Nepal’s Public Debt Nears Rs 3 Trillion: What Rs 93,600 Per Citizen Really Means

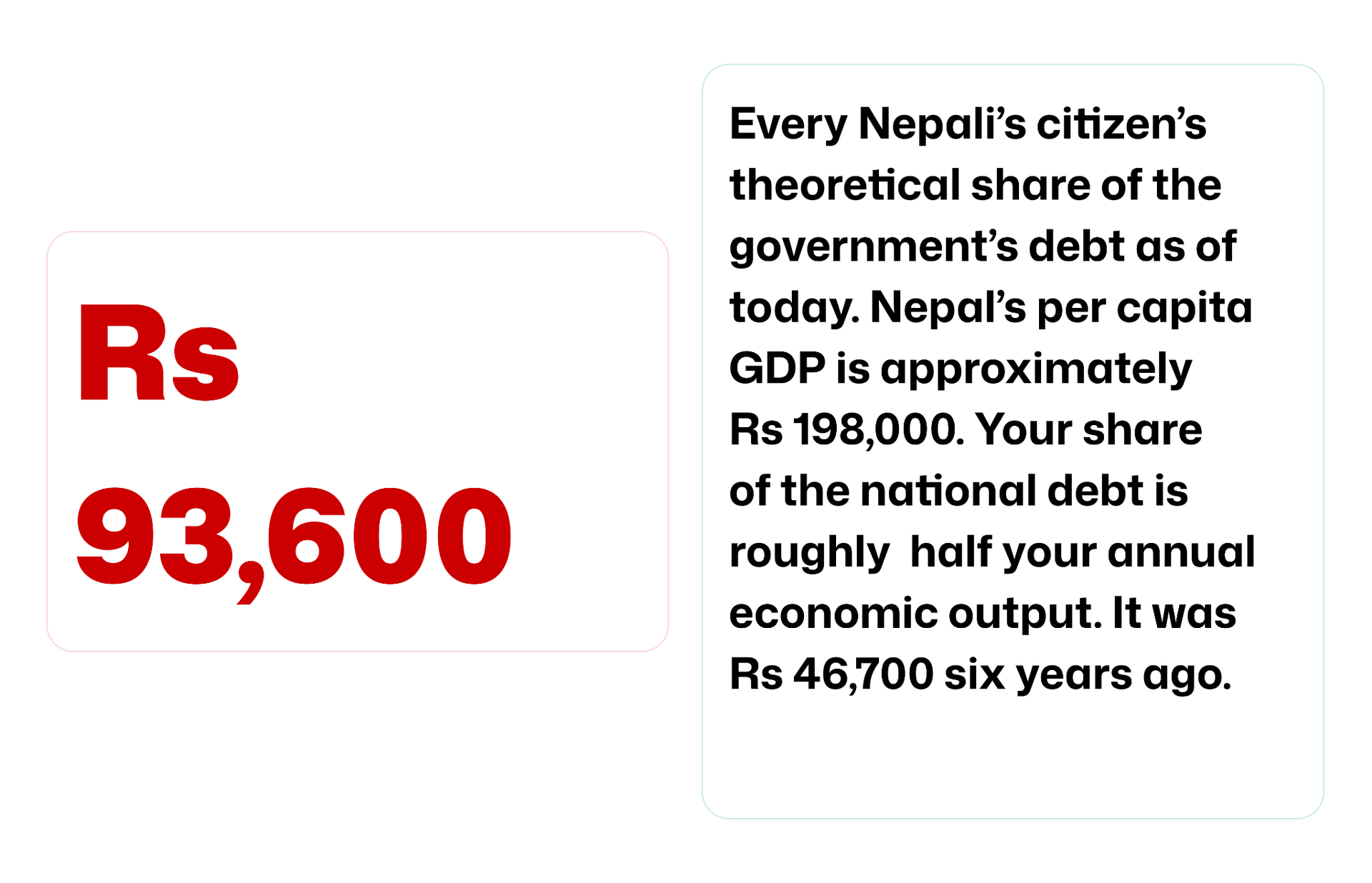

Nepal’s public debt has surged to Rs 2.878 trillion, translating to roughly Rs 93,600 per citizen

Nepal's public debt crossed Rs 27 trillion. Here is what that means per citizen.

The government calls it “low risk of debt distress.” That phrase is doing a lot of work. Here is what it is covering.

Nepal's public debt hit Rs 2.878 trillion as of mid-March 2026. That is the official number from the Public Debt Management Office. Every major outlet covered it with the same two-sentence summary: debt crossed X trillion, debt-to-GDP is now 47%, Nepal remains at low risk of debt distress. Then the story moved on. This piece does not move on. Because what those two sentences contain is technically accurate and contextually incomplete in ways that matter.

The per capita framing is not a scare tactic. It is just arithmetic. Rs 2.878 trillion divided by 30.7 million people is Rs 93,600 per head. What makes it meaningful is not the absolute figure; plenty of countries carry more debt per citizen and function fine. What makes it meaningful is what sits alongside it. The government has earmarked Rs 411 billion for debt servicing this fiscal year. That is principal repayments plus interest. One line item. Rs 411 billion. More than the entire capital budget that historically gets spent.

Capital spending execution in Nepal has averaged 55% of allocation for years. In the first half of FY26 it was 12.1% partly because of last year's political unrest, partly because implementation delays are Nepal's permanent condition. Debt servicing execution is 100%. It has to be, because the consequence of missing a payment is not a delayed project. It is a sovereign credit event. So the government always finds money for the Rs 411 billion. It finds it by crowding out the things that do not have the same legal compulsion.

"Nepal is spending more on its past debt than it is building new things and that gap has widened every year since 2022."

The World Bank's April 2026 Development Update, the most current independent assessment available, confirms this directly. Capital expenditure has consistently lagged debt servicing since H1 FY22. The gap stood at 2.2% of GDP in H1 FY26 and is widening. This is not a one-year anomaly caused by the election. It is a structural pattern that predates the September 2025 unrest by several years.

Now here is what "low risk of debt distress" actually means, technically. It means the IMF and World Bank believe Nepal can service its existing debt obligations under their baseline scenario primarily because most external debt carries concessional terms. The average interest rate on Nepal's debt is 3.4%, with an average maturity of 8 years. World Bank and ADB loans come with long grace periods. On those terms, the debt is serviceable. The rating is not wrong.

But it is built on terms that are changing. Nepal is on track to graduate from Least Developed Country status. As that happens, access to the most concessional borrowing facilities, the ones that make 3.4% possible, will gradually close. The PDMO's own medium-term strategy document has already modelled this, noting that concessional sources "will slowly start to dry" and projecting a shift toward non-concessional multilateral borrowing at higher rates. The same debt level at 6% is a structurally different problem from the same debt level at 3.4%. The rating captures today. It does not capture the trajectory.

There is one more number worth holding. In the first eight months of this fiscal year, Rs 98 billion was added to Nepal's debt burden not from any borrowing decision, but purely from the rupee's depreciation against the dollar. The rupee fell from Rs 137.88 to Rs 150.67 per dollar in eight months, the weakest level in Nepal's currency history. Because 73% of external debt is denominated in Special Drawing Rights and another 20% in US dollars, a weaker rupee inflates the debt in local currency terms automatically. Rs 98 billion. No loan was signed. No asset was built. The currency moved and the liability grew.

The question is not whether Nepal can pay. It probably can, on current terms. The question is what Nepal got for Rs 2.878 trillion and whether the next trillion will be borrowed at the same rates, for the same purposes, with the same execution.

Nepal's public debt was Rs 1.433 trillion in FY 2019/20 and represented 38% of GDP. In six years it has nearly doubled. The World Bank projects a mild decline to around 45% of GDP over FY27–FY28, contingent on revenue recovery, contained spending, and the new government's structural reforms. Those projections are reasonable. They are not guaranteed. Revenue collection has been falling as a share of GDP. Capital spending execution is at 12%. The political conditions that produced last year's unrest have not been resolved by an election; they have been temporarily redirected.

Rs 93,600 per citizen. Rs 411 billion in servicing. A gap between what the government owes the past and what it is building for the future has widened every year for four consecutive years. Whether this is a crisis depends on the definition. Whether it is a problem depends on the trajectory. The number that crossed Rs 27 trillion deserved more than two sentences.