Nepal's Microfinance Sector Has Crossed a Dangerous Line

Nepal's microfinance bad-loan rate has jumped to 11.32% in a year, half the field is now over 10% and the buffer is thinner than the hole.

Nepal's microfinance bad-loan rate has jumped to 11.32% in a year, half the field is now over 10% and the buffer is thinner than the hole. The fix the central bank actually wants isn't a bailout, it's a merger.

This is not a bad quarter, it is a broken model. The average bad-loan ratio across retail microfinance has jumped to 11.32 percent from 7.25 percent in a single year and the capital buffer meant to absorb it, 10.3 percent, is now smaller than the hole. The group-lending machine that built the sector assumed a borrower with steady income and the social pressure to repay. Two years of protests, over-indebtedness and frozen disbursement erased that borrower. Rights shares can patch the ratio; they cannot rebuild the borrower. Nepal Rastra Bank knows it which is why its real preference is not recapitalisation but consolidation and a merger wave is already under way.

Timing sharpens all of this. The sector is closing its books at Ashad-end into a market that is already draining turnover thin, large holders sitting out so there is no wave of fresh buying to absorb the equity these institutions now need to raise. Microfinance is also where Nepal's financial inclusion actually happens: the retail lenders reach roughly 2.7 million borrowers, most of them low-income and rural, which is why the regulator cannot simply let the weak ones fail and why the resolution will be managed rather than abruptly. Read the numbers in order of the damage, then the buffer, then the response and the sector's next two years come into focus.

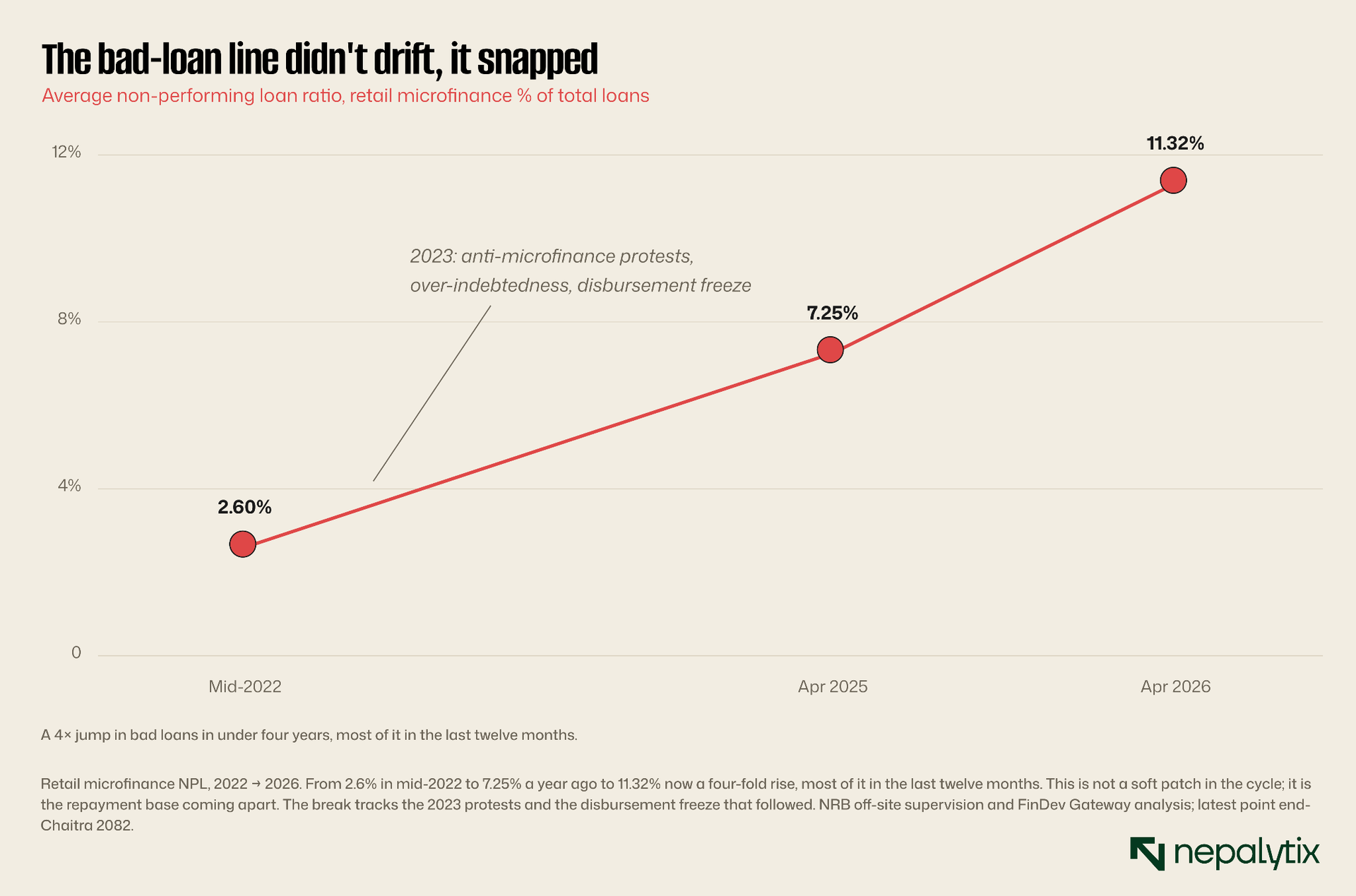

The bad-loan line didn't drift; it snapped

The number that matters is not this quarter's profit, it is the slope of the loans that stopped being repaid. Retail microfinance carried a non-performing-loan ratio of 2.6 percent in mid-2022. A year ago it was 7.25 percent. It is now 11.32 percent: a four-fold rise in under four years and most of the damage arrived in the last twelve months alone. This is not the shape of a cycle softening; it is the shape of a repayment base coming apart.

The trigger is well documented the anti-microfinance protests that began in 2023, the over-indebtedness they exposed and the regulatory tightening that followed: caps on how many lenders a single borrower could carry, limits on loan size, all landing on the book at once. The model that built the sector assumed a borrower with steady income and the group pressure to repay, and two hard years erased both. And because microfinance lending is overwhelmingly unsecured collateralised loans are barely a sixth of the book a loan that goes bad tends to stay bad. There is no house to seize; there is only the write-down.

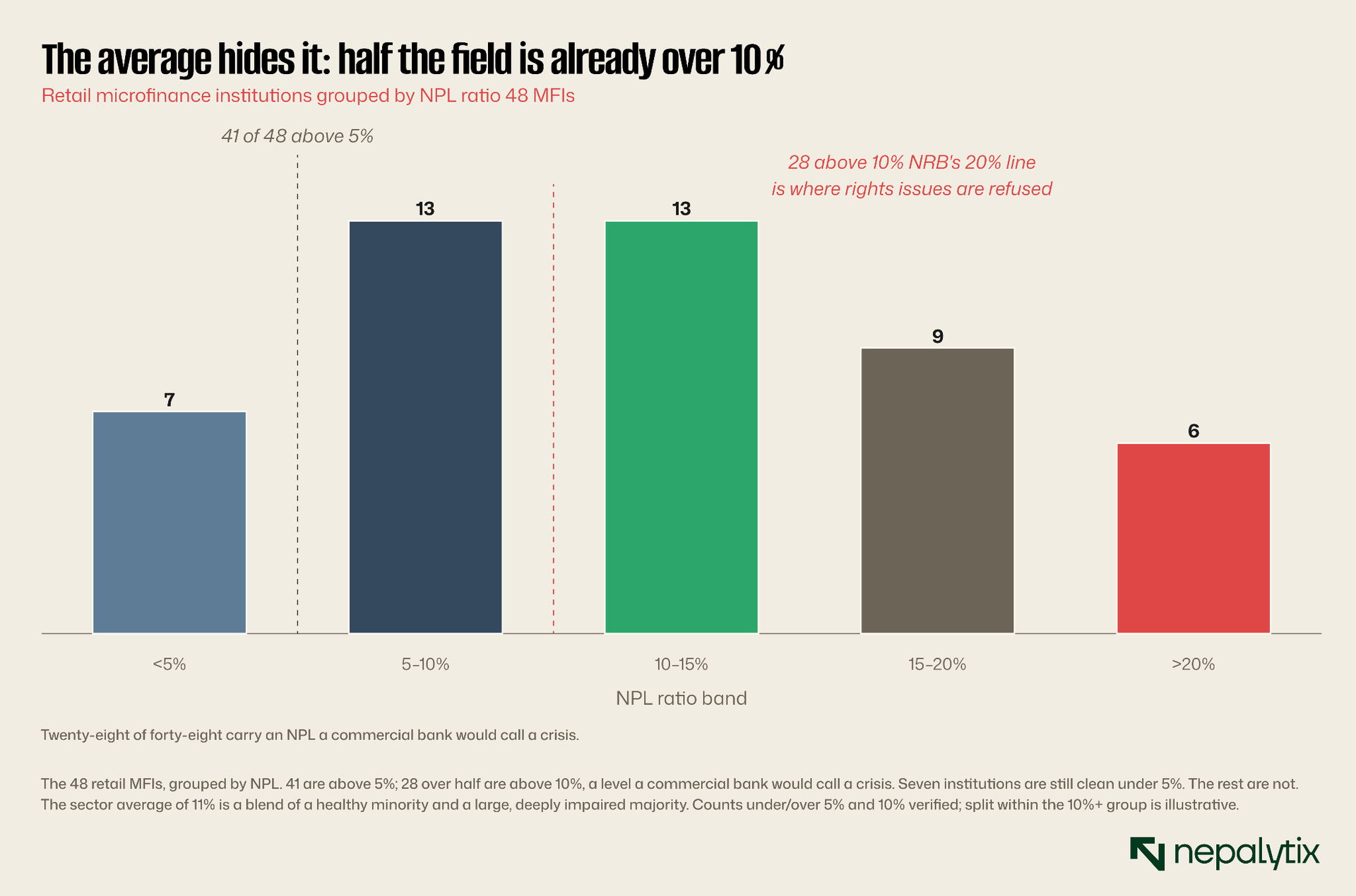

The average hides it, half the field is already over 10%

An 11 percent average is alarming on its own. The distribution behind it is worse, because the average quietly blends a healthy minority with a deeply impaired majority. Of the 48 retail institutions, 41 now run an NPL above 5 percent, and 28 more than half the field sit above 10 percent, a level a commercial bank would treat as an emergency. Only seven remain clean under 5 percent.

Layer capital on top and the same split appears: 35 of the 48 hold a capital-adequacy ratio below 12 percent, against an 8 percent regulatory floor that was written for a 2-percent-NPL world, not an 11-percent one. The sector is not facing a problem; it is separating into two populations: a small group of well-reserved survivors and a large group running out of both earnings and buffers. Every sector-average statistic you read is a weighted blend of those two groups, and it describes neither.

And the damage is specific to the retail model. Wholesale microfinance, the handful of institutions that fund the retail lenders rather than end-borrowers, runs an NPL near 3 percent, a fraction of the retail figure. The problem is not "microfinance" in the abstract; it is the retail group-lending book where an unsecured, high-turnover model met a borrower who could no longer turn it over.

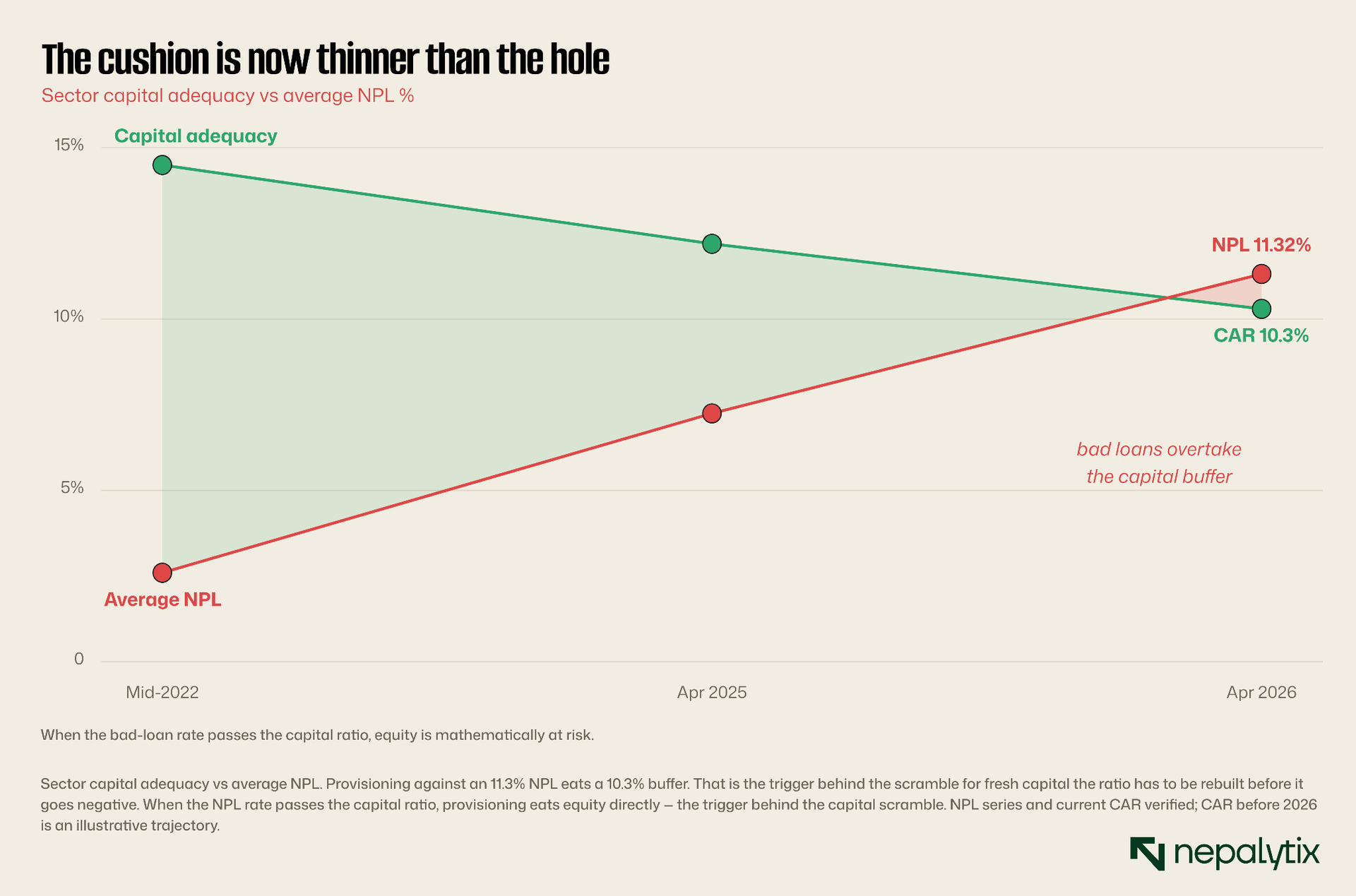

The cushion is now thinner than the hole

Here is why the clock is running rather than merely ticking. A lender absorbs bad loans out of its capital buffer, so the two numbers that matter are the size of the hole and the size of the cushion. The sector's average capital-adequacy ratio is 10.3 percent. Its average NPL is 11.32 percent. The hole is now larger than the cushion.

In rupee terms the retail book carries roughly Rs 31.5 billion of non-performing loans against about Rs 15.7 billion of provisions set aside for them barely half-covered on a total book near Rs 435 billion. Every further slip in recovery has to be provisioned, and provisioning comes straight out of equity. Once the bad-loan rate passes the capital ratio, the arithmetic has a direction and it is down. This is not a hypothetical failure mode: Super Laghubitta's capital ratio reached minus 126 percent before the central bank seized its proof of where this path ends if the buffer is not refilled in time.

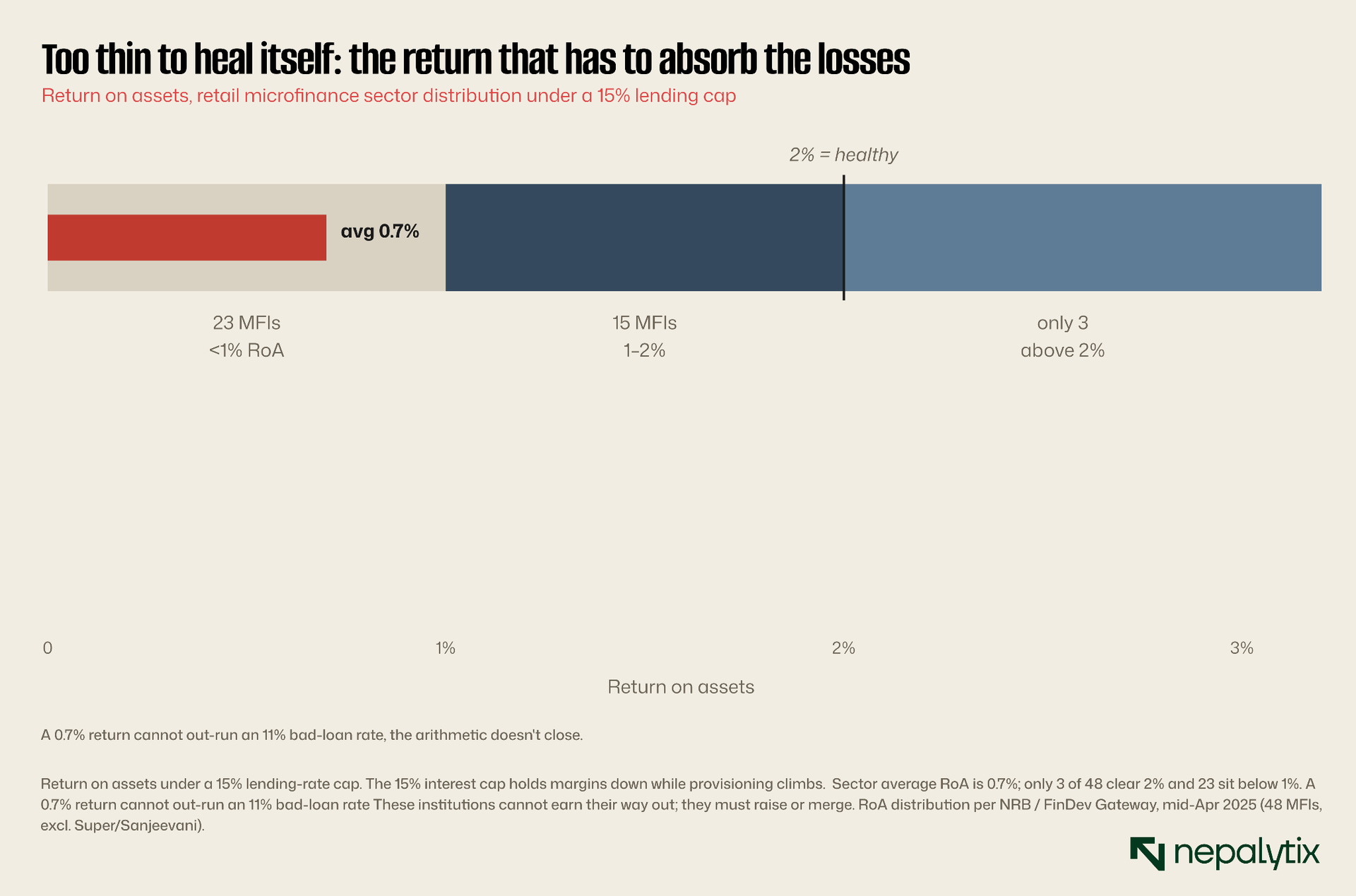

Too thin to heal itself, the cap collides with the loss

Could these institutions simply earn their way out? No and this is the cruelest constraint. A 15 percent cap on microfinance lending rates holds margins down at exactly the moment provisioning is climbing. The result is a sector-wide return on assets of 0.7 percent. Only three of the 48 clear a 2 percent RoA; 23 sit below 1 percent.

A 0.7 percent return cannot out-run an 11 percent bad-loan rate, the arithmetic does not close, and no amount of cost-cutting bridges a gap that wide. Retained earnings, the healthy way to rebuild a buffer are off the table when there are barely any earnings to retain. An institution that cannot generate enough profit to absorb its own losses has exactly two moves left: raise external capital or merge into someone who has it. And NRB now ties how much an institution may distribute to its own capital and NPL ratios so the impaired names cannot even pay a dividend to make themselves attractive to new capital the door is bolted from both sides. That single collision, a capped return against an uncapped loss is why this cannot be fixed from the inside.

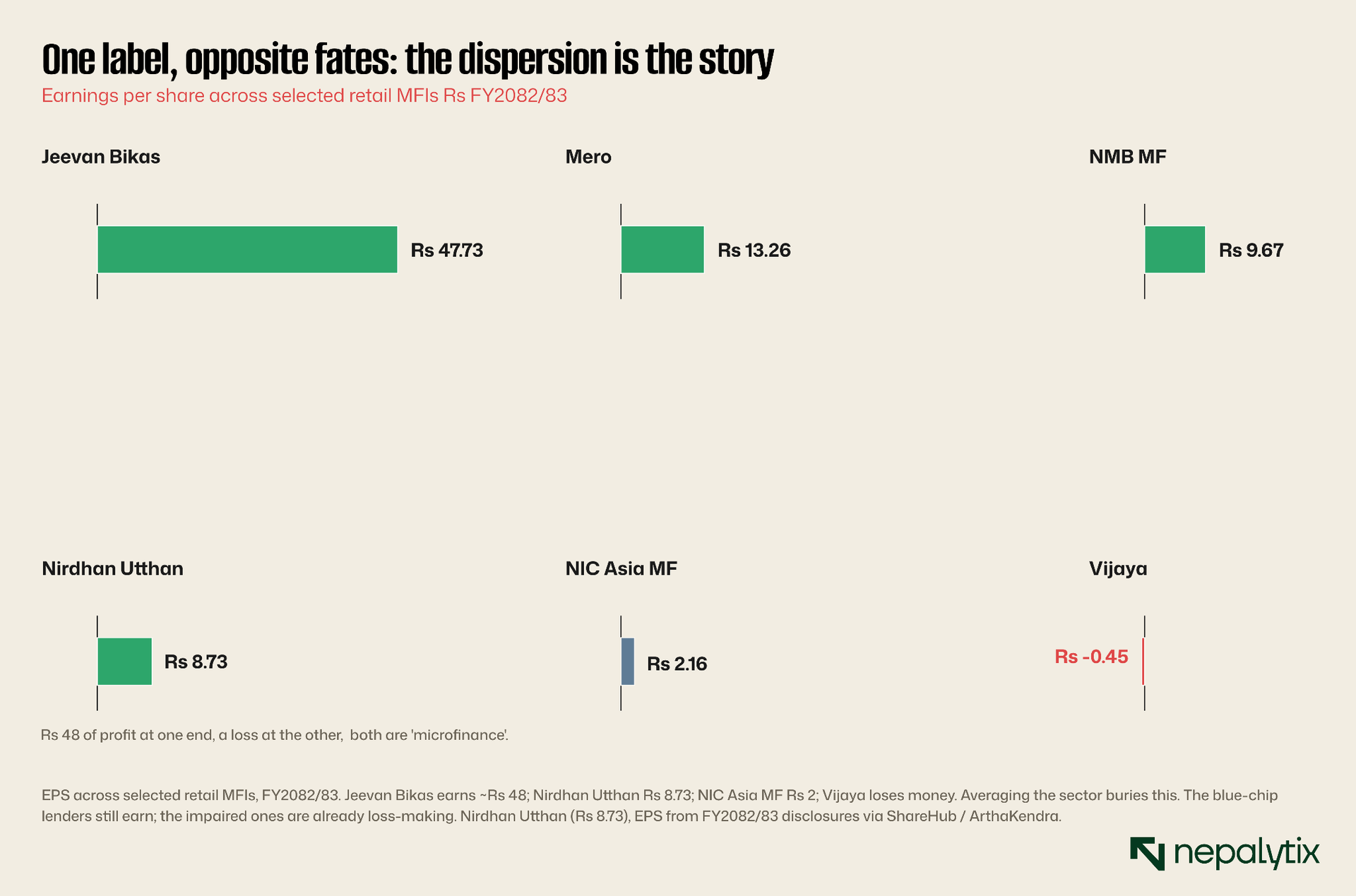

Survivors and the drowning: the dispersion is the story

Which is why treating "microfinance" as one trade is a category error, and the individual names prove it. Jeevan Bikas earns roughly Rs 48 a share. Mero earns Rs 13. Nirdhan Utthan, the sector's oldest and largest retail lender earns Rs 8.73 on a book value above Rs 200. NIC Asia's microfinance arm earns Rs 2. Vijaya loses money outright. Same sector index, opposite fates.

The difference is not luck; it is structure. The survivors carry deep reserves; Chhimek and Nirdhan sit on the largest reserve buffers in the sector, enforce recovery discipline and fund themselves more cheaply, which is precisely what lets them keep earning while the impaired names bleed. Averaging these institutions together produces a number that describes none of them. Tomorrow's research note takes the strongest of them, Nirdhan Utthan and asks the only question that matters in a sector like this: what separates a survivor from the 28 institutions now over 10 percent and is that separation durable or merely early?

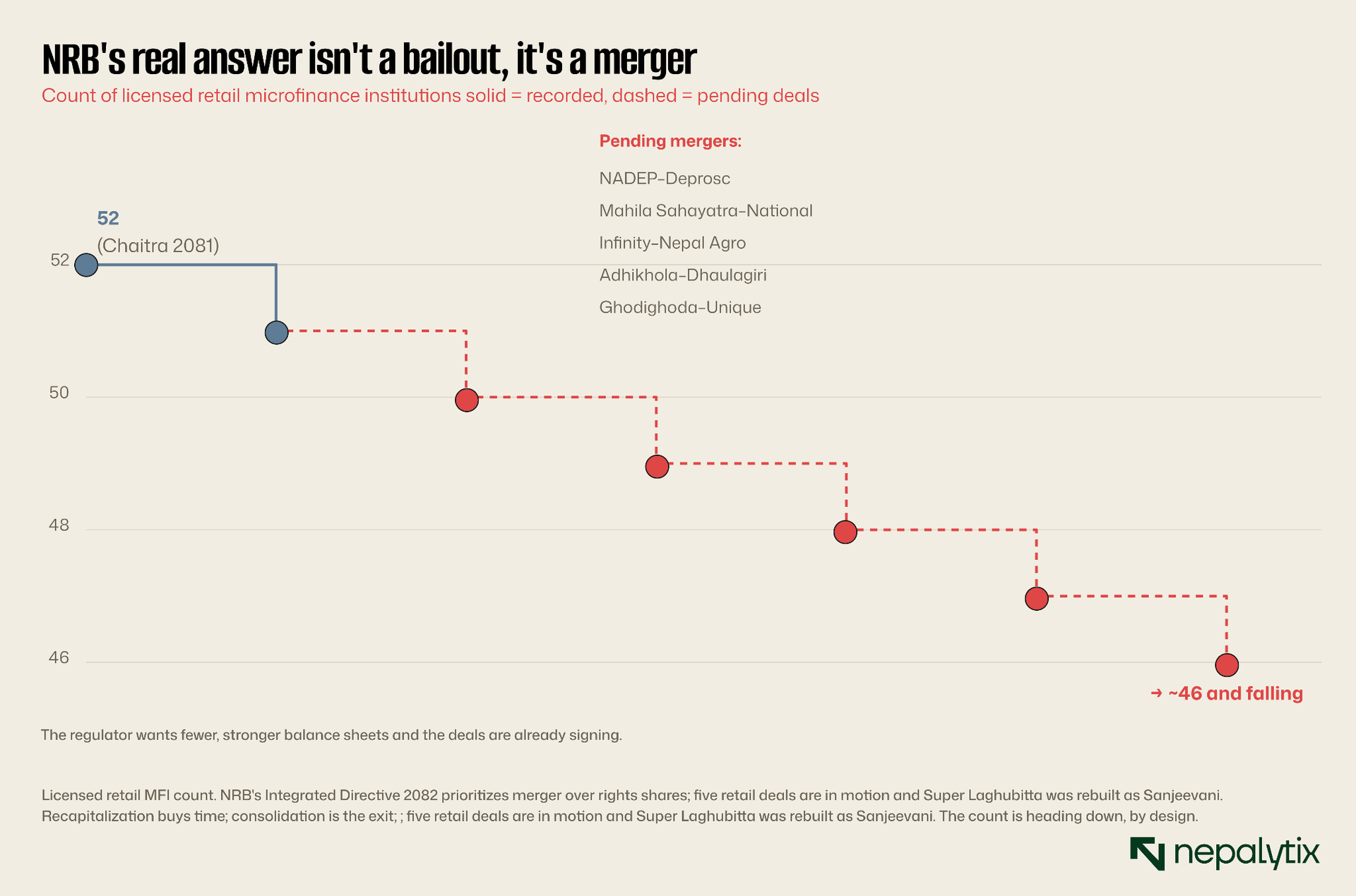

NRB's real answer is a merger, not a bailout

So what happens to the casualties? Not a bailout and reading NRB's actual policy rather than the headlines is the whole edge. The "rush to rights shares" is real but it is the second-best option the regulator tolerates, not the one it wants. NRB's Integrated Directive 2082 reaffirmed this January, is explicit: the central bank prioritises merger and acquisition over rights issues as the route to stronger capital and has done so across two directive cycles. It will clear a rights issue for an institution genuinely unable to hold its ratio despite real effort but it has drawn a hard line at institutions whose NPL runs above 20 percent, roughly double the average, with no recovery to show. Fresh equity for a lender that is far gone is not a rescue; it is handing the loss to new shareholders.

What the regulator wants instead is fewer, stronger balance sheets and the deals are already signing: NADEP with Deprosc, Mahila Sahayatra with National, Infinity with Nepal Agro, Adhikhola with Dhaulagiri, Ghodighoda with Unique five retail mergers in motion trading halted on several while they close. And Super Laghubitta was not rescued as itself; it was recapitalised by banks converting their loan exposure into equity rebranded Sanjeevani, and dragged from minus 126 percent capital back to a positive 28. That is the template. The weak institutions do not recover. They disappear into stronger ones.

What it means for the investor

The reading is unsentimental. Microfinance is not a buy or a sell; it is a sorting problem. The sector average NPL, the average CAR, the sub-index every one of them is an average of two populations that are pulling apart, so owning "the sector" means owning the failures alongside the survivors in whatever weights the index happens to assign. The question that pays is not whether microfinance is cheap. It is which specific institutions have the reserves, the recovery discipline, and the funding cost to still be standing when the consolidation finishes and better still, to be the acquirer rather than the acquired.

Rights shares buy the weak ones time; they do not buy them a future because the thing that broke was not the balance sheet, it was the borrower. The model that assumed a borrower who could repay is gone and fresh equity does not rebuild it. What rebuilds this sector is subtraction and the subtraction has started.

The single number to watch from here is the sector's next NPL print. If 11.32 percent rolls over, the survivors re-rate first and hardest, and the gap between the two populations begins to close from the top. If it climbs again even the strong names get repriced alongside the weak because at that point the market stops believing the sorting is finished. Everything in this Signal reduces to that one line and it reports quarterly.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.