NRB’s Expansionary Policy That Isn’t Expanding

Nepal Rastra Bank labeled FY 2025/26 monetary policy “discretionary and expansionary,” targeting 12% private credit growth with inflation capped at 5%.

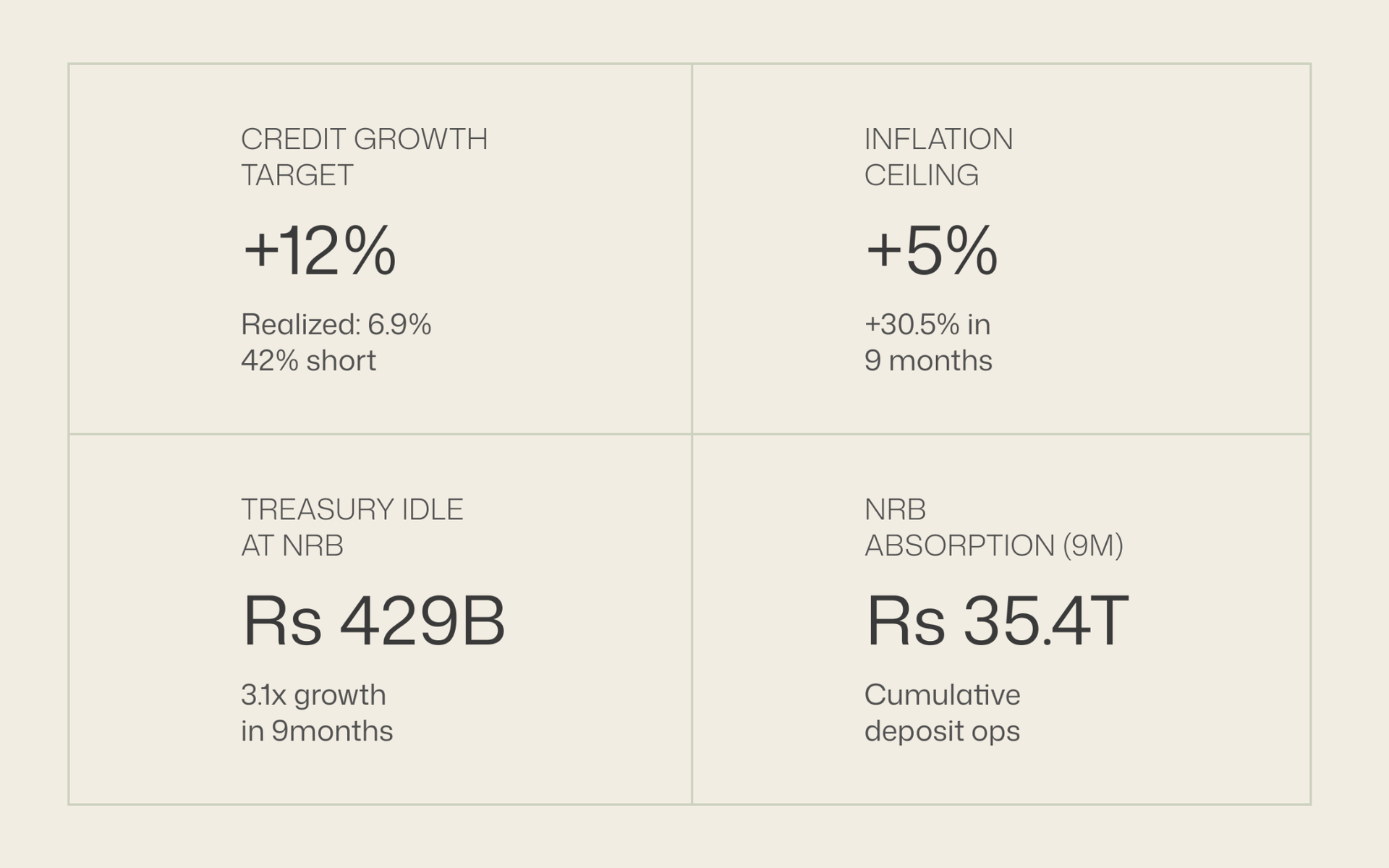

NRB declared FY 25/26 monetary policy "discretionary and expansionary" in July 2025. The Governor projected 12 percent private credit growth and a 5 percent inflation ceiling. Nine months later, credit growth has run at 6.9 percent, the Treasury has accumulated Rs 291 billion in idle cash at the central bank, NRB has run cumulative deposit-collection operations averaging Rs 130 billion per day (Rs 35.4 trillion across nine months, with daily rollover)and inflation has stayed below the policy ceiling for the entire period. The stated stance and the operational reality are running in opposite directions.

On July 11, 2025, Nepal Rastra Bank's newly appointed Governor Dr. Biswo Nath Poudel unveiled the 59th monetary policy, covering FY 2082/83 (2025/26) the first full policy cycle of his tenure. The official stance language: "discretionary and expansionary." The Governor explained the reasoning in plain terms during the announcement: "Given the low inflation and comfortable foreign exchange reserves, NRB has formulated a cautiously flexible monetary policy." \

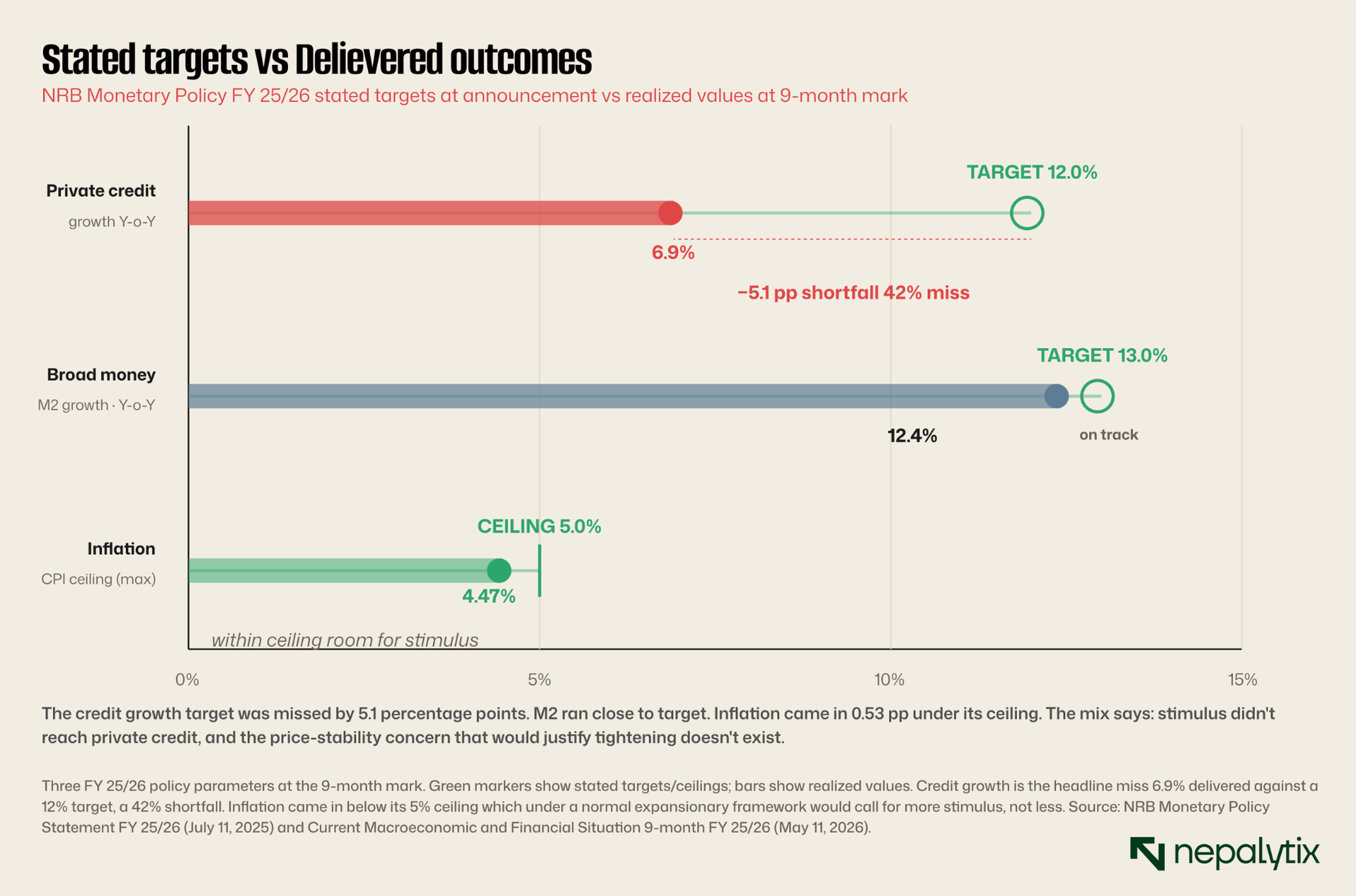

The targets matched the language. Private sector credit was projected to grow 12 percent. Broad money supply (M2) was projected to grow 13 percent. Inflation was set at a 5 percent ceiling. Policy rates were cut to support the stimulus: the repo rate was lowered to 4.25 percent, the bank rate to 5.75 percent, the deposit collection rate (overnight) to 2.75 percent. The cash reserve ratio was reduced. Working capital loan guidelines were relaxed for agriculture and communications.

The narrative was internally consistent. Banks were sitting on over Rs 700 billion of loanable funds. Credit demand had been weak. Imports had pulled rupee liquidity through trade. The central bank's job, as articulated, was to push that idle liquidity into productive lending to lower the cost of capital, encourage banks to lend and re-energize the credit channel.

Nine months in, the gap between stance and delivery is striking. The chart below shows what was promised against what was delivered for the policy's two most measurable targets.

Two contractionary forces running simultaneously

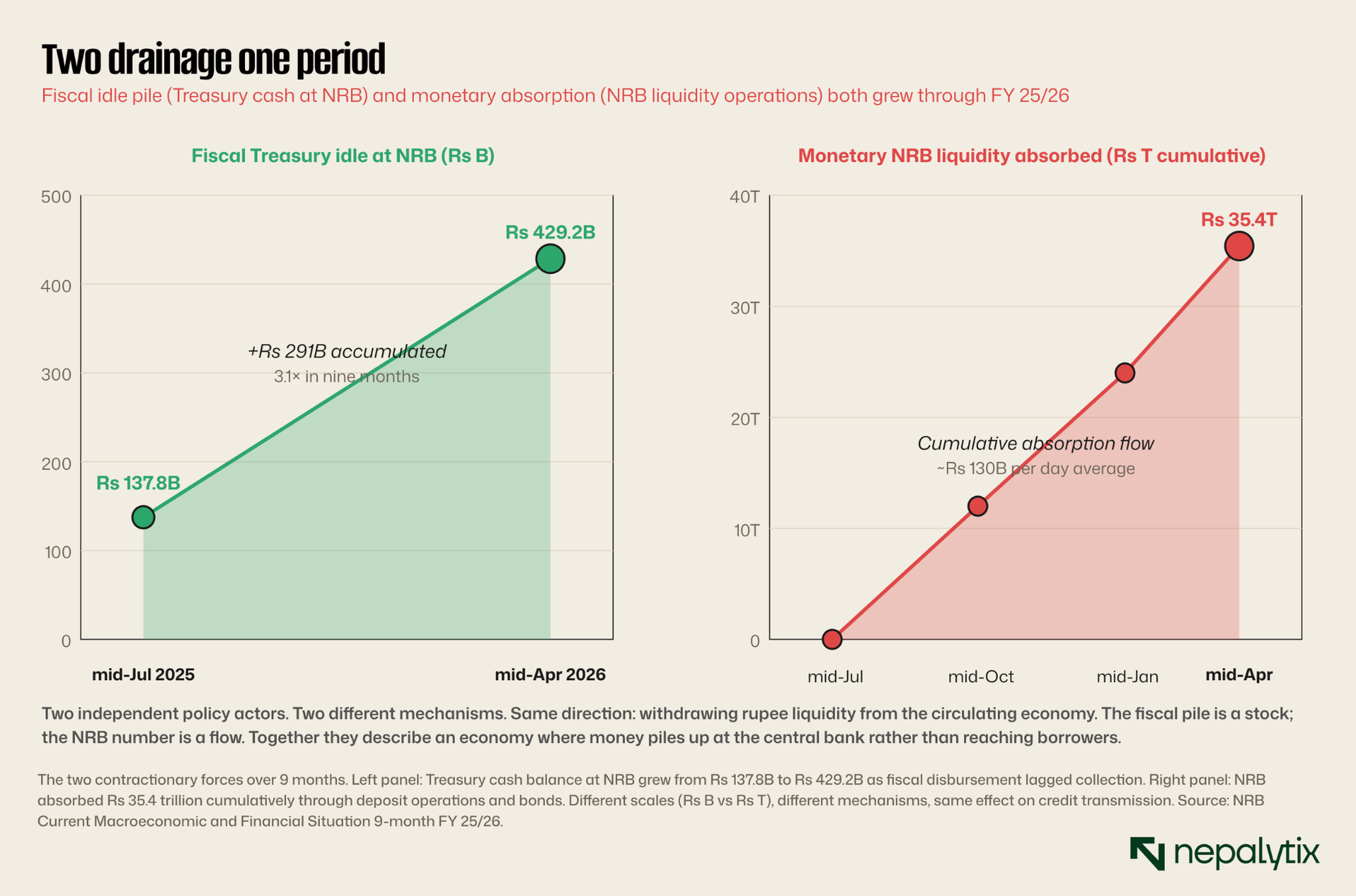

If the stance is expansionary and the inflation ceiling is intact, why isn't credit growth reaching its target? The answer is in the operational data the policy statement doesn't emphasize: the Treasury and the central bank are simultaneously withdrawing liquidity from circulation, by separate mechanisms, at remarkable scale.

The fiscal side: government cash balance at NRB stood at Rs 137.78 billion in mid-July 2025. By mid-April 2026 it had grown to Rs 429.17 billion. The increase of Rs 291.39 billion represents fiscal resources collected through taxation and other revenue, allocated in the budget but never deployed. The money sits in the Treasury's account at the central bank neither spent into the economy nor returned to credit circulation through bank deposits. It is, by definition, contractionary.

The monetary side: through deposit collection auctions, Standing Deposit Facility utilization and NRB bond issuance, the central bank absorbed Rs 35,409.25 billion of cumulative liquidity flow over the nine months. This is the operational signature of an active mopping policy. The Standing Deposit Facility rate at 2.75 percent sets the floor that banks earn for parking idle liquidity at NRB rather than lending it to the economy.

The credit transmission failure is the symptom. Banks received Rs 615.67 billion of new deposits over the nine months. They lent out Rs 311.95 billion. The Rs 304 billion gap had to go somewhere. A substantial share went to NRB through the Standing Deposit Facility and deposit collection auctions, earning 2.75 percent risk-free rather than being lent to the productive economy at 6.77 percent into a 5.60 percent non-performing loan environment.

This is the textbook signature of a liquidity trap reinforced by central bank action. The reduced cost of money isn't translating into credit deployment, because the central bank is simultaneously offering banks a safe alternative and the fiscal authority is removing potential demand by not spending its budget.

Inflation tracked below targets the entire period

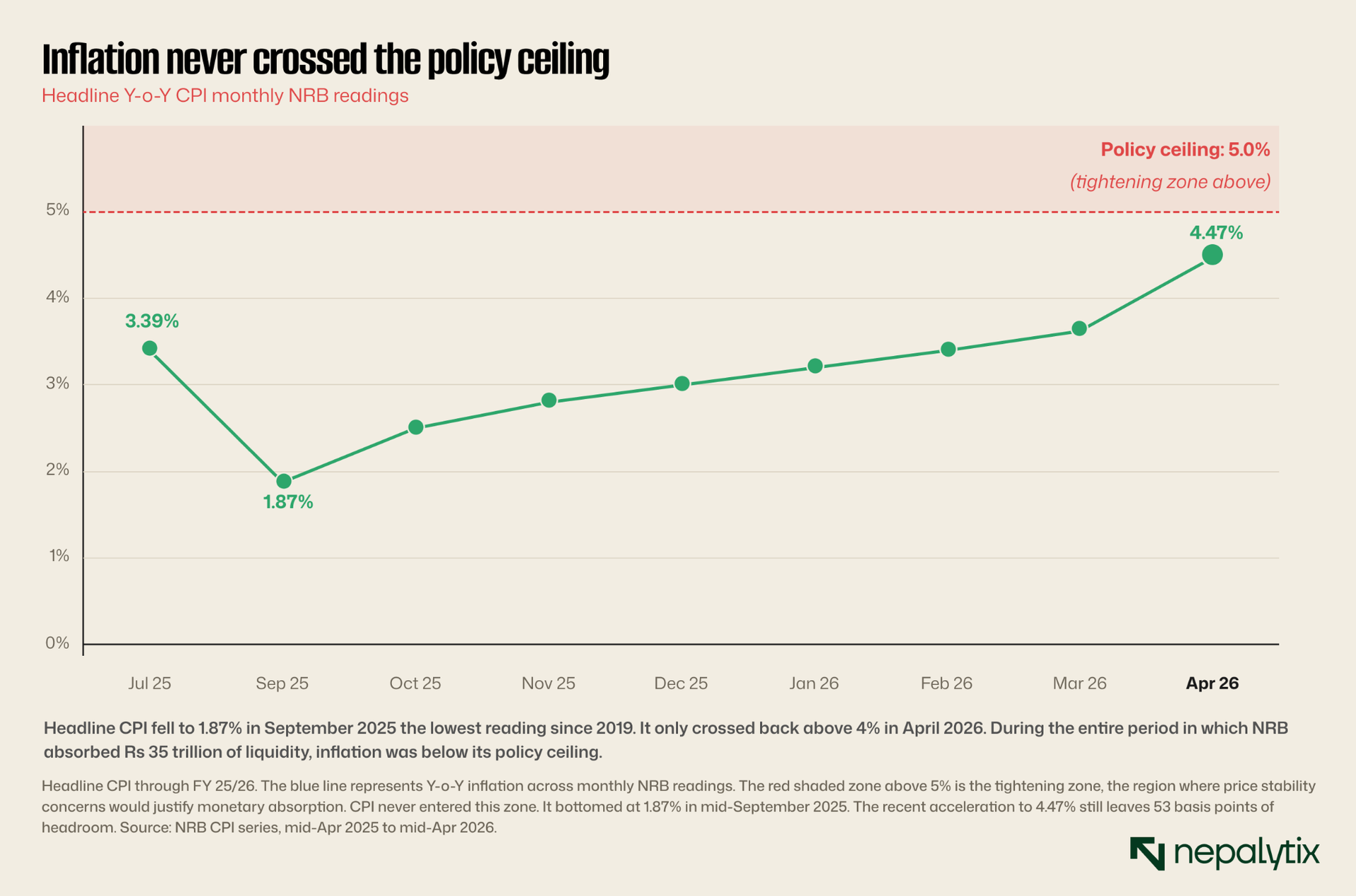

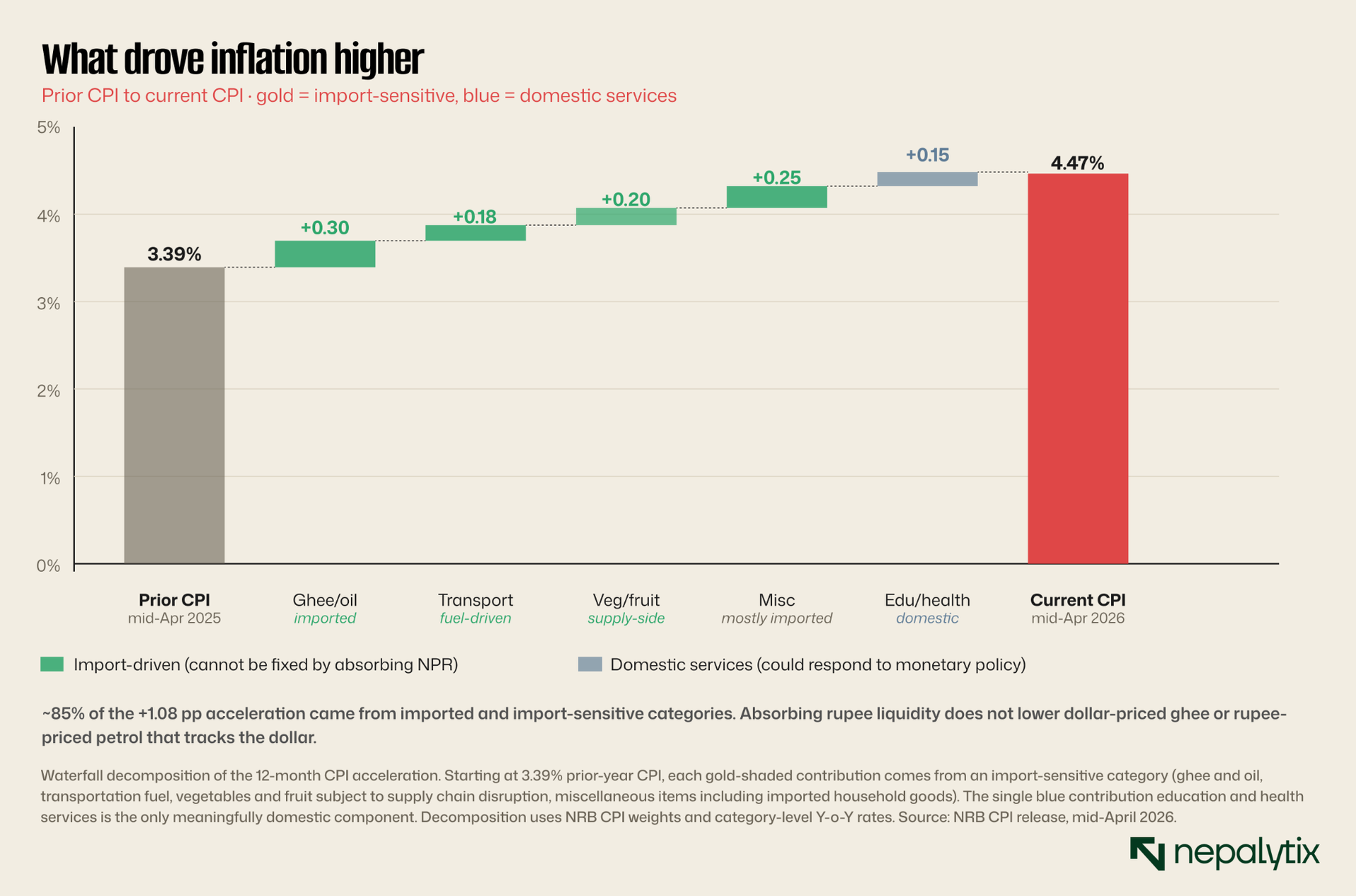

The justification for monetary tightening in any framework is to suppress an emerging or actual price-level overshoot. The data shows neither. Headline CPI accelerated from 3.39 percent in mid-April 2025 to 4.47 percent in mid-April 2026 an increase, yes but still 53 basis points below the policy ceiling. Through every interim quarter, inflation remained inside the policy band.

The combination is what makes the operational stance contractionary in effect. Credit growth missed target by 42 percent. Treasury cash piled up at the central bank. NRB absorbed liquidity at a trillion-rupee scale. And inflation, the only metric that could justify tightening never tested the ceiling.

What's pushing CPI

Imports, not money supply

The deeper analytical question is: what is actually driving the inflation that did materialize? If the answer were "domestic monetary excess" , too many rupees chasing too few goods produced in Nepal then NRB's absorption would be the correct response. The data says otherwise.

The Y-o-Y CPI moved from 3.39 percent to 4.47 percent, a 1.08 percentage point acceleration. Decomposing this acceleration by category shows the source clearly: imported and import-sensitive items account for the bulk of the upward pressure.

The implications follow immediately. If 85 percent of the inflation acceleration comes from imported categories, the monetary policy tool that addresses imported inflation is exchange rate management and NRB has the right tool for that. NRB sold USD 3.00 billion during the period to purchase Indian rupees equivalent to Rs 431.06 billion, defending the NPR-INR peg at 1.6. That intervention is targeted, appropriate, and operationally distinct from broad domestic liquidity absorption.

Absorbing Rs 35 trillion of domestic liquidity does not lower the price of ghee or petrol or imported household goods. It lowers the price of credit which is already weak. The wrong tool is being used to address inflation pressures the tool cannot actually reach.

What NRB would say in its defense

To the central bank's credit, there are reasonable arguments for the current operational posture, and the analytical work demands fairly representing them.

The strongest defense runs as follows. Remittance inflows hit Rs 1,659 billion over the nine months, the highest in eight years. That liquidity entered the banking system as deposits. Without active absorption, those rupee deposits would either fuel credit growth into already-overextended sectors (real estate, margin lending) or pressure the NPR-INR peg through asset-market channels. Either outcome would create instability. The choice between "absorb the liquidity through monetary operations" and "let it create asset bubbles or peg pressure" is not a free choice.

Further: the rupee did depreciate against the dollar by 7.5 percent during the period. Reserves grew in NPR terms but the exchange rate moved against Nepal. That movement is what's transmitting global commodity prices (Brent crude up 84.5 percent, gold up 46.2 percent) into the domestic CPI. If NRB had not actively defended the peg through USD sales Rs 35 trillion of mopping plus USD 3 billion of FX intervention, the rupee could be 10 percent or 15 percent weaker now, and imported inflation would be 8 percent or 10 percent, not 4.47 percent.

On this reading, the absorption is precisely the right policy: leaning against an external shock that would otherwise drive inflation through the exchange rate channel.

Right tool, wrong target

The defense above is internally coherent. It also misidentifies which tool is doing the work.

The intervention that actually addressed rupee depreciation was the FX operation NRB selling USD 3 billion to purchase INR. That is the tool for managing exchange rate pressure. It was used. It worked: the NPR-INR ratio held at 1.6 throughout the period. The NPR weakness against the USD that did occur was therefore not a function of insufficient FX intervention. It was a function of the dollar strengthening against the Indian rupee, a movement entirely outside NRB's control and shared across the region.

If 85 percent of the inflation acceleration came from imports priced in dollars, and if the rupee weakness driving that pass-through is a function of global dollar strength outside NRB's control, then the tool that would address remaining inflation pressure is more aggressive FX intervention selling more dollars to support the rupee not absorbing more rupee liquidity from domestic banks. The two tools target different problems. Conflating them produces the current outcome: credit growth strangled to address an inflation problem that domestic credit isn't causing.

What this means in practice

The argument here is not that NRB should reverse course and flood the economy with liquidity. Nor is it that the central bank should ignore the external account. The argument is more specific: the two policy actions being run simultaneously contradict each other in their effect on the credit channel, and the resolution is to disentangle them.

Practical implications

Fiscal side: the Rs 291 billion sitting idle at NRB is the most direct source of the contractionary pressure. Capital expenditure ran at minus 6.5 percent year-on-year fiscal disbursement is going backwards while collection runs forward. This is a Finance Ministry execution problem more than a Nepal Rastra Bank policy problem. The two authorities sit inside the same government and the contractionary effect compounds when they don't coordinate. The Treasury is not a savings account.

Monetary side: the absorption mix should shift toward foreign-exchange sterilization (USD sales to defend the rupee) and away from broad domestic liquidity mopping. The first tool addresses the actual inflation problem; the second tool addresses a different problem that isn't currently visible in the data.

Communication side: if the operational stance is going to remain contractionary for the next quarter, the policy statement should say so. "Discretionary and expansionary" is not what the data is delivering. Markets are pricing on the stated stance; the credit channel is responding to the operational stance. The mismatch is the largest source of distortion in the current policy framework.

What to watch

NRB's mid-policy review is typically published in February; the next full monetary policy framework for FY 2026/27 will be announced in July 2026. The Q4 FY 25/26 macroeconomic situation report (covering the full fiscal year, expected August 2026) is the data point that will lock in whether private credit growth closed below 8 percent for the full year. If it does, the gap between the stated stance and the operational delivery will be on the record at policy-cycle granularity not just at the 9-month read.

The credit transmission problem is not going to resolve through more rate cuts. It is going to resolve when the fiscal authority spends what it has collected, and when monetary policy absorption is narrowed from broad to targeted. Until one or both of those things happens, the chart on stated targets versus delivered outcomes is going to keep getting redrawn each quarter with the same widening gap.