, conservative buffers against expected losses. As those problem loans move through the cycle, either resolved through repayment, recovered through restructuring, or written off as expected, the required provisioning naturally falls. A bank that booked Rs 2.29 arba in provisions last year against a known set of stressed loans doesn't need to book that again this year if those loans have moved through the cycle. The provision releases. And it lands in operating profit.

Nabil's 79% impairment cut translates to roughly Rs 1.81 arba of released provisions in a single quarter. That's the size of an entire mid-tier bank's quarterly profit, just sitting on the income statement waiting to be claimed. The bank's NPL ratio fell from 4.96% to 4.37% over the same period, real asset quality improvement, but a fraction of the magnitude of the impairment cut. The provision release is large because last year's provisioning was large. Once the cycle ends, the lever stops working.

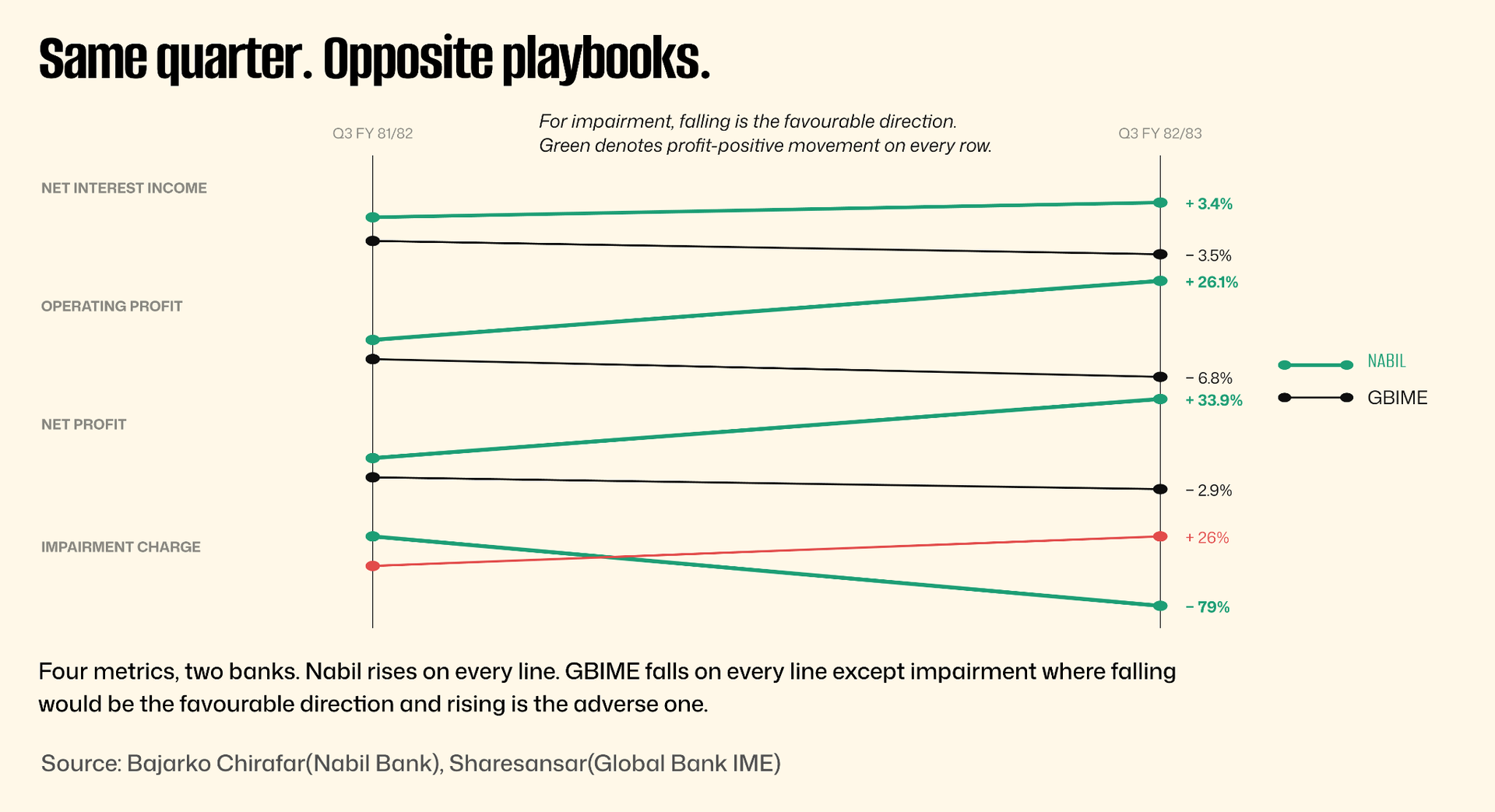

That's where banks running clean books and banks running deteriorating books diverge in Q3. Two banks tell the cleanest version of the story by doing opposite things.

Same quarter. Opposite mechanics. Opposite Outcomes.

Why would a bank not pull the lever, when the regulatory cover is sitting right there? Two reasons. The first is institutional culture. Some bank boards don't game quarterly numbers as a matter of policy, they treat provisioning as conservative protection rather than profit theater. They'll take a bad-looking quarter rather than borrow profit from a future write-down.

The second is more interesting. Some banks can't release provisions because their loan book is still actively deteriorating, new stressed loans appearing faster than old ones are resolved. The cycle that's ending for Nabil is just beginning for them. They have to keep adding to provisions, not releasing them. They take the impairment charge, and they take the hit to operating profit.

Global IME may fall in either camp. Q3 alone doesn't tell you which. Q4 might.

If the credit improved, the credit metric would say so. It doesn't.

The provisioning relief story has one story that exposes whether the impairment cut was earned or accommodated. It's the non-performing loan ratio. NPLs are loans where the borrower is 90 or more days behind on payments. They are the most direct, regulator-defined measure of how a bank's loan book is actually doing. If a bank reduces impairment charges because borrower behavior is genuinely improving, NPLs should fall in proportion. The two should track. A 79% impairment cut should correspond to a meaningful NPL improvement. Nabil's NPL ratio fell from 4.96% to 4.37%. A 0.59% point improvement. About a 12% relative improvement in non-performing loans.

That isn't 79%. The two numbers don't describe the same loan book.

Across the cohort, NPLs remain elevated and broadly comparable to a year ago. A banking system that just engineered 19% profit growth on credit improvement would show NPLs falling 1 to 2% points across the cohort. That is not what the numbers show. The credit didn't improve enough to justify the profit growth. The profit growth came from elsewhere.

More than half of the reported growth came from below the income line.

Add up the magnitudes and the maths closes neatly.

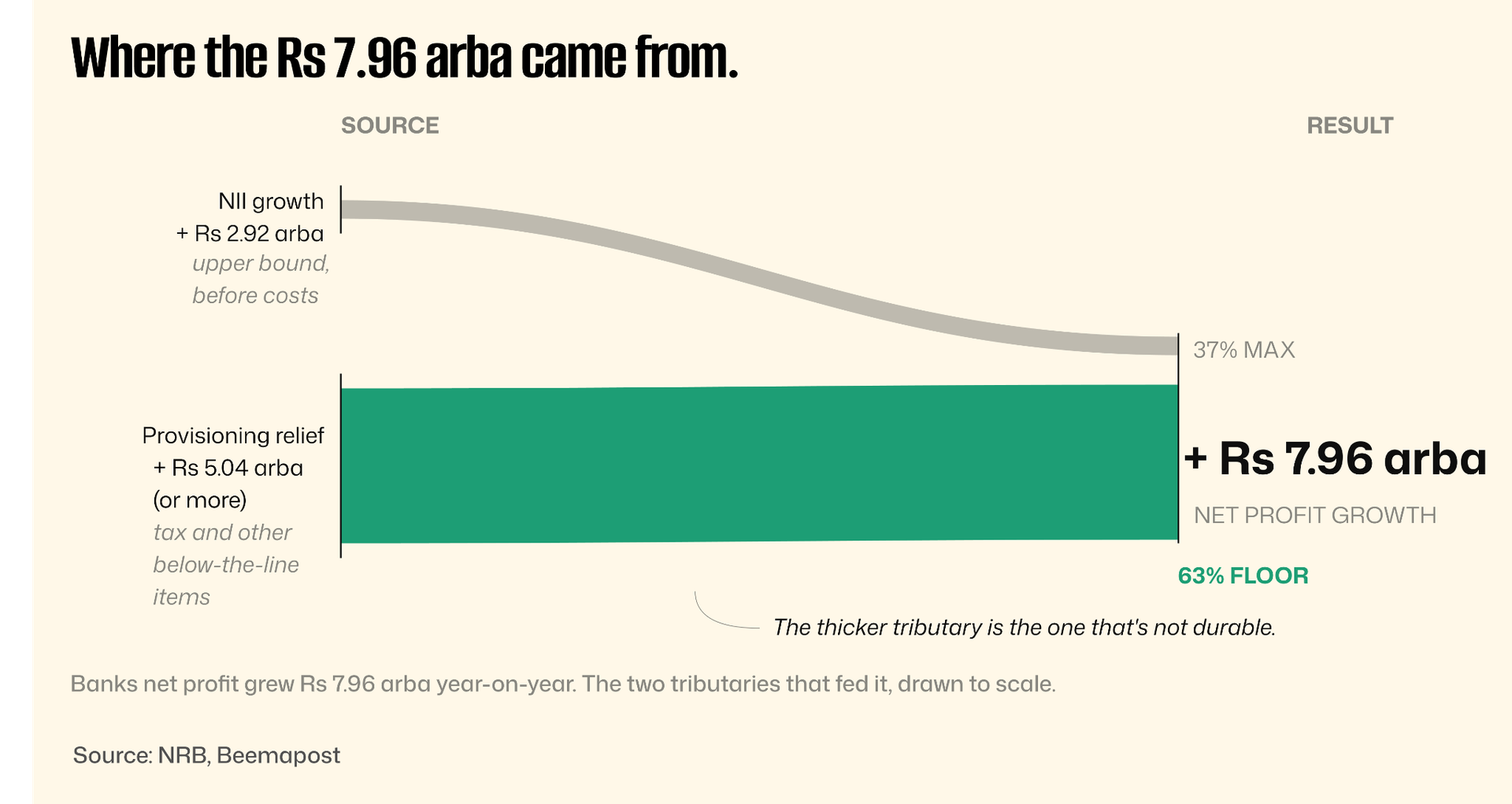

Aggregate cohort net profit grew Rs 7.96 arba from Rs 41.25 to Rs 49.21. Aggregate NII grew Rs 2.92 arba, that's the entire absolute increase in net interest income, before any operating costs are deducted. In any realistic accounting, NII contribution to profit growth is well below Rs 2.92, probably closer to Rs 1.5 to 2 arba once staff costs and operating expenses are factored in. Which means somewhere between Rs 5 and 6.5 arba of the reported Rs 7.96 arba in profit growth originated below the income line. The decomposition shows the upper bound on what NII could have contributed, and the floor of what came from somewhere else.

The majority of the cohort's reported profit growth this quarter came not from the banks earning more, but from the banks reaching the end of their provisioning cycles and releasing what they no longer needed.

Provisioning relief is real capital. It just isn’t durable.

It can be deployed. It can be distributed as a dividend. It is real money on the bank's balance sheet today. But it isn't an income stream. Next quarter, the same lever pulled releases nothing, there is no provision left to release on those particular loans. The income has to start doing the work, or the profit number changes shape.

Three signals that resolve the question by November.

The current fiscal year ends mid-July 2026. Q4 results land in late August or September. Three things will tell you which version of Q3 was true.

First: net interest income. If Q4 NII growth comes in at the 2% to 4%range like Q3, the core lending business is genuinely flat and the Q3 profit print was indeed an accounting tailwind. If NII picks up sharply to 8% to 10 % growth, that suggests credit demand has finally returned and the Q3 numbers were an early read of a real recovery.

Second: impairment normalization. If banks continue to release provisions in Q4, the regulatory accommodation continues and the math continues to work for them. If impairment reverts toward Q3 FY 81/82 levels, Nabil back at Rs 2-plus arba, Global IME at Rs 4 arba, the cohort impairment line returning to historical magnitudes, the Q3 relief was a one-quarter affair and the rerating begins.

Third, and the cleanest signal: the dividend declarations. Distributable profit is what a bank can actually return to shareholders, and dividend policy is the closest thing to a bank board's honest read of its own profit quality. If banks declare dividends that match their reported net profit growth, material increases over the prior year, in line with the 19% headline, they believe the profit is durable. If they hold back, declare flat or modestly higher dividends despite headline-strong profits, they're treating the Q3 number as accounting, not income.

The first dividend declarations begin in November and December as banks complete their AGM cycle. By the end of December 2026, the question of whether Q3 FY 82/83 was earned or accommodated will be settled not by analysts, but by the banks themselves.