Nepal’s Budget Week: Idle Liquidity, Rising Debt and NEPSE’s 2,790 Wall

NEPSE tested resistance twice before the FY2083/84 budget as rising debt, idle liquidity and CGT uncertainty shaped market positioning.

A three-session holiday week, and a market that refused to commit before Jestha 15. NEPSE rallied Monday, tested 2,790 twice, failed both times, and drifted into the budget on thinning volume. Underneath the quiet tape sits the real story: a budget shrinking into a record debt load, a banking system buried in idle cash, and a capital-gains question the government has dodged for three years.

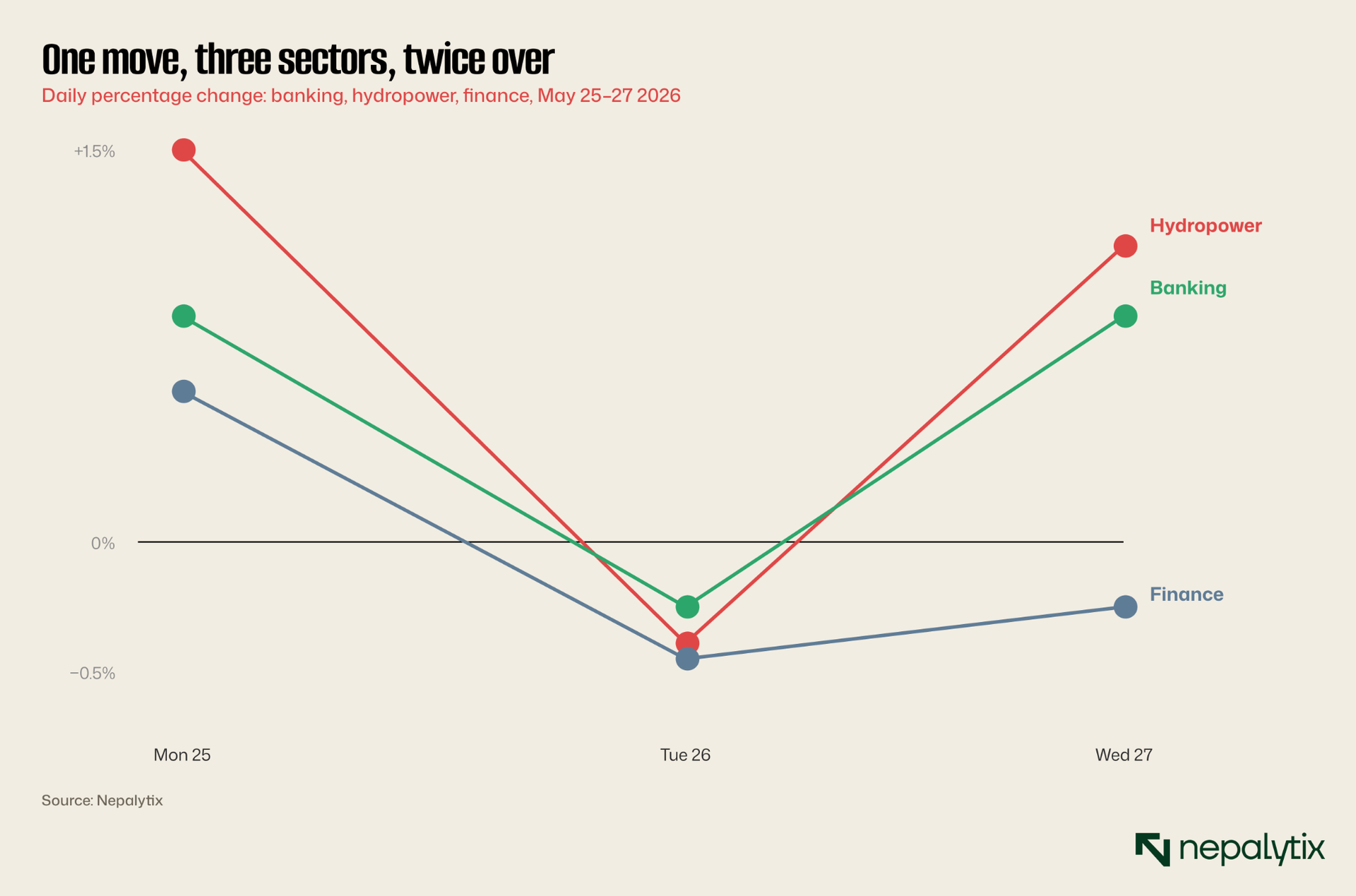

→ NEPSE full week: 2,758.49 → 2,782.1, a 3-session move of 23.61 points (0.86%), a Monday rally, a Tuesday flush, a Wednesday recovery.

→ Advancers, Tuesday to Wednesday. Breadth went from 69 up / 190 down to 151 up / 100 down, the flush and the snap-back.

→ Sub-indices green Wednesday, reversing Tuesday's all-red. Non-life insurance led (+1.87%); only finance stayed down.

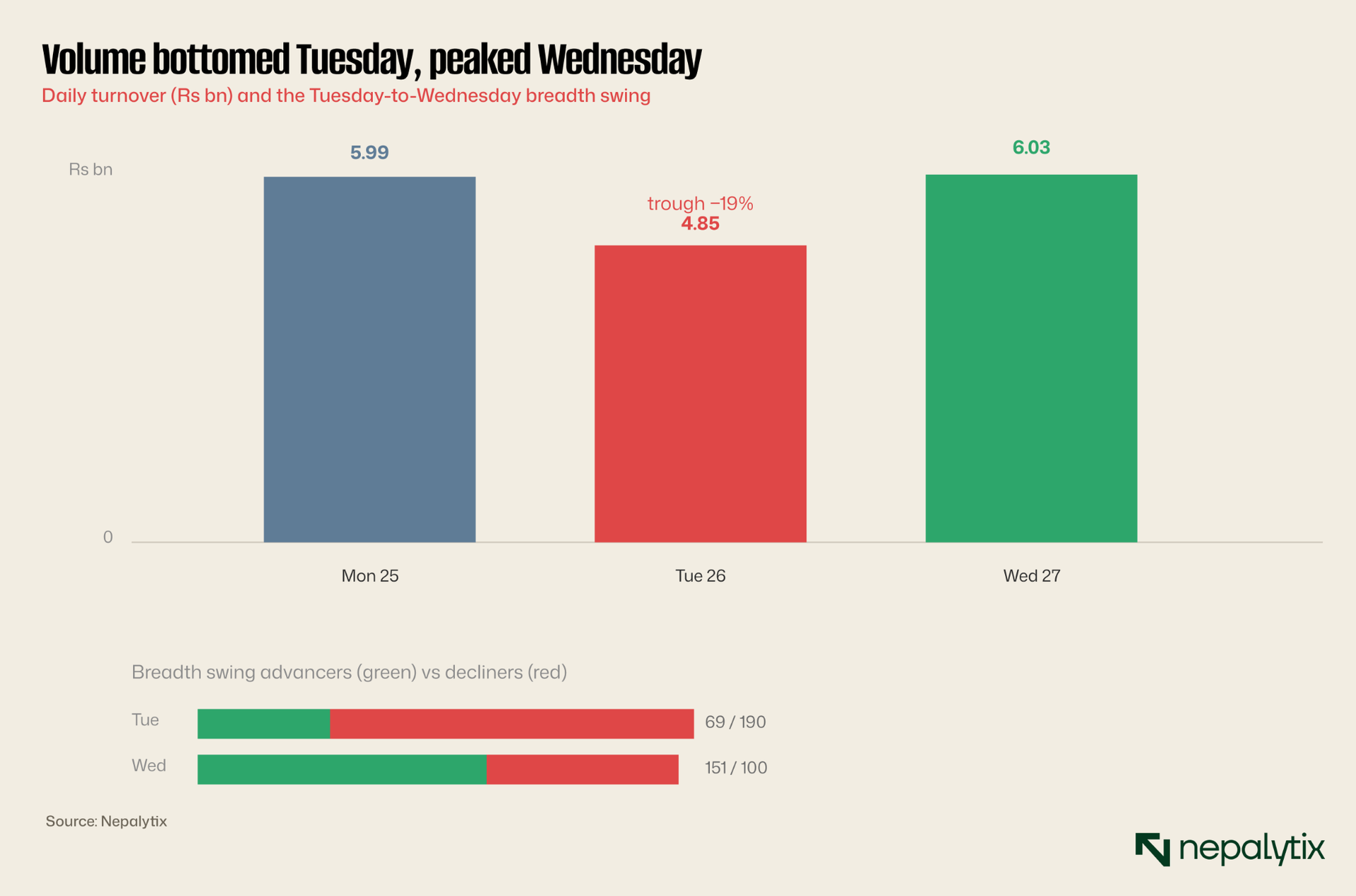

→ Three-session turnover. 5.99 → 4.85 → 6.03bn bottomed Tuesday and peaked Wednesday, the week's heaviest, into the budget.

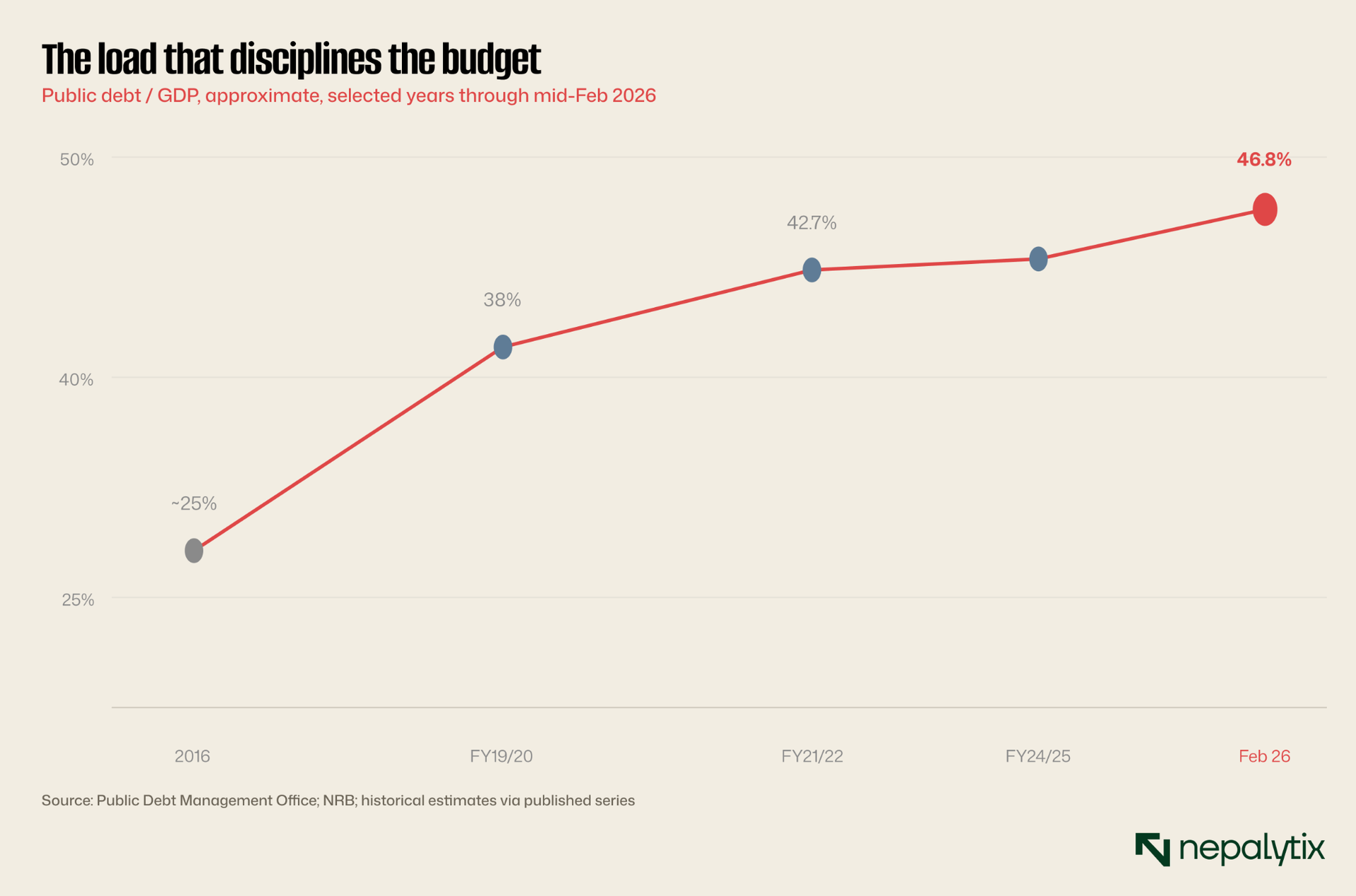

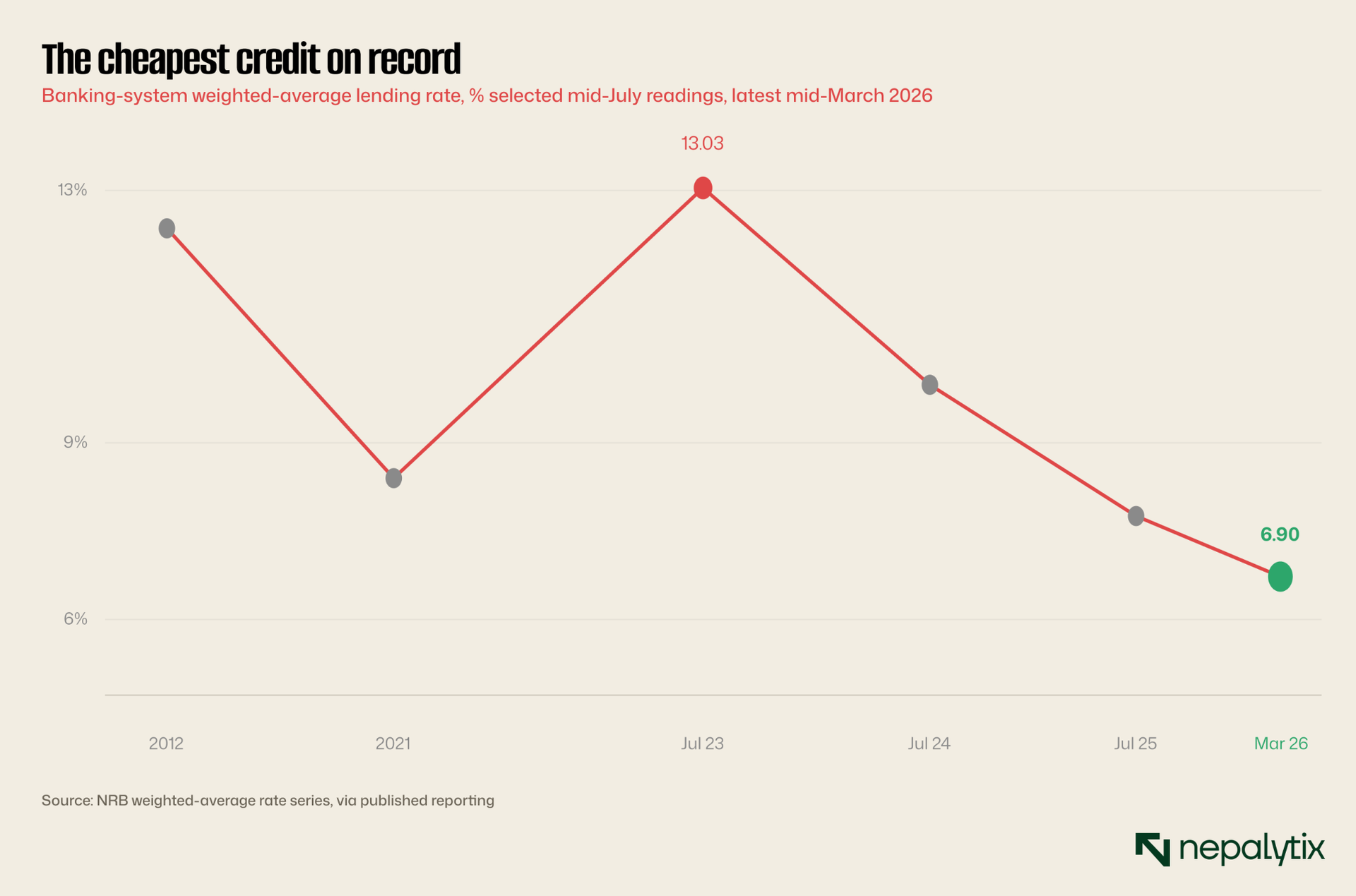

→ 46.8% public debt as a share of GDP Rs 2.858tn, up from 38% in FY19/20. The constraint behind a shrinking budget.

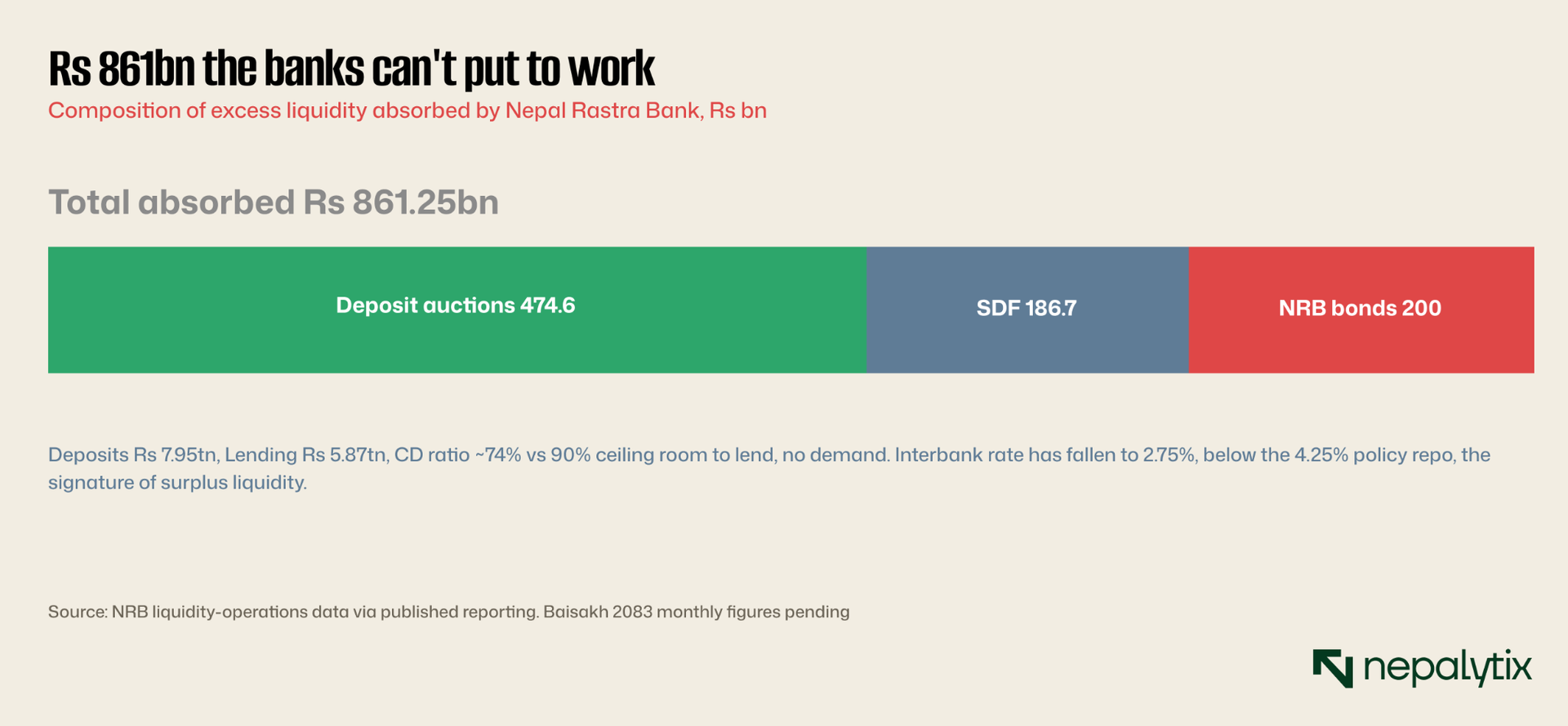

→ Rs 861bn bank cash sitting idle at NRB. The system is drowning in money it cannot lend which reframes every budget lever

I. The week in three sessions

Monday opened soft, the index gapped down to 2,752.94, below Friday's close and then rallied for the rest of the day to finish at 2,786.35, up 1.01%. Hydropower led (+1.51%), banking followed (+0.87%), and it had the shape of conviction. Tuesday printed a fresh intraday high of 2,791.85, was rejected inside the hour, and closed down 0.33% on a 190-to-69 decline ratio, the week's risk-off flush. Then Wednesday did the opposite: it opened at 2,777.71, recovered to close up 0.18% at 2,782.10, with breadth flipping to 151 advancers and the heaviest turnover of the week behind it.

Start with the candles. Twice Monday's 2,790.34 and Tuesday's 2,791.85, the index walked up to the same overhead supply and was sold. Wednesday's recovery stopped short of it, peaking at 2,785.33. That band, not any single close, is the week's real number, and the budget will decide whether it breaks.

The sector tape confirms the read. This was not a stock-picker's week; it was a risk-on, risk-off, risk-on week, and the three largest sub-indices moved as a single block up together Monday, down together Tuesday, up together Wednesday. When the heaviest sectors trace the identical V, the market is trading a macro event, not company fundamentals. Hydropower swung the widest at both ends (+1.51%, −0.39%, +1.17%); only finance failed to fully recover on Wednesday.

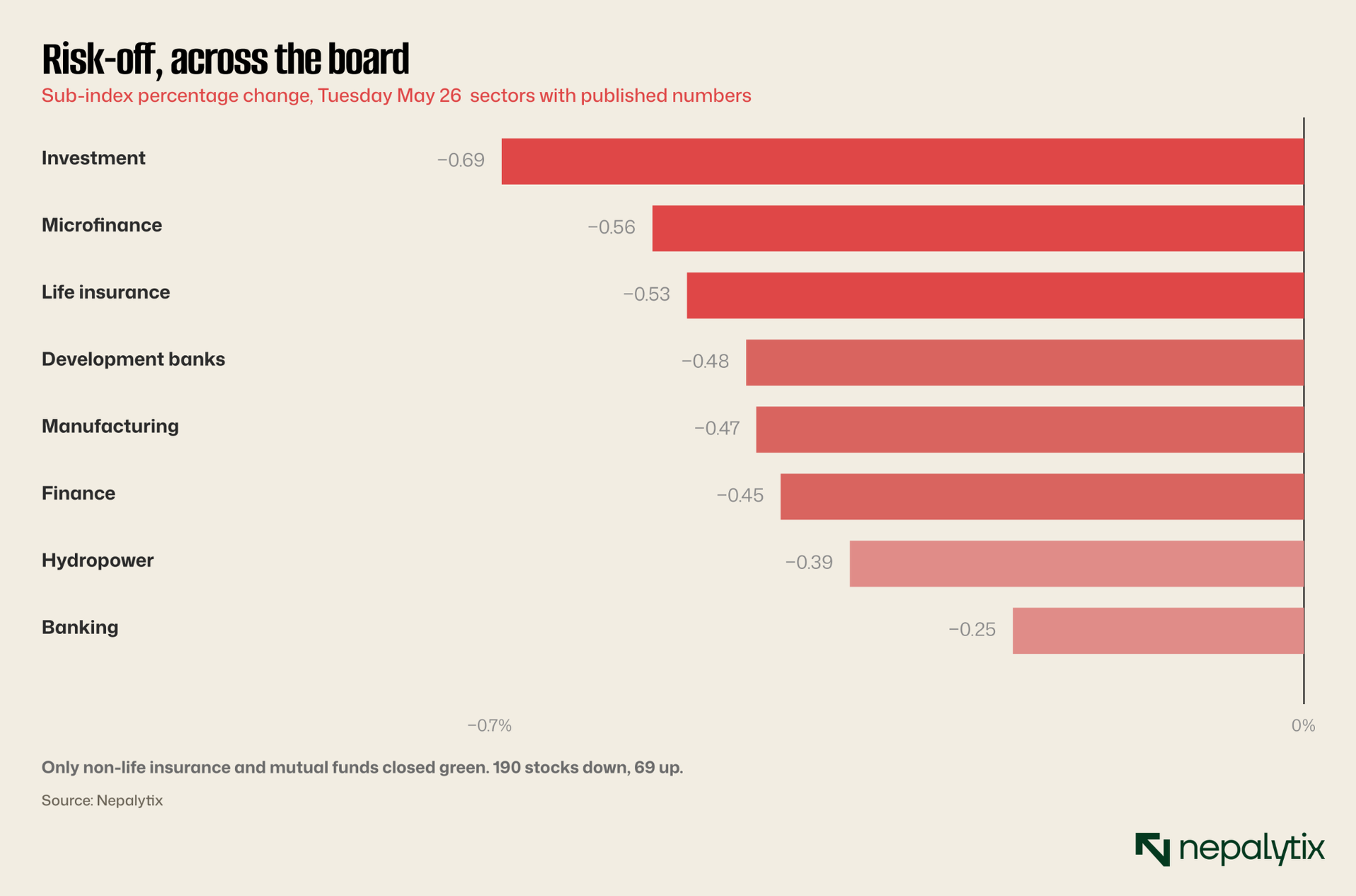

Tuesday is the session worth dwelling on, because it shows what the index was hiding. The headline fell only a third of a percent, cushioned by the heavyweight blue chips, the Sensitive Index slipped to 474.29 but underneath, the selling was uniform. Every numbered sub-index fell, led by investment (−0.69%), microfinance (−0.56%), and life insurance (−0.53%). Only non-life insurance and mutual funds closed green. That is not rotation; that is a market quietly stepping to the sidelines.

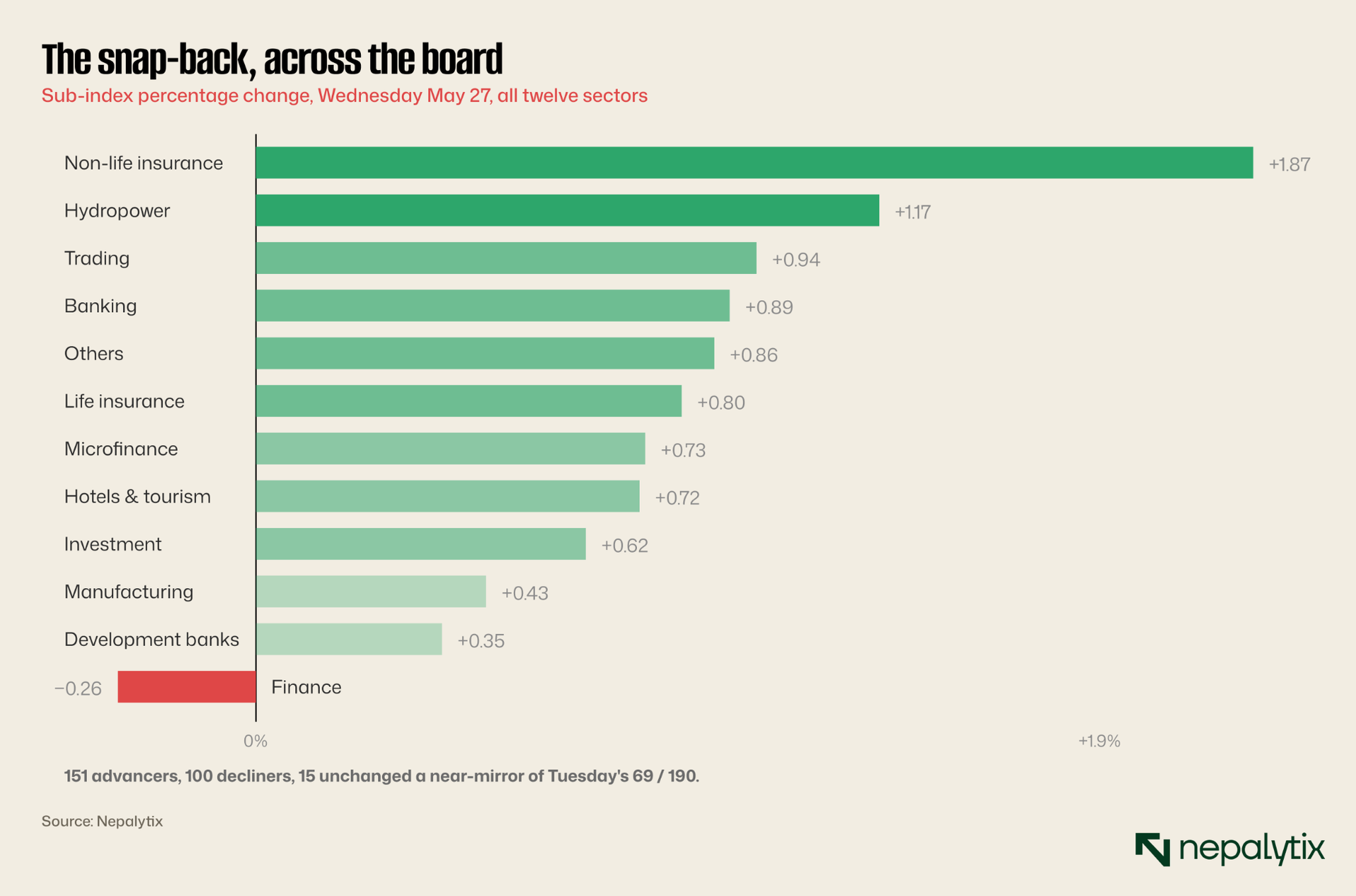

Then Wednesday inverted it almost perfectly. Eleven of the twelve sub-indices closed green, led by non-life insurance (+1.87%) and hydropower (+1.17%); only finance stayed underwater, and only just (−0.26%). The same large-caps that had cushioned Tuesday's decline now led the advance, and breadth confirmed it 151 up against 100 down, a clean reversal of Tuesday's 69-against-190. A market that flushed its weak hands on Tuesday went back in on Wednesday.

The single-stock tape tells the same recovery story. Wednesday's gainers were led by Bungal Hydro (+13.37%) and Crest Micro Life (+8.52%), with hydropower names AKJCL, Ridi and Modi crowding the leaderboard; the losers were idiosyncratic Samaj Laghubitta at the −10% floor, Shivam Laghubitta and Corporate Development Bank both off 4.93%. The damage was stock-specific, the strength sector-wide. That is the profile of a market that has finished selling and started repositioning.

And the fuel gauge tells the cleanest version of the arc. Turnover did not simply fade into the holiday; it dipped 19% to a Tuesday trough of Rs 4.85bn, then rebounded to Rs 6.03bn on Wednesday, the heaviest session of the week. Whatever de-risking happened on Tuesday, the money came back on Wednesday, carrying the market into the budget rather than away from it.

One estimate worth stating plainly because the platform record is incomplete: with the benchmark up 0.86% off the Rs 4.704tn market cap recorded at Friday's 2,758.49 close, investor wealth rose by roughly Rs 40bn on the week, to an estimated ~Rs 4.74tn. Treat that as an index-derived approximation, not a reported figure NEPSE's official market cap reflects float adjustments the index move alone does not capture.

II. What the market is actually pricing

The FY2083/84 budget was presented Jestha 15, May 29 the day after this window closed. This week is the setup; the verdict is next week. So the question for this week is not what the budget says but what the market was positioning around. Three levers, in descending order of how directly they hit the secondary market.

Capital gains tax is first because it changes the after-tax arithmetic of every realised trade immediately. Margin lending is second but here the conventional framing is already out of date. Financial-sector reform cooperatives, BFI consolidation, asset-quality cleanup is the slow third, the one that shapes the next cycle rather than the next session.

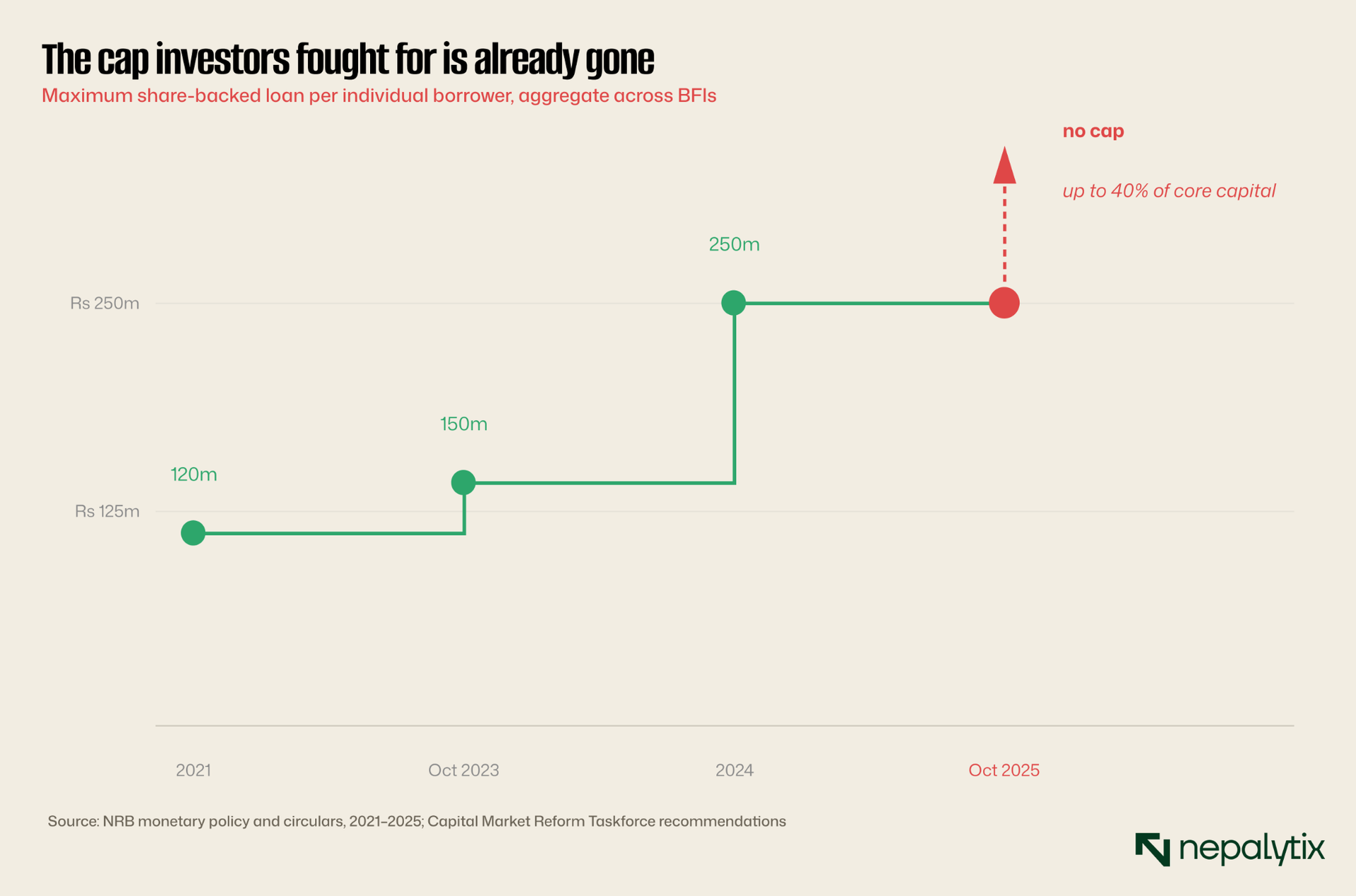

Take margin lending, because it is the most misunderstood of the three. The investor lobby spent years demanding the central bank lift the cap on share-backed loans and it won. NRB removed the per-customer ceiling entirely in Asoj 2082 (October 2025), the last step in a long climb: from the Rs 40m-per-bank / Rs 120m-total "4/12" regime of 2021, to Rs 150m/200m in 2023, to a Rs 250m aggregate, to no cap at all, with banks now permitted to lend up to 40% of core capital against shares.

So the margin question is no longer "will the budget loosen credit to the market?" The credit is already there, on paper. The live questions are subtler: whether the new SEBON Margin Trading Directive 2082 actually puts broker-financed leverage to work, whether banks will be allowed to invest directly in equities (a standing investor demand), and whether any of it matters while loan demand is dead. Which is the bridge to the two sections that follow the budget's fiscal posture, and the wall of idle money behind it.

III. THE CGT question, in numbers

Nepal taxes capital gains on listed securities by holding period: 7.5% on shares held a year or less, 5% beyond 365 days. Those rates have held for years, and stability not the level is what the market is asking the budget to protect.

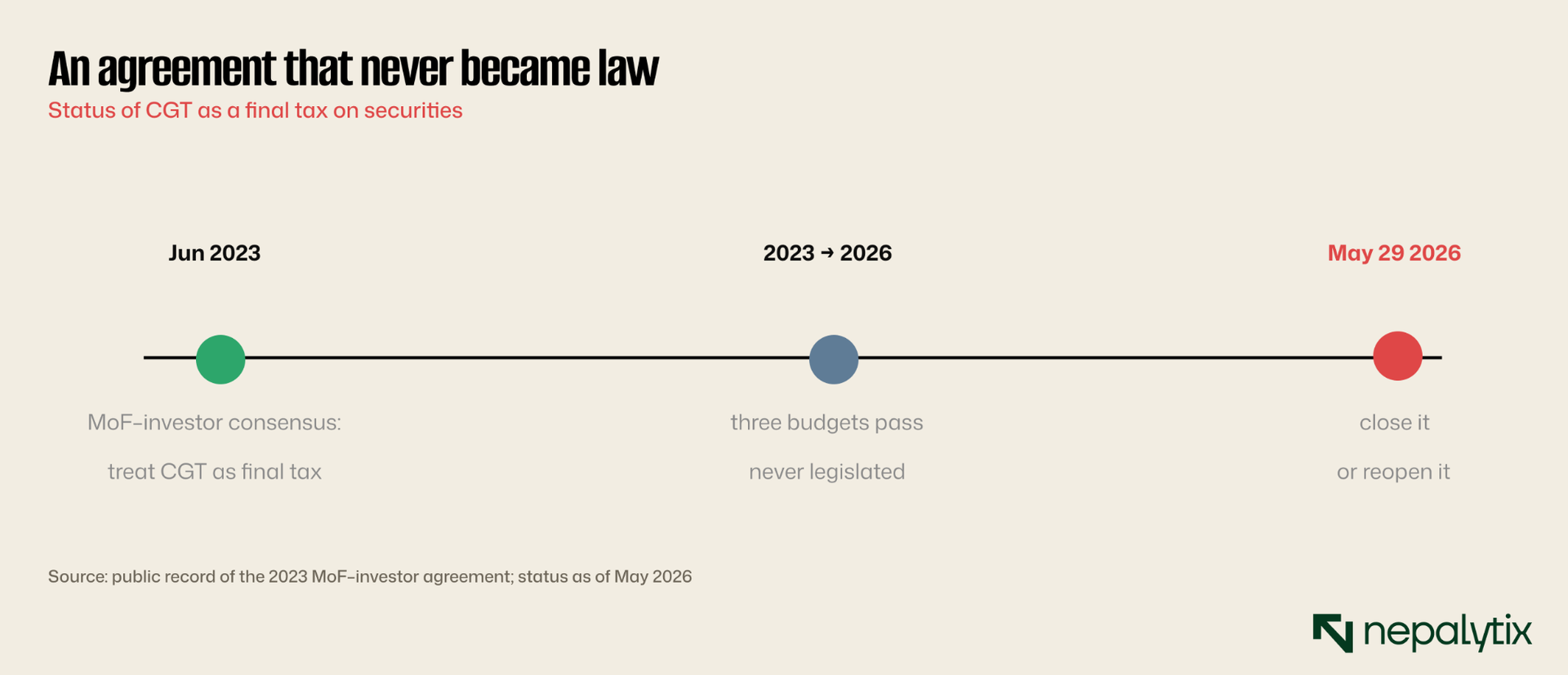

The anxiety is not the rate itself most market voices, including investor-association leaders, call 5% and 7.5% entirely reasonable. The anxiety is the combination of a rumoured hike and a legal question the government has left open for three years. In June 2023, investor groups and the Ministry of Finance reached a consensus to treat CGT as a final tax on securities. It was never written into law. Every budget since has been an opportunity to formalise it, and every budget has passed without doing so.

Continuity is the asset. Investors aren't asking for a cut, they're asking the government to stop moving the goalposts.

Why does a few percentage points carry such weight? Because the cost is not only the rupees withheld it is behavioural. Run the mechanics on a clean Rs 100,000 long-term gain.

A market that already struggles to generate Rs 5bn of daily turnover does not need a tax that rewards sitting still. The legal backstory is short, and unresolved.

IV. The arithmetic behind the gavel

Here is the fact that frames everything else: the FY2083/84 budget is expected to be smaller than the one before it. The proposed ceiling is around Rs 1.89tn, against Rs 1.964tn for FY2082/83, a rare nominal contraction. After a decade of budgets that grew almost every year, the government is signalling restraint, and the market has to decide whether that is credibility or austerity.

The restraint is not a choice so much as a constraint. Public debt has nearly doubled in six years from Rs 1.433tn (38% of GDP) in FY2019/20 to Rs 2.858tn, 46.81% of GDP, by mid-February 2026, per the Public Debt Management Office. A decade ago it sat near a quarter of GDP. Much of the recent jump is not even fresh borrowing: a depreciating rupee inflated the local-currency value of external debt, which is roughly 73% denominated in SDRs. The government now spends more servicing debt than it invests in many development heads.

That constraint has a direct NEPSE channel. With debt-financed development off the table, the government has signalled that flagship projects Nijgadh Airport, the Budhi Gandaki Hydropower Project should move to public-private partnership and FDI models. Given how heavily hydropower weighs on the exchange, the financing framework for these projects is not an abstraction; it is a question about future listed supply and the sector's earnings base. Watch whether the budget puts numbers and a mechanism behind the rhetoric, or leaves it at the level of intention.

V. The wall of idle money

Now the paradox that should shape how you read the whole budget. The banking system is not short of money, it is buried in it. Total deposits stand at Rs 7.95tn against Rs 5.87tn of lending, a credit-to-deposit ratio of roughly 74% against a 90% ceiling. Banks have ample room to lend and almost no one to lend to. NRB set a 12% credit-growth target for the year; on current trends it will miss badly.

The clearest measure of the glut is how much cash banks have simply handed back to the central bank because they cannot deploy it: more than Rs 861bn, parked through deposit auctions, the standing deposit facility, and NRB bonds.

The glut has crushed the cost of money. The weighted-average lending rate has fallen to 6.90%, the lowest on record since NRB began the series in 2012 after spiking to 13.03% during the 2023 liquidity crunch. Deposit rates have followed, with fixed-deposit ceilings dropping below 5% across the system in Baisakh. Loans are cheaper than they have ever been, and borrowers are still holding back. Economists have a name for it: a liquidity trap.

This is why the budget's market levers cut differently than they look. Cheap, abundant credit and a margin cap already removed mean the constraint on NEPSE is not the supply of money, it is the absence of anywhere else to put it. That same wall of idle cash is also why the market is sensitive to CGT and direct-bank-investment rules: with deposits paying under 5% and land illiquid, equities are one of the few places savings can chase a return. Whatever the budget does to the cost of holding shares lands on a captive audience.

VI. The primary markets didn’t wait

While the secondary market idled, the primary pipeline ran straight through the holiday calendar and fittingly for a market where hydropower dominates both turnover and listings, both anchor names were power companies.

Crest Micro Life Insurance, freshly listed, kept seasoning after a strong debut, and the Q3 reporting tail is still being swept up. None of it moved the index but supply does not pause for a budget, and the demand that meets this pipeline will be priced by whatever the budget does to CGT and bank participation. The primary market is, in effect, a leveraged bet on the same three fault-lines.