Nepal's Highest-Paying Bonds Can Earn Less Than a Fixed Deposit

Nepal's corporate debenture market is witnessing record demand, but headline double-digit coupons are masking a different reality.

Big money is stampeding into Nepal's corporate debentures for their double-digit coupons and paying premiums of up to 32%. Run the yields and the trade inverts: the loudest bonds pay less than a bank deposit and the highest-yielding bond on the board has the lowest coupon on it.

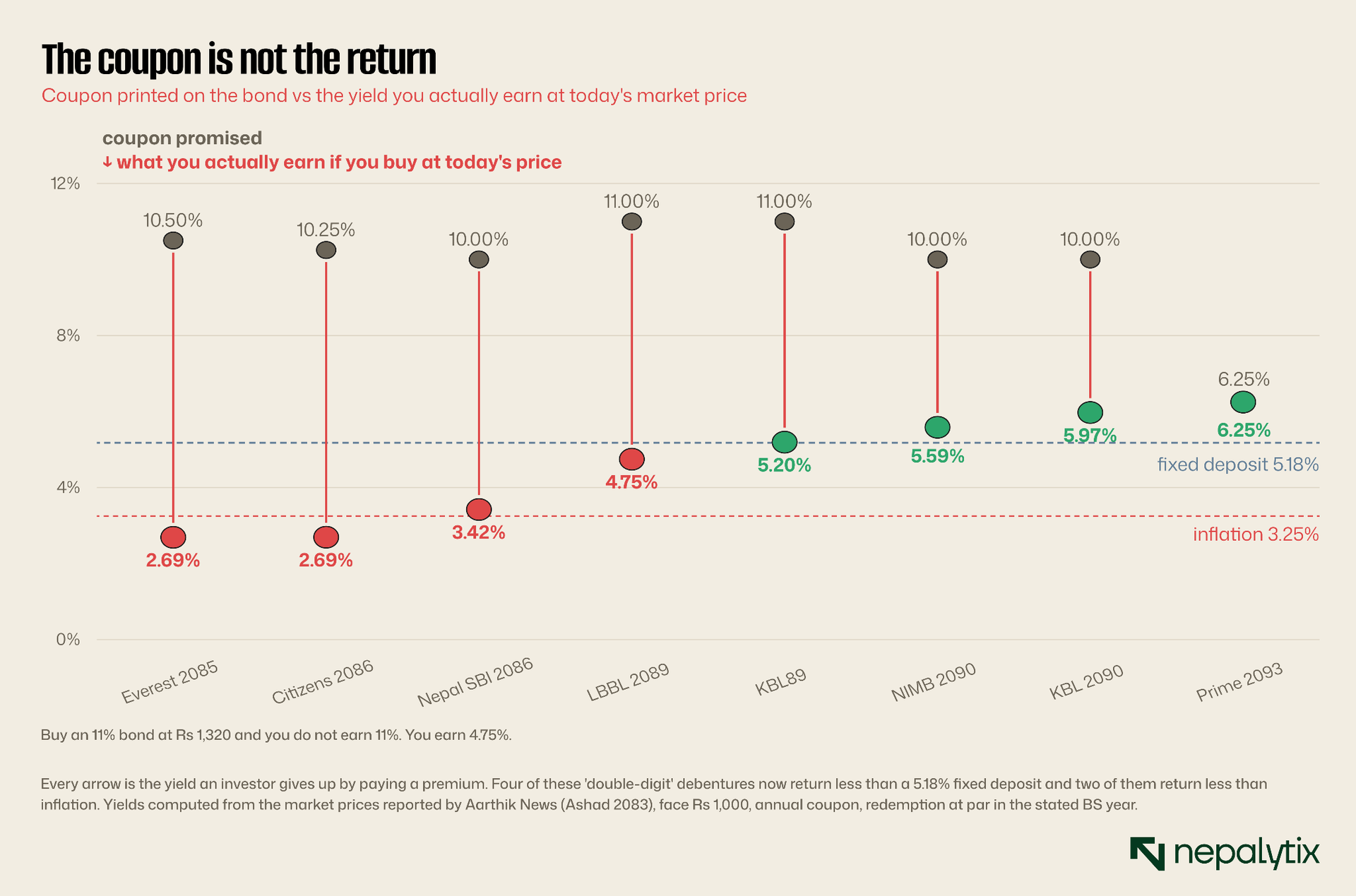

Start with the arithmetic everyone is skipping. A Nepali corporate debenture has a face value of Rs 1,000. The coupon 10%, 10.5%, 11% is paid on that Rs 1,000 not on whatever you paid for the bond. And at maturity, the issuer redeems it at Rs 1,000. Not at Rs 1,320. Not at whatever the last trade printed. At par.

So when an investor pays Rs 1,320 for an 11% debenture, two things happen at once. They buy a stream of Rs 110 annual coupons and they lock in a Rs 320 capital loss, payable at maturity, guaranteed with no market risk and no ambiguity about it. The only honest way to measure what they earn is yield-to-maturity: the single rate that reconciles the coupons they receive with the premium they will lose. Nobody in the coverage of this rally is computing it. So we did for every bond named.

The results are not marginal. They invert the entire story. The 10.50% Everest Bank debenture, at Rs 1,150.10, returns 2.69% to a buyer today. The 10.25% Citizens Bank debenture, at Rs 1,215, returns 2.69%. The 10% Nepal SBI debenture, at Rs 1,184.50, returns 3.42%. All three sit below the 5.18% a bank will pay on a fixed deposit, the very instrument these buyers believe they are escaping. Two of them sit below inflation, which means the investor is paying, in real terms, for the privilege of lending.

Four of the market's "double-digit" debentures now yield less than a term deposit. Two of them lose to inflation. The coupon was never returned.

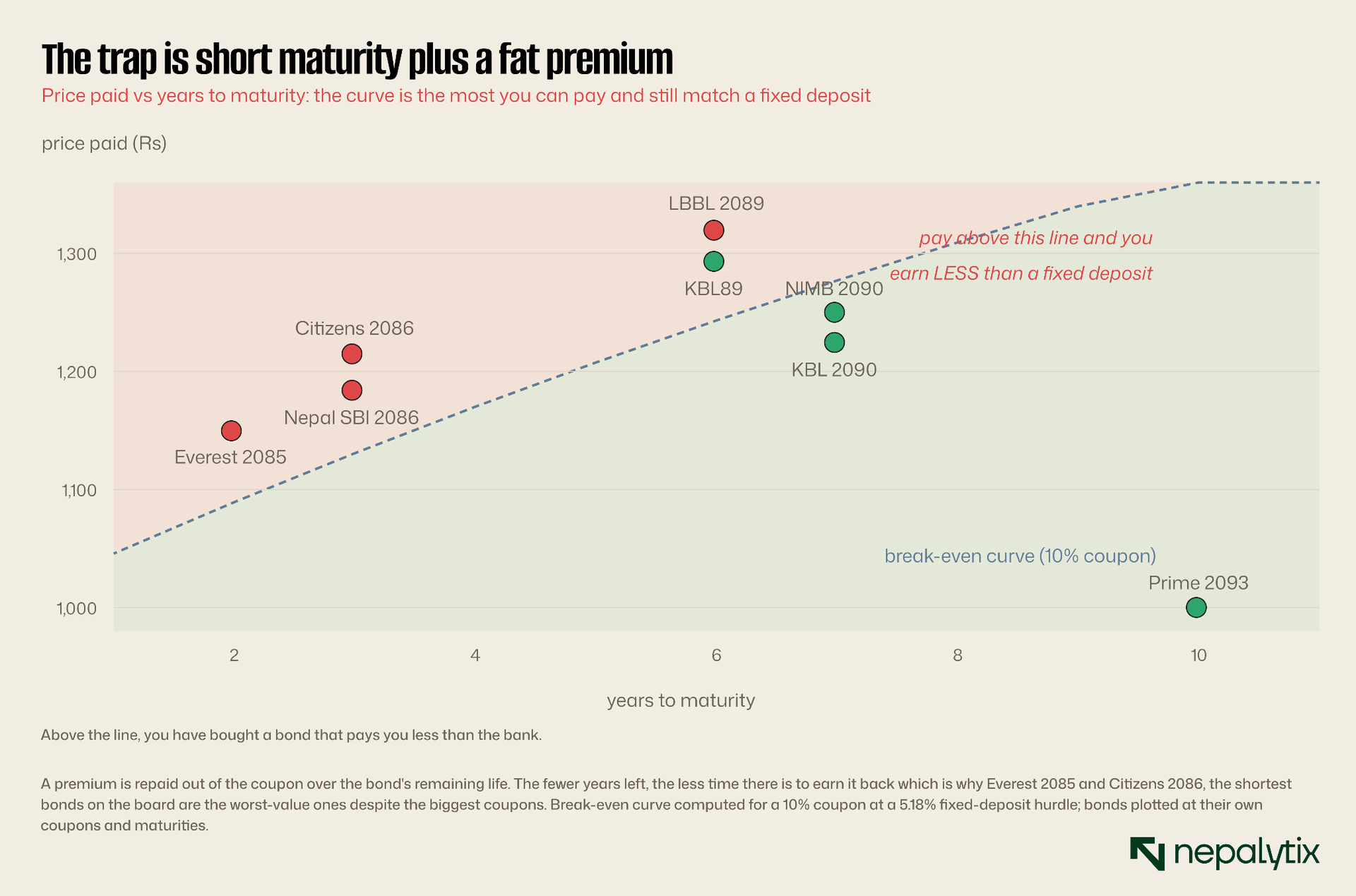

Why the shortest bonds are the worst trap

Look at which bonds are the worst value and a pattern jumps out: they are the ones closest to maturity. That is not a coincidence, it is the mechanism.

A premium is repaid out of the coupon spread across whatever life the bond has left. Pay Rs 320 over face on a bond with ten years to run and you have ten years of coupons to earn it back. Pay Rs 150 over face on a bond with two years to run and the loss lands almost immediately with barely any coupon income to offset it. Everest 2085 has roughly two years left. Citizens and Nepal SBI's 2086 bonds have about three. These are the shortest bonds on the board and precisely because of that, a modest-looking premium destroys their yield.

The chart draws the line explicitly. For a 10% coupon, a two-year bond stops beating a fixed deposit above about Rs 1,099, Everest trades at Rs 1,150. A three-year bond breaks even around Rs 1,131, Nepal SBI trades at Rs 1,184.50, and Citizens at Rs 1,215, nearly Rs 80 beyond its own ceiling. These are not fine judgment calls. They are bonds trading well past the point where the arithmetic works.

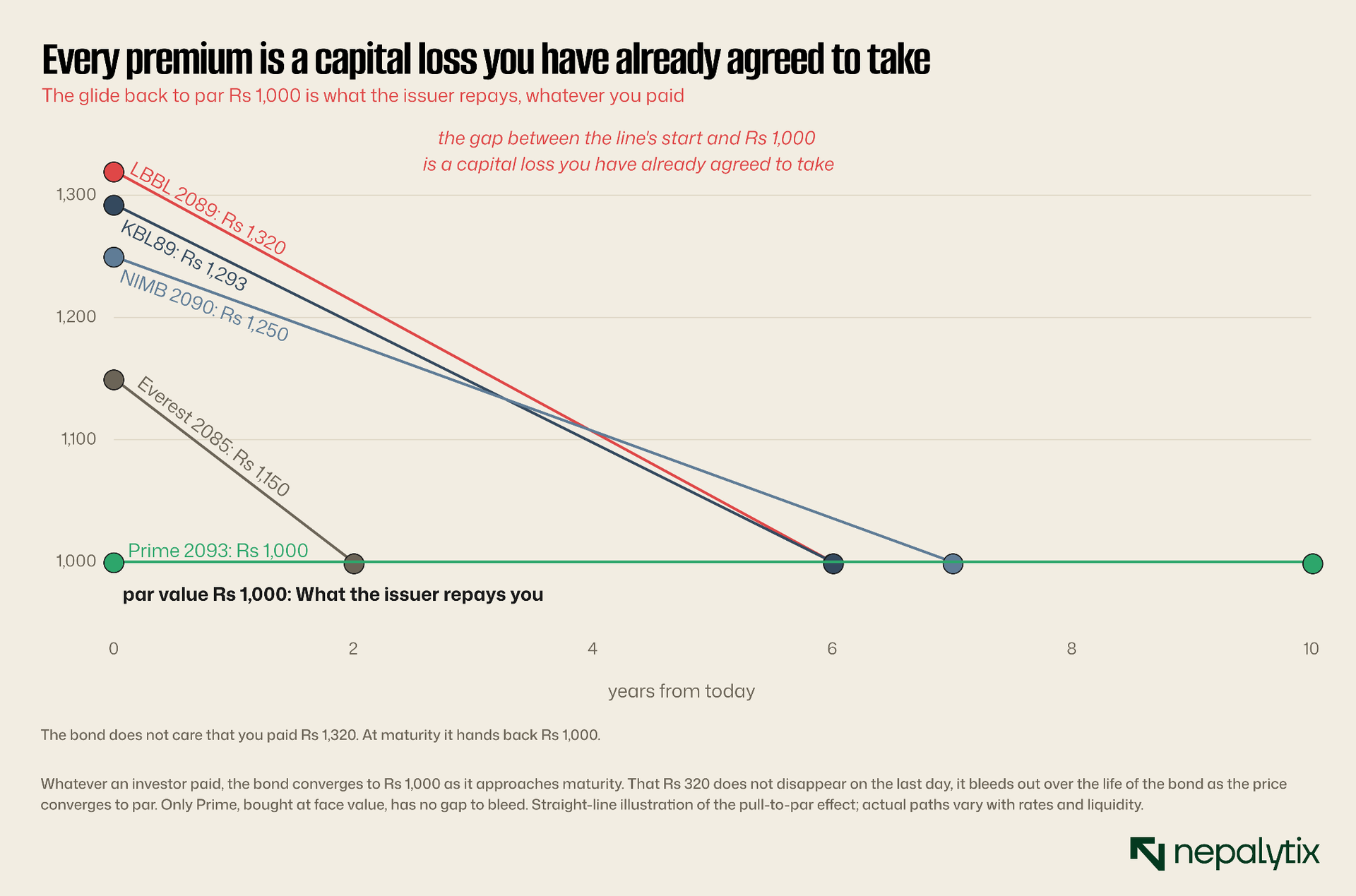

The capital loss you have already agreed to take

There is a comforting story an investor can tell here: the premium doesn't matter, I'll just sell before maturity at a similar premium. It is worth being blunt about why that reasoning is circular. It requires a buyer, later, to make the same mistake and to make it with less time left on the bond which is exactly when the premium is hardest to justify. As the maturity date approaches, the price is dragged toward Rs 1,000 with mathematical certainty. This is called pull-to-par and it is not a market opinion. It is the redemption terms.

The premium is not a risk. It is a certainty with a date attached. And that reframes what this market is doing: buyers are not being paid extra for taking on risk. They are pre-paying for a coupon stream, at a price that hands most of the coupon straight back.

The bond everyone mocked is the best one on the board

Which brings us to the most useful thing in this entire market, and the detail the coverage treats as an afterthought. Prime Bank's recently-issued debenture carries a coupon of just 6.25%, a number that looks feeble beside the 11% names, and which the reporting frames as tolerable "despite its lower coupon rate."

Prime's 6.25% bond is the highest-yielding debenture on the board.

It yields exactly 6.25% because it trades at face value.

There is no premium to claw back, no capital loss to absorb. It beats every premium-priced double-digit bond in this analysis: KBL 2090 at 5.97%, NIMB at 5.59%, KBL89 at 5.20%, LBBL at 4.75% and the three short bonds trailing below 3.5%. The lowest coupon on the board bought at the right price is the best investment on the board.

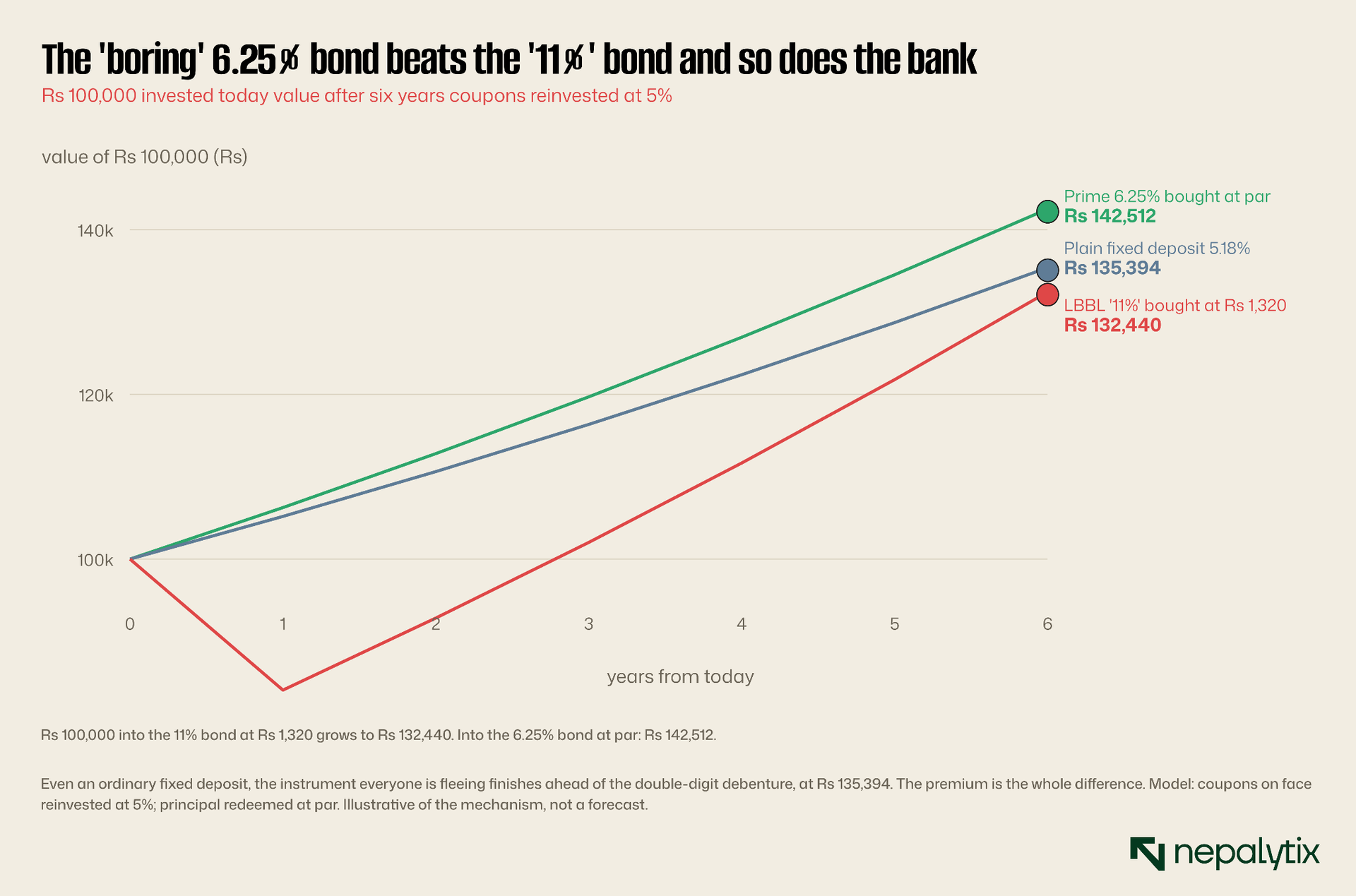

Put money behind it and the gap is stark. Rs 100,000 into the 11% LBBL debenture at Rs 1,320 coupons reinvested grows to about Rs 132,440 over six years. The same Rs 100,000 into Prime's 6.25% bond at par grows to about Rs 142,512 more than Rs 10,000 ahead and the fixed deposit these investors are fleeing? Rs 135,394. The double-digit bond finishes behind the bank.

What survives after inflation

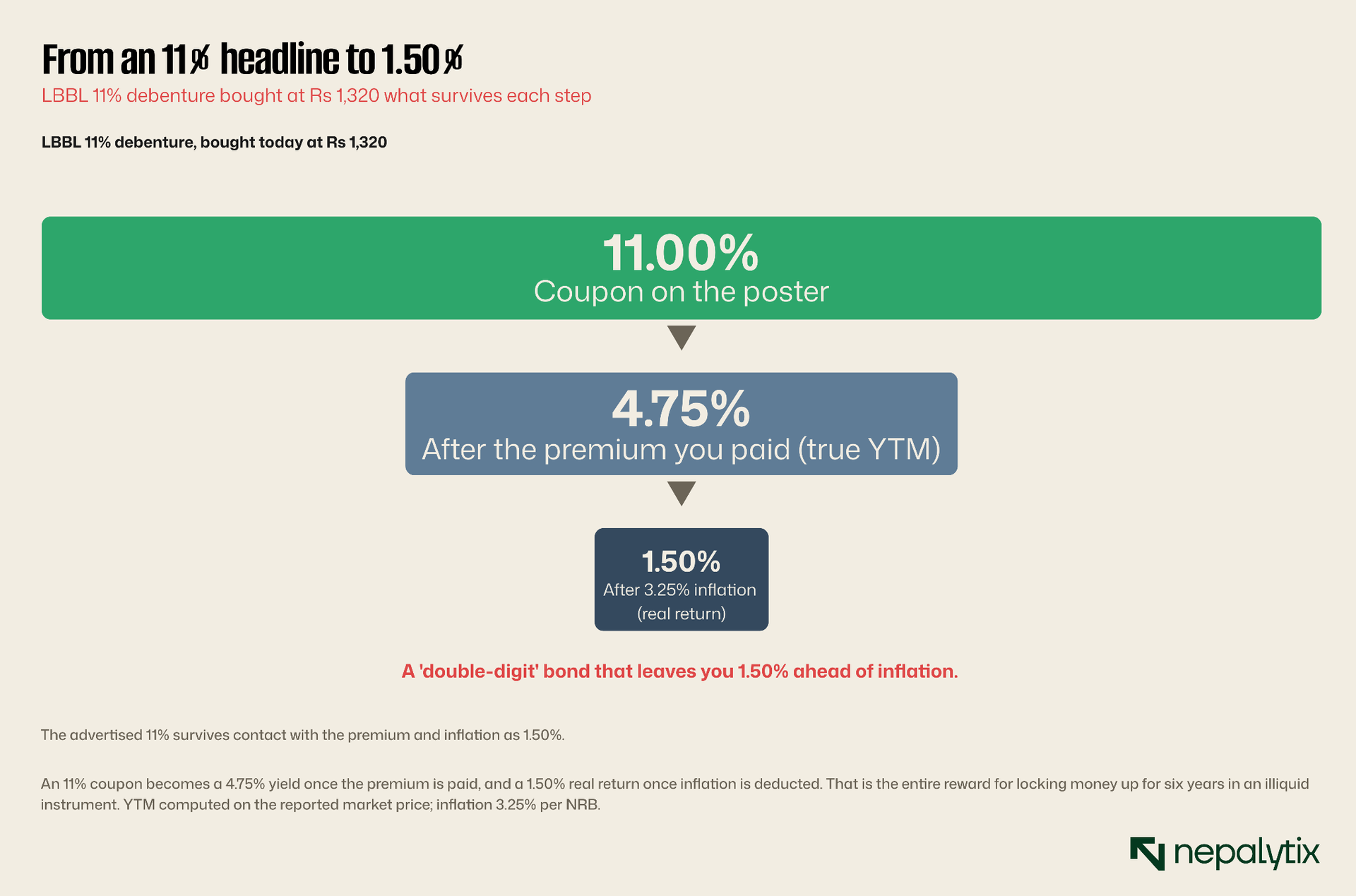

One more subtraction, and it is the one that matters to a saver. Inflation is running at 3.25%. Take the LBBL bond, the biggest premium and the loudest coupon and follow the number down.

Eleven percent on the poster. Four point seven five percent once the price is accounted for. One point five percent after inflation. That is the real compensation for tying up capital for six years in an instrument that trades thinly and cannot easily be exited. For the short bonds, the number after inflation is negative, the investor is guaranteed to end up with less purchasing power than they started with having done everything the market told them was clever.

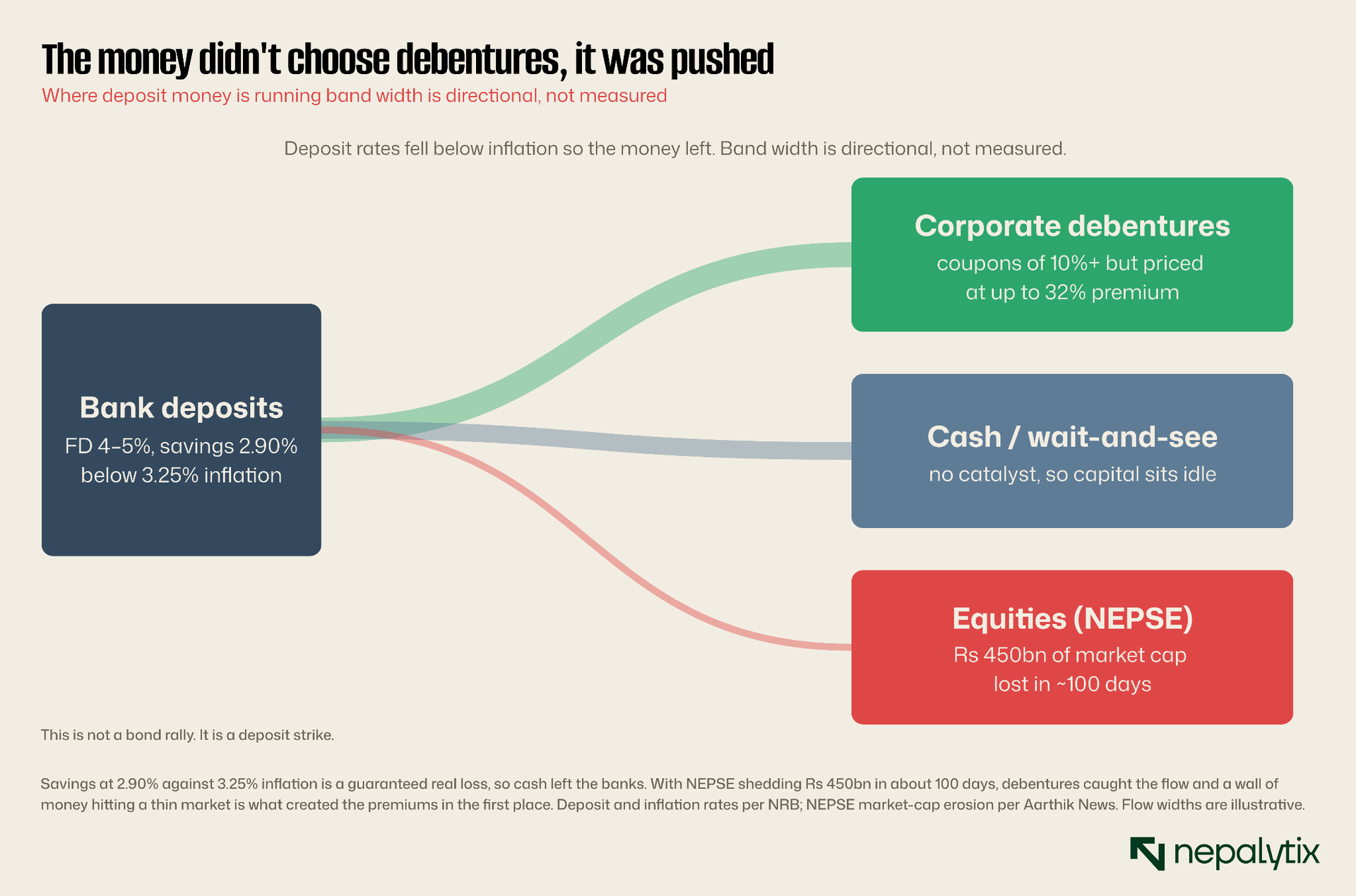

This is a deposit strike not a bond rally

Step back and ask why any of this is happening because the cause explains the mispricing. Nepali banks are sitting on a liquidity glut: the credit-to-deposit ratio is around 74% against a 90% cap, the interbank rate has fallen to 2.75%, and savings deposits pay 2.90% against 3.25% inflation. A saver who leaves money in the bank is guaranteed to lose purchasing power. So the money left.

But it left into a market that could not absorb it. Nepal's listed debenture market is small and thin 34 bonds with coupons above 10% in a country where NEPSE has just shed Rs 450 billion of market cap in about a hundred days and equity investors have gone to the sidelines. A wall of institutional and high-net-worth money hitting a thin market does not discover a price. It overruns one. The premiums are not a judgment about credit quality or a considered view on the rate cycle. They are the footprint of too much money chasing too few instruments.

A wall of money hitting a thin market does not discover a price. It overruns one.

What to actually do with this

The discipline here is unglamorous and completely mechanical. Before buying any listed debenture, compute the yield-to-maturity at the price you would actually pay, and compare it to the fixed deposit you are rejecting. Not the coupon. The yield. If a bond does not clear roughly 5.2% on that basis, it is worse than a term deposit at a bank with worse liquidity, and with credit risk a deposit does not carry.

On today's prices, that test rules out the loudest names in the market and points at the quietest. Prime's 6.25% at par clears it comfortably. KBL 2090 at Rs 1,225 and NIMB 2090 at Rs 1,250 clear it modestly, helped by long maturities that give the premium time to amortise. LBBL at Rs 1,320, KBL89 at Rs 1,292.80, and all three short bonds fail it. And the general rule follows from the same arithmetic: in a premium market, favour long maturities and small premiums, and treat a short-dated bond trading far above par as what it is, a fixed deposit with extra steps, minus the return.

The bitter irony is that investors did the right thing for the right reason. Deposit rates below inflation genuinely are a signal to move. They simply moved into an instrument they priced by its headline instead of its yield and in doing so recreated the exact outcome they were running from a sub-inflation return with less liquidity and more credit risk attached. The escape route and the trap turned out to be the same door. This is analysis, not investment advice; run the numbers on your own purchase price before you act.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.