Nepal’s strongest reserve position in a decade is also it's biggest macro bet

The Bagmati Provincial Government has announced a public holiday across the province on Baisakh 24 to mark the Official Language Day, while Nepal’s stock market will continue regular operations.

Nepal's reserves cushion is the strongest it has been in a decade. It is also the most concentrated bet a country can make.

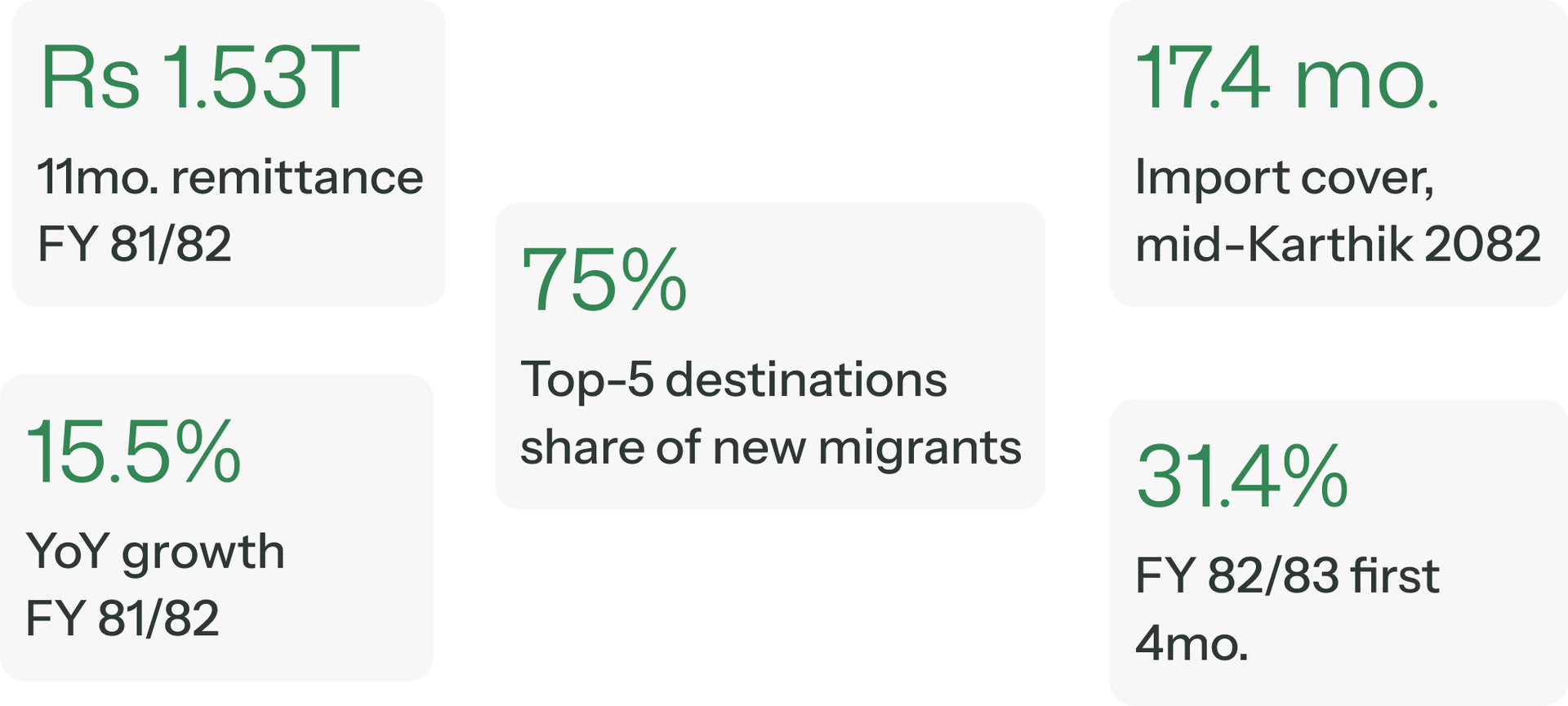

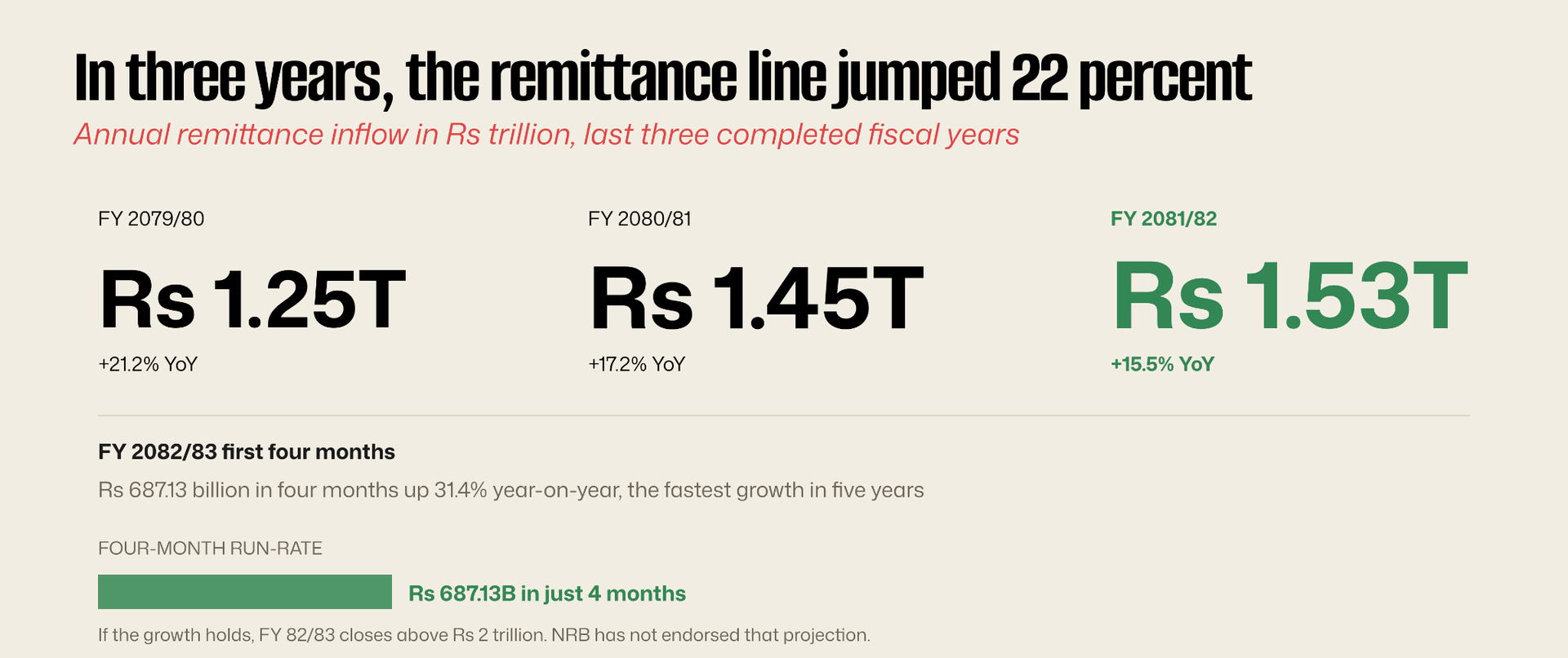

In Jestha 2082, Nepal recorded the single largest monthly remittance inflow in the country's history. Rs 176.32 billion arrived through formal banking channels in one Nepali month. The figure was larger than Nepal's total annual export earnings five years earlier. It was the seventh consecutive month of double-digit year-on-year growth, and it pushed the eleven-month total for fiscal year 2081/82 to Rs 1.532 trillion.

The number gets reported every month. It is the most-cited statistic in Nepali macroeconomic coverage. It is also the most misunderstood. Most coverage treats remittance as income to households. It is. But every rupee that arrives also passes through a chain of regulated institutions, each touch shaping what that rupee ultimately funds. By the time the money reaches the family in Bhaktapur or Nawalparasi or Bardiya, most of the macroeconomic decisions about it have already been made. This piece traces the flow. Where the money comes from, where it sits, what it funds, and what happens when the source slows.

The arc

The eleven-year story is one of the most stable upward trends in Nepali macro data. Annual remittance inflows have nearly tripled since FY 2071/72. Through fiscal 2079/80 the country received Rs 1.25 trillion. Through fiscal 2080/81, Rs 1.45 trillion. Through eleven months of fiscal 2081/82, Rs 1.532 trillion. The trajectory has now extended into fiscal 2082/83, where the first four months alone delivered Rs 687.13 billion, a 31.4 percent year-on-year jump and the fastest growth rate the country has recorded in five years.

Three forces produced this curve. The demographic shift: Nepal's working-age population now exceeds total domestic formal employment by a wide margin, and labour migration has become the default response. The destination shift: the Gulf construction boom of 2014 to 2024 absorbed Nepali workers at scale. The channel shift: a decade of Nepal Rastra bank (NRB) rule-tightening has progressively pushed flows from informal hundi networks into formal banking channels, where they show up in the monthly statistics rather than disappearing into private exchange.

The reported number is therefore both an economic measurement and a regulatory artefact. The same Rs 176.32 billion a month would have been Rs 130 or Rs 140 billion a decade ago, with the difference travelling through hundi networks invisible to NRB. Some of the headline growth is real labour income. Some are formalisation. Both matter.

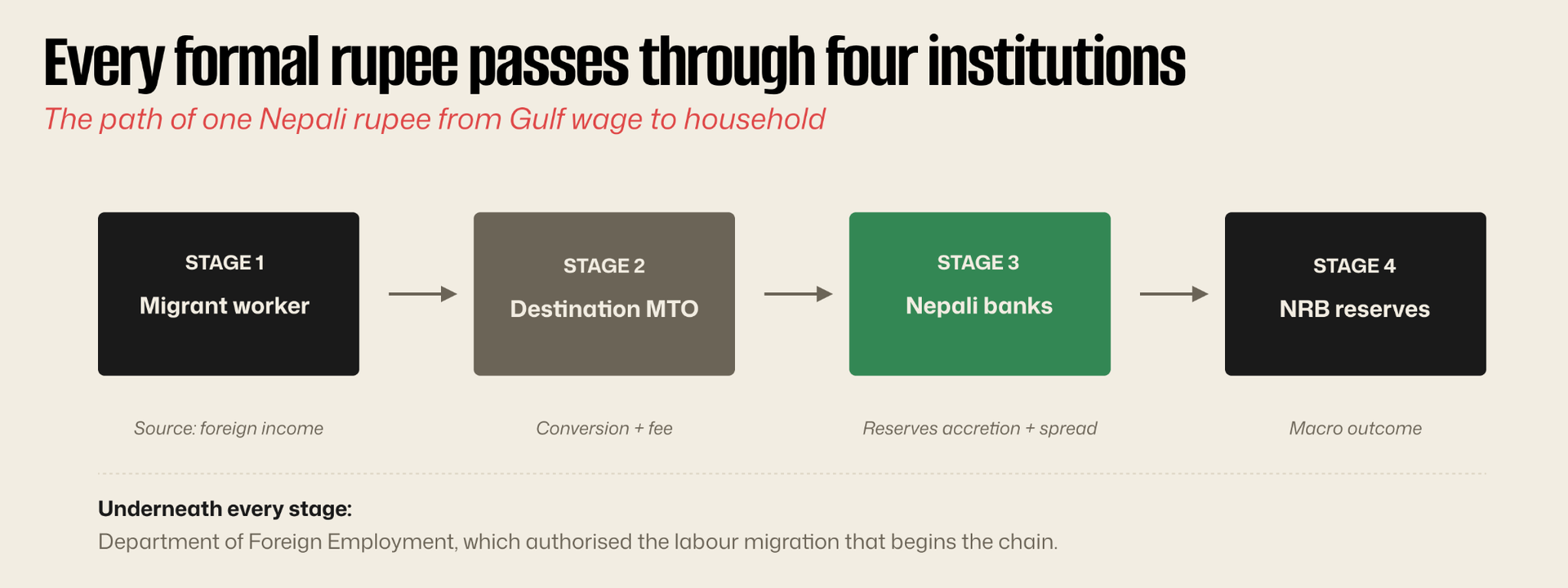

The four institutions that touch every rupee

Every formally remitted rupee passes through a chain. A Nepali worker in Sharjah earns dirhams. The worker walks to a money transfer operator Western Union, Al Ansari, LuLu or to a UAE bank. The Money Transfer Operator(MTO) converts to rupees at a wholesale rate and routes the funds through a corresponding bank in Nepal. The Nepali commercial bank most often IME, Prabhu, Nabil, or Global IME, the four largest remittance handlers, receives the inbound credit and posts it to a beneficiary account. Nepal Rastra Bank's foreign exchange reserves account swells. The household withdraws the rupees in Bhaktapur.

Four institutions touch every rupee: the destination MTO or bank, the Nepali commercial bank, NRB, and invisibly upstream the Department of Foreign Employment, which issued the labour approval that made the migration legal in the first place. Each touch creates a fee, a regulatory record, and a data point.

The fee structure is where remittance leaves a visible imprint on Nepal's banking sector. Remittance handling fees and the foreign exchange spread are among the most profitable lines for the four largest commercial bank handlers. NRB itself earns nothing directly on these flows, but the reserves they build give it the most consequential lever in Nepali monetary policy: import cover.

The destination concentration

In the first month of fiscal year 2082/83 alone, 44,466 Nepalis received labour approval to work abroad. Five countries absorbed roughly three-quarters of them. The United Arab Emirates took 17,779 workers 40 percent of the total making it now the single largest destination for new Nepali migrants, having overtaken Saudi Arabia in recent years. Saudi Arabia followed at 13.3 percent, Qatar at 9.9 percent, Kuwait at 5.9 percent, and Malaysia rounded out the top five.

Within those five countries, Nepali workers cluster in three industries: construction, hospitality and domestic service. A wage cycle in Gulf construction is mechanically a household income cycle in Nepal. The reverse is also true. When oil revenues squeeze Gulf state fiscal capacity, the first line item to compress is the construction pipeline and Nepal's largest export earnings compress with it.

The diversification that isn't

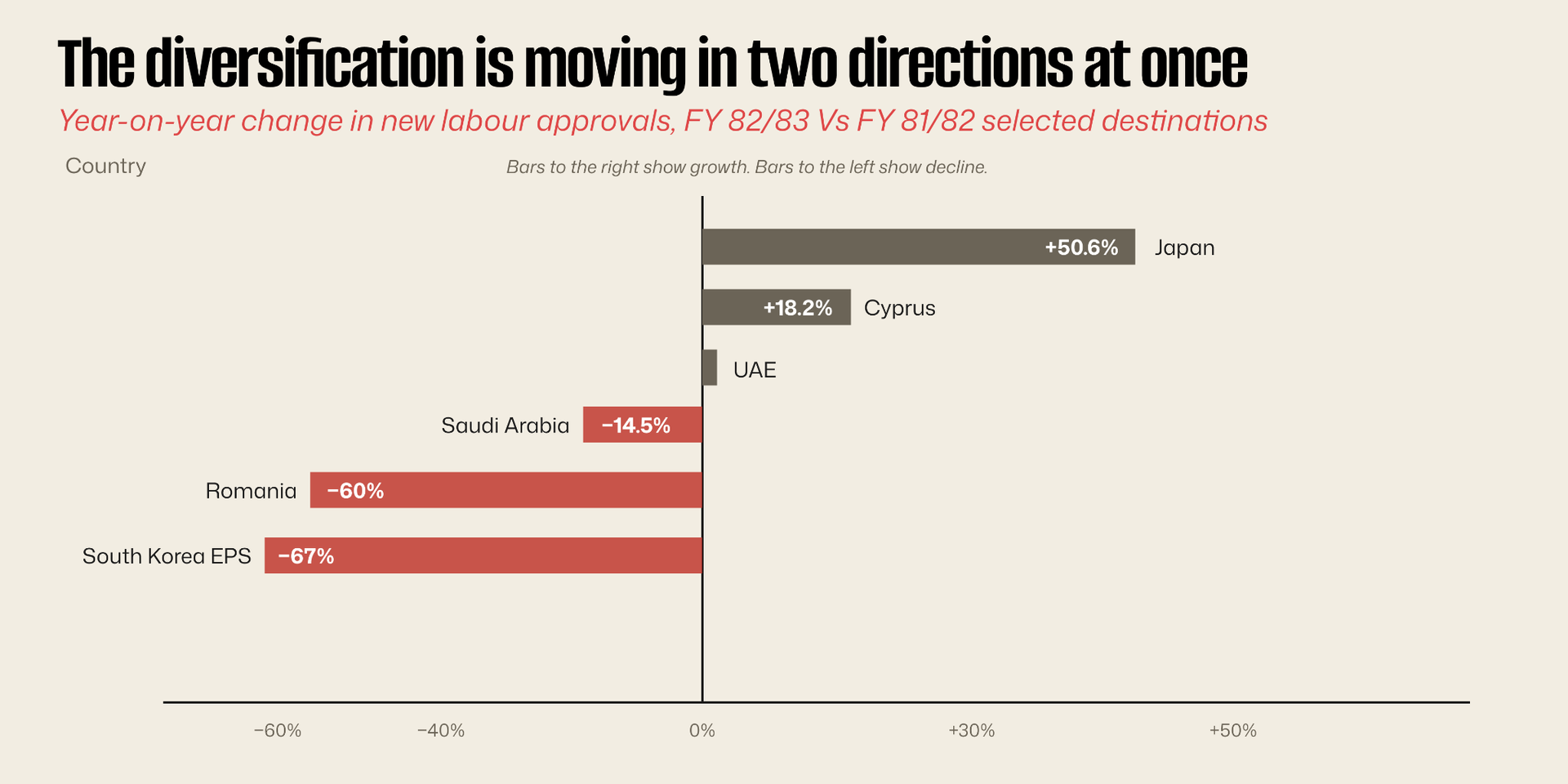

The narrative around Nepali labour migration has begun to shift in recent quarters. Japan, with its expanded Specified Skilled Worker programme, recorded 50.6 percent year-on-year growth in Nepali labour approvals in fiscal 2025/26. Cyprus rose 18.2 percent. The reading from this is that Nepal is finally diversifying away from the Gulf and toward higher-paying safer destinations.

The numbers tell a more complicated story. Saudi Arabia fell 14.5 percent year-on-year. Romania, which boomed in 2024 as a European entry point fell 60 percent in 2025/26 as Romanian labour markets tightened and recruitment fees became unsustainable. South Korea's Employment Permit System long the safest and best-paying legal channel for Nepali workers shrank 67 percent as quotas tightened and skill barriers rose.

The diversification narrative is half-true. Japan and Cyprus are growing fast, but from tiny bases together they account for less than four percent of new approvals. The countries actually losing share are also the safer, higher-paying ones: South Korea EPS, Romania. The labour markets that lost Saudi workers did not pick them up in Tokyo or Limassol. They picked them up in Dubai. The structural diversification away from Gulf construction has not yet happened. The geographic concentration has merely reshuffled within the Gulf.

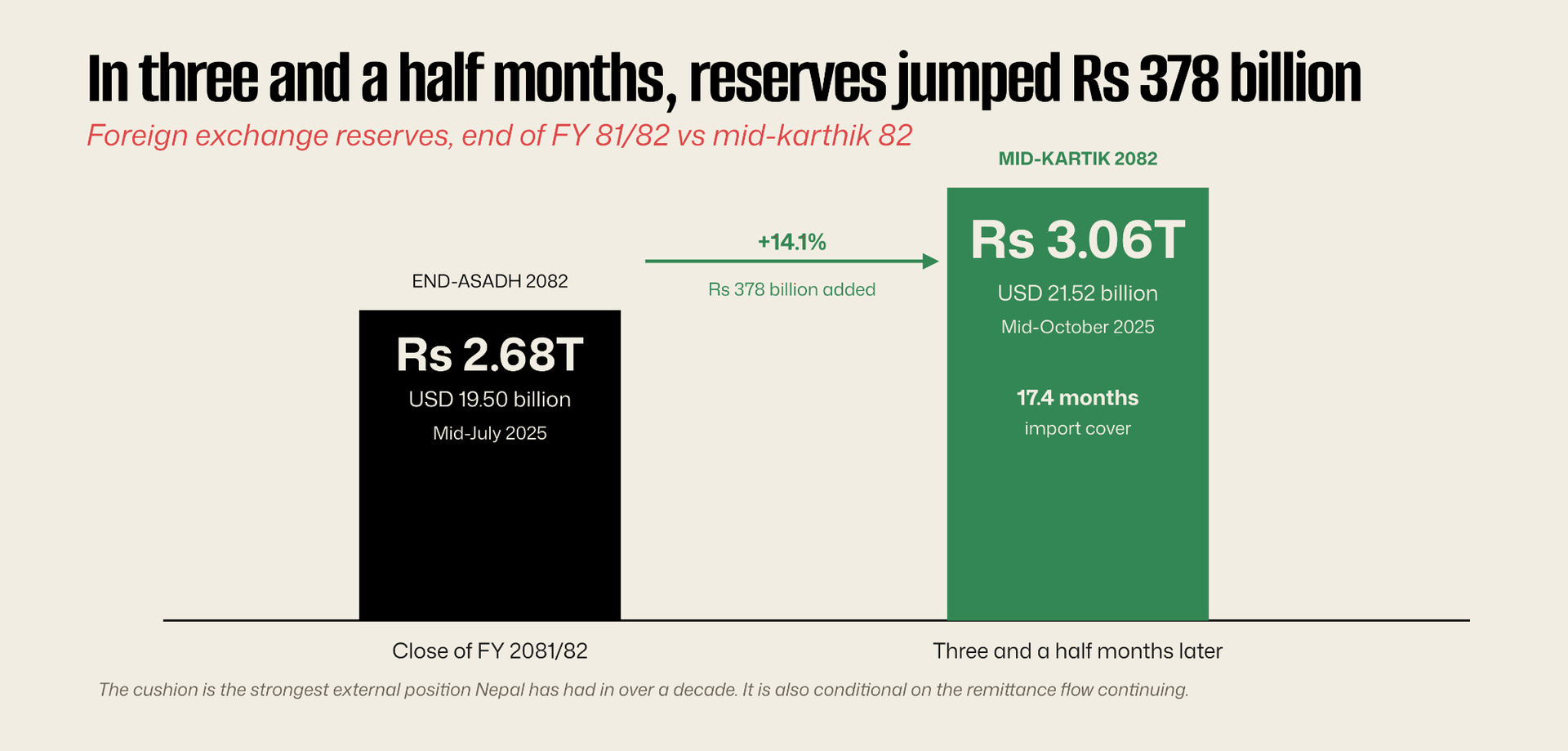

The reserves position the remittance built

The flow has produced a balance-of-payments outcome few emerging economies have achieved in the post-pandemic period. Nepal's foreign exchange reserves stood at Rs 3.055 trillion at mid-Kartik 2082, up 14.1 percent in just three and a half months. In US dollar terms, reserves reached USD 21.52 billion. Import cover, the ratio that matters most for sovereign external resilience, sits at 17.4 months when measured against merchandise and services imports and a remarkable 20.8 months when measured against merchandise alone.

This is the strongest external position Nepal has had in over a decade. It is also entirely a function of the remittance flow continuing at current pace.

Run the counterfactual. If remittance growth were to fall to zero, not decline, simply stop growing for two consecutive fiscal years, the reserves cushion would draw down toward a more normal 10 to 11 months of cover as imports continued to grow at their structural 13 percent annual pace. If remittance were actually to decline by 15 percent, the cushion would compress to under nine months inside two years. The cushion is real. The cushion is also conditional.

The conditionality matters because every Nepali macroeconomic decision currently being taken, the expansionary monetary policy stance for FY 2082/83, the comfortable fiscal deficit, the willingness to import without restriction is taken against the implicit assumption that the remittance flow continues. NRB has the same assumption embedded in its policy framework. The Ministry of Finance has the same assumption embedded in its budget. The assumption may be correct. It is also an assumption.

What the rupee does not fund

The closing argument concerns absorption. Remittance, as decades of NRB analytical work has documented, funds household consumption: food, fuel, school fees, healthcare, festival expenses. Remittance funds residential real estate. Remittance funds what economists somewhat clinically call "social reproduction." It does not, at scale, fund manufacturing investment. It does not fund agricultural productivity. It does not fund the productive lending that would create the domestic jobs that would, in turn, reduce the country's dependence on labour migration in the first place.

The pattern is well-known in development economics. Economies with very high remittance-to-GDP ratios, Nepal at roughly 25 percent, Tajikistan at 30 percent, Lesotho at 25 percent tend to develop characteristic structural distortions: appreciating real exchange rates, declining tradable-goods competitiveness, rising import dependence as households spend foreign income on consumer goods that domestic industry cannot supply. Nepal's import-to-export ratio is now among the most extreme in Asia. Total imports for fiscal 2081/82 ran at multiples of total goods exports. The remittance flow is structurally what permits that imbalance to persist without triggering a balance-of-payments crisis.

The phrase usually applied to this dynamic is "Dutch disease" , the original case being the Netherlands' experience with North Sea gas in the 1970s, where commodity-driven foreign exchange inflows hollowed out the country's manufacturing base. The Nepali variant is different in cause but similar in consequence: foreign exchange inflows arrive in volumes large enough to keep the rupee stable and imports affordable, but the flow does not pass through the productive sectors of the economy on its way in. It arrives, sits briefly in commercial bank deposits, and exits as imports.

The reserves cushion the remittance built is the strongest asset Nepal has in its external account. It is also the strongest evidence that the country has not yet built the productive capacity to thrive without the cushion.

Three-quarters of the flow comes from five labour markets. Those labour markets run on construction cycles in petro-states. Those construction cycles run on oil prices, Gulf fiscal policy, and visa regimes set in capitals where Nepal has limited diplomatic leverage. In April 2026, the Department of Foreign Employment had to suspend new approvals to a dozen Gulf and Middle Eastern destinations for nearly two months when US-Iran tensions threatened regional stability. The flow recovered. The reminder of how exposed Nepal is to events outside its borders did not.

The seventeen-month import cover buys Nepal time. Roughly two years of policy space if remittance growth stays positive. Closer to eighteen months if growth turns flat. Less if it turns negative. What the country does with that time whether it uses the breathing room to build the manufacturing, agricultural, and service-sector capacity that would reduce its labour-export dependency, or whether it uses the breathing room to consume more imported goods financed by more remittance is the actual macroeconomic question for FY 2082/83. The remittance flow is not the answer. It is the time the country has bought to find one.