Nepal’s Liquidity Glut: Why Cheap Money Isn’t Creating Growth

Nepal's banking system has gone from a severe liquidity shortage to an unprecedented cash surplus in just three years. Interest rates have fallen to decade lows, yet private-sector credit growth remains far below target as businesses and households hesitate to borrow.

Nepal's banks are drowning in deposits and short of borrowers. The cost of money has roughly halved since the 2022-23 crunch, credit is growing at a third of target and the surplus is leaking into treasury bills and share prices instead of the real economy. A look at the glut and why another rate cut won't clear it.

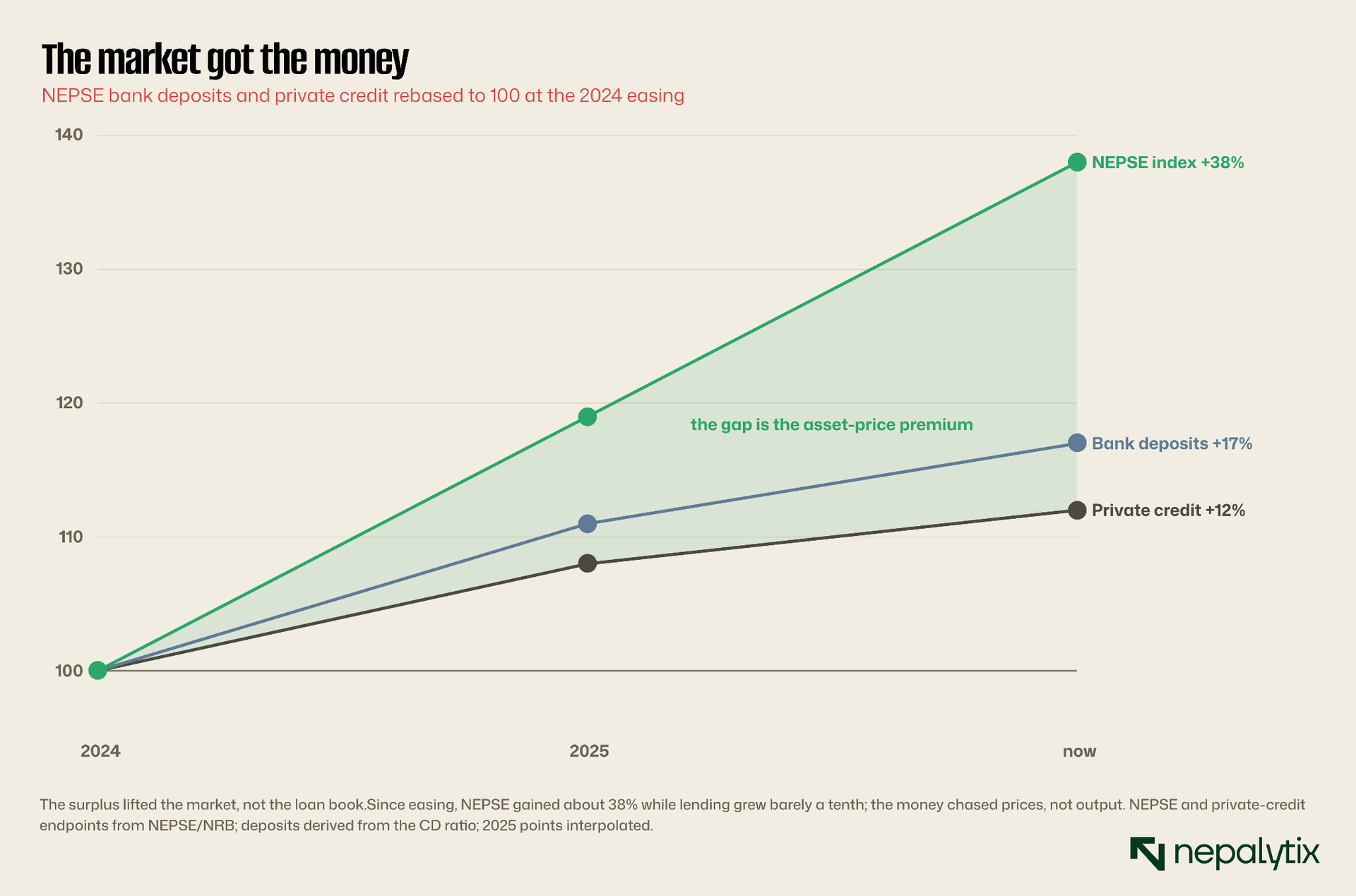

The price of money has roughly halved since 2023 yet private credit is expanding at 3.6% against a 12% target. The surplus is pooling in deposits, government paper and asset prices and the central bank is now paying banks to park cash it cannot lend. Cheap money has arrived in Nepal. Productive money has not.

Every so often a financial system flips from scarcity to surfeit, and the second problem proves harder to manage than the first. Nepal has just made that flip. The crunch that defined 2022 and 2023 is gone, replaced by a surplus so large the central bank now spends its days absorbing money rather than supplying it. What follows traces how the glut formed, why cutting rates has stopped working, and where the unspent rupees are ending up.

Money Has Never Been This Cheap

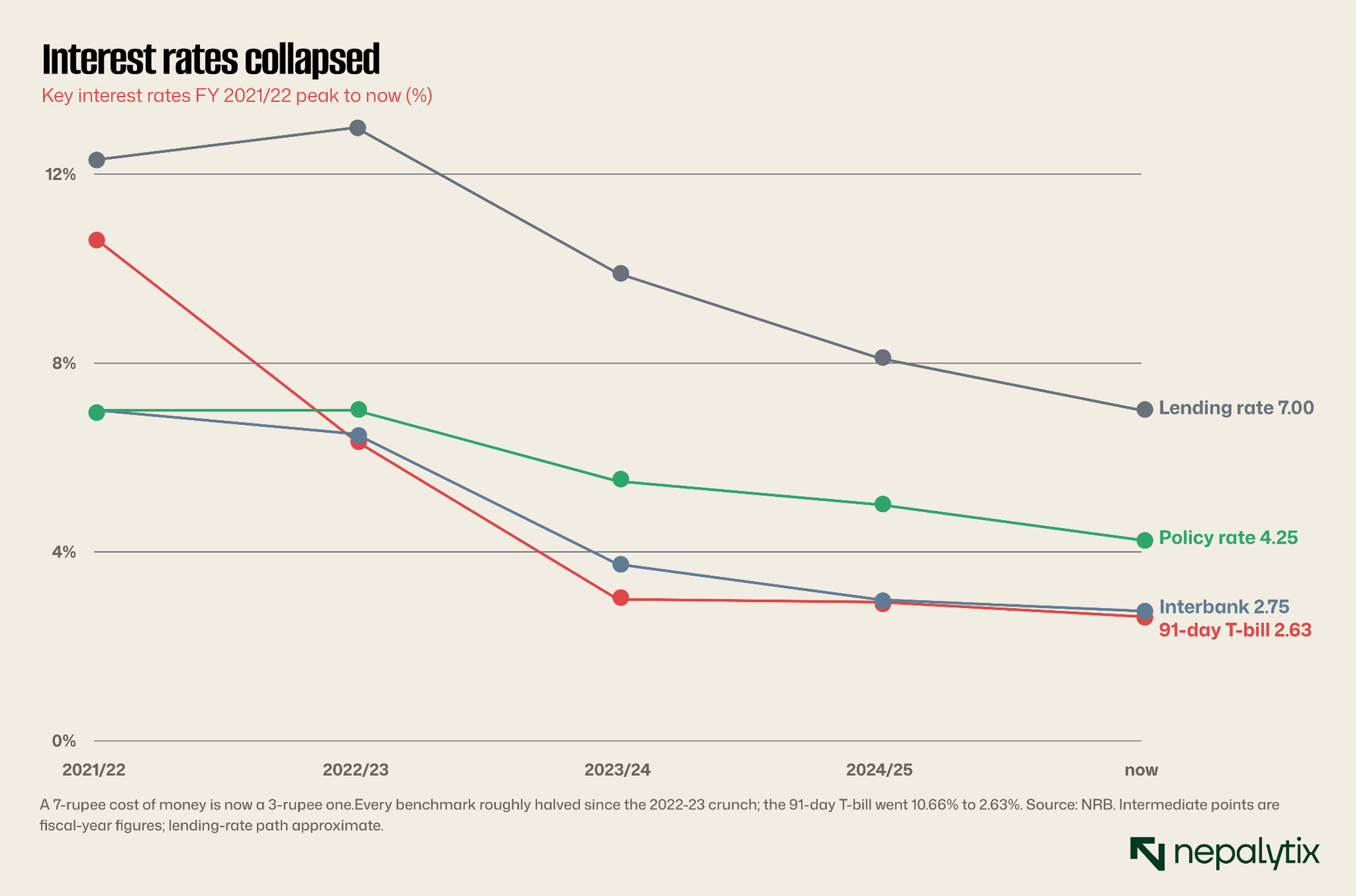

Two years ago Nepal had the opposite problem. The banking system was starved of cash, the 91-day treasury bill yielded 10.66%, lending rates touched 13% and businesses queued for credit they could not get. Inflation had climbed past 8% on the back of a global price shock and a sliding rupee, property transactions had fallen by more than half and the central bank was draining reserves to pay for imports. To defend the currency and cool demand it tightened hard, lifting the policy rate to 7% by September 2022.

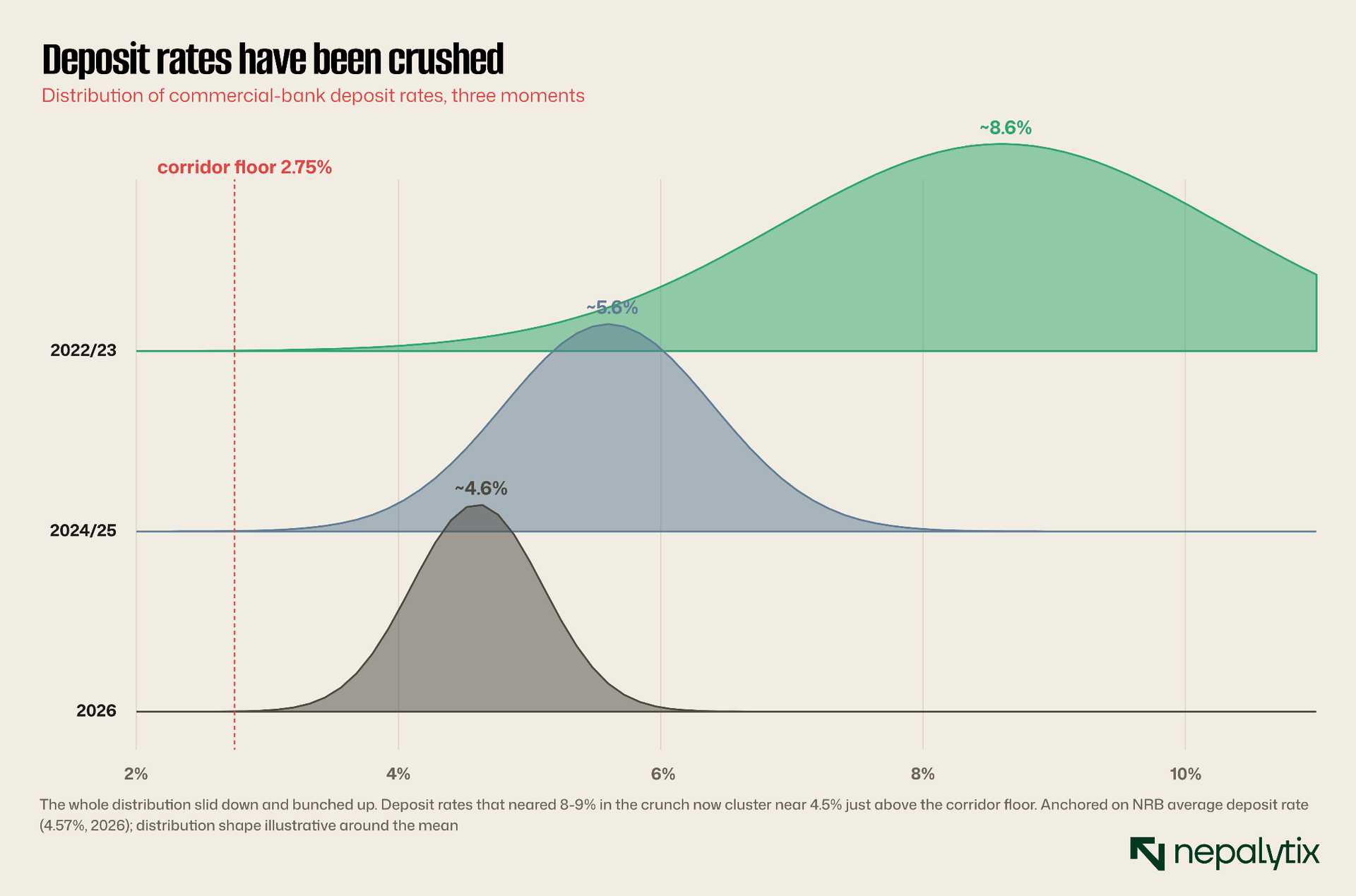

Then the squeeze reversed. Remittances came flooding back as labour migration surged, foreign-exchange reserves climbed to records, and inflation rolled over. From June 2023 the central bank began easing and it has not stopped since. Every benchmark rate has roughly halved. The policy repo rate sits at 4.25% after a 75-basis-point cut this year; the bank rate is 5.75%, and the deposit-collection rate that forms the floor of the corridor is 2.75%. The weighted interbank rate, the cost banks charge each other overnight, has fallen to that 2.75% floor from above 7% in mid-2022.

Government paper tells the same story in sharper relief. The 91-day treasury bill, which paid 10.66% at the height of the crunch, now yields 2.63%; the 28-day bill pays just 1.65%. The average lending rate has come down to 7.00%, half its peak. A borrower who could not find money at any price in 2023 can now find it cheaply. The problem, it turns out, is that almost nobody is looking.

Strip away the noise and the shift is stark. In the space of three years Nepal has gone from a system where the overnight rate sat near 7% to one where it cannot stay above 2.75% without the central bank fighting to hold it there. The corridor that bounds those rates has been narrowed and lowered repeatedly and the standing liquidity facility banks once leaned on for emergency cash now priced at 5.75%, is rarely needed. The machinery built to relieve a shortage is idling in a surplus.

The Economy Stopped Responding

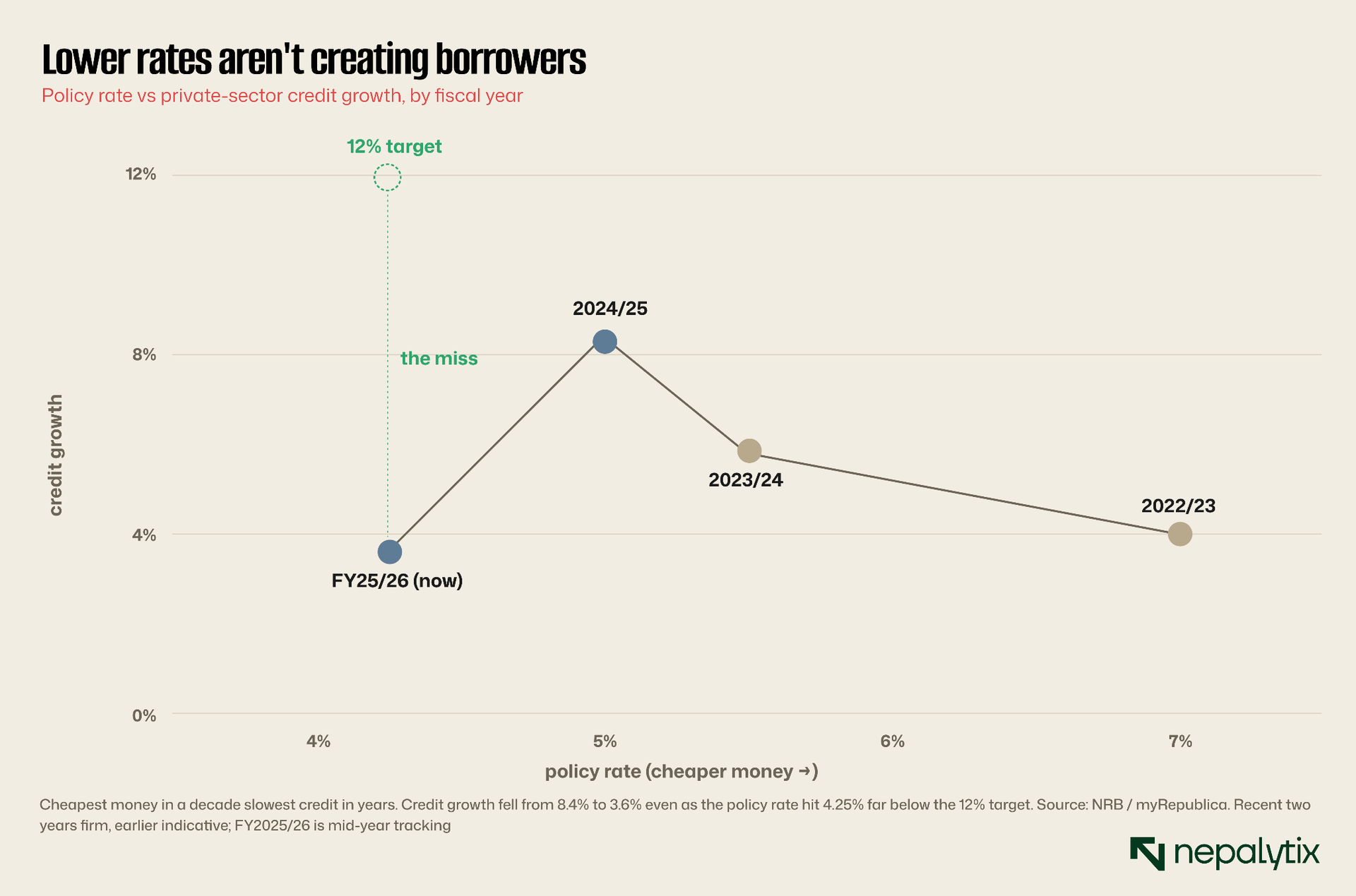

The textbook says cheaper money should pull more borrowing. In Nepal it has not. The central bank set a 12% target for private-sector credit growth this year and, by mid-January, had delivered 3.6%. The year before it managed 8.4%. So the policy rate is the lowest in a decade while credit growth is among the slowest in years, the two falling together rather than trading off as theory expects.

The detail underneath is just as flat. Loans to non-financial companies grew 0.9% in the latest survey; household credit grew 0.9% as well. Neither businesses nor families are reaching for the cheap money on offer. The central bank loosened its working-capital rules at the mid-term review, handing banks discretion over loan tenures to ease repayment pressure, and still the needle barely moved. Its own review concedes the point bluntly: the constraints on credit growth this year were "largely non-monetary in nature," meaning monetary policy alone cannot drive lending.

That is the crux. After September's Gen-Z unrest disrupted business and dented confidence, after years of sluggish investment, and with private credit already running near 92% of GDP against a world average closer to 52%, the appetite to borrow simply is not there. Foreign investors pledged Rs 35 billion in the first quarter yet actual inflows trailed the commitments, the same gap between intention and action that defines the whole economy right now. Cutting the price of credit does nothing when the shortage is of borrowers, not of funds.

History sharpens the contrast. Over the past two decades private-sector credit in Nepal grew by an average of nearly 20% a year, the kind of double-digit expansion that built the banks now listed on NEPSE. To slow from that to 3.6% with money at its cheapest in a decade is not a gentle deceleration. It is a credit market that has stopped responding to the one lever the central bank controls and a sign that the next phase of growth will have to come from something other than ever more bank lending.

Every Indicator Says the Same Thing

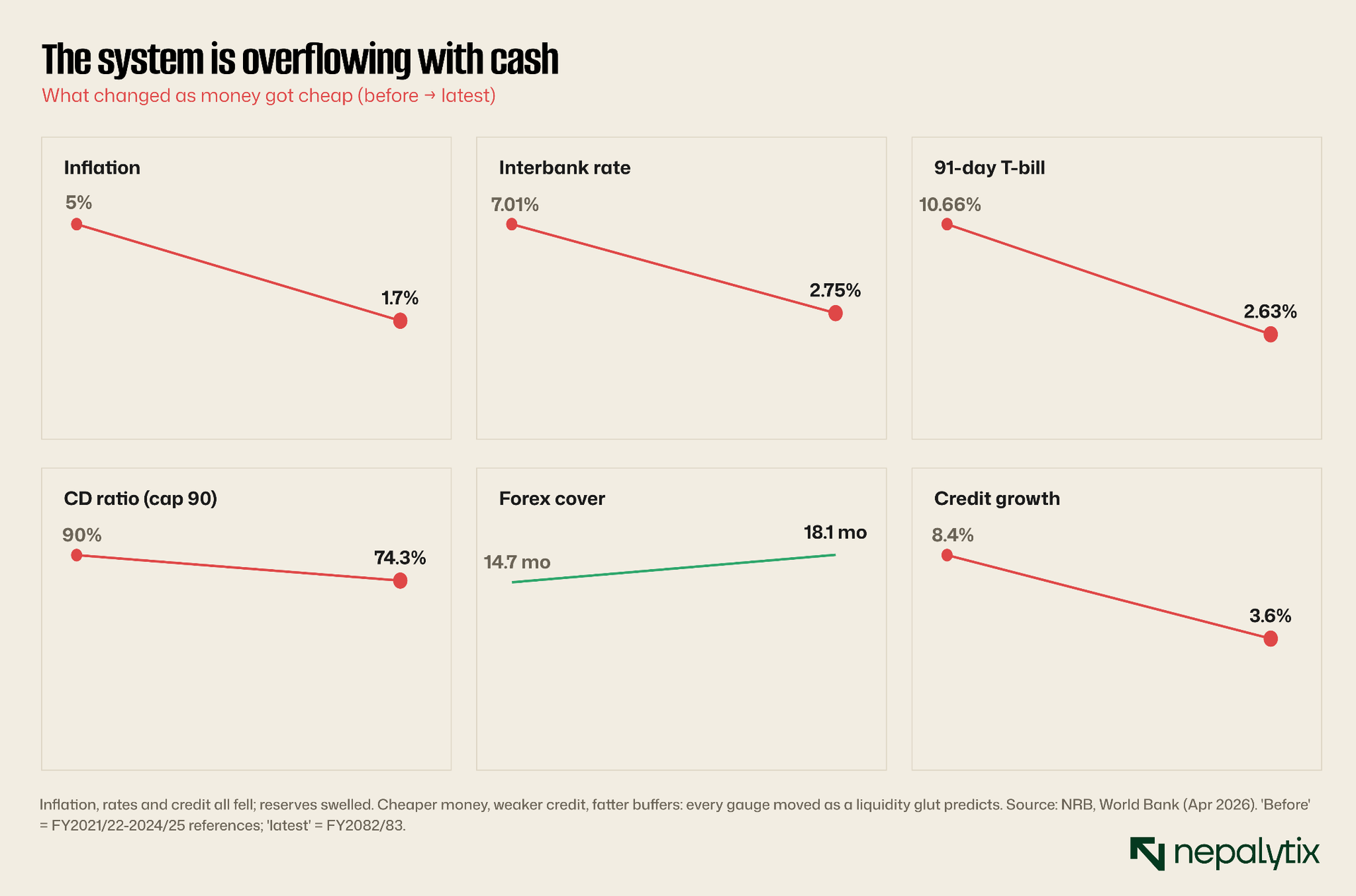

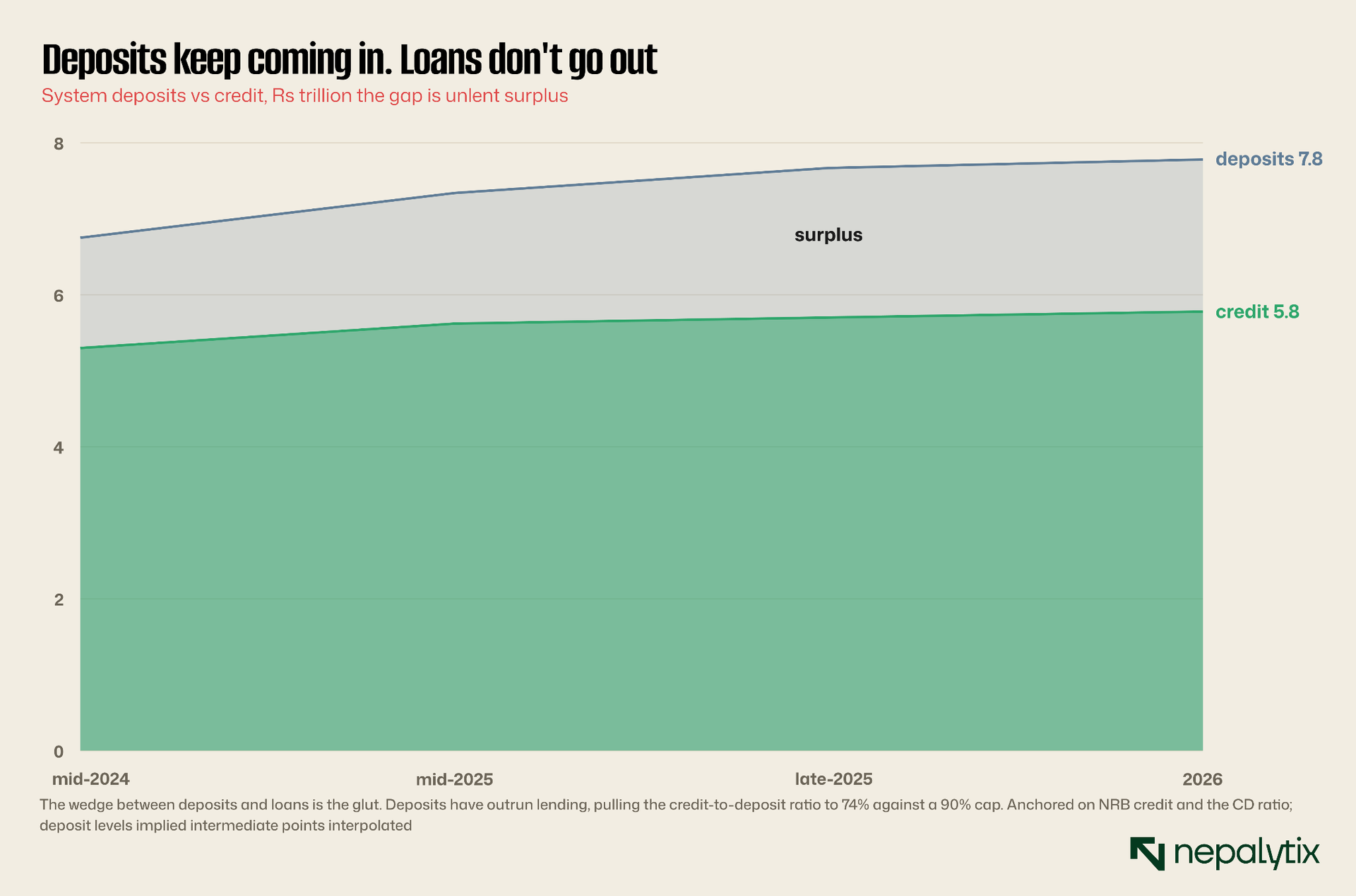

A liquidity glut leaves the same fingerprints on every gauge, and Nepal's all point the same way at once. Inflation has fallen to 1.7%, a record low from 5% a year earlier. The interbank rate and the 91-day bill have both collapsed toward the floor. The credit-to-deposit ratio has slid from its 90% cap to 74%. Foreign-exchange cover has swelled from 14.7 to 18.1 months of imports, more than double the regulatory minimum of seven.

The sources of the flood sit on the external account. Remittances jumped 35.4% to Rs 553 billion in the first quarter alone, reaching 16.6% of GDP, and lifted the current account into a surplus worth 6.7% of output. The balance of payments ran a surplus above Rs 260 billion, and reserves climbed past USD 22 billion. Each of those dollars arriving has to be converted, and the conversion is where the rupees come from.

Here is the mechanism that makes the glut self-feeding. To stop the rupee from appreciating as dollars pour in the central bank buys the foreign currency paying for it in newly created local money. That single channel injected an estimated Rs 673 billion last year. The cash lands in bank deposits, the deposits cannot be lent fast enough and the surplus builds. Low inflation which would normally be unambiguously good news, here also signals how little of this money is chasing real goods. Only gold and silver prices show much heat which is itself a clue about where savers are hiding.

The composition of the inflows matters as much as their size. This is not an export boom or a surge of foreign investment building productive capacity; it is overwhelmingly money sent home by Nepalis working abroad deposited by their families and waiting to be spent or invested. That makes the glut both a strength and a vulnerability. It has handed Nepal record reserves and rock-bottom rates but it has tied the health of the banking system to labour markets in the Gulf and Malaysia, far outside any domestic policymaker's control.

Deposits Keep Rising. Lending Doesn't

The mechanical result is a wedge. Deposits keep arriving, lending does not keep pace, and the space between the two is surplus the banks cannot put to work. A credit-to-deposit ratio of 74% against a 90% ceiling leaves roughly sixteen points of lending capacity idle across the system with state-owned banks sitting more conservatively still and private banks alone pushing toward the cap.

So the central bank is now doing the reverse of easing. Rather than inject money, it has spent the year mopping it up draining an estimated Rs 200 billion through repo auctions, fixed-deposit collections and a standing deposit facility it has stretched to 175 days. In one recent operation it offered to absorb Rs 50 billion for 42 days; it has promised to issue its own bonds if the tide rises further. To keep the interbank rate from sinking below the corridor floor, it has even barred banks that pay savers below the floor from parking cash at the facility.

A central bank that cuts rates to encourage lending is, at the same time, paying banks to hand cash back because there is nowhere productive for it to go. The banks are not unhappy about it. Flush with deposits and earning a spread of around 3.5 percentage points between what they charge borrowers and pay savers, they can sit on government paper and the deposit facility and still post a profit. Comfortable for the lender; a sign of a stalled engine for everyone else.

None of this is how an interest-rate corridor is meant to behave. In a balanced system the interbank rate floats near the policy rate, banks lend their surplus to one another, and the central bank intervenes only at the edges. In Nepal the interbank rate is glued to the bottom of the corridor and the central bank intervenes constantly, not to add liquidity but to remove it. The corridor has become a one-way valve, and the volume of cash flowing back to the regulator is the clearest single measure of how little the economy can absorb.

The Return on Safety Has Vanished

Someone pays for cheap money and in Nepal it is the saver. Deposit rates that neared 8 to 9% during the crunch now cluster around 4.5%, with commercial banks ranging from 4.25% to 5.10%, a sliver above the 2.75% corridor floor. Fixed deposits average 5.18%, ordinary savings 2.90%, and call deposits just 0.73%.

Low inflation softens the blow on paper. With prices rising 1.7%, a 4.5% deposit still earns a small positive real return, better than the negative real rates savers endured during the high-inflation crunch. But the trend is unmistakable and one-directional. The whole distribution of bank deposit rates has slid down and bunched against the floor and the central bank has cleared the way for it, removing the cap on institutional deposit rates so banks could trim the maximum they pay individuals.

For a saver the message is plain: a bank deposit now barely keeps pace with the cost of living and the gap between the best and worst rates on offer has narrowed to almost nothing. That is exactly the condition that sends money looking for a better home. When the safe option pays close to zero in real terms, the not-so-safe options start to look reasonable and a great deal of Nepali savings has come to precisely that conclusion.

The squeeze on savers carries a second-round effect the central bank cannot ignore. Push the return on a deposit low enough and the rational response is to stop saving in deposits, which would eventually starve the very banks now drowning in them. For now the remittance flood more than replaces any money that drifts away so deposits keep growing despite the meagre rates. The dynamic is still worth holding in mind: the glut is comfortable only as long as savers stay put and the thinner their reward the less certain that becomes.

Where the money actually went

Where it looked, it found asset prices. With productive credit crawling and deposits paying 4.5%, the surplus chased returns into the secondary market and into property. NEPSE has risen by roughly 38% since 2024 to record territory; real estate, where transactions had collapsed 56% during the crunch, has revived as cheaper home loans and higher loan limits drew buyers back. Government paper soaked up much of the rest.

This is not a charge anyone has to infer. The central bank's own macroeconomic report concedes that the last round of easing "could not be fully absorbed by the market especially in productive sectors," and was instead reflected in asset prices, "with a record stock market index and real estate prices." Cheap money did not build factories. It bid up the things already built and lending to the real economy slipped to the back of the queue.

The loop tightens because the buyers are often the same institutions sitting on the surplus. Banks, insurers and the broader financial sector are themselves large holders of NEPSE-listed shares, so a market awash in their float is partly holding itself up. Eased risk weights on smaller margin loans add another turn of leverage. None of that is dangerous while the inflows continue. It becomes dangerous precisely when they stop, because an asset price lifted by liquidity rather than earnings has nothing to stand on once the liquidity recedes.

The numbers around the rotation are striking on their own. A stock index up nearly 40% in two years, a property market swinging from a 56% collapse to a visible revival and a deposit base earning under 5% sit beside a real economy whose credit is barely growing. That divergence, between asset prices and the activity supposed to underpin them, is the clearest symptom of money with nowhere productive to go. It is also the part of the story most easily mistaken for a healthy bull market.

The Problem Isn't the Cost of Money

The uncomfortable conclusion is that another rate cut will not fix this. The central bank has already cut to 4.25% and watched the credit stall because the binding constraint is not the price of money. It is weak investment demand in an economy still rattled by September's unrest, and a structural ceiling on how much more credit a country already lent to the hilt can absorb. Non-performing loans are rising and bank spreads are thinning at the same time, which is why the regulator is reaching past interest rates altogether.

Its toolkit now runs to an asset-management company to take bad loans off bank books, looser working-capital rules, productive-sector lending targets and prompt-corrective action reforms for weak institutions. These are supply-side fixes for a demand-side problem and the central bank knows it; what it cannot do with any instrument is manufacture borrowers. The structural work, an investment climate worth committing to, credit guarantees, coordinated fiscal support, sits largely outside its remit.

For an investor the read-through is blunt. As long as money stays cheap and the real economy cannot absorb it, the surplus keeps flowing toward NEPSE, property and bonds, supporting asset prices for reasons that have little to do with corporate earnings. That is a tailwind worth riding and a risk worth respecting because a glut that lifts prices without lifting output unwinds the day the inflows slow. The single number to watch is remittances, the source of the flood; the FY2083/84 monetary policy due in July cannot conjure demand and can only decide how hard to lean against a tide of cheap money with nowhere to go.

A few warning lights are worth naming before then. Non-performing loans are creeping up even as the headline figures look benign, public debt has climbed toward 44% of GDP, and the asset-price gains flattering portfolios rest on inflows rather than earnings. None of these is a crisis today. Together they describe a system that has solved its liquidity shortage and replaced it with a subtler one: too much money, too few productive homes for it and an asset market drifting away from the economy beneath it. That is the imbalance the next policy inherits.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.