Nepal's Largest Hydropower Company Isn't Printing Money

Upper Tamakoshi is Nepal's largest hydropower project and one of the country's most widely held stocks.

Upper Tamakoshi is the largest and proudest hydropower project in Nepal, supplies about a sixth of the country's electricity and runs at a 97% gross margin. It also loses money every year, has wiped out half its shareholders capital and trades at more than four times a shrinking book. This is an initiation on the most important, and most misunderstood, share on the exchange: what the flagship is really worth once you read past the megawatts.

The operating asset is excellent and effectively irreplaceable but the equity is a leveraged, decades-long bet on deleveraging into a tariff that is permanently capped below today's rates. At about Rs 206, more than four times a book value depressed by accumulated losses, the price already embeds much of the recovery. We see a quality asset at a demanding price with risk-reward that rewards patience and a lower entry over chasing the story.

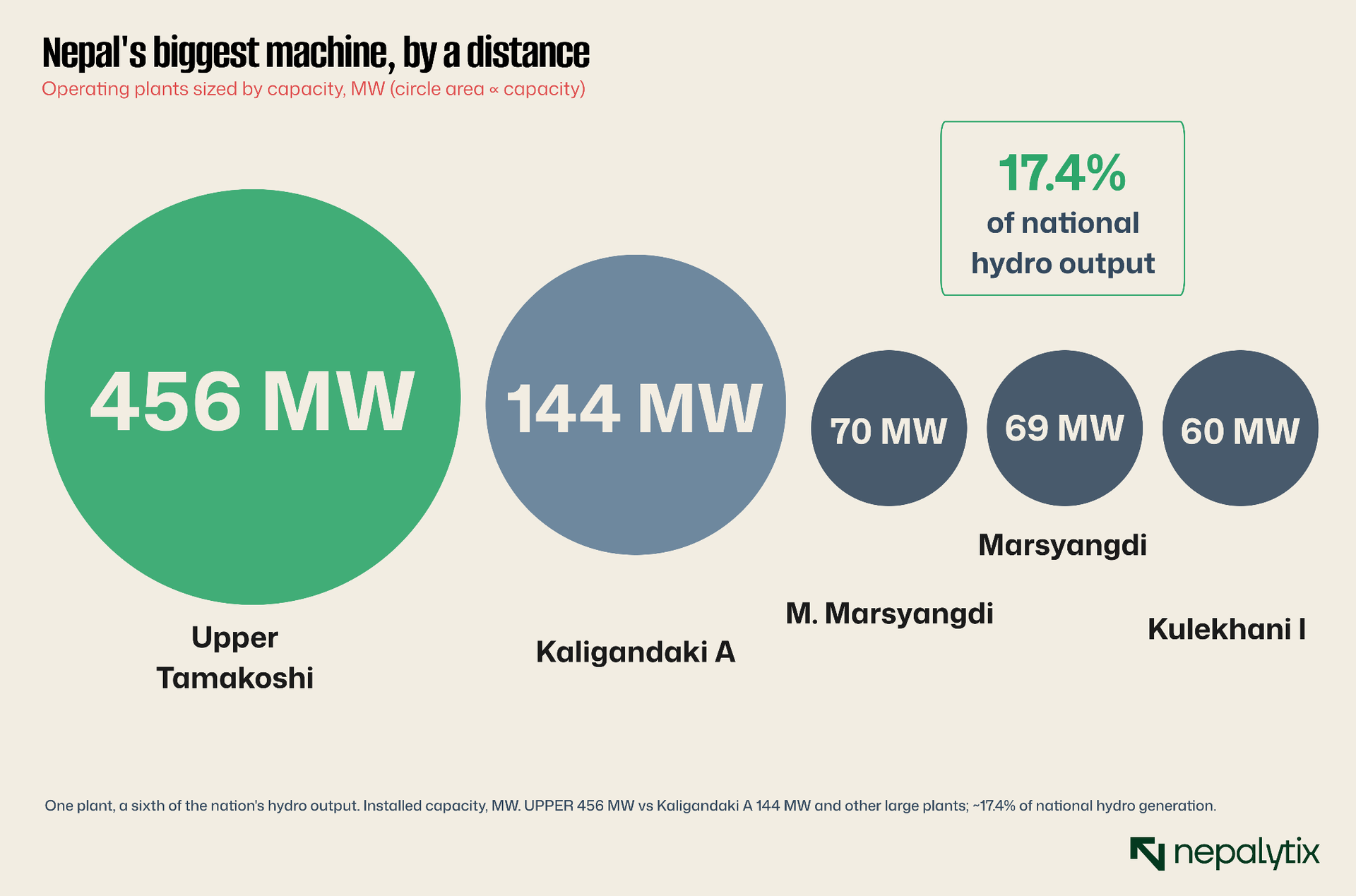

Begin with what is genuinely impressive because it is the reason this share exists and the reason so many Nepalis own it. The Upper Tamakoshi Hydroelectric Project, in Dolakha district near the Tibetan border is the largest power plant in Nepal by a wide margin. Its 456 megawatts are more than three times the capacity of the next-biggest operating plant, the Nepal Electricity Authority's own Kaligandaki A and the project alone accounts for roughly seventeen percent of the country's hydroelectric output. It was conceived as a national-priority undertaking developed by a company the NEA established in 2007 and financed substantially with the savings of ordinary Nepalis and their pension funds. When it was finally commissioned in 2021, it was treated as a milestone in the country's long climb out of load-shedding.

The plant itself is a fine piece of engineering and in operating terms, a fine business. Hydropower has no fuel cost and few moving parts, so once a plant is running its gross margins are extraordinary; Upper Tamakoshi converts about ninety-seven percent of its revenue into gross profit. It sells almost all of its electricity to the NEA under a take-or-pay agreement which in principle guarantees payment for contracted energy regardless of how much the grid actually absorbs. On the face of it, this is exactly the kind of asset an investor should want: a strategic, irreplaceable, high-margin monopoly supplier with a guaranteed buyer.

And yet it loses money. That is the paradox this initiation exists to explain. Everything that makes Upper Tamakoshi a national triumph sits above the operating line and everything that makes it a troubled investment sits below it. To understand the share, you have to follow the rupee all the way down the income statement past the gross margin that everyone quotes, to the net line that almost no one does.

The contrast with the rest of the sector is instructive. Most listed hydropower companies are small run-of-river plants of a few tens of megawatts financed in the same era on the same template. Upper Tamakoshi is that template at maximum scale, the same economics, the same debt-heavy structure and the same frozen tariffs magnified roughly tenfold. That makes it both the single most important hydropower share to understand and the most concentrated expression of everything that can go wrong and right in the sector. An investor who can read Upper Tamakoshi can read almost any plant on the exchange.

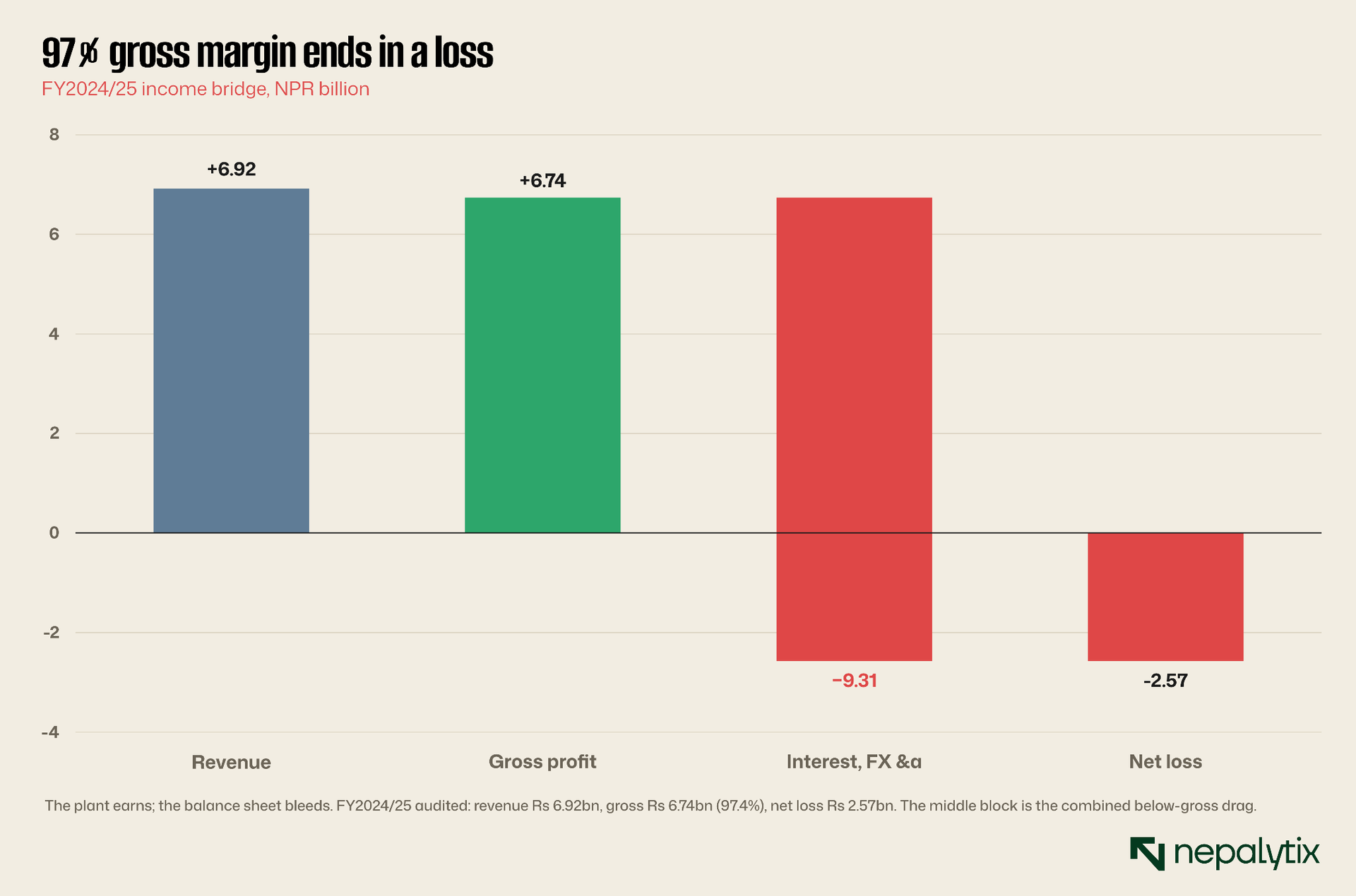

The paradox: a 97% margin that loses money The single most important chart in this report is the bridge from revenue to net result. In the audited 2024/25 financial year, Upper Tamakoshi booked revenue of Rs 6.92bn and gross profit of Rs 6.74bn that headline ninety-seven percent margin. By the time the income statement reached the bottom, that Rs 6.74bn of gross profit had become a net loss of Rs 2.57bn. The gap, more than Rs 9bn, is the combined weight of three forces below the operating line: interest on the project's enormous debt, foreign-exchange losses, and depreciation of a costly asset base.

This is not a one-off. The company has reported negative returns on equity and assets essentially since the plant began operating. The losses are structural, not operational which is precisely what makes them so often misunderstood. A casual reader sees a plant running well, generating power, earning a near-perfect gross margin and concludes the business must be healthy. The financial reality is the opposite: the operating business is excellent and the capital structure attached to it is broken. For an equity investor, the capital structure is what you own.

The rest of this initiation is, in effect, an examination of the three forces in that bridge, the debt, the tariff and the cost of building the thing followed by what they mean for the balance sheet, the share price and ultimately, the value of the equity.

It is worth pausing on why this pattern is so common in Nepali hydropower specifically. These are capital-intensive assets built almost entirely with debt sold at administered prices in a currency that tends to weaken against the dollars in which much equipment is bought. The result is an industry in which a plant can be operationally flawless and financially loss-making for years, and in which the gross margin, the number that dominates promotional material and retail conversation, is close to meaningless as a guide to whether shareholders make money. Upper Tamakoshi is the textbook illustration but the lesson generalises across the sector.

The debt that outruns the plant

The largest of the three forces is debt. Upper Tamakoshi was built like most Nepali hydropower on roughly seventy percent borrowed money but on a project whose cost ballooned far beyond its original budget that gearing translated into an extraordinary absolute debt load, on the order of forty billion rupees with interest running into the billions every year.

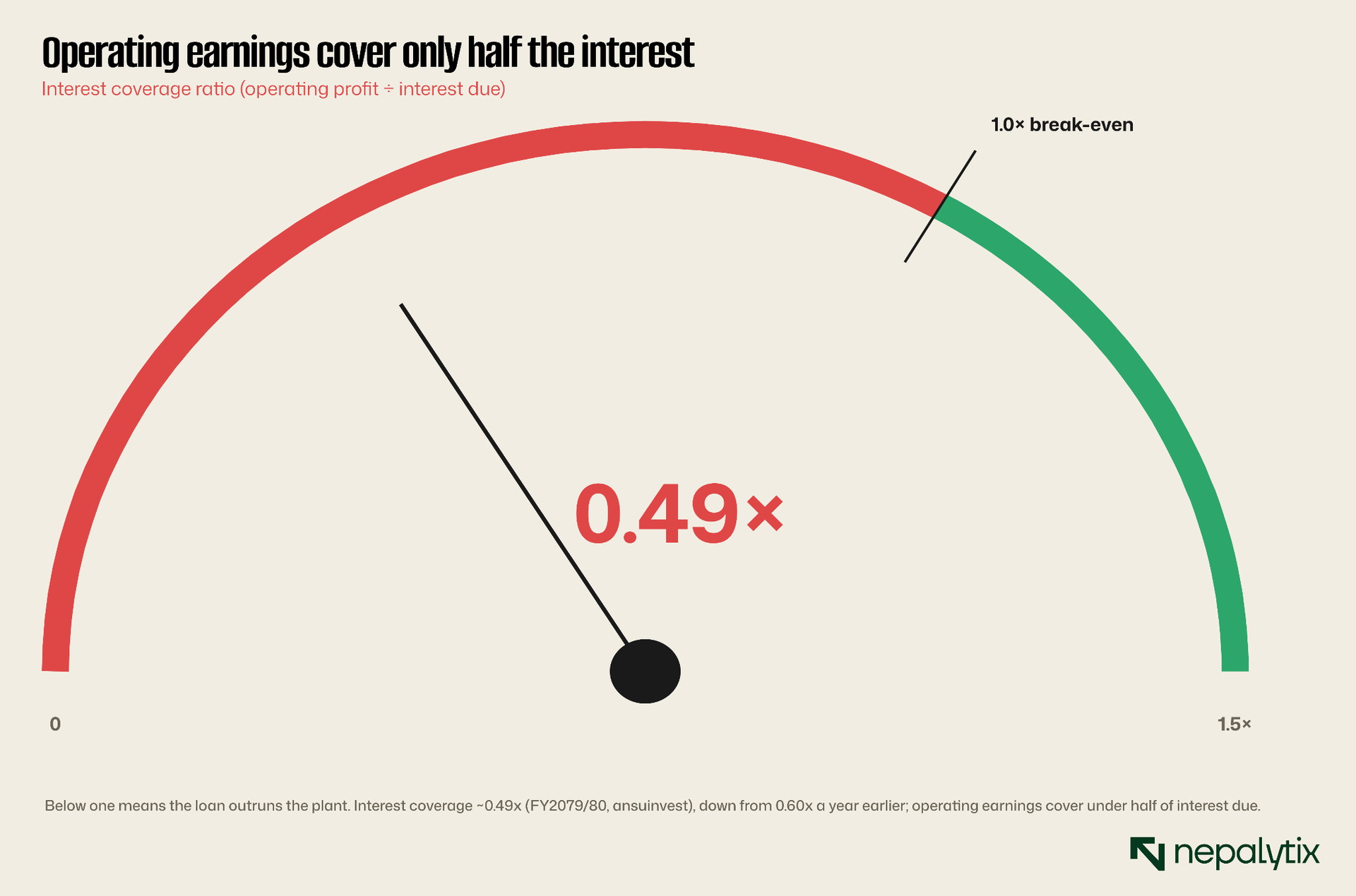

The cleanest way to see the problem is the interest-coverage ratio, which measures how comfortably a company's operating earnings cover its interest bill. A healthy company earns several times its interest. Upper Tamakoshi's ratio has been below one around 0.49 in 2079/80 and falling from 0.60 the year before. A ratio under one has a stark meaning: the business does not generate enough profit before financing to pay the interest on its loans let alone repay any principal. The plant earns about forty-nine paisa of operating profit for every rupee of interest it owes. The remaining gap is borrowed, capitalised or simply lost and it is the core engine of the net loss.

This also explains why the company's own analysts and management concede that even after repaying billions of rupees of principal, interest expense will still run into the billions for years. The debt is not a temporary financing wrinkle to be refinanced away. It is the central fact of the equity story and the single variable that matters most to whether this investment ever works is the pace at which that debt, and the interest it carries comes down.

There is a glimmer of help from the macro backdrop. Nepal's banking system is awash with deposits and interest rates have fallen to unusually low levels which lowers the cost of any refinancing the company undertakes and eases, at the margin, the burden on floating-rate debt. That is a real tailwind but a modest one against a debt load of this size, and it can reverse. The investor should treat cheap money as a helpful accelerant to deleveraging not a substitute for it. The principal still has to be repaid and only generation revenue, capped by the tariff, can ultimately do that.

The tariff frozen in time

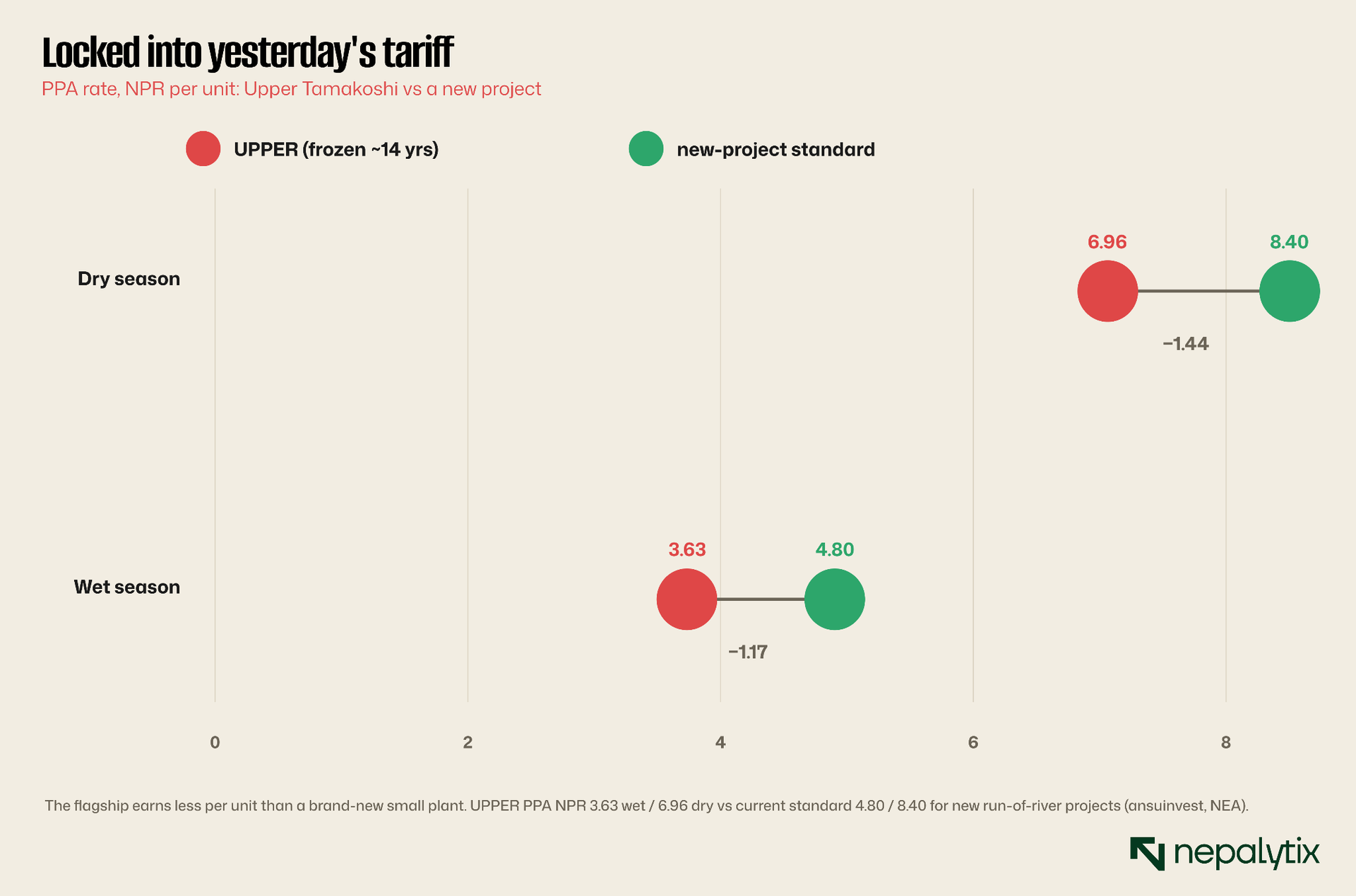

If debt is the largest force, the frozen tariff is the most insidious because it caps the revenue that has to service everything else. Upper Tamakoshi's power purchase agreement was signed nearly fourteen years ago when the project was conceived, at rates of about Rs 3.63 per unit in the wet season and Rs 6.96 in the dry season. Those rates have never been reset. A run-of-river plant signing a new agreement today would receive about Rs 4.80 and Rs 8.40 respectively.

The consequence is brutal and permanent: the country's flagship, its largest and most strategically important plant earns roughly a quarter less per unit of electricity than a brand-new small project commissioned this year. The tariff is fixed for the life of the contract so there is no mechanism by which this gap closes; if anything inflation widens it in real terms with every passing year. A great deal of the optimism around Upper Tamakoshi implicitly assumes the revenue line can grow. Contractually, it largely cannot. The plant can generate more units in a good water year but the price of each unit is locked in yesterday's terms.

This is the cruel irony of having built early and large. The projects financed and contracted in the sector's earlier, lower-tariff era are precisely the ones that carry the most debt because they were the most expensive to build and the least revenue per unit with which to service it. Upper Tamakoshi is the extreme case of both.

The standard agreement does carry a modest annual escalation but only for a limited number of years before the rate is frozen for the remaining decades so even that does little to close the gap against newer contracts over the life of the deal. The deeper point for valuation is that the revenue line of a Nepali hydropower company is not a growth line; it is a slowly eroding annuity set by a contract signed long ago. Any model that projects Upper Tamakoshi's revenue compounding upward is mis-specified from the first cell. The units can rise with better water and the Rolwaling diversion; the price per unit cannot.

One technical nuance is worth flagging for the sophisticated reader. A handful of large projects in Nepal have been signed on partly dollar-denominated tariffs which shield the developer against rupee depreciation. Upper Tamakoshi is not among them; its tariff is in rupees while a portion of its costs and debt carried foreign-currency exposure during construction. That asymmetry, rupee revenue against partly hard-currency costs is one more reason the project's economics proved so much worse than its planners assumed, and one more structural feature an investor cannot fix.

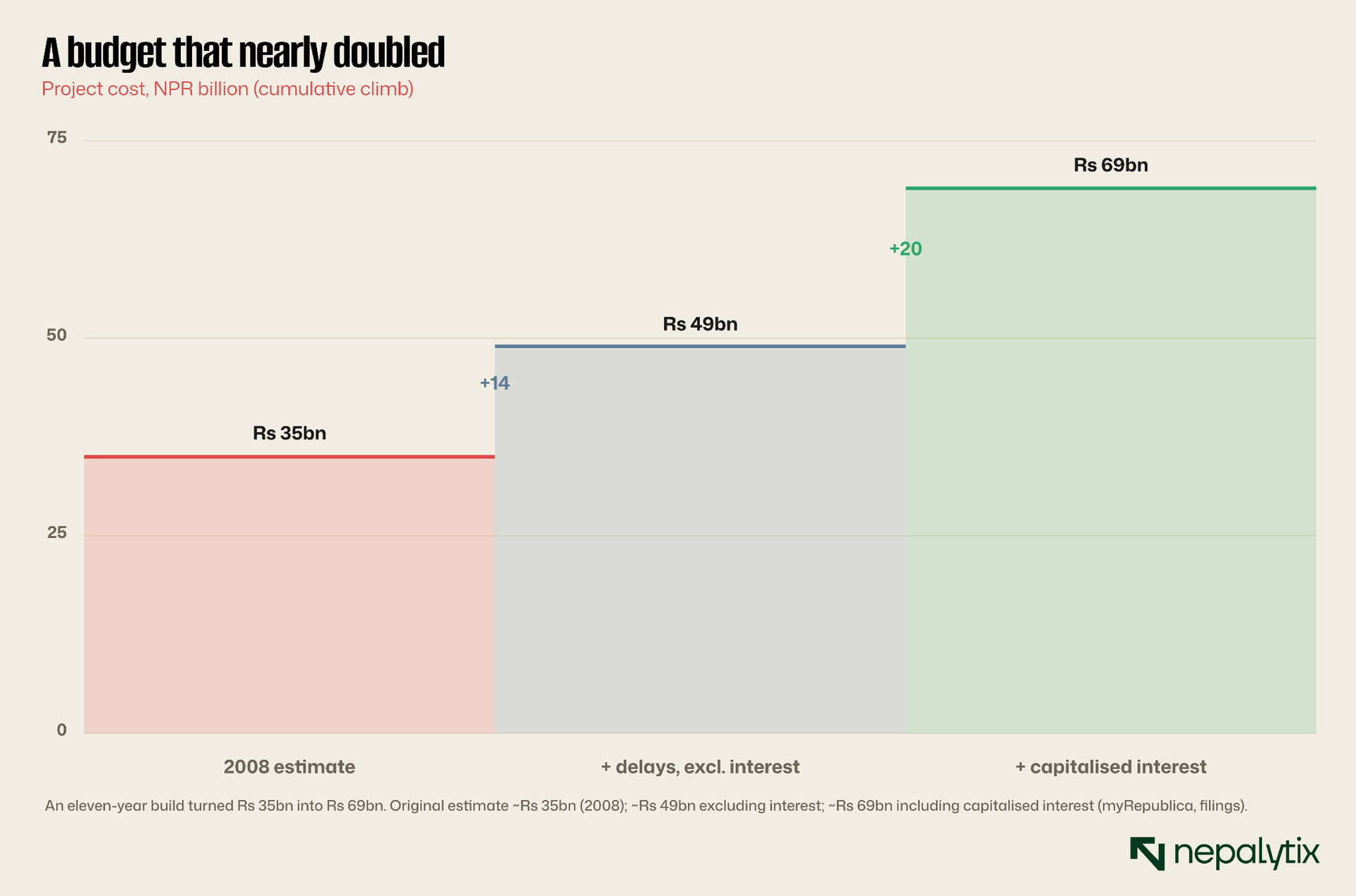

The cost of building it

The debt is large because the project was expensive and the project was expensive because it took eleven years to build. The cost estimate approved in 2008 was about Rs 35bn. By completion, the figure was roughly Rs 49bn excluding interest and around Rs 69bn including the interest that accrued during construction. The budget did not so much overrun as nearly double.

The causes were partly beyond management's control and partly the nature of building large infrastructure in Nepal. The 2015 earthquake struck the project hard; the subsequent Terai unrest and India-Nepal border blockade choked the supply of equipment and fuel; and the COVID-19 pandemic added further delay. A single year's slippage in 2018/19 is estimated to have added around Rs 20bn to the cost on its own. Layered on top were foreign-exchange losses, as a project with currency exposure faced a rupee that weakened over the long build. Every one of these added to the debt that now sits on the income statement.

Two further consequences deserve emphasis. First, the delays did not just raise the cost; they shortened the earning life. The operating window implied by the licence fell to roughly twenty-five years with the licence expiring around 2055, so the company has fewer years over which to recover a much larger cost. Second, the fragility did not end at commissioning: in October 2024 a landslide at the dam site halted generation entirely for eighty-eight days cutting revenue and prompting an insurance claim that, at last report, had not been paid. The asset is magnificent but the terrain it sits in is unforgiving, and the financial model has little slack to absorb shocks.

Depreciation deserves a mention of its own because it is the quietest of the three forces in the bridge and the most permanent. A Rs 69bn asset written down over a compressed operating life carries a heavy annual non-cash charge that suppresses reported profit for years even as cash flow improves. This is why the company's cash position can strengthen well before its reported earnings turn positive and why a patient investor should watch operating cash flow and the debt balance at least as closely as the headline profit line. The accounting loss and the cash reality can diverge for a long time in an asset like this.

Revenue at the mercy of the river

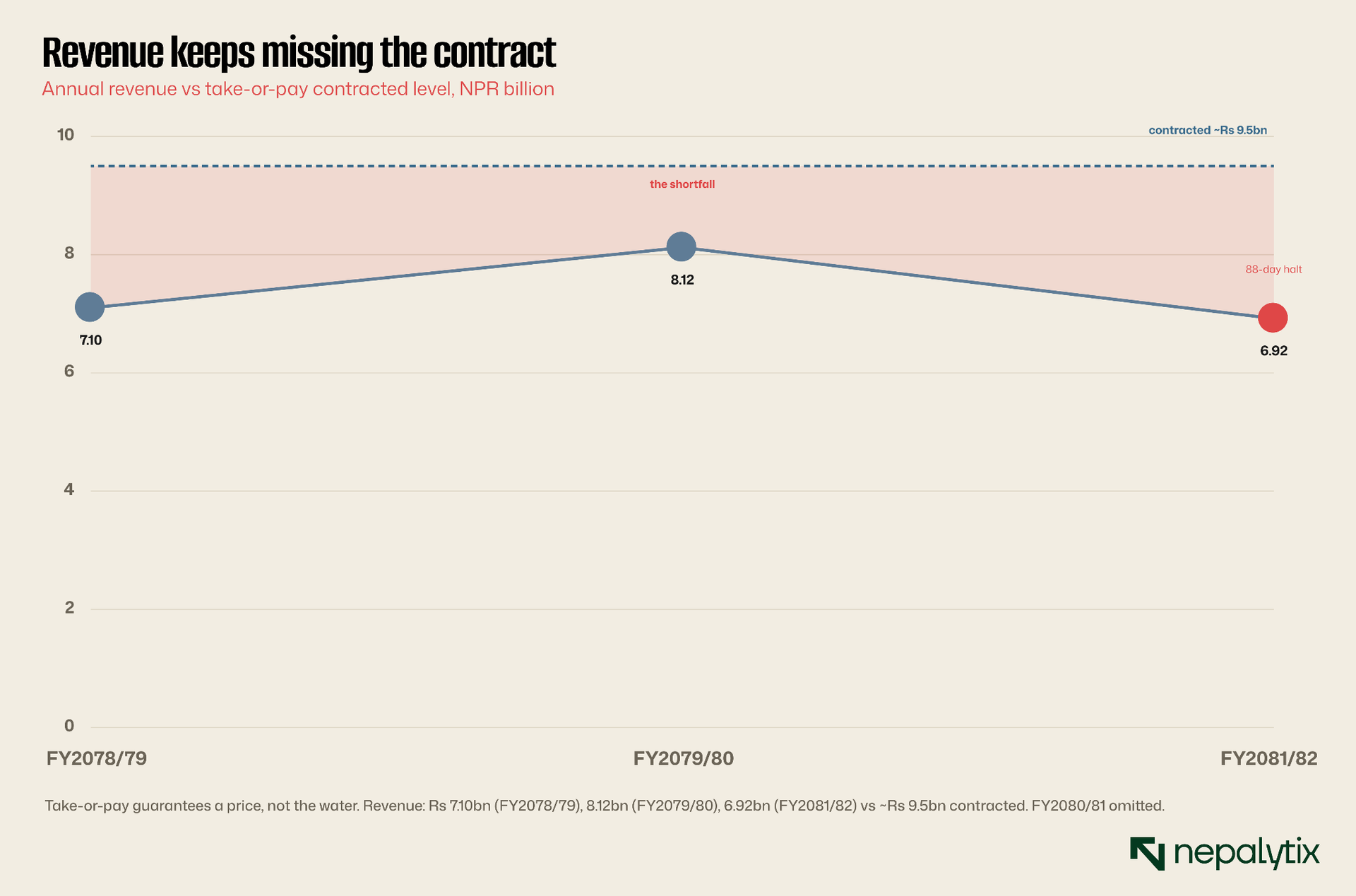

Take-or-pay is often described as a guarantee of revenue. It is more accurate to call it a guarantee of price. The NEA commits to pay for the energy the plant is contracted to deliver, but the plant still has to generate that energy and generation depends on the river. Upper Tamakoshi's contracted revenue is around Rs 9.5bn a year but actual revenue has run well below it: about Rs 7.1bn in 2078/79, Rs 8.12bn in 2079/80 and Rs 6.92bn in 2081/82, the last depressed by the landslide halt.

The plant operates at a contract plant load factor of about fifty-seven percent which is to say it converts a little over half of its nameplate capacity into actual energy across the year concentrated heavily in the monsoon. In the dry winter months when the river runs low, output falls sharply, exactly when under the tariff structure, each unit is worth most. This is the seasonality that defines every run-of-river plant in Nepal, and Upper Tamakoshi is not exempt from it despite its scale.

It is partly to address this that the company is building the small Rolwaling Khola project and more importantly, a diversion that will channel water from the Rolwaling River into the Upper Tamakoshi intake. Management expects this to add around 212 gigawatt-hours of dry-season generation and about Rs 1.4bn of revenue by 2084/85. That is a genuine and sensible improvement, because dry-season power is the valuable kind, but it is years away and modest against the scale of the debt.

The seasonality also frames the single most important risk to the sector's economics: the shift the government began in 2025 from take-or-pay toward take-and-pay for new contracts. Upper Tamakoshi's existing agreement is grandfathered and remains take-or-pay which protects its contracted price. But the direction of policy is a warning to the whole sector and a reminder that even the offtake guarantee underpinning the model is not immutable. For now it holds for Upper Tamakoshi; the investor should simply note that the one genuine protection in the structure is a contractual promise from a financially strained counterparty.

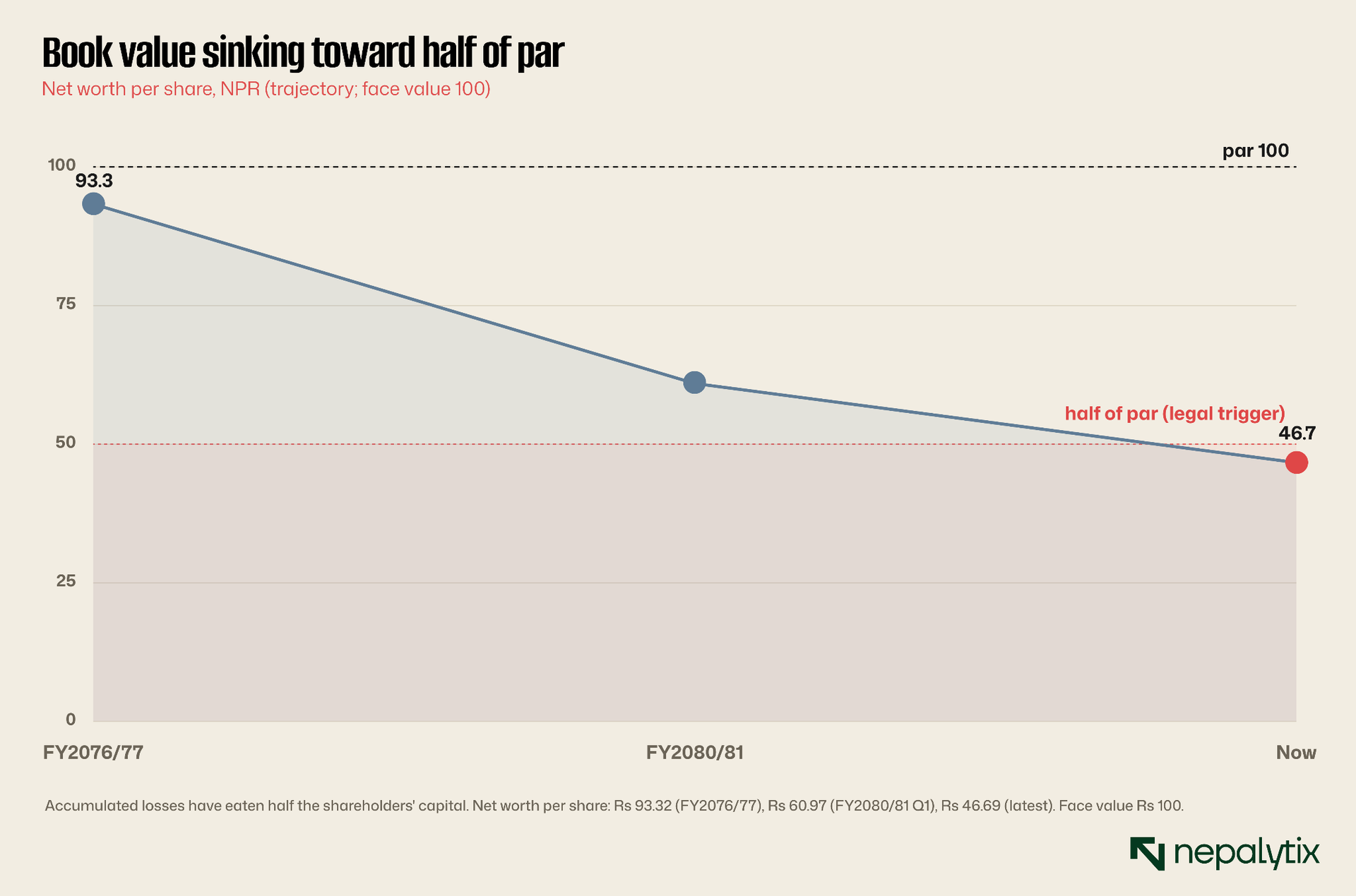

A balance sheet eaten by losses

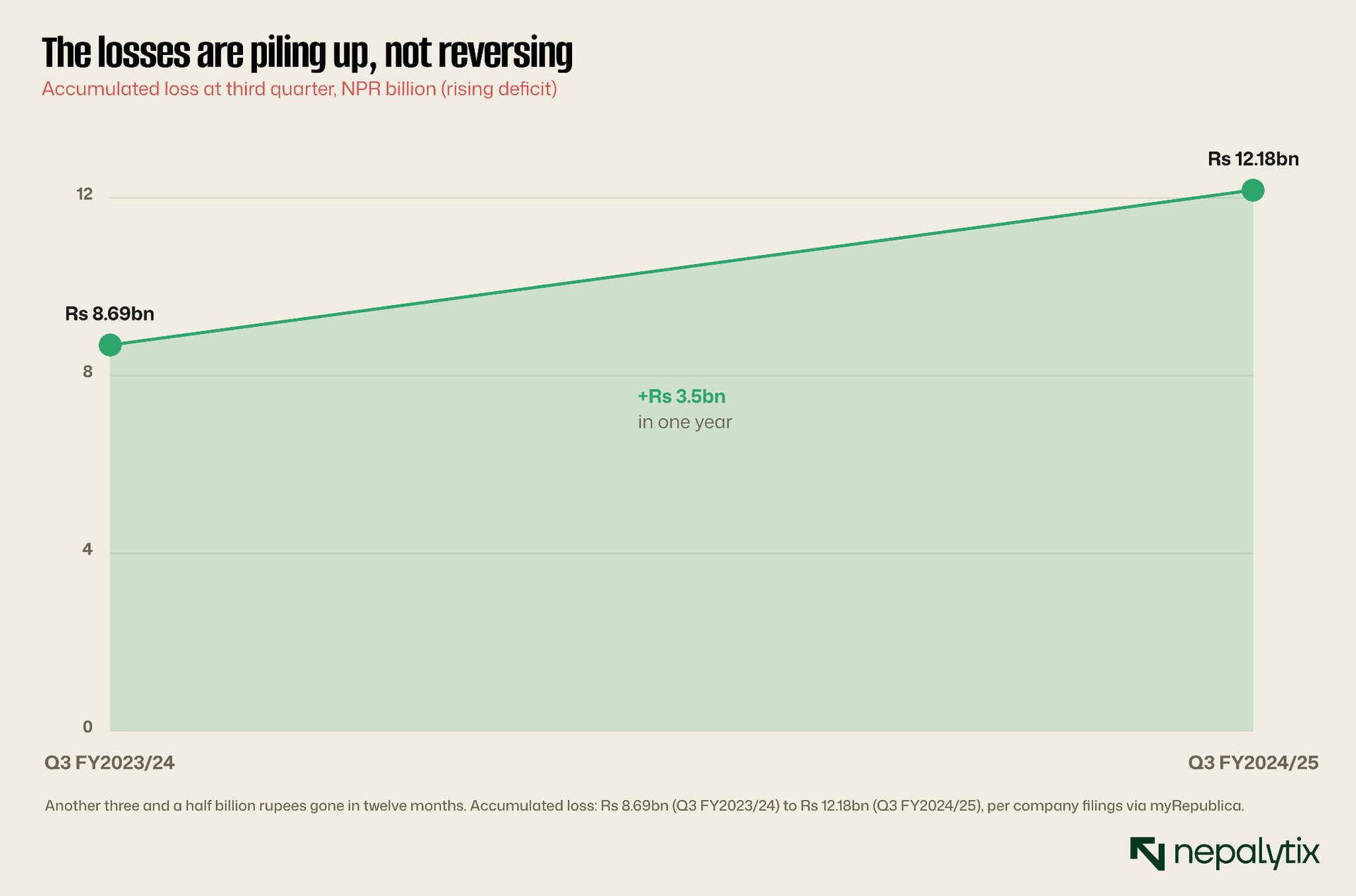

Years of losses do not just dent the income statement; they consume the balance sheet. Upper Tamakoshi's net worth per share has fallen from above its Rs 100 face value during construction to about Rs 60.97 by 2080/81 and roughly Rs 46.69 today. In other words, accumulated losses have eaten away more than half of the capital shareholders put in. The accumulated deficit reached about Rs 12.18bn by the third quarter of 2024/25 up from Rs 8.69bn a year earlier, a further Rs 3.5bn of losses booked in a single year.

This is not merely an accounting embarrassment. Nepal's Companies Act requires a board to formulate a remedial plan once net worth falls to half or less of paid-up capital and Upper Tamakoshi has been trending at or below that threshold. The company's response was a 100% rights issue: in 2023 it offered one new share for every share held at the Rs 100 face value roughly doubling the share count from about 105.9m to 211.8m and raising on the order of Rs 10bn. Around Rs 7bn of that was earmarked to reduce debt with the balance toward the Rolwaling works.

An investor should read that rights issue clearly for what it was: a defensive recapitalisation to relieve an unsustainable interest burden, not an offensive raise to fund growth. It diluted existing holders and it helped, but it did not solve the problem. The debt remains large, the tariff remains frozen and the losses, while they should narrow as the rights proceeds are applied, did not stop. The balance sheet bought time, not a cure.

The dilution is worth quantifying because retail holders often miss it. Doubling the share count means the eventual post-debt profit whenever it arrives is spread across twice as many shares so the recovery per share is half what the same recovery would have delivered before the issue. The rights issue was the right decision for the company's survival and the wrong kind of event for an existing shareholder's returns, both at once. A modest share premium of about Rs 914m sits alongside the paid-up capital but it does little to offset the accumulated deficit. The capital structure is healthier than it was; it is still a long way from healthy.

A small but telling detail from that rights issue: of the new shares offered, more than seventeen million went unclaimed and had to be auctioned off separately. In a market where retail investors queue in their millions for almost any new issue, a flagship name failing to place all of its rights shares is a quiet signal of how far sentiment had turned and of how many existing holders were unwilling or unable to put more money into a loss-making company. The enthusiasm that priced the stock at Rs 962 was by the time the company needed it most, conspicuously absent.

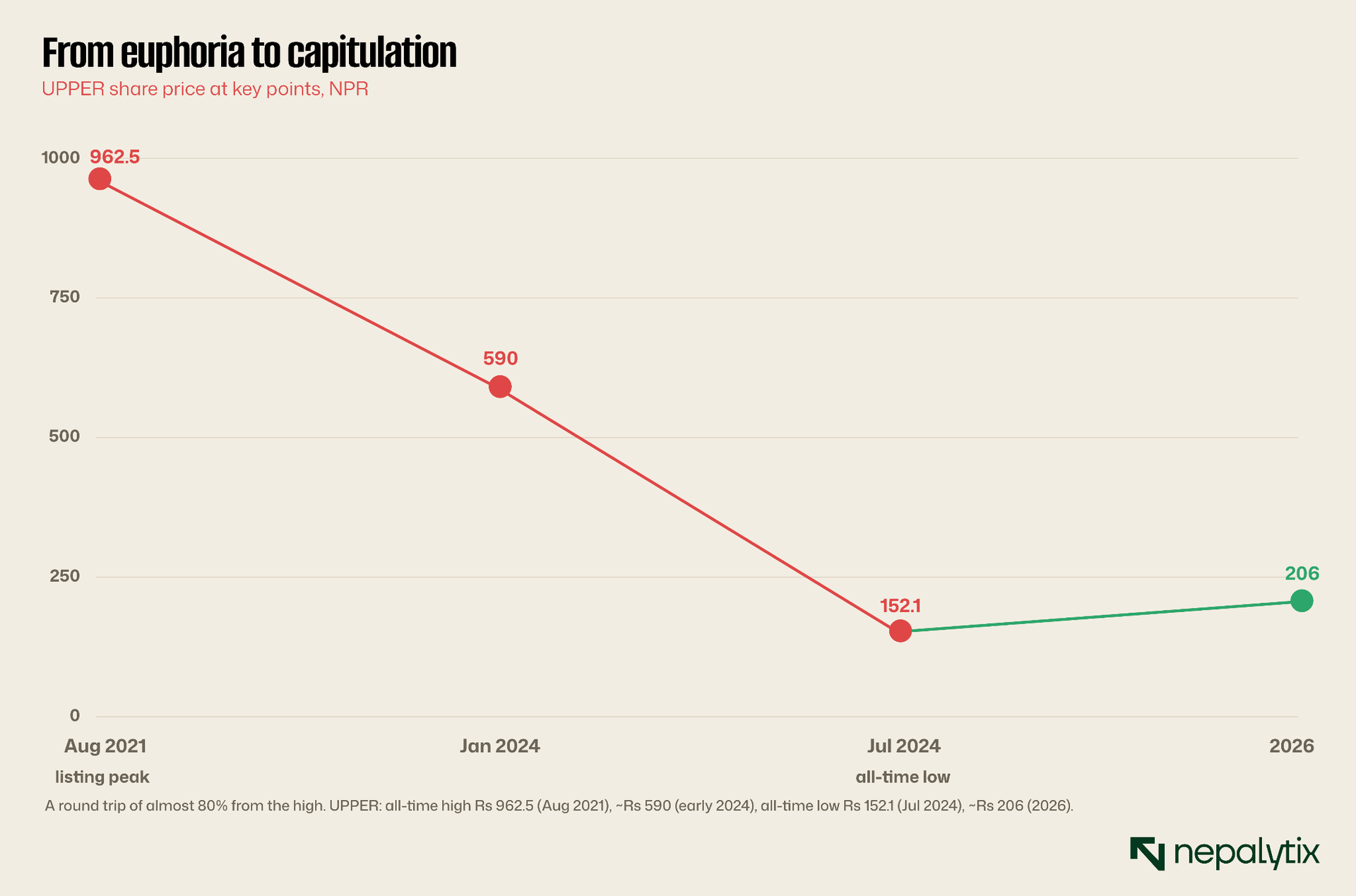

The share price: euphoria to capitulation

Few Nepali shares illustrate the gap between narrative and numbers as vividly as Upper Tamakoshi's price history. The stock reached an all-time high of about Rs 962.5 in August 2021 in the euphoria around the plant's commissioning when the market priced the flagship as a triumph and largely ignored its balance sheet. As the losses became undeniable, the price collapsed touching an all-time low of about Rs 152.1 in July 2024, a fall of roughly eighty percent from the peak. It has since steadied in the low two hundreds, around Rs 206.

That round trip is the single best lesson the share offers the wider market, and it is the same lesson our recent primer on reading a hydropower company drew: the dam is not the investment. Investors who bought the megawatts and the national pride at Rs 900 have lost most of their capital; the financial reality that was always visible in the interest-coverage ratio simply took time to assert itself over the story. The market has now swung from crowning the asset to something closer to ambivalence which is a more rational place to begin an analysis even if it is still not obviously cheap.

There is a behavioural footnote that matters for anyone trading the share. Upper Tamakoshi is widely held and reasonably liquid by NEPSE standards so it tends to move with retail sentiment and the broad index as much as with its own fundamentals. In the euphoric phase that worked spectacularly in its favour; in a cooling market it can work against it, pushing the price below any reasonable estimate of value just as it once pushed it far above. For a patient investor, that volatility is the opportunity: the time to build a position in a capped-but-recovering asset is when the retail crowd has given up on it, not when it is celebrating.

Who owns it and why that matters

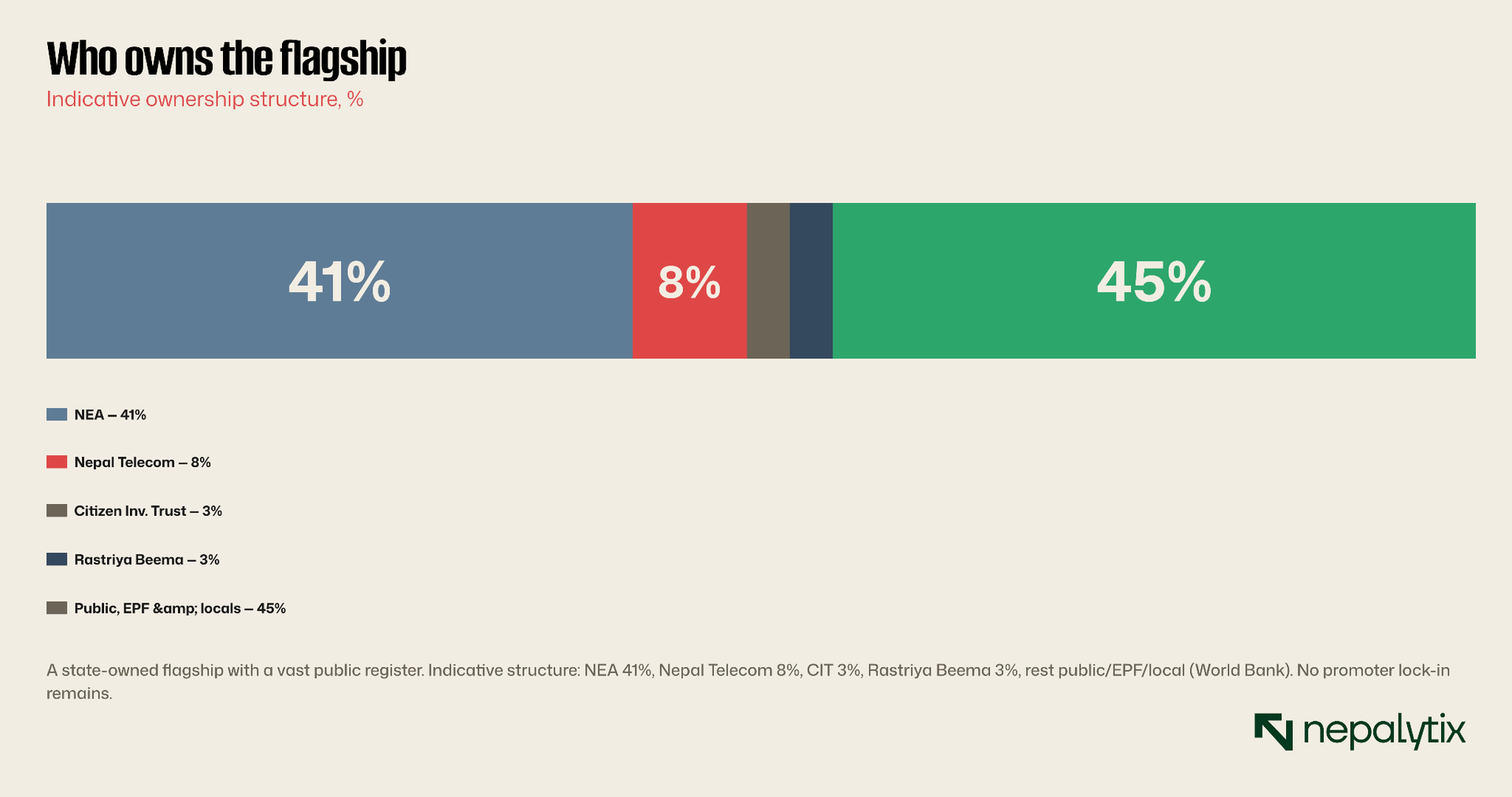

Upper Tamakoshi's ownership is unusual and consequential. It was built by the NEA together with other public institutions: indicatively, the NEA itself held around 41%, Nepal Telecom about 8% and the Citizen Investment Trust and Rastriya Beema Sansthan around 3% each with the remaining 45% or so placed with the Employees Provident Fund, employees, lending institutions, project-affected locals and the general public. The debt, too, came substantially from these same public institutions and the government.

Two implications follow. The first is reassurance: a project this strategic, this state-entwined is highly unlikely to be allowed to fail outright, and there is a national interest in seeing it through to the post-debt years. The second is a caution: the same state involvement means the company's fortunes are bound up with state decisions it does not control, on tariffs, on the NEA's own solvency and on the proposed unbundling of the NEA that could reshape its only customer. There is no longer any promoter lock-in; all the shares trade freely so the register is an unusually broad mix of state institutions, pension money and retail investors all of whom share the same capped-upside, slow-recovery proposition.

The counterparty point is the one most worth dwelling on. Upper Tamakoshi sells almost all its power to a single buyer, the NEA whose own pre-tax profit fell by more than a third in the most recent year and whose finances are under growing strain as it absorbs a swelling monsoon surplus. A creditor-like equity, dependent on decades of payments from a financially pressured state monopsony carries a counterparty risk that no amount of operational excellence at the plant can offset. If the buyer's condition deteriorates every hydropower company that sells to it is exposed and the largest supplier most of all.

The bull case: a deleveraging story

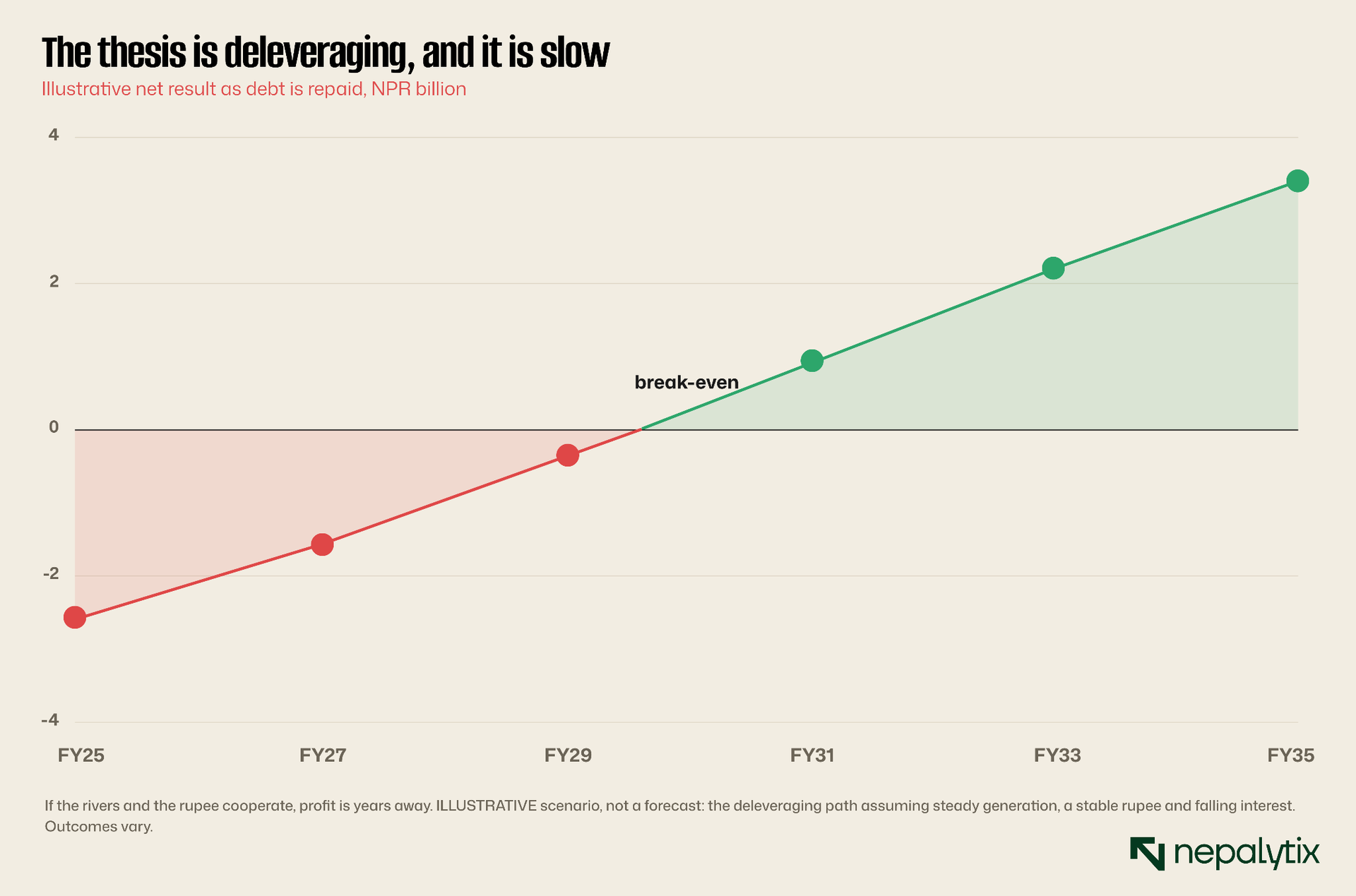

For all the gloom in the numbers, there is a genuine investment case and it rests on a single word: deleveraging. The losses are entirely below the operating line and the operating line is strong on the order of Rs 3.5bn of operating profit in a normal year. If the debt and its interest can be brought down, through the rights-issue proceeds, scheduled amortisation and the simple passage of time, the net result mechanically improves. As interest falls, the same plant that loses money today can cross into profit and eventually throw off the dividends its operating economics imply.

Our illustrative deleveraging path suggests break-even is plausible in the early 2030s with rising profits thereafter, though we stress this is a scenario, not a forecast and it depends on steady hydrology, a stable rupee and a falling interest burden. To that base improvement, the bull would add three things: the Rolwaling diversion which adds valuable dry-season generation toward the middle of the next decade; the option of power exports as Nepal builds cross-border capacity and the flagship's scale makes it a natural candidate to feed an export market; and the sheer irreplaceability of a 456-megawatt asset that could not be rebuilt today at anything like its historic cost.

In this reading, Upper Tamakoshi is a bond-like, late-cycle recovery play: buy the leading asset while it is loss-making and unloved, accept years of patience and own the dividend machine that emerges once the debt is gone and the licence still has years to run. It is a coherent thesis, and for an investor with a genuinely long horizon and a tolerance for the risks below, not an unreasonable one.

It helps to size the prize. If, post-debt, the plant can convert something close to its Rs 3.5bn of operating profit into a few billion rupees of net profit then across 211.8m shares the normalised earnings power is on the order of Rs 10 to 15 a share, enough to support a dividend an income investor would value. The catch and it is the whole catch is the word post-debt: that earnings power is real but deferred by years of repayment, and a rupee of profit a decade away is worth far less than a rupee today. The bull case is not wrong about the destination. It is a bet on the patience required to reach it and on nothing going wrong along the way.

The export leg of the bull case deserves a sober weighting. Nepal does now export surplus monsoon power to India and a 456-megawatt plant is exactly the kind of asset a serious export programme would lean on. But Upper Tamakoshi sells under a long-term agreement to the NEA not directly into an export market so it captures export economics only indirectly and only if the NEA and the government choose to route and price it that way. Treat export as a genuine but second-order source of upside, a reason the asset retains strategic value, rather than a near-term catalyst that changes the cash flows an investor can bank on today.

The bear case: a permanently capped return

The bear case does not dispute that the asset is excellent or that deleveraging helps. It disputes how much the equity can ever be worth given the ceiling above it. The frozen tariff is the crux: even a fully deleveraged Upper Tamakoshi earns a price per unit set fourteen years ago and never reset eroding in real terms every year. The upside is therefore capped not by the debt, which is temporary but by the contract which is not. The plant can become profitable but it can never become highly profitable at those rates.

Around that central point the bear stacks several lesser concerns. The shortened licence expiring around 2055 means the recovery years are also the closing years and the clock is running through the loss period. Debt paydown is slow; even optimistic scenarios imply more than a decade before the balance sheet is comfortable. Foreign-exchange exposure means a weakening rupee can reopen losses the operating recovery had closed. Hydrology and disaster risk are real and recurring, as the eighty-eight-day landslide halt demonstrated. And the return on equity that the project was originally underwritten to deliver, around fifteen percent, has already been revised down toward twelve as costs rose, debt grew and the licence shortened.

Put together, the bear sees a business whose best realistic outcome is a modest, capped, late-arriving return, attached to a stock that still trades at more than four times a depressed book value. On that view, the market is once again paying for a story, the recovery, before it has arrived and without demanding much margin of safety for the considerable chance that it arrives slowly, partially or not at all.

There is also an opportunity-cost dimension the bear emphasises. Capital committed to Upper Tamakoshi at today's price is locked into a decade-long wait for a capped return in a market that offers other ways to earn while waiting from deposits yielding mid-single digits to mature, debt-light hydropower plants already paying dividends. The question is not only whether Upper Tamakoshi eventually works but whether it works better than the alternatives over the same horizon. For much of the next decade, on the bear's arithmetic, it may not.

Valuation and the call

Conventional multiples are of little use here. The price-to-earnings ratio is meaningless while the company is loss-making, and the price-to-book of about 4.4 times is flattering in the wrong direction because the book value in the denominator has itself been halved by accumulated losses. A high multiple of a depressed book is not the bargain it can superficially appear to be.

The only honest way to value Upper Tamakoshi is on its normalised, post-debt earnings power discounted heavily for the long wait, the capped tariff and the execution risk along the way. Doing so produces a wide range rather than a point, which is itself the most important conclusion. Our illustrative range runs from roughly Rs 95 in a bear case where deleveraging is slow and the capped tariff dominates through about Rs 150 in a base case of steady deleveraging plus the Rolwaling uplift, to around Rs 235 in a bull case that adds faster debt reduction, export revenue and a scarcity premium for the irreplaceable asset.

At about Rs 206, the share sits in the upper half of that range. That is the call. We are not bearish on the asset which is genuine and strategic and we are not calling the stock a short. But at today's price the market is already paying for a substantial part of the recovery it has not yet seen and the margin of safety is thin. We would rather own this flagship on evidence of actual deleveraging ideally at a lower entry than pay up front for a recovery that the interest-coverage ratio says is still years away. For a publication that prizes reading the contract over admiring the dam, Upper Tamakoshi is the clearest case on the exchange of why the two are not the same.

For investors who want a single summarising lens, think of Upper Tamakoshi as a long-dated, low-coupon bond with equity risk: a stream of capped, deferred cash flows whose present value is highly sensitive to the discount rate, the speed of deleveraging and the residual life of the licence. Small changes in any of those assumptions swing the fair value by tens of rupees which is exactly why our range is wide and why we resist a single point estimate. Anyone quoting a precise target for this share is overstating what the inputs can support. The honest output is a range and a view on where in that range the current price sits.

To make the sensitivity concrete: shift the assumed pace of debt repayment by a couple of years or the discount rate by a single percentage point and the base-case value moves by twenty or thirty rupees. Add or remove the export and scarcity premium and the bull case moves further still. None of these inputs is knowable with precision today, which is the honest reason the gap between our bear and bull cases is so wide. The investor's job here is not to pick the single right number but to decide which scenario the evidence is trending toward and to demand a price that pays them to wait for it. At Rs 206, on our reading, the price is not yet doing that.

Key risks

The risks cut in both directions. On the downside: a weakening rupee reopening foreign-exchange losses; hydrology and natural-disaster risk including further landslides, floods or seismic damage against which the financial model has little slack; slower-than-expected debt reduction; an adverse outcome from the proposed restructuring of the NEA, the company's sole customer; any drift of the wider sector's take-or-pay terms toward take-and-pay; and the possibility of further capital raising and dilution if losses persist. On the upside: faster deleveraging, a firmer rupee, a higher or renegotiated tariff, earlier-than-expected export revenue, and successful, on-time completion of the Rolwaling works would each move the equity toward the upper end of our range sooner than our base case assumes.

The honest summary is that Upper Tamakoshi is a high-quality asset wrapped in a high-risk balance sheet and a low, fixed price. Whether the equity rewards today's buyer depends almost entirely on the speed of deleveraging and the behaviour of the rupee and the rivers none of which the investor controls and much of which the current price already assumes goes well.

We will revisit this initiation as the deleveraging evidence accumulates. The signposts to watch are concrete: the trajectory of the interest bill and total borrowings, the path of net worth per share back toward and above par, the resolution of the landslide insurance claim, progress on the Rolwaling diversion, and any change to the tariff regime or the NEA's own finances. A sustained turn in those indicators, more than any movement in the share price itself is what would move our fair-value range and our stance. Until then, the asset earns our admiration and the equity earns our patience.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.