Nepal's Best Microfinance Stock Isn't a Buy Right Now. Here's Why.

Nirdhan Utthan Laghubitta remains one of Nepal's strongest microfinance institutions, but despite its resilient business model and survivor status, the current valuation already prices in much of the expected recovery.

Nirdhan Utthan is where Nepali microfinance began. It started life in 1998 as the banking arm of an NGO called Nirdhan, took a central-bank licence in 1999 and built the template the rest of the industry copied: group lending on the Grameen model supplemented by its own Self-Reliant Group method, delivered through a branch network that today reaches 185 offices across all 77 districts. It is, in the sector's own language, "the bank for upliftment of the poor," and for two decades it was the blue-chip of the group, the name you owned if you owned one microfinance stock.

It still is the blue-chip. That is precisely the problem this note has to work through. Because the sector Nirdhan pioneered is now in the worst structural crisis of its history the average retail bad-loan ratio has jumped to 11.3 percent more than half the field sits above 10 percent and Nepal Rastra Bank has made clear it would rather merge the weak institutions than recapitalise them. Against that backdrop, Nirdhan is one of the handful of names that will unambiguously still be standing when the dust settles. The market knows it and it has priced it accordingly.

It is worth restating the stakes, because they frame why survival itself commands a premium here. Nepali microfinance reaches roughly 2.7 million borrowers, overwhelmingly low-income and rural through around fifty institutions, a number NRB is actively working to shrink. Of those, the regulator's own data shows 28 now carry a bad-loan ratio above 10 percent, a level at which capital is being eaten faster than a capped 15-percent margin can replace it. An institution that is demonstrably not in that danger zone profitable, deeply reserved, deposit-funded is a genuinely scarce asset and scarce assets do not trade cheaply. The premium is the market pricing the scarcity of safety. The question this note presses is whether it has overpriced it.

At Rs 691 a share, Nirdhan carries a market capitalisation of roughly Rs 19 billion on 27.4 million shares, split almost evenly between promoters (51 percent) and the public (49 percent) , a genuinely liquid float by microfinance standards worth about Rs 9.3 billion. It trades at 3.24 times its book value of Rs 213 and, more startlingly, at 79 times trailing earnings of Rs 8.73 a share. Those two numbers frame the entire debate. A price-to-book of 3.2 says the market is paying a clear premium for quality. A price-to-earnings of 79 says either the market has lost its mind or the earnings are at a cyclical trough and the multiple is an artefact. This note argues it is the latter and then asks the harder question of whether, even so, the price leaves anything on the table.

The short version of our conclusion stated up front in the research-note tradition: the quality is real and largely verifiable, the survival is not in doubt and the valuation already assumes the recovery it is waiting for. Nirdhan is a name to own at a price that is not today's.

The business: How a microfinance rupee is made

To judge the earnings you have to understand where they come from, and microfinance economics are deceptively simple. Nirdhan borrows money from its own depositors and from wholesale lenders at one rate and lends it to low-income group members at a higher one. The difference in net interest income is the engine; everything else is a modifier on that spread.

The lending itself runs on the group model Nirdhan helped pioneer. Borrowers organise into small groups that jointly guarantee each member's loan and the social pressure of the group substitutes for the collateral a commercial bank would demand. It is an elegant mechanism when it works because it turns a borrower's neighbours into the recovery department and a brutal one when it fails because when a whole community's income drops, the joint guarantee collapses all at once rather than one loan at a time. That is precisely what the last two years did and it is why microfinance bad loans did not drift upward but jumped: the group model transmits distress in bulk.

On the funding side, Nirdhan's deposit licence changes the arithmetic. Most MFIs fund themselves entirely by borrowing wholesale from commercial banks so their cost of funds tracks the banking system's rates and reprices constantly. Nirdhan raises a large share of its funding as member deposits, which are cheaper and far stickier. When the lending rate is capped at 15 percent, the yield side of the spread is fixed by regulation, so the only lever left is the funding cost and Nirdhan's deposit base gives it one of the lowest in the sector. The spread it defends is structurally wider than a pure borrow-and-lend peer's.

Around the core spread sit two ancillary lines that are easy to overlook: micro-insurance and remittance. Nirdhan distributes both to its member base earning fee income that does not depend on the interest cycle at all. These are small relative to net interest income, but they are exactly the kind of capital-light, fee-based revenue a maturing microfinance franchise leans on as pure lending growth slows and part of why the mature blue-chips are more resilient than the monoline lenders.

The takeaway for the valuation is this: Nirdhan's revenue engine, the spread plus fees is stable and structurally advantaged. What sits between that engine and reported profit is the impairment charge, and the impairment charge is the borrower. Read the company in that order and the whole case clarifies: you are underwriting a good engine, temporarily throttled by a bad credit cycle.

Management and the promoter lineage

Nirdhan's institutional DNA is unusual and in the current environment it is an asset. The company grew out of an NGO Nirdhan that had been delivering microfinance to poor communities before the formal entity was created in 1998 with the NGO becoming lead promoter when operations transferred to the licensed institution in 1999. That lineage matters because it means the franchise was built by practitioners with a development mandate not by financiers chasing the growth that got much of the sector into trouble. The promoter block still holds 51 percent of the shares so the founding interest remains aligned with the institution's long-term survival rather than a quick exit.

The management team has run the institution conservatively through multiple cycles, and the conservatism shows in the two things that now define the investment case: the sector-leading reserve buffer and the disciplined, deposit-heavy funding base. Neither is an accident; both are the product of years of retaining earnings and building capital rather than distributing everything and chasing book growth. In a sector where aggressive expansion is precisely what produced the over-indebtedness crisis, Nirdhan's caution has become its competitive advantage.

The governance caveat is the standard Nepali microfinance one. A 51 percent promoter block means minority holders are along for the ride on major decisions, and the steady bonus-share issuance that has diluted per-share earnings is a board choice that favours capital-building over per-share returns. Neither is a red flag but both are structural features an investor should price rather than ignore.

The engine is impairment's mirror image

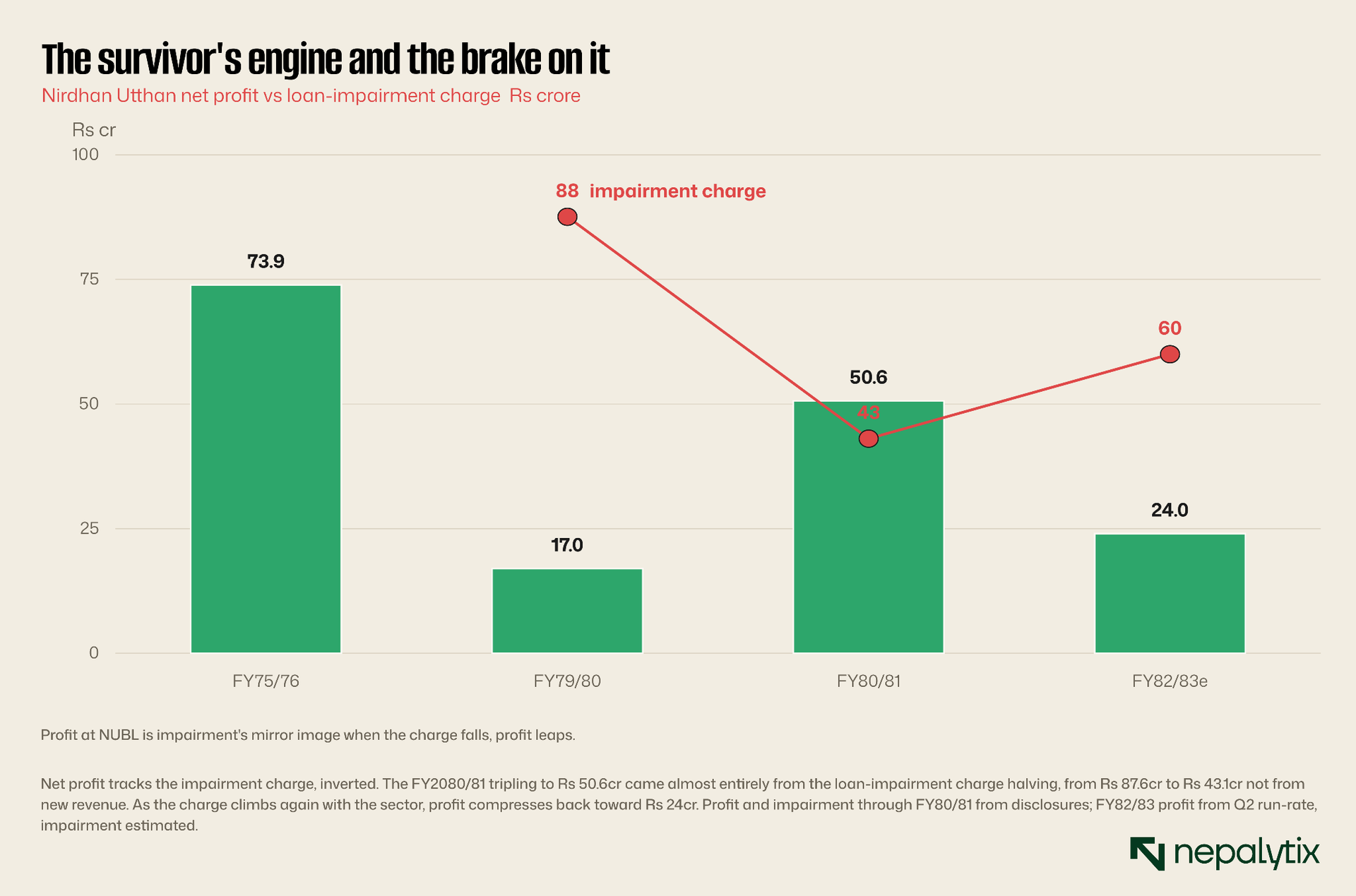

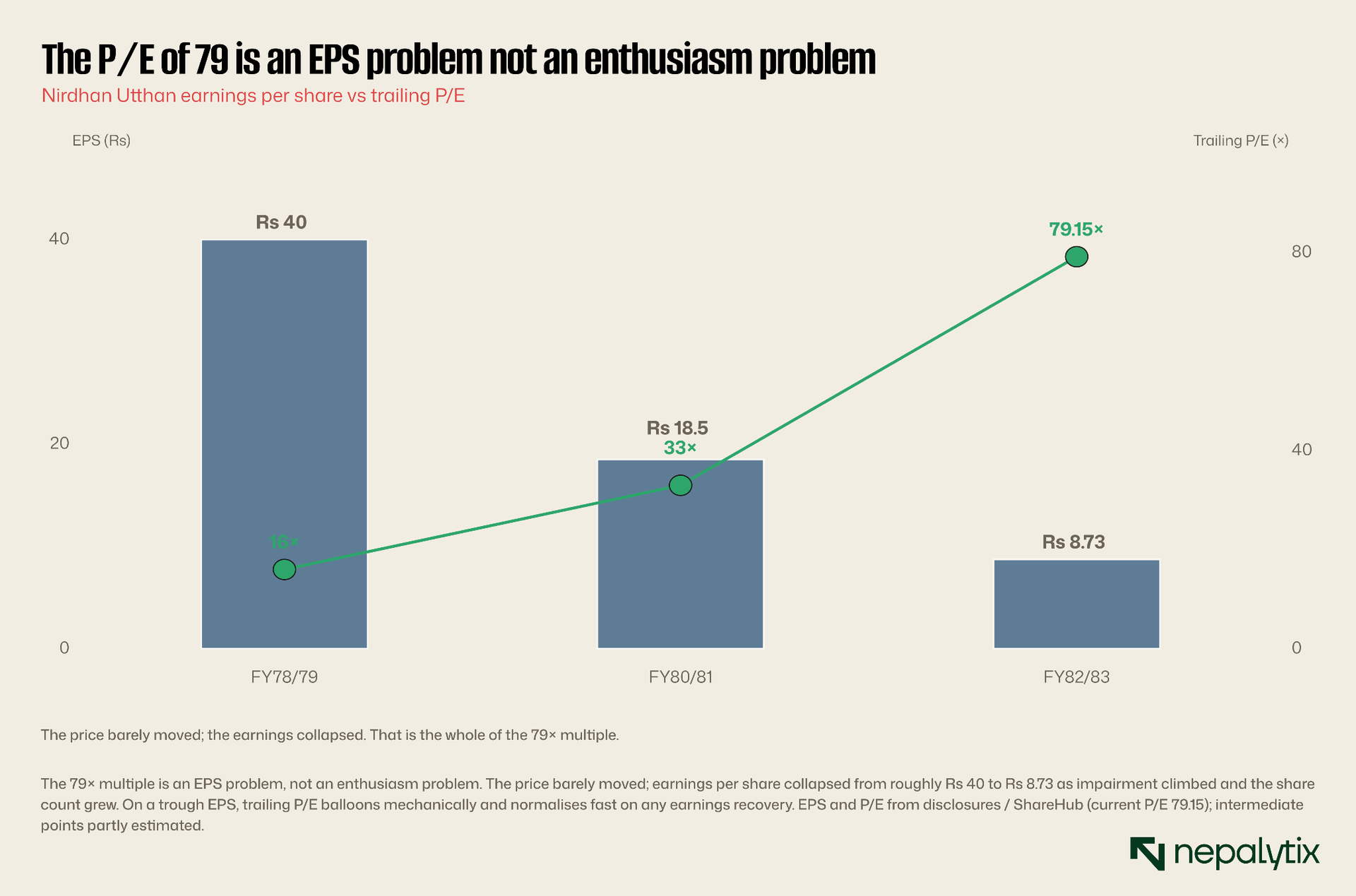

Start with the earnings because everything about Nirdhan's valuation flows from a single misunderstanding of them. Over the last decade the company's net profit has not trended; it has oscillated. It earned roughly Rs 74 crore in FY2075/76, at the top of the last microfinance boom. It collapsed to Rs 17 crore in FY2079/80. It then more than tripled, to Rs 50.6 crore, in FY2080/81. And on the current year's run-rate it is back down near Rs 24 crore. A casual reader sees chaos. A careful one sees a single variable doing all the work.

The variable is the impairment charge the money set aside against loans that may not be repaid. In FY2079/80 that charge was Rs 87.6 crore, and it crushed the bottom line to Rs 17 crore. The next year the charge nearly halved to Rs 43.1 crore and profit tripled. Nothing fundamental changed about the business between those two years; the loan book, the branches, and the interest margin were broadly stable. What changed was how many rupees the company had to reserve against bad loans. Nirdhan's reported profit, in other words, is not a measure of how much money the lending business makes. It is a measure of where the credit cycle sits.

Nirdhan's profit is not a measure of the business. It is a measure of the credit cycle and the cycle just turned against it.

This matters enormously for what you are buying at Rs 691. The current Rs 24 crore run-rate is not a normal year; it is a year in which the sector-wide bad-loan surge is forcing the impairment charge back up. If and it is a large if the borrower base stabilises and the charge recedes the way it did in FY2080/81, the same loan book will throw off two to three times the profit with no change to the underlying franchise. That is the mechanical bull case and it is why a trailing P/E of 79 is not the absurdity it appears. It is also, we will argue, already in the price.

It helps to see the mechanism concretely. Nepal's central bank sets provisioning norms that rise sharply as a loan ages past due a small reserve against a loan a few weeks late, escalating to full provision once it is classified as bad. So an institution does not choose its impairment charge; the charge is dictated by how much of the book has slipped, and by how far. This is why the line is so volatile: a modest deterioration in on-time repayment cascades through the ageing buckets and lands as a large swing in the charge. It also means the charge is a faithful, if brutal, real-time readout of borrower health which is exactly why it, and not the smoothed profit figure, is the number to watch each quarter.

Even the strongest name runs at half its peak

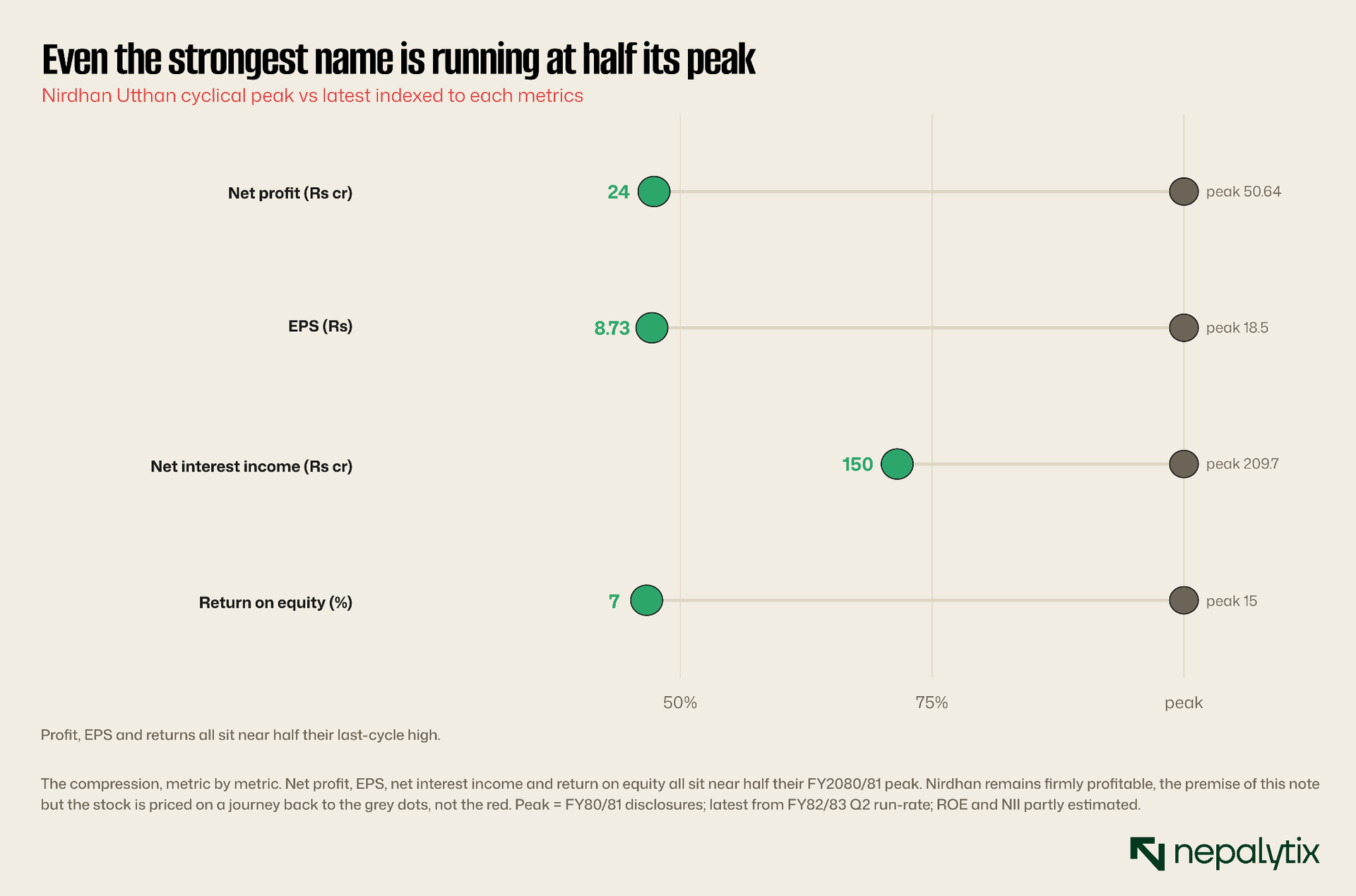

Before building the recovery case, it is worth being honest about the damage, because "survivor" is too often read as "unscathed." Nirdhan is not unscathed. On every headline metric it is running at roughly half its last-cycle high.

Net profit is down from Rs 50.6 crore to Rs 24 crore. Earnings per share has fallen from the high teens to Rs 8.73, a decline amplified by the bonus-share issuance that has steadily enlarged the share count over the years, a recurring feature of Nepali microfinance that dilutes per-share figures even when absolute profit holds. Net interest income has eased from a peak above Rs 200 crore. Return on equity which sat in the low-to-mid twenties in Nirdhan's prime, has compressed into single digits.

None of these signals distress a return on equity of seven-ish percent through the worst sector downturn in memory is, in context, a mark of resilience not weakness. But it does discipline the valuation discussion. The investor buying at Rs 691 is not paying for the company as it is earning today; they are paying for a reversion toward what it earned two years ago. The rest of this note is an assessment of how likely that reversion is and how much of it the price already assumes.

Why it survives when others drown

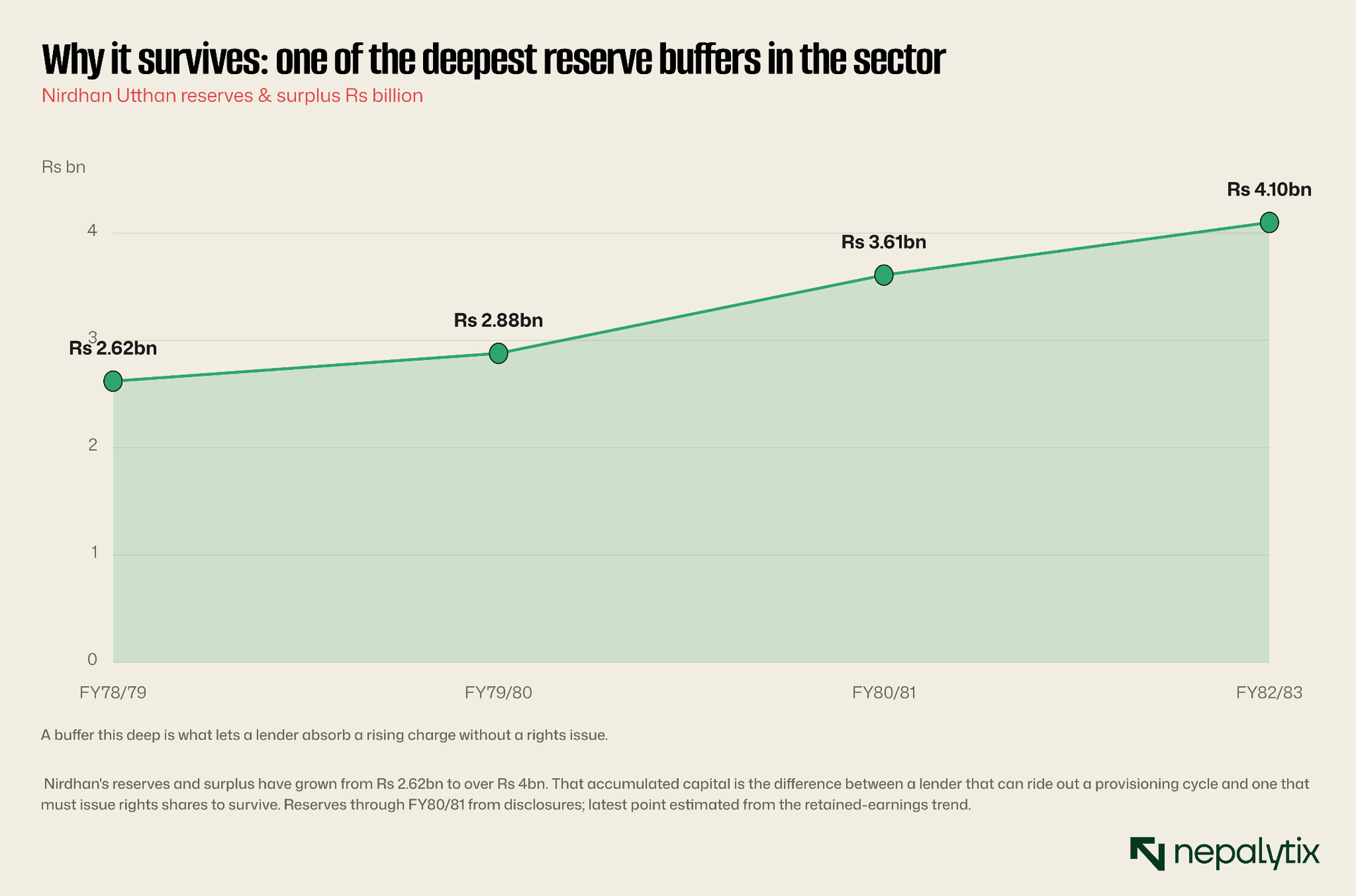

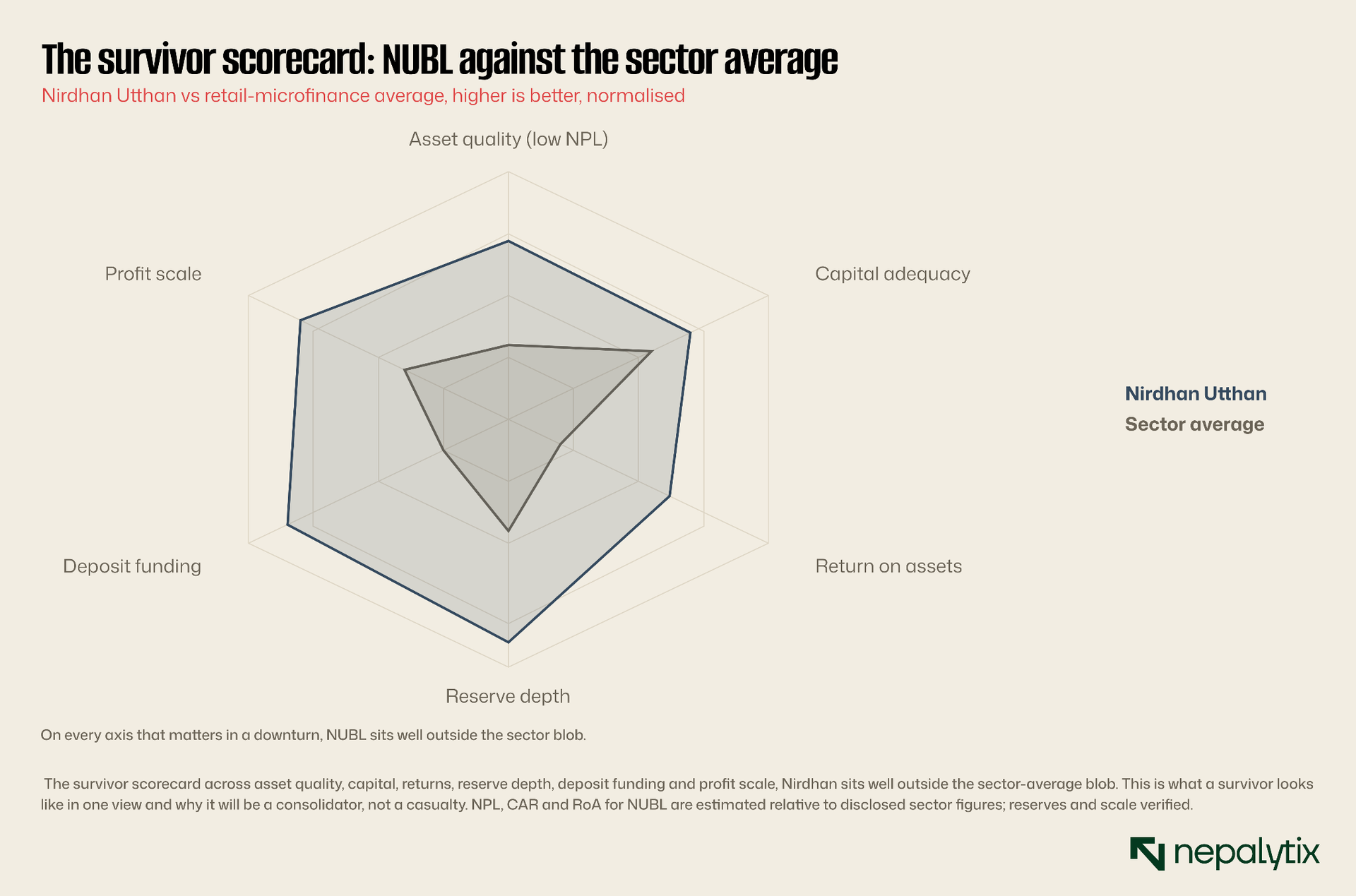

Nirdhan's resilience is not luck or brand sentiment. It rests on two concrete, structural advantages that the impaired majority of the sector simply does not have: a reserve buffer deep enough to absorb a rising charge without going to shareholders and a funding base cheap enough to protect the margin while the rate cap squeezes everyone else.

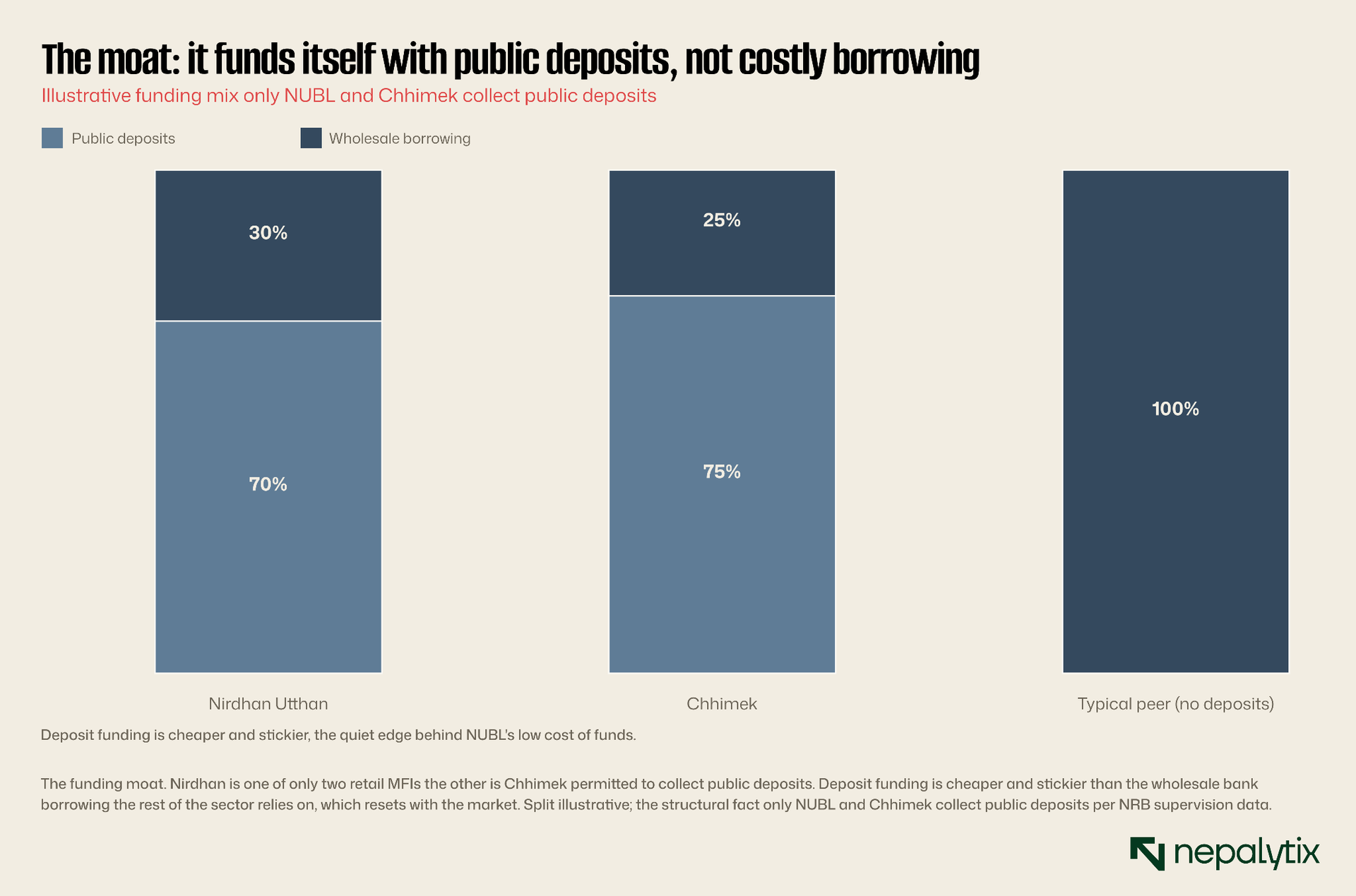

Take the reserves first. Nirdhan and Chhimek carry the two largest reserve-and-surplus balances in Nepali microfinance, and Nirdhan's has grown steadily past Rs 4 billion. This is the single most important line on its balance sheet in the current environment, because it is exactly what the 28 institutions now scrambling for rights-share approvals lack. When a bad-loan charge climbs, it is absorbed out of accumulated capital. An institution with a deep reserve simply eats the charge and carries on; an institution without one breaches its capital-adequacy floor and is forced to raise equity into a falling market or, increasingly, to merge. Nirdhan's reserve is its licence to ignore the panic that is gripping the rest of the sector.

The second advantage is subtler and, in a rising-rate world, more valuable: how Nirdhan funds itself. Almost every microfinance institution in Nepal is a borrower; it takes wholesale funding from commercial banks and lends it on to the poor, earning the spread. Nirdhan is one of only two retail MFIs, alongside Chhimek, licensed to collect deposits directly from the public. Deposit funding is cheaper than wholesale borrowing and far stickier; it does not reprice every time the interbank rate moves. That is why Nirdhan's cost of funds has historically sat below the sector's, and why its margin has proven more defensible through the squeeze. In a sector where a 15 percent lending cap holds the asset yield down, the institution with the lowest funding cost keeps the widest spread and Nirdhan is structurally one of them.

Put the two advantages together with Nirdhan's scale and the picture is a company built to be a consolidator. In a sector NRB is actively steering toward merger, the institutions with deep capital and cheap funding are the ones that acquire; the ones without are the ones acquired. Nirdhan sits firmly in the first group. Whatever the microfinance sector looks like in three years, it will be smaller. Nirdhan is overwhelmingly likely to be one of the names that absorbed others rather than one that disappeared. For an equity investor, that distinction is the whole game: solvency risk, the thing destroying value across the rest of the sector, is largely off the table here.

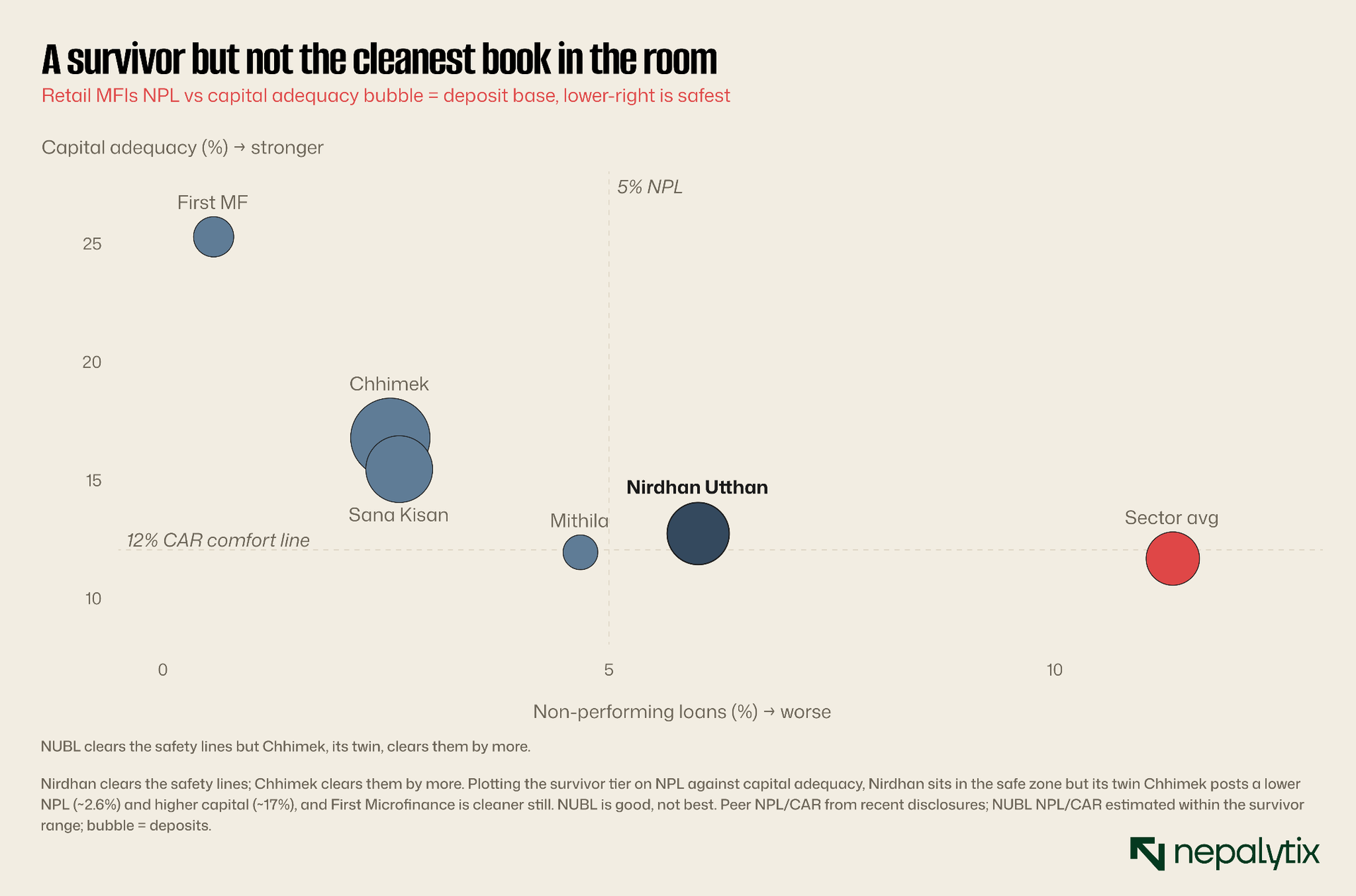

A survivor but not the cleanest book in the room

Here the note has to check its own enthusiasm. Nirdhan is a survivor but it is not the strongest survivor and an investor paying a premium for quality should know exactly what they are paying for relative to the alternatives.

The direct comparison is with Chhimek, Nirdhan's structural twin, the other public-deposit MFI, the other deep-reserve name, the other perennial blue-chip. On the numbers that matter in a downturn, Chhimek currently looks like the better book: a capital-adequacy ratio around 17 percent against Nirdhan's estimated low-teens, a non-performing loan ratio near 2.6 percent against Nirdhan's higher (though still well-below-average) figure and a dividend payout that has recently run above 60 percent of paid-up value comfortably ahead of Nirdhan's. First Microfinance, smaller but pristine, posts a 25 percent capital ratio and a sub-1 percent NPL. The point is not that Nirdhan is weak; it is that the survivor tier has several members and Nirdhan is not the standout on credit quality.

This is the first genuine mark against the investment case. If you are paying a premium specifically for the safety of a survivor, the rational question is why pay it for the second-safest name rather than the first. Nirdhan's answer and it is a real one is scale, franchise depth, the pioneer's brand, and a more liquid float. But it is an answer that has to be weighed not assumed and it puts additional pressure on the valuation to be reasonable. It is not.

How to resolve it? For an investor who simply wants the safest microfinance balance sheet, Chhimek is the more logical default, and this note says so plainly. Nirdhan earns its place in a portfolio on different grounds: the larger more liquid float that makes it easier to build and exit a position; the deeper branch network and member base that make it the more natural consolidator; and the pioneer franchise that, in a sector being actively merged, is more likely to be the surviving brand. Those are real, but they are second-order advantages to hold Nirdhan alongside Chhimek, not instead of it and certainly not at a premium to it. The valuation has to respect that ordering, and at Rs 691 it does not.

The business works; the provisioning is the problem

To separate the franchise from the cycle, look at the top line against the bottom line. If Nirdhan's troubles were a broken business, customers gone, margin collapsed, branches unprofitable you would see it in net interest income. You do not.

Net interest income, the actual output of the lending machine, interest earned less interest paid has drifted down only modestly from its peak above Rs 200 crore in line with a loan book that has slowed but not shrunk dramatically. Net profit, meanwhile, has lurched from Rs 40 crore to Rs 51 crore to Rs 24 crore. The entire difference between the stable top line and the volatile bottom line is the impairment charge. That is a diagnostic result: it tells you Nirdhan does not have a franchise problem or a margin problem. It has a borrower problem, and a borrower problem is, at least in principle, cyclical rather than terminal. When the microfinance borrower begins repaying again after the protests fade after over-indebtedness works through after NRB's tighter lending rules stabilise the base the impairment charge recedes and the profit line springs back up toward the interest-income line. That is the recovery the fan chart in the next section tries to size. It is real and it is also, critically, not guaranteed and not imminent.

The valuation: paying today for tomorrow's recovery

Now to the number everyone stumbles on. A trailing price-to-earnings ratio of 79 is on its face, indefensible for a microfinance stock in a sector crisis. It is not indefensible but understanding why leads directly to why the stock is nonetheless not cheap.

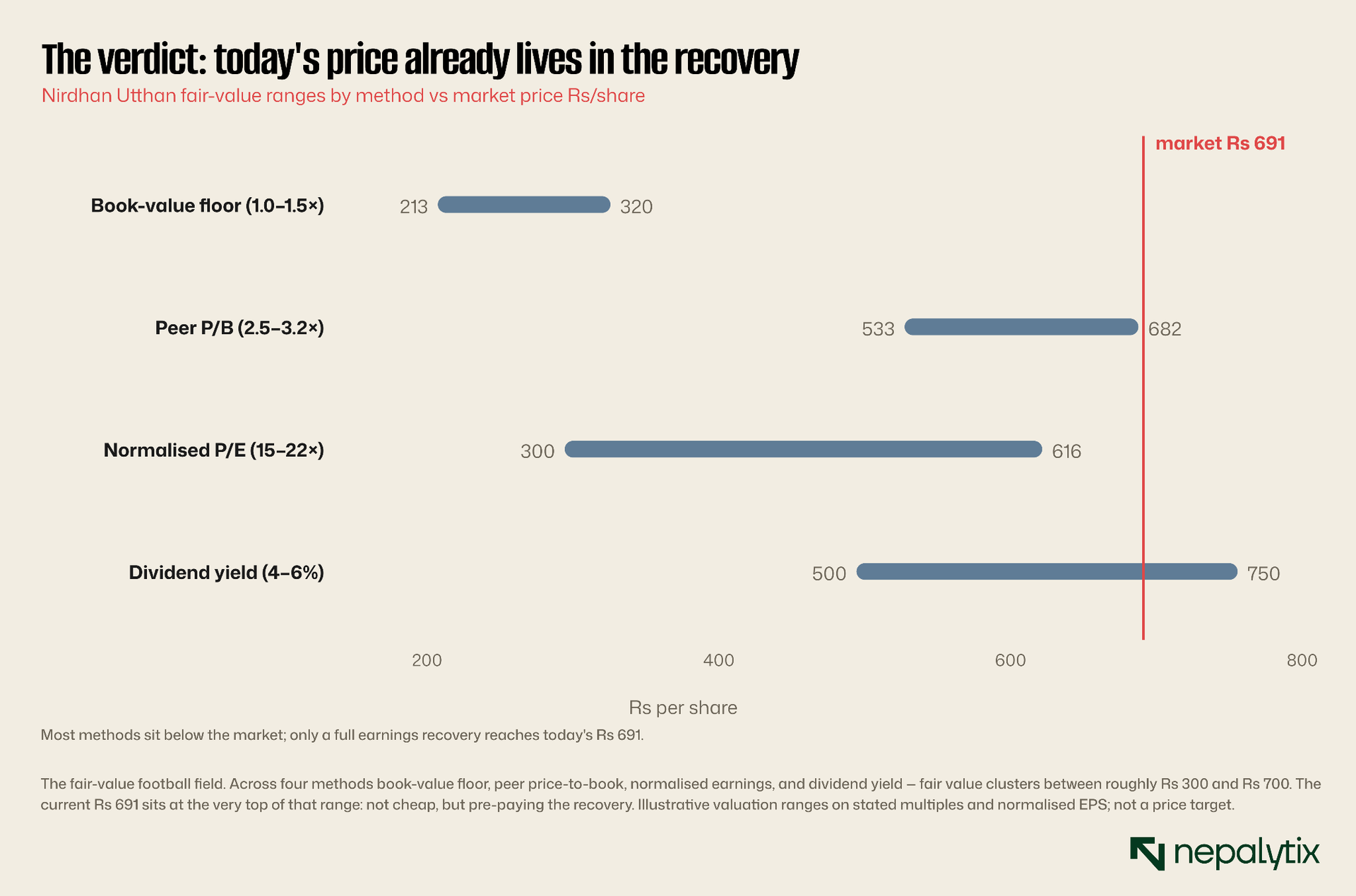

The P/E is high because the E is at a trough, not because the P is euphoric. Earnings per share has fallen from around Rs 40 in Nirdhan's prime to Rs 8.73 today driven both by the impairment squeeze and by years of bonus-share dilution. Divide a roughly stable price by a collapsed denominator and the ratio explodes mechanically not emotionally. On even a partial earnings recovery toward, say, Rs 20 of EPS, the same price implies a P/E in the mid-30s; on a full recovery toward the mid Rs-20s, the low 30s or high 20s. So the trailing multiple, taken literally, misleads. The honest valuation anchor is not the P/E at all, it is the price-to-book of 3.24 which does not depend on a single volatile year's earnings.

Triangulate the fair value across methods and a consistent picture emerges. The book-value floor what you would pay for the equity with no premium at all is about Rs 213 rising to perhaps Rs 320 at a modest 1.5 times book. A peer-based price-to-book of 2.5 to 3.2 times in line with where the strong names trade puts fair value in the Rs 530 to Rs 680 band. Capitalising normalised earnings of Rs 20 to Rs 28 at a sector-appropriate 15 to 22 times lands between roughly Rs 300 and Rs 620. And a dividend-based approach assuming Nirdhan restores a healthier payout, supports something in the Rs 500 to Rs 750 range. Stack those together and the current Rs 691 does not sit in the middle of fair value. It sits at the top of it. There is a coherent set of assumptions under which the stock is worth what it costs but they are the optimistic assumptions, and the price already embeds them.

The dividend history reinforces the point. Nirdhan has historically been a generous payer with cash-plus-bonus distributions ranging from around 30 percent to as high as 80 percent of paid-up value in stronger years. At the current depressed earnings the payout has necessarily thinned the trailing yield to just 2.68 percent but a normalised Nirdhan earning north of Rs 20 a share could comfortably support a mid-single-digit yield on a lower price. That is the basis for the dividend-yield valuation line, and it points to the same conclusion by a different road: the income case works at a price in the Rs 500s not at Rs 691.

The stock is not cheap. It is fully valued for a recovery that has not yet started.

What you are actually buying: a call on the borrower

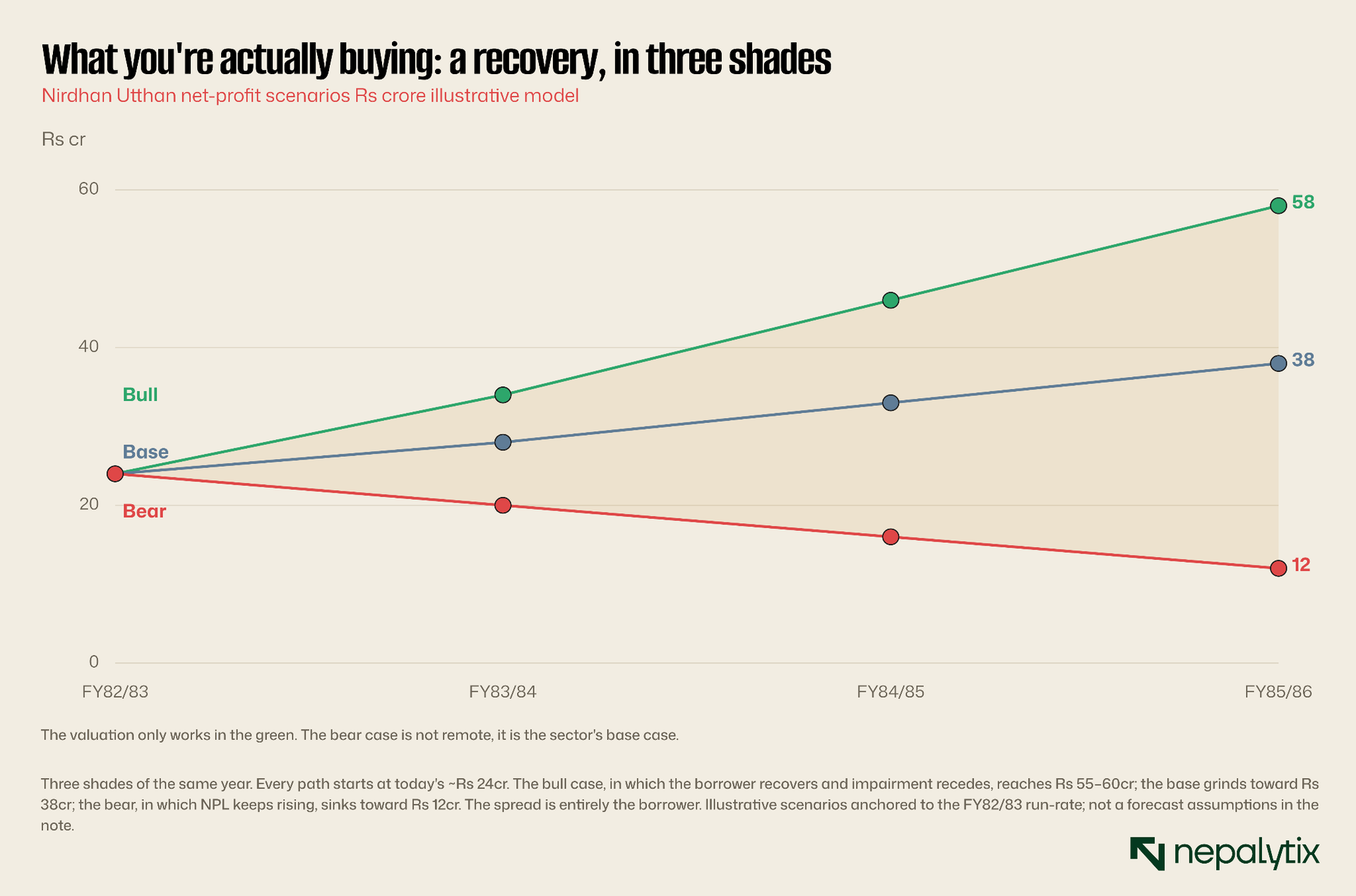

Strip away the branches and the reserves and the pioneer's history, and the Nirdhan investment reduces to a single question: will the Nepali microfinance borrower start repaying again, and how soon? Everything about the forward earnings and therefore the valuation pivots on that one variable.

The fan chart above is not a forecast; it is a decomposition of the bet. In the bull case, the protests recede into memory, NRB's tighter per-borrower lending limits stabilise the base, the impairment charge halves the way it did in FY2080/81, and profit climbs back toward Rs 55–60 crore at which point today's price looks like foresight. In the base case, the sector muddles through, impairment stays elevated but stops rising, and profit grinds up toward the high-Rs-30s-crore at which point the stock is roughly fairly valued and you have made your money from dividends and time. In the bear case, the bad-loan rate keeps climbing the way it has for two years running, the charge grows, and profit sinks toward Rs 12 crore at which point Rs 691 was a mistake.

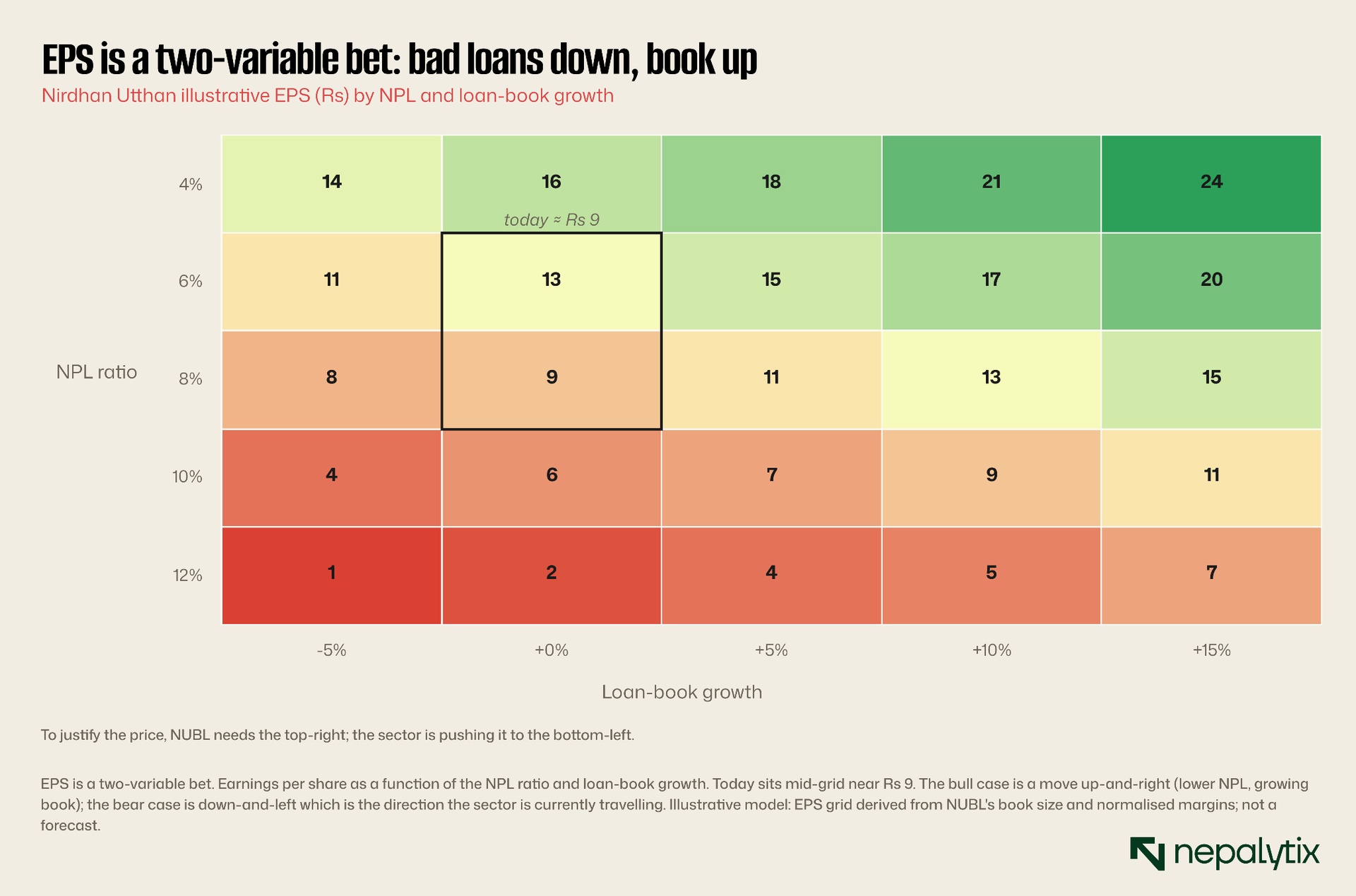

The sensitivity grid makes the asymmetry uncomfortably clear. Nirdhan's earnings power is a function of two things it only partly controls: the bad-loan rate and the growth of its loan book. Move both favourably NPL down toward 4 percent, book growing double digits and EPS climbs toward the low Rs-20s, validating the price. Move both against it the direction the entire sector is currently travelling and EPS falls toward low single digits leaving the stock stranded at 79 times a shrinking number. The honest reading is that the base case is fine and the bull case is plausible but the bear case is not a tail scenario. It is, right now, the sector's central tendency. You are being asked to pay the top of fair value for an outcome that is, at best, a coin-flip better than the prevailing trend.

That asymmetry is the heart of the matter. The upside from here a clean recovery to Rs 55–60 crore of profit is perhaps a 40 to 60 percent gain on the stock over two to three years. The downside, a continued grind lower with the sector is a 20 to 30 percent de-rating that could arrive far sooner, because a full-priced stock does not need bad news to fall; it only needs the good news to be late. Reward roughly comparable to risk, with the risk front-loaded and the reward back-loaded, is not a compelling entry. It is a reason to wait for a better one.

Risks

The bull case rests on a recovery that has not started, so the risks are mostly the ways that recovery fails to arrive or arrives too slowly to justify the price.

Borrower deterioration continues. The central risk is simply that the sector's bad-loan rate keeps climbing. It has risen for two years straight, from 2.6 percent to 11.3 percent, with no confirmed inflection yet. If the group-lending base stays broken, Nirdhan's impairment charge keeps climbing and the profit line keeps compressing, the bear path on the fan chart, and currently the sector's central tendency rather than a tail.

The rate cap limits the rebound. Even in recovery, the 15 percent lending ceiling caps how much margin Nirdhan can rebuild. Higher volumes and better asset quality lift profit but the cap puts a hard lid on the yield side of the spread so the earnings ceiling is lower than in previous cycles. The bull case is real, but bounded.

Bonus-share dilution. Nirdhan has a long history of issuing bonus shares, which steadily enlarges the share count and dilutes per-share earnings even when absolute profit grows. An investor modelling an EPS recovery must net out the near-certainty of further bonus issuance, which can absorb a meaningful slice of any profit rebound before it reaches EPS.

Regulatory shift. Microfinance is heavily and actively regulated. NRB has already tightened per-borrower lending limits, tied dividends to capital and NPL ratios, and signalled a merger-first stance. Further tightening on provisioning norms, capital requirements, or permissible dividends could constrain both the earnings recovery and the cash returned to shareholders.

Sector contagion and forced consolidation. Even a strong institution is not immune to a sector in distress. If a disorderly failure among the impaired majority shakes depositor or investor confidence or if NRB's consolidation drive pushes Nirdhan into an acquisition on dilutive or distracting terms, the equity could de-rate regardless of its own book.

Valuation de-rating. Finally, the price itself is a risk. At 3.2 times book and 79 times trough earnings, Nirdhan has little valuation cushion. If the recovery is delayed, the market can simply re-rate the stock toward the middle of its fair-value range, a 20 to 30 percent move with no deterioration in the business at all. Buying at the top of fair value means the valuation is working against you from day one.

Catalysts and what to watch

The thesis turns on a small number of observable signals, and an investor can track the bull-bear balance in near real time by watching them.

The impairment line, quarter by quarter. The single most important number in every Nirdhan quarterly is the impairment charge, not the headline profit. A charge that stops rising even before it falls is the first hard evidence the credit cycle has turned and it will move the stock before the profit recovery is visible.

The sector NPL prints. NRB's microfinance supervision data and the quarterly sector compilations are the leading indicator for Nirdhan's own book. The sector rate rolling over from 11.3 percent underwrites the bull case; another leg higher confirms the bear.

Monetary policy and the rate cap. Any move by NRB on the 15 percent lending cap, on microfinance provisioning norms, or on the broader rate environment feeds directly into the spread. The policy calendar is a genuine catalyst in either direction.

Consolidation activity. Nirdhan is positioned to be an acquirer. A well-priced acquisition that adds book and members without straining capital would be a concrete demonstration of the survivor thesis; a poorly-priced or dilutive one would undercut it.

The dividend. Nirdhan has historically paid generously. A restored, healthy dividend would signal management's confidence in the capital position and put a yield floor under the stock; a cut or suspension would signal the opposite.

The price itself. And, prosaically, the level. The stance here is that Nirdhan is worth accumulating on weakness toward the middle of its fair-value range. A retreat into the Rs 400s to low Rs 500s converts a full-price quality name into an attractive one.

The verdict

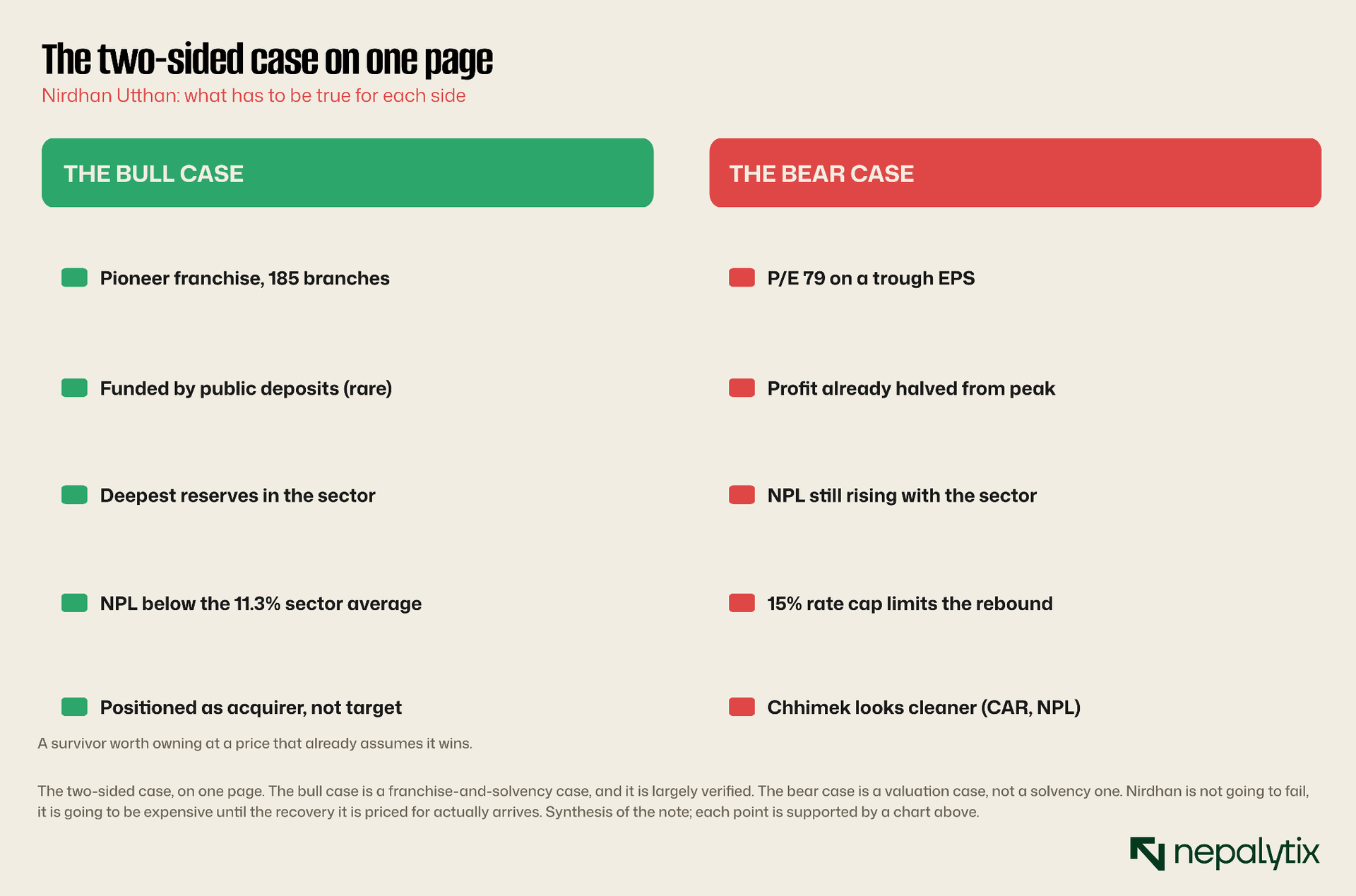

Set the two sides against each other honestly. The bull case is real and unusually mostly verifiable: a pioneer franchise with 185 branches, one of only two deposit-funded MFIs, the deepest reserves in the sector, a below-average bad-loan rate, and a balance sheet built to acquire rather than be acquired. The bear case is narrower but sharper, and it is entirely a valuation case: a P/E of 79 on trough earnings, profit already halved, a bad-loan rate still rising, a rate cap limiting the rebound, and a twin Chhimek that looks cleaner on the numbers that matter.

Note what the bear case is not: it is not a solvency case. That is the crux. Nirdhan is not going to fail; choosing it over the 28 institutions above 10 percent NPL is precisely how you take solvency risk off the table. What you take on instead is valuation risk. At Rs 691 you are paying the top of a defensible fair-value range for a recovery that has not begun in a sector whose central tendency is still deterioration. That is not a bad company. It is a good company at a full price.

Stance. Nirdhan Utthan is the quality name in a broken sector, and quality is worth owning through a consolidation that will reward the acquirers. But the current price already discounts the recovery it is waiting for, and the cleaner balance sheet next door raises the bar further. The place to own Nirdhan is on weakness when the price retreats toward the middle of fair value in the Rs 400s to low Rs 500s where the recovery is an upside option rather than the base assumption. At today's 79 times trough earnings and 3.2 times book, it is one to accumulate patiently not to chase.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.