NIC Asia and the Yes Bank Parallel: Are Nepal’s Banking Warning Signals Being Ignored?

India’s Yes Bank collapse in 2020 did not happen overnight. The warning signs were visible nearly thirty months earlier through rising bad loans, governance actions, provisioning shocks, and capital stress.

It was a Thursday morning in March 2020 when the queues began to form outside Yes Bank ATMs across India. The Reserve Bank of India had announced overnight that depositor withdrawals from India's fourth-largest private sector bank would be capped at fifty thousand rupees. Customers with larger account balances stood in lines with patient anxiety. The branches were open. The ATMs functioned within the cap. The bank was still trading. But the institution they had trusted with their savings, a fixture on India's growth-story list for fifteen years, was effectively under guardianship.

By the end of that month, Yes Bank's shareholders had been wiped out by 90 percent. Its Additional Tier-1 bondholders including pensioners who had been sold the instruments as low-risk fixed-income substitutes had been written off entirely. The State Bank of India had taken a 49 percent stake in a rescue capital infusion. Eight new directors had been appointed by the RBI to a reconstructed board. The founder Rana Kapoor was in custody on money-laundering charges. Yes Bank as an independent institution, was finished.

This piece is not about Yes Bank. It is about what an analyst reading the Nepali banking sector in May 2026 should notice when looking at NIC Asia Bank Limited and at the broader pattern of bank distress signals that have been visible in the public regulatory record for the last eighteen months. The Yes Bank story is the setup not the subject. The question is whether the same kind of leading indicators that were visible at Yes Bank in 2018 and 2019 are now visible at NIC Asia in 2024 and 2025 and if so what that should change about how the institution is regulated, valued, and read.

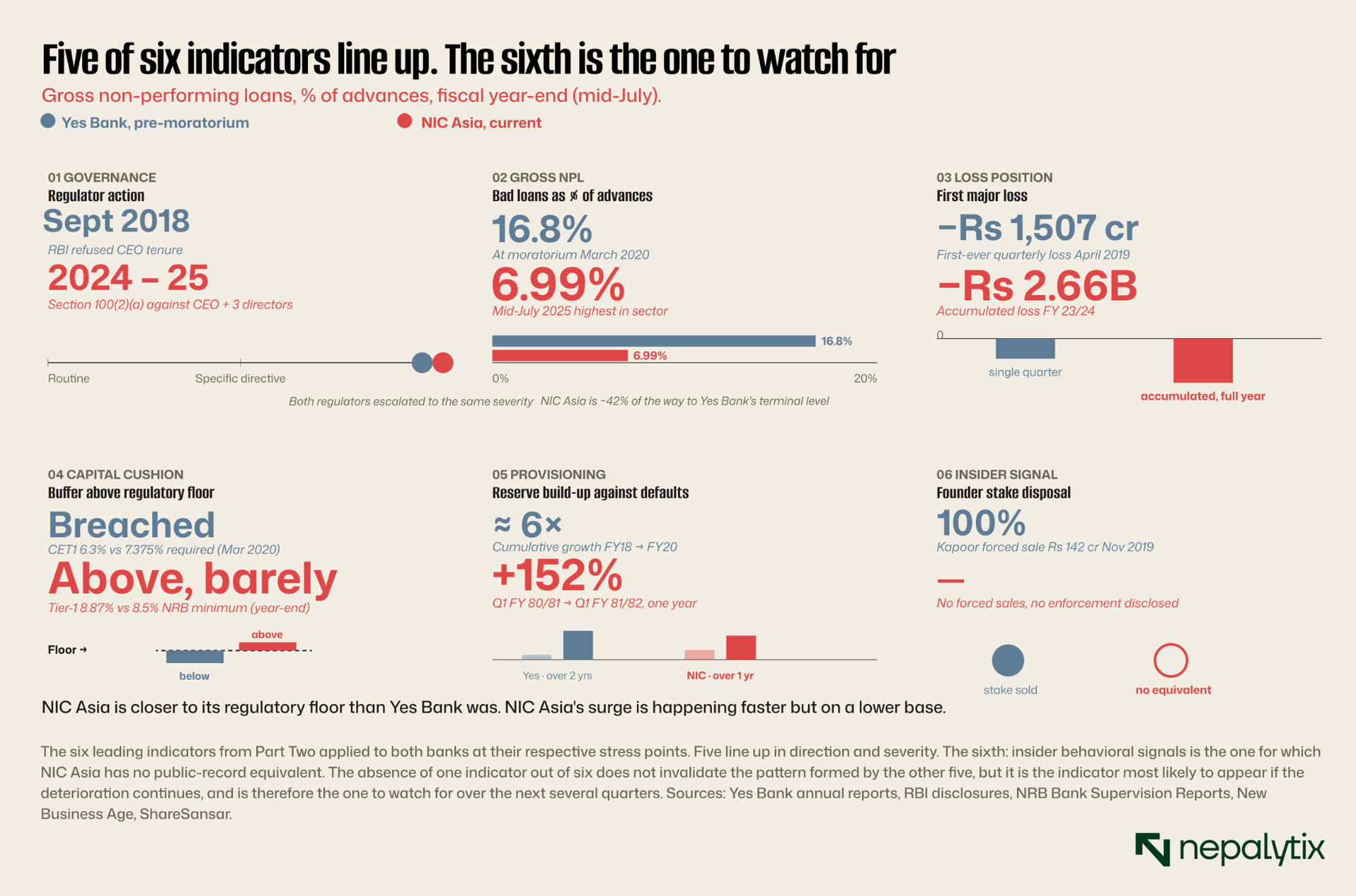

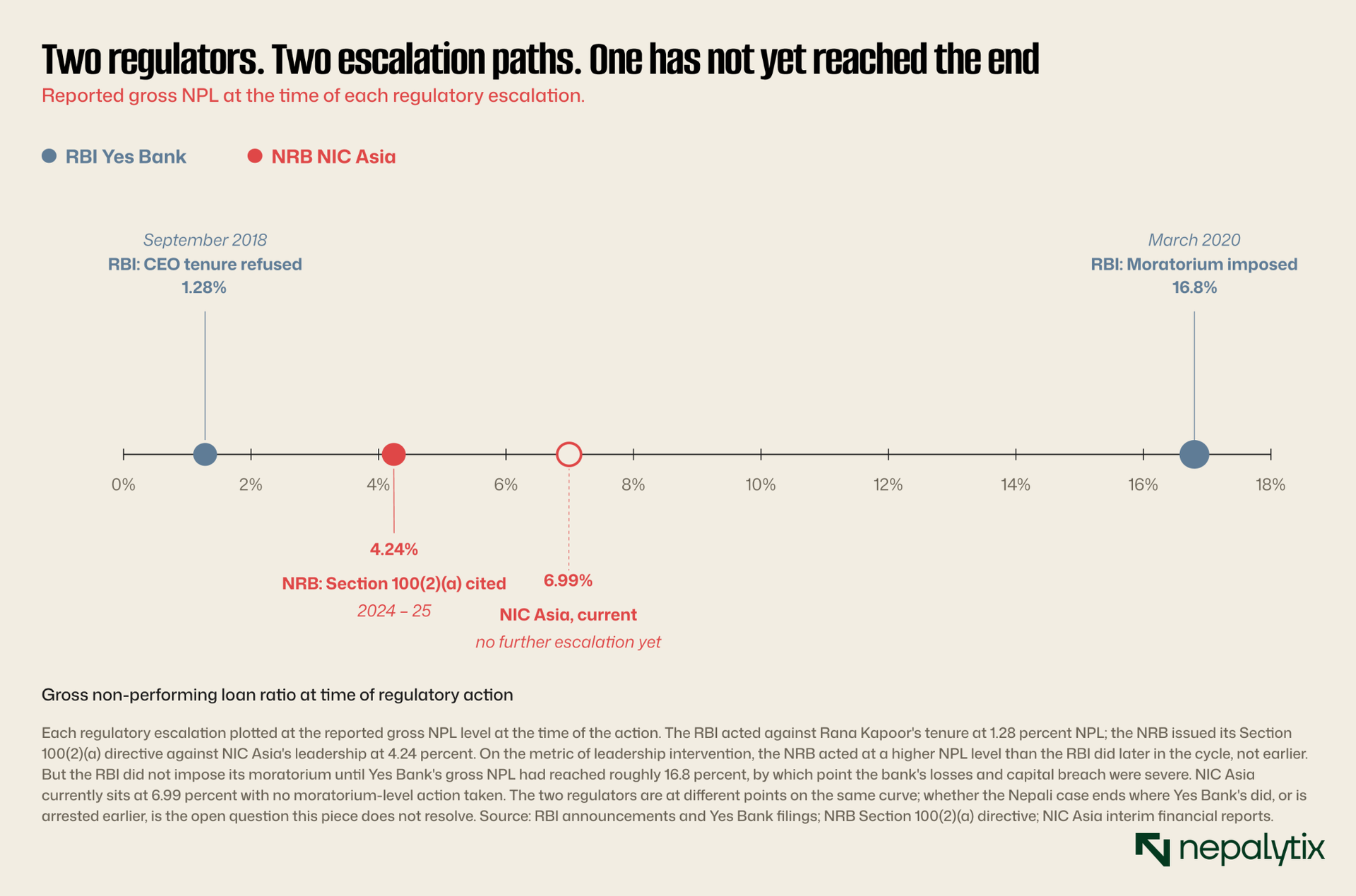

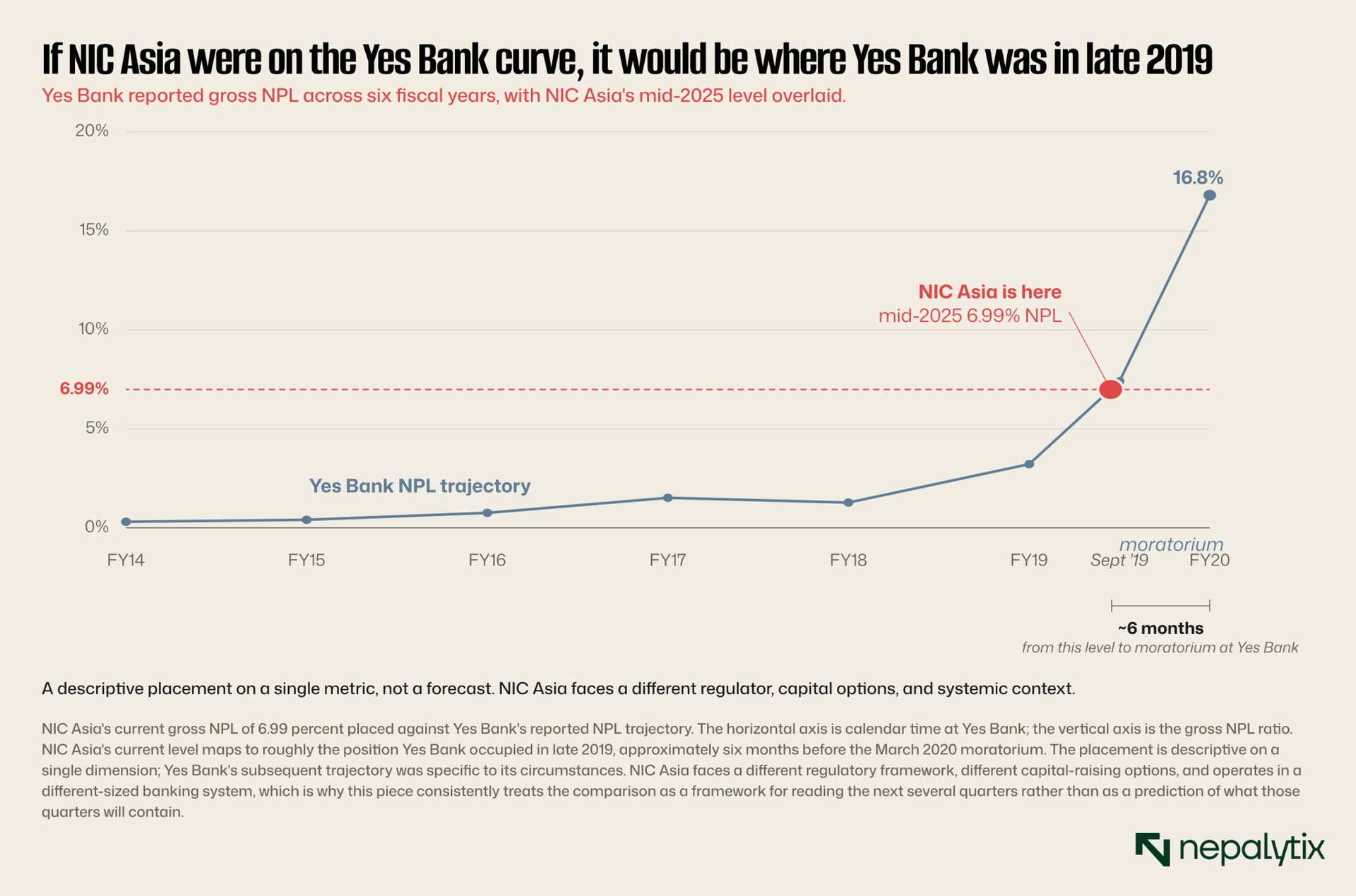

The short answer is that several of the indicators are remarkably similar. A few of them are different in important ways. And the most consequential difference is one of regulatory sequencing that cuts in two directions: Nepal's central bank the Nepal Rastra Bank cited specific statutory provisions against named senior leadership when NIC Asia's reported NPL was about 4.24 percent whereas the RBI acted against Yes Bank's leadership earlier at 1.28 percent reported NPL. But the RBI then allowed Yes Bank's position to deteriorate all the way to roughly 16.8 percent NPL before imposing its moratorium. So the NRB has not, on the leadership-action metric, moved earlier than the RBI did; the open question is whether it escalates further before NIC Asia reaches anything like the level at which the RBI finally intervened decisively. Whether that earlier intervention is decisive enough to break the pattern is the question this piece tries to address.

To do that, the piece walks through three things in order. First, what actually happened at Yes Bank between 2017 and March 2020 was not the headline collapse but the slow accumulation of warning signs that preceded it. Second, what is currently visible in the public record about NIC Asia. Third, where the parallel holds, where it breaks down and what it means for how observers should read the institution and the sector around it.

How Yes Bank actually fell apart

Yes Bank was founded in November 2003 by three Mumbai-based bankers Rana Kapoor, Ashok Kapur and Harkirat Singh using proceeds from the sale of their stakes in Rabo India Finance, a partnership they had previously built with the Netherlands-based Rabobank. The bank obtained its license from the Reserve Bank of India in May 2004 and opened its first branch in August of the same year. By 2005, it had launched an IPO that raised Rs 315 crore from the public market. By the early 2010s, Yes Bank was widely regarded as one of India's most successful private sector banks with a balance sheet that had grown at compound annual growth rates well above the industry average, an aggressive corporate banking franchise that competed effectively with larger established lenders and a brand that had become synonymous with the kind of high-growth, technology-forward private sector banking that the Indian financial press celebrated.

The growth was real. The corporate banking franchise was substantive. The brand was, for years, justified. What was not visible from the outside and what would become the central element of Yes Bank's eventual collapse was the quality of the loan book underneath the growth.

Under Rana Kapoor's leadership, Yes Bank had positioned itself in his own description as a "lender of last resort" to small and medium enterprises and to corporate borrowers who could not easily obtain credit from larger state-owned banks. The pitch was the standard pitch of any aggressive challenger bank that the larger lenders were too conservative, that the bank's superior credit assessment processes allowed it to identify borrowers who looked risky on paper but were actually viable and that the higher yields available on those loans more than compensated for any additional risk. The pitch was not, in itself, wrong. Many of the borrowers Yes Bank funded did become viable businesses. The problem was the discipline applied to the ones that did not.

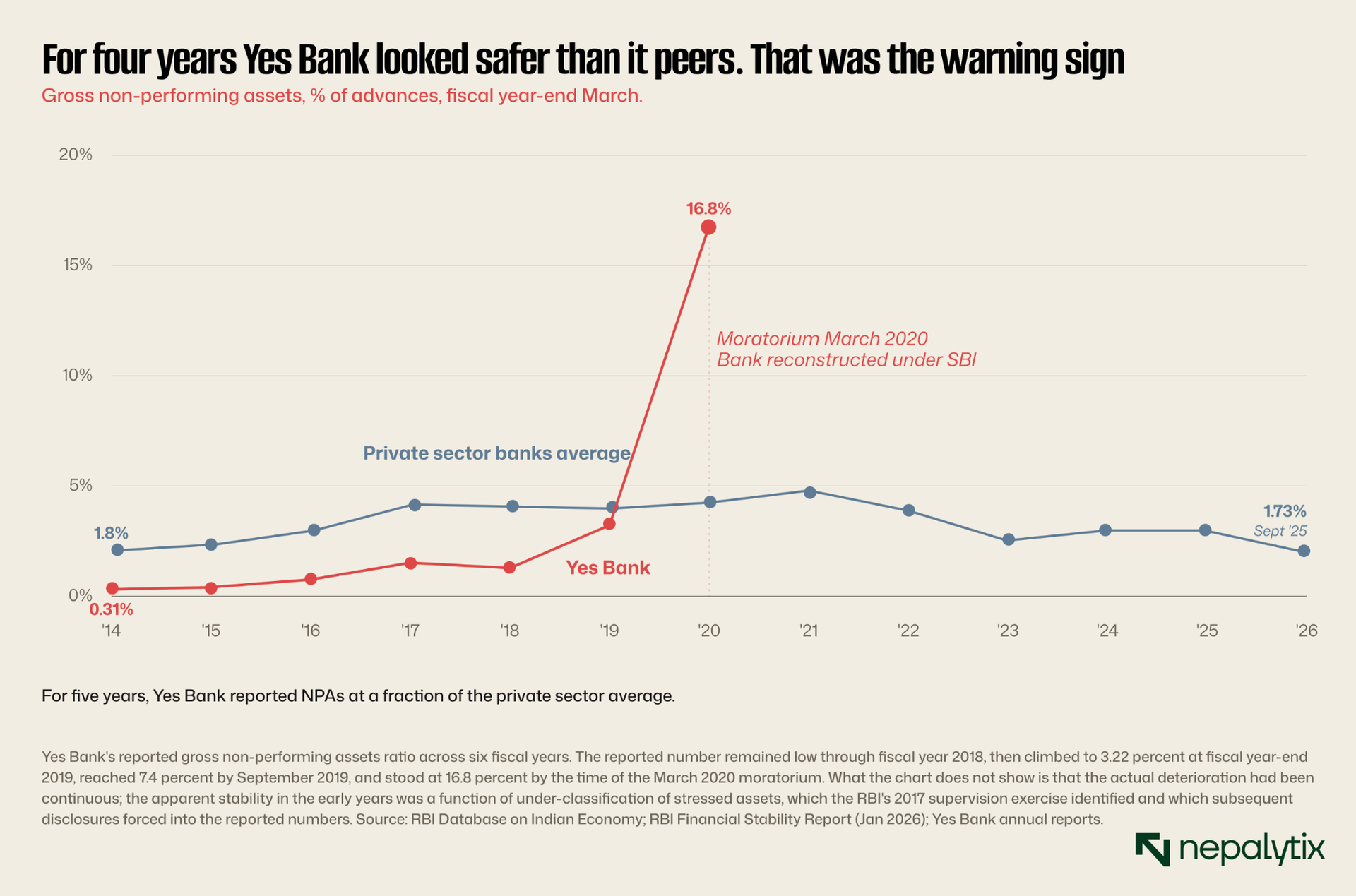

In 2017, the Reserve Bank of India's annual supervision exercise identified material under-reporting of non-performing assets at Yes Bank bad loans that the bank had not classified as bad, advances that should have been provisioned against but had not been. The under-reporting was substantial. In subsequent disclosures, the bank acknowledged that it had under-reported NPAs by approximately Rs 3,277 crore in fiscal year 2018-19 alone. The figures the bank had been publishing in its quarterly results to shareholders in other words had been understating the actual deterioration of its loan book by a meaningful margin for at least two reporting cycles and probably longer.

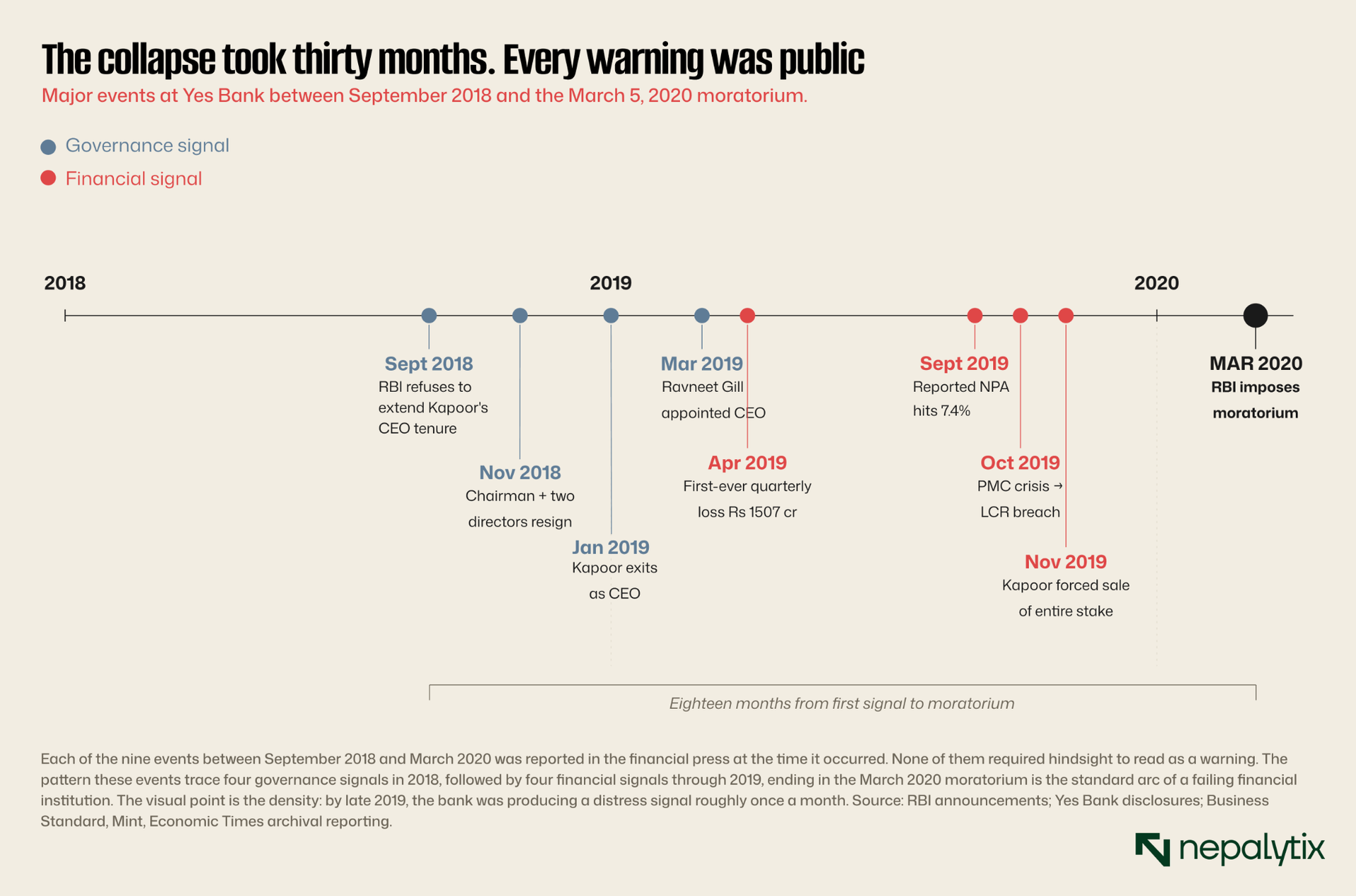

The RBI's response to the under-reporting was not, at first, a moratorium. It was a governance action. In September 2018, the central bank declined to extend Kapoor's tenure as managing director and chief executive officer. The action was not a removal, Kapoor was permitted to complete his term which ran until January 2019 but it was an unmistakable signal that the regulator had lost confidence in the bank's leadership. The signal was understood by the market. Within weeks of the RBI's announcement, Yes Bank's shares had fallen by more than thirty percent and the bank's cost of funds in the wholesale market had widened materially. The signal was also understood by Yes Bank's own board. In November 2018, the chairman and two independent directors resigned within a single week citing irreconcilable governance differences with the founder and his continued operational influence over the institution.

The events of 2019 followed the standard arc of a failing financial institution. In March, the bank appointed Ravneet Gill from Deutsche Bank as its new chief executive officer with a mandate to raise fresh capital and clean up the loan book. In April, Yes Bank reported its first quarterly loss in the institution's history of Rs 1507 crore, driven primarily by increased provisioning against previously under classified bad loans. In September, the reported gross NPA ratio jumped to 7.4 percent from 1.28 percent the prior fiscal year reflecting the cleanup that Gill's team was conducting. In October, a separate crisis at the Punjab and Maharashtra Cooperative Bank caused liquidity outflows from the broader Indian private banking sector and Yes Bank briefly breached its Liquidity Coverage Ratio requirement. In November, Rana Kapoor sold his entire remaining shareholding in the bank approximately Rs 142 crore worth of stock in what was reported as a forced sale to meet pledged-share commitments that had been invoked by his lenders. By the end of 2019, every public indicator of Yes Bank's health was flashing distress. The reported NPA ratio was at 7.4 percent and rising. The bank had reported its first-ever quarterly loss and was forecast to report further losses. Rating agencies had downgraded the bank's debt multiple times during the year. The founder had been forced to sell his entire shareholding. The chairman and two independent directors had resigned a year earlier. The CEO had been changed under regulatory pressure. The bank had attempted to raise fresh equity capital first through a planned investment from a Canadian institutional investor then through a smaller proposed deal with multiple investors and both attempts had failed to close. The Liquidity Coverage Ratio had been breached at least once. Deposit outflows had accelerated.

On March 5, 2020, the RBI moved. It imposed a thirty-day moratorium on Yes Bank capping depositor withdrawals at fifty thousand rupees superseding the existing board and appointing Prashant Kumar of the State Bank of India as administrator. Within four weeks, the central bank announced a reconstruction scheme: the State Bank of India would acquire 49 percent of Yes Bank's equity through a Rs 10,000 crore capital infusion joined by HDFC Bank, ICICI Bank, Axis Bank and Kotak Mahindra Bank as additional investors. Existing equity shareholders were diluted by approximately 90 percent. The Additional Tier-1 bonds Rs 8,415 crore worth of perpetual instruments that had been sold to retail and institutional investors as relatively safe fixed-income substitutes were written off entirely. A new board was appointed by the RBI. Yes Bank, as an independent corporate entity ceased to exist in the form in which it had been founded.

The collapse looked sudden from the outside. From the regulatory record, it had been thirty months in the making.

Six leaks. Each from a different actor under pressure

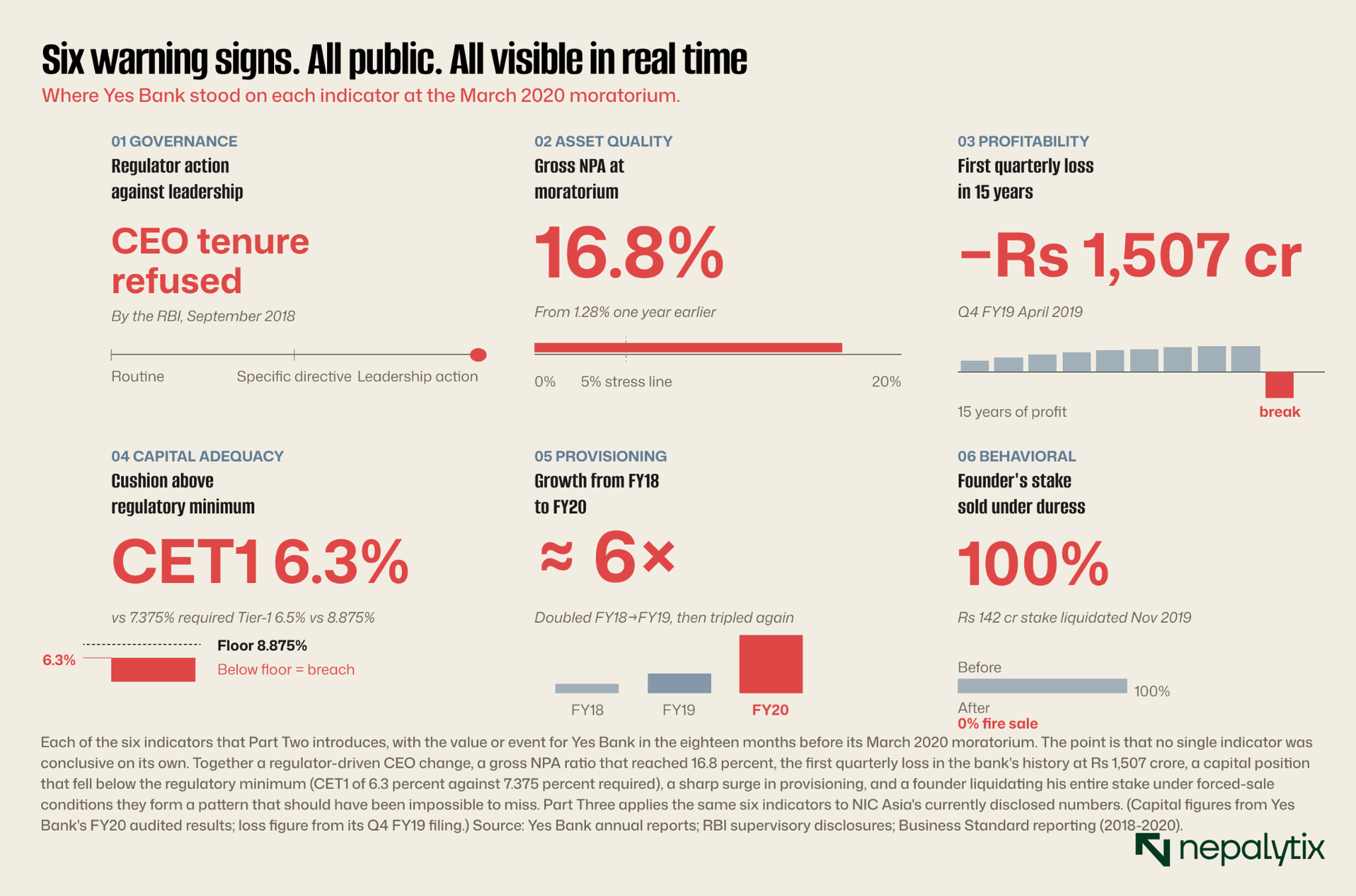

The Yes Bank case is now a standard study in Indian banking regulation. The institutional record: the EliScholar Yale case study, the RBI's own supervisory reports, the multiple academic papers in the Indian Journal of Finance and the Journal of Central Banking Theory converges on six categories of leading indicators that were visible in the public record before the March 2020 moratorium. Each of them could have been identified by an analyst reading the bank's quarterly filings and the RBI's annual supervision reports. None of them required access to private supervisory information. All of them, in retrospect, mattered.

What makes these six useful rather than arbitrary is that each captures a different actor revealing information involuntarily. The regulator reveals supervisory concern through formal actions against named leadership and through divergence findings that force restatement of NPAs. Management reveals stress through the timing of the first quarterly loss, the size of provisioning increases that eat into reported profit before any loan is formally written off and the degree to which the capital adequacy ratio drifts toward the regulatory floor. Insiders reveal their private estimate of the institution's prospects through the timing and forced character of their own share sales. The six categories: governance, asset quality, profitability, capital adequacy, provisioning, behavioral are not a checklist someone wrote up after the fact. They are the points at which information that the bank would prefer to keep internal leaks out under regulatory or market pressure.

At Yes Bank, all six leaked between September 2018 and November 2019. The RBI refused Rana Kapoor's CEO tenure extension while the reported gross NPA was 1.28 percent, a figure that, after the cleanup forced by Ravneet Gill's team in 2019 was revised to 7.4 percent and ultimately 16.8 percent by the time of the moratorium. The first quarterly loss came in April 2019. By the time of the moratorium the bank's capital had fallen below the regulatory minimum entirely: a Common Equity Tier-1 ratio of 6.3 percent against 7.375 percent required, and a Tier-1 ratio of 6.5 percent against 8.875 percent required. This was a breach, not a thin cushion. Provisioning expenses approximately doubled FY18 to FY19 and tripled again into FY20. And in November 2019, four months before the moratorium, Rana Kapoor sold his entire remaining shareholding approximately Rs 142 crore under what was reported as forced-sale conditions to meet pledged-share margin calls.

Each of the six indicators was visible in the public record. Each of them, individually, would have been a meaningful warning. Together, they constituted a pattern that should have been impossible to miss. The question for an analyst reading any bank's public disclosures in any market, two years after Yes Bank, is whether the same indicators are visible elsewhere.

The pattern at NIC Asia: Six indicators, applied to a different bank in a different country

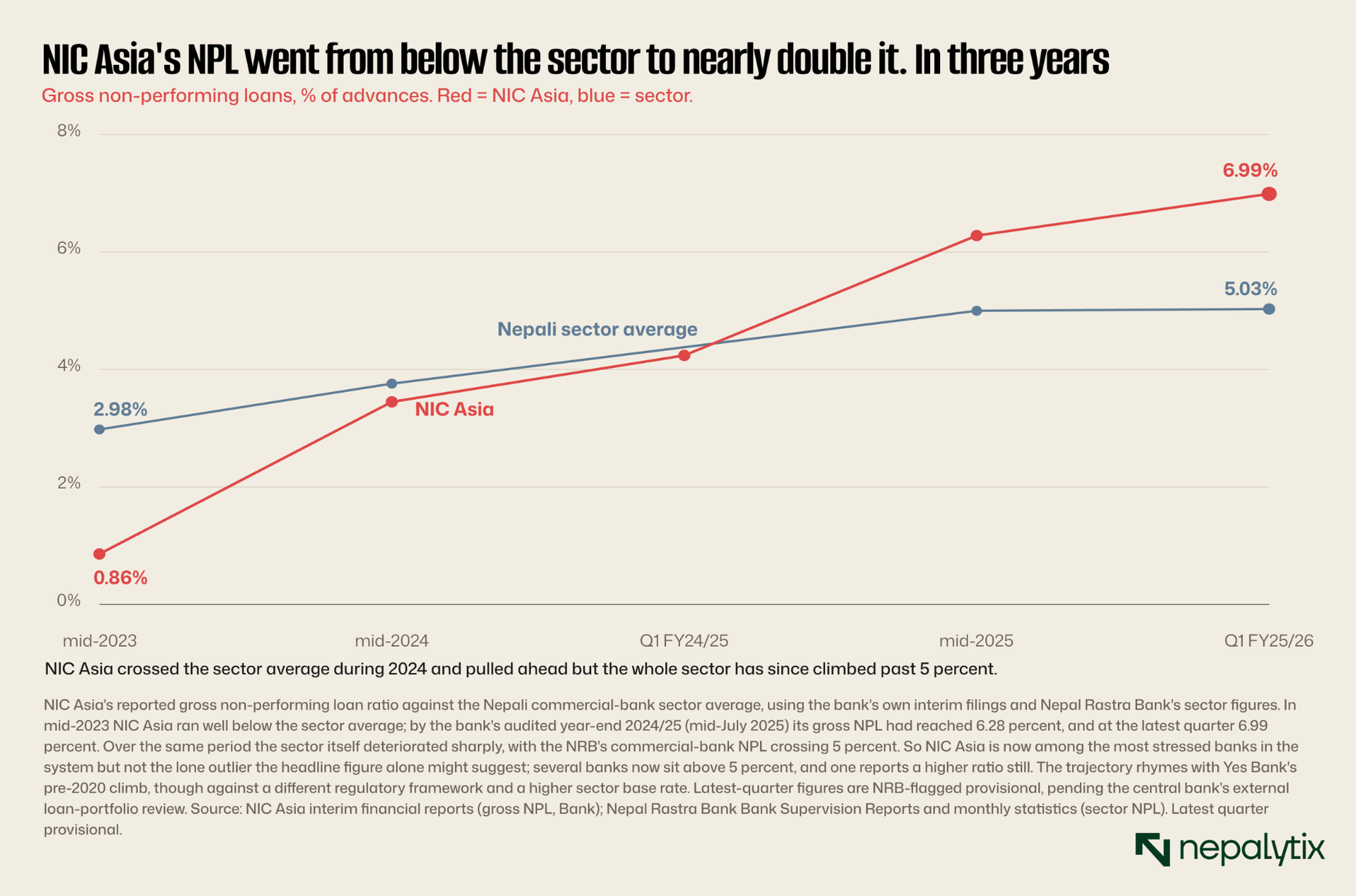

NIC Asia Bank Limited is the fourth-largest commercial bank in Nepal by deposit base, the result of a 2013 merger between NIC Bank Limited and Bank of Asia. The combined entity has built itself over the subsequent decade into one of Nepal's most aggressive private-sector lenders with a deposit base about Rs 319 billion at its audited year-end (mid-July 2025), a loan book of Rs 266 billion and a paid-up capital position of Rs 14.91 billion. Through the late 2010s and early 2020s, the bank reported consistently strong profits ranking in the top quartile of Nepali commercial banks by net income in most years. In fiscal year 2022/23, the bank's reported net profit was Rs 3.53 billion, a meaningful contribution to a sector total of approximately Rs 71 billion across all twenty commercial banks.

In fiscal year 2023/24, something broke.

The reasons for the deterioration are by now reasonably well-documented in the public record. In late 2024 and early 2025, the Nepal Rastra Bank issued a series of supervisory communications to NIC Asia's board and management regarding asset quality, capital position, and the bank's practice of charging excess interest to retail borrowers. The supervisory record shows that the central bank's engagement with NIC Asia escalated substantially during this period moving from routine prudential dialogue to formal corrective directives within twelve months. The bank's response, visible in its quarterly disclosures, has been to recognize losses, increase provisioning, and consult with the regulator on capital-raising plans.

The third-quarter results for fiscal year 2081/82 published in April 2025 were the clearest single data point. NIC Asia reported a cumulative nine-month net profit of Rs 156.7 million approximately Rs 15.67 crore against a prior-year comparable figure of Rs 1.91 billion. The year-on-year decline in nine-month cumulative net profit was 91.81 percent. The bank's annualized earnings per share for the period was Rs 1.40, the lowest among the twenty Nepali commercial banks reporting third-quarter results. The industry average earnings per share for the same period was Rs 15.12 with eleven banks reporting figures above the industry average.

If we apply the Yes Bank framework the six leading indicator categories identified in the previous section to NIC Asia's currently available public record, the parallel is uncomfortably direct.

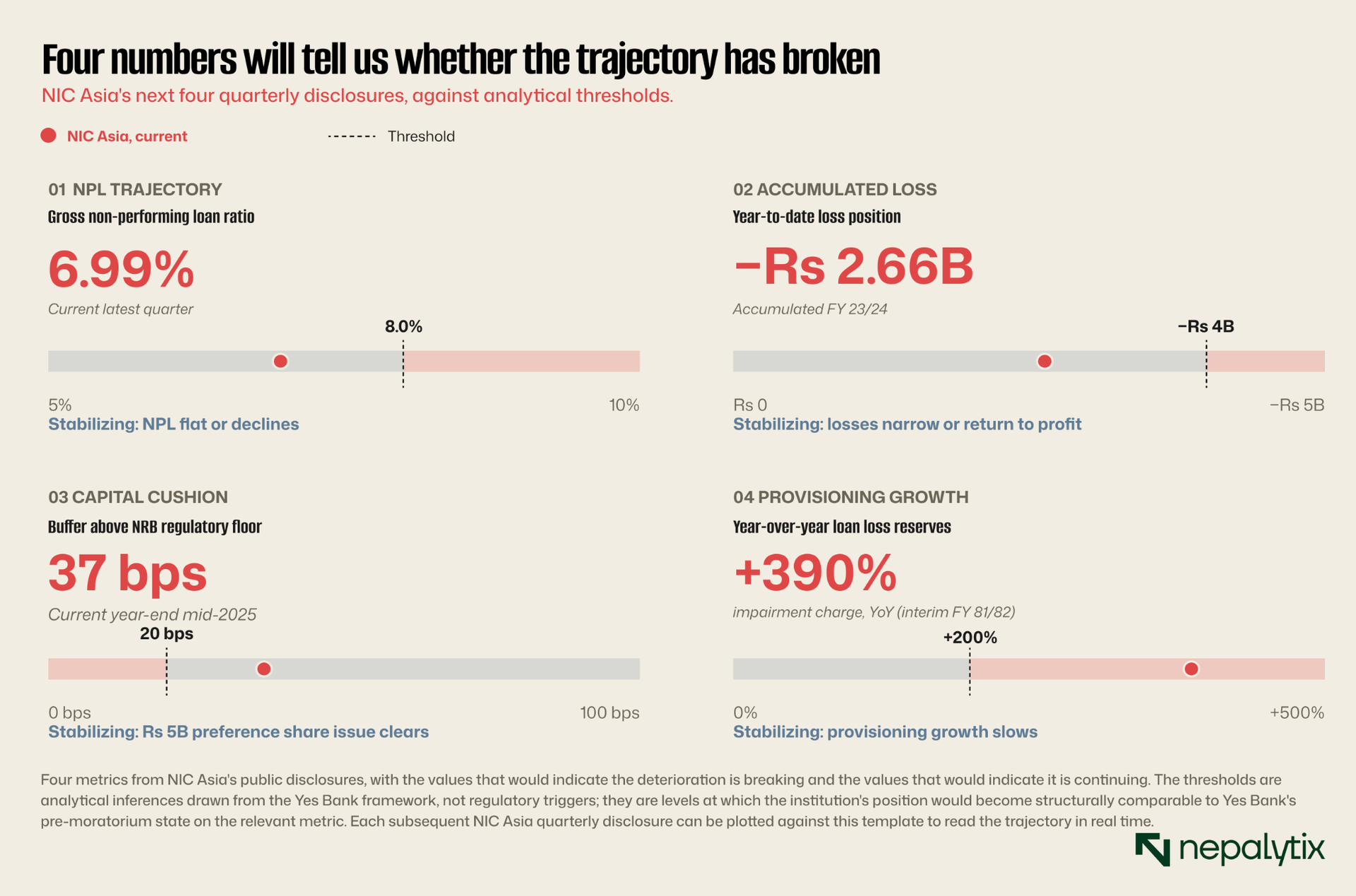

NIC Asia's reported gross non-performing loan ratio at fiscal year-end 2023/24 was 3.45 percent. By the first quarter of fiscal year 2024/25 it was 4.24 percent; at the audited year-end 2024/25 (mid-July 2025) it reached 6.28 percent, and at the latest quarter it stood at 6.99 percent among the highest in the Nepali commercial banking sector though not the single highest,and well above the NRB's sector average of roughly 5 percent. The deterioration of several percentage points in roughly two years is comparable, in rate, to the Yes Bank deterioration between 2018 and 2019. The current level 6.99 percent is close to the 7.4 percent Yes Bank reported in September 2019, about six months before its moratorium; though Yes Bank's NPL then ran far higher, to 16.8 percent, before the RBI acted decisively.

Move to profitability. NIC Asia's nine-month net profit through Q3 of fiscal year 2081/82 was Rs 156.7 million, against Rs 1.91 billion in the comparable period of the prior year, a 91.81 percent year-on-year decline. The full-year accumulated loss for fiscal year 2023/24 was Rs 2.66 billion. This is not a cyclical fluctuation; it is the earnings profile of a different bank. The closest Yes Bank parallel was the bank's April 2019 first quarterly loss of approximately Rs 1507 crore which had been reported within twelve months of the RBI's September 2018 governance action.

Move to provisioning. The bank's loan loss provisions roughly Rs 2.3 billion to Rs 5.8 billion year on year (about 152 percent), while its impairment charge the current-period flow rather than the accumulated stock rose even more steeply, on the order of 390 percent in the interim results. Either way, the increase is, mechanically, an admission by the bank's own management that a substantially larger portion of the loan book is expected to default than was previously classified.The provisioning surge is what is driving the current profit collapse: most of the reduced reported income is being absorbed by reserves against future defaults, not by the defaults themselves.

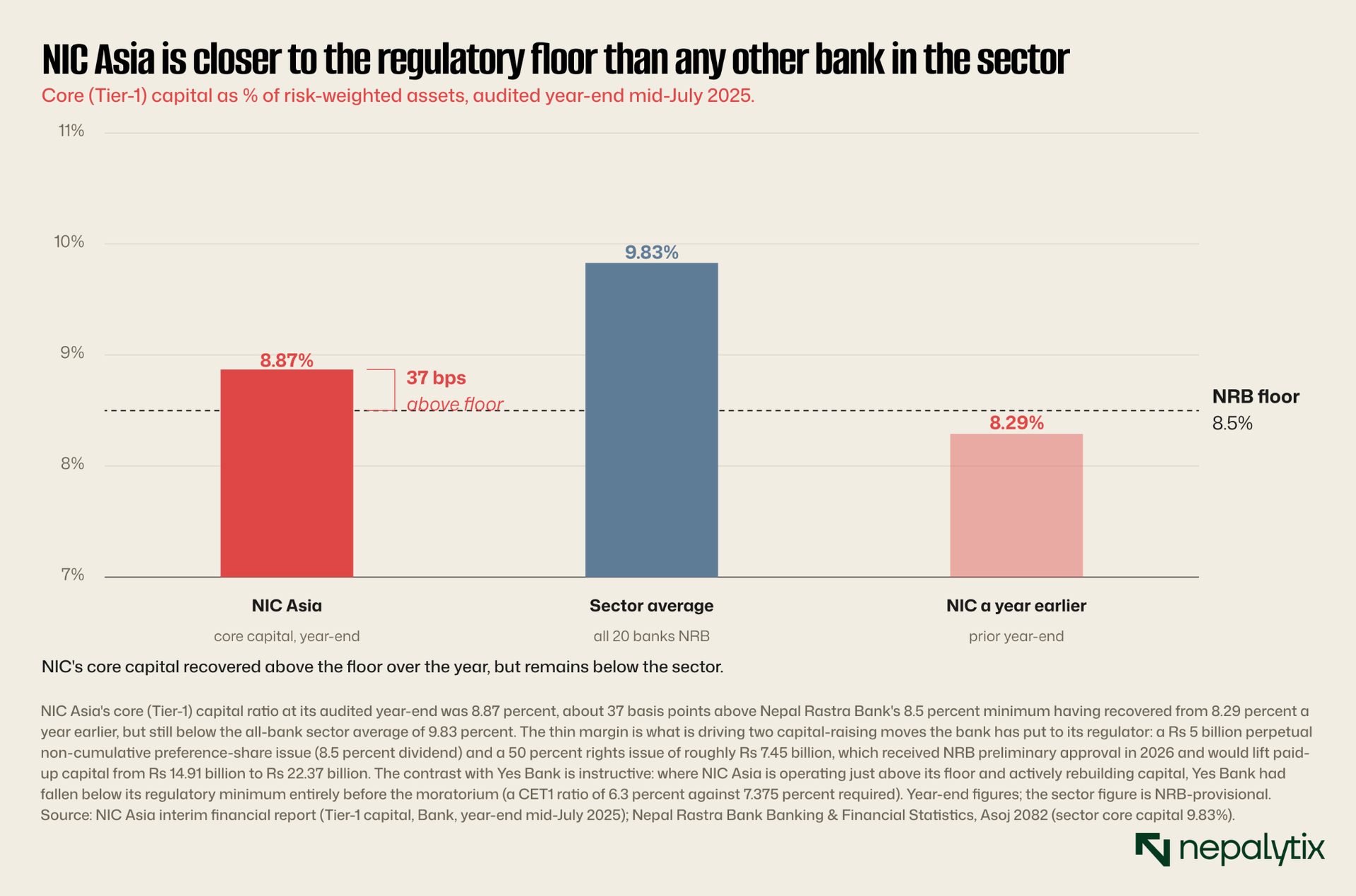

Move to capital adequacy. NIC Asia's core (Tier-1) capital ratio at its audited year-end was 8.87 percent, against a regulatory minimum of 8.5 percent, a cushion of about 37 basis points, up from 8.29 percent a year earlier but still below the all-bank sector average of roughly 9.83 percent. For a bank with a deposit base of about Rs 319 billion and a loan book that is actively deteriorating, that is the kind of margin that gets consumed by a single bad reporting period. The bank has two capital-raising moves before its regulator: a Rs 5 billion perpetual non-cumulative preference-share issue and a 50 percent rights issue of roughly Rs 7.45 billion, which received NRB preliminary approval and would lift paid-up capital from Rs 14.91 billion to Rs 22.37 billion. Whether the issue clears at the planned price and on the planned timeline is one of the more important things to watch in the next several quarters.

Move to governance. In late 2024 and early 2025, the Nepal Rastra Bank issued a specific supervisory directive to NIC Asia citing Section 100(2)(a) of the Nepal Rastra Bank Act against the chief executive officer Roshan Neupane, chairman Tulsi Ram Agrawal, and directors Trilok Chandra Agrawal and Ramchandra Sanghai. The directive required the named individuals to refrain from continuing certain interest-rate practices that the central bank had determined to be inappropriate, and required the bank to refund excess interest charged to borrowers. The use of Section 100(2)(a) is a specific statutory tool that the NRB does not deploy frequently or casually. The Yes Bank parallel is the RBI's September 2018 refusal to extend Rana Kapoor's CEO tenure, a specific regulator-initiated action against named senior leadership, taken in response to identified prudential concerns.

Move to dividend behavior. NIC Asia's annual general meeting in March 2025 was asked to approve a proposal to forgo dividend distribution for fiscal year 2023/24 the year in which the bank reported its first major accumulated loss. The proposal was approved. This was not the first time NIC Asia had been required to forgo dividends; the NRB had previously restricted dividend payouts for fiscal years 2020/21 and 2021/22 on the grounds that the bank was not maintaining adequate core capital. The cumulative pattern is of a bank that has, across multiple fiscal years, been unable to meet the capital position required to distribute earnings to shareholders. The Yes Bank parallel is the suspension of dividends that preceded the 2020 moratorium.

The sixth Yes Bank indicator, behavioral signals from insiders is the one for which the NIC Asia parallel is, as of this writing, less direct. There is no public record of forced share sales by NIC Asia's founders or senior management. There are no money laundering charges, no enforcement actions against individuals, no equivalent of Rana Kapoor's November 2019 fire sale. The absence of this particular signal is meaningful and should not be glossed over. But the absence of one indicator out of six does not invalidate the pattern formed by the other five. It modifies the assessment; it does not negate it.

Standing back, then, the pattern at NIC Asia in 2025 maps closely to the pattern at Yes Bank in 2018-2019. The asset quality trajectory is structurally similar. The profitability collapse is more severe in percentage terms than Yes Bank's 2019 first quarterly loss. The provisioning surge follows the same direction. On capital, the comparison actually runs the other way: NIC Asia remains just above its regulatory floor, whereas Yes Bank had breached its minimum outright before the moratorium so NIC's position is less dire than Yes Bank's was at the comparable stage. The governance action is comparable in nature, though different in specific statutory tools. The dividend forgone is the same. And NIC Asia's deterioration, while the sharpest single case, is occurring within a sector that has broadly crossed the 5 percent NPL line not in isolation. The one missing indicator inside behavioral signals is conspicuous in its absence but not, by itself, dispositive.

Where the parallel breaks down

The strength of an analytical parallel is measured by where it breaks. A framework that explains everything explains nothing. The Yes Bank framework applied to NIC Asia is genuinely informative; it is also incomplete in ways that matter for any forward assessment. Three differences in particular, are consequential.

The first and most important is the timing of regulatory intervention. The RBI's September 2018 governance action against Rana Kapoor came at a point when Yes Bank's reported gross NPA was 1.28 percent although the under-reporting issue meant that the actual figure was materially higher. The RBI's next escalation, the March 2020 moratorium did not come until the reported figure had reached roughly 16.8 percent. There was in other words a long gap during which the bank's asset quality deteriorated enormously before the central bank moved to the moratorium stage. The Nepal Rastra Bank's Section 100(2)(a) action against NIC Asia's leadership came when the bank's reported gross NPL was 4.24 percent. NIC Asia's current NPL of about 6.99 percent has not triggered any escalation to moratorium-level intervention, and may not. The picture on timing is therefore mixed: on the leadership-action metric the NRB actually moved at a higher NPL than the RBI did (4.24 versus 1.28 percent), but the RBI then tolerated deterioration far beyond NIC Asia's current level all the way to about 16.8 percent before its decisive intervention.

Whether the action taken so far is sufficient to break the pattern is the question. The deterioration at NIC Asia continued from 4.24 percent at the time of the NRB action to about 6.99 percent over the following several quarters. The provisioning expanded. The accumulated loss grew. The core capital ratio held about 37 basis points above the regulatory minimum, but the loan book on which that capital is calculated is by every available measure of lower quality than it was a year ago. The NRB's governance action has not, on the current evidence, halted the deterioration though NIC Asia remains far short of the NPL level at which the RBI ultimately moved against Yes Bank. Whether the planned Rs 5 billion preference share issue, the dividend forgone and the corrective action plan submitted to the central bank are sufficient to break the trajectory is something that will be visible in the next two to four quarterly reports.

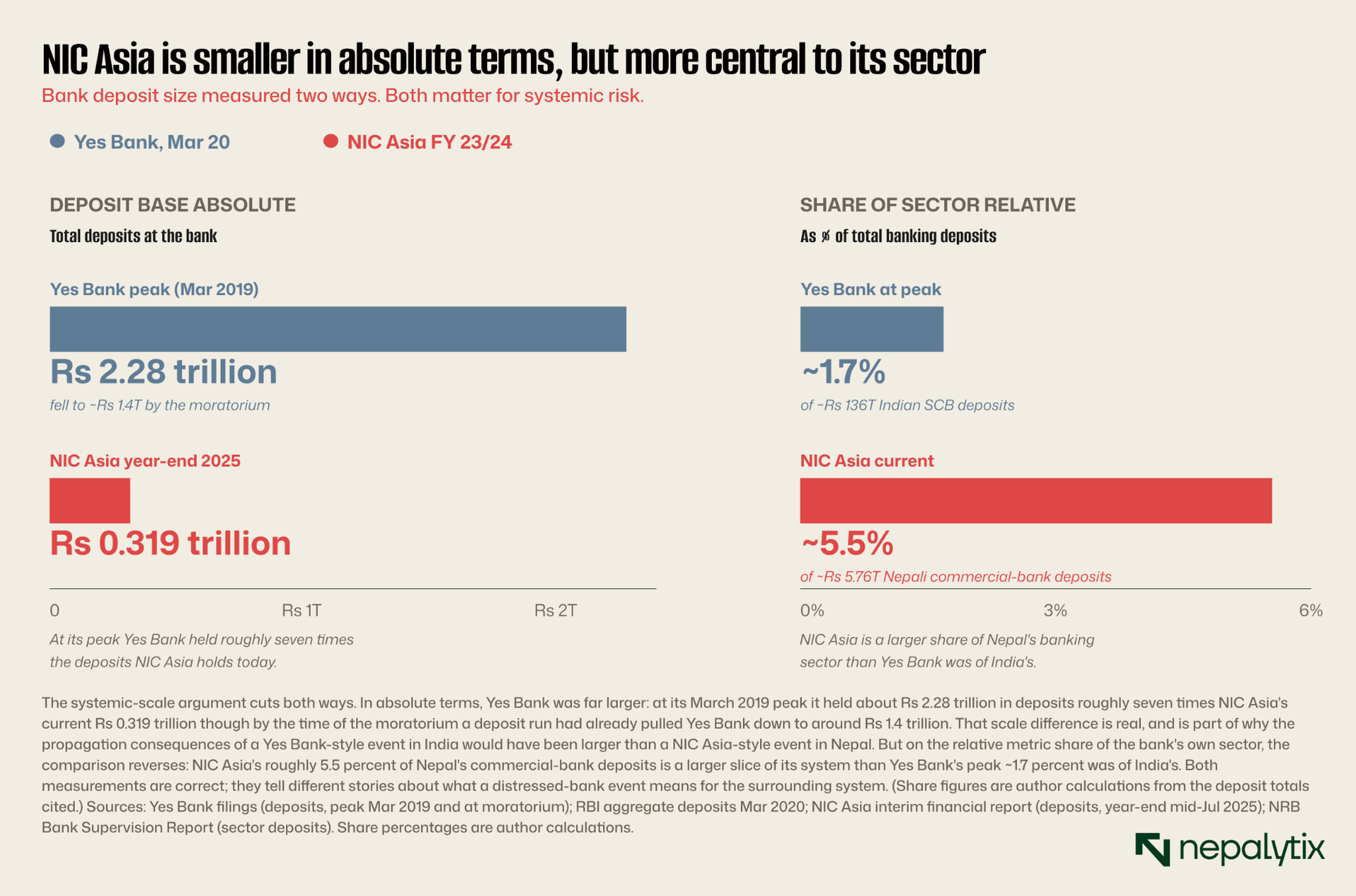

The second difference is systemic scale. Yes Bank, at its peak, was India's fourth-largest private sector bank by deposits with a deposit base of about Rs 2.28 trillion at its March 2019 peak, though a deposit run had pulled that down to roughly Rs 1.4 trillion by the time of the moratorium. A failure event at Yes Bank would have rippled through the Indian financial system with consequences that the RBI was, in March 2020, explicitly engineering the bailout to prevent. NIC Asia, in the Nepali context, is large but not systemically central in the same way. Its deposit base of about Rs 319 billion is meaningful but does not approach the size at which a failure would propagate uncontrollably through the broader sector, which gives the Nepal Rastra Bank more options for resolving an NIC Asia distress scenario than the RBI had for Yes Bank including options short of a moratorium-style intervention.

The third difference is the off-balance-sheet structure. Yes Bank's Additional Tier-1 bond issuance of Rs 8,415 crore of perpetual debt instruments sold to retail and institutional investors became one of the central controversies of the 2020 collapse. The instruments were written off entirely during the reconstruction, leaving bondholders with zero recovery and triggering ongoing litigation that has continued for years. NIC Asia does not, as of public disclosure, have an equivalent off-balance-sheet retail-distributed perpetual instrument outstanding, which means the constituencies that would be affected by a hypothetical distress event are different and the Yes Bank-style controversy over wiped-out AT-1 holders is not part of the NIC Asia setup.

These three differences: earlier regulatory intervention, lower systemic centrality, simpler capital stack do not invalidate the parallel. They modify the trajectory. They suggest that even if NIC Asia's underlying deterioration follows a similar path to Yes Bank's, the resolution may take a different form. A reconstruction-style intervention with mandatory equity dilution and bondholder write-off is the most likely Yes Bank-analogous outcome; for NIC Asia, the more likely scenarios may involve regulator-supervised capital raising, board reshuffling, asset disposals, or eventual managed merger with a stronger bank. None of these are good outcomes for current equity holders. Several of them are meaningfully less bad than the Yes Bank scenario was.

What this means going forward: For NRB, for NIC Asia, for analysts reading the next set of quarterly disclosures

For the Nepal Rastra Bank, the most important next question is whether the corrective action plan currently in place at NIC Asia is sufficient. The Section 100(2)(a) action against the bank's leadership was meaningful, and the earlier timing of the intervention relative to Yes Bank is genuinely better. But the deterioration has continued: the NPL has moved from 4.24 percent at the time of the NRB action to about 6.99 percent. The accumulated loss has grown. The core capital cushion is around 37 basis points. On the public evidence available, the corrective action plan is not yet halting the trajectory. Whether the NRB now escalates to additional supervisory measures, requires external recapitalization, mandates management changes, or invokes additional statutory tools will determine whether the parallel with Yes Bank ultimately breaks or holds.

NIC Asia's board and management face an immediate operational task that is straightforward in framing if not in execution. The bank needs to demonstrate, in the next two quarterly reporting cycles, that the deterioration has stopped by reducing the NPL trajectory completing the planned Rs 5 billion preference share issue at acceptable terms, recovering or writing off the existing stock of problem loans in a way that allows the loan book to be re-baselined and rebuilding the capital cushion to a level that gives the institution actual operational flexibility.

Analysts reading the Nepali banking sector should take the more general lesson. The leading-indicator framework that worked at Yes Bank asset quality trajectory, profitability inflection, provisioning surge, capital cushion compression, regulator-initiated governance action, dividend behavior is generalizable across emerging market private-sector banks, and it is reasonable to apply the same framework, in real time, to other Nepali banks that may be showing similar patterns. By the NRB's own figures the sector-wide NPL has crossed 5 percent, with roughly nine of the twenty commercial banks above that line and at least one private bank reporting a gross NPL higher than NIC Asia's so the stress is broad, not confined to a single institution. NIC Asia is the clearest single-bank case. It may not be the only one.

Equity investors with positions in NIC Asia specifically should be asking a different question. It is not known whether the bank will fail outright; the regulatory toolkit available to the NRB makes a Yes Bank-style outright failure substantially less likely than the underlying deterioration would suggest. The question is what the recovery path looks like for current shareholders. A dilutive recapitalization at significantly below current trading prices is the most likely intermediate-term scenario. A managed merger with a stronger institution, at terms that protect depositors and absorb the existing capital, is also possible. Either scenario implies meaningful equity dilution for current holders, and neither is consistent with the bank trading at its current valuation as a normal-bank stock.

The broader question for the Nepali financial system is whether NIC Asia represents an isolated case of aggressive growth meeting credit-cycle reality, or whether it is the leading edge of a sector-wide pattern. The sector data an average NPL of roughly 5 percent against historical norms below 3 percent, elevated total banking sector provisions of Rs 35.07 billion in a single quarter, several other banks with NPL ratios in the 4 to 5 percent range suggests that NIC Asia is the most extreme expression of a stress that exists more broadly. The Yes Bank parallel for NIC Asia is the strongest. The parallel may be weaker but still meaningful for other banks. The next twelve to twenty-four months in Nepali banking will be defined by how the consequences of the post-COVID credit expansion are absorbed against a low-rate, low-credit-demand environment that compresses bank profitability while requiring elevated provisioning against legacy loan books.

If NIC Asia were on the Yes Bank curve, it would be at approximately Q2 2019. The next eighteen months are when the question gets answered.

The Yes Bank lesson applied to NIC Asia is that the warning signs were visible in the public record. They were identifiable in real time. They did not require hindsight to read. The Indian regulatory response, in retrospect, was too slow at the early stages and too consequential at the late stage, a moratorium that protected systemic stability but wiped out shareholders and AT-1 bondholders in the process. The Nepali regulatory response so far has been earlier and more measured. Whether it is sufficient is an open question.

What is certain is that the next four quarters of NIC Asia's public disclosures will tell us. The NPL trajectory either stabilizes or continues. The accumulated loss either narrows or widens. The capital cushion either rebuilds via the planned preference share issue or it does not. The provisioning either normalizes or escalates further. Each quarterly report will, in retrospect, be either the inflection point or another data point on the same curve.

It was a Thursday morning in March 2020 when the queues began to form outside Yes Bank ATMs across India. The pattern that produced those queues was visible thirty months earlier. The Nepali pattern is visible now. Whether it produces the same queues or a different ending depends on what the next four quarters look like and on whether the regulatory action that has already occurred, and the regulatory action that is yet to come, is sufficient to break a trajectory that, on its current path, points to an outcome no one in Nepal's banking sector should want to see arrive.