NTC : A Cash Pile Wearing a telecom

Nepal Telecom's reported profit plunged 57% in FY 2081/82, but the operating business remained largely intact.

Nepal Telecom is still the country’s biggest network and its most misunderstood blue chip. Last year’s headline, a 57 percent drop in net profit was not the operating story it looked like. The operating story is quieter, slower and harder to fix.

There is a version of Nepal Telecom that exists only in headlines. In that version, the company that has carried the country’s phone calls for three generations suddenly forgot how to make money and a 57 percent collapse in net profit is the proof. It is a tidy story. It is also wrong in the way that matters most for anyone deciding what the shares are worth.

The truer picture is duller and more important. Nepal Telecom’s operations did not fall apart last year. Earnings before interest, tax, depreciation and amortisation actually rose. Pre-tax profit barely moved. What broke sat below the operating line, in two places the market tends not to look: the interest the company earns on a very large pile of cash and a set of one-off accounting provisions that landed in a single year. Strip those out and you are left with a business that is doing roughly what it did the year before which is to say slowly, structurally and not always in the direction its owners would like.

This note initiates coverage on Nepal Telecom. It is a long company with a short float, a monopoly heritage and a competitive present, and a balance sheet that behaves more like a bond fund than a network operator. Over the next several thousand words we will take it apart in the order the numbers demand: first the profit that was not lost, then the profit that was, then the businesses underneath, and finally the price the market is asking you to pay for all of it. The thesis, stated plainly up front, is that this is a monopoly in slow decline, priced as though the decline is optional.

A 57 percent fall in net profit sitting on top of flat pre-tax earnings

Start with the income statement, because almost everything that has been written about Nepal Telecom this year starts and stops at the wrong line of it. For the year to mid-July 2025, the company reported net profit of Rs 2.66 billion, down 57.2 percent from Rs 6.24 billion the year before. That is the number that travelled. It is real and it is bad and it is also the single most misleading figure the company disclosed all year.

Here is why. EBITDA for the same period was Rs 19.26 billion, up 6.8 percent. Pre-tax profit was Rs 11.22 billion down a rounding error, 0.3 percent, from Rs 11.25 billion. So we have a company whose operating cash generation grew, whose pre-tax profit held flat, and whose net profit more than halved. All three statements are true at once. The gap between them is the whole story.

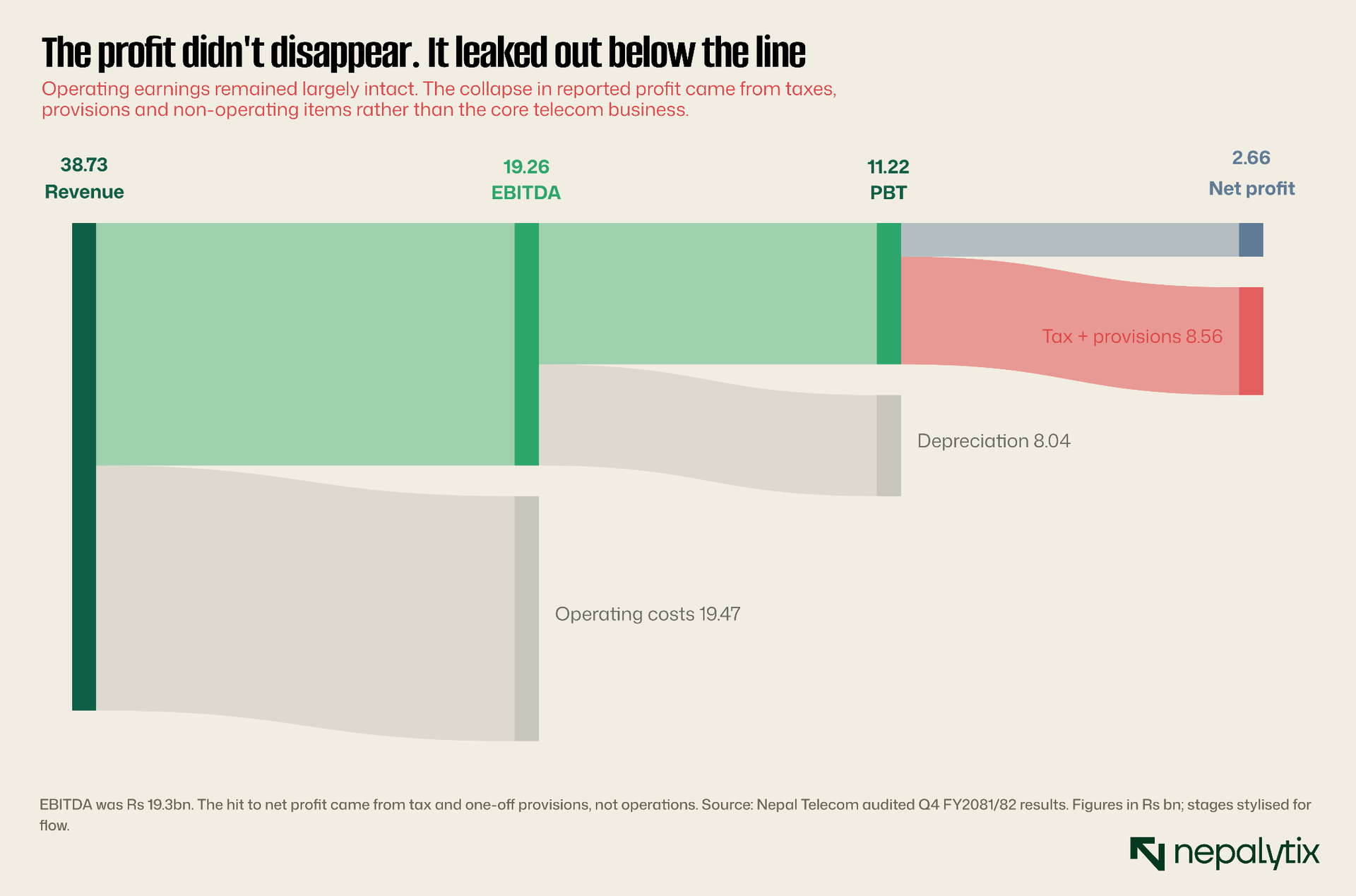

The chart above traces a single rupee of revenue down through the statement. Revenue of Rs 38.73 billion covers operating costs of roughly Rs 19.5 billion and still throws off Rs 19.26 billion of EBITDA, a margin near 50 percent that most operators in the region would envy. Depreciation takes another Rs 8 billion which is the unavoidable price of running a national network. Down to pre-tax profit, nothing is broken. The damage is concentrated entirely in the last green-to-red transition: a tax and provisions charge of roughly Rs 8.56 billion against pre-tax profit of Rs 11.22 billion. That is an effective charge of about 76 percent against something closer to 45 percent the year before. Almost the entire profit collapse lives in that one widening.

It is worth being precise about what this means, because it is the foundation of everything that follows. The operating business of Nepal Telecom did not have a bad year. The reported profit had a bad year, for reasons that have very little to do with how many calls were made or how much data was sold. If you are an equity investor, the distinction is not academic. A company that loses operating profit is a company in trouble. A company that loses reported profit to a one-off provision and a rate cycle is a company having a bad print. Those are different securities, and they are worth different prices.

The second chart isolates the divergence. The upper line, pre-tax profit runs almost dead flat from one year to the next. The lower line, net profit, falls off a cliff. The shaded gap between them is what the tax line and the provisions did to shareholders in a single twelve-month window. The market, reasonably enough, looked at the bottom line, saw a 57 percent drop, and re-rated the stock as though the franchise had cracked. We think it looked at the wrong line.

The one-line version of Nepal Telecom did not stop making money last year. It stopped reporting money because the line below operating profit broke and the line above it did not.

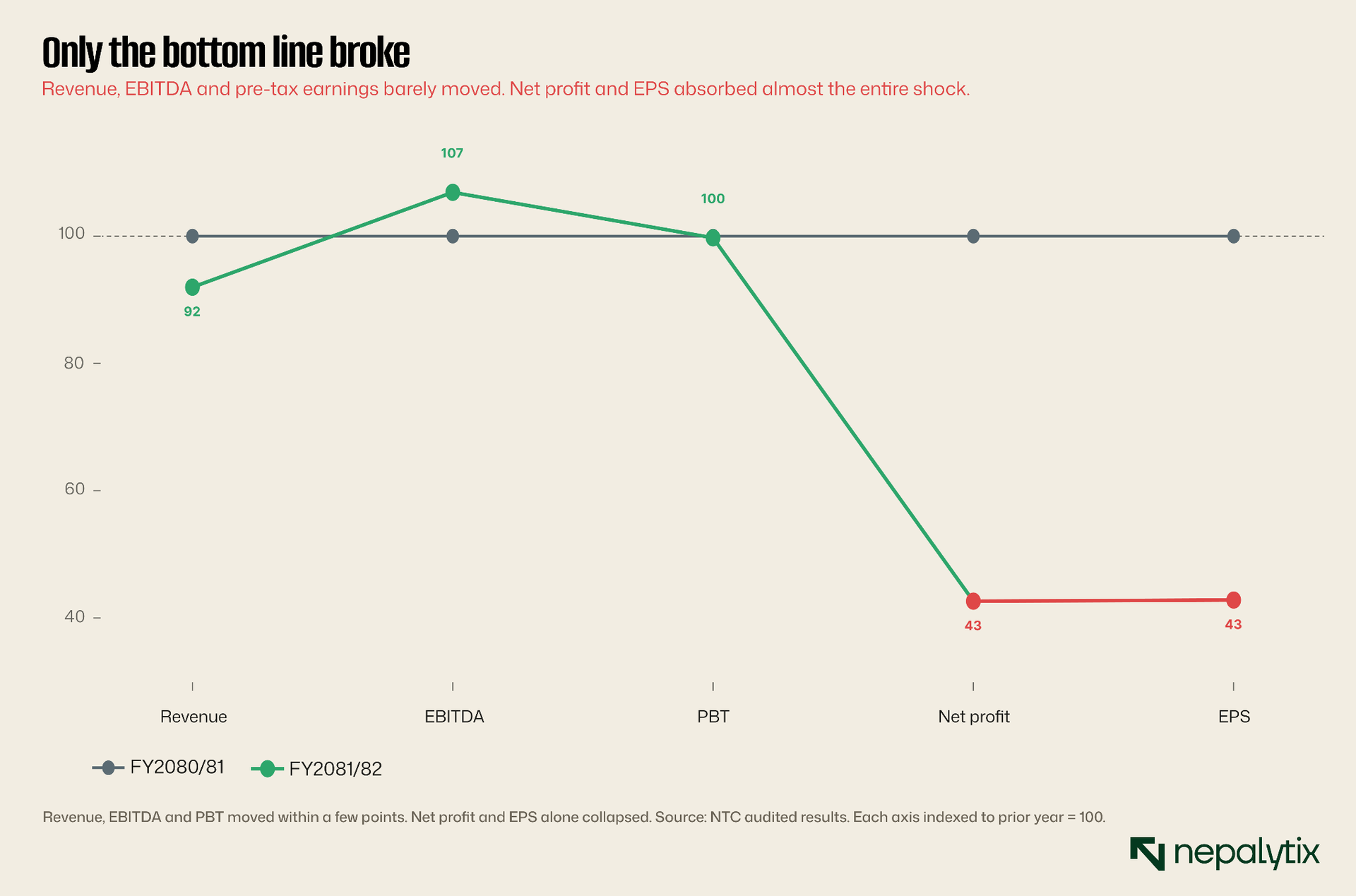

Five core metrics, indexed to the prior year

Four of them barely move.

If the income statement is too granular, index everything to a common base and watch which lines actually travel. Setting the prior year, FY2080/81, at 100 here is how the five headline figures moved.

Revenue lands a little below the base near 92 reflecting an 8 percent decline in the topline as legacy voice and international traffic continue to thin out. EBITDA sits above the base near 107. Pre-tax profit lands almost exactly on 100. And then net profit and earnings per share fall to roughly 43, a near-vertical drop that has no counterpart anywhere else on the page. Four of the five metrics move within a band you could cover with a thumb. The fifth falls through the floor.

This is the visual signature of an accounting and below-the-line event, not an operational one. When a business is genuinely deteriorating, the damage shows up at the top and compounds downward: revenue softens, margins compress, EBITDA slips, and the bottom line follows the lot of them down. That is not what happened here. Here the top of the statement is intact and only the very bottom is severed. Whatever went wrong, it went wrong in the last few feet of the waterfall.

We labour this point because it is the fulcrum of the entire investment case. Everything bullish you can say about Nepal Telecom rests on the claim that FY81/82 was a distorted year that flatters the downside and that normalised earnings are materially higher than the audited Rs 2.66 billion suggests. Everything bearish rests on the claim that the distortions mask a slower erosion that is real and ongoing. Both claims are true. The art is in weighing them, and you cannot begin to weigh them until you accept that the headline number is not the operating number.

Two things happened below the operating line. One was the rate cycle. One was a pension.

So what actually happened in that last widening of the funnel? Two distinct events, layered on top of each other in the same fiscal year, which is why the result looked so much worse than the trend.

The first is interest income. Nepal Telecom sits on an enormous reserve fund roughly Rs 72.7 billion at last disclosure, the accumulated profit of decades of monopoly that has never been fully distributed or reinvested. That cash earns interest, and for a few years it earned a lot of it because interest rates in Nepal were unusually high. As we set out in Monday’s Signal, the 91-day Treasury bill rate peaked above 10.6 percent and has since fallen to around 2.6 percent. When the rate on idle cash falls by roughly three quarters, so does the income that cash produces. Interest income at Nepal Telecom fell about 45 percent from somewhere near Rs 6.8 billion to around Rs 3.7 billion. That single swing, several billion rupees of pre-tax income that simply evaporated with the rate cycle, is the largest piece of the puzzle.

The second is a one-off provision. Under the relevant accounting standard for employee benefits, the company revalued its pension and gratuity obligations using a lower discount rate cut from 7.5 percent to 7.0 percent. The mechanism is worth understanding because it will recur. A defined-benefit obligation is the present value of pensions the company has promised to pay decades into the future. To express those distant promises in today’s rupees you discount them and the lower the discount rate, the larger the present value. Trim the rate by half a percentage point and the booked liability swells, and the swelling has to pass through the income statement in the year it is recognised. Add to that a set of credit-loss provisions against receivables, and you get a charge that landed almost entirely in the second half of the year. It is non-cash, it is largely non-recurring and it is the reason the effective charge against pre-tax profit jumped to roughly 76 percent. The point for an investor is that this was an accounting recognition not a cash outflow and not a sign that the operating business consumed more of its revenue than before.

The half-year split makes the timing unmistakable. Through the first half of FY81/82, Nepal Telecom had already earned net profit of about Rs 4.79 billion. The full year came in at Rs 2.66 billion. That arithmetic implies the company ran an implied net loss of roughly Rs 2.1 billion in the second half alone. A business does not swing from solid profit to a multi-billion-rupee loss in six months because its operations collapsed. It does so because a large, lumpy, backward-looking provision dropped in a single quarter.

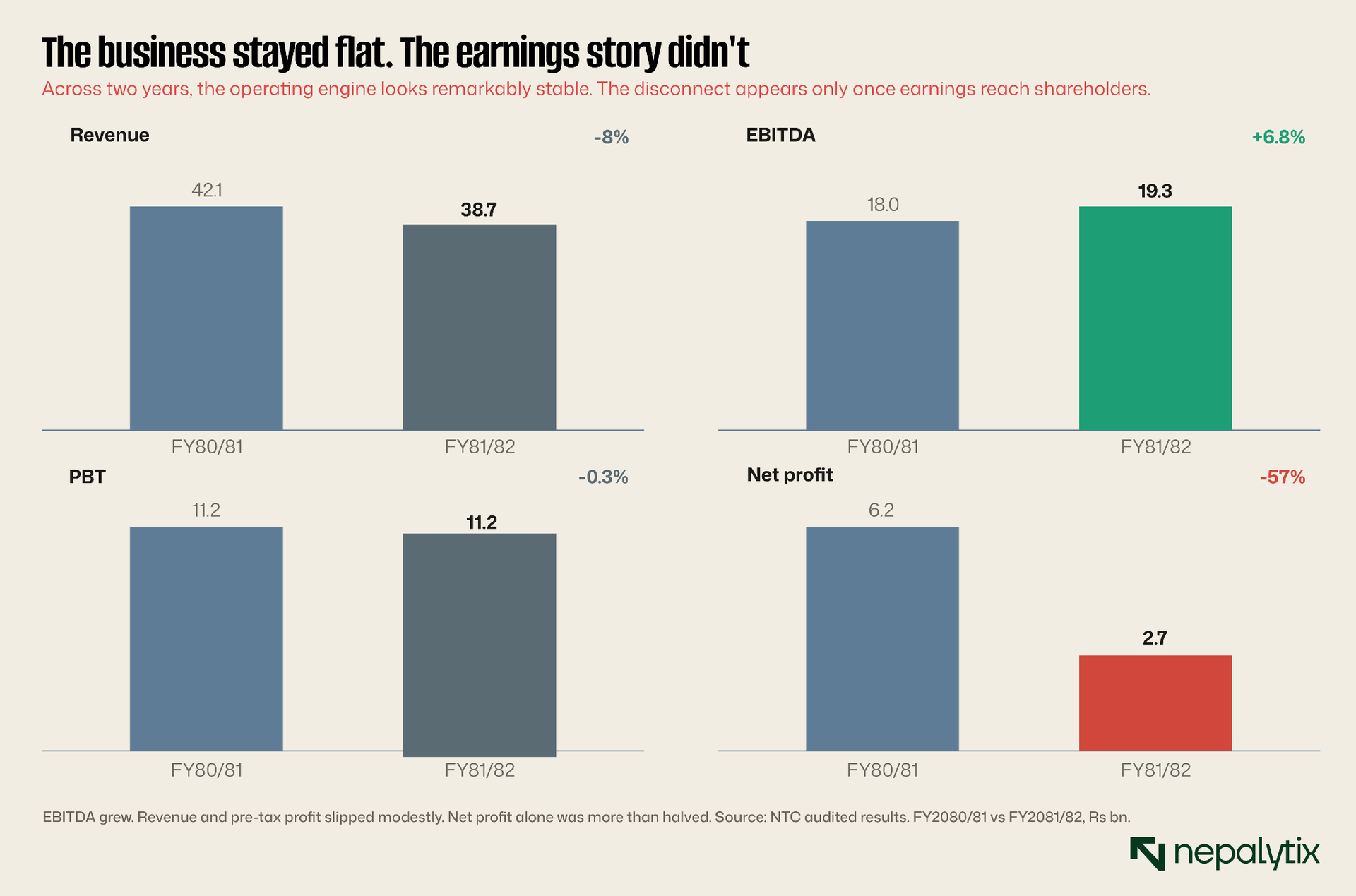

Seen in absolute rupees rather than percentages, the picture is almost calm at the top and violent only at the bottom. Revenue, EBITDA and pre-tax profit are each within a short step of the prior year. Net profit alone is more than halved. The chart is a useful corrective to the headline because percentages exaggerate small bases and the net-profit base is small. In rupee terms, three of the four bars are roughly the same height as last year. One is not.

None of this makes the year good. A company that earns Rs 2.66 billion of audited net profit is, on that measure, a company that earned Rs 2.66 billion and the dividend was set accordingly at 30 percent cash and no bonus. But it does mean the run-rate matters more than the print, and the run-rate has been recovering. First-quarter FY82/83 net profit was Rs 1.32 billion; the first half reached Rs 4.16 billion; third-quarter earnings per share annualised to something in the mid-40s. The provision year is washing out. What it leaves behind is the real question.

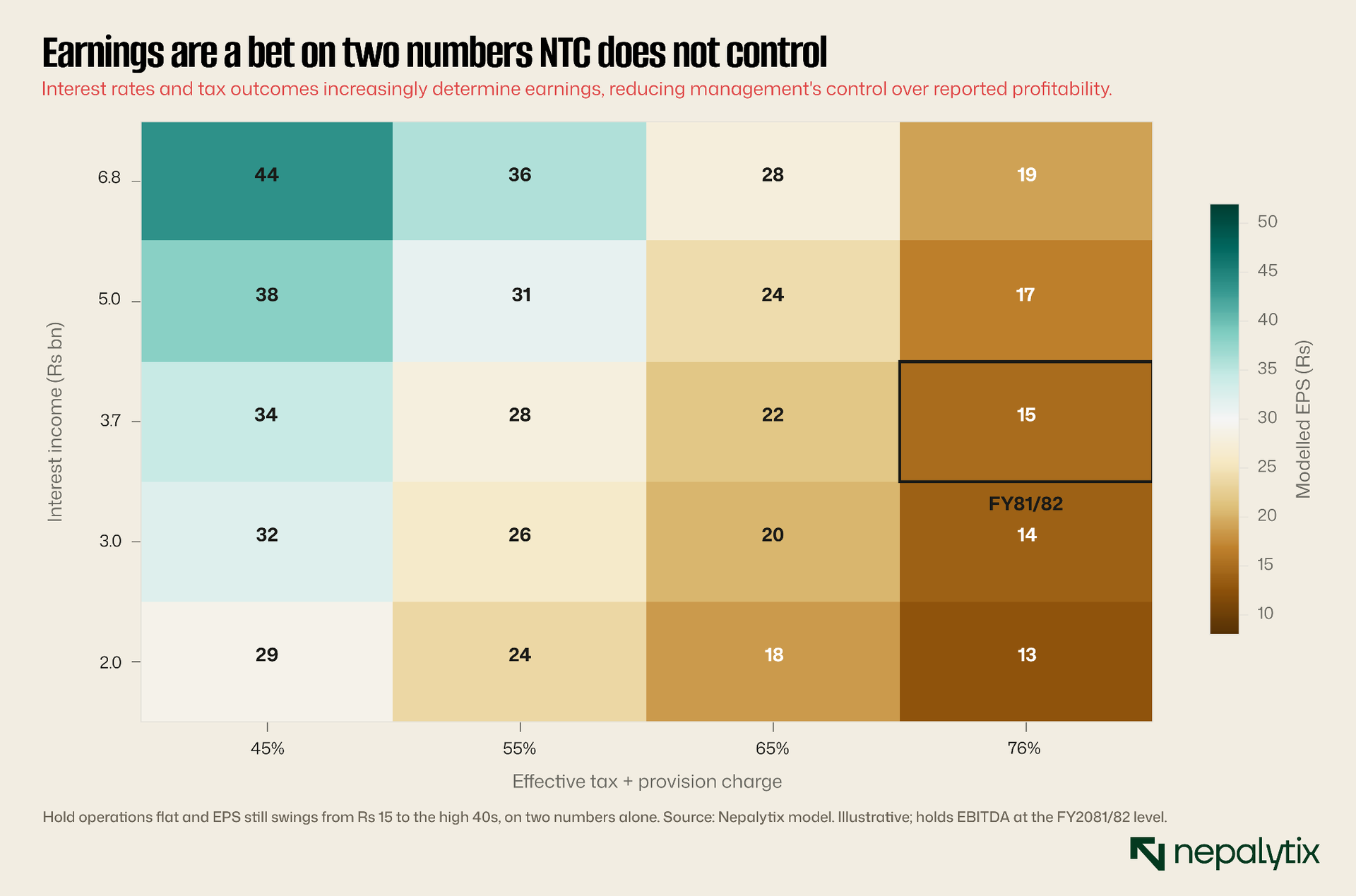

Hold operations flat, and the bottom line is decided by interest rates and the provision charge

Once you accept that the operating business is comparatively stable and the volatility lives below the line, an uncomfortable conclusion follows. Nepal Telecom’s reported earnings are governed, to a remarkable degree, by two variables that management does not control: the interest rate on its cash and the size of the provision and tax charge in any given year.

The grid above is a simple sensitivity model and should be read as illustrative rather than as a forecast. It holds the operating business steady at roughly its FY81/82 level and varies only those two inputs: interest income down the side, from Rs 2 billion to Rs 6.8 billion and the effective charge across the top, from 45 percent to 76 percent. Each cell is the modelled earnings per share that results. The boxed cell is roughly where FY81/82 actually landed, at the punishing intersection of low interest income and a high charge, for a modelled figure near Rs 15. Move to the top-left corner, high interest income and a normal charge, and the same operating business produces well over Rs 40 of earnings per share.

That is a startling range for a company whose underlying network barely changed. It tells you that buying Nepal Telecom is in significant part, buying a position in Nepali interest rates and a guess about provisioning. The franchise is the floor. The rate cycle is the swing. For an equity investor used to thinking about a telco in terms of subscribers and tariffs, this is the first thing that has to be unlearned. Subscribers and tariffs set the operating profit, and the operating profit is the stable part. The exciting part, the part that moved 57 percent is essentially a macro trade wearing a telephone company’s logo.

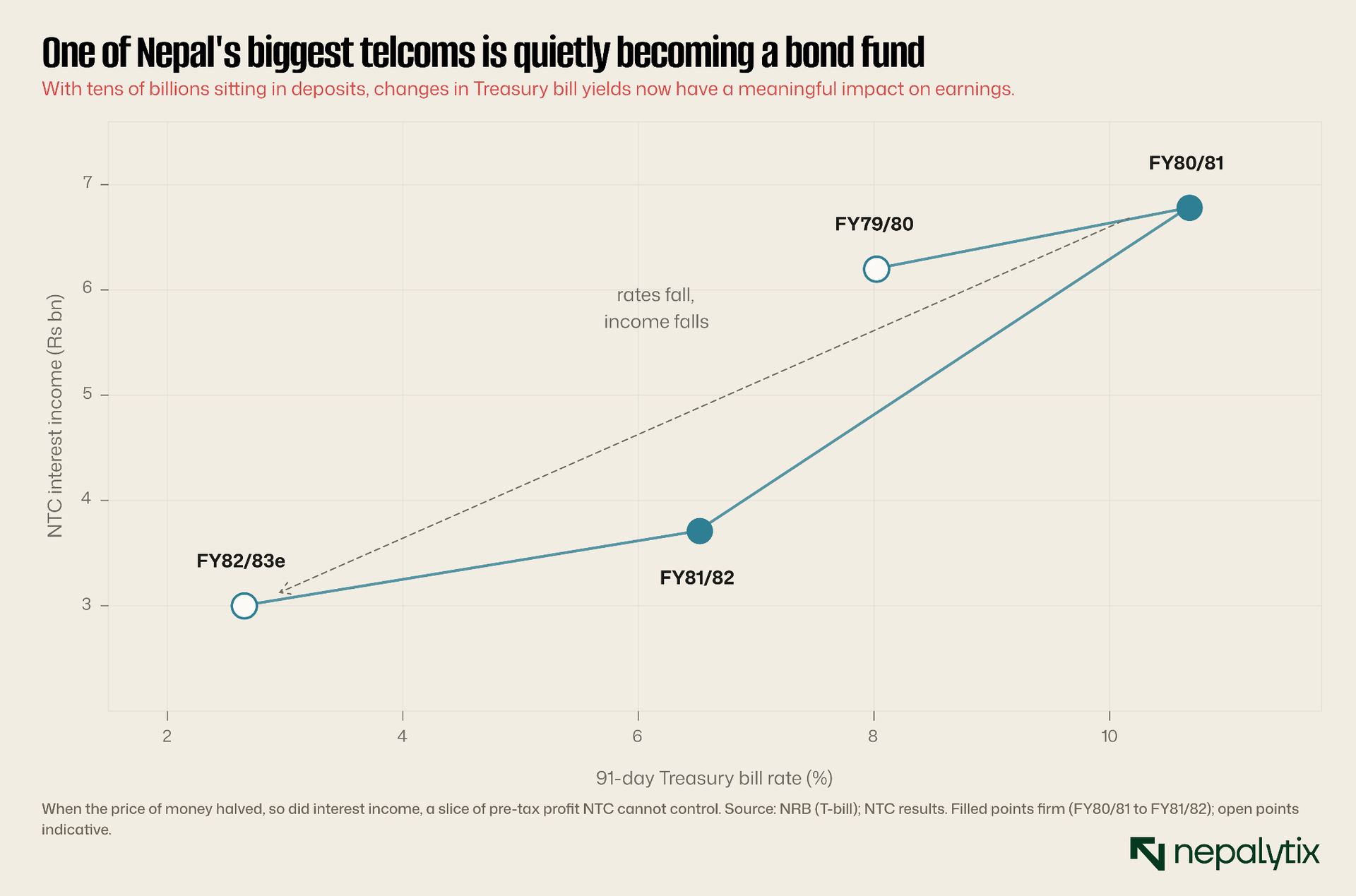

Interest income tracks the Treasury bill rate almost one for one

To make the point concrete, plot interest income against the short-term interest rate directly and the relationship is hard to miss.

The two firm points are the years we can pin down with audited figures: a high-rate year with interest income near Rs 6.8 billion and the low-rate year just reported with interest income near Rs 3.7 billion. The two open points are indicative, sketching where the prior year and the current year-in-progress plausibly sit. The line slopes the way intuition says it should. When the price of money halves so does a meaningful slice of pre-tax profit and there is very little Nepal Telecom can do about it from quarter to quarter.

This is the structural oddity at the heart of the company. A reserve fund of more than Rs 70 billion is, on paper, a fortress. In practice it is a fortress that pays a floating coupon. In the high-rate years it flattered earnings and made the company look more profitable than its operations alone justified. In the low-rate years it does the reverse, dragging reported profit down and making the franchise look weaker than it is. The market, watching the bottom line, cheers in the first case and panics in the second. Neither reaction has much to do with the telecom business.

The fortress balance sheet pays a floating coupon. In good years it flatters the franchise; in bad years it buries it.

There is a sharper way to say this and it is the title of this note. Nepal Telecom is, to a first approximation, a large pool of cash with a national network attached. The cash decides the headline. The network decides the future. Confusing the two is how the market gets this stock wrong in both directions.

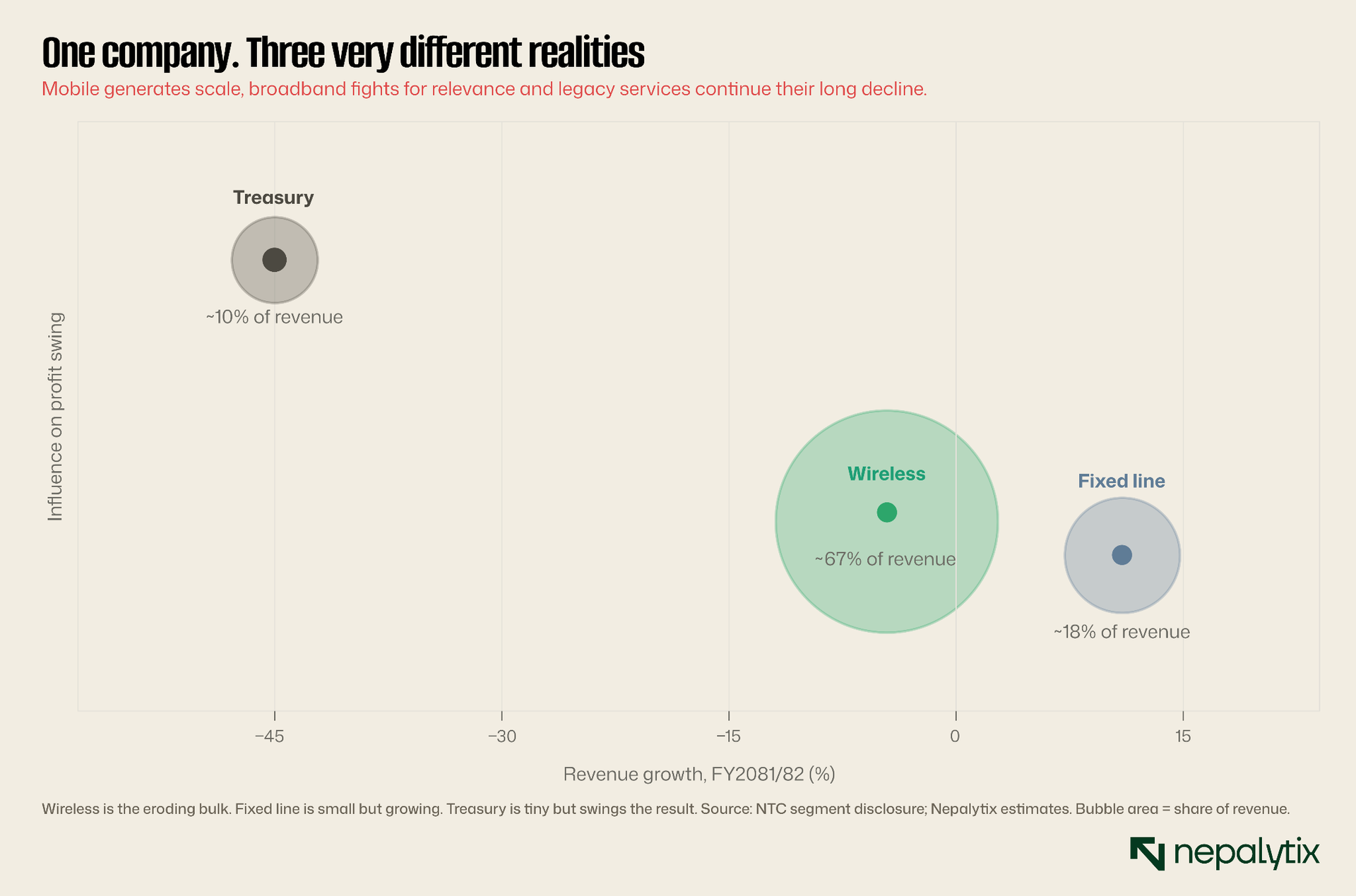

A wireless giant, a fixed-line legacy, and a treasury operation, all under one symbolIf the balance sheet behaves like a bond fund, the operating company is really three businesses stapled together and they could hardly be more different in character. The segment disclosure, confirmed in the company’s formal structure, splits into wireless, fixed line and a treasury function with an unallocated remainder.

Wireless is the engine, by our estimate around two thirds of revenue. It is the business most people mean when they say Nepal Telecom: a national mobile network with the largest subscriber base in the country. It is also the business most exposed to the slow erosion we will come to, because voice and text revenue are being hollowed out by the same internet apps that carry conversations for free. Fixed line is the legacy, around a sixth of revenue, shrinking on the copper side and not yet winning on the fibre side. And treasury, perhaps a tenth of revenue in a normal year, is the cash operation we have just spent two sections on, the one that swings the bottom line far out of proportion to its size. The bubble chart positions each segment by its revenue growth and by how much it moves the consolidated profit line. The takeaway is that the biggest business, wireless, is the one with the softest growth, and the smallest meaningful contributor, treasury, is the one that whipsaws the result. That is an awkward shape for a company. The part that should drive the future is the part that is slowly shrinking, and the part that drives the headline is the part nobody can plan around. A clean operating story this is not. It is worth pausing on the treasury segment, because it is unusual for a telecom operator to run one large enough to matter at the consolidated level. Most network companies carry working capital and perhaps a modest cash buffer. Nepal Telecom carries a reserve fund that rivals its annual revenue, the residue of decades of monopoly profits that were neither fully distributed to the state nor reinvested in the network. That money has to sit somewhere, and where it sits is in deposits and government paper, earning whatever the prevailing rate happens to be. The result is that a chunk of what looks like a telecom company’s profit is, in substance, the return on a sovereign-and-deposit bond portfolio. When you value the operating business you are valuing two thirds of a company; the other third is a fixed-income fund whose yield you cannot forecast.

Dominant where the market is maturing

Now to the operating business proper because this is where the slow decline actually lives. Nepal Telecom’s competitive position is a study in being strongest exactly where it matters least.

In mobile, the company is still the leader. On the most recent regulator data it holds roughly 54 percent of mobile voice and about 56 percent of mobile internet ahead of Ncell on both. Its voice subscriber base runs past 16 million on a population where voice penetration has already passed 100 percent. These are commanding numbers. They are also numbers in a maturing, in places declining, market. Voice and SMS revenue per user has been falling for years as over-the-top apps such as WhatsApp and Viber absorb the calls and messages that once showed up on a bill. International call revenue historically a fat margin line for the incumbent has been particularly hard hit. Being the largest player in a shrinking pool is still better than the alternative but it is not growth.

Fibre is where the growth is and fibre is where Nepal Telecom is weak. Total fixed broadband connections in the country run to roughly 3.4 million and the leaders are private internet service providers, not the state incumbent. WorldLink alone holds close to 1.08 million connections around 31 percent of the market and comfortably first. Dish Home and Vianet each sit in the mid-300-thousands. Nepal Telecom with about 354,000 fibre-to-the-home connections is fourth on a market share near 10 percent and it is adding only around 27,000 connections a year. In the one part of the communications market that is unambiguously growing, where households are actually choosing to spend more, the former monopolist ranks behind three private competitors and is gaining ground slowly.

There is a second-order squeeze hiding inside these numbers. As private ISPs wire up homes with fibre, those same households increasingly route their phones onto home and office WiFi the moment they walk through the door. Mobile data, the one growing line inside the wireless business, leaks onto fixed broadband that a competitor owns. So the fibre weakness is not contained to the fixed-line segment; it quietly caps the upside in mobile data too. Meanwhile the richest legacy line of all, international call termination, the fee the incumbent earned for landing calls from the Nepali diaspora abroad has been gutted by the same over-the-top apps that carry those calls as data for nothing. Each of these erosions is small in a given quarter. Compounded over years, they are in decline.

Nepal Telecom owns the market that is going away and rents space in the market that is arriving.

That is the entire operating thesis in one sentence. This is the texture of a monopoly in slow decline. There is no cliff, no single quarter where the franchise visibly snaps. There is instead a steady reallocation of where Nepalis spend their communications money away from the metered voice and SMS that the incumbent dominates and toward the fibre and data that private players lead. Nepal Telecom is not losing the war in any given month. It is losing the map.

5G is stalled and the bill to fix that is larger than a year of profit

Layer onto the competitive picture a problem of capital. The next leg of mobile is 5G and on 5G Nepal Telecom has stalled. The company has run internal trials on the 2600 MHz band, but there is no nationwide commercial rollout, at a point when neighbouring India and China have deployed at national scale. A modern 5G network across Nepal’s difficult terrain is not cheap. We estimate the capital cost at somewhere in the order of Rs 50 to 60 billion and that figure should be treated as a rough estimate rather than a disclosed number.

Set that against an audited net profit of Rs 2.66 billion and the tension is obvious. Even on a normalised run-rate closer to Rs 8 billion, a 5G build of that scale is several years of entire net profit. The company does, of course, have the reserve fund and 5G is precisely the kind of long-horizon national-infrastructure project that such a fund could in principle finance. But spending the cash pile on 5G means giving up the interest income that the cash pile generates, which is currently doing a great deal of heavy lifting on the bottom line. The reserve fund cannot be both the earnings cushion and the capital-expenditure war chest at the same time. Management, and its majority owner the government, will at some point have to choose. So far they have chosen to wait.

Waiting has a cost. Every year that 5G slips is a year in which the data growth that should accrue to the incumbent’s mobile network is more likely to be captured by fixed wireless and fibre from private competitors, the very players already winning the broadband market. The capital overhang is not just a balance-sheet question. It is the mechanism by which the slow decline could speed up.

The Ncell wildcard: A contested, low-probability scenario that nonetheless sits in the file

No honest note on Nepal Telecom can ignore its competitor’s ownership saga because the two are entangled by policy. Ncell, the private number two in mobile, recently became fully Nepali-owned after its foreign parent’s stake changed hands. There is a long-running and contested expectation tied to the terms of Ncell’s licence that its assets could revert to state hands toward the end of the decade.

We flag this for completeness and then set it down lightly, because it is genuinely uncertain and the timeline and mechanism are both disputed. If something like a reversion did occur, the competitive map for Nepal Telecom would change materially, potentially in its favour. But betting an investment case on a contested policy outcome several years away is not analysis, it is speculation, and we will not dress it as anything else. It belongs in the risk register as a low-probability, high-impact wildcard, not in the base case.

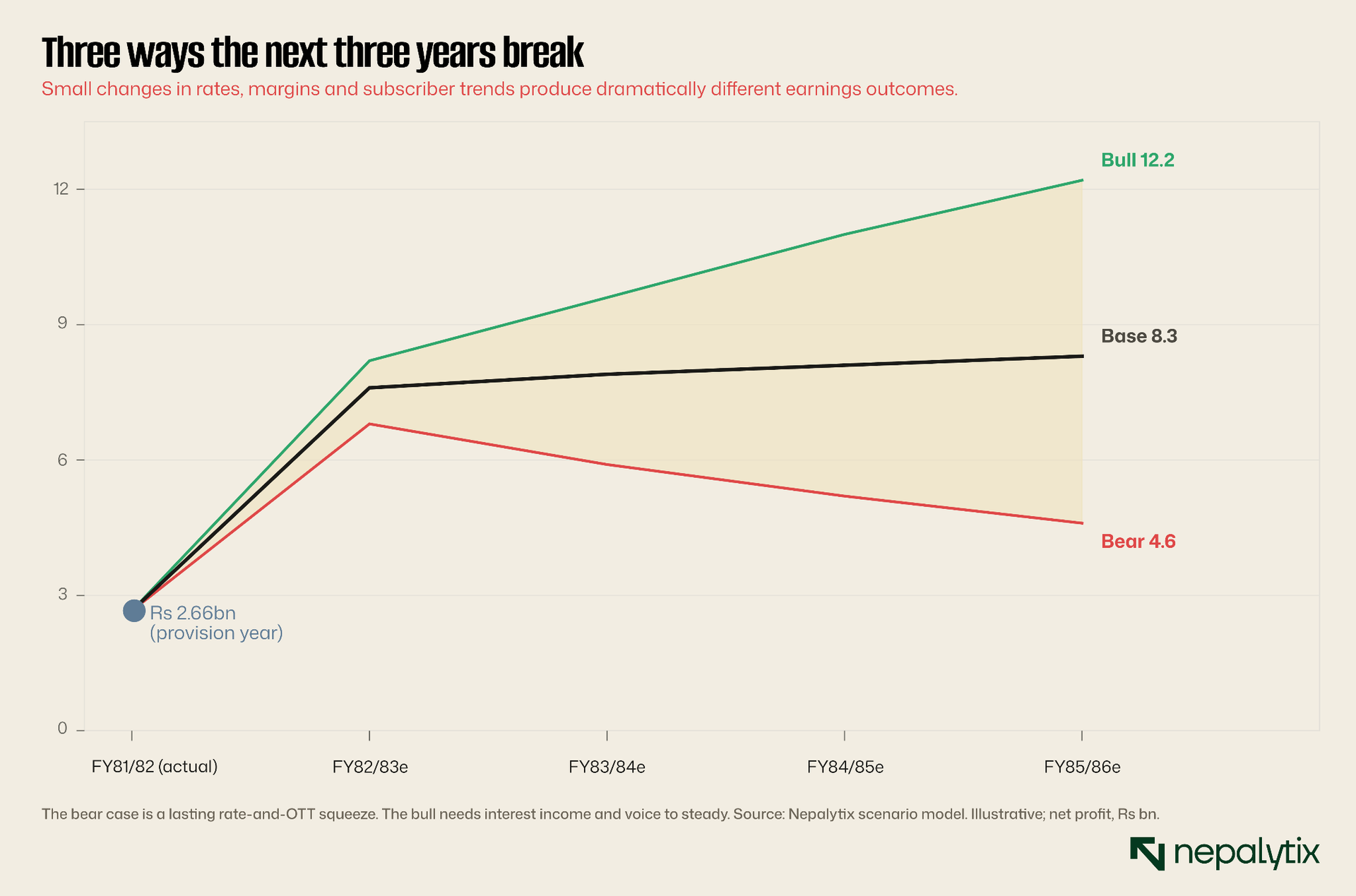

Three scenarios, driven mostly by rates, provisions and the pace of erosion

Pull the threads together and the forward path is less about subscribers than about the two below-the-line variables and the speed of the operating drift. The cone below sketches three illustrative net-profit scenarios out to FY85/86. It is a scenario model, not a forecast and the numbers are deliberately round.

The base case, in the middle, has net profit recovering from the depressed Rs 2.66 billion print toward something in the region of Rs 8 billion as the provision year washes out and interest income stabilises at a lower but positive level, while the operating business continues to erode gently. This is roughly consistent with the recovering run-rate visible in the recent quarterly numbers. It assumes no disaster and no miracle.

The bear case, the lower line has interest rates staying low, a further squeeze from over-the-top erosion of voice and SMS, fibre share gains failing to offset legacy decline, and net profit settling nearer Rs 4.6 billion. The bull case, the upper line, has rates recovering, the reserve fund again earning a fat coupon, a successful pivot into fibre and eventually 5G and net profit pushing past Rs 12 billion. The width of the cone is itself the message. A company whose earnings hinge on interest rates and provisions has a genuinely wide range of plausible outcomes, and most of that width comes from factors the company does not control.

Note what is not in any of these scenarios: a return to rapid growth. Even the bull case is, at heart, a story about a stable franchise earning a good coupon on its cash, not about a telco winning new markets. That is the honest ceiling on this business as currently configured.

Valuation: the market already pays for the recovery

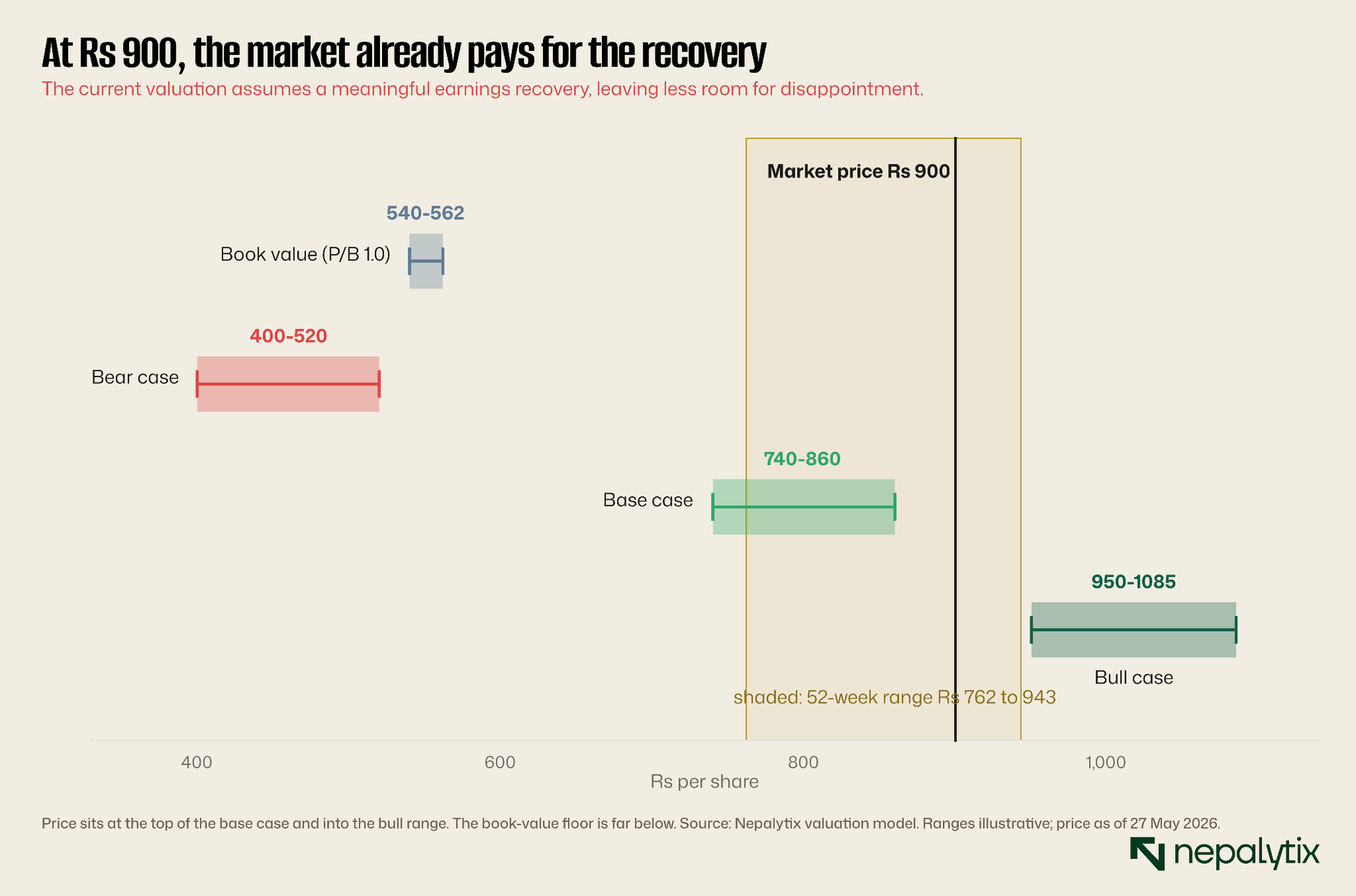

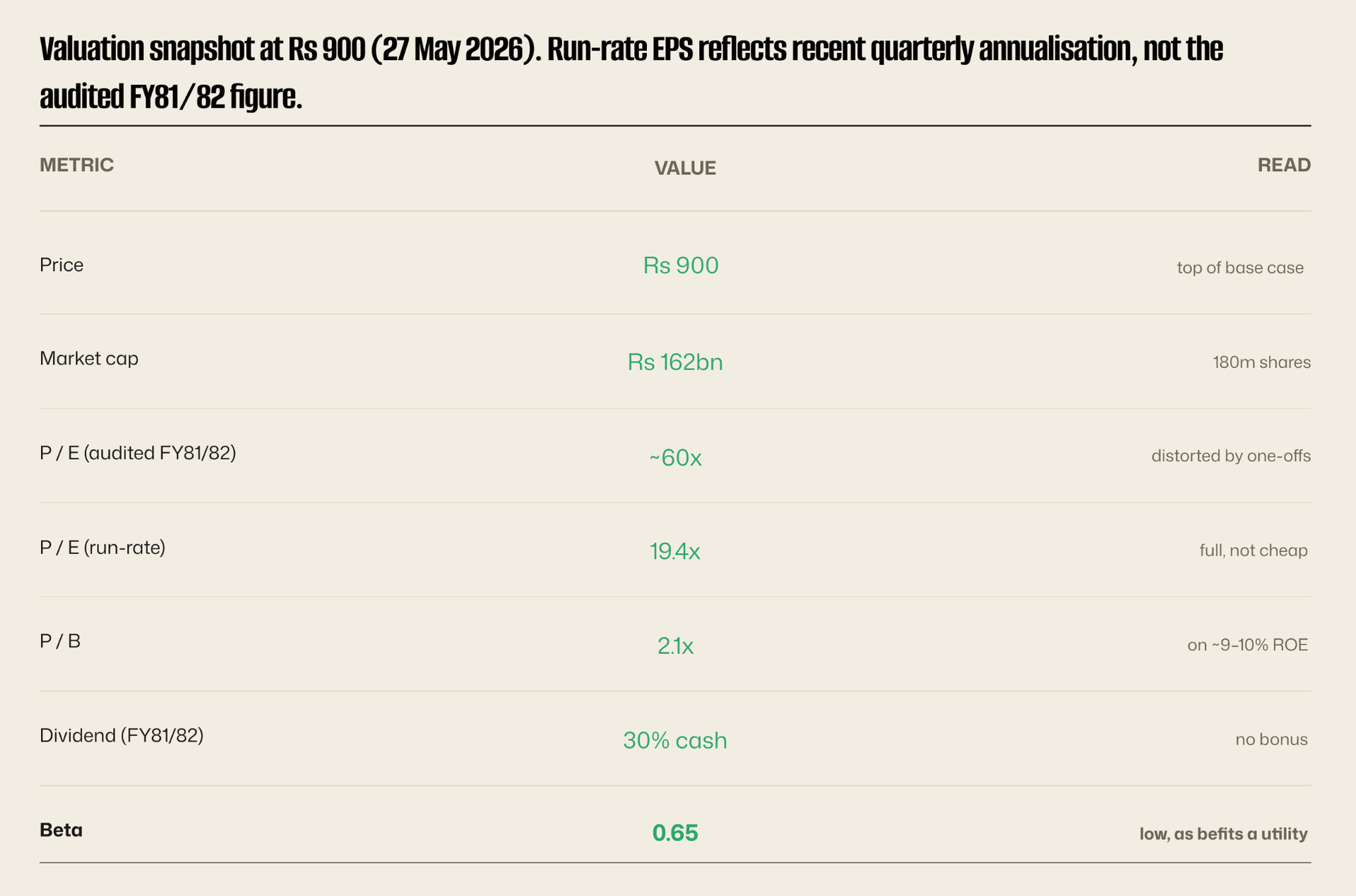

At Rs 900, the price sits at the top of the base case and into the bull range. Which brings us to price and to the question every initiation has to answer: is the stock cheap? At Rs 900, with Rs 162 billion of market capitalisation, the answer is no, not obviously and arguably the opposite.

The valuation range above is illustrative and built from the scenarios just described. Book value provides a floor near Rs 540 to 560 per share against a stated book value per share of Rs 551. Our bear case sits well below the current price. Our base case spans roughly Rs 740 to 860. The bull case reaches into the Rs 950 to 1,085 region. The current market price of Rs 900, the vertical line, sits at the very top of the base case and pokes into the bull range. The 52-week trading band is shaded behind it for context.

Read that honestly and it says the market is not pricing Nepal Telecom for its depressed FY81/82 earnings at all. On the audited number, the trailing price-to-earnings multiple would be an absurd 60-odd times, which nobody sensible is paying. The market is instead pricing the recovered run-rate, where a price-to-earnings multiple near 19 times on normalised earnings of around Rs 46 to 47 per share looks far more reasonable, and a price-to-book of 2.1 times on a 9 to 10 percent return on equity is full but not insane. In other words, the share price has already done the work of looking through the bad year. The recovery is in the price.

That is the crux of the valuation case. To make money from here, you do not need the bad year to wash out, because the market has already assumed it will. You need the business to beat the recovered run-rate, which means you need some combination of higher interest rates, a faster fibre pivot, a 5G story that the market can believe or the ownership change we turn to next. Absent those, at Rs 900 you are paying a fair price for a stable-to-slowly-declining franchise and being asked to hope for the upside. This is not a deep-value situation. It is a quality-at-a-full-price situation, with a structural drift working against you.

The blue chip almost nobody can own

There is one more fact about Nepal Telecom that shapes everything else and it is on the share register rather than the income statement. The government of Nepal owns 91.49 percent of the company. The investing public holds 8.48 percent. A sliver sits with the citizen investment fund. For one of the largest companies on the exchange, the tradeable float is tiny.

The waffle makes the imbalance plain. Of every hundred shares, more than ninety belong to the state and fewer than nine trade. A float that thin distorts everything around it. It makes the share price more volatile and more easily moved, it concentrates governance entirely in government hands, and it means the market price is set by the small minority of shares that actually change hands rather than by the company’s full economic weight. Price discovery on a 9 percent float is a noisy business.

This is also where the single largest catalyst sits. The government has signalled, in the budget announced in Jestha 2082 and reiterated by the finance minister since, an intention to divest Nepal Telecom down to a 30 percent public float. The right panel of the chart shows what that would look like: the public block roughly trebling, the state block falling to 70. If it happens, and the history of state divestment in Nepal counsels patience on the timing, it would be the most consequential event in the stock’s recent life. A larger float would deepen liquidity, broaden the shareholder base, sharpen price discovery, and quite possibly force a more commercial posture on a company that has long had the luxury of a single, patient, non-commercial majority owner.

It cuts both ways for the share price. A large new supply of stock hitting the market could weigh on the price in the near term, the standard overhang that accompanies any big divestment. But a more liquid, more widely held, more commercially run Nepal Telecom is plausibly a more valuable one over time. We would watch the divestment timeline more closely than any single quarter of earnings. It is the one development that could change what kind of company this is, rather than merely how good or bad a given year looks.

What we are watching

If the operating business changes slowly and the headline is governed by forces outside management’s control, then the things worth tracking are not the routine quarterly beats and misses. They are the structural shifts that would change what kind of company this is. There are four that matter.

First, the divestment. The government’s plan to take the public float to 30 percent is the single largest swing factor in the story, and its timing is the great unknown. Watch the budget cycle and the finance ministry’s follow-through rather than the company’s own announcements. A credible, scheduled sale would change the liquidity, the governance and the commercial posture of the business all at once and would likely matter more to the long-run value than any two or three years of earnings.

Second, the interest rate path. Because a meaningful slice of pre-tax profit is the coupon on the reserve fund, the direction of short-term rates is bluntly, a direction of Nepal Telecom’s reported earnings. A sustained recovery in the Treasury bill rate would lift the bottom line mechanically, with no operational change required. A prolonged low-rate environment would keep the headline suppressed even as the operations tick along. This is the variable to model first and the one the market most often confuses with company performance.

Third, the fibre trajectory and the 5G decision. These are the two operating levers that could either arrest the slow decline or confirm it. A visible acceleration in fibre-to-the-home additions, narrowing the gap with WorldLink and the other private leaders, would be the first hard evidence that the incumbent can compete where the market is actually growing. A funded, scheduled 5G rollout would be the second. Continued drift on both, which is the current state, validates the bear case by default.

Fourth and most lightly, the Ncell ownership question. We treat it as a low-probability wildcard rather than a forecastable event, but any concrete policy movement on the licence or the asset would warrant a full reassessment of the competitive map. Until then it sits in the file and not in the model.

Notice what is absent from this list: subscriber adds, tariff tweaks, the next dividend. Those are the metrics a conventional telco analyst would lead with, and for Nepal Telecom they are largely noise around a stable operating core. The signal is in the rate cycle, the float, and the two capital decisions. Watch those, and you are watching the company. Watch the quarterly net-profit headline in isolation, and you are mostly watching interest rates and accounting.

The bottom line: A stable franchise, a macro-driven headline, a full price, and one catalyst worth watching.

Initiate, then, with a clear-eyed rather than an enthusiastic view. Nepal Telecom is a high-quality, low-growth, structurally drifting incumbent whose reported earnings are dominated by forces below the operating line. The 57 percent profit collapse that defined its year was overwhelmingly a rate-and-provision event, not an operational one; pre-tax profit was flat and EBITDA grew. Anyone selling the stock on the headline misread the income statement. But anyone buying it as a recovery bargain should look at where the price already sits.

The operating reality underneath is a monopoly in slow decline. The company is dominant in mobile voice and mobile internet, both maturing, and a distant fourth in fibre, the one part of the market that is growing. Over-the-top apps continue to erode its richest legacy revenue. A 5G bill it cannot comfortably fund hangs over the next several years, and spending the reserve fund to meet it would cost the very interest income that currently props up the bottom line. None of this is an emergency. All of it is a drift.

At Rs 900, on a run-rate price-to-earnings near 19 times and a price-to-book of 2.1 times, the market has already looked through the bad year and is paying for the recovery. That leaves little margin of safety and puts the burden of proof on the upside. The genuine swing factor is not next quarter’s earnings but the government’s planned divestment to a 30 percent float, which over time could change the company’s liquidity, its governance, and its commercial ambition. That is the thing to watch.

Put simply: a fortress balance sheet, a fading franchise, a fair-to-full price and one structural catalyst that could reset the whole picture. A cash pile wearing a telcom priced as though the telcom is doing the earning. It mostly isn’t.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.