The Broker is the Risk

The Bhrikuti Stock Broking scandal is more than a case of broker fraud—it exposes deep structural flaws in Nepal's capital market.

A NEPSE broker has been suspended for taking no margin, mixing up client money and letting one favoured client run billions of rupees of credit with no settlement date. The market is filing it under one bad apple. It is the wrong file. What Bhrikuti exposed is not a rogue firm but a rotten join in the market's plumbing, the point where your cash sits, unprotected, every single time you trade. The fraud is the symptom. The plumbing is the story.

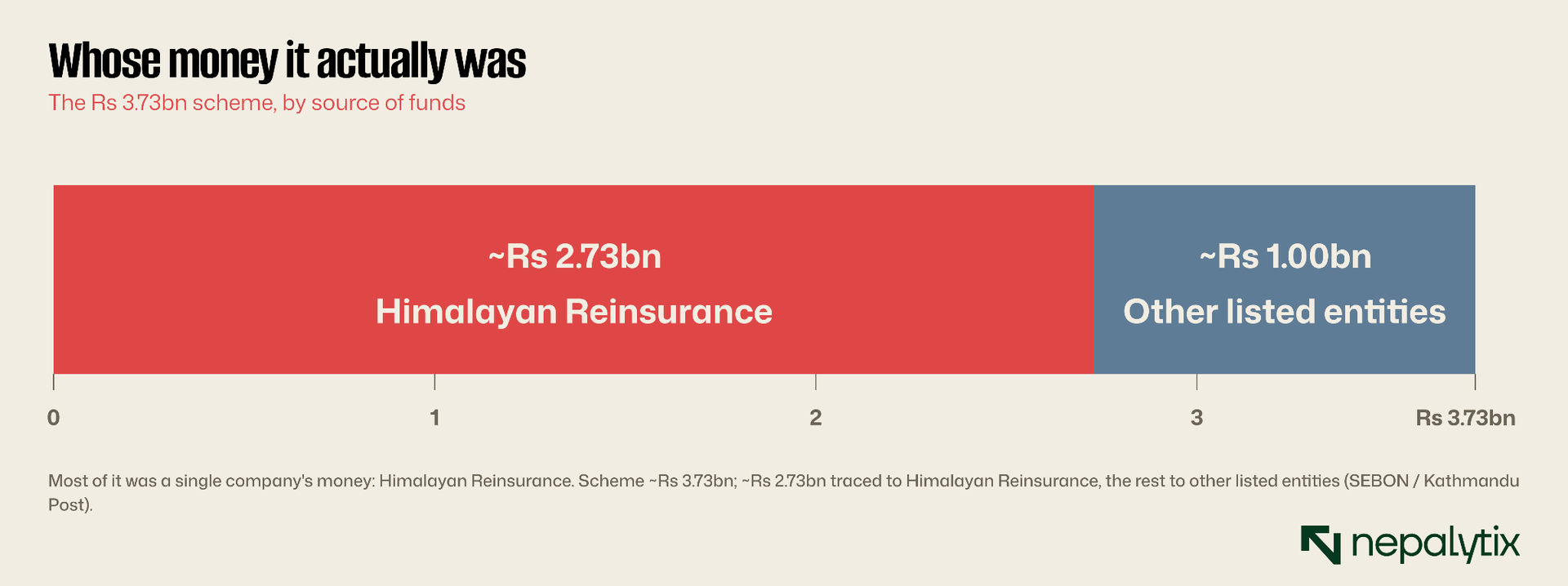

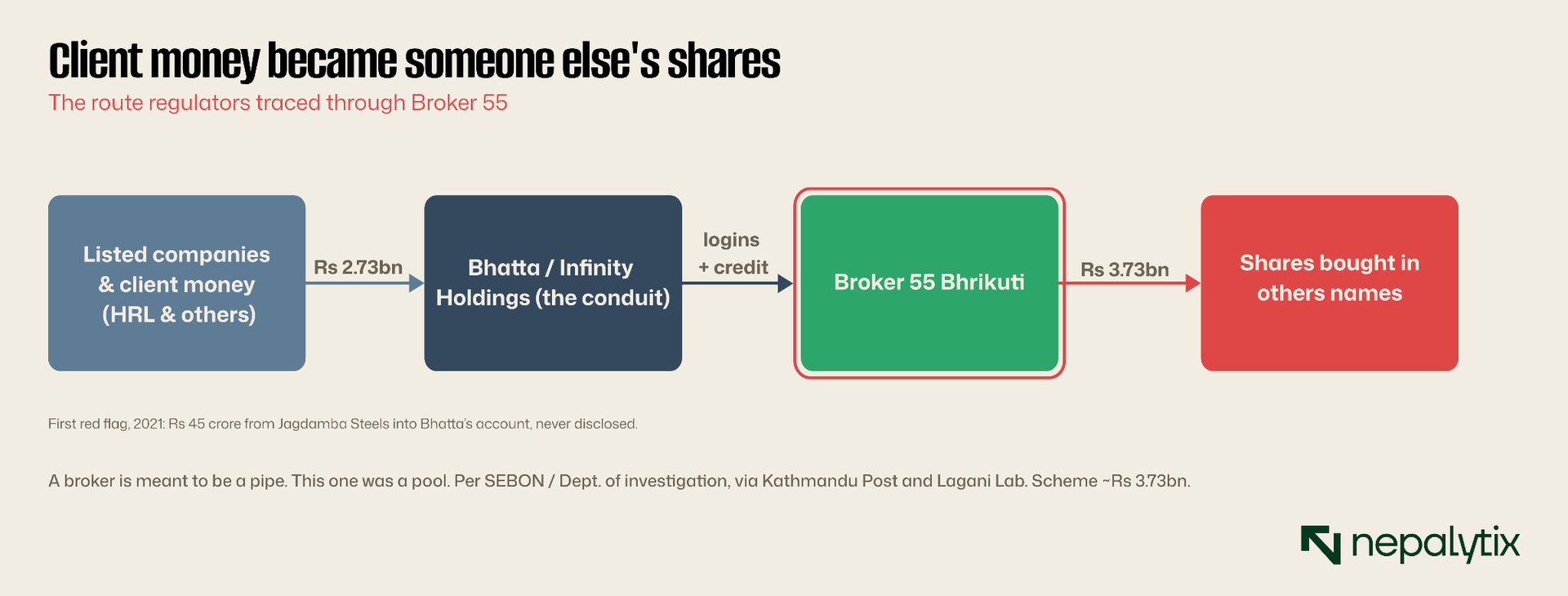

Start with the broker because the broker is where it broke. In early April, NEPSE and the Securities Board suspended Bhrikuti Stock Broking number 55 among the country's brokers in business since 2008. Then they tallied the damage: a scheme regulators size at around Rs 3.73bn in which shares were bought in the names of one businessman Deepak Bhatta and his circle using money that belonged to other people. The single largest slug, some Rs 2.73bn was drained from the share sales of one listed company, Himalayan Reinsurance and pushed through the broker into stock held in unrelated names.

The shape of it matters. This was not a broker skimming small sums from many clients over many years. It was one company's money, moved almost whole with a handful of other listed entities making up the rest. A theft that concentrates is not opportunism. It is design and design is what should worry a regulator because design repeats.

How does a broker let that happen? By switching off every check meant to stop it. Bhrikuti took no advance margin, though the rules demand at least a quarter up front. It commingled client money, the cardinal sin of using one company's cash to buy shares for another party and it settled nothing on time, running open-ended credit in place of the mandatory three-day cycle. Three rules exist to keep client money where it belongs. Any one of them would have stopped this. None were.

The most revealing line is the client's own defence. Bhatta says he had a margin-trading deal with the broker: credit now, reconcile later. The trouble is that no broker in Nepal is licensed to offer margin trading at all. His alibi describes a service that is itself illegal. That is the tell. This market runs quietly and routinely on arrangements that exist only in the dark.

When it finally unravelled, it did so almost domestically. By the accounts of the businessmen involved, the theft surfaced only when partners in a shared trading pool noticed money missing and cornered Bhatta at an emergency meeting to demand it back. Far too late. Himalayan Reinsurance has since sued the broker in the Kathmandu district court, the regulator has issued a show-cause notice, and the promoter at the centre of it sits in custody. A cosy arrangement between a broker and a favoured client ended in courtrooms and a cancelled licence.

And Bhrikuti was no fringe outfit. It was broker number 55 of ninety-two, a decade and a half old with offices across the country, the kind of ordinary licensed firm thousands of investors hand their savings to without a second thought. That is the unsettling part. This did not happen at the market's disreputable edge. It happened in the middle of it.

The biggest risk isn't the stock you buy

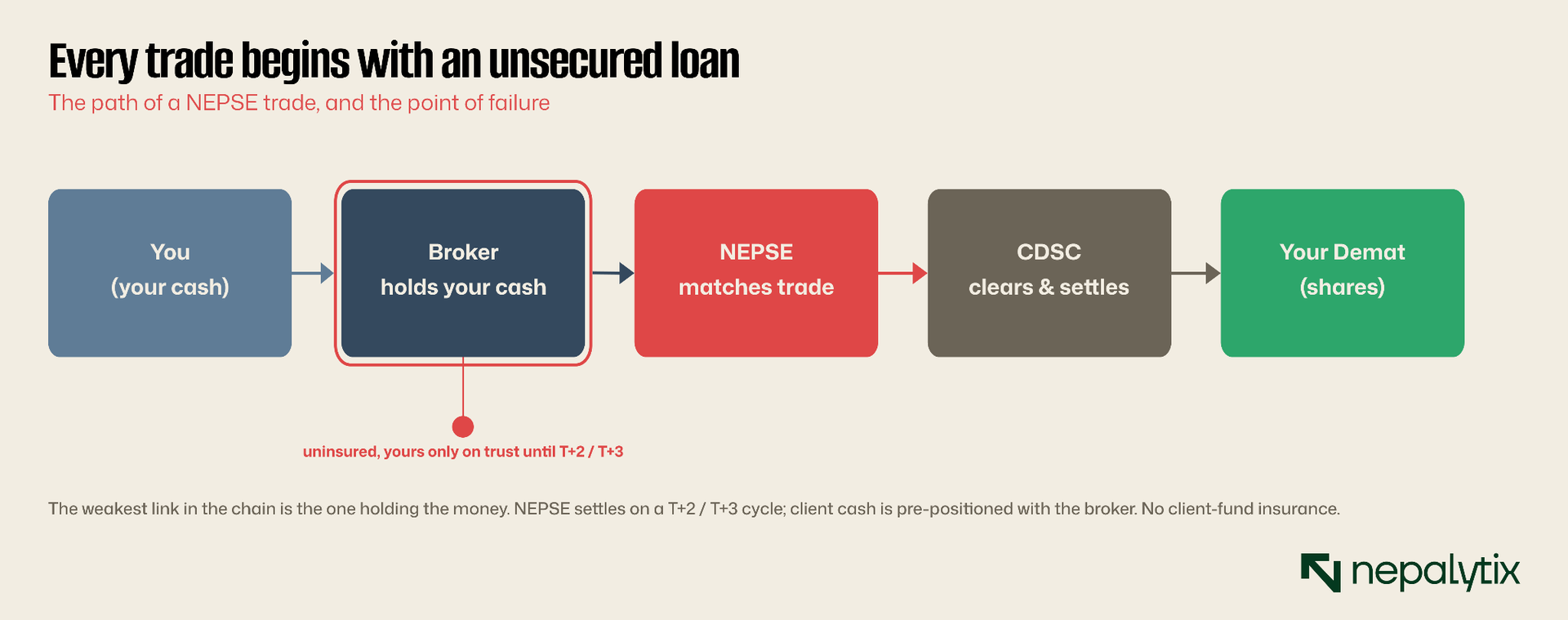

Here is the part most investors never think about and the part that turns one broker's fraud into everyone's problem. Every time you trade, you hand your cash to the broker first. The broker places the order, NEPSE matches it, the depository clears it and the whole thing settles two or three days later. For those days, your money and on a sale your shares, sit inside the broker.

So the broker is not a neutral pipe through which money flows untouched. It is a private company, of whatever size and character, holding your cash on trust and it is the flimsiest link in a chain whose other links, the exchange and the depository, are solid central institutions. The risk in the system is concentrated exactly where the supervision is thinnest. Strengthen the centre all you like; the system is only ever as safe as its weakest broker on its worst day.

And nothing stands behind it. There is no client-fund insurance in Nepal, no pool that quietly makes you whole if your broker loses or misuses your money. Trade on NEPSE and, for the length of every transaction, you are an unsecured creditor of your broker. You did not agree to that loan. You may not even know you have made it. Bhrikuti did not pick a lock; it walked through a door the system leaves open at all ninety-two brokers.

Other markets shut this door, which is proof it can be shut. In more developed systems client money sits in segregated accounts the broker legally cannot touch for its own ends, with an investor-protection scheme behind it to repay clients up to a limit if the firm fails. Nepal has neither in any robust form: segregation is more aspiration than enforced fact and the compensation scheme that would rescue a wronged investor does not exist. Bhrikuti is not a freak. It is what missing both safeguards eventually produces.

The rules failed before the broker did

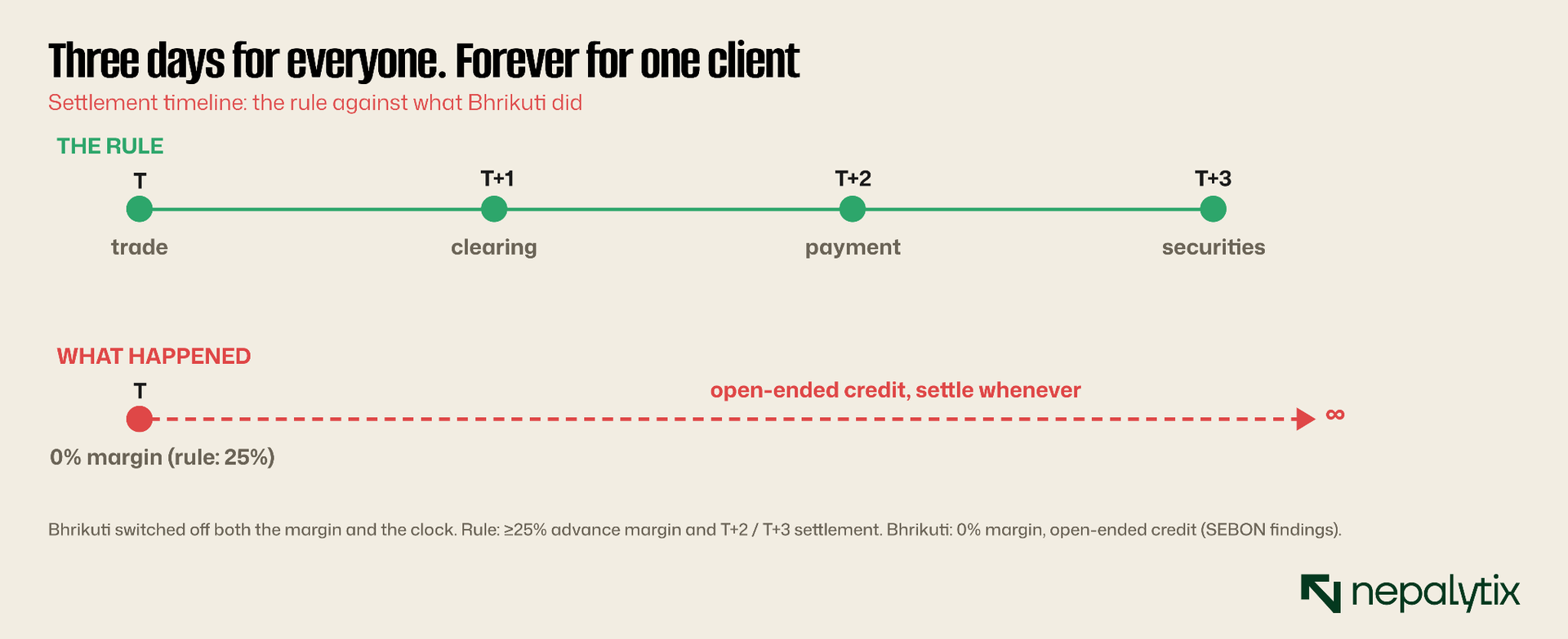

The rules Bhrikuti broke are not bureaucratic clutter. They are the safeguards themselves. The margin requirement, a quarter of the trade paid up front, exists so no one can buy what they cannot pay for and so a broker never ends up bankrolling a client's bets with other people's money. The three-day settlement clock exists so positions close fast, before exposure can pile up.

Bhrikuti disabled both. No margin, no settlement date just credit running off into the distance. In that moment the broker stopped being a broker and became an unlicensed lender, financing enormous share purchases on a handshake. And because every other protection assumes trades are paid for and settled on time, once those two safeguards fall, the whole control framework falls with them.

What makes this worse than a slip is that the missing piece, a legal margin regime, has never existed here. Investors want leverage; the regulator has never licensed it; so the demand gets met in the shadows by brokers extending credit they are neither allowed to give nor capitalised to lose. Ban the thing everyone wants instead of supervising it, and you do not kill it. You blind yourself to it. Bhrikuti is what blindness costs.

A supervised margin market would not be exotic. It would mean a licensed facility, leverage capped by rule, collateral held centrally rather than at a broker's discretion and margin calls triggered automatically instead of by relationship. Every ingredient already works in other markets; none of it operates here. The absence is a choice and Bhrikuti is the bill for making it. Markets do not get safer by accident; they get safer by rule and here the rule was never written.

The incentives all push the wrong way, too. A broker earns commission on turnover, so quietly financing a big client to trade more is, in the short run, good business. The client wants leverage and the legal market denies him. Both sides are tempted toward exactly what the rules forbid and little enforcement stands in the way. A market that outlaws a service everyone wants does not abolish it. It exports it to the one place no one is watching.

The losses spread far beyond one account

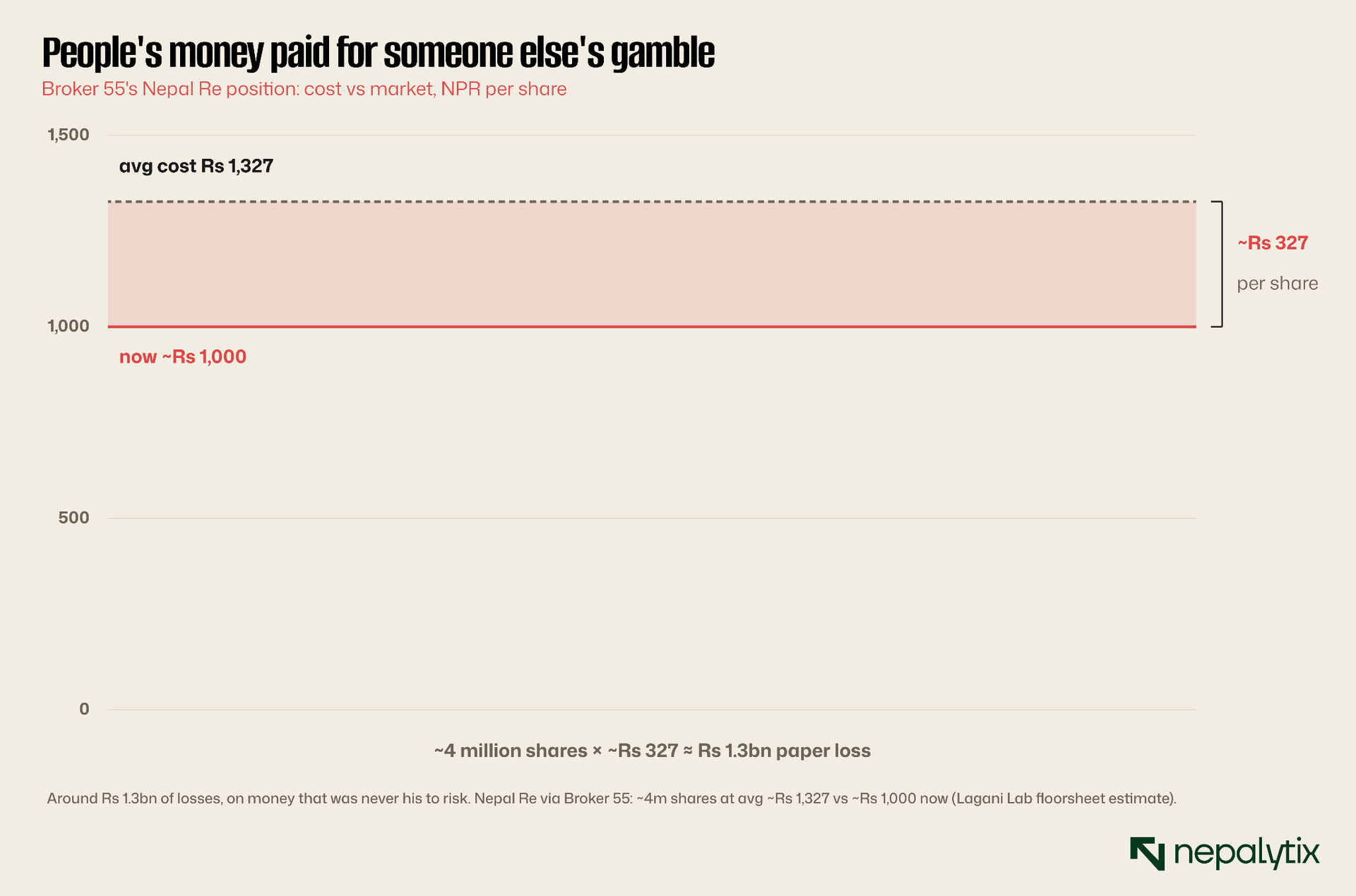

Follow the money one more step and the abstraction turns into a number. The stolen funds did not sit in an account; they bought shares, and the shares fell. Through Broker 55 roughly four million shares of Nepal Reinsurance were hoovered up at an average near Rs 1,327. The stock now trades around Rs 1,000. That is about Rs 1.3bn of losses, on money that was never the buyer's to gamble in the first place.

The wreckage did not stay inside the broker. Himalayan Reinsurance, the company whose money was used, was battered as the story broke, slammed to its ten-percent daily floor and leading the market's selling; its promoter is now jailed and its chairman has resigned. This is the part of broker risk that never appears in a valuation. When client money is misused on this scale, the share prices of the companies whose money it was taking the hit and ordinary shareholders who did nothing wrong help pay for it. The loss radiates outward in widening circles, and the outermost circle is full of people who never heard the broker's name.

Nor was Nepal Re the only name in the net. Funds and companies tied to the same circle, a large-cap mutual fund, a micro-insurer, a securities house, all surfaced in the investigation as sources or conduits of the money. One broker, one client and a web of listed entities whose balance sheets were quietly turned into a private trading account. The contagion here is not a theory. It is a list of tickers.

It is also why broker-flow data has quietly become one of the most watched signals in Nepal. When a single broker's account is seen amassing millions of shares of one stock at prices the fundamentals cannot justify, that pattern now reads as a warning rather than a curiosity. The trades that built the Bhrikuti position sat in the public floorsheet the whole time. Read after the fact, that floorsheet is a confession. Read in time, it is a warning the market is only now learning to heed.

When brokers fail, investors stand alone

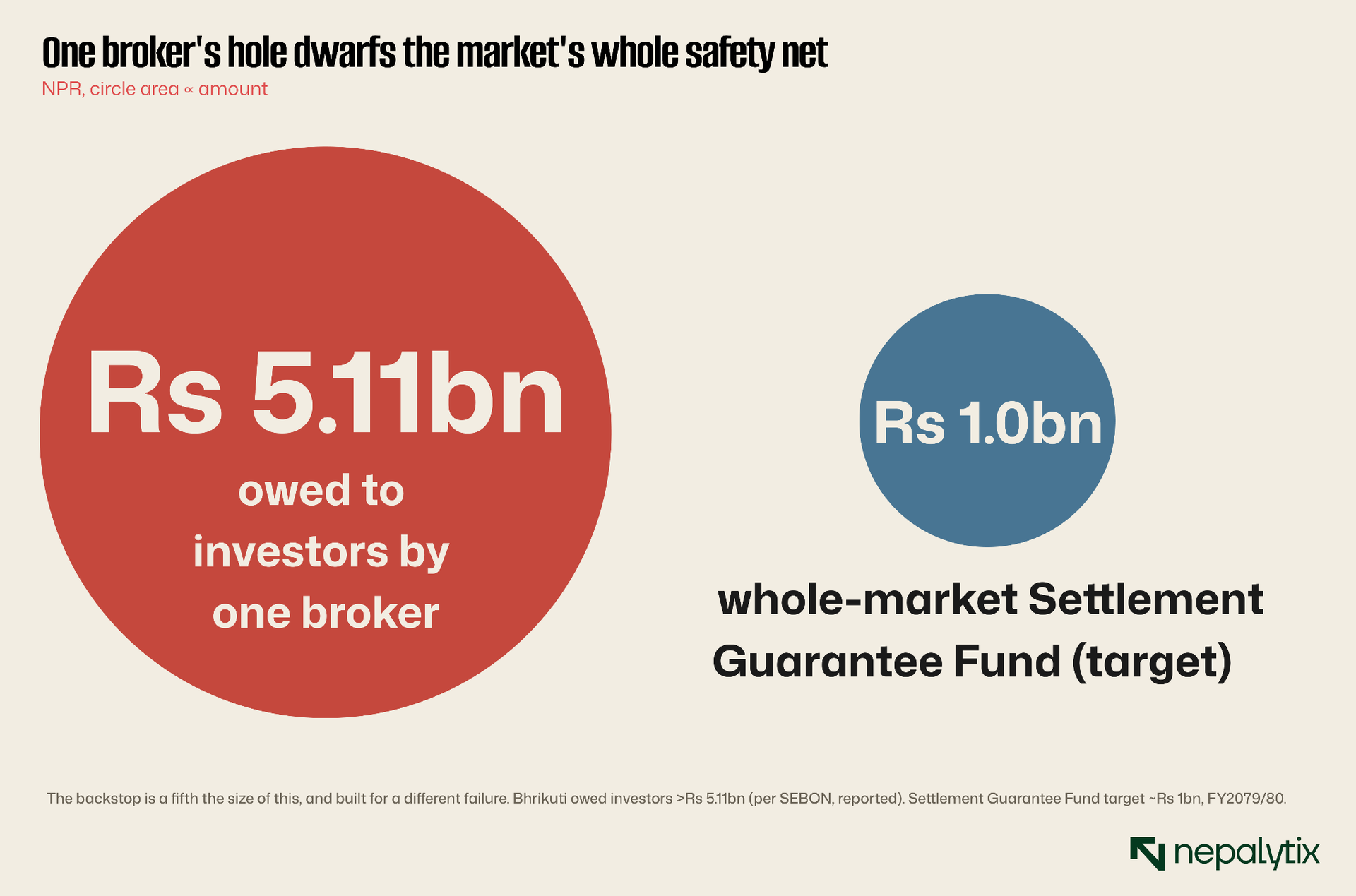

So what catches an investor when a broker falls? Almost nothing built for the job. NEPSE has spent years assembling a Settlement Guarantee Fund, with a target around Rs 1bn. But read what it is for: it covers settlement shortfalls, a buyer failing to pay a seller so honest counterparties are not left short. It was never meant to repay clients whose broker emptied their accounts. Right problem, wrong fund.

And even on its own terms it is tiny. That Rs 1bn target is one-fifth of the more than Rs 5.11bn Bhrikuti alone is reported to have owed investors. The market's whole pooled safety net is dwarfed by the hole at a single mid-tier broker and pointed at a different failure besides. A broader trade-guarantee fund and an auction procedure were still in draft as recently as last year.

And recovery for the investors actually out of pocket, is slow and uncertain. Their claim winds through the courts and a show-cause process, not through any fund that pays on demand. The money that was real enough to steal in a single morning becomes, in the getting back, a years-long maybe if it returns at all. Justice here is measured in fiscal years not trading days.

Set that against the market's shape: ninety-two licensed brokers, every one of them holding client cash with no client-fund insurance and no capital buffer sized to anything like this. For almost everyone, almost all the time none of this is visible. It becomes the only thing that matters on the single day a broker fails. And on that day, the discovery that the net was never built for this failure is not a footnote. It is the whole story.

The fund's origins give the game away. The regulator ordered it built back in 2021, after a wave of complaints from sellers paid late, funded by the exchange, settlement providers and the brokers, topped up each month from a sliver of turnover. It was designed to fix slow settlement, a real but far smaller problem than a broker draining client accounts. Turning it into genuine investor protection is not a tweak. It is a different institution, with a far larger balance sheet, that Nepal has not yet built.

This is structural, not a bad apple

The reassuring read is that Bhrikuti was one fraud, now caught and the system worked. The harder read is that everything which made it possible is normal. Brokers hold client cash as a matter of course. Informal credit fills the gap a banned margin market leaves, everywhere not just here. Segregation is preached, not enforced. And NEPSE's usual answer to a defaulting broker has been a one-week suspension, a penalty that treats the loss of client money like an overdue library book.

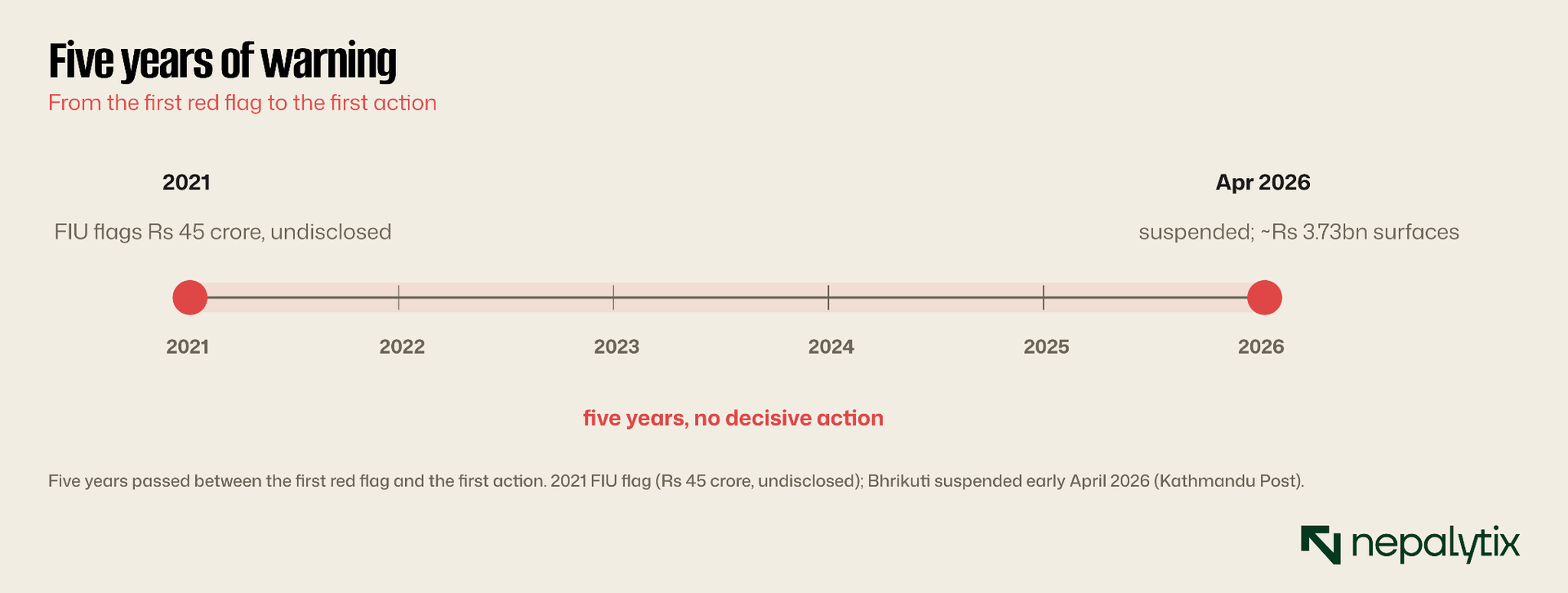

The clearest proof is how long the warning went unheeded. The first red flag on this very network was raised back in 2021 when the financial-intelligence unit traced tens of millions of rupees moving undisclosed into the same businessman's account. Nothing decisive followed. Five years passed, the position swelled into the billions, and only once the money was gone did the suspension arrive. A system that sees the smoke in 2021 and turns up after the building has burned is not under-informed. It is under-enforced.

When the conditions that enable a fraud are the everyday state of the market, the size of this one is the warning not the comfort. If a mid-sized broker can open a Rs 5.11bn hole under today's rules, then the rules, not the broker, are the exposure. The next failure will wear a different name and run through the same gap: a private firm holding public money, thinly capitalised, thinly policed, standing between every investor and the market.

And there is a final, deflating layer. The body that would have to fix all of this, the Securities Board, has itself been leaderless for stretches of the past year, its chair gone amid a separate scandal with no permanent successor named. A market whose plumbing needs urgent, technical, politically awkward repair is being asked to deliver it through a regulator short of both leadership and capacity. The watchdog, on the days the market most needs it awake, has been between owners.

Think of the broker layer as the market's wiring. You never see it, you assume it is up to code, and you find out otherwise only when something burns. Bhrikuti is the scorch mark that shows the wiring was never up to code to begin with. The fire was always possible. It just needed someone willing to light it.

Strip out the names and the lesson is plain and uncomfortable. In a market that argues endlessly about which share to buy, the bigger danger for many investors sits a layer beneath the share price entirely, in whether the broker holding their money is solvent and honest. Bhrikuti did not expose a bad company. It exposed a bad joint in the pipe. You can pick the right company and still be undone by the wrong custodian.

Watch four things from here. Whether the regulator moves from after-the-fact suspensions to enforced segregation and real broker capital. Whether a legal, supervised margin market finally replaces the shadow one that keeps breaking. Whether the guarantee funds become real and grow from settlement cover into genuine investor protection. And whether the Rs 5.11bn is ever recovered because that answer sets the precedent for who eats broker risk in Nepal. Until they change, trading on NEPSE means lending your broker money, unsecured, every time you press the buy button. The market has not priced that, because it has never had to. One day it will.

None of this means NEPSE is uniquely unsafe, or that brokers are not, overwhelmingly, honest. It means the system leans on that honesty far harder than it should and has built almost nothing to fall back on when it is absent. A maturing market earns trust by not requiring it. On that test, Nepal still has the harder half of the work ahead.

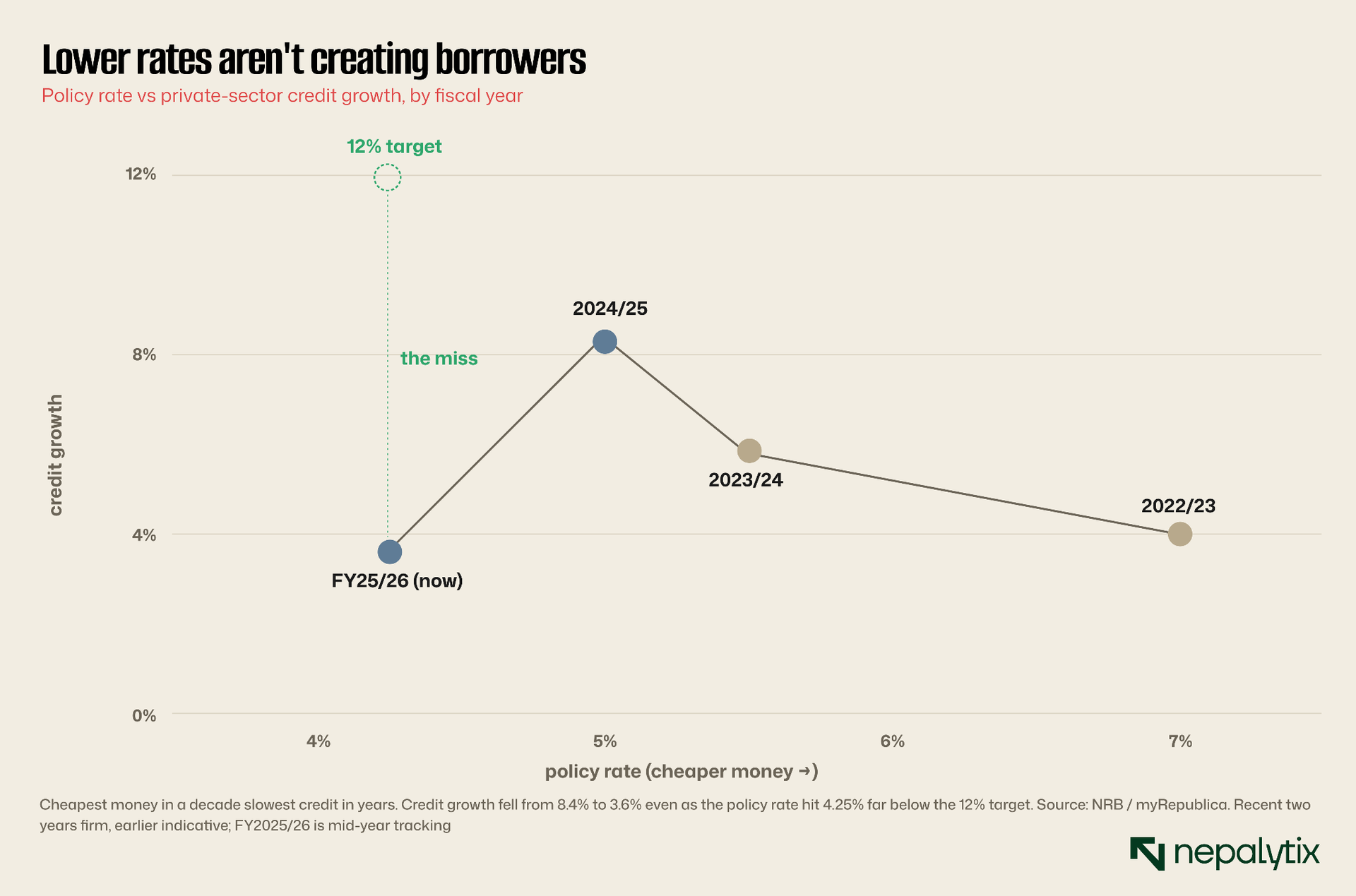

That is the crux. After September's Gen-Z unrest disrupted business and dented confidence, after years of sluggish investment, and with private credit already running near 92% of GDP against a world average closer to 52%, the appetite to borrow simply is not there. Foreign investors pledged Rs 35 billion in the first quarter yet actual inflows trailed the commitments, the same gap between intention and action that defines the whole economy right now. Cutting the price of credit does nothing when the shortage is of borrowers, not of funds.

History sharpens the contrast. Over the past two decades private-sector credit in Nepal grew by an average of nearly 20% a year, the kind of double-digit expansion that built the banks now listed on NEPSE. To slow from that to 3.6% with money at its cheapest in a decade is not a gentle deceleration. It is a credit market that has stopped responding to the one lever the central bank controls and a sign that the next phase of growth will have to come from something other than ever more bank lending.

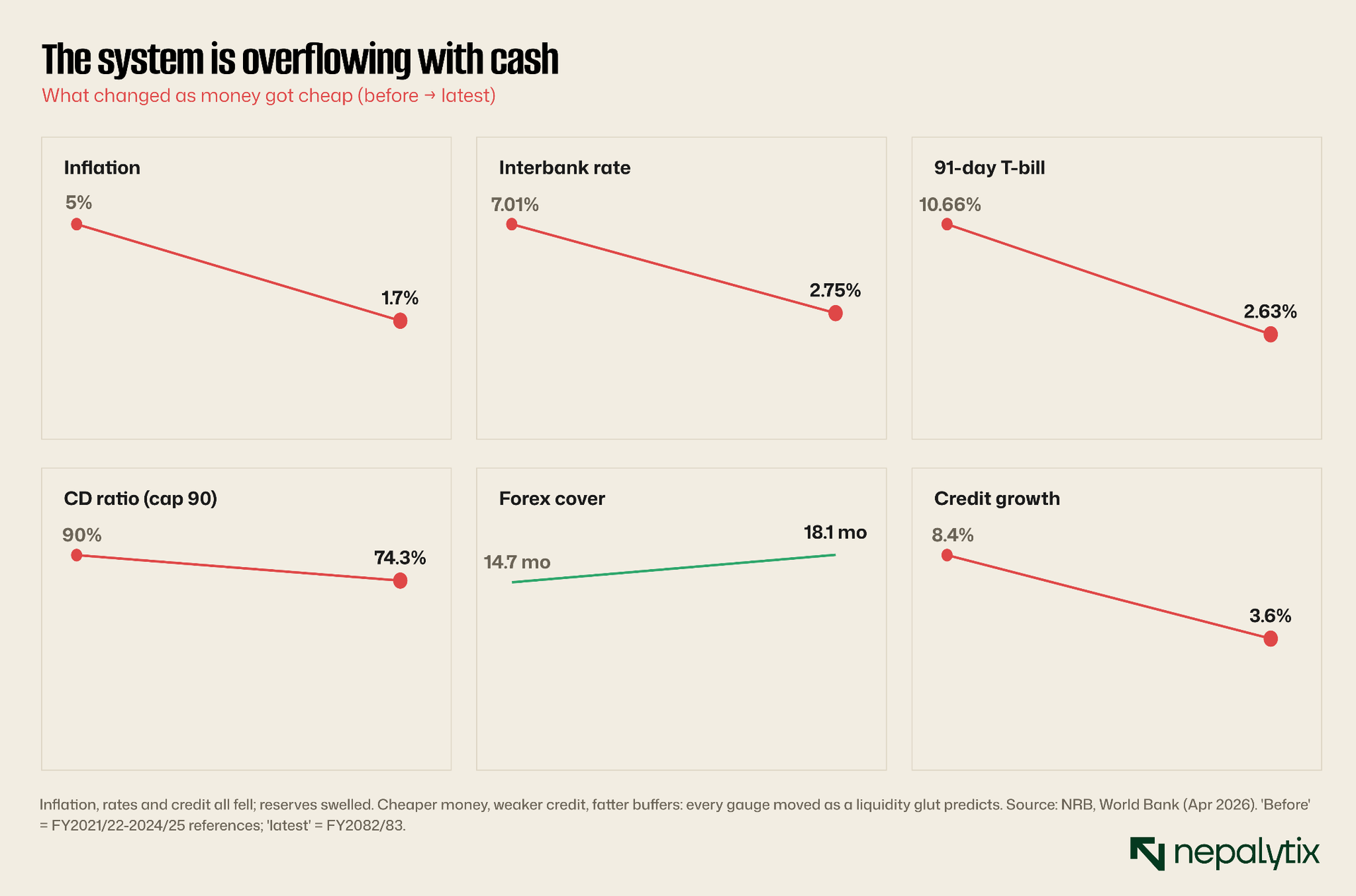

Every Indicator Says the Same Thing

A liquidity glut leaves the same fingerprints on every gauge, and Nepal's all point the same way at once. Inflation has fallen to 1.7%, a record low from 5% a year earlier. The interbank rate and the 91-day bill have both collapsed toward the floor. The credit-to-deposit ratio has slid from its 90% cap to 74%. Foreign-exchange cover has swelled from 14.7 to 18.1 months of imports, more than double the regulatory minimum of seven.

The sources of the flood sit on the external account. Remittances jumped 35.4% to Rs 553 billion in the first quarter alone, reaching 16.6% of GDP, and lifted the current account into a surplus worth 6.7% of output. The balance of payments ran a surplus above Rs 260 billion, and reserves climbed past USD 22 billion. Each of those dollars arriving has to be converted, and the conversion is where the rupees come from.

Here is the mechanism that makes the glut self-feeding. To stop the rupee from appreciating as dollars pour in the central bank buys the foreign currency paying for it in newly created local money. That single channel injected an estimated Rs 673 billion last year. The cash lands in bank deposits, the deposits cannot be lent fast enough and the surplus builds. Low inflation which would normally be unambiguously good news, here also signals how little of this money is chasing real goods. Only gold and silver prices show much heat which is itself a clue about where savers are hiding.

The composition of the inflows matters as much as their size. This is not an export boom or a surge of foreign investment building productive capacity; it is overwhelmingly money sent home by Nepalis working abroad deposited by their families and waiting to be spent or invested. That makes the glut both a strength and a vulnerability. It has handed Nepal record reserves and rock-bottom rates but it has tied the health of the banking system to labour markets in the Gulf and Malaysia, far outside any domestic policymaker's control.

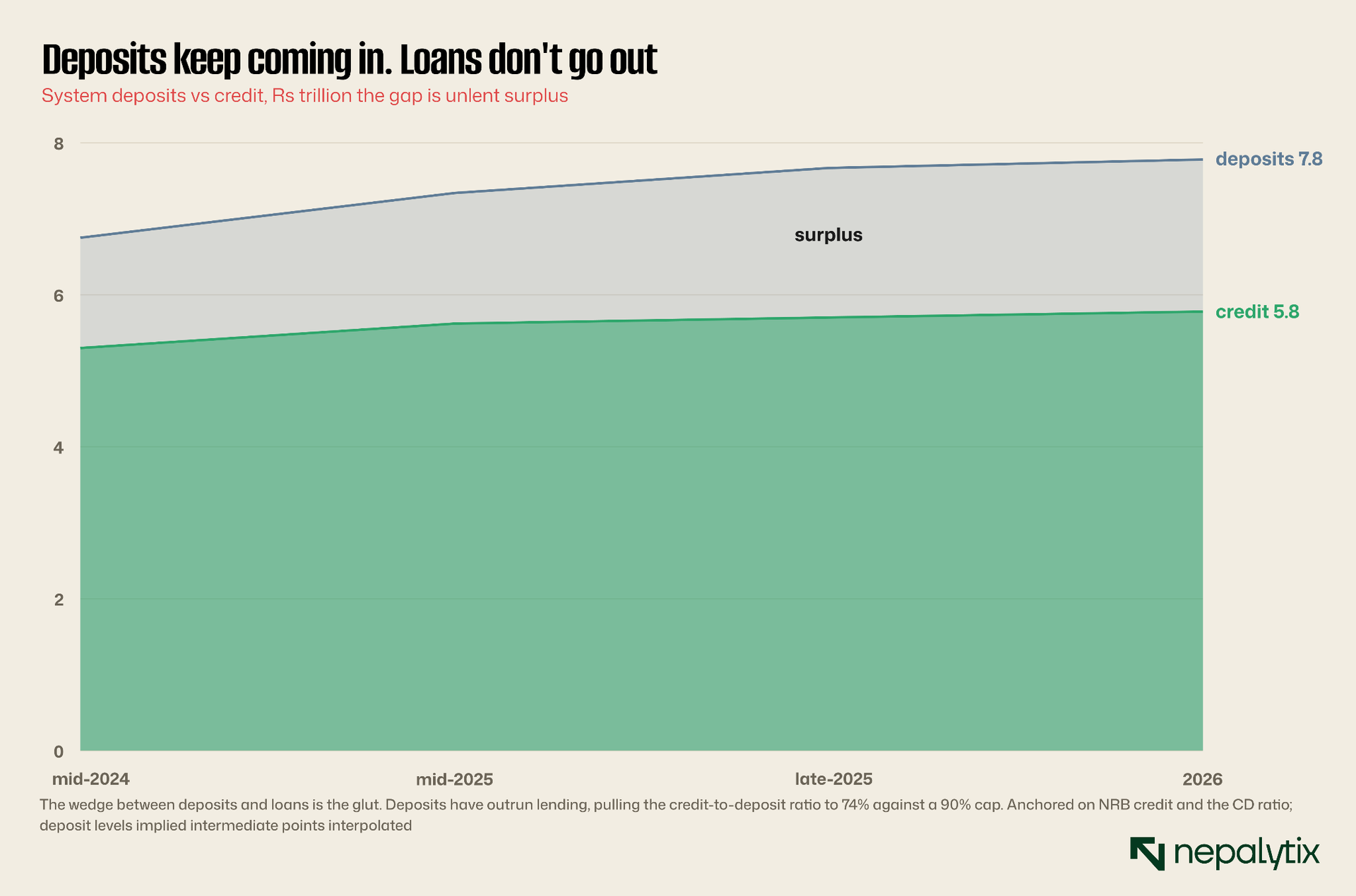

Deposits Keep Rising. Lending Doesn't

The mechanical result is a wedge. Deposits keep arriving, lending does not keep pace, and the space between the two is surplus the banks cannot put to work. A credit-to-deposit ratio of 74% against a 90% ceiling leaves roughly sixteen points of lending capacity idle across the system with state-owned banks sitting more conservatively still and private banks alone pushing toward the cap.

So the central bank is now doing the reverse of easing. Rather than inject money, it has spent the year mopping it up draining an estimated Rs 200 billion through repo auctions, fixed-deposit collections and a standing deposit facility it has stretched to 175 days. In one recent operation it offered to absorb Rs 50 billion for 42 days; it has promised to issue its own bonds if the tide rises further. To keep the interbank rate from sinking below the corridor floor, it has even barred banks that pay savers below the floor from parking cash at the facility.

A central bank that cuts rates to encourage lending is, at the same time, paying banks to hand cash back because there is nowhere productive for it to go. The banks are not unhappy about it. Flush with deposits and earning a spread of around 3.5 percentage points between what they charge borrowers and pay savers, they can sit on government paper and the deposit facility and still post a profit. Comfortable for the lender; a sign of a stalled engine for everyone else.

None of this is how an interest-rate corridor is meant to behave. In a balanced system the interbank rate floats near the policy rate, banks lend their surplus to one another, and the central bank intervenes only at the edges. In Nepal the interbank rate is glued to the bottom of the corridor and the central bank intervenes constantly, not to add liquidity but to remove it. The corridor has become a one-way valve, and the volume of cash flowing back to the regulator is the clearest single measure of how little the economy can absorb.

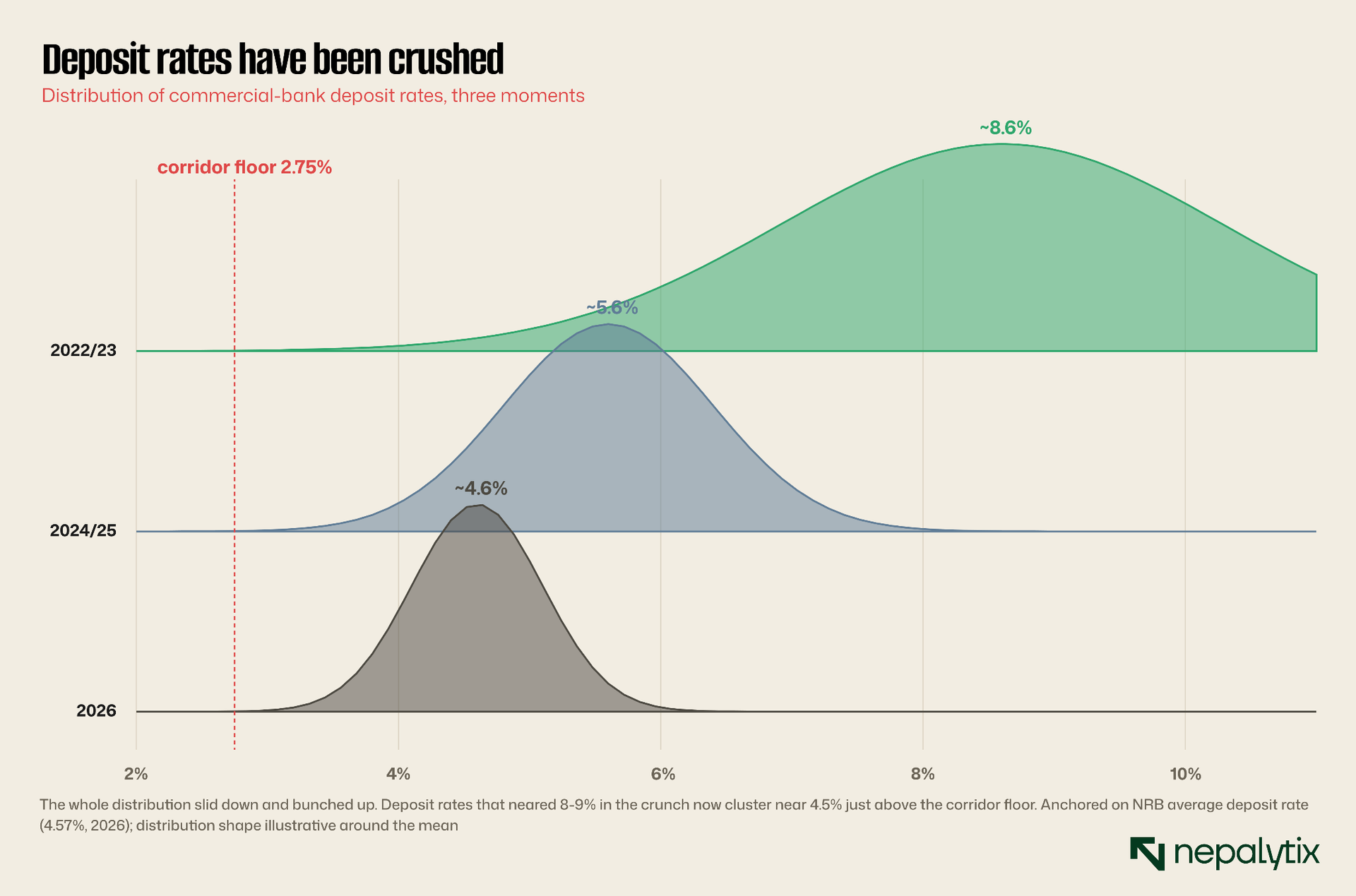

The Return on Safety Has Vanished

Someone pays for cheap money and in Nepal it is the saver. Deposit rates that neared 8 to 9% during the crunch now cluster around 4.5%, with commercial banks ranging from 4.25% to 5.10%, a sliver above the 2.75% corridor floor. Fixed deposits average 5.18%, ordinary savings 2.90%, and call deposits just 0.73%.

Low inflation softens the blow on paper. With prices rising 1.7%, a 4.5% deposit still earns a small positive real return, better than the negative real rates savers endured during the high-inflation crunch. But the trend is unmistakable and one-directional. The whole distribution of bank deposit rates has slid down and bunched against the floor and the central bank has cleared the way for it, removing the cap on institutional deposit rates so banks could trim the maximum they pay individuals.

For a saver the message is plain: a bank deposit now barely keeps pace with the cost of living and the gap between the best and worst rates on offer has narrowed to almost nothing. That is exactly the condition that sends money looking for a better home. When the safe option pays close to zero in real terms, the not-so-safe options start to look reasonable and a great deal of Nepali savings has come to precisely that conclusion.

The squeeze on savers carries a second-round effect the central bank cannot ignore. Push the return on a deposit low enough and the rational response is to stop saving in deposits, which would eventually starve the very banks now drowning in them. For now the remittance flood more than replaces any money that drifts away so deposits keep growing despite the meagre rates. The dynamic is still worth holding in mind: the glut is comfortable only as long as savers stay put and the thinner their reward the less certain that becomes.

Where the money actually went

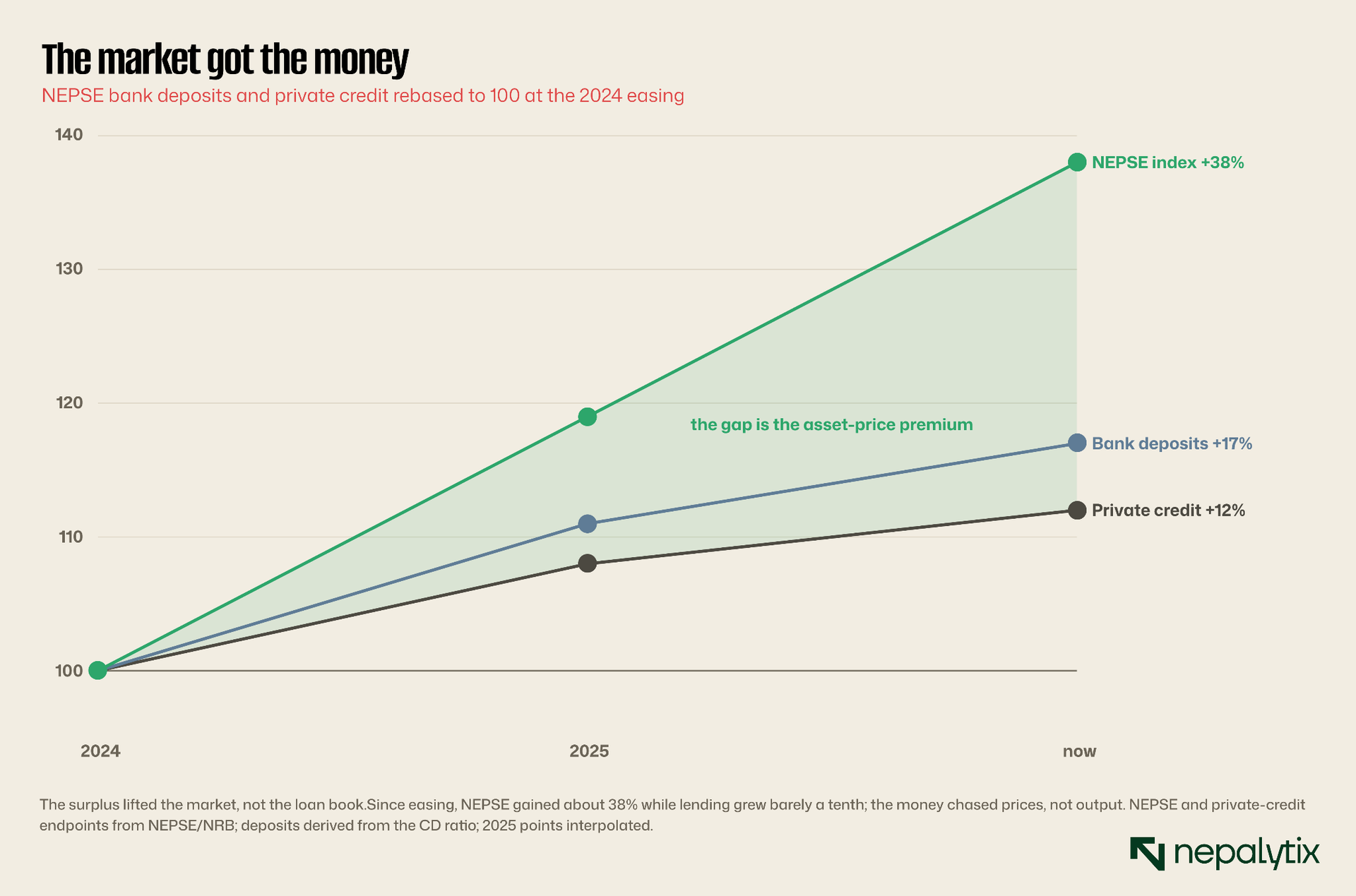

Where it looked, it found asset prices. With productive credit crawling and deposits paying 4.5%, the surplus chased returns into the secondary market and into property. NEPSE has risen by roughly 38% since 2024 to record territory; real estate, where transactions had collapsed 56% during the crunch, has revived as cheaper home loans and higher loan limits drew buyers back. Government paper soaked up much of the rest.

This is not a charge anyone has to infer. The central bank's own macroeconomic report concedes that the last round of easing "could not be fully absorbed by the market especially in productive sectors," and was instead reflected in asset prices, "with a record stock market index and real estate prices." Cheap money did not build factories. It bid up the things already built and lending to the real economy slipped to the back of the queue.

The loop tightens because the buyers are often the same institutions sitting on the surplus. Banks, insurers and the broader financial sector are themselves large holders of NEPSE-listed shares, so a market awash in their float is partly holding itself up. Eased risk weights on smaller margin loans add another turn of leverage. None of that is dangerous while the inflows continue. It becomes dangerous precisely when they stop, because an asset price lifted by liquidity rather than earnings has nothing to stand on once the liquidity recedes.

The numbers around the rotation are striking on their own. A stock index up nearly 40% in two years, a property market swinging from a 56% collapse to a visible revival and a deposit base earning under 5% sit beside a real economy whose credit is barely growing. That divergence, between asset prices and the activity supposed to underpin them, is the clearest symptom of money with nowhere productive to go. It is also the part of the story most easily mistaken for a healthy bull market.

The Problem Isn't the Cost of Money

The uncomfortable conclusion is that another rate cut will not fix this. The central bank has already cut to 4.25% and watched the credit stall because the binding constraint is not the price of money. It is weak investment demand in an economy still rattled by September's unrest, and a structural ceiling on how much more credit a country already lent to the hilt can absorb. Non-performing loans are rising and bank spreads are thinning at the same time, which is why the regulator is reaching past interest rates altogether.

Its toolkit now runs to an asset-management company to take bad loans off bank books, looser working-capital rules, productive-sector lending targets and prompt-corrective action reforms for weak institutions. These are supply-side fixes for a demand-side problem and the central bank knows it; what it cannot do with any instrument is manufacture borrowers. The structural work, an investment climate worth committing to, credit guarantees, coordinated fiscal support, sits largely outside its remit.

For an investor the read-through is blunt. As long as money stays cheap and the real economy cannot absorb it, the surplus keeps flowing toward NEPSE, property and bonds, supporting asset prices for reasons that have little to do with corporate earnings. That is a tailwind worth riding and a risk worth respecting because a glut that lifts prices without lifting output unwinds the day the inflows slow. The single number to watch is remittances, the source of the flood; the FY2083/84 monetary policy due in July cannot conjure demand and can only decide how hard to lean against a tide of cheap money with nowhere to go.

A few warning lights are worth naming before then. Non-performing loans are creeping up even as the headline figures look benign, public debt has climbed toward 44% of GDP, and the asset-price gains flattering portfolios rest on inflows rather than earnings. None of these is a crisis today. Together they describe a system that has solved its liquidity shortage and replaced it with a subtler one: too much money, too few productive homes for it and an asset market drifting away from the economy beneath it. That is the imbalance the next policy inherits.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.