Standard Chartered Nepal is choosing stability over growth.

Standard Chartered Nepal appears to be underperforming its peers on growth and earnings, but a deeper analysis reveals a deliberate strategy focused on capital discipline, low-cost funding, and high-quality returns rather than aggressive expansion.

Standard Chartered Nepal earns less than its peers, lends less, holds more capital and pays less for deposits. The number says it is winning a different game.

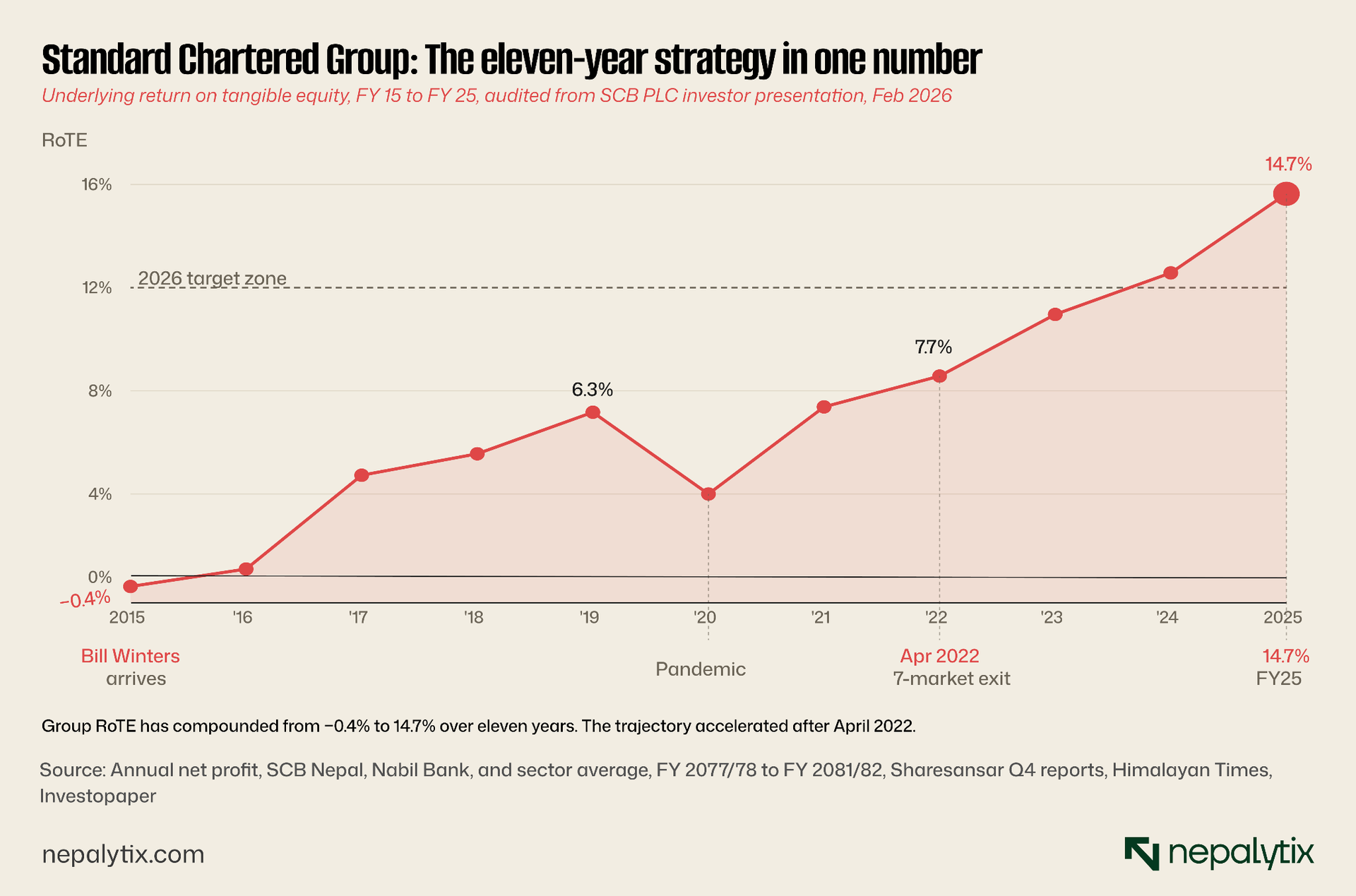

In June 2015, Bill Winters became group chief executive of Standard Chartered PLC. The London-listed bank operated in dozens of markets across Asia, Africa, and the Middle East, and was struggling to earn its cost of capital. The strategy that emerged over the following decade was unusual for a global bank. Rather than expand, Standard Chartered would leave several markets entirely. Rather than chase scale, it would shrink toward the corporate clients and cross-border franchises where it could compound returns.

The most visible expression of that strategy came in April 2022 when Standard Chartered announced full exits from Cameroon, Gambia, Sierra Leone, Angola, Zimbabwe, Lebanon, and Jordan, alongside consumer-banking withdrawals from Tanzania and Côte d'Ivoire. The group underlying return on tangible equity stood at 7.7 percent that year. By fiscal 2025, on the strength of those exits and the discipline that surrounded them, the figure had reached 14.7 percent.

Six and a half thousand kilometres east of London, Standard Chartered owns 70.21 percent of a small commercial bank listed on NEPSE. Standard Chartered Bank Nepal Limited is the smallest of Nepal's twenty commercial banks by every balance-sheet measure that matters: deposits, loans, paid-up capital. Its earnings have declined for three consecutive fiscal years. The local financial press has read this as caution, or worse, decline.

The reading is wrong. SCB Nepal is executing the same strategy its London parent has spent a decade refining and the numbers, read against the right benchmarks, say it is winning.

The bank that does not behave like its peers

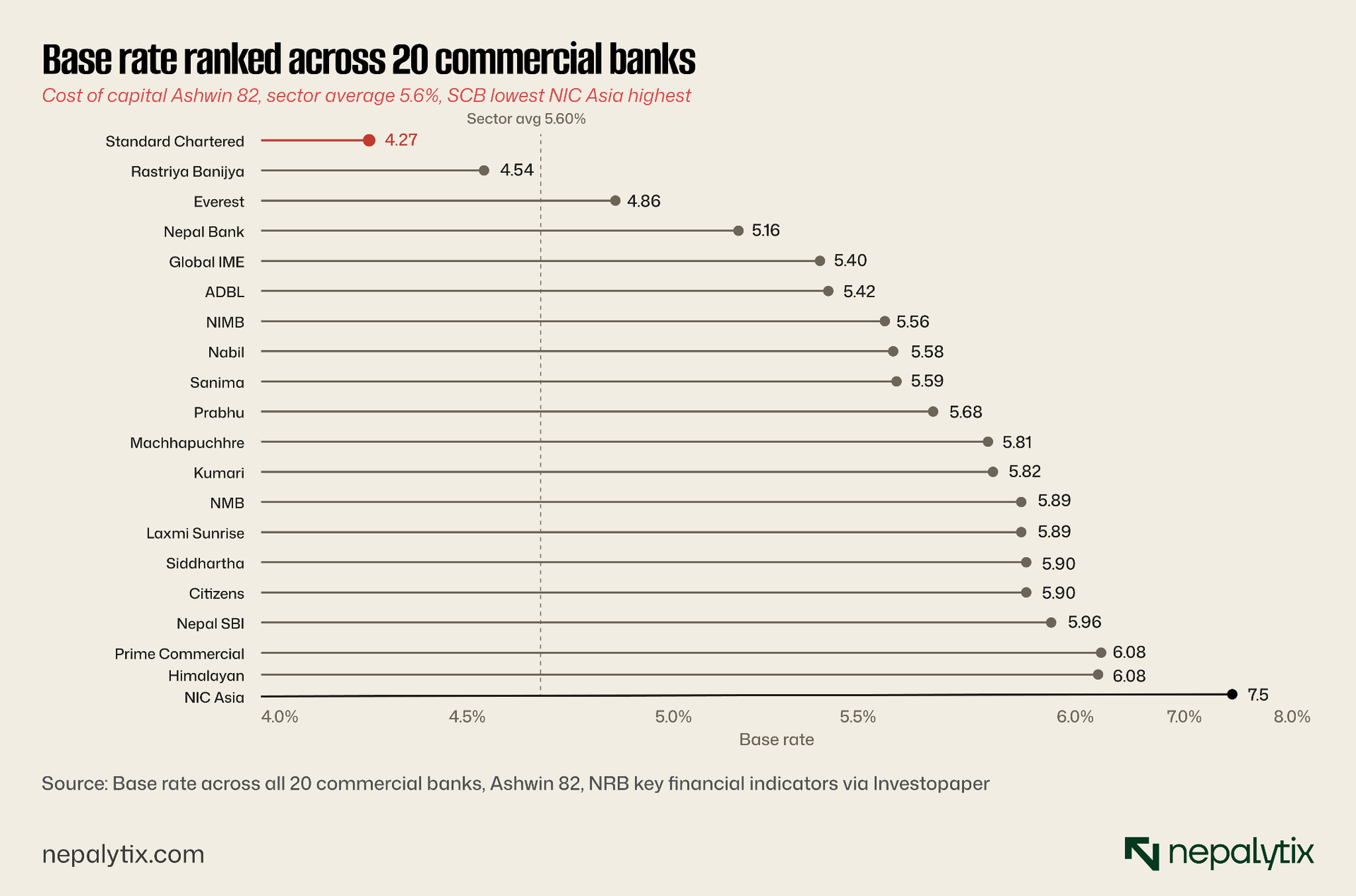

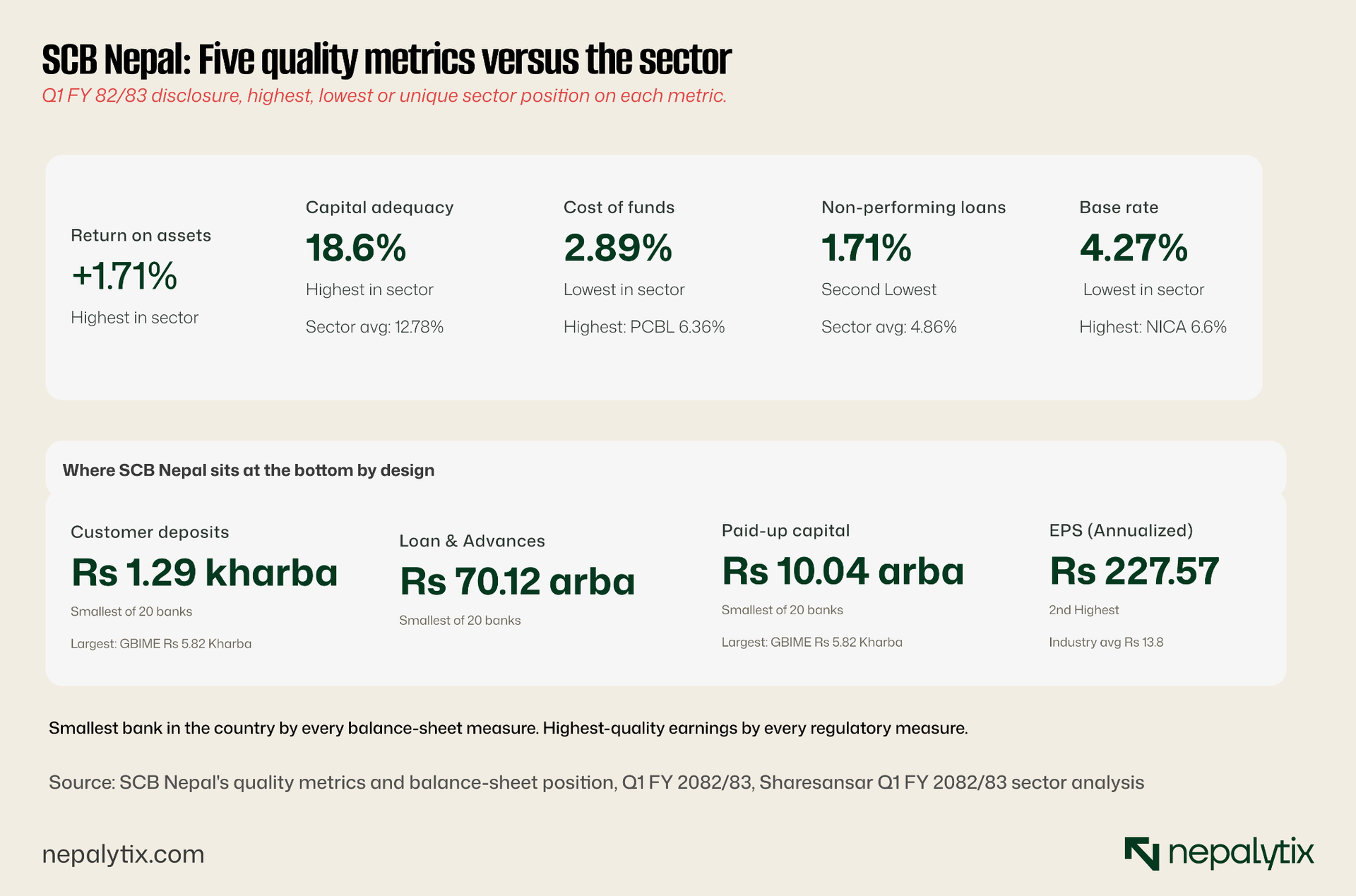

To understand SCB Nepal, look at what it does not do. It does not chase deposit market share. Its base rate at Ashwin 82, the most recent disclosure, was 4.27 percent, the lowest among the twenty Nepali commercial banks, against a sector average of 5.60 percent and a high of 6.60 percent at NIC Asia. The 233-basis-point gap between the cheapest and most expensive cost of capital in the sector is the gap between a deposit franchise held by relationship and one held by yield.

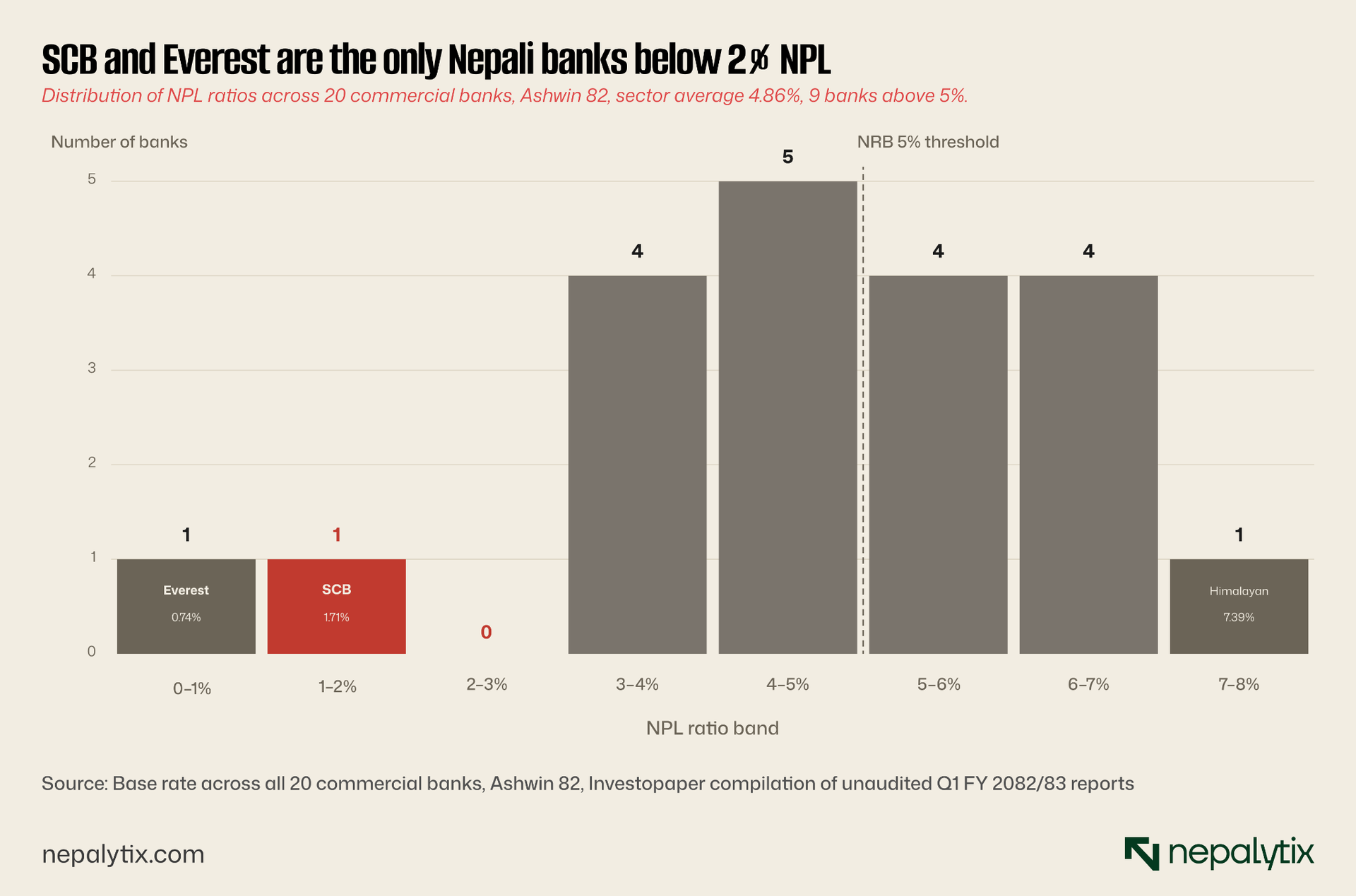

It does not chase loan growth either. While most Nepali commercial banks expanded credit aggressively through the FY 2079–2080 window, the years that produced the asset-quality crisis, now visible at NIC Asia, Himalayan, and Kumari, SCB Nepal kept its book conservative. Its gross non-performing loan ratio at Ashwin 82 was 1.71 percent, against a sector average of 4.86 percent and a regulatory threshold of concern at 5 percent. Only Everest Bank, at 0.74 percent, reported a lower figure. The remaining eighteen banks spread broadly from 3 percent to over 7 percent. SCB and Everest are alone in the band below 2 percent.

It does not chase scale. Capital adequacy at the close of FY 2081/82 was 17.82 percent against a regulatory minimum of 11.0 percent and a sector average near 12.78 percent. By Ashwin 82, the next disclosure that figure had risen to 18.60 percent, the highest in the sector by a clear margin. The next-highest bank at the FY-end snapshot, Prabhu at 13.90 percent, sat 392 basis points below.

Three years of declining earnings

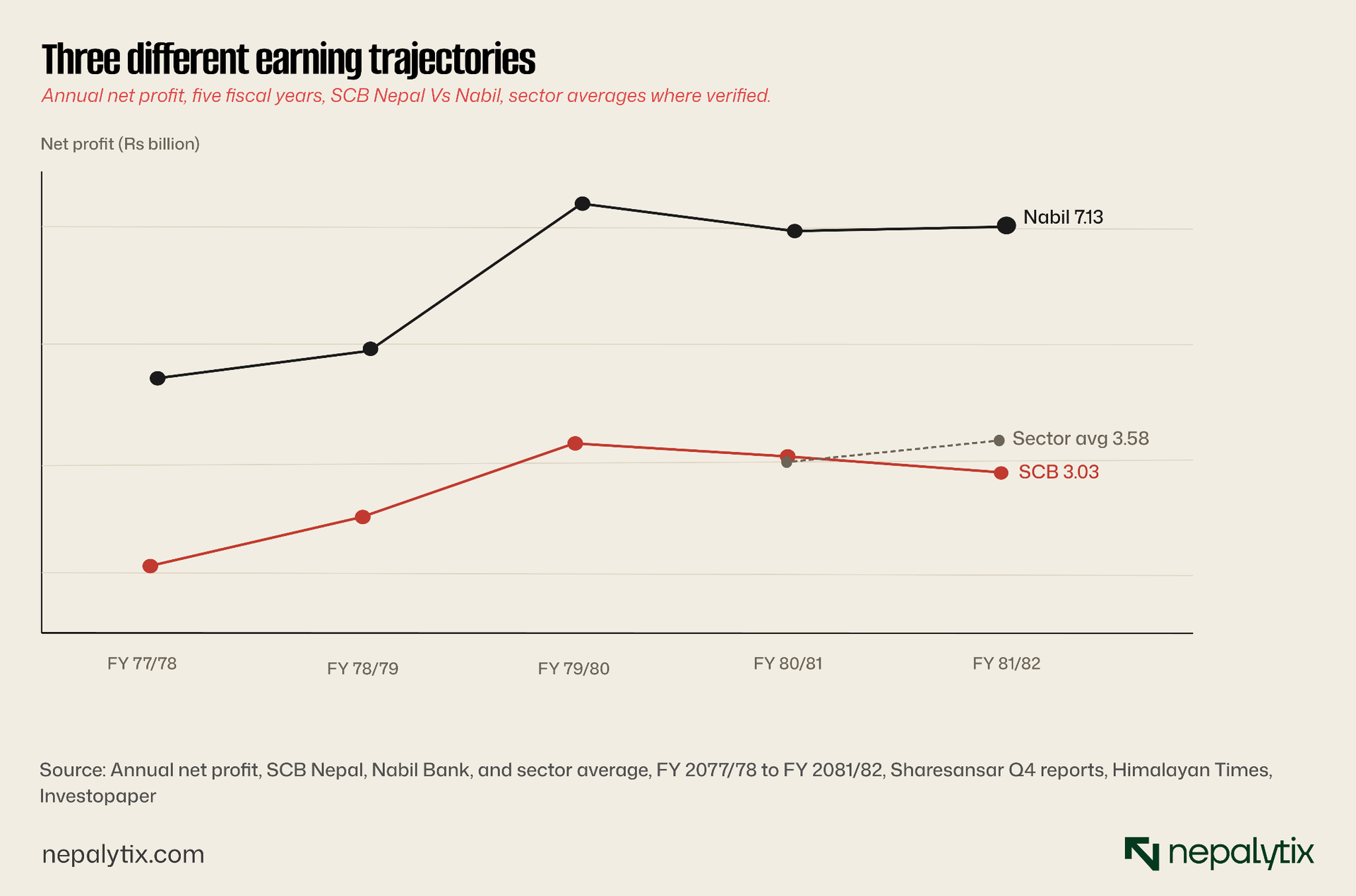

SCB Nepal's annual net profit has fallen for three consecutive fiscal years. In FY 2078/79, the bank earned Rs 2.26 billion, a 62 percent jump on the previous year. The trajectory continued upward to Rs 3.52 billion in FY 2079/80. Then it reversed: Rs 3.30 billion in FY 2080/81, and Rs 3.03 billion in FY 2081/82. The 39th Annual General Meeting in late 2025 disclosed underlying profit after tax of Rs 3 billion, return on equity of 14.3 percent, earnings per share of Rs 30, and a 19 percent cash dividend.

The same period at Nabil Bank, the closest comparable in the upper tier of Nepali commercial banking, looked very different. Nabil's net profit moved from Rs 4.50 billion in FY 2077/78 to Rs 7.13 billion in FY 2081/82, with a sharp jump in FY 2079/80 driven by the merger with Nepal Bangladesh Bank. The sector aggregate over the same window shows growth: total commercial-banking net profit rose from Rs 64.15 billion in FY 2080/81 to Rs 71.50 billion in FY 2081/82, a 43 percent year-on-year increase.

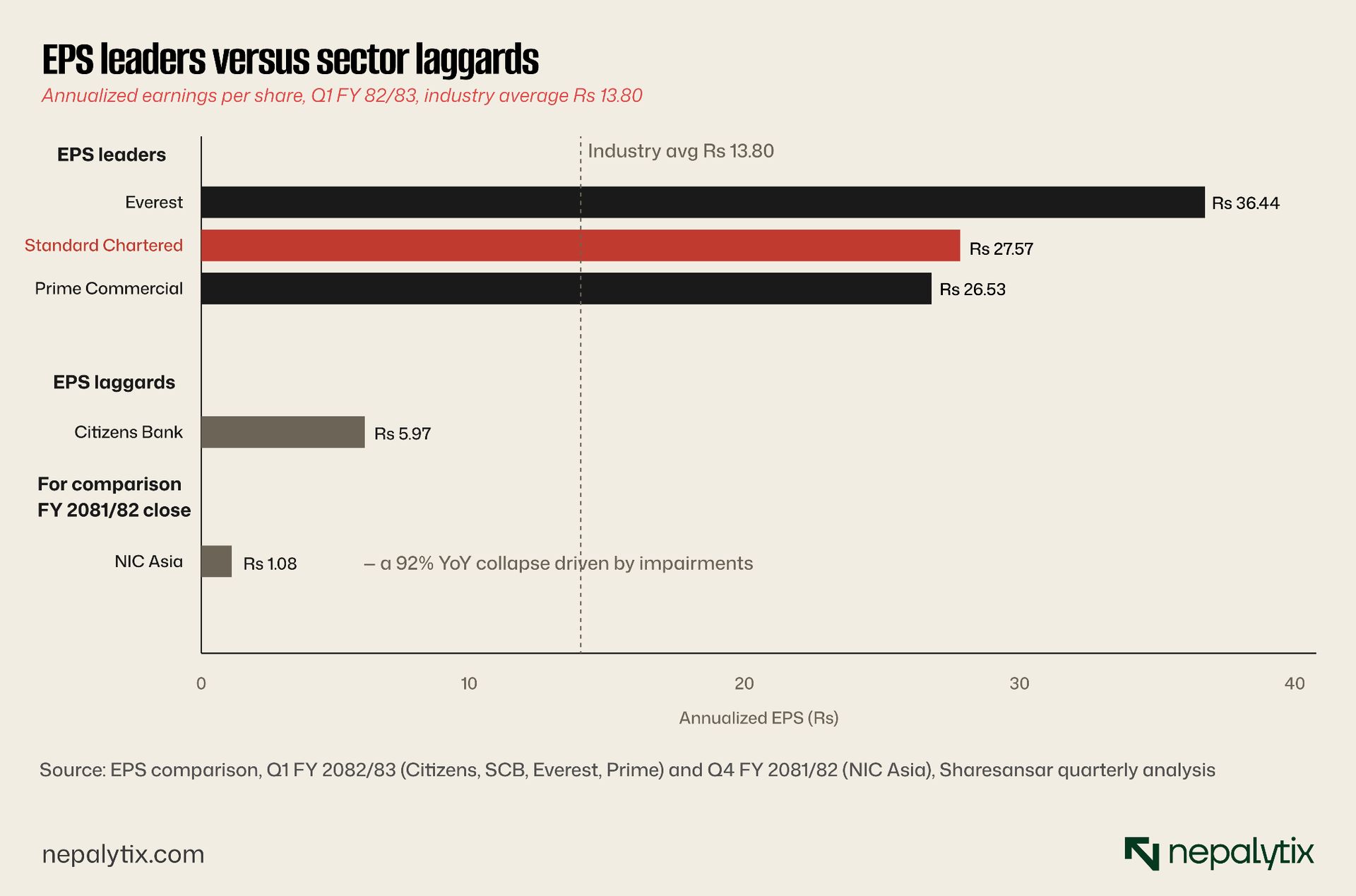

Read in isolation, three consecutive years of declining earnings looks like a problem. Read against the bank's other quarterly disclosures, it looks deliberate. SCB Nepal's Q1 FY 2082/83 results, published in November 2025, disclosed return on assets of 1.71 percent, the highest in the sector. Cost of funds at 2.89 percent, the lowest in the sector, against PCBL's 6.36 percent. EPS at Rs 27.57, second only to Everest's Rs 36.44 and well above the industry average of Rs 13.80. The bank earns less in absolute rupees because it has less capital, fewer loans, and a smaller deposit base. The earnings it does generate are, by every quality metric Nepal Rastra Bank publishes, the cleanest in the country.

The London playbook, applied locally

Standard Chartered Group's strategy under Bill Winters is unusual among global banks. Rather than expand, the parent has spent a decade contracting toward a smaller set of high-quality markets. The April 2022 announcement was the most public expression: full exits from seven markets in Africa and the Middle East, alongside consumer-banking pull-backs from two more. Each of those decisions reflected the same underlying logic that operating in a market where the bank could not be the partner of choice, at the scale required to earn its cost of capital, was a worse use of group resources than redeploying them.

Read SCB Nepal's behaviour against that playbook and the picture clarifies. Nepal is, by any global-banking measure, sub-scale. The country's entire commercial banking sector at FY 2081/82 closed Rs 64.43 Kharba in customer deposits, roughly Rs 6.4 trillion, a figure that would not register as material on Standard Chartered's group balance sheet. There is no realistic future in which SCB Nepal becomes a dominant local player. There is no path by which it competes on lending volume with NIC Asia, Nabil, or Global IME. What Nepal is, instead, is a profitable corner of a global network, a market where Standard Chartered can do what it does well anywhere else: serve cross-border corporates, finance trade, run a conservative deposit franchise, and earn high returns on a small balance sheet.

The earnings of a bank that refuses to grow

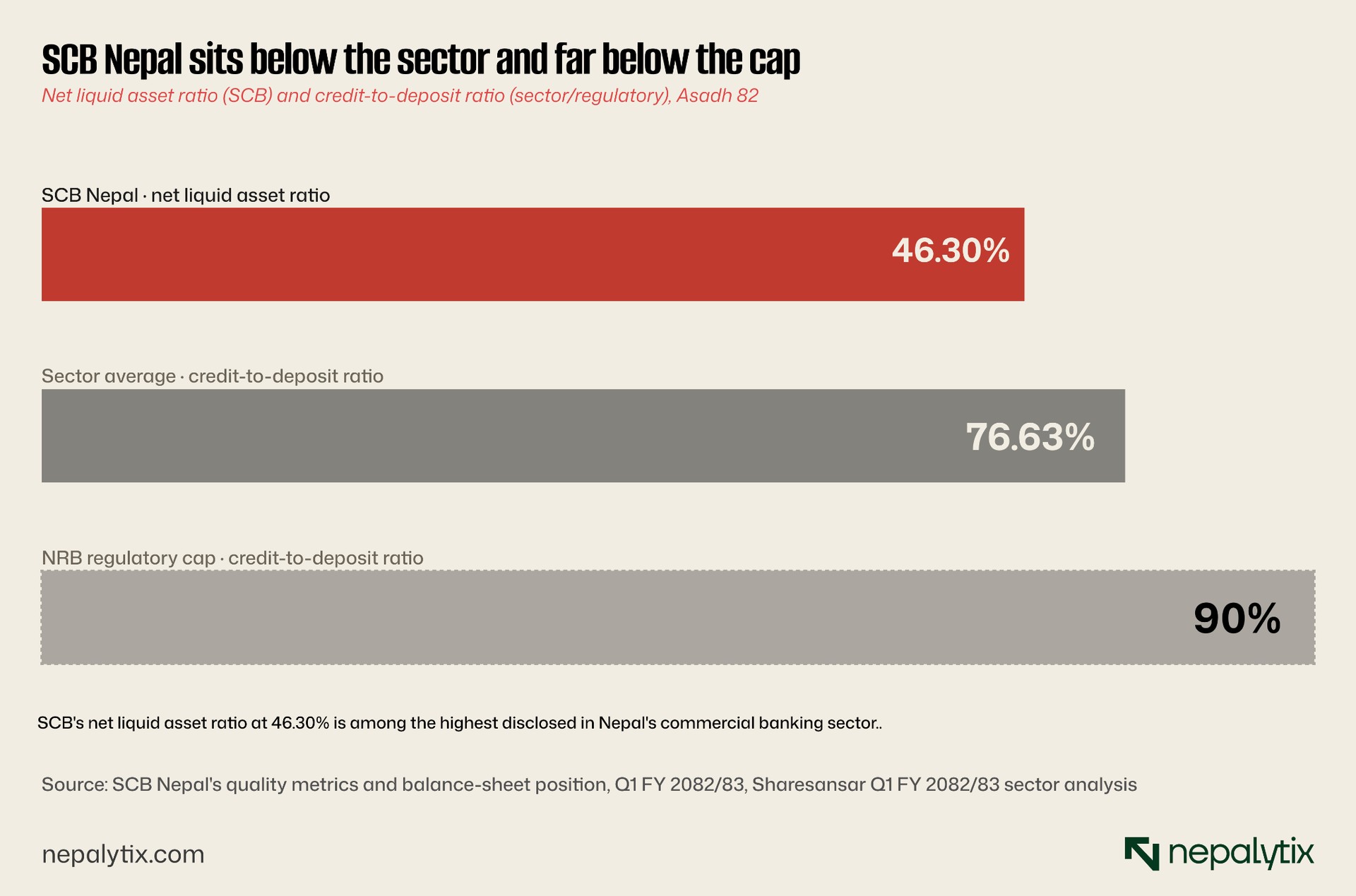

The pattern visible in the headline earnings number resolves once the supporting metrics are read alongside it. SCB Nepal at the close of FY 2081/82 disclosed return on equity of 14.41 percent, return on assets of 1.95 percent, and a non-performing loan ratio that had improved to 1.47 percent from 2.14 percent the previous year. Provisioning coverage strengthened to 160.08 percent, meaning the bank holds Rs 1.60 in reserves for every Rs 1 of impaired loan, well above the regulatory minimum. Cost of funds fell to 3.22 percent from 3.84 percent. The base rate fell to 4.99 percent. Net liquid asset ratio rose to 46.30 percent.

Where the deposits actually go

SCB Nepal's net liquid asset ratio of 46.30 percent at FY 2081/82 close is unusual by any standard. The figure represents nearly half of the bank's deposit base parked in cash and government securities rather than deployed as loans, an opportunity cost the bank has chosen to bear in exchange for a fortress liquidity position. Its credit-to-deposit ratio at the FY-end disclosure was substantially below the sector average of 76.63 percent and well below the regulatory cap of 90 percent.

This is the operational expression of the strategy. SCB Nepal does not deploy its deposit base into the sector-average book of corporate term loans, real-estate exposures, and consumer credit. It deploys some of its book into a smaller, more selective set of corporate and trade-finance relationships, and parks the rest in government securities and cash. The result is a bank that is structurally less profitable in any given year than a peer running the same balance sheet at higher utilisation and a bank that is structurally more resilient to any given credit cycle.

What the market pays for

NEPSE's pricing of the sector reflects the divergence. Through the most recent quarter, banks with strong earnings and clean books trade at modest multiples of those earnings; Prime Commercial at 8.97 times, Kumari at 11.26 times. NIC Asia, having reported Q4 FY 2081/82 EPS of Rs 1.08, a 92 percent year-on-year collapse driven by impairments trades at multiples that have effectively decoupled from current earnings. SCB Nepal sits in a third category: high-quality earnings, modest absolute size, and a valuation that reflects the consistency rather than the growth.

The strategy in one number

Standard Chartered Group's RoTE trajectory from 2015 onward is the single number that explains the parent's posture. The bank that arrived at -0.4 percent RoTE in 2015 has reached 14.7 percent in 2025, a recovery built almost entirely on cutting unprofitable exposures rather than growing profitable ones. The shape of that curve is slow then accelerating after April 2022, is the most important fact about Standard Chartered as an institution. The discipline that produced it is the same discipline visible in the Nepal subsidiary's quarterly disclosures.

SCB Nepal is not failing. It is also not, in the way Nepali banking culture defines the word, succeeding. It is not gaining market share. It is not opening branches. It is not adding deposits. It is doing what Standard Chartered has spent a decade learning to do: stay small, stay disciplined, hold the highest capital cushion in the market, accept the lowest cost of funds in exchange for the slowest growth, and let scale be someone else's problem.

For Nepali shareholders holding the 29.79 percent public float, this has been a stable position. The bank pays consistent dividends, most recently a 19 percent cash dividend for FY 2081/82, declared at the 39th AGM in late 2025. It does not require capital injections. It does not surprise on the downside. It is, in the literal sense, boring. In a sector where Himalayan, Kumari, NIC Asia, and Citizens have produced large negative surprises in the past two years, that boredom carries valuation.

The interesting question is not whether the strategy is working. The numbers say it is. The interesting question is how long London continues to find Nepal worth keeping in the portfolio at all.

Standard Chartered Group, having sold out of seven markets and thousands of corporate clients to fund 14.7 percent return on tangible equity, will at some point ask the same question of every remaining subsidiary. The answer might be that Nepal continues to clear the hurdle. The answer might be that, when the next round of group portfolio review concludes, a small Nepali bank with the highest capital adequacy and the lowest cost of funds in the country is exactly the kind of asset that fetches a clean buyer at a clean price. Either way the SCB Nepal that remains is a bank executing the only strategy that ever made sense for it and the local market increasingly is starting to recognise the discipline behind the smaller numbers.