What Three Bank Issues Reveal About Nepal's Capital Markets

Three major Nepali banks issued perpetual preference shares at the same 8.25% coupon within a single quarter.

Three commercial banks priced perpetual preference shares at the same 8.25% coupon within a quarter. Three more are pricing between 8% and 9%. The cluster is the loudest signal banking equity has sent in two years.

The Signal

When the upper tier of Nepali commercial banking issues perpetual paper at 8.25% rather than common equity at depressed valuations, the market is telling you two things at once. One, bank equity is too cheap to issue against. Two, the institutional buyer base has finally deepened enough to absorb hybrid securities at scale. The first is a bearish read on banking stocks. The second is a structural milestone for NEPSE.

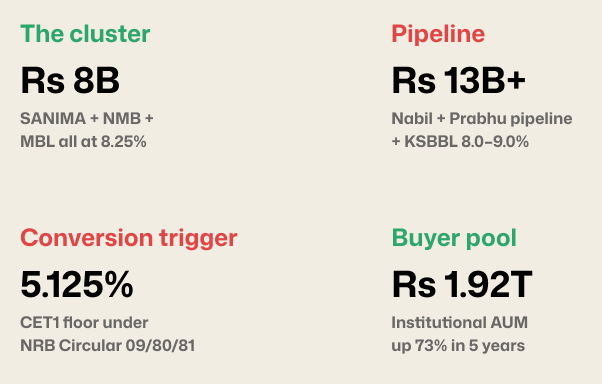

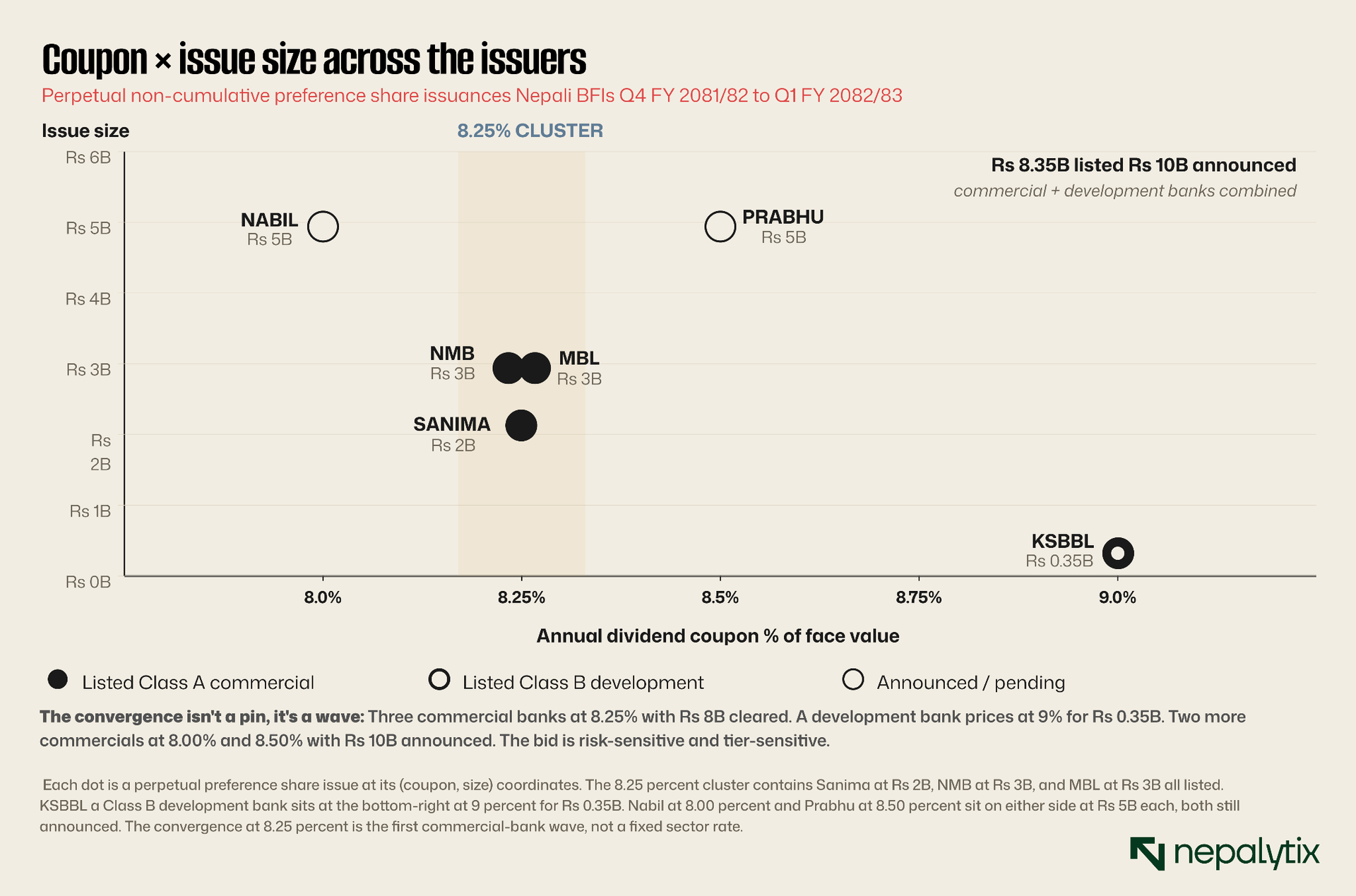

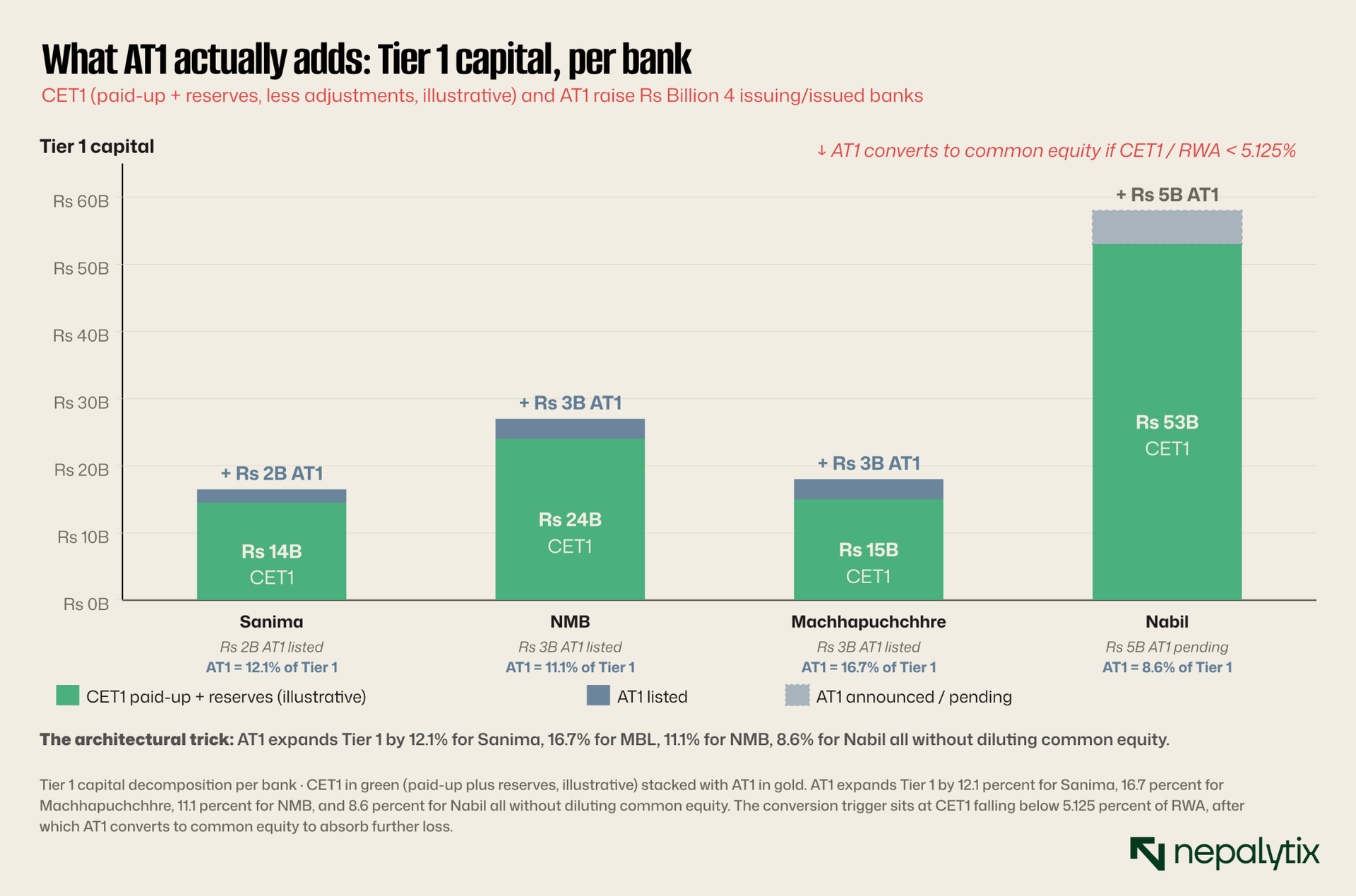

Sanima Bank Limited listed its perpetual non-cumulative preference shares on NEPSE in late May 2026. The ticker is SANIMAPNP. Twenty million units at a face value of Rs 100, paying an 8.25 percent dividend when the bank is profitable, no redemption date, institutional investors only. Total issue size: Rs 2 billion. Within weeks, NMB Bank's listing for NMBPNP was scheduled on the NEPSE main page at the same 8.25 percent coupon and a Rs 3 billion issue. Machhapuchchhre Bank's MBLPNP SEBON approval granted on Falgun 04, 2082 followed at the same 8.25 percent for Rs 3 billion.

Three commercial banks. Same instrument. Same coupon. Same quarter. What gets less attention is what is underneath it. Kamana Sewa Bikas Bank KSBBL, a Class B development bank listed its own perpetual preference share on April 6, 2026 at 9 percent Rs 350 million, 3.5 million units. Prabhu Bank's board approved Rs 5 billion at 8.5 percent on Chaitra 27, 2082 pending SGM and NRB clearance. Nabil Bank has proposed Rs 5 billion at 8 percent, awaiting regulatory approval. Six BFIs across three coupon tiers in the same eight-month window. The convergence at 8.25 percent is not a sector pin. It is the opening bid.

The event: Three banks, one coupon, one quarter The point worth landing first is that this did not happen by coincidence. Nepal Rastra Bank opened the door in June 2024 with Circular 09/80/81 which permitted commercial banks and national-level development banks under the Capital Adequacy Framework 2015 to issue Perpetual Non-Cumulative Preference Shares as a way to ease primary capital position and meet Basel III Tier 1 requirements. The circular set out twelve conditions, the most important of which is that the instrument has no fixed maturity, must be held by institutional investors only, pays dividends only out of current-year profit, and converts to common equity if the bank's CET1 falls below 5.125 percent of risk-weighted assets.

The framework was created in June 2024. The first listings came in late May 2026 roughly twenty-three months later. That is the lag between a regulator opening a window and the market actually walking through it. For most of those twenty-three months, banks were figuring out the prospectus mechanics, the institutional buyer mechanics, and the pricing.

What you are looking at is the convergence point of a first wave. Three banks that were positioned similarly in the capital-stack sense, upper-tier commercial, mid-range capital adequacy, and similar growth ambitions all priced their AT1 instruments at the same coupon. That tells you these were either coordinated implicitly through a shared institutional buyer pool, or coordinated explicitly through informal benchmarking against the first approved issue. SEBON's role in this matters: the first approval anchors the market. Once SANIMAPNP cleared at 8.25 percent, subsequent issuers had a precedent to match.

Why 8.25%: The institutional anchor, not a regulatory pin

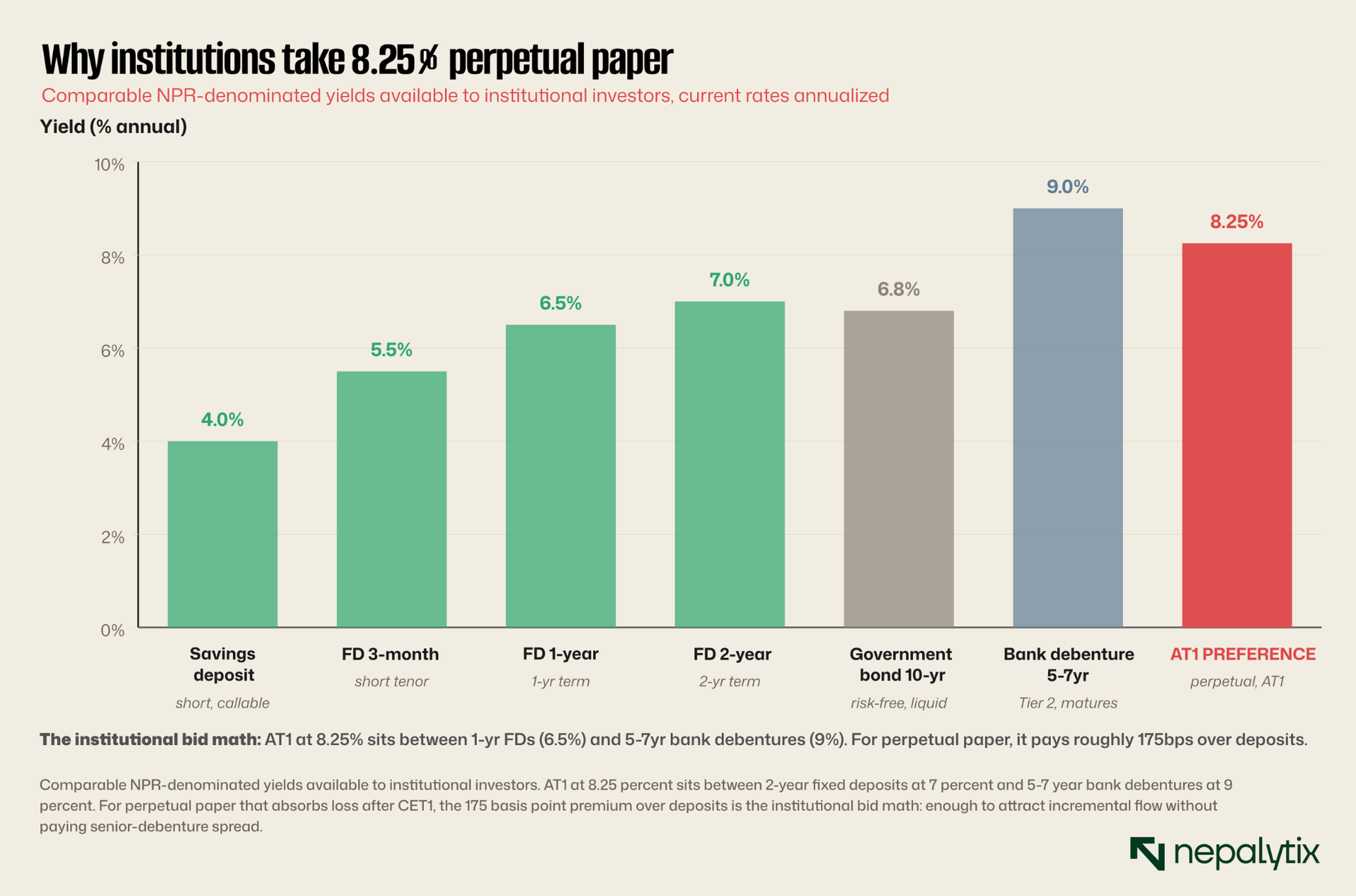

The first instinct on seeing three identical coupons is to assume regulatory direction. That is wrong. NRB did not set a price. Circular 09/80/81 sets conditions on the instrument structure but no coupon. SEBON approves issues but does not price them. The 8.25 percent number came from somewhere else: from the institutional buyer pool's willingness to absorb perpetual paper at that yield and from the issuing banks' willingness to pay it.

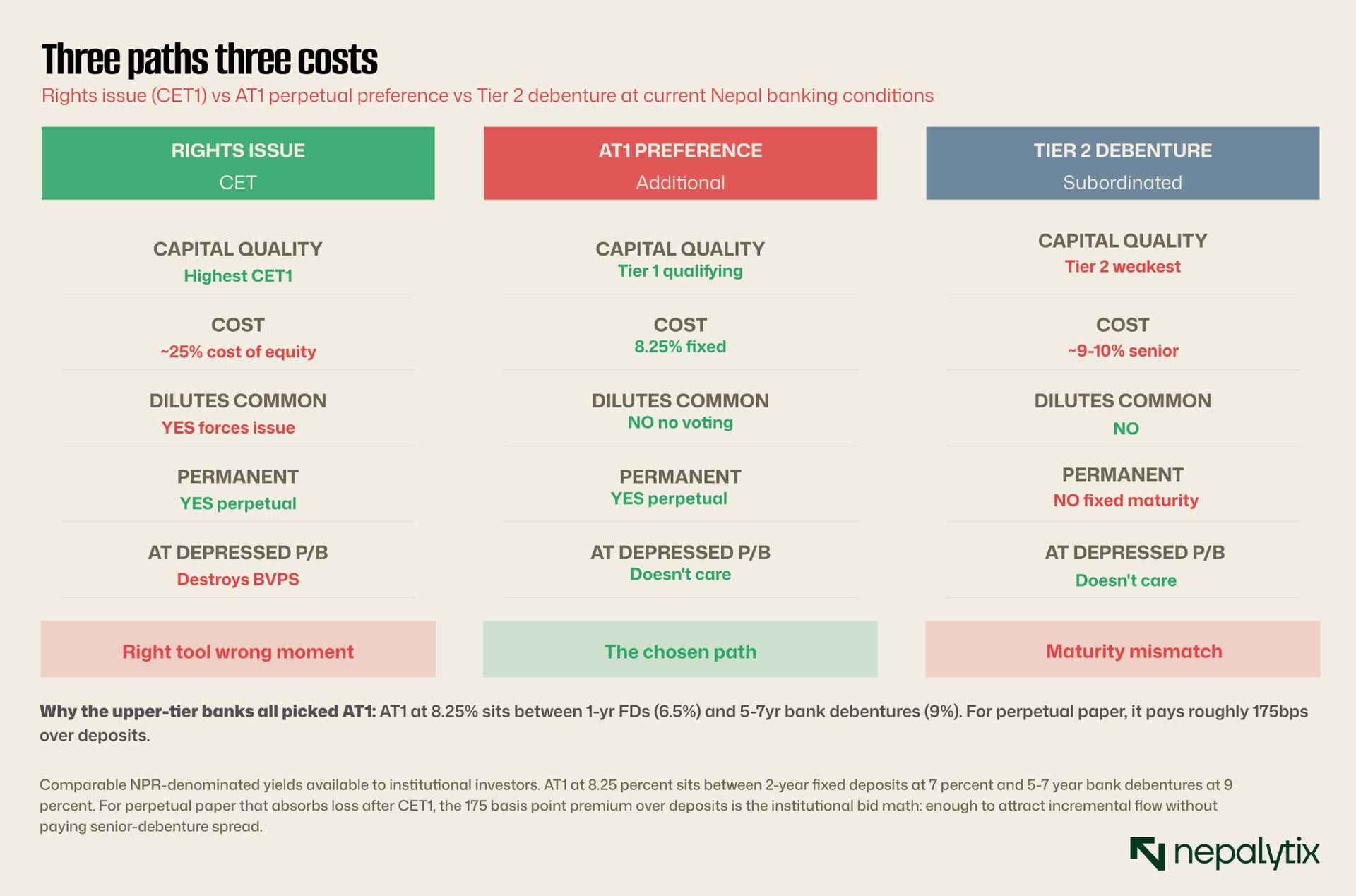

The institutional pool's math is straightforward. Institutional fixed deposit rates sit between roughly 4 and 7 percent depending on tenor. A 10-year government bond yields around 6.8 percent. A 5–7 year listed bank debenture pays around 9 percent. AT1 at 8.25 percent sits between the 2-year FD and the senior debenture roughly 175 basis points over comparable FDs but for perpetual paper that absorbs first loss after CET1.

The banks' math is equally direct. Current cost of equity for a Nepali commercial bank computed against book value at current NEPSE valuations sits in the high teens to mid-twenties. AT1 at 8.25 percent is dramatically cheaper than CET1 in cost-of-capital terms even after adjusting for loss-absorbing features. The math is overwhelming.

The three banks landed at the same number because the calculation produces the same number. The institutional pool wanted at least 175 basis points over deposits to take on perpetual loss-absorbing paper. The issuing banks would pay anything up to roughly 10 percent before AT1 stops being meaningfully cheaper than debenture-plus-equity-mix. The 8.25 percent number is in the middle of that band and happens to round to a quarter point, easy to communicate, easy to compare, easy to anchor.

The deviation from 8.25 is the more interesting story. KSBBL at 9.0 percent prices wider because it's a smaller Class B development bank, different credit profile, different buyer expectations, and a much smaller issue at Rs 350M. Prabhu at 8.5 sits between commercial-bank cluster and development-bank pricing. Nabil at 8.0 proposed, awaiting clearance prices through the commercial-bank cluster, which would be unusual unless its name and balance-sheet strength let it command a premium yield-curve position when it finally comes to market.

The architecture: What AT1 actually is and why NRB cleared it

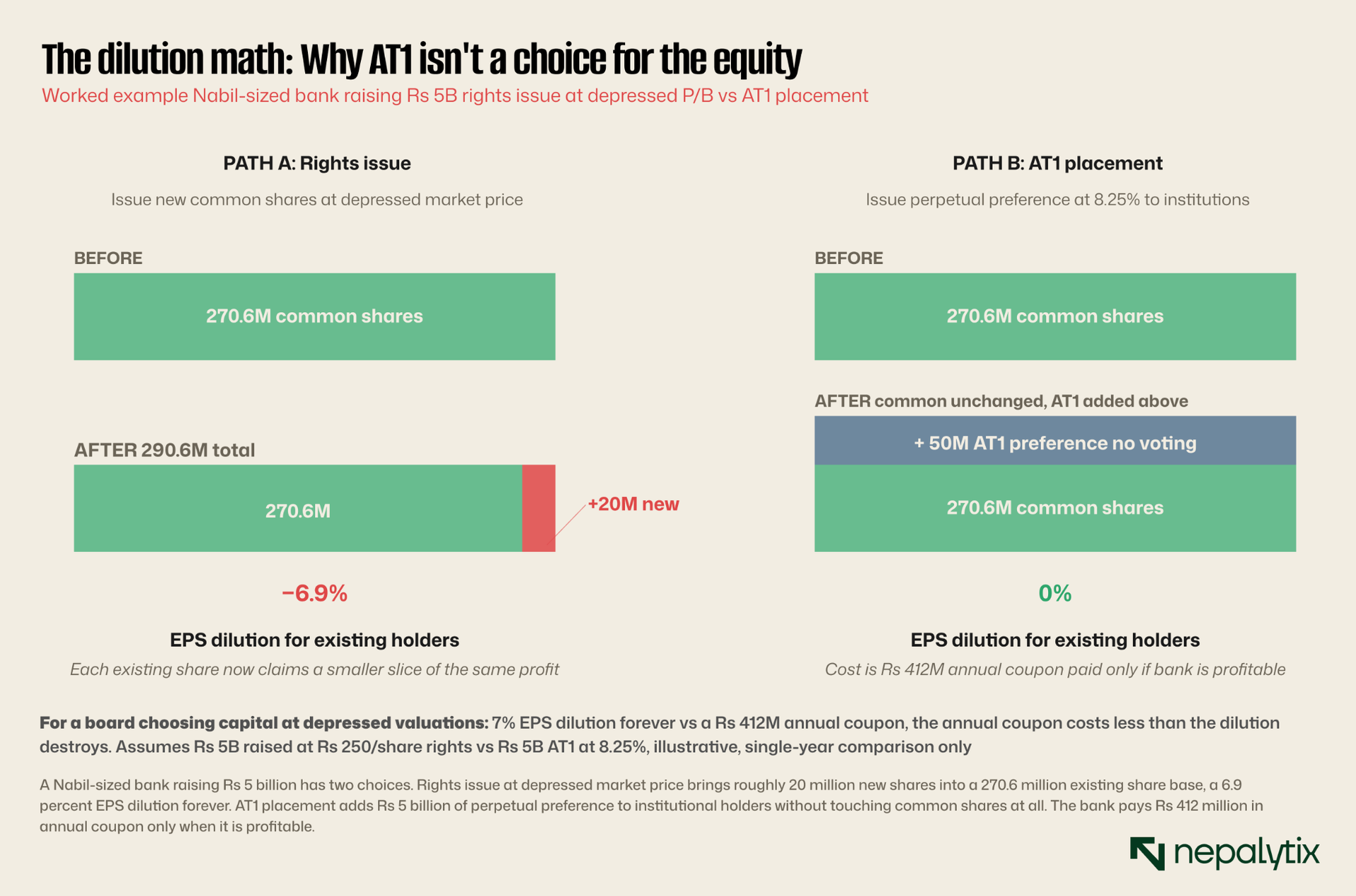

To understand what the cluster signals, you have to understand what AT1 is and is not. AT1 is not debt. AT1 is not common equity. AT1 is a hybrid security designed under Basel III to sit between the two providing loss-absorbing capacity without forcing equity dilution. The mechanics are precise. AT1 pays a coupon not interest. The bank pays only out of current-year profit never out of retained earnings. If the bank is in loss for a given year, the coupon is skipped and does not accumulate. Holders have no recourse. They cannot force redemption. They cannot vote. They cannot sue for unpaid dividends.

The conversion trigger is the loss-absorbing mechanism. Under NRB Circular 09/80/81, if the issuing bank's CET1 ratio falls below 5.125 percent of risk-weighted assets, the AT1 instrument must convert to common equity. The conversion is when permanent holders become ordinary shareholders. This is the structural feature that makes AT1 qualify as Tier 1 capital under Basel III rather than as Tier 2. The instrument absorbs loss before the bank approaches insolvency, the way common equity does, just without immediately diluting existing common shareholders the way a rights issue would.

NRB cleared the instrument because the sector needed a broader menu of qualifying capital instruments. Rights issues dilute. FPOs require a market price strong enough to issue without destroying book value per share. Debentures are Tier 2 only; they help with total CAR but not with the CET1 or Tier 1 ratios that the regulator weights most heavily. AT1 fills a specific hole: Tier 1 capital that does not dilute and does not require strong equity market conditions to issue.

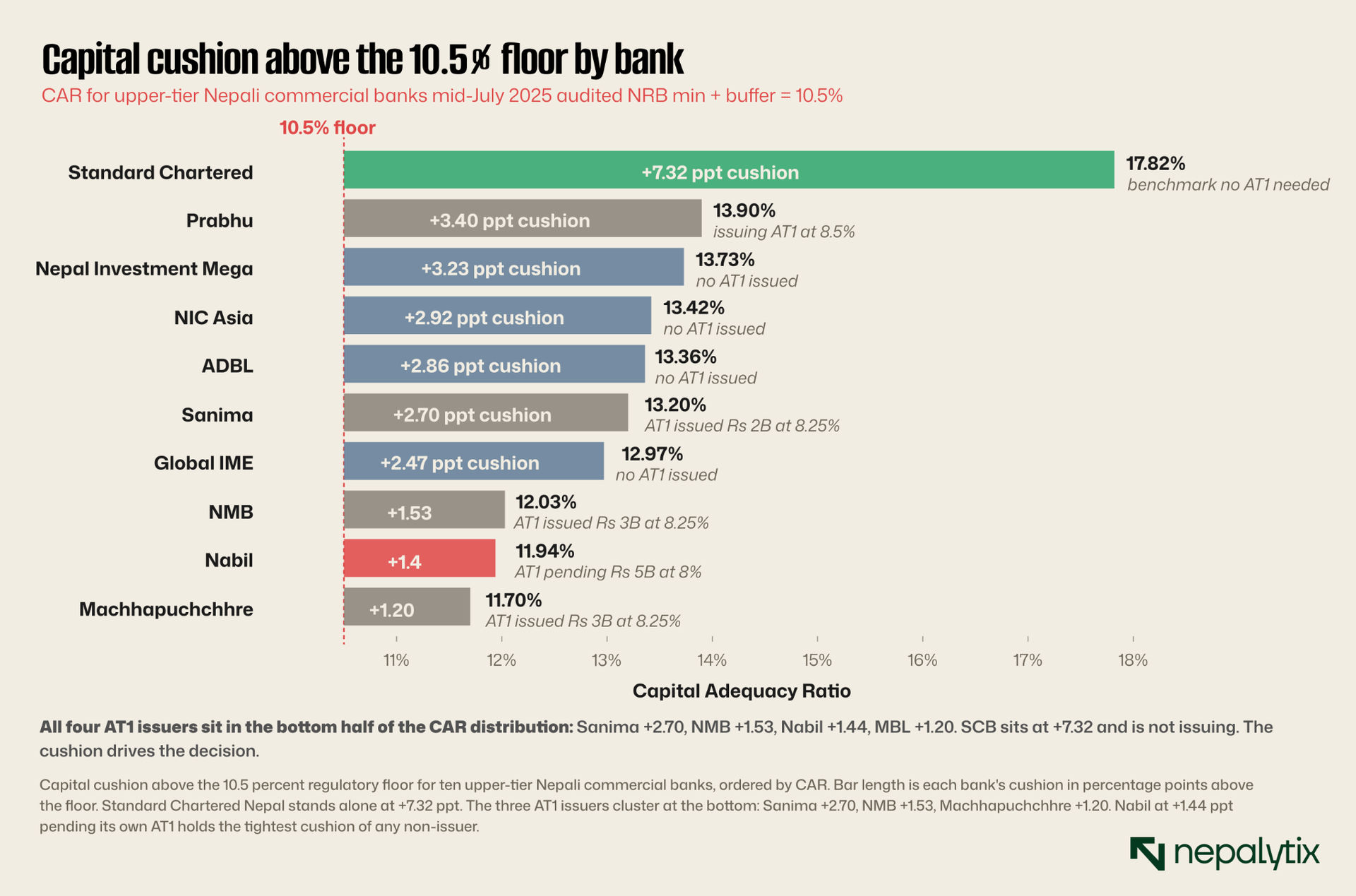

Why now: Capital cushions compressing across the upper tier The question of why this is happening now answers itself when you look at the capital ratios of the issuing banks. Sanima's CAR has drifted from 13.51 percent in FY 2079/80 to 13.20 percent in FY 2081/82. NMB has gone from 12.30 percent to 12.03 percent. Machhapuchchhre, the smallest of the three issuers, has slipped from 12.00 percent to 11.70 percent. All three sit in a band that is uncomfortably close to the 10.5 percent minimum-plus-conservation-buffer threshold that triggers regulatory restrictions on dividends and capital actions.

Standard Chartered Nepal is the outlier with 17.82 percent CAR over seven percentage points above the floor. SCB does not need AT1 and is not issuing AT1. The three AT1 issuers sit between 11.70 and 13.20 percent with buffers between 1.20 and 2.70 percentage points. One bad year NFRS 9 transition provisioning, rising NPL costs, credit growth outpacing capital generation and they would be in regulatory territory where dividends get blocked.

Nabil's position is the most instructive. At 11.94 percent CAR, Nabil sits 1.44 percentage points above the floor, the tightest cushion of any non-issuer. The bank has announced a Rs 5 billion AT1 proposal at 8.0 percent pending NRB clearance. Same situation the three issuers were in six months ago: thin cushion, options narrowing, AT1 as the path of least resistance. The proposed 8 percent coupon below the 8.25 cluster — suggests Nabil's franchise commands a yield-curve premium when it comes to market.

The reason this is happening now and not two years ago is that the cushion has actually compressed in the meantime. NFRS 9 implementation has crunched capital across the sector through expected-credit-loss provisioning that runs alongside the traditional NRB classification. Sector NPLs have climbed to 4.44 to 4.62 percent. Credit-to-GDP at 91.31 percent indicates Nepal's banks are running close to maximum useful leverage at current macro conditions. The combination is a CAR squeeze that did not exist when the AT1 framework was first published.

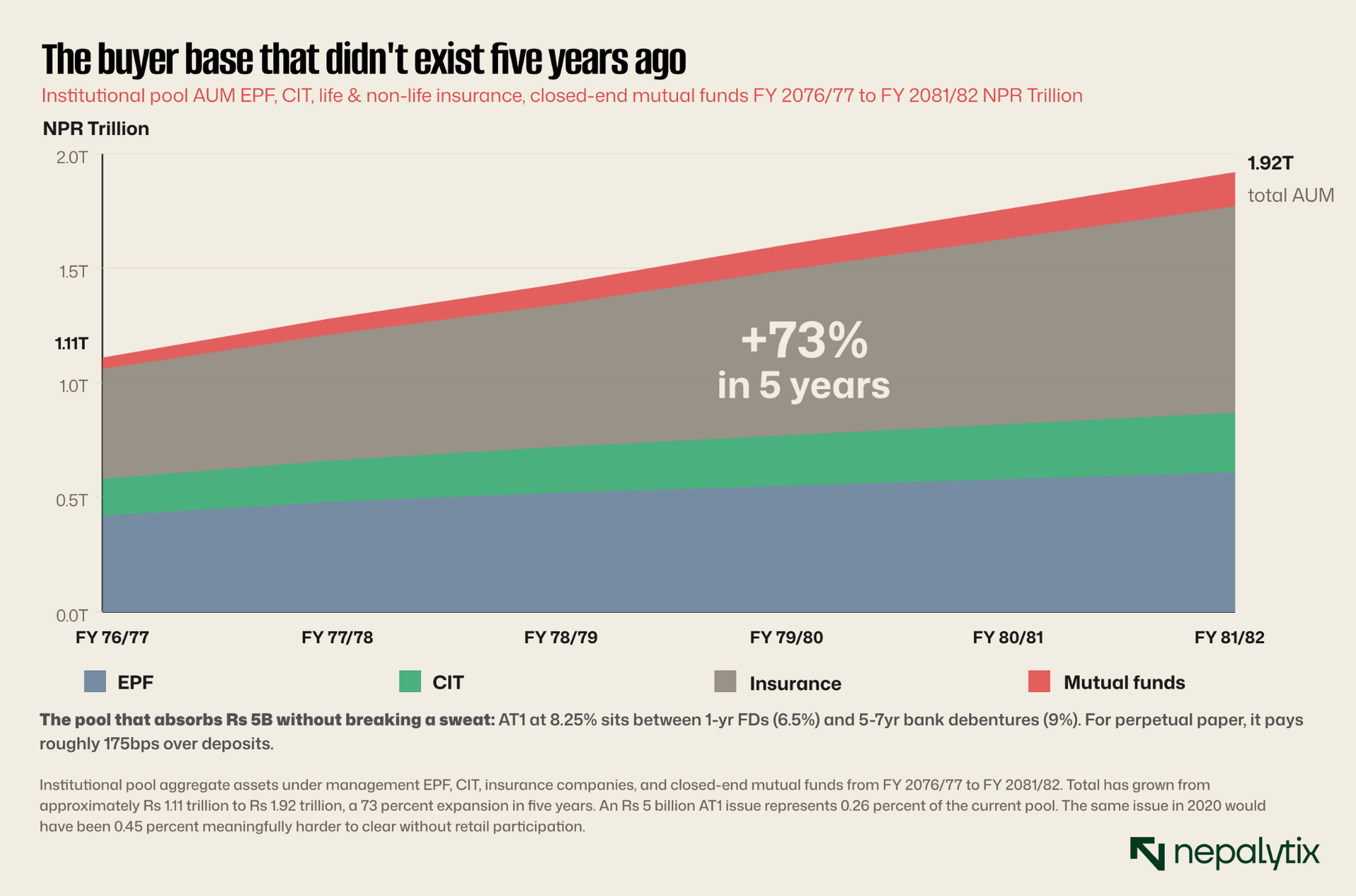

Who is buying: The Rs 1.9T pool that didn't exist five years ago The other half of the cluster's story is the buyer base. AT1 is restricted to institutional investors. That restriction makes the issue clearable only if the institutional pool is deep enough to absorb the size. Five years ago, the pool was not.

The four pillars of institutional capital in Nepal are the Employees Provident Fund, Citizen Investment Trust, the insurance sector (life and non-life combined), and the closed-end mutual fund industry managed by bank-affiliated capital companies. EPF alone runs approximately Rs 610 billion in invested assets. CIT adds another Rs 260 billion. The insurance sector: Nepal Life, Rastriya Beema, Citizen Life, and a dozen smaller companies collectively manage around Rs 900 billion. Closed-end mutual funds run by the various Capital Limited subsidiaries (NMB Capital, Nabil Invest, Sanima Capital, Prabhu Capital, Citizens Capital) control roughly Rs 150 billion. Total: roughly Rs 1.92 trillion.

The relevant comparison is five years ago: the same pool was approximately Rs 1.11 trillion. The pool has expanded by 73 percent in five years, driven primarily by life insurance premium growth and EPF inflows from a rising formal-sector workforce.

The pool's structure makes it a natural buyer for AT1. Each of the four components has long-duration NPR-denominated liabilities, pension promises, life insurance payouts, mutual fund mandates that need long-duration NPR-denominated assets to match. The traditional menu in Nepal has been fixed deposits (short, reprice with rate cycles), government bonds (limited float, mostly held by banks for SLR), and equities (volatile, hard to size for matching purposes). AT1 fills a gap that the institutional pool has been quietly asking for.

That Rs 5 billion can clear at 0.26 percent of the institutional pool size is the structural change. Five years ago, the same issue at 0.45 percent of the pool would have required retail participation, which would have changed the regulatory treatment and the price. Today it does not. The institutional pool can absorb the issue without surfacing in any retail tradeable form.

Two readings: Bearish on bank equity, bullish on market evolution

What does the cluster mean for the rest of NEPSE banking? Two readings, both with honest weight.

The bearish read on bank equity is direct. When the issuers choose AT1 over common equity at this price level, they are telling you they do not believe their own equity is fairly priced for capital raising. CET1 is the strongest form of regulatory capital — it is what regulators want banks to have more of. Issuing AT1 instead of CET1 means the issuer accepts a worse capital instrument because the equity route would destroy book value per share.

The implication is sector-wide. If Nabil at 11.94 percent CAR cannot issue equity without destroying value, then no commercial bank below 13 percent CAR can. That includes NMB, Machhapuchchhre, Citizens, Prabhu, Global IME, and Nepal Bank roughly half the sector. The equity-issuance channel is functionally closed for those banks until NEPSE banking valuations recover or capital cushions expand through retained earnings.

The bullish read on market evolution is the other side of the same coin. The cluster represents the first time Nepal has successfully placed hybrid securities at institutional scale across multiple issuers in a coordinated window. The plumbing now exists, the buyer base is real, and the pricing has been established. That is a structural milestone, the kind of plumbing-deepening that has to happen before a frontier capital market matures. The next step is whether the same plumbing extends beyond bank AT1 to corporate hybrid issuance. The cluster is the precondition.

What to watch: Five tells in the next two quarters Five specific things to monitor will tell you whether the cluster was a one-time Basel III adaptation or the start of a structural shift.

First, the next AT1 coupon. If Nabil clears at 8.0 percent, the institutional bid is tightening and the cluster expands. If Nabil has to widen to 8.25 or higher, then 8.25 was the floor and KSBBL's 9 percent was the development-bank early warning. Watch Nabil's placement carefully.

Second, the secondary market for the listed AT1s. SANIMAPNP, NMBPNP, and MBLPNP are tradeable on NEPSE between institutional holders only. If institutional holders rotate among themselves at observable prices, AT1 becomes a real asset class with mark-to-market pricing. If quotes stay stale, AT1 stays a private placement market that just happens to list.

Third, the first non-bank issuance. Insurance companies, hydropower developers, and trading conglomerates could in principle issue hybrid paper to the same pool. If any does within two quarters, that is the phase-3 marker Nepal moves from a bank-only hybrid market to a corporate hybrid market.

Fourth, NRB's response. The regulator opened the door in June 2024 and has been silent on the cluster since. Clarifying guidance, tighter disclosure, or signalling discomfort at 8.25 percent would age the cluster quickly. Continued hands-off lets it expand.

Fifth and the one that matters most NEPSE banking equity performance. If the banking sub-index recovers 25 percent or more in the next four quarters, the equity-issuance channel reopens for the upper tier and AT1 becomes optional. If the sub-index stays depressed, AT1 becomes the only path and the cluster keeps expanding.

The first reading is the consensus view. The second is the under-priced one. For two years, the question for Nepali bank investors has been whether earnings would recover faster than NPLs deteriorated. That question has not gone away. A new question has been added: how is the bank funding its own capital base while it waits for earnings recovery? The answer, for at least three banks, is now public. For three more, the answer is coming.

The cluster is the answer becoming public. Keep watching what gets priced next.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.