NIC Asia bank recovery isn't still visible in numbers

NIC Asia’s share price suggests recovery, but its latest results tell a more complicated story of weak earnings, elevated NPLs, and ongoing balance sheet repair.

Three fiscal years ago NIC Asia earned the highest EPS of any Nepali commercial bank. Today it earns the lowest. The Q3 print released in April 2026 says the recovery the share price implies is not yet visible in the numbers and the numbers say the bank is in a balance-sheet repair that will take longer than the market is willing to wait.

At Rs 353, NIC Asia trades on a P/B of roughly 2.04x against book value of Rs 172.97 and an annualised P/E above 280x. The market is pricing recovery on a timeline that the Q3 results, released in April 2026, do not support. Net profit for the first nine months of FY 2082/83 fell to Rs 140.3 million from Rs 156.7 million the previous year, a decline of 10.49%. Net interest income fell 20.78% to Rs 6.30 billion. Distributable profit deepened to negative Rs 13.65 billion, approximately 92% of paid-up capital. The Q1 turnaround under new CEO Santosh Rathi, where net profit rose 10.52% YoY, did not carry through Q2 and Q3.

This piece walks through eight angles on what the Q3 print actually says: the four-year earnings collapse, the divergence from the sector leader, how interest income compressed, the asset quality trajectory and where it sits in sector ranking, the balance sheet contraction nobody is discussing, the cost of funds inversion, the capital cushion that is thinner than it looks, and the sector-wide positioning map that places NIC Asia alone in the corner of the chart. The piece ends with three fair value scenarios and what each one requires the next four quarters to deliver.

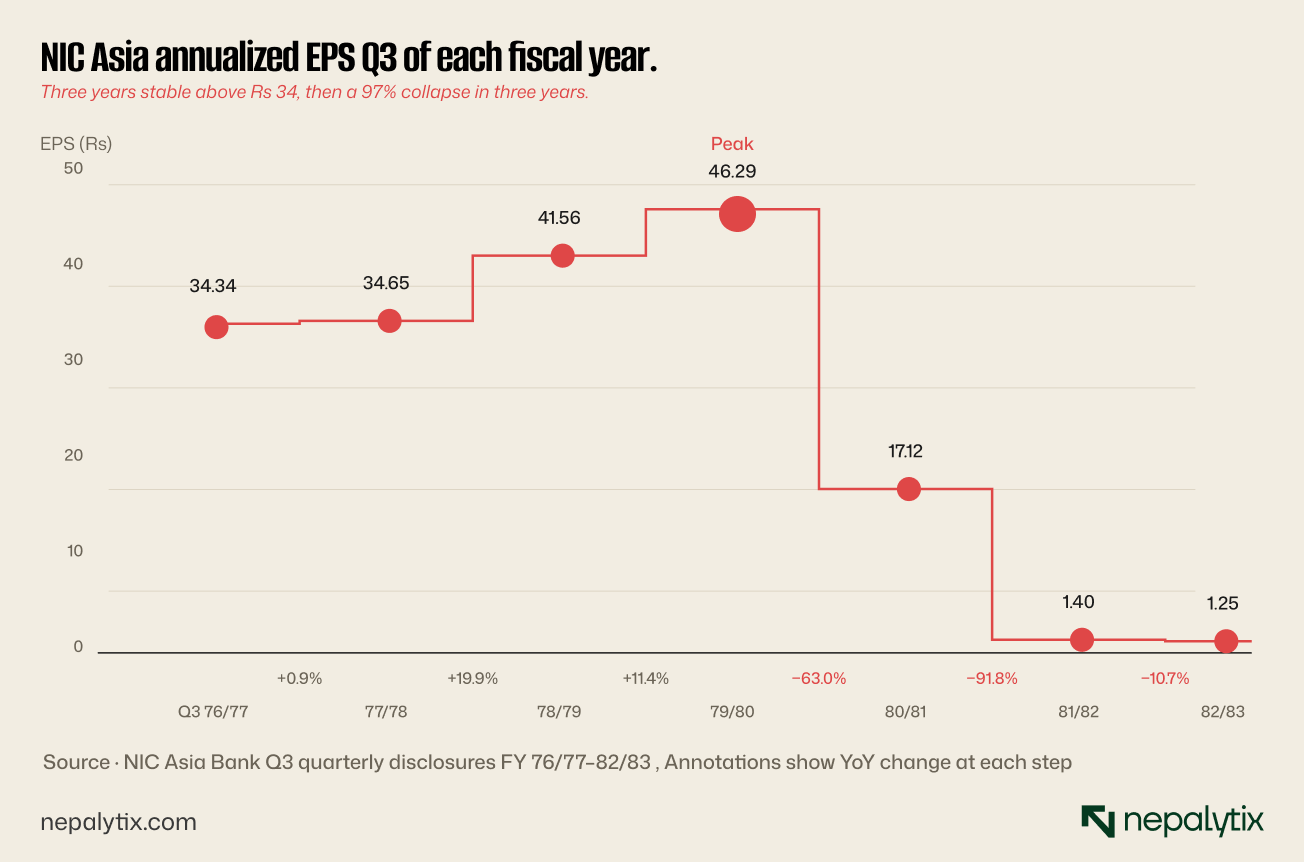

The collapse, in one line

NIC Asia's Q3 EPS peaked at Rs 46.29 in fiscal year 2079/80. It was a stable performer for three years before that, sitting in the Rs 34–42 range. Over the four years since the peak, EPS has moved to Rs 17.12, then Rs 1.40, then Rs 1.25, a 97% decline from the FY 79/80 high. The deterioration is not a single bad quarter that mean-reverts. It is a sustained four-year slide where each fiscal year's print has been weaker than the last, and the rate of decline has only recently slowed because the absolute level has nowhere left to fall.

The divergence from the sector leader

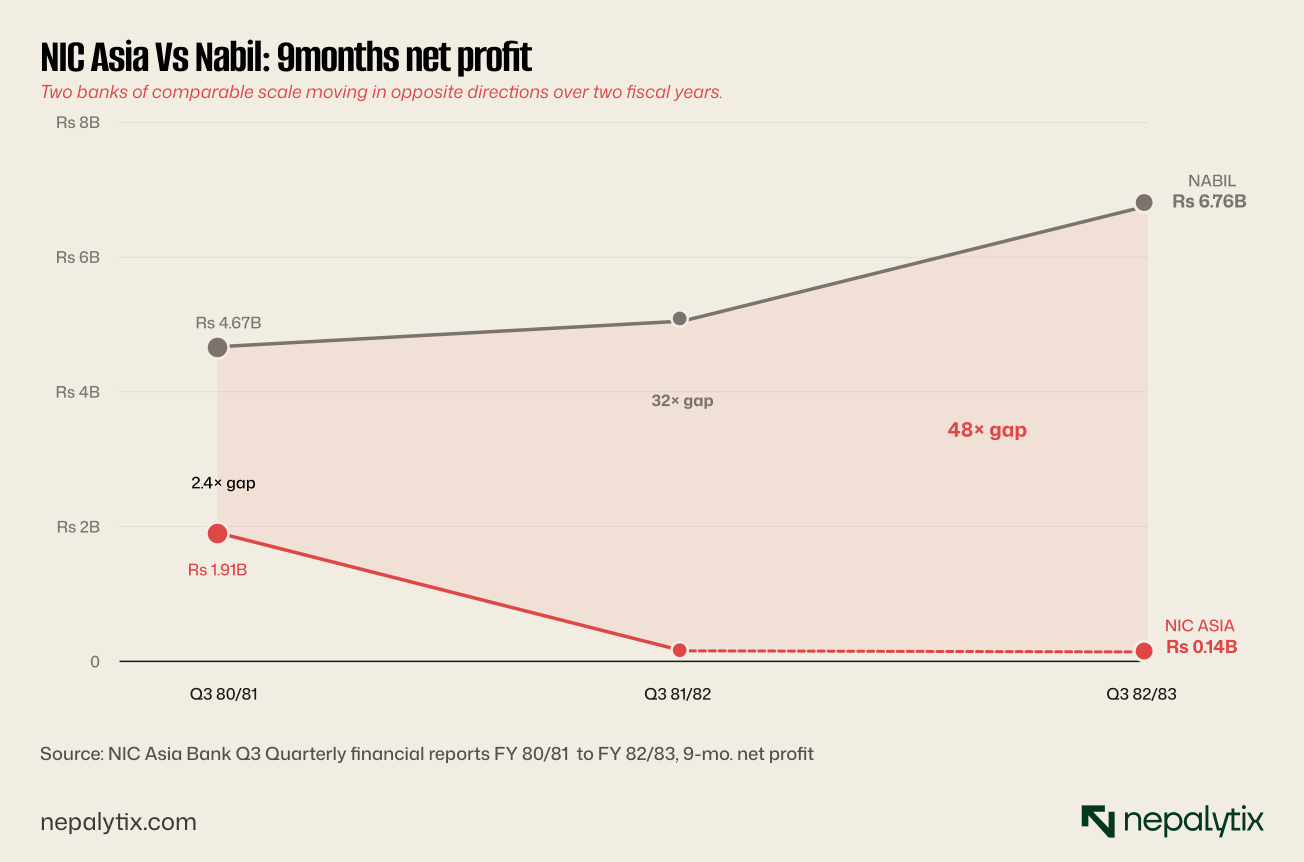

Two fiscal years ago NIC Asia's nine-month net profit was approximately Rs 1.91 billion. Nabil's was Rs 4.67 billion. They were comparable banks operating at comparable scale, and a Rs 4.67 billion to Rs 1.91 billion spread looked like the natural gap between the largest and the second-tier major commercial banks in Nepal. Today Nabil's Q3 82/83 net profit is Rs 6.76 billion, up 33.92% YoY. NIC Asia's is Rs 140 million. The ratio between them has gone from approximately 2.4x to approximately 48x in two fiscal years.

This is not a sector-wide phenomenon. Both banks operated under the same NRB regime over the same window, the same monetary policy, the same NPL classification rules, the same prescribed sector lending mandates, the same liquidity conditions. The factors that drove Nabil's profit to grow 45% over two years and NIC Asia's to fall 93% are internal to each bank: loan book composition, risk management, deposit cost. Macro tailwinds and headwinds were shared. The outcomes were not.

Nabil's Q3 82/83 print also showed impairment charges down 79.12%, the bank is releasing provisions, not adding to them. NIC Asia's Q3 numbers show the opposite trajectory: provisions still flowing through, distributable profit deepening from negative Rs 1.72 billion at Q3 80/81 to negative Rs 13.65 billion at Q3 82/83. The gap is not closing.

How the interest income evaporated

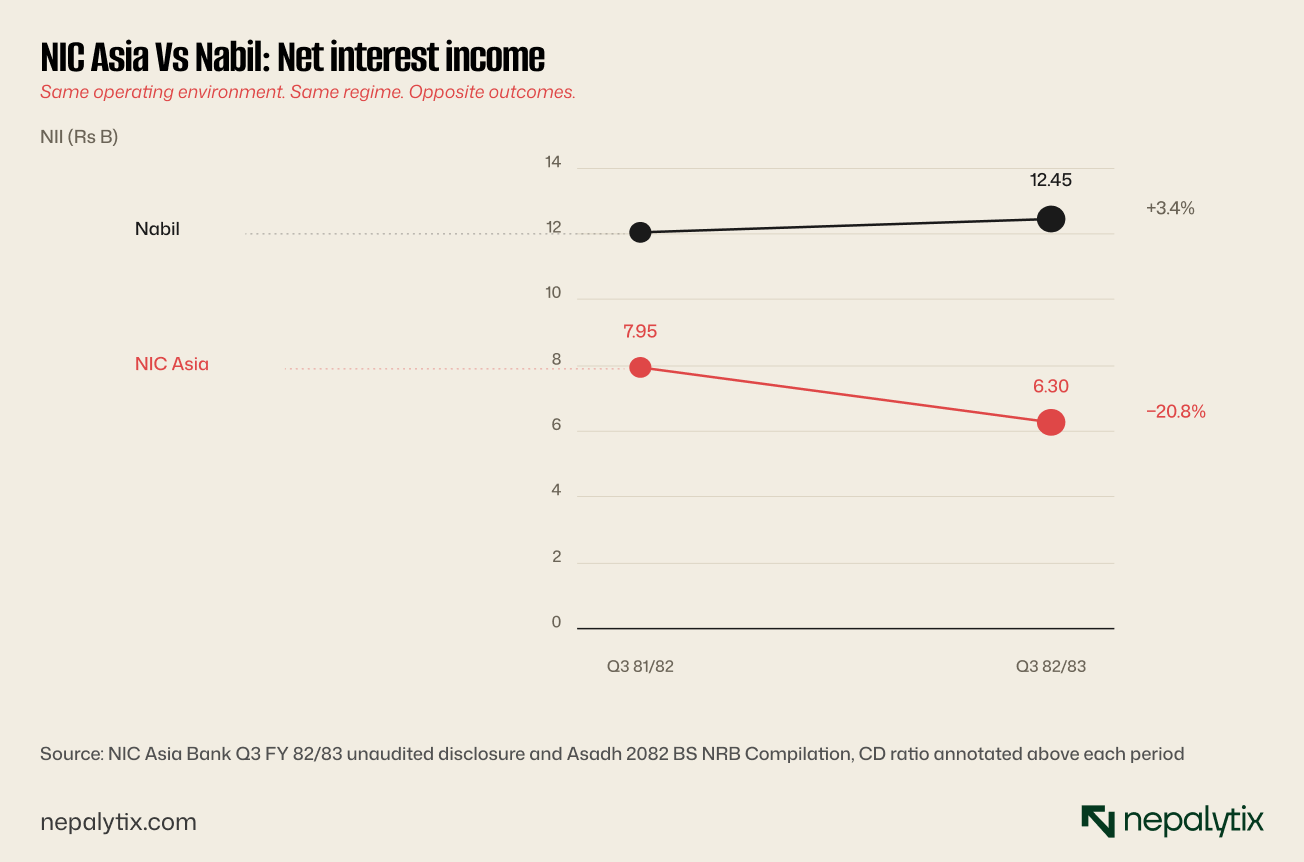

Net interest income is the line that decides a commercial bank's earnings power. NIC Asia's Q3 82/83 NII was Rs 6.30 billion, down 20.78% from approximately Rs 7.95 billion the prior fiscal year. Nabil's NII was Rs 12.45 billion, up 3.36% from Rs 12.05 billion. Two banks. Same operating environment. NICA's NII fell by roughly Rs 1.65 billion in a year. Nabil's added roughly Rs 0.40 billion. The mechanical drivers of NII are three: the size of the interest-earning loan book, the yield on that book, and the cost of the funding base.

On all three, NIC Asia is moving in the wrong direction at the same time. The loan book is shrinking. The yield on the book is constrained because new loans are being booked cautiously and old loans are being written down. The cost of funds is rising because the deposit base is rate-elastic and other banks are cutting deposit rates faster. Three compressions, one quarter, and the Rs 1.65 billion gap is what falls out of the bottom of the income statement.

The asset quality story

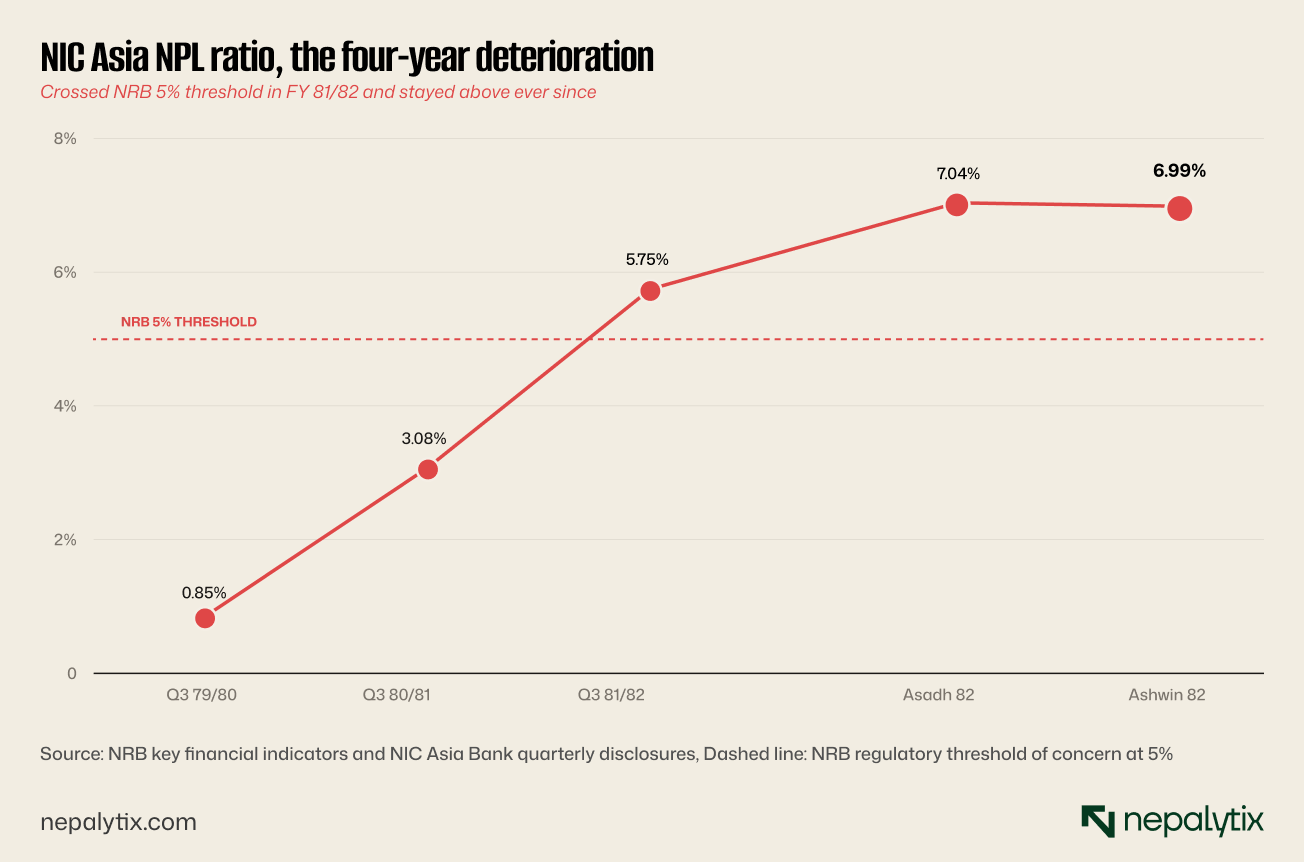

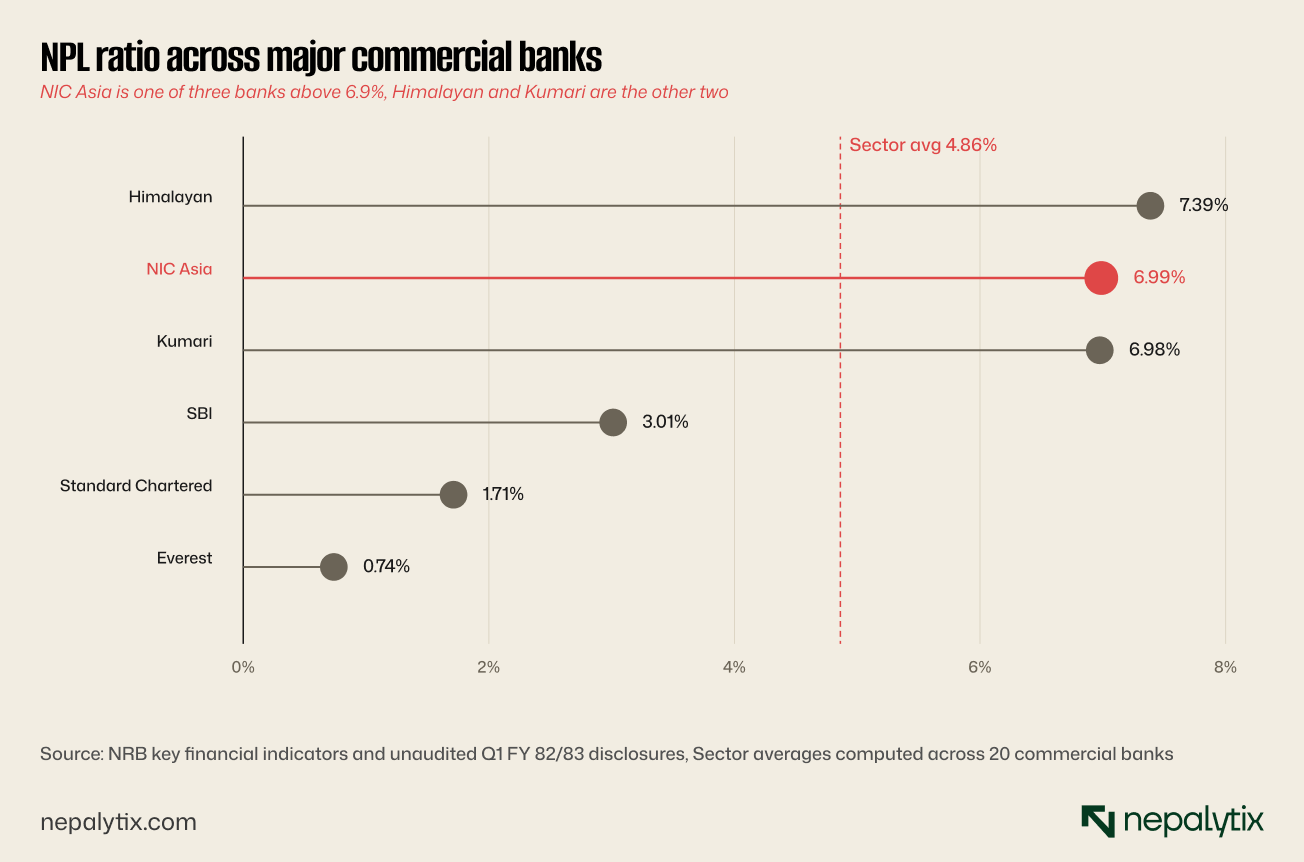

NIC Asia's NPL trajectory tells a four-year story. At Q3 FY 2079/80 the ratio was 0.85% among the cleanest loan books in the commercial bank universe. The bank was widely cited as a model for retail and SME lending growth. By Q3 80/81 NPL had climbed to 3.08%. By Q3 81/82 it sat at 5.75%, having crossed NRB's 5% concern threshold. By Asadh 82, the close of the previous fiscal year, the print was 7.04%, the highest among all commercial banks. At Ashwin 82, the most recent disclosure, the ratio is 6.99%. For two consecutive fiscal years NIC Asia has reported NPL above the regulatory threshold of concern.

The shape of the trajectory matters. The 2.23% point jump from FY 79/80 to FY 80/81 was the inflection. The 2.67% point jump from FY 80/81 to FY 81/82 was a catastrophic year. The 1.29% point jump from FY 81/82 to Asadh 82 was the last leg of acute deterioration. The 0.05% point decline from Asadh 82 to Ashwin 82, a small reversal at a high level is the only sign of stabilisation in the data, and it is barely a sign at all.

Sector context places NIC Asia among three banks with NPL above 6.9% at Ashwin 82: Himalayan at 7.39%, NIC Asia at 6.99%, and Kumari at 6.98%. Three banks sit below 3.1%: SBI at 3.01%, Standard Chartered at 1.71%, and Everest at 0.74%. The sector is split into two regimes; banks that grew aggressively into mid-tier corporate, retail, MSME, and hire-purchase exposures in 2079–2080 and are now provisioning for that growth, and banks that stayed disciplined and are reaping the benefit of cleaner books.

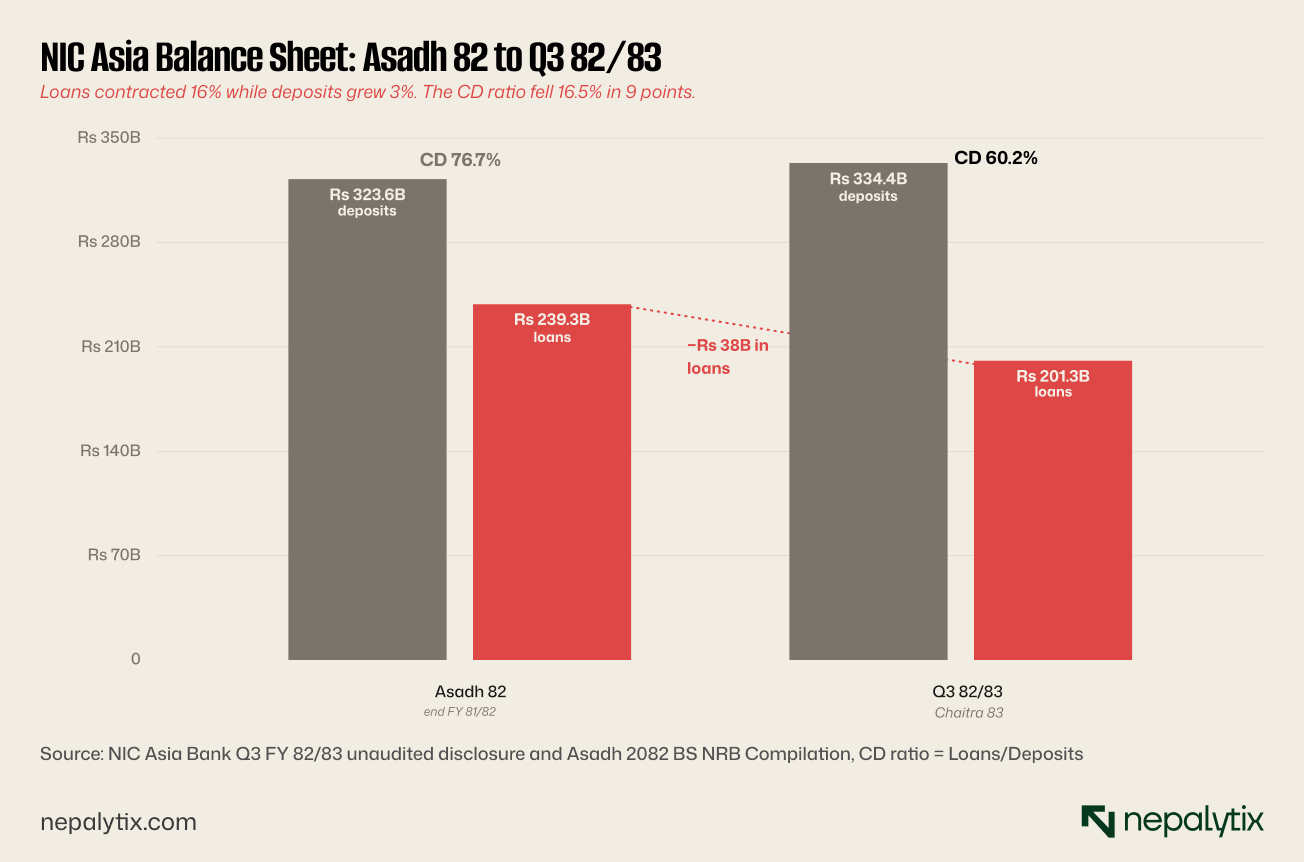

The balance sheet contraction nobody is discussing

The most important number in the Q3 82/83 disclosure is not the EPS or the NPL. It is a loan book. At Asadh 82, NIC Asia's loans and advances stood at Rs 239.33 billion. At Q3 82/83 (Chaitra 83), the same line is Rs 201.34 billion. The book contracted by Rs 38 billion, or roughly 16%, in nine months. Deposits over the same window grew from Rs 323.56 billion to Rs 334.37 billion up Rs 10.8 billion, or 3.3%. The credit-to-deposit ratio collapsed from 76.72% to 60.2%, a 16.5% point drop in three quarters.

Sector context: NRB's regulatory cap on CD ratio is 90%. Most A-class banks operate in the 80–85% band. A 60% CD ratio is unusually low for a Nepali commercial bank, especially one of NIC Asia's size. It signals one of three things, all of which are happening here. First, the bank is writing off and recovering NPL exposures, which mechanically reduces gross loans. Second, new loan origination has slowed sharply under the new management's risk discipline. Third, NRB-driven supervisory pressure has constrained new lending while the bank cleans up.

The cost of this is direct. Every billion of deposits sitting at NRB or in low-yield government securities instead of being deployed as loans is interest income foregone. Roughly Rs 38 billion of deposits raised but not lent represents, at a sector-typical lending margin of 4 percentage points, approximately Rs 1.5 billion of NII per year that simply does not exist on NIC Asia's income statement. That is roughly 95% of the YoY decline in Q3 82/83 NII. The earnings collapse is, mechanically, the balance sheet shrinkage.

The cost of funds inversion

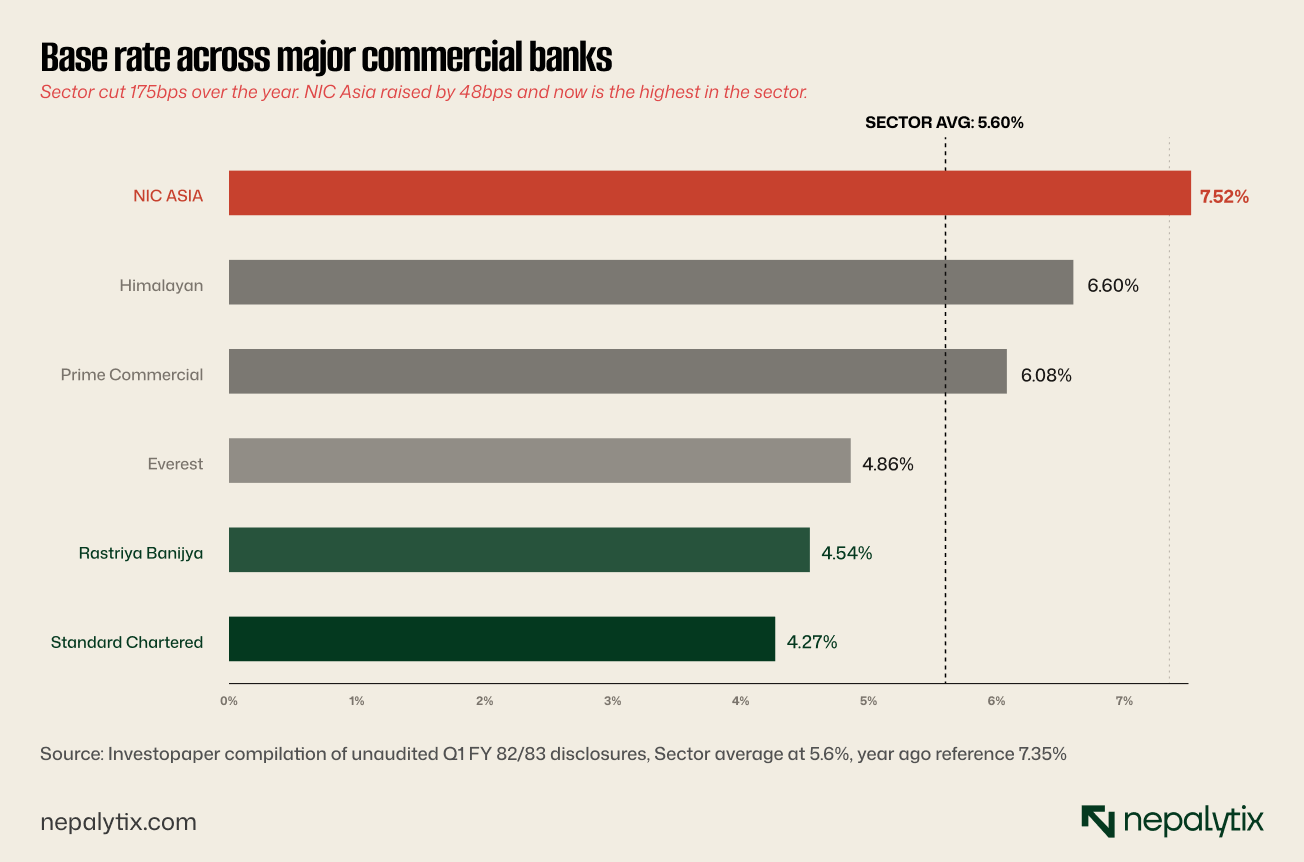

A bank's base rate is the floor below which it cannot profitably lend. It is built up from the cost of deposits, the cost of capital, statutory reserves, and operating costs. In a normal cycle, all banks' base rates move in the same direction at roughly the same pace, with differentials reflecting underlying funding mix. From a year ago to now, the sector average base rate has fallen from 7.35% (Ashwin 81) to 5.60% (Ashwin 82), a cut of 175 basis points as NRB's policy easing and excess sector liquidity flow through to deposit pricing.

NIC Asia did the opposite. At Asadh 82 the bank's base rate was 7.04%. At Ashwin 82, the same quarter when sector average dropped to 5.60% NIC Asia's base rate moved up to 7.52%. A 48 basis point increase against a sector cutting 30+ bps in the same quarter. NIC Asia is now the highest base rate in the sector by a clear margin: 7.52% versus 4.27% at Standard Chartered, 4.54% at Rastriya Banijya Bank, and 4.86% at Everest. The gap to the sector-leading low-cost banks is approximately 325 basis points.

A bank holds deposits with one of two things: rate or relationship. Standard Chartered, Nabil, Everest, and the state banks hold deposits primarily through relationships: corporate accounts, NRI deposits, government and PSU mandates, salary accounts, transactional banking. The cost of those deposits is structurally low because the depositor is not optimising for yield. NIC Asia's 7.52% base rate signals the opposite, a rate-held deposit base. When the sector cuts deposit rates by 175 bps and one bank has to raise by 48 bps to retain its deposits, the most likely explanation is that the deposit base is leaving and the bank is paying up to slow the outflow.

The capital cushion is thinner than it looks

NIC Asia's capital adequacy ratio at Asadh 82 was 13.42%. NRB's minimum CAR for commercial banks is 11.0% — 8.5% Tier 1 plus a 2.5% capital conservation buffer. The gap between NIC Asia's reported CAR and the regulatory floor is approximately 2.4 percentage points. For a bank operating with NPL above 6.9% and accumulated negative distributable profit of Rs 13.65 billion, that cushion is thinner than the headline number suggests.

The arithmetic: every additional rupee that has to be classified from performing to non-performing increases provisioning, which reduces retained earnings, which reduces Tier 1 capital. If even 1.5 percentage points of additional NPL classification rolls through over the next two quarters entirely plausible given the pattern of restructured-loan reclassification across the sector, the CAR cushion narrows further. The bank is not at imminent breach risk, but the headroom for absorbing additional asset quality surprises is finite.

By comparison, Standard Chartered Nepal reported CAR of 17.50% at Q1 81/82, a cushion of 6.5 percentage points above the floor. The structural difference is what allows Standard Chartered to keep base rates at sector lows and still absorb cyclical NPL fluctuation without capital pressure. NIC Asia does not have that buffer.

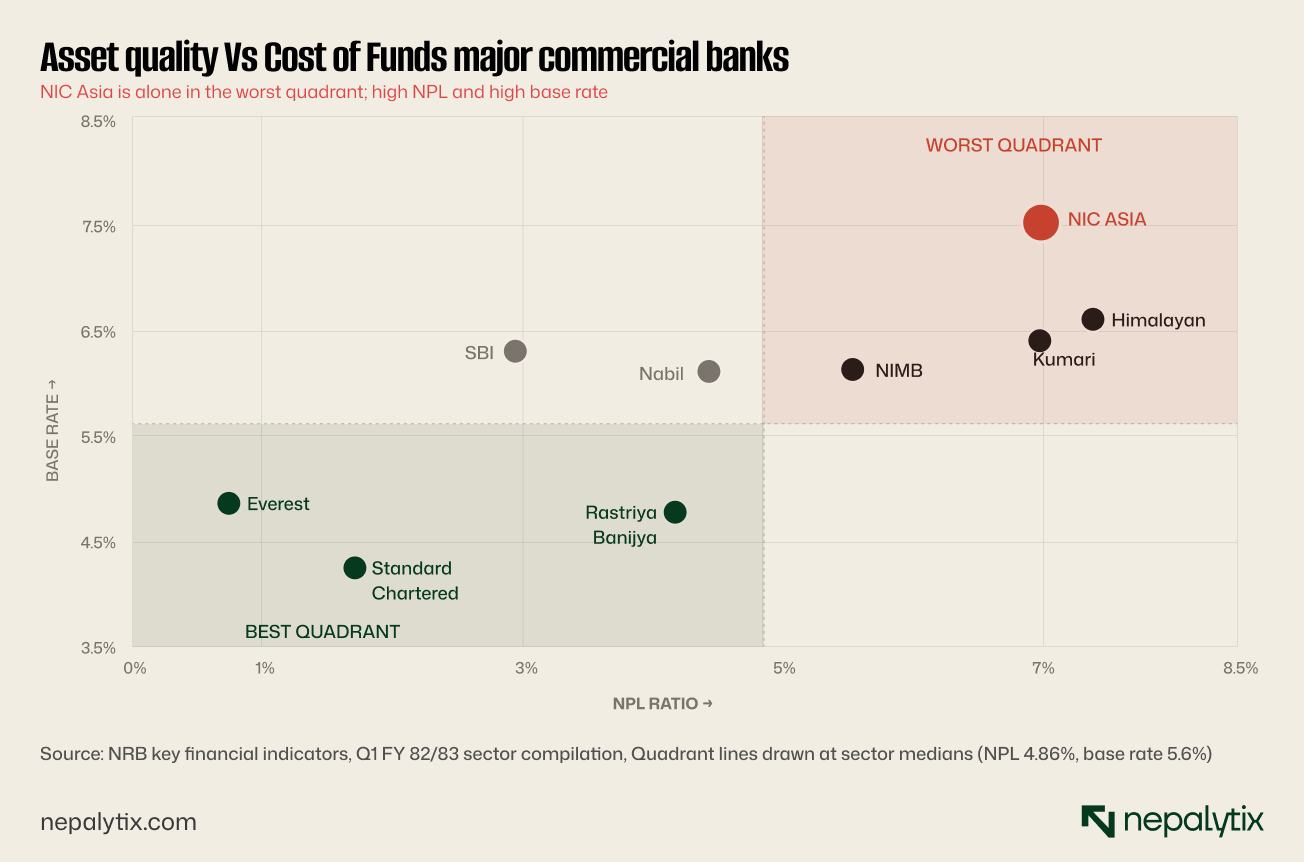

Where NIC Asia sits on the sector map

Plot any major Nepali commercial bank on a two-axis chart with NPL ratio on one axis and base rate on the other and the sector splits into recognisable quadrants. Low NPL plus low base rate is where Standard Chartered, Everest, and Nabil sit relationship deposit bases, disciplined lending, repeatable profitability. High NPL plus high base rate is the worst quadrant: rate-held deposits funding aggressive lending that is now provisioning. NIC Asia is the only bank in this quadrant at the extreme. Himalayan and Kumari sit nearby on NPL but with more moderate base rates. The position implies that the recovery path requires improvement on both axes simultaneously, and the improvements are linked, cleaning up NPL is what allows base rate to fall, which is what allows NII to recover.

The deposit concentration question the market is not pricing

NIC Asia's deposit base is Rs 334.37 billion. The structural risk this NFI flags as the primary market mispricing is the rate elasticity of that base. A bank holding deposits at a 7.52% base rate while sector peers offering 4.27% to 5.60% is paying approximately 200 to 325 basis points more for funding than the comparison set. Depositors are receiving what looks like a yield premium and that yield premium is the only thing keeping a meaningful portion of those deposits from rotating.

Two scenarios force the question. First, NIC Asia attempts to repair its NIM by cutting deposit rates to converge with the sector. Deposits move out, the funding base shrinks, and balance sheet contraction accelerates. Second, NIC Asia keeps deposit rates elevated to retain its book. NIM stays compressed and earnings recovery is delayed by the cost of holding the deposits. Either path is constrained by the deposit base's rate elasticity, which the market does not appear to be pricing into the equity at Rs 353.

A tertiary scenario sits underneath both: depositor concern about asset quality. Nepal's deposit insurance covers Rs 5 lakh per account. For a retail depositor with smaller balances this is sufficient protection. For corporate or high-net-worth depositors with balances multiplied above the insurance cap, the asset quality story matters and the rate premium does not fully compensate. If even 5–10% of the rate-elastic portion of the deposit base rotates over the next two quarters, the bank is forced into the first scenario whether it intends to be or not. The numbers are not in the public Q3 disclosure to size this risk precisely. The deposit composition by tenor and depositor type sourced from the audited annual report when it is released is the data that decides whether this risk is sized at 5% of deposits or 25%.

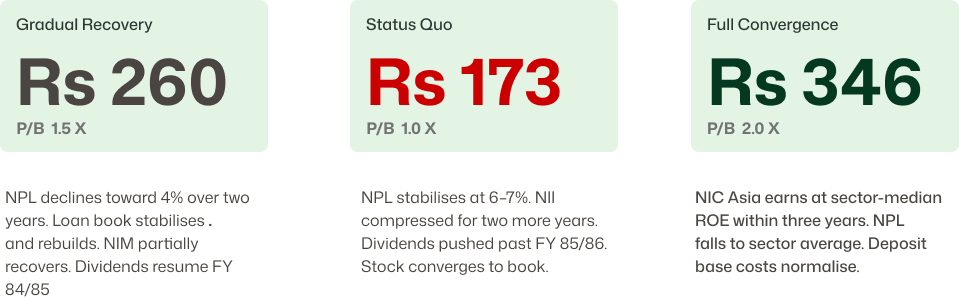

Fair value: three scenarios, three different outcomes

Method: book value of Rs 172.97 anchors the floor. The premium to book reflects the market's expectation that the bank's earnings power returns toward sector norms. The Q3 print is the test of that expectation, and the test is being failed in the current quarter. Three scenarios bracket the range.

The market price at Rs 353 sits within the third scenario's implied range. The Q3 data sits closer to the second. The gap between the two, approximately Rs 90 per share is what the next four quarters of disclosures have to close. The variables that decide which scenario is realised are observable and quarterly: the NPL print, the NII trajectory, the loan book direction, and the base rate movement. Each Q4 82/83 and Q1 83/84 disclosure will either narrow the range or widen it.

What to watch in Q4 82/83 and beyond

Five quarterly data points carry disproportionate signal weight for NIC Asia over the next two disclosures. First, NPL whether the Ashwin 82 reading of 6.99% holds, climbs, or starts a meaningful descent. A move below 6% would be the first concrete sign of asset quality reversal. Second, the loan book whether the contraction reverses or continues. Stabilisation around Rs 200 billion suggests a planned bottom; further decline suggests the cleanup is still active. Third, the base rate whether NIC Asia begins converging toward sector levels in Q4 82/83 or maintains the 7.5%-plus level. Fourth, the impairment charge: the line that decides whether profits resume flowing or continue being absorbed by provisions. Fifth, the distributable profit whether the negative bucket starts narrowing or continues widening.

A bank in balance sheet repair tends to show those five lines move together. They have not yet. Until they do, the equity market is pricing a recovery, the income statement is not yet delivering, and the risk skew is to the downside. The deposit concentration question is the variable that determines whether the second scenario remains achievable or whether the gravitational pull of the first scenario takes over.