The budget real job is fixing the machinery not spending the money

Nepal’s biggest economic problem isn’t a lack of money, it’s a broken system for deploying it. As Budget 2083 arrives, the real question is whether the government will fix the country’s clogged financial machinery or simply spend more through it.

Tomorrow's budget will be judged on the wrong things. The headlines will count the total outlay, the social allocations, the tax tweaks. But Nepal's binding constraint is not how much the government spends. It is that the country's entire capital-formation machinery, the securities regulator, the trapped pension and insurance pools, the disconnect between fiscal and monetary policy is broken in ways that no amount of spending fixes. This is the first budget with the political room to repair it. The question is whether it will.

Every year the budget arrives and the country argues about the same things: the size of the headline number, which districts got which projects, and whether the social security allowance went up. These arguments are not unimportant. But they consistently miss the structural reality, which is that Nepal does not primarily have a money problem. It has a plumbing problem. The capital exists. The savings exist. The institutions that are supposed to move that capital from where it sits to where it is needed have stopped working and in some cases are actively making things worse. A budget that adds another hundred billion rupees of spending to a financial system whose pipes are clogged is pouring water into a blocked drain.

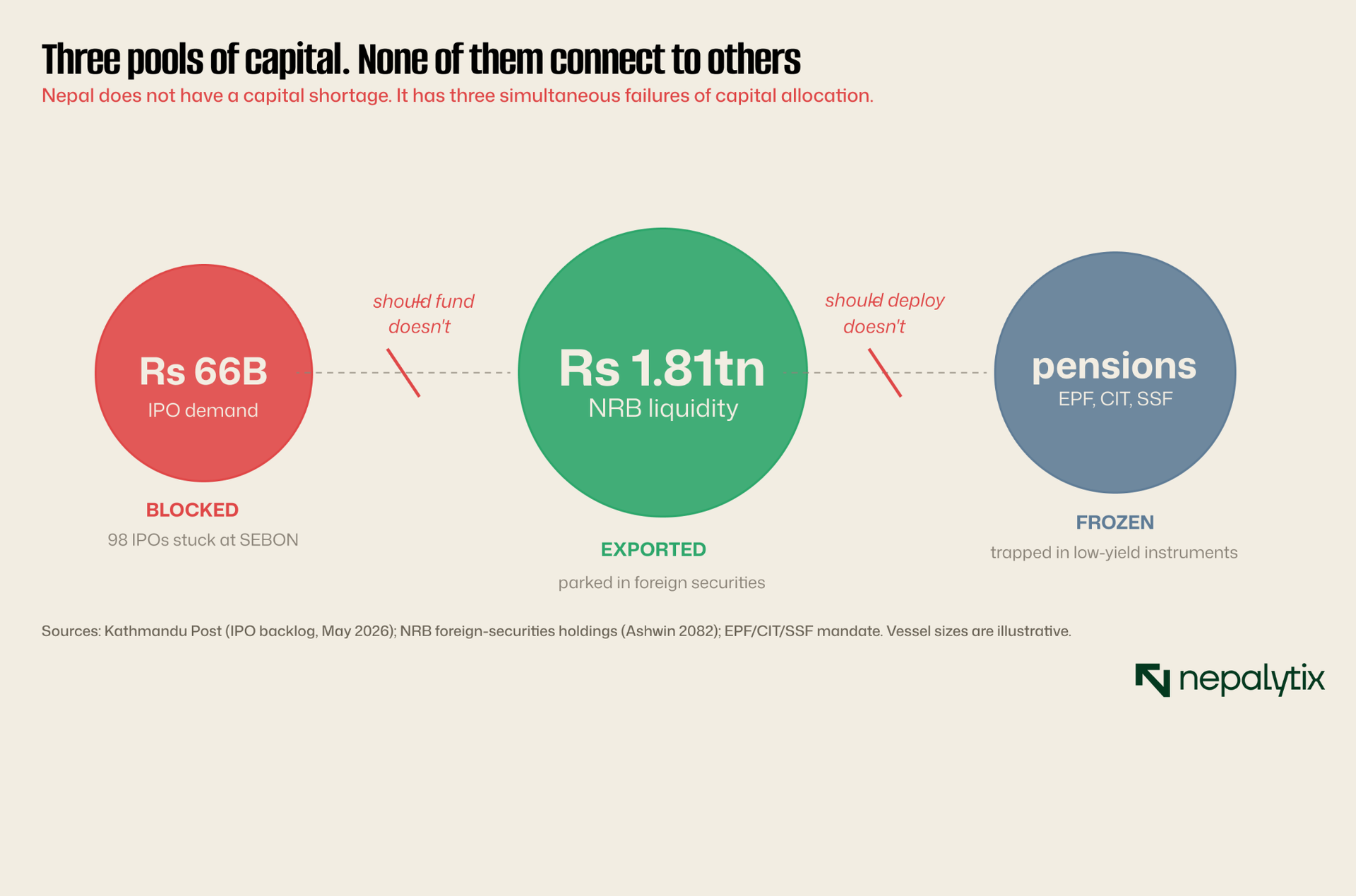

Consider three facts that are all true at the same time in Nepal's financial system as of this writing. First, the Securities Board of Nepal is sitting on ninety-eight initial public offering applications seeking to raise approximately Rs 66 billion, having approved only a handful in the past eighteen months, with its chairman having resigned in April 2026 amid a corruption investigation. Second, the Nepal Rastra Bank is parking Rs 1.811 trillion in foreign securities abroad because it cannot find sufficient productive domestic deployment for the liquidity sloshing through the banking system. Third, the country's pension and provident funds institutions holding the retirement savings of more than a million Nepalis were until weeks ago legally restricted to fixed deposits, government bonds, and a narrow set of shares, earning yields that barely keep pace with inflation.

Put those three facts next to each other and the picture is absurd. Companies that want to raise capital cannot, because the regulator is paralyzed. The central bank has more capital than it can deploy and sends it overseas. And the largest domestic pools of long-term savings sit in low-yield instruments because the law would not let them do anything else. This is not a capital shortage. This is a capital-allocation failure, institutionalized across three separate parts of the financial system simultaneously. That is what the budget should be addressing. Whether it spends Rs 1.9 trillion or Rs 2.1 trillion is almost beside the point.

SEBON has stopped doing the one thing it exists to do

The Securities Board of Nepal exists to regulate the capital market and at the most fundamental level, that means approving the orderly entry of new companies onto the exchange so that they can raise capital from the public and so that the public can participate in their growth. This is the primary market function. It is the reason a securities regulator exists at all. And it is precisely the function that SEBON has effectively stopped performing.

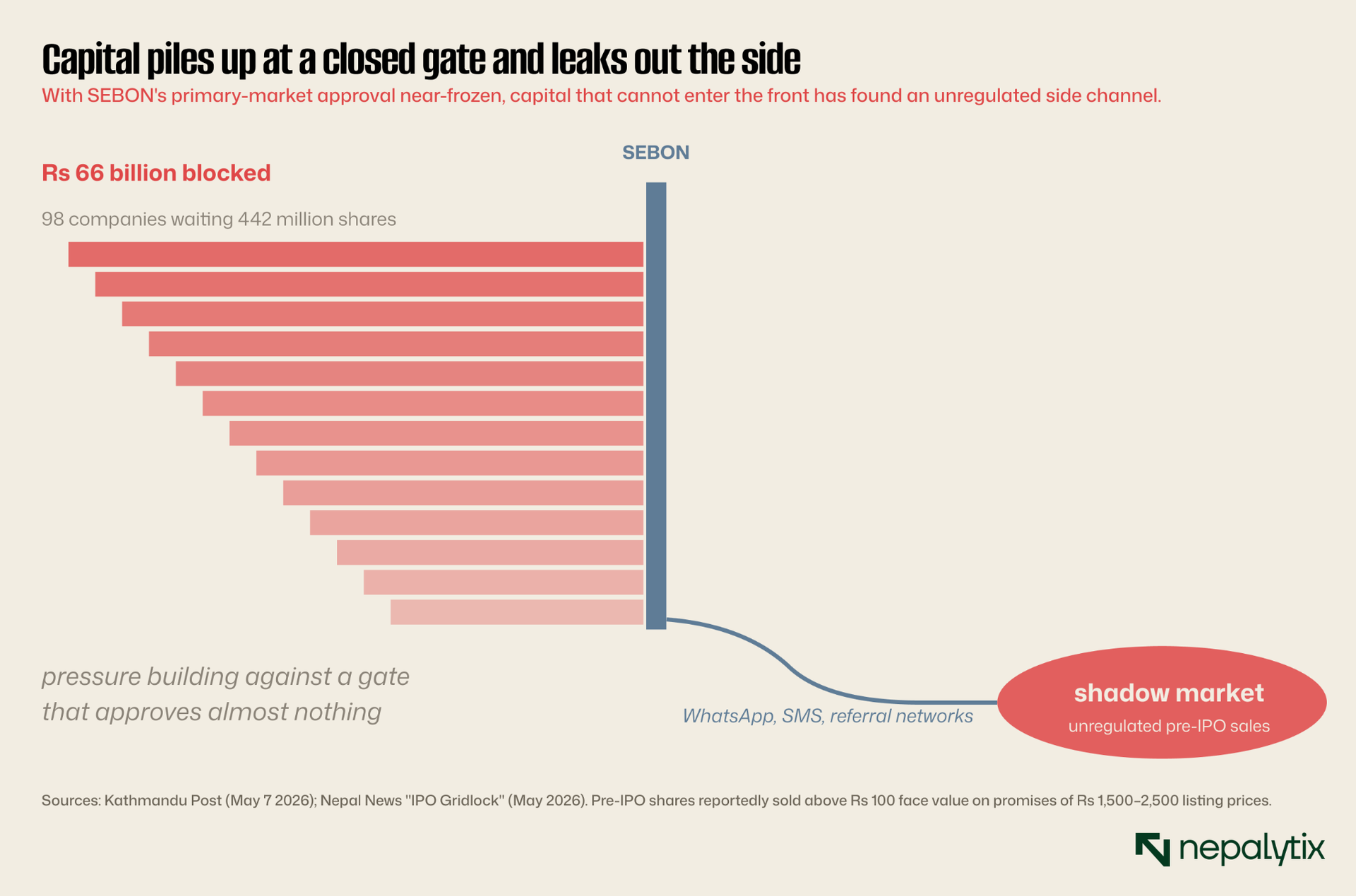

The numbers are stark. As of early May 2026, ninety-eight companies had applications pending with SEBON seeking to raise a combined Rs 66.23 billion through the issuance of 442 million shares. Thirty-two of those are hydropower companies seeking Rs 15.54 billion: capital that is in many cases the final financing step for projects that are otherwise built and ready. Eighteen are hotel and tourism companies. Over an entire preceding year, at one low point, SEBON had approved exactly one IPO that of Guardian Microinsurance. The regulator was without a chairman from late 2023 until November 2024. The chairman appointed then, Santosh Narayan Shrestha, resigned in April 2026, with his tenure having drawn criticism for the limited number of approvals and having attracted a Commission for the Investigation of Abuse of Authority inquiry into alleged irregularities in the approval process.

The consequences of this paralysis go beyond inconvenience. When the front door of the capital market is effectively closed, capital finds a side door and the side door is unregulated and dangerous. In SEBON's absence, an unregulated pre-IPO market has expanded dramatically. Companies raise hundreds of millions of rupees from private investors before any SEBON approval, using merchant banks, WhatsApp groups, direct SMS, and personal referral networks to sell equity stakes at multiples of the Rs 100 face value. Investors are promised that once the company eventually lists, the shares will trade at Rs 1,500 to Rs 2,500 and that after a lock-in period they can exit handsomely. This is precisely the kind of unregulated securities solicitation that a functioning securities regulator exists to prevent. SEBON's paralysis has not stopped capital from moving; it has pushed it into channels with no investor protection at all.

There was supposed to be a fix. After widespread criticism of the capital market's inefficiency, a Capital Market Reform Task Force was formed under a Finance Minister-level decision. It submitted a comprehensive report on September 25, 2025, recommending reforms in three phases with specific timelines. The Ministry of Finance directed SEBON, NEPSE, and the CDSC to implement the recommendations. SEBON's share of the plan included nine short-term tasks with deadlines, four of them to be completed immediately. As of late 2025, none had been completed or even initiated. The regulator released a token action plan only after investors physically surrounded its office in protest. The reform roadmap exists. The institutional will to implement it does not.

This is where the budget comes in. A budget cannot by itself, approve an IPO. But a budget is the government's primary instrument for signaling institutional priority and allocating the resources and legal authority that reform requires. The budget can commit to amending the Securities Act to introduce time-bound approval requirements, a statutory clock that forces SEBON to approve or reject within a defined window, with deemed approval if it fails to act. It can fund the regulator's capacity, since part of the paralysis is genuine under-resourcing. It can commit to the demutualization of NEPSE separating the exchange's ownership from its members which has been discussed for years and never executed. It can mandate the implementation of the reform task force's roadmap with budget-backed accountability. None of these are spending decisions in the conventional sense. All of them are things a serious budget would address.

The trapped pools are finally being unlocked clumsily

Nepal's largest pools of long-term domestic capital are its retirement and social-security institutions: the Employees Provident Fund, which manages the savings of roughly 600,000 government and private-sector employees; the Citizen Investment Trust, which has managed pensions, retirement funds, and long-term savings for over three decades; and the newer Social Security Fund. Together they hold a substantial share of the long-duration savings in the entire economy. Long-duration savings are precisely the kind of capital that should be funding long-duration productive investment: infrastructure, growth equity, the kind of patient capital that an emerging economy desperately needs.

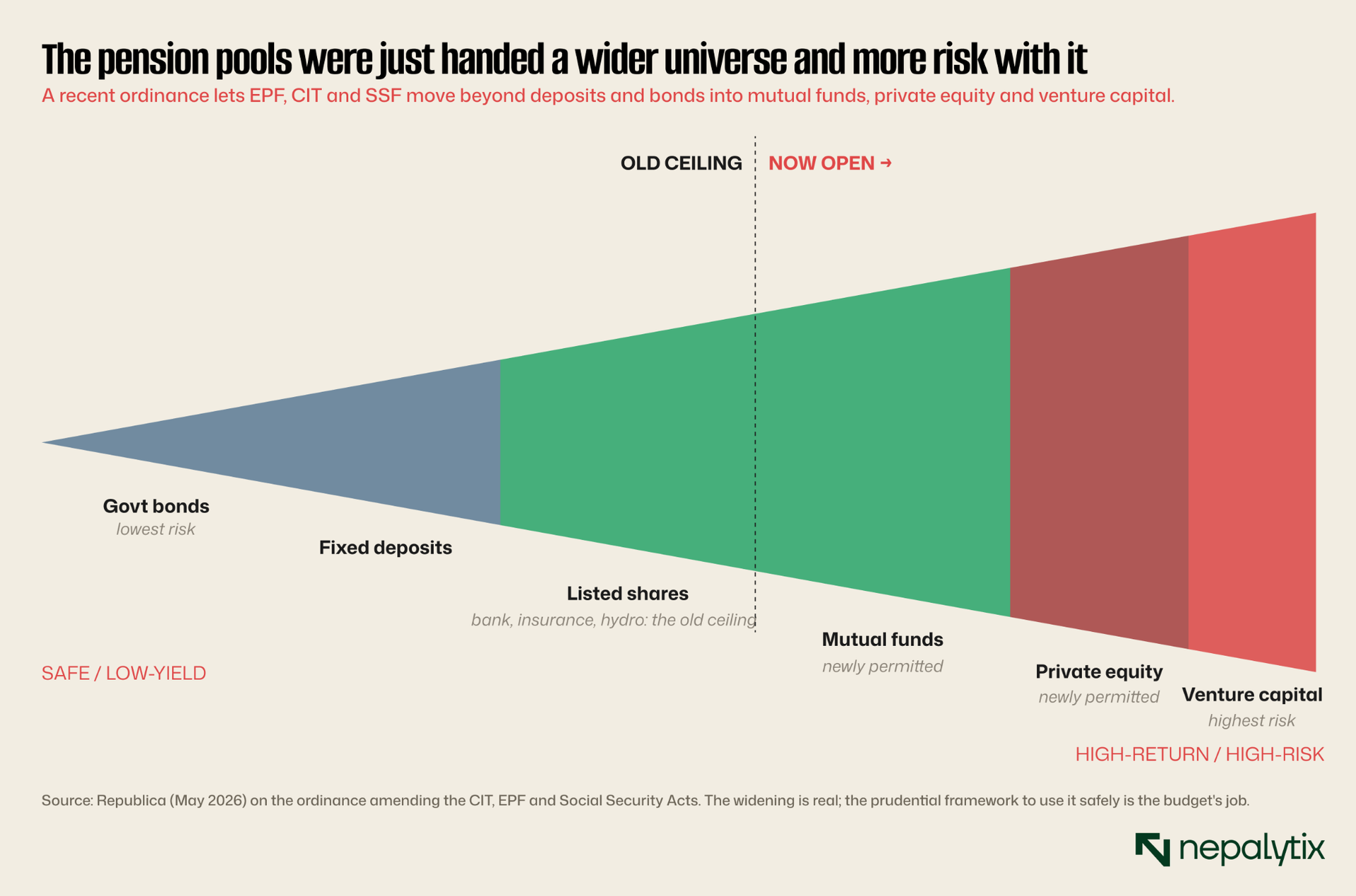

Until weeks ago, they could not. The EPF, CIT, and SSF were legally restricted, for the most part, to fixed deposits, government bonds, and a narrow set of permitted shares, primarily banks, insurance companies, and hydropower. The result was that the nation's largest patient-capital pools were earning bank-deposit yields in a falling-rate environment, on the retirement savings of more than a million people. The capital that should have been the backbone of Nepal's growth-equity and infrastructure-financing ecosystem was instead recycling through the same bank deposits that the entire system is already drowning in.

This has just changed and the timing relative to the budget is the point. Through an ordinance amending the CIT Act, the EPF Act, and the contribution-based Social Security Act, the government has now permitted these three funds to invest in mutual funds, private equity and venture capital. The CIT can move beyond bank and insurance shares into SEBON-approved mutual funds and venture-capital instruments. The EPF which previously ran only its own internal collective investment scheme, can now participate in external funds. The SSF can diversify into private equity. This is, in principle, exactly the right direction. The trapped capital is being given somewhere to go.

But an ordinance that opens a door is not the same as a framework that makes walking through it safe. This is where the budget's responsibility begins, and it is a responsibility that cuts in two directions at once. On one side, the reform must be operationalized, the implementing regulations, the governance structures, the professional fund-management capacity that allows a pension fund to actually deploy into private equity and venture capital competently rather than disastrously. A provident fund that suddenly has legal permission to invest in venture capital, but no internal capability to assess venture-capital risk, is not safer than before. It is more dangerous. The budget should fund and mandate the institutional capacity-building that makes the new latitude usable.

On the other side and this is the harder argument there must be limits. These are retirement savings. The entire reason they were restricted to low-risk instruments in the first place was to protect contributors from exactly the kind of capital loss that private equity and venture capital can inflict. The right answer is not to swing from one extreme to the other from a stifling all-conservative mandate to an open-ended permission to chase returns in the riskiest asset classes. The right answer is a calibrated allocation framework: a capped percentage of the portfolio permitted into higher-risk assets, with the bulk remaining in instruments appropriate to the fiduciary obligation these funds owe to people who are counting on this money for their old age. The budget, and the regulatory architecture it directs, is where that calibration should be set. Getting this wrong in either direction is too restrictive and the capital stays trapped, too permissive and pensioners bear losses they never consented to is the single most consequential financial-sector decision in this budget cycle.

A pension fund with permission to chase venture-capital returns, but no capability to assess venture-capital risk, is not freer. It is more exposed.

Fiscal policy keeps leaving monetary policy to fight alone

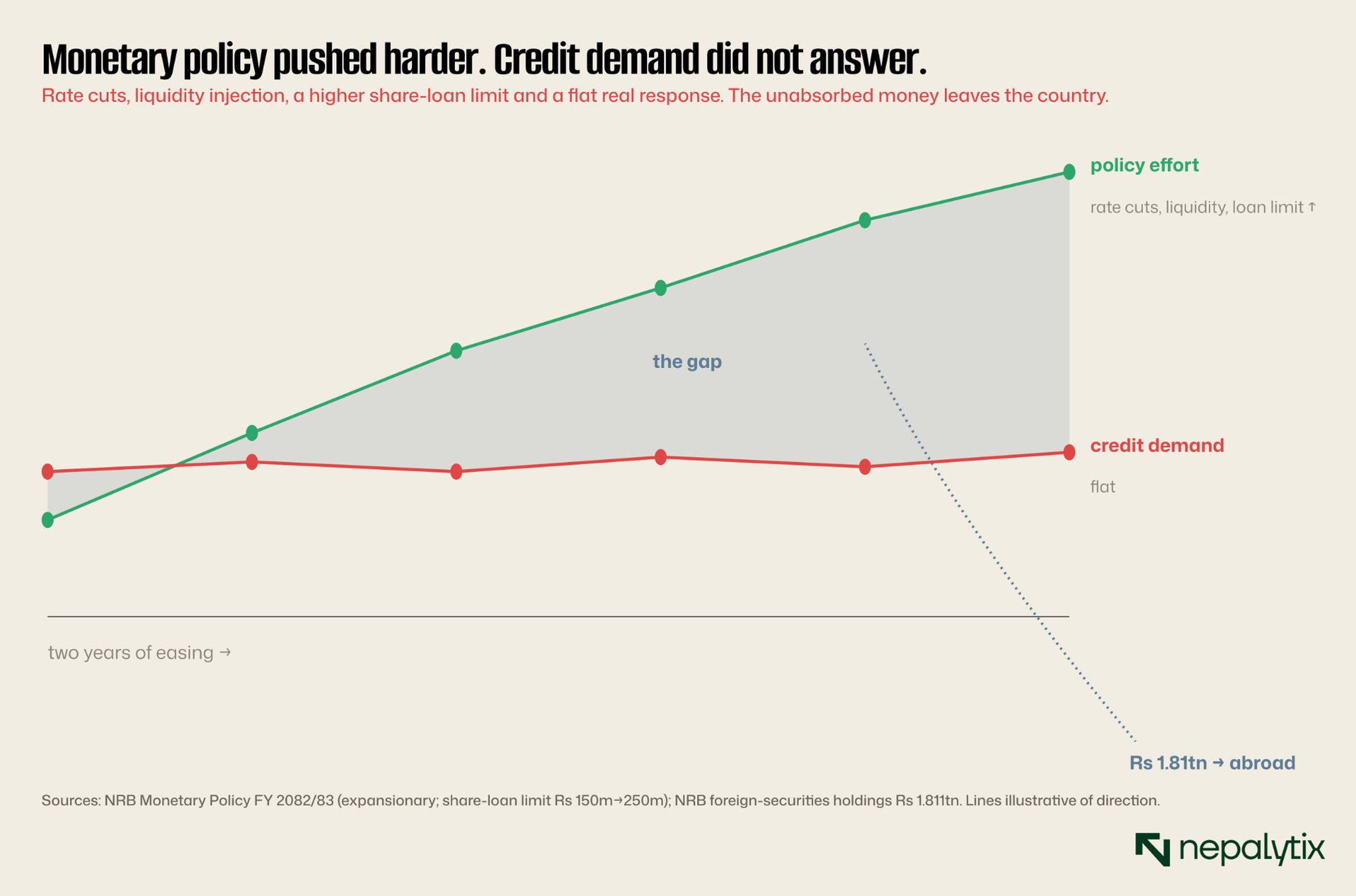

For two years, Nepal's monetary policy has been trying to revive private-sector credit demand and has been failing not because the policy is wrong but because monetary policy cannot do this job by itself. The Nepal Rastra Bank has cut rates. It has flooded the system with liquidity. It has raised the share-collateral lending limit from Rs 150 million to Rs 250 million to stimulate capital-market activity. It has permitted banks to invest in infrastructure bonds. The monetary policy for the current fiscal year was explicitly expansionary and discretionary designed to inject money and lower the cost of borrowing. And still, private-sector credit demand has remained weak, banks sit on excess liquidity and the central bank exports Rs 1.811 trillion to foreign securities because it cannot find domestic productive deployment. The reason monetary policy cannot fix this alone is that the problem is not the price of money. It is the absence of bankable demand for it. Businesses are not borrowing and investing not because rates are too high but because the real-economy conditions that would make investment profitable are reliable infrastructure, predictable regulation, functioning project-approval pipelines and demand visibility are not there. Those are fiscal and structural conditions, not monetary ones. A central bank can make money cheap. It cannot make a project bankable. Only fiscal policy and structural reform can do that.

This is the fiscal-monetary disconnect and it is the most important macro-financial relationship in the budget. The budget should be designed explicitly to do the things monetary policy cannot: clear the infrastructure bottlenecks that make private projects viable, accelerate the capital-expenditure execution that has chronically underperformed (the government routinely spends a fraction of its allocated capital budget leaving development spending on the table while recurrent spending balloons) and create the project-pipeline visibility that lets private capital commit. Every rupee of well-executed capital expenditure that makes a private project viable does more to revive credit demand than another rate cut. The budget's capital-expenditure execution rate, not its allocation, its actual execution is arguably the single most important number for the financial sector that will come out of tomorrow's document.

The insurers are stuck in the same trap, with the same key

The same structural logic applies to the insurance sector, which this publication examined in detail earlier this week. Nepal's insurers life and non-life hold large investment portfolios that are concentrated by regulatory constraint, in bank fixed deposits. Roughly three-quarters of the non-life sector's investment book sits in BFI deposits. As deposit rates have fallen, insurer investment income has compressed, squeezing the profitability of the entire sector regardless of how well the underwriting is managed. The insurers have been petitioning the Nepal Insurance Authority for permission to invest a portion of their funds overseas, in higher-yielding instruments, precisely because the domestic permitted universe cannot generate the returns needed to fund long-term policy liabilities.

The parallel to the pension funds is exact. Here is another large pool of long-duration domestic capital, trapped by regulation in low-yield instruments seeking permission to deploy more productively. The budget and its associated regulatory direction should treat the insurance investment framework as part of the same reform agenda as the pension-fund liberalization with the same calibration logic. Insurers, like pension funds, owe a fiduciary obligation to policyholders, and the answer is the same: a calibrated widening of the permitted universe, with prudential caps, professional capacity requirements, and risk-appropriate limits, rather than either continued suffocation or reckless liberalization. Treating the pension funds, the insurance pools, and the broader capital-deployment question as a single coherent reform rather than three separate ad-hoc ordinances is what a serious budget would do.

The opposing view, treated fairly

There is a serious argument against everything written above, and it deserves a fair hearing. The argument is this: Nepal's institutions are weak, its governance is fragile, and its capital markets are shallow and prone to manipulation. In that environment, the conservative restrictions on pension funds, the slow IPO approvals, and the cautious investment mandates are not bugs they are appropriate guardrails for an immature financial system. Loosening them invites exactly the kind of losses, frauds, and bubbles that a poorly-supervised emerging market is most vulnerable to. On this view, the SEBON paralysis is bad, but the answer is better administration within the existing cautious framework, not a structural liberalization that the supervisory capacity cannot safely handle.

This argument is not wrong about the risks. An emerging market that liberalizes its capital allocation faster than it builds its supervisory capacity does invite crises; the history of financial liberalization across emerging markets is littered with exactly those episodes. The pre-IPO shadow market that has grown in SEBON's absence is itself a preview of what under-supervised capital activity looks like.

But the argument ultimately fails on a single point: the conservative framework is not actually producing safety. It is producing a different kind of risk. Capital trapped in low-yield instruments while inflation erodes it is not safe, it is a slow, certain loss disguised as prudence. An IPO regime so paralyzed that it pushes capital into unregulated WhatsApp share-selling is not protecting investors it is exposing them to the worst kind of unprotected risk. The status quo is not the safe option. It is simply a less visible kind of danger. The choice is not between reform-risk and safety; it is between the managed risk of careful liberalization and the unmanaged risk of institutionalized dysfunction. The careful version is better.

Why this budget, specifically : The political window that will not stay open

Every argument in this piece could have been made about any of the last several budgets. The structural problems are not new. SEBON has been weak for years. The pension funds have been trapped for decades. The fiscal-monetary disconnect has been visible since the post-pandemic liquidity built up. So why argue it now, with unusual urgency, for this budget specifically?

Because the political configuration that produces this budget is genuinely different, and the difference creates a window. This is the first full budget cycle following the Gen-Z movement of September 2025, the fall of the prior government, and the generational political shift that the 2026 elections produced. Whatever else one thinks of that upheaval, it has produced a government with something its predecessors lacked: the political legitimacy, and the popular mandate for institutional reform, to do things that entrenched interests had previously blocked. The capital-market reform task force recommendations were ignored under the old configuration. The SEBON dysfunction persisted because the constituencies that benefited from the status quo had the political weight to protect it. A genuinely reformist budget one that restructures the broken machinery rather than simply spending through it requires exactly the kind of political room that rarely exists and does not last.

Windows like this close. The reformist energy of a post-upheaval government dissipates as the ordinary politics of entrenchment reassert themselves. The budget that lands tomorrow is the clearest early test of whether the new political configuration will use its mandate to fix the structural machinery of Nepal's financial system, or whether it will do what every prior government did count the headline number, distribute the allocations, tweak the taxes, and leave the broken plumbing for next year. If the structural reforms are not signaled now, with this mandate, they are unlikely to come from a weaker future government.

What to actually look for tomorrow: The five signals that matter

When the budget is read tomorrow, the headlines will focus on the total size, the social allocations, and the tax changes. Readers of this publication should look instead for five specific things, because these are the signals that will reveal whether the budget is serious about the machinery or merely about the money.

First, any commitment to amend the Securities Act with time-bound IPO approval requirements, or any explicit budget-backed mandate to implement the Capital Market Reform Task Force roadmap. Vague language about "strengthening the capital market" is the tell of non-seriousness; a statutory approval clock is the tell of seriousness.

Second, the operational framework for the newly-permitted pension and provident fund investments. Does the budget fund the capacity-building and set the prudential caps that make the EPF/CIT/SSF liberalization safe, or does it simply celebrate the ordinance and move on? The presence or absence of a calibrated allocation framework is the signal.

Third, the capital-expenditure execution commitment, not the allocation, is the execution mechanism. Does the budget include concrete measures to fix the chronic under-execution of development spending, or does it allocate large capital figures that everyone knows will not actually be spent?

Fourth, the insurance investment framework. Is there any signal of a coherent approach to the insurers' trapped-capital problem, ideally connected to the pension-fund reform as part of a single capital-deployment agenda?

Fifth, and most telling, whether any of this is framed as structural reform at all, or whether the financial sector appears in the budget only as a source of revenue and a destination for incidental tinkering. The framing reveals the intent.

The budget tomorrow will spend roughly two trillion rupees. The number will dominate the coverage. But the number is not the test. The test is whether, somewhere in the document, the government demonstrates that it understands its real job: not to pour more capital into a financial system whose pipes are blocked, but to fix the pipes. Nepal does not need a bigger budget. It needs a budget that repairs the machinery through which all the other money is supposed to flow. Tomorrow we will find out if it got one.