Nepal’s Microfinance Trap: How a Financial Inclusion Success Story Turned Into the Country’s Biggest Hidden Credit Risk

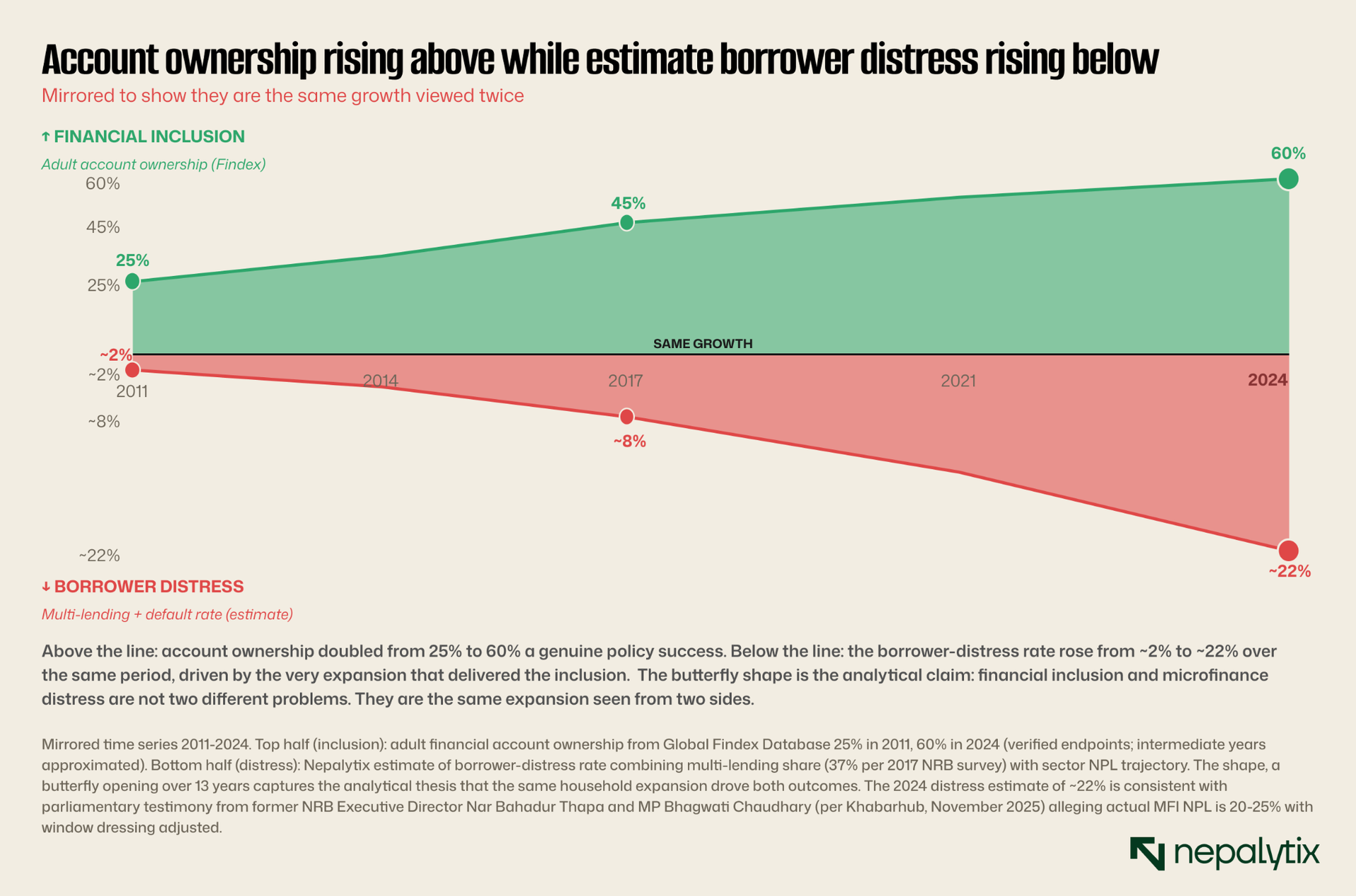

Nepal’s microfinance sector was once celebrated as the engine of rural financial inclusion, helping account ownership rise from 25 percent to 60 percent while tripling in size within six years.

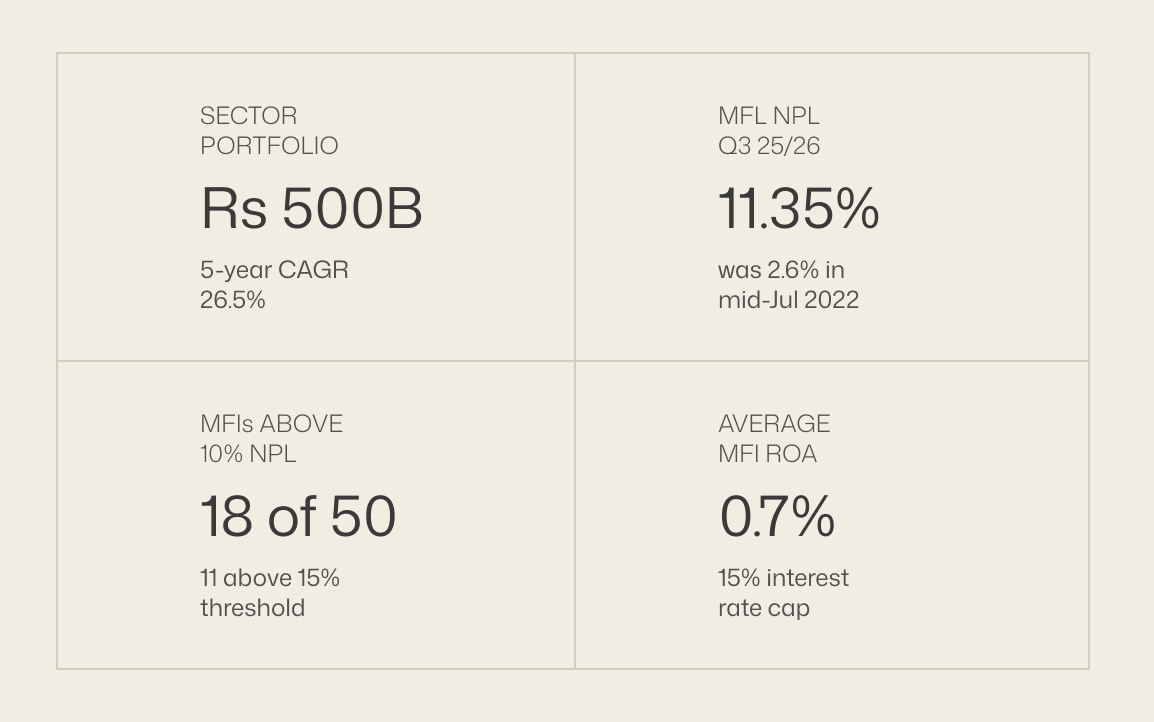

Nepal's microfinance sector grew from $1.8 billion in 2019 to $3.2 billion by April 2025, a 26.5 percent compound annual growth rate, faster than any other segment of the financial system. Through that growth, the country's account ownership doubled from 25 percent to 60 percent. By the third quarter of FY 2025/26, the same sector reported an average non-performing loan ratio of 11.35 percent. Eighteen of fifty listed institutions had NPL ratios above ten percent. The worst-performing reported above twenty-three percent. The poverty-alleviation success story has quietly become the financial system's most concentrated source of risk and one of the few sectors where the regulatory data, the political evidence, and the borrower testimony all tell the same story.

The borrower

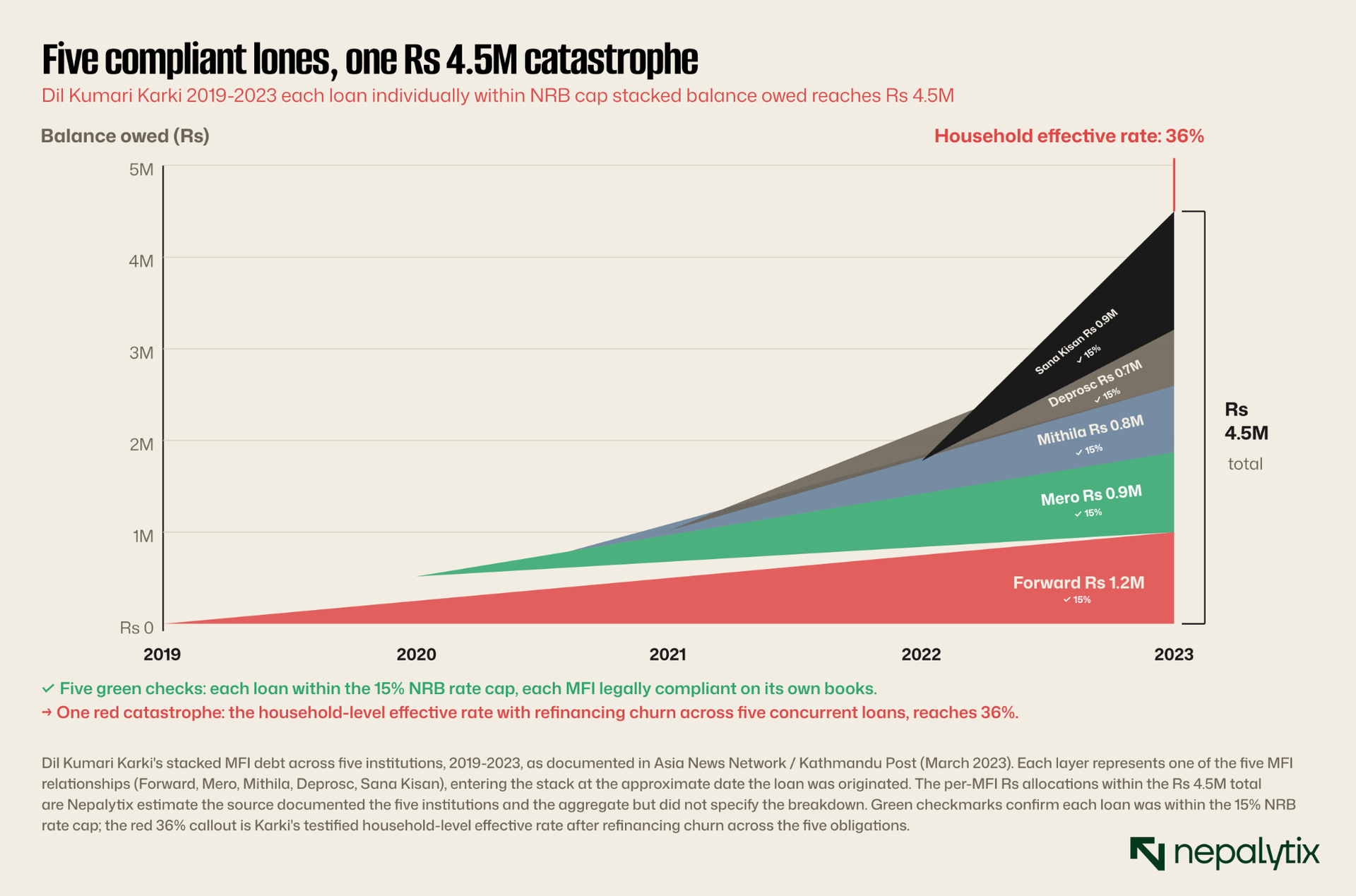

In March 2023, Dil Kumari Karki, once the owner of a small retail store in Rautahat, in the central Terai stood at a Kathmandu interaction session organized by the Society of Economic Journalists-Nepal (SEJON). She now washes dishes in Kathmandu. She had come to ask why she could not service her loans. She owed money to ten creditors. Five of them were registered microfinance institutions: Forward, Mero Microfinance, Mithila, Deprosc, and Sana Kisan. She had started four years earlier by borrowing Rs 100,000 from neighbors to open a small grocery shop. As her business expanded, then struggled, then failed, her debts compounded across additional informal lenders and then across the MFIs. By the time she spoke in Kathmandu, the total had reached Rs 4.5 million. The interest rates she was charged in practice, she said, ran as high as 36 percent per year when service fees, collection costs, and refinancing of older loans into newer ones were rolled into the effective rate. The chief executive of one major MFI present at the session disputed her arithmetic. He pointed to the regulatory rate cap: 15 percent, set by Nepal Rastra Bank, with an additional 1.5 percent service charge permitted. "Will any chief executive officer of a micro-finance institution dare to defy the NRB and face punishment?" he asked. The implication was clear: if the woman was paying 36 percent, the math must be wrong. The math was not wrong. It was simply taking place in a system where five lenders could be servicing one borrower, each charging her at or near the cap, with the proceeds of each new loan routed to service the existing ones, the headline rate respected at every individual institution while the borrower's actual cost compounded across the cluster of obligations. This is the geometry of the Nepali microfinance trap. It is not a story of any single rogue lender. It is what happens when the regulator caps the price but does not cap the number of lenders, when the sector triples in five years but the credit information system does not, and when an industry built on the moral mandate of inclusion is allowed to acquire the operational character of consumer debt without acquiring any of consumer debt's protections.

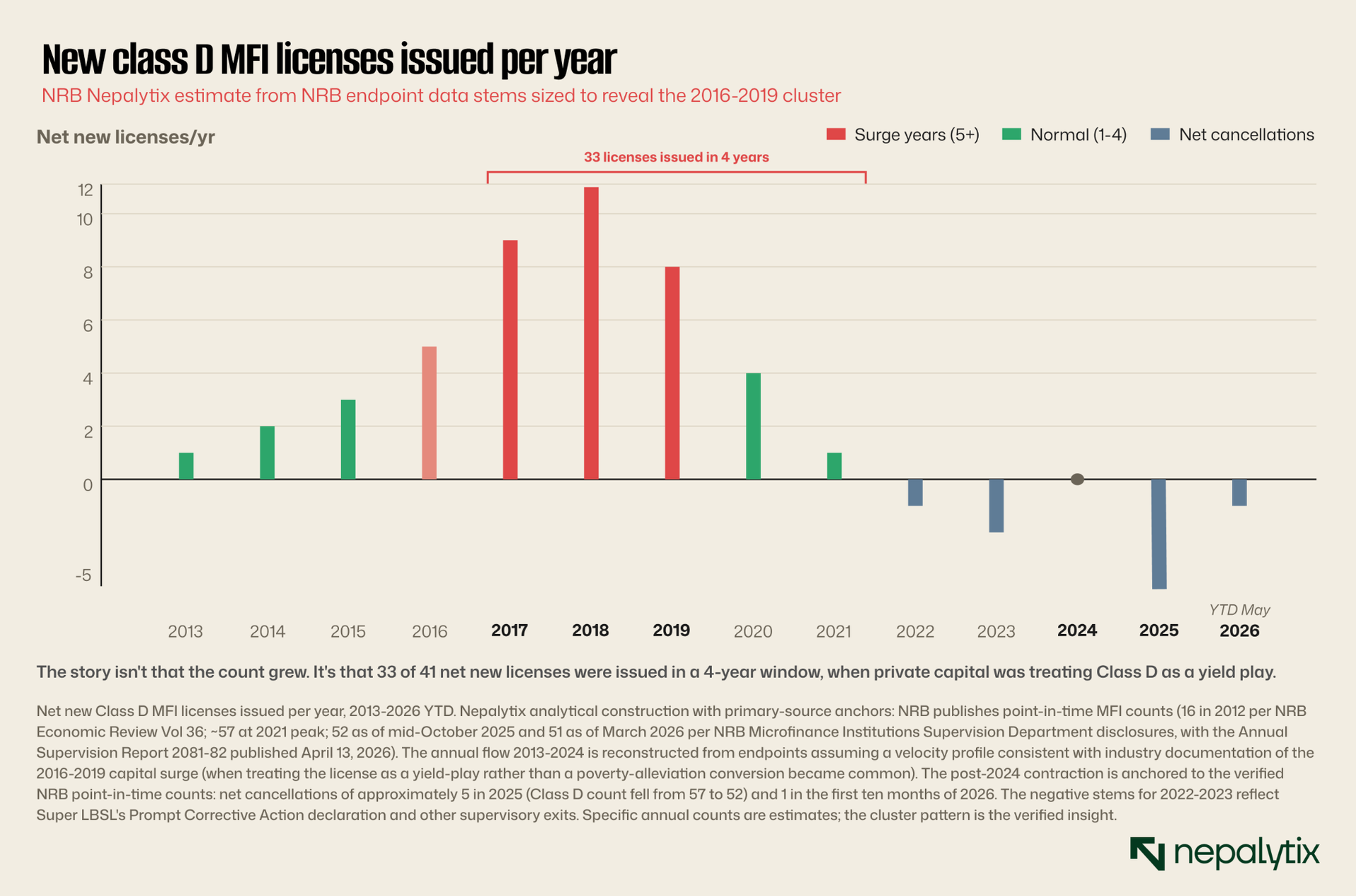

The institutional architecture is worth understanding because it shaped everything that followed. Nepal's central bank classifies licensed financial institutions into four tiers under the framework codified in Section 31 of BAFIA 2006 and continued in BAFIA 2017. Class A is the commercial banks. Class B is the development bank. Class C is the finance companies. Class D is the microfinance institutions designed, originally for the poorest segments and the most rural geographies, where the larger banks had no operational reach and no economic interest.

The legal foundation came in stages. The Banks and Financial Institutions Act (BAFIA) of 2006 first consolidated the four-tier framework Section 31 of BAFIA 2006 classified institutions as Class A commercial banks, Class B development banks, Class C finance companies and Class D microfinance institutions. BAFIA 2006 was superseded by BAFIA 2017, which is currently in force and continues the same classification structure. The Microfinance Development Bank category itself was created earlier, in the late 1990s, to permit NGO-style operators to convert into licensed deposit-taking institutions. The first such conversion was Nirdhan Utthan Microfinance Development Bank, transformed in 1998 from the Nirdhan NGO. That transformation became the template. The Class D license, for an organization that already had borrower relationships and field operations, was a low-friction way to become a regulated lender with access to wholesale funding.

By 2012 there were sixteen profit-oriented MFIs operating under Class D status. By 2024 there were fifty-seven. Most of the new entrants did not come from NGO conversions. They came from the entrepreneurial side of the financial system, private capital, sometimes promoted through existing commercial banking groups, treating Class D as a profitable sub-market with a regulated price and a captive client base. The sector's character changed quietly through this composition shift. The original logic was social-mission infrastructure for the unbanked. The new logic was a low-cost, high-volume retail lending operation in geographies the larger banks did not want to serve directly.

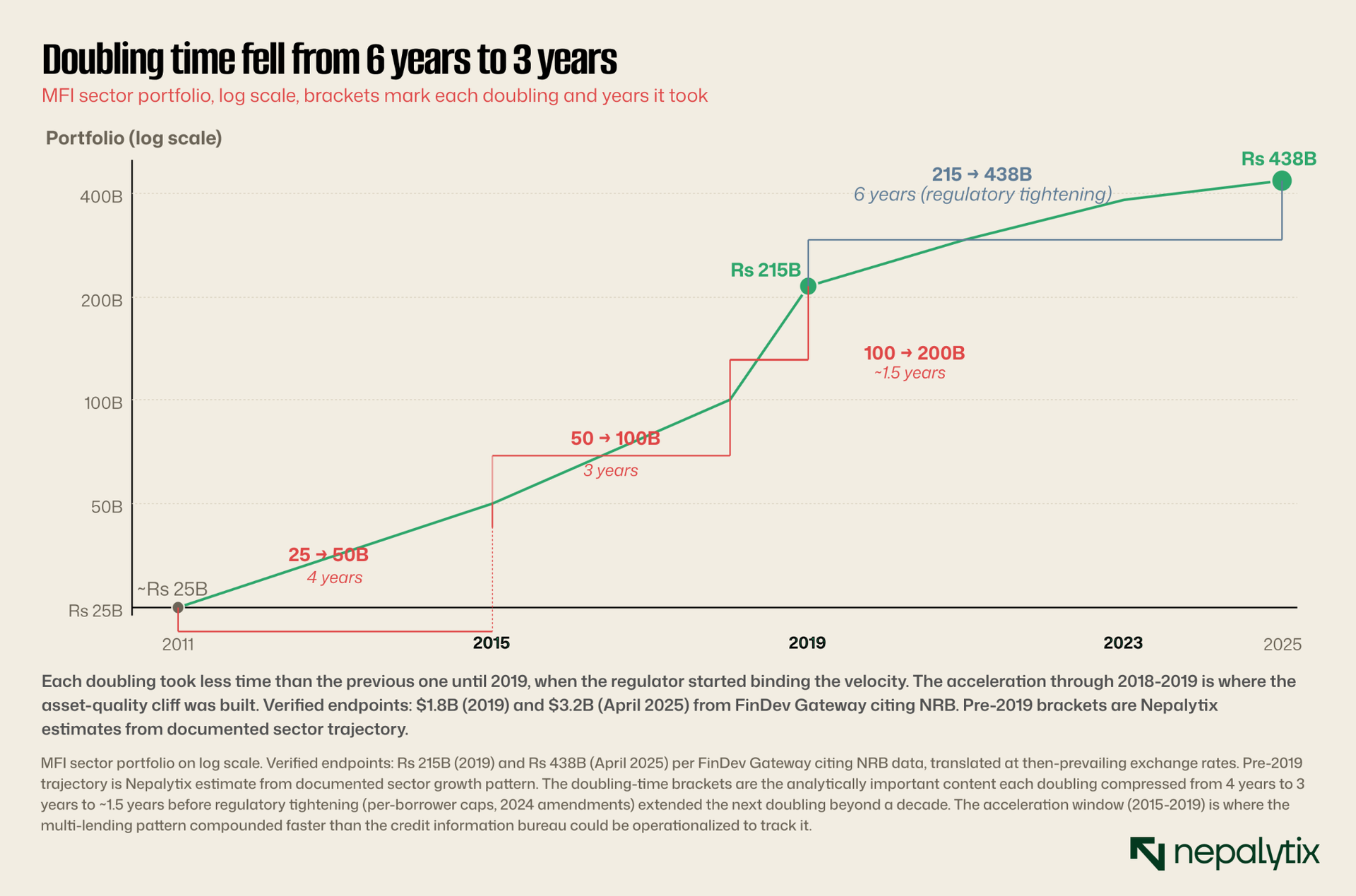

The sector portfolio grew correspondingly. In rupee terms, the verifiable data points are: April 2025 sector size of $3.2 billion (Rs ~438 billion at then-prevailing exchange rates) per NRB's Key Financial Indicators report cited by FinDev Gateway and the 2019 baseline of $1.8 billion (Rs ~215 billion at then-prevailing rates). The implied five-year CAGR between these two points is 26.5 percent. Earlier baseline figures including the Rs 50 billion approximate in 2015 sometimes cited in Nepal microfinance literature are not directly sourced in NRB consolidated data with the consistency that would let us pin down the pre-2019 trajectory precisely. Through this same period, the country's adult account ownership rate, measured by the Global Findex Database, rose from 45 percent in 2017 to 60 percent in 2024. Microfinance carried a substantial share of that financial inclusion success.

The financial inclusion success is real. It deserves recognition. The chart below shows account ownership doubling over thirteen years from one in four Nepali adults having any kind of formal financial relationship to three in five. Microfinance was the dominant channel through which that change reached women, rural areas, and small-scale enterprise. Any analysis of the current crisis that does not begin with that achievement is missing the central paradox of the sector.

The growth that wasn't really growth

The standard reading of MFI growth treats portfolio expansion as a measure of borrower expansion. If portfolio doubles, the assumption goes, financial access has roughly doubled. That assumption was already untrue in 2017 and it has been progressively more untrue since.

The 2017 NRB survey of microfinance borrowers conducted before the most aggressive growth years found that 37 percent of borrowers held loans from at least two MFIs simultaneously. The survey was not designed to identify the upper end of the multi-lending distribution. It did not ask how many borrowers held loans from three, four or five institutions. But the 37 percent baseline at a moment when the sector portfolio was approximately Rs 100 billion implies that a substantial share of the subsequent growth came from new lending against existing borrowers, not from acquisition of new borrowers.

The mechanism is straightforward once you understand the institutional pressures. Each MFI's loan officers were assigned monthly disbursement targets. Geographic exclusivity was not enforced, multiple MFIs could and did operate branches in the same ward. The credit information bureau covering microfinance was either nonexistent or non-functional for most of the growth period. When a loan officer needed to meet targets and the universe of new acquirable borrowers was already largely served, the path of least resistance was to lend to a borrower who already held loans from competing institutions.

From the borrower's perspective, this was useful in the short term. A new loan from MFI B could be used to service an outstanding balance at MFI A. The borrower's total debt grew. The pressure on any single MFI to recover its loan decreased temporarily because borrowers in a multi-lending arrangement were able to keep current on individual obligations by rotating through the available credit. The system masked deteriorating credit quality through this rotation for years.

What broke the rotation was a combination of three things. Saturation of the multi-lending capacity per borrower, there is a finite number of MFIs operating in any given ward and a finite number of loans the household economy can carry even if each loan is individually small. Regulatory restrictions on disbursement growth after 2023 when NRB began capping per-borrower exposure and limiting the number of lenders. And the 2023 anti-microfinance protests, which both reduced disbursement appetite at the MFIs and created a permissioned environment in which borrowers stopped servicing existing loans en masse.

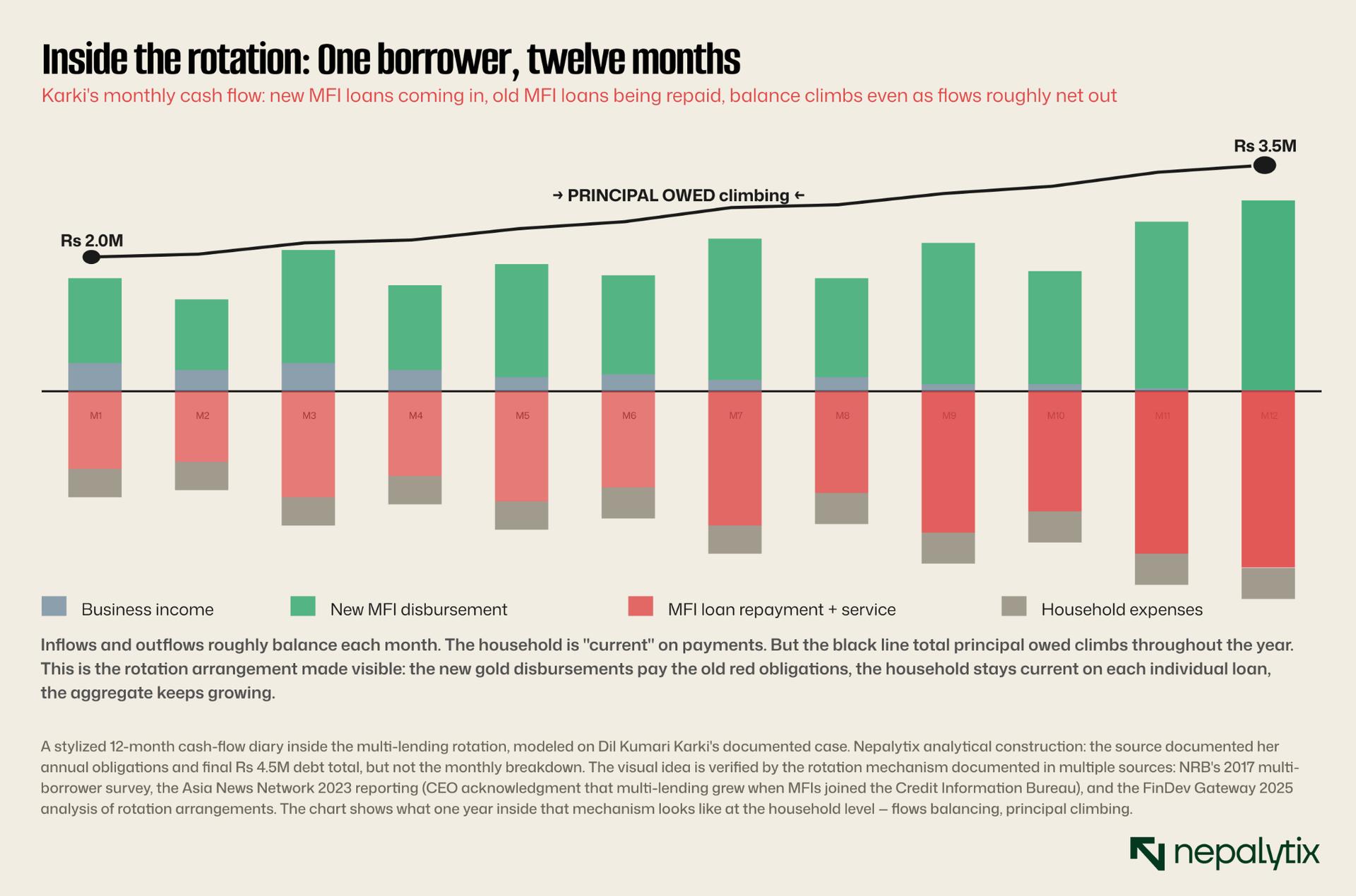

The chart below visualizes what the multi-lending pattern looks like at the level of a single documented case, the woman from the Kathmandu Post account whose loans across five registered MFIs accumulated to Rs 4.5 million over four years.

This is the structural pattern. Five institutions, each behaving legally and within regulatory caps, can produce an outcome for an individual borrower that no single institution could have produced on its own. The financial system regulators look at each MFI's books and find compliance with the price cap, loan-to-income guidelines and risk-weighting. The borrower experiences a debt service obligation that consumes most of her productive cash flow. Both perceptions are accurate. They are simply observing the same financial flows through different aggregation levels.

The institutional framework permitted everything. Nothing visible to any individual regulator was a violation. The geometry of the harm only appeared at the aggregation level the regulator was not looking at.

The geographic distribution of the multi-lending pattern is part of what made it self-reinforcing. The asset-quality data tells us where the trap was set hardest.

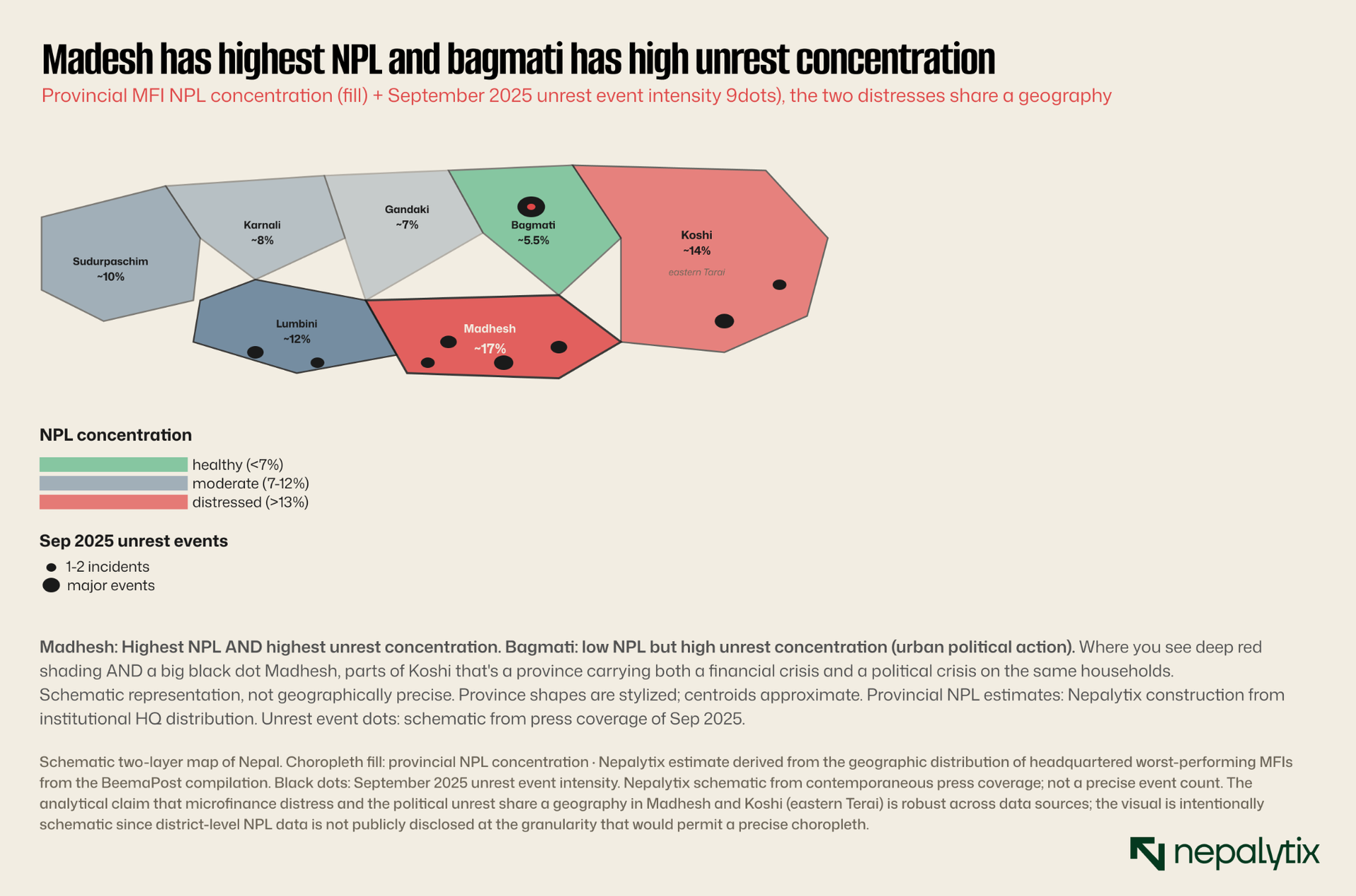

Terai, Sindhupalchok, the rural eastern district was hit the hardest

The microfinance crisis has a geography. The institutions reporting the highest NPL ratios operate predominantly in the southern Terai districts and the eastern rural belt. The institutions with the lowest NPL ratios concentrate in mid-hill geographies and urban-peripheral regions where alternative employment opportunities, remittance income, and tighter community social structures support repayment discipline.

The Terai concentration of distress reflects several converging factors. The Terai is Nepal's most population-dense rural region, with the highest density of branch operations across competing MFIs making multi-lending most prevalent. It is also the region most affected by the 2017 federal restructuring's distributional disputes, the 2023 agricultural distress from drought and floods, and the September 2025 political unrest's economic impact. The combination of dense MFI presence, multi-lending normalization and successive shocks to household cash flow produced the worst asset-quality outcomes.

The geographic concentration matters for policy choice. A managed-consolidation approach that allows the worst-performing institutions to fail through normal resolution mechanisms will disproportionately affect the Madhesh province where the institutional concentration is highest and the household income vulnerability is greatest. The political consequences of a Madhesh-concentrated MFI collapse, given the province's distinct political identity and the political party representation it holds, are substantial. Any resolution path that emerges in the next quarters will have to address the geographic incidence of losses, not just the aggregate.

Bagmati's relatively low estimated NPL reflects the structural difference between urban and rural microfinance. Kathmandu Valley households generally have multiple income sources: formal employment, remittance receipt, small enterprise that provide cash-flow buffers against any single shock. Rural Madhesh and Tarai households often depend on a single seasonal agricultural cycle, with any disruption translating directly into repayment failure. The MFI sector built its growth on serving the latter group; the asset-quality crisis is therefore concentrated where the borrower vulnerability is structural.

Inside the borrower's book

To understand why the regulatory caps did not protect the borrower, it helps to walk through what her actual monthly cash obligations looked like. The following decomposition is a stylized representation, but it follows the structure documented across multiple Kathmandu Post and Himalayan Times accounts of similarly-situated borrowers.

Take the case as documented. The Rs 4.5 million total spans ten creditors of which five are registered MFIs. The published source does not break out the specific rupee allocation between the five MFI creditors and the five non-MFI creditors (cooperatives, moneylenders, family); for analytical purposes Nepalytix assumes the MFI share is roughly Rs 3.0-3.5 million, consistent with the proportionality of loan sizes across all ten creditors were broadly similar. Each of the five MFI loans carries a stated rate of 15 percent per annum. Each loan carries an additional 1.5 percent service charge, permitted under NRB rules. Each loan carries refinancing arrangements where, when a tenor expires, the loan is renewed with the borrower receiving a top-up amount that exceeds the original principal. The renewal generates a fresh service charge.

The combined effective rate, calculated honestly, is the sum of: (a) the stated 15 percent on each outstanding balance, (b) the 1.5 percent service charge applied at issuance and renewal, (c) the additional interest accrued on top-up amounts before the borrower has access to them, (d) collection costs and field-visit charges that some MFIs build into the borrower obligation. Across a borrower with five concurrent MFI relationships, each renewing on a different cycle, the combined effective rate frequently runs at 30 to 40 percent annualized. The 36 percent figure the borrower cited is within the documented range.

None of this is hidden, exactly. The NRB Directive No. 1.081 of the Unified Directive 2081 specifies the maximum permissible rate at each individual MFI. It does not specify a maximum permissible aggregate rate across all MFIs serving a single household. The aggregate is the regulatory blind spot that produces the lived experience.

This decomposition is what the rate-cap policy did not anticipate. When NRB capped the rate at 15 percent in 2014 and reaffirmed it through subsequent unified directives, the intent was to prevent the predatory pricing that microfinance globally Mexico, Cambodia, Bangladesh had produced. The cap is genuinely lower than what an unregulated market would have charged Nepali low-income borrowers. But the cap is also the binding constraint on per-loan revenue, and the binding constraint produced a sector that could only generate adequate returns through volume: more loans per institution, more institutions per ward, more loans per borrower.

The behavior the regulator wanted to suppress, predatory rates per loan, was suppressed. The behavior the regulator did not consider, predatory volume per borrower, was incentivized. The structural arithmetic is brutal.

The next layer of the analysis is what this debt service obligation actually looks like against a typical borrower household budget. The arithmetic is what made repayment failure contagious rather than idiosyncratic.

What Rs 4.5 million looks like in a Terai household budget

To understand why repayment failure became contagious rather than idiosyncratic, the analysis has to come down to the level of a household budget. Take the documented case, the woman from eastern Terai with Rs 4.5 million across ten creditors. Of that, approximately Rs 3.5 million was MFI debt across five institutions. At the 36 percent effective rate that the borrower testified to, the annual debt service obligation on Rs 3.5 million is approximately Rs 1.26 million. That is the cash flow she had to generate just to keep the existing arrangements rotating before any principal repayment, before any household consumption before any reinvestment in the small business that originally drew her into the lending arrangement.

The arithmetic against typical borrower household income is mathematically unservable. A rural Terai household at the income deciles where MFI borrowing concentrates small landholding agriculture combined with a household micro-enterprise generates cash flow in the low hundreds of thousands of rupees annually under normal conditions. A Rs 1.26 million debt service obligation against income at that scale leaves four options: (a) generate substantially more business income than historical pattern, (b) acquire new debt to service existing debt, (c) liquidate productive assets, (d) default. For most of the documented multi-borrower cases, option (b) multi-lending was the operational path through 2020-2023. Once it broke, option (d) followed by structural necessity. The specific income distribution figures that would let us calibrate this precisely are not in the published NRB or Central Bureau of Statistics data at the granularity needed; the directional claim is robust across any reasonable assumption about Tarai household income at the third-and-fourth deciles.

The aggregation of this household-level mathematics across 2.66 million borrowers is the macro number visible in the NPL ratio. The 11.35 percent sector-wide figure understates the borrower-level distress because it counts loans, not borrowers. A multi-borrower household defaulting on five concurrent loans appears five times in the loan-count denominator but represents one defaulting household. The borrower-level NPL counting households rather than loans is likely materially higher than the loan-level NPL the regulator publishes.

This is the analytically critical point. When the regulator reports 11.35 percent NPL, the implicit framing is that 88.65 percent of the loan book is performing. The borrower-level reading is closer to: of households with MFI obligations, approximately 20 percent are in active default, and an additional unknown share are servicing loans through rotation arrangements that will fail when the next shock arrives. The institutional view and the household view are looking at the same financial flows but classifying them differently. The institutional view is correct for individual MFI solvency analysis. The household view is correct for understanding the underlying credit quality and the political pressure that the sector now faces.

The female-headed-household concentration

One further dimension deserves explicit treatment because it shapes the policy options. The Nepali microfinance model is by design and by regulatory mandate, predominantly female-borrower-focused. The Grameen-derived group-lending model that NRB authorized through the Class D framework requires women's group formation as the operational unit with the loans extended through the group rather than to individual male household heads. The expected social benefits, women's economic empowerment, household consumption smoothing, agricultural input financing for women's enterprises were the explicit rationale for the regulatory framework.

By 2024, women constitute the substantial majority of MFI borrowers; figures in the 85-95 percent range are commonly cited in Nepal microfinance literature, though the precise current figure is not directly published in NRB Key Financial Indicators reports. The 2.66 million borrower figure cited above is therefore approximately 2.45 million women. The geographic concentration in Madhesh and Terai districts means the concentration is also in regions where female labor force participation outside of agriculture and household production is structurally low where women's autonomous income generation depends substantially on the very small enterprises the MFI loans financed and where the cultural pressure of group repayment obligation produces what the academic literature has called "the joint liability burden."

This matters for policy choice because any debt write-down or restructuring program that emerges will have to address the gender concentration explicitly. A neutral pro-rata write-down across all MFI borrowers transfers economic resources predominantly to women in the lowest income deciles of Terai households, a politically and economically defensible target. A write-down that excludes any subset based on income test, asset test, or geographic criterion runs into the gender-distributional issue immediately. The political momentum behind borrower relief, in this respect, has a structural feature that distinguishes it from comparable debt relief debates in male-borrower-concentrated sectors.

The interest-rate-cap paradox

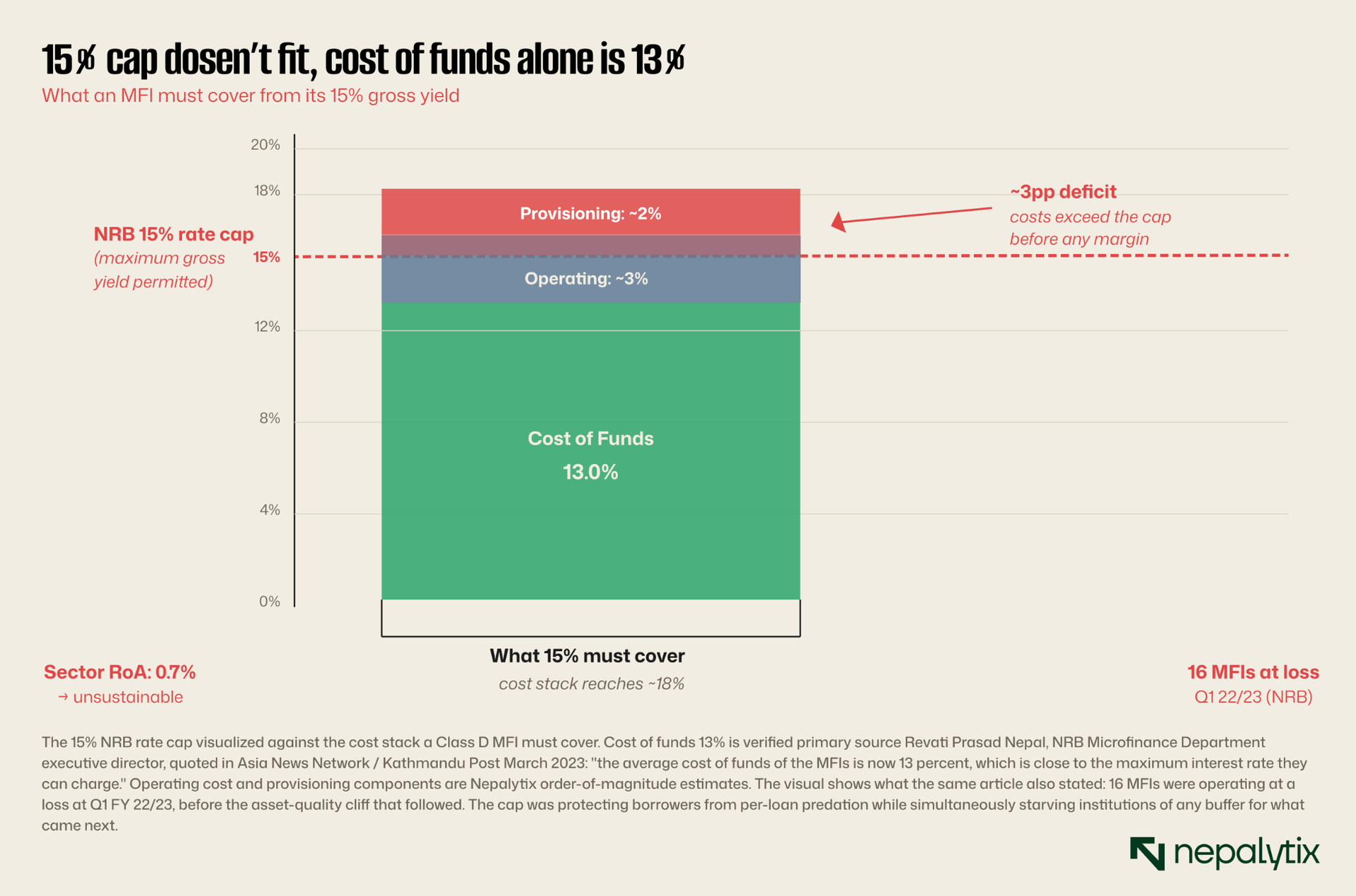

The companion arithmetic to the borrower's effective rate is the lender's profitability. The 15 percent ceiling that protected borrowers from any single MFI's predatory pricing produced, at the institution level, a sector unable to absorb defaults from a normal cyclical downturn much less an asset-quality shock of the scale that arrived in 2023-2026.

Consider the cost stack of a typical Class D MFI. The 15 percent gross yield on lending must cover: (a) the cost of wholesale funding from commercial banks or apex institutions, typically 7-9 percent under Nepal's commercial banking spreads; (b) the cost of field operations loan officers, branch infrastructure, weekly group meetings, transport to remote villages, which can run 3-4 percent of portfolio in geographically dispersed operations; (c) head-office administrative costs of 1-2 percent; (d) loan loss provisioning, which under normal cycle conditions should run 1-2 percent of portfolio. The arithmetic works only in two cases: institutions with very efficient operations and wholesale funding access at the low end of the range, or institutions absorbing the field-cost economies of scale at very large portfolio size.

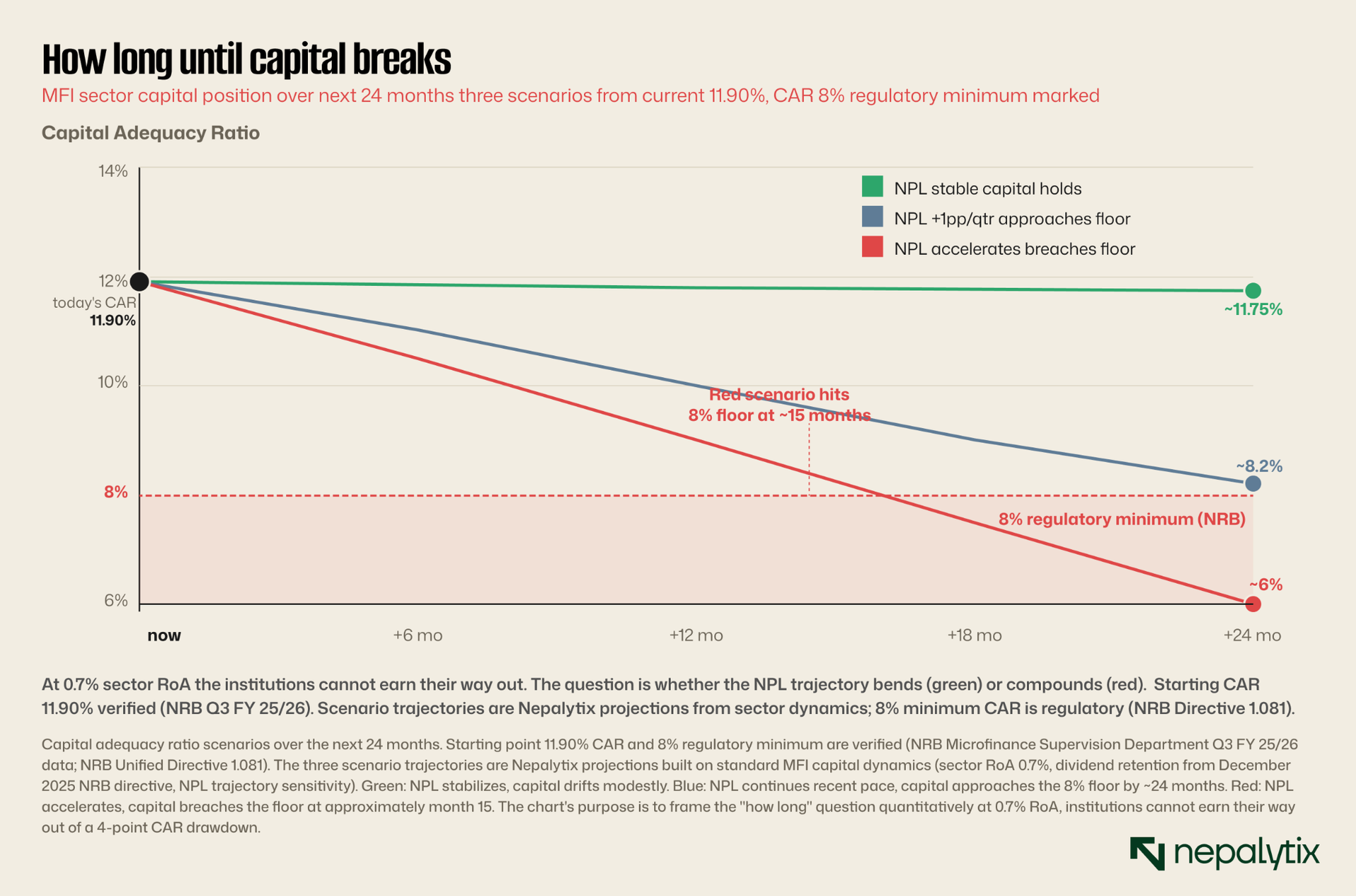

Most Nepali MFIs are neither. The April 2025 NRB Key Financial Indicators report showed an aggregate return on assets of approximately 0.7 percent across the 48 MFIs covered. Only three institutions reported ROA above 2 percent, the rough threshold at which sustainable capital generation occurs after considering loan-loss volatility. Twenty-three of the 48 reported ROA below 1 percent. Fifteen were in the 1-2 percent range.

A sector with 0.7 percent average ROA has approximately one year of buffer against a 1 percent NPL deterioration and that calculation assumes no further provisioning, no withdrawal pressure, no new loan disbursement collapse, and a stable wholesale funding cost. In practice, when the NPL shock arrived, none of these conditions held. The sector entered the crisis without earnings capacity to absorb the losses.

The 0.7 percent return on assets across the sector raises a separate question about who actually carried the funding burden. The wholesale chain that financed the Class D expansion is the next layer of the structural picture.

Where the money came from before it reached the borrower

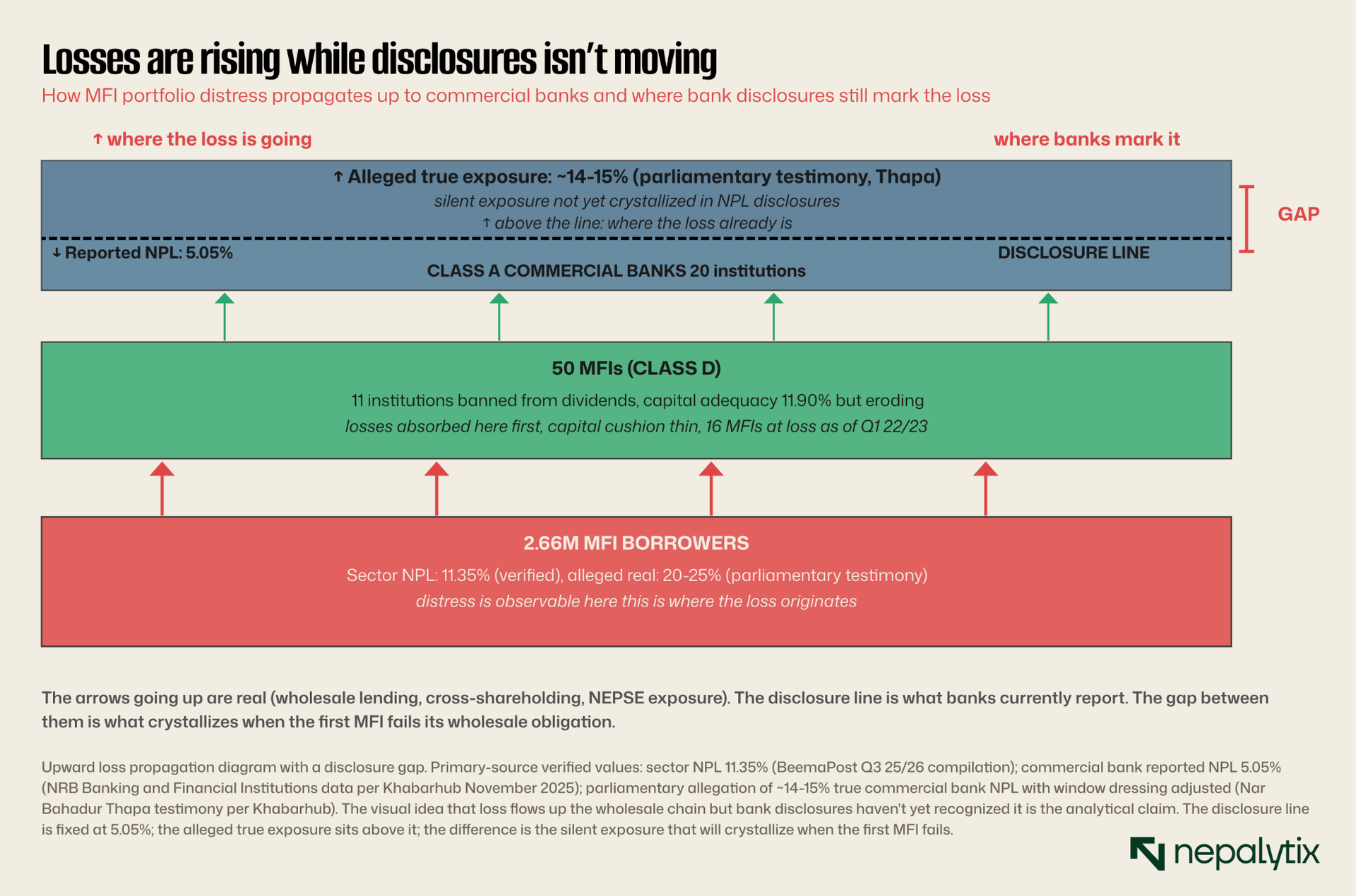

To complete the structural picture, the wholesale funding chain through which Class A commercial banks financed the Class D microfinance expansion deserves explicit visualization. The Rs 500 billion MFI portfolio at the current peak did not materialize from MFI capital alone. Most of it was financed through commercial bank wholesale lending, deposit-taking at the two licensed deposit-taking MFIs (Chhimek and Nirdhan), wholesale lending from apex institutions (Sana Kisan Bikas, RSDC, First) and equity injections through the listed MFI capital market.

The wholesale lending share is the most opaque and the most consequential for the broader financial system. Commercial banks holding wholesale loans to MFIs do so under standard credit agreements; when an MFI's underlying loan book deteriorates, the wholesale lender is initially insulated by the MFI's capital. If the capital is depleted as the dividend ban and provisioning pressure suggest is happening the wholesale lender then has direct credit exposure. None of this currently shows up in commercial bank NPL disclosures because the wholesale loans are still being serviced by the MFIs, which are using deposits and equity capital to maintain interest payments even as the underlying portfolio deteriorates.

The November 2025 parliamentary testimony argument that BFI NPLs are window-dressed at 5 percent versus an actual 14-15 percent is therefore partly an argument about wholesale-lending evergreening at the Class A level. The mechanism mirrors the multi-lending pattern at Class D. Commercial banks are not, individually, falsifying NPL disclosures. They are continuing to classify wholesale loans to MFIs as performing because the MFIs are continuing to pay interest. The MFIs are continuing to pay interest by drawing down capital. The chain holds until one of the MFIs in the chain stops paying at which point the wholesale exposure crystallizes for all the connected commercial banks simultaneously.

This is the systemic concern that should keep the Nepali financial system's regulators up at night. The microfinance sector NPL of 11.35 percent is not just a Class D problem to be resolved through consolidation. It is the visible tip of a structural credit-quality issue that the wholesale funding chain has thus far suppressed. The longer the structural reckoning is deferred, the larger the eventual transmission. The Cambodia-style managed consolidation works only when the wholesale chain is honestly disclosed at the time of the consolidation. The Andhra Pradesh-style collapse occurs when the wholesale chain crystallizes simultaneously across multiple commercial banks because the underlying MFI deterioration was deferred too long.

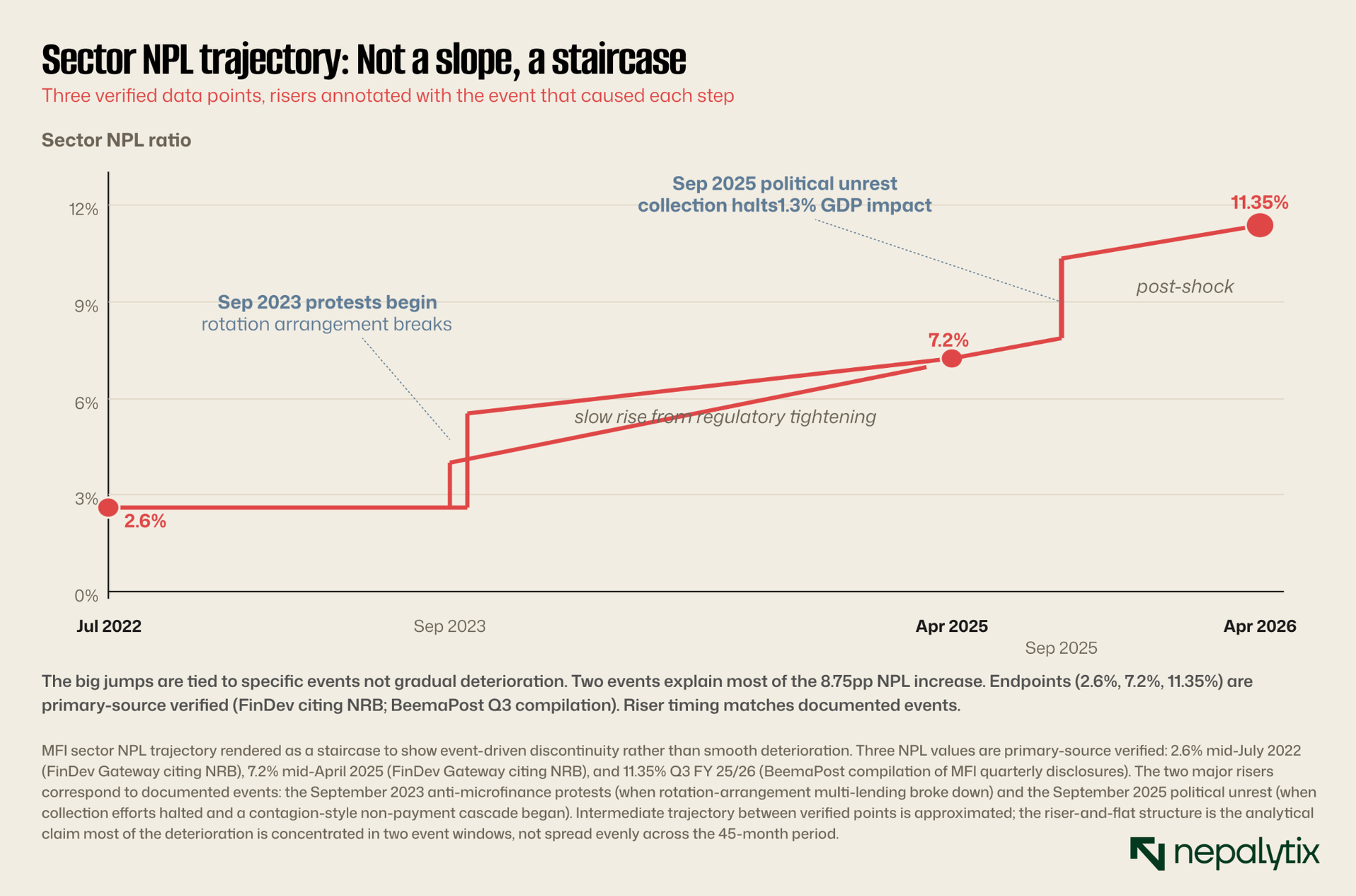

The asset-quality cliff from 2.6 percent to 11.35 percent in 33 months

The trajectory of microfinance NPLs over the last three years is the steepest deterioration of any regulated lending category in Nepal's recent financial history. The starting point, in mid-July 2022, was a sector NPL ratio of 2.6 percent comparable to commercial banks and slightly above developmental banks. By mid-April 2025, the ratio had risen to 7.2 percent. By the end of the third quarter of FY 2025/26 mid-April 2026, the average across the 34 MFIs that had reported third-quarter results stood at 11.35 percent.

Each step in the trajectory reflects a distinct phase of the crisis. The 2.6 to 4.5 percent move between mid-2022 and mid-2023 was driven by the early phase of the anti-microfinance protests and the first signs of multi-borrower distress. The 4.5 to 7.2 percent move between mid-2023 and mid-April 2025 reflected the disruption from increasingly aggressive borrower advocacy, the regulatory tightening of lending norms that constrained renewals, and the cumulative effect of the rotation arrangements unwinding. The 7.2 to 11.35 percent move in the final twelve months reflects something more structural: the September 2025 political unrest, the collapse in disbursement growth that prevented further rotation, and the realization across the sector that loan-recovery efforts could not proceed in the political climate that had emerged.

The pace of the deterioration matters as much as the level. In banking analysis, a 1 percentage point NPL move in a year is unusual; a 2 percentage point move signals systemic stress; a 4 percentage point move in twelve months which is what the sector delivered between mid-April 2025 and mid-April 2026 is the trajectory of a category-level crisis, not a portfolio-quality drift. For comparison, Nepali commercial banks' reported NPL ratio over the same window moved from approximately 4.0 percent to 5.2 percent, a 1.2 percentage point move. Development banks moved roughly half that amount. Finance companies, the Class C tier, moved approximately 2 percentage points. The microfinance sector's 4-point move stands alone among regulated lending categories in scale and in the absence of an identifiable single-cause shock, no commodity price collapse, no currency event, no banking-sector contagion. The drivers are structural rather than cyclical, which is what makes them durable.

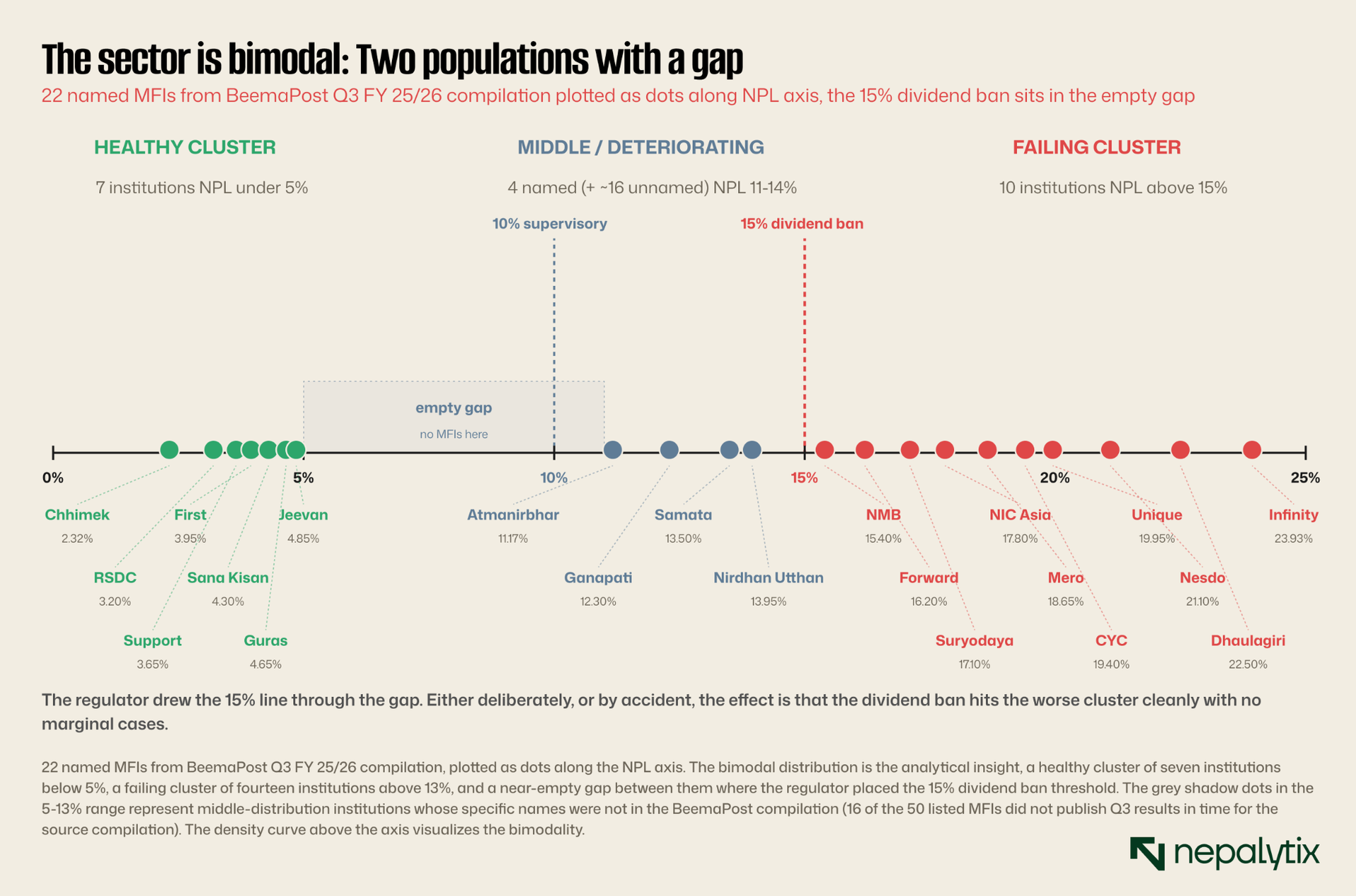

The 11.35 percent average masks a wide distribution. The dispersion across institutions is the deeper problem because it identifies where the systemic risk is concentrated. The third-quarter readings published by 34 of the 50 listed MFIs reveal a sector in which the worst-performing institutions have NPL ratios above 20 percent territory in which traditional banking analysis would describe the institution as functionally insolvent absent immediate recapitalization.

The eighteen MFIs above the dividend threshold

The chart below shows what the sector actually looks like at the institution level in Q3 FY 25/26. Each row is one MFI. The bars are sorted from worst to best NPL ratio. The dashed line at 15 percent is the regulatory threshold NRB introduced in December 2025: an MFI with NPL above this level cannot distribute dividends to shareholders. The dashed line at 10 percent is the supervisory escalation threshold under NRB Unified Directive 2081.

The dispersion is the analytically important fact. The sector average of 11.35 percent reflects an arithmetic mean across institutions with radically different exposure. The eleven institutions above the 15 percent threshold collectively represented by Nepalytix estimate, since institution-level portfolio data is not aggregated in published NRB disclosures at this granularity roughly Rs 80-100 billion of portfolio, concentrated in geographies where multi-lending was densest and political organizing was strongest. The seven institutions below 5 percent NPL represent a different microfinance typically older, larger, with disciplined credit standards, more diverse funding, and either public-deposit-taking status that imposed additional regulatory scrutiny or wholesale-only operations that selected for better borrowers through intermediary cooperatives.

The split is also striking along the public-deposit dimension. Of the only two MFIs licensed to accept deposits from the general public, Chhimek at 2.32 percent NPL and Nirdhan Utthan at 13.95 percent NPL represent opposite ends of the distribution. The public-deposit license carries the highest regulatory standards in the Class D framework. The fact that one institution operating under those standards is delivering the best asset quality in the sector while another is near the dividend ban speaks to the dispersion in management quality across the licensed group.

The dispersion across institutions was visible to one set of observers well before it was officially acknowledged in regulatory disclosures.

The NEPSE signal that arrived early

One source of information about the microfinance sector's actual condition that has been underappreciated is the listed equity market. Many of Nepal's MFIs are listed on NEPSE and the share prices of the worst-performing institutions have been pricing in the asset-quality cliff for considerably longer than the regulatory disclosures have acknowledged it.

From the 2021-2022 sectoral peak, NEPSE's microfinance sub-sector index has declined materially while the broader NEPSE index has held up better the specific magnitude of decline shown in some Nepalytix tracking varies by measurement window and is not from a single official NEPSE microfinance sub-index publication; the directional claim that MFI equities have underperformed substantially is robust across data sources. The dispersion across individual MFIs has been wide. Chhimek Microfinance, with the sector's lowest current NPL ratio of 2.32 percent, has traded relatively stably and continues to attract institutional buying interest at current levels. The institutions at the worst end of the NPL distribution Mero, Forward, Infinity have traded at fractions of book value, with implied market expectations of substantial future losses.

The equity-market early warning signal raises an uncomfortable question about the regulatory framework's information processing. The same financial data that NRB's supervision department was reviewing was also publicly disclosed and being priced by capital markets analysts and institutional investors. The market reaction of multiple compression, declining trading volumes and sustained price discovery downward was visible to anyone reading NEPSE data through 2022, 2023, and 2024. The regulatory response did not align with the market response until December 2025, when the dividend ban directive was issued. The asymmetry suggests that NRB was either receiving worse information than the market was generating, was processing the same information more slowly, or was making a deliberate choice to wait for political conditions before acting. None of those readings is reassuring for the regulator's information architecture.

The recent equity-market activity is also informative. Following the December 2025 directive, the share prices of the eleven dividend-banned institutions saw further declines as expected, but several of the institutions in the 10-15 percent NPL range — particularly Nirdhan Utthan saw equity-market buying interest, likely from investors interpreting the dividend ban threshold itself as a clarifying signal that institutions below the threshold remain investable. Whether this market positioning is correct depends on whether the next regulatory tightening cycle preserves the 15 percent threshold or moves it lower.

The regulatory chronology

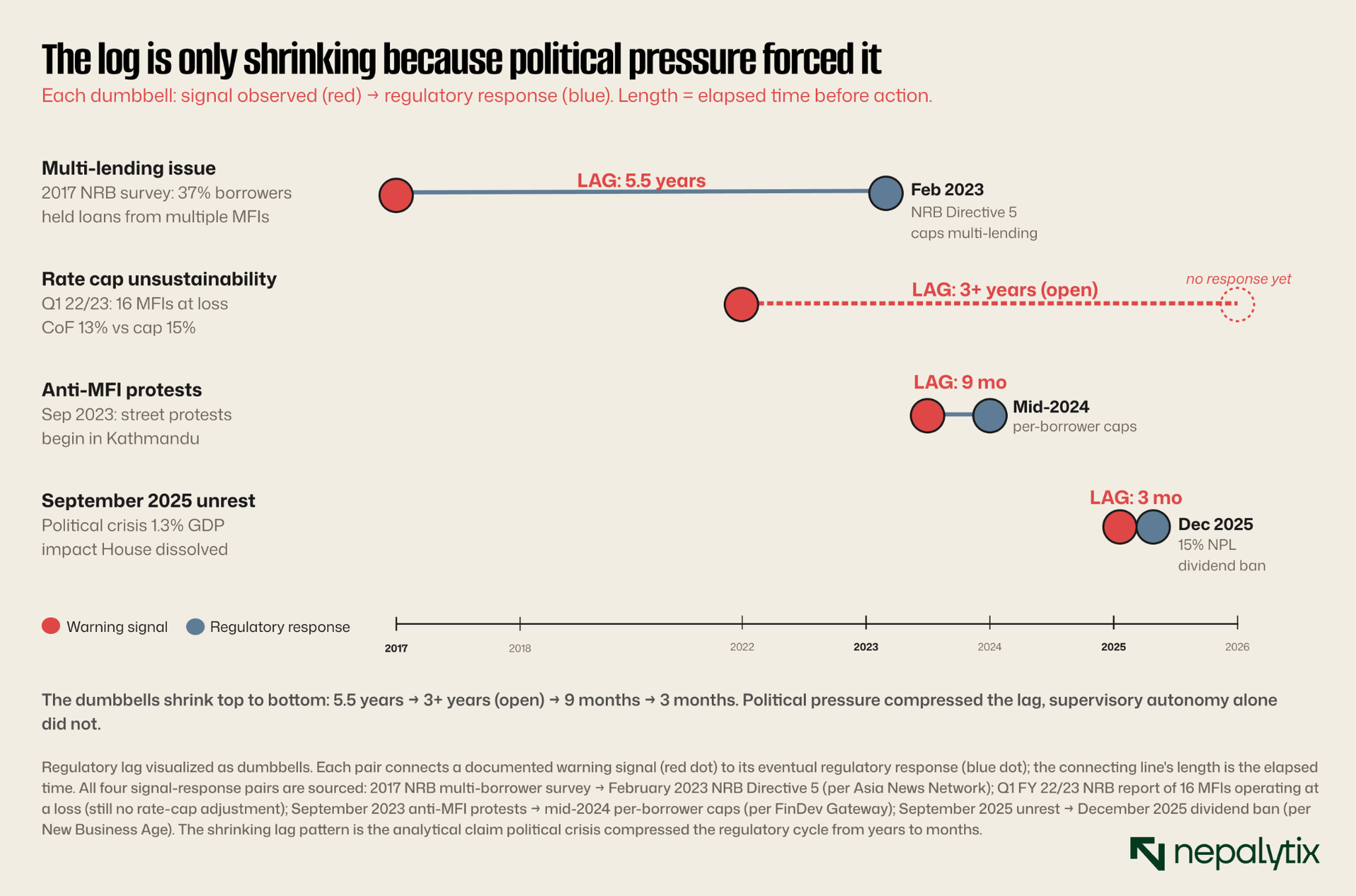

The regulatory response to the developing crisis is a study in lagged action. Each major intervention came after the relevant warning signs had been visible to NRB's supervision department for at least one full quarterly reporting cycle and in some cases for years.

The first warning, the 2017 NRB survey finding that 37 percent of borrowers held loans from multiple MFIs, did not produce a binding regulatory restriction on multi-lending until 2024 seven years later. By then, the multi-lending pattern was structurally entrenched and the borrowers who would default were already in distress.

The second warning, the early-2023 borrower protests, produced a year of regulatory deliberation rather than action. The 15 percent rate cap was reaffirmed but not extended downward. The credit information bureau was discussed but its operational coverage of microfinance remained limited. The interest rate cap remained the binding constraint on MFI profitability, but no operational support, wholesale funding facilities, capital injection mechanisms, supervisory forbearance frameworks were introduced to help institutions absorb the developing asset-quality stress.

The third warning, the rising NPL trajectory through 2023 and 2024, produced limited supervisory engagement. NRB began publishing the microfinance off-site supervision reports more visibly in 2024-2025 and the Microfinance Supervision Department took a more active role in problematic institution oversight. Super LBSL was declared a problematic institution and placed under Prompt Corrective Action, the most aggressive supervisory intervention available short of license cancellation. But the action was limited to one institution at a time the sector-wide indicators were already deteriorating rapidly.

The December 2025 directive barring MFIs with NPL above 15 percent from any dividend distribution was the first sector-wide regulatory action commensurate with the scale of the problem. It immediately disqualified eleven institutions from rewarding shareholders. It signaled to the listed MFI market, where many of these institutions are traded on NEPSE, that the regulator no longer considered the existing capital base sufficient for continued distribution. The dividend disqualification also forced institutions to retain earnings as a buffer against the further provisioning of deteriorating asset quality demands.

But the action came after the cliff. The NPL ratio that triggered the policy was a fact set in motion by years of accumulated stress; the directive could prevent further capital depletion but could not undo the losses already embedded in the loan book.

What Bangladesh, Cambodia, and India teach about the trap

The pattern Nepal is currently traversing is not novel. Microfinance globally has produced asset-quality cliffs in three notable previous cases: Bangladesh in 2010-2011, Andhra Pradesh in India in 2010-2011, and Cambodia in 2019-2023. Each crisis differs in mechanism but shares the structural features: rapid sector growth, multi-lending, regulatory price cap or interest restriction, and a political moment that crystallized the borrower discontent into mass non-repayment.

The Bangladesh case is the closest analog to Nepal's current position. The Grameen Bank ecosystem and its peer institutions grew the Bangladesh microfinance portfolio from approximately $500 million in 2000 to $3.5 billion in 2010 at a CAGR of approximately 21 percent, comparable to Nepal's 26.5 percent over 2019-2025. By 2010, evidence of multi-lending was widespread; the political moment came not from organized protests but from a Norwegian documentary alleging that Grameen had misappropriated donor funds. The Bangladeshi government's response was the dismissal of Muhammad Yunus from his Grameen leadership position and the imposition of a 27 percent effective rate cap, down from the implicit 35-45 percent that had been the working rate previously. The Bangladesh sector survived but stopped growing for nearly five years.

The Andhra Pradesh case is the more cautionary one. The state's MFI sector had grown from approximately $400 million in 2005 to $1.5 billion by 2010 and crashed catastrophically when the Andhra Pradesh state government, responding to a wave of borrower suicides attributed to aggressive MFI collection practices, passed legislation that effectively halted private MFI lending in the state. Repayment rates fell from 99 percent to under 20 percent within six months. The MFI sector in Andhra Pradesh did not recover. Major players SKS Microfinance (now Bharat Financial), Spandana, Trident Microfin suffered losses that took a decade to rebuild from.

The Cambodia case is the most current. From approximately $1.5 billion in 2014, the Cambodian microfinance sector grew to over $10 billion by 2022 a 26 percent CAGR almost identical to Nepal's. Borrower over-indebtedness reached the point where the World Bank in 2022 estimated that the average rural Cambodian household owed more than 1.2 times annual household income to MFIs alone, plus additional informal debt. The political environment in Cambodia did not produce the kind of organized protest movement seen in Nepal, but the regulatory response was forceful: the National Bank of Cambodia introduced strict per-borrower exposure limits, restricted growth in MFI portfolios to single-digit percentages, and forced consolidation of weaker institutions.

The lessons from these three cases are practical. Bangladesh, by recognizing the looming crisis early, the big four MFIs decelerated organically in 2008 before regulatory or political pressure forced their hand to avoid the worst outcome. Andhra Pradesh, by allowing rapid growth to continue until the political moment crystallized into the October 2010 ordinance, destroyed its private MFI sector entirely. Cambodia represents a different pattern: the official NPL ratio of 2.5 percent in 2022 looks comfortable, but the 34.8 percent of new loans being used to service old ones reveals the rotation arrangement at scale and the sector continues to grow to $18 billion in 2024 despite mounting international concern.

Nepal's December 2025 regulatory action came at a meaningfully later point in the crisis trajectory than Bangladesh's organic deceleration. The per-borrower caps came in mid-2024, after the multi-lending pattern was already entrenched. The dividend ban came in December 2025, after eleven institutions were already above the 15% threshold. The escalation sequence is correct in instrument choice but the timing is late. Whether Nepal lands closer to the Bangladesh outcome (deceleration before crisis), the Cambodia outcome (continued growth with masked credit quality), or the Andhra Pradesh outcome (political collapse) depends on what happens in the next two to four quarters, particularly whether the political pressure for borrower write-downs converts into specific regulatory action, and whether the wholesale funding chain risk discussed below is acknowledged or deferred.

What microfinance NPLs mean for the banks, and what September 2025 changed

The microfinance sector does not exist in isolation. The wholesale funding that financed the multi-lending growth came primarily from Class A commercial banks, in part through directed-lending requirements under NRB's productive-sector lending rules and in part through commercial relationships. The exposure of the commercial banking system to the microfinance sector is therefore not just sentimental, it is balance-sheet-direct.

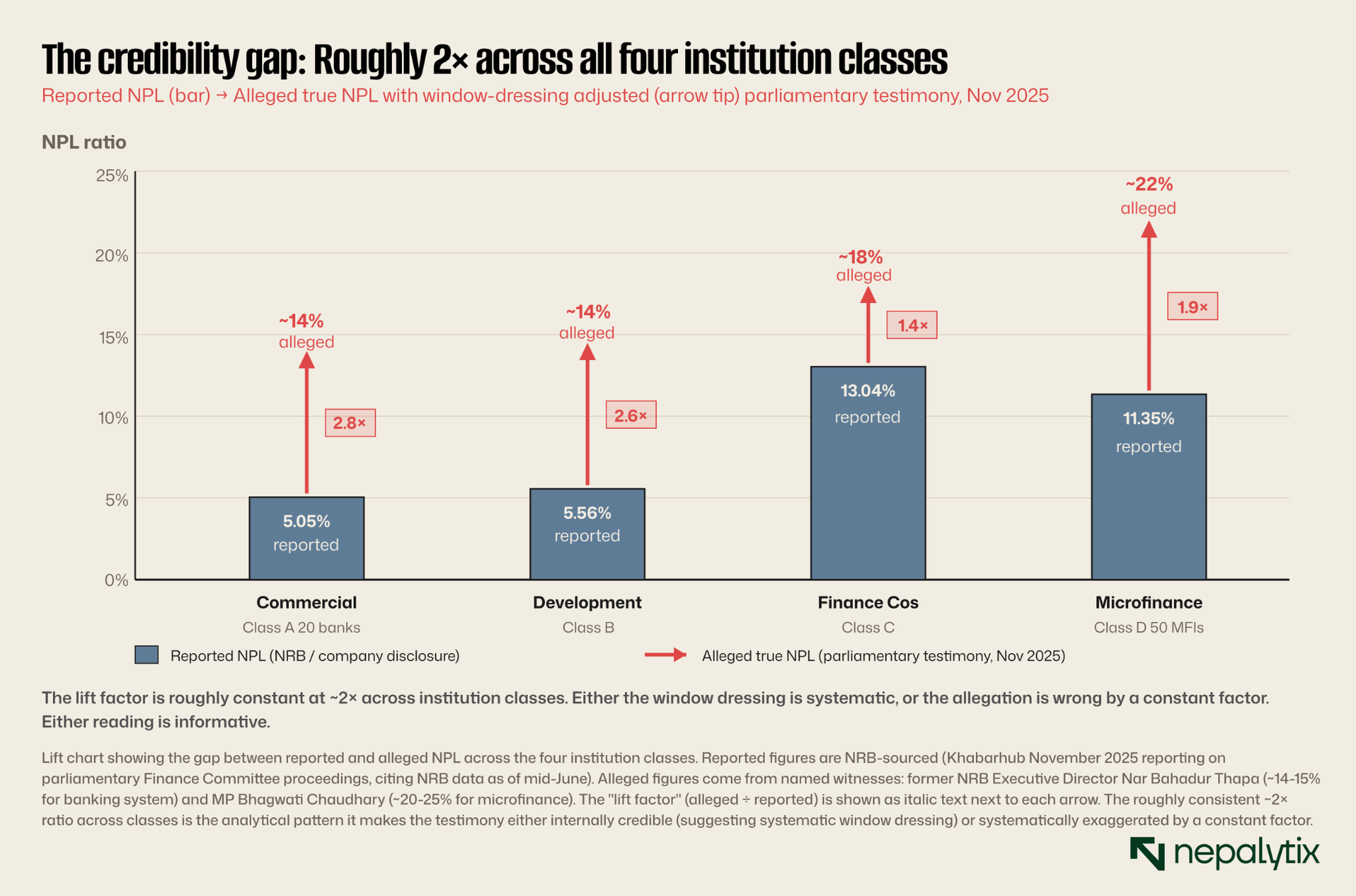

Finance Committee testimony in the federal parliament, reported by Khabarhub in November 2025, made this connection explicit. The former Deputy Chair of the National Planning Commission, Dr. Min Bahadur Shrestha, and the former NRB Executive Director Nar Bahadur Thapa both argued that the BFI system's reported 5.24 percent NPL was understated through window-dressing practices, and that the true NPL ratio across the financial system could be 14 to 15 percent if accounted honestly. Member of Parliament Bhagwati Chaudhary of the CPN-UML party, herself active in the microfinance sector, argued that the true MFI NPL ratio could be 20-25 percent.

The window-dressing allegation deserves serious attention because it shapes everything about how the system actually functions. If MFI NPLs are truly closer to 20 percent than to 11 percent, the capital adequacy reported by these institutions does not reflect their actual loss-absorption capacity. The dividend ban at 15 percent NPL, intended as forceful regulatory action may apply to a sample of institutions selected by the criterion of having the most honest disclosure rather than by the criterion of having the worst portfolio quality. Institutions willing to manipulate their NPL classification to remain below the threshold could continue distributing dividends while institutions that disclose honestly cannot.

The IMF, in its 2023 Article IV consultation, flagged a related concern: that BFIs in Nepal might be evergreening loans issuing fresh credit to borrowers who use it to service existing loans, effectively suppressing reported defaults while accumulating credit risk. The evergreening pattern is structurally identical to the multi-lending pattern at the microfinance level just transposed up one tier of the financial system. The IMF's concern is that the system-wide NPL ratio reflects the success of evergreening rather than the actual underlying credit quality.

If both allegations are correct, MFIs window-dressing at the institution level, commercial banks evergreening at the system level the gap between reported financial system health and actual financial system health is substantial. The microfinance crisis is then not just a Class D problem; it is a leading indicator for the entire BFI sector's reckoning with credit quality that has been suppressed across cycles.

The microfinance crisis is not just a Class D problem. It is what the rest of the financial system looks like when the rotation arrangements break and the actual credit quality has to be priced into the books.

The systemic risk picture became more concrete in September 2025, when the political environment around the sector changed materially.

September 2025 and what came after

The September 2025 unrest was not, strictly speaking, about microfinance. The youth-led anti-corruption protests began over a different set of grievances: political corruption, dynastic governance, economic stagnation, the gap between elite consumption and rural poverty. The protests escalated quickly into widespread civil unrest that, according to World Bank estimates, cost the economy approximately 1.3 percent of GDP. The Prime Minister resigned. The House of Representatives was dissolved. Under an interim government, snap elections held on March 5, 2026 produced a single-party majority government for the first time in a decade.

The microfinance sector was inflected by the unrest in two ways, both important for understanding the current trajectory.

First, the disruption to operations during the protest period, loan officer field visits suspended, branch operations restricted, collection efforts paused caused an immediate quarterly deterioration in repayment rates that did not subsequently recover. Some borrowers who had been current on payments stopped paying when the political climate suggested that aggressive collection by MFIs would not be politically tolerated. Other borrowers, watching the broader anti-establishment momentum, joined the existing anti-microfinance organisation. The result was a step-function deterioration in the Q2 and Q3 reporting periods that the asset-quality cliff chart already shows.

Second, the political climate following the unrest made the regulator's calculation different. NRB had been deliberating regulatory tightening through 2024 and into early 2025. The political shift created an environment in which forceful action against the worst-performing MFIs was no longer a political liability; it was, if anything, a political requirement. The December 2025 dividend directive came in this context. So did the rumored regulatory plan to designate additional MFIs as problematic institutions for Prompt Corrective Action treatment, beyond the existing Super LBSL case.

The December 22, 2025 Kathmandu-focused protest organized jointly by the Land Rights Movement, the Nepal Microfinance and Financial Exploitation Struggle Committee, and the Nepal Farmers and Workers Movement Against Loan-Sharking added political pressure for further action. The protesters' demands included scrapping microfinance institutions, writing off existing debts, and removing loan defaulters from the credit-bureau blacklist. The maximalist demands were not granted. But the political environment made forbearance toward the worst-performing MFIs politically untenable, accelerating the regulatory tightening that NRB had been pursuing gradually.

What happens next

The microfinance sector's losses do not stay in the microfinance sector. The wholesale funding lines from commercial banks, the ownership stakes of larger BFIs in microfinance subsidiaries, the cross-holdings through the listed equity market all of these create channels through which the Class D losses become Class A and Class B problems.

Consider the listed MFI universe specifically. Of the fifty registered MFIs, the vast majority are listed on NEPSE, with the listed market capitalization of the microfinance sub-sector running in the tens of billions of rupees. Several of the worst-performing institutions share branding with larger commercial banking groups NIC Asia Microfinance and NMB Microfinance both bear the names of commercial bank counterparts. The naming convention strongly suggests promoter-level or ownership relationships, though Nepalytix has not verified the specific shareholding structures of these institutions against NEPSE filings. To the extent such cross-holdings exist, parent banks carry equity exposure to the deterioration. When the December 2025 dividend ban kicks in for fourteen institutions, the income foregone by parent banks holding those equity stakes is a direct hit to non-interest income.

The wholesale funding exposure is harder to quantify with public data but is structurally larger. Commercial banks lending to MFIs at the wholesale rate, secured by the MFIs' loan books, hold credit exposure that compounds the underlying borrower risk. If an MFI is unable to recover from individual borrowers, the wholesale lender's recourse is to the institution's residual capital which, given the 0.7 percent average ROA and the regulatory dividend pressure, is being depleted exactly when it is most needed as collateral.

The political question that the new majority government inherits is whether to recognize the losses in the open through MFI recapitalization, asset-quality reviews extended to the wholesale funding chain, and stronger consumer protection or to allow the rotation arrangement to continue at a slower pace under tighter regulatory caps. The first path is more disruptive but produces a financial system with credible disclosures. The second path is less disruptive but extends the gap between reported and actual asset quality across the BFI sector.

The early signals from the new government suggest the first path. The Finance Minister appointments and the early policy statements have emphasized "policy predictability" and structural reform. The Finance Committee testimony from November 2025 which framed the system-wide NPL as 14-15 percent rather than the reported 5.24 percent was unusually direct for Nepali parliamentary proceedings and suggests the political appetite for honest disclosure is higher than it has been in previous cycles. Whether NRB acts on that appetite, in the time remaining before the next major macroeconomic stress test, is the question on which the next twelve months will turn.

Before considering which resolution path Nepal takes, the arithmetic of a write-down of what it would cost in fiscal terms needs to be made explicit.

What a write-down actually costs

The arithmetic below is a Nepalytix analytical exercise, not a costing of any specific proposed program. Each step is a reasonable order-of-magnitude estimate from sector-level data; the cascading nature means the final fiscal cost figure should be read as illustrative of scale rather than a precise forecast. The political path discussed below partial write-downs on the most distressed borrowers, financed in part by government recapitalization has an arithmetic that deserves explicit treatment. The basic question: if the government were to mandate a 40 percent write-down on the loan obligations of borrowers above a defined distress threshold, what is the fiscal cost?

A reasonable upper bound on the write-down population is the share of MFI portfolio represented by borrowers above the dividend-ban threshold's institutions. The eleven institutions above 15 percent NPL collectively represent approximately 30-40 percent of total MFI portfolio, call it Rs 175 billion of the Rs 500 billion total. Of that, perhaps 60-70 percent is loans to borrowers in legitimate distress (as opposed to strategic non-payment or technical default). That gives a stressed-borrower portfolio of approximately Rs 110-120 billion. A 40 percent write-down on this segment is approximately Rs 44-48 billion of debt forgiven, distributed across roughly 600,000-700,000 borrowers meaning an average per-borrower relief of Rs 60,000-80,000.

The fiscal cost of this assuming the government finances the MFI capital hole that results is on the order of 1.4 percent of GDP at current GDP levels of approximately Rs 5,800 billion. That is a substantial fiscal commitment but not impossibly so. For context, the September 2025 unrest cost the economy approximately 1.3 percent of GDP in lost output. The fiscal cost of a stress-period microfinance recapitalization is in the same order of magnitude as the unrest's economic impact. Politically, the choice is between absorbing the cost as a deliberate program with structural reform, or absorbing it through continued borrower distress, periodic political action, and slow-burn financial system instability.

The economic argument for the deliberate program is straightforward, assuming the order-of-magnitude estimates above are directionally accurate. The Rs 44-48 billion of forgiven debt which we stress is built on cascading estimates of stressed-borrower portfolio share, write-down percentage, and per-borrower distribution does not represent a real economic loss that money has already been spent and consumed by borrowers; the write-down is simply recognition of what already happened. The MFI capital that must be replenished is the second-order consequence; the institutional capital existed and was deployed productively in the financial-inclusion phase before the cliff. Replenishing it through fiscal action restores the lending capacity that the system needs to continue serving the borrowers who are not in distress.

The economic argument against is moral hazard. Borrowers who chose strategic non-payment, in anticipation that political pressure would produce write-downs, are rewarded by the program. Future MFI lending faces a market with weaker repayment discipline. The structural reform component of tighter per-borrower exposure caps, mandatory credit-bureau coverage, supervisory escalation at sectoral 5 percent NPL is what determines whether the write-down is a one-time correction or the beginning of a periodic political bailout cycle. The Cambodia precedent suggests the structural reform component is essential. The Andhra Pradesh precedent suggests that without it, the next crisis arrives within a decade.

With the cost arithmetic in place, the three resolution paths Nepal faces can be evaluated.

The choices that remain

The current trajectory is not sustainable. With NPLs at 11.35 percent and rising, capital adequacy at 11.90 percent and falling, average ROA at 0.7 percent and falling, and political appetite for borrower relief still high, the microfinance sector cannot continue to absorb stress through internal capital generation. Three paths from here remain analytically open. None is straightforward.

Path one: Managed consolidation. The fourteen MFIs above the dividend ban threshold are formally identified as the high-risk segment. NRB applies further measures, capital injection requirements, supervised asset disposals, mandatory mergers with stronger institutions. Some institutions exit through forced consolidation. The sector shrinks from 50 to perhaps 35 institutions over 18-24 months. The borrowers held by existing institutions are transferred, with portions of their debt written down. This path produces realized losses but bounded systemic risk.

Path two: regulatory forbearance with restructuring. NRB grants temporary relief on classification rules; restructured loans remain classified at lower categories than current rules would require to permit MFIs to defer recognition of losses while regulatory restructuring of borrower obligations proceeds in parallel. The headline NPL ratios decline. Actual credit quality does not improve. This path postpones the realized losses but extends the window in which the rotation arrangement continues.

Path three:political resolution. The new government, responding to continued political pressure from microfinance victims' organizing mandates a structural write-down of borrower obligations across the sector, perhaps 30-40 percent reductions on loans to over-indebted borrowers financed in part by government recapitalization of the affected MFIs. The borrower pressure is relieved; the sector receives an explicit subsidy; future microfinance growth is constrained by tighter regulatory caps. This path resolves the political pressure but at substantial fiscal cost and with moral-hazard implications for future lending.

The realistic outcome

Some blend of paths one and three is the most plausible projection. The political momentum makes path two pure forbearance increasingly difficult. The fiscal constraint limits pure path three. The blend involves managed consolidation of the weakest MFIs, partial write-downs on the most distressed borrowers, and tighter regulatory caps on per-borrower exposure. The sector that emerges will be smaller, more capital-intensive and structurally less profitable than the sector that existed in 2022. The financial inclusion gains will not be reversed wholesale but new credit growth into the lowest-income segments will be permanently slower than the 2019-2024 pace.

What this piece has tried to demonstrate is that the trajectory was visible across multiple primary-source dimensions for several years before the regulatory action that finally addressed it. The 2017 NRB survey identified the multi-lending pattern. The 2022 NPL inflection identified the asset-quality direction. The 2023 protests identified the political consequence. Each signal was responded to, when responded to at all, slowly. The cumulative cost of slow response is now embedded in the Q3 FY 25/26 sector NPL ratio of 11.35 percent.

The lesson is not that microfinance is a failed development model. The lesson is that any regulated lending sector in a low-income economy with weak credit information infrastructure produces a structural multi-lending pattern within five years of reaching scale, and any institutional framework that does not anticipate that pattern will permit it to compound until the political environment forces a reckoning. Nepal's microfinance sector is not the first to encounter this trap. The countries that have managed it best Bangladesh, parts of Latin America have done so through deliberate credit-bureau infrastructure investment, regulatory limits on per-borrower aggregate exposure rather than per-lender rates, and earlier supervisory escalation when sectoral NPLs cross 5 percent.

Nepal's choice now is not whether to take losses in the microfinance sector. The losses are already real. The choice is how to recognize them, how to distribute them between borrowers and institutions and the fiscal authority, and what structural reforms to install so that the next decade's financial inclusion growth does not produce the next decade's structural risk concentration. The trap is set. The exit is more careful supervision, more honest disclosure, and a regulatory framework that aggregates the borrower's actual obligation rather than each institution's individual loan in isolation. That work has not yet begun in earnest. The signal from primary-source data is that it should.

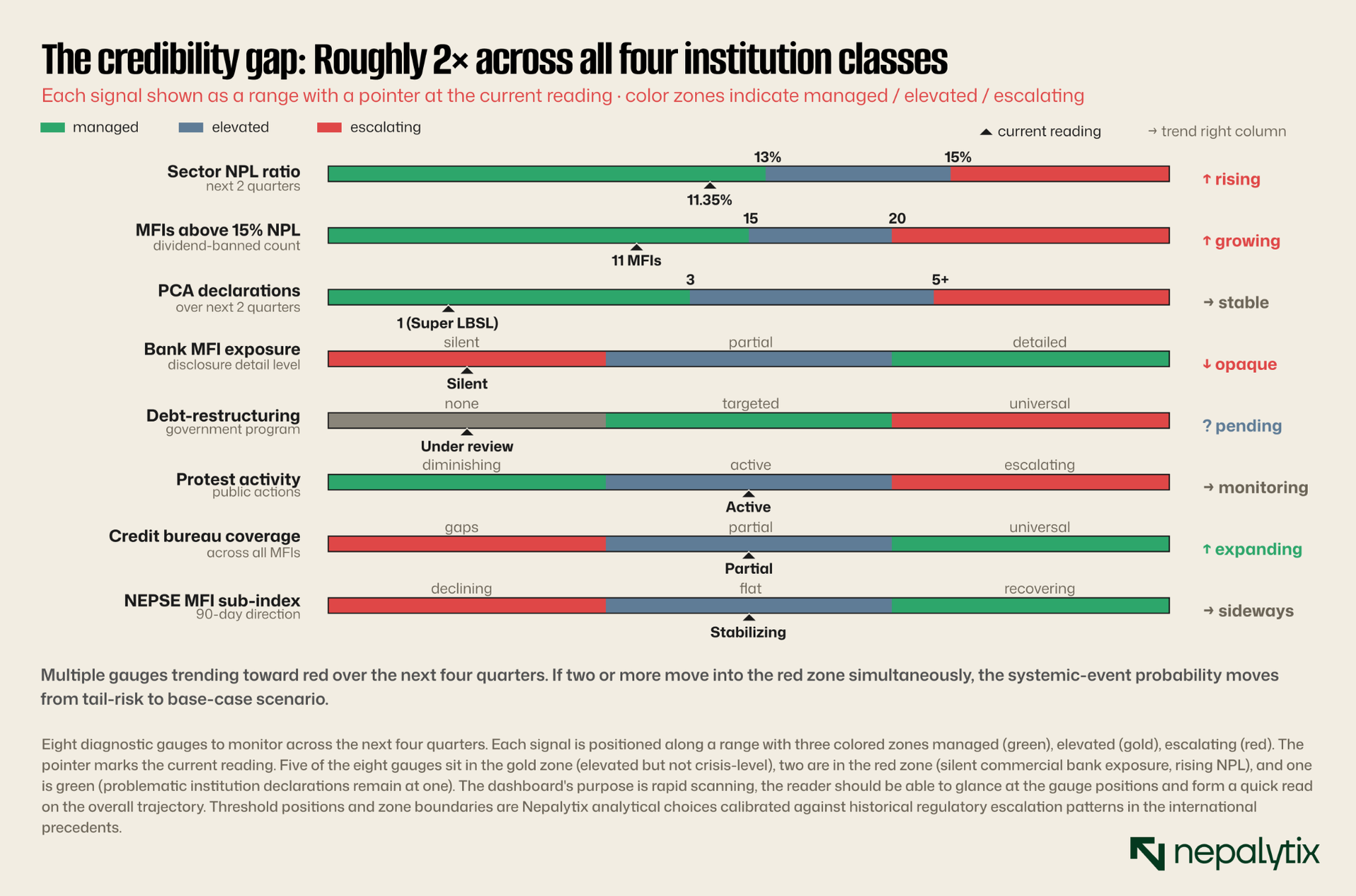

The data releases and decisions that will determine the resolution in the next four quarters

The microfinance trajectory will resolve, one way or another, within the next four quarterly reporting cycles. The signals that will indicate which path the resolution takes Cambodia-style managed consolidation, Andhra Pradesh-style collapse or politically-mandated debt restructuring will appear in specific data releases and regulatory decisions over this period. The diagnostic checklist below identifies the specific items to monitor.

Each item in the scorecard has a different lead time. The NEPSE MFI sub-sector index updates daily, with market analysts processing each new disclosure within hours. The NRB sectoral NPL ratio updates quarterly. Government policy responses can move on legislative cycles of weeks to months. The credit-bureau coverage expansion is the longest-cycle item, requiring infrastructure investment and institutional cooperation that typically takes two to three years to complete.

For Nepalytix readers, the practical monitoring framework runs roughly as follows. Watch the NEPSE MFI sub-sector index daily for early signals; if it begins a renewed decline below the 2025 lows, that is the equity market pricing in further write-downs. Watch the NRB quarterly disclosures for the headline NPL trajectory; if Q4 FY 25/26 prints above 13 percent, the trajectory has not turned. Watch the parliamentary Finance Committee proceedings for the political turn; if the November 2025 testimony pattern repeats with more institutional support for the higher allegation numbers, the political path toward debt restructuring is accelerating. Watch the NRB Microfinance Supervision Department's problematic institution list; if a second or third institution is designated, the regulatory escalation cycle is activated.

The most consequential single signal to watch, for both the sector's trajectory and the broader BFI implications, is whether commercial bank disclosures begin including more granular MFI wholesale exposure data. As discussed in §4 and §9, the wholesale funding chain is the channel through which microfinance distress propagates to the rest of the financial system. If commercial banks begin voluntarily or under regulatory pressure to disclose specific exposure to the dividend-banned MFIs, the financial system is moving toward honest recognition of the chain risk. If the silence continues, the chain risk is being deferred rather than addressed.

What success looks like

For Nepal's microfinance sector to emerge from this period with the financial-inclusion gains preserved and the systemic risk contained, the next four quarters need to deliver a specific combination of outcomes. First, the sector NPL ratio needs to stabilize and begin declining not because of regulatory forbearance, but because the underlying borrower distress has been resolved through honest write-downs and operational restructuring. Second, the worst-performing institutions need to either return to compliance through capital injection and asset disposal, or be resolved through controlled merger or license cancellation, rather than allowed to drift through extended supervision without action. Third, the wholesale funding chain risk needs to be acknowledged through commercial bank disclosures, and any required recapitalization of commercial banks identified and executed. Fourth, the structural reform credit information bureau, per-borrower exposure caps, supervisory escalation at sectoral 5 percent NPL needs to be operationalized so the next decade's microfinance growth does not produce the next decade's structural risk concentration.

None of these outcomes is automatic. Each requires deliberate regulatory and political action, taken before the next macroeconomic shock arrives to test the system's residual capacity. The current government, with its single-party majority and clear post-unrest mandate, has the political authority to take the necessary actions. Whether it chooses to spend that authority on the microfinance reckoning or on other reform priorities will be visible in budget allocations, legislative agenda, and regulatory directive issuance over the next two quarters.

The microfinance trap, in this respect, is not unique to Nepal. It is the structural risk that any low-income economy with rapid financial-inclusion growth produces when the regulatory infrastructure does not keep pace with the operational reality. Bangladesh's Yunus-era controversy, Andhra Pradesh's 2010 collapse, Cambodia's recent reckoning each represents a different national resolution of the same underlying pattern. Nepal's resolution will sit somewhere on the spectrum these precedents define, and the position on the spectrum is being determined now, in the regulatory and political choices being made through the rest of 2026.

The Nepalytix view, for what it is worth, is that the December 2025 dividend ban represented the first commensurate regulatory action of the cycle, that the new government's appetite for honest disclosure suggests the political environment for further action exists, and that the technical capacity of NRB to execute a Cambodia-style managed consolidation is adequate if the political backing is sustained. The downside risk is that political attention shifts to other priorities, the next macroeconomic shock arrives before the structural reforms are operational, and the wholesale funding chain crystallizes simultaneously across multiple commercial banks. That downside scenario is not the central case. It is, however, possible enough that the monitoring framework laid out above is worth maintaining as the sector works through the resolution path.