The Budget Taxed Your Gains. Here's What It Got Wrong

Nepal's FY 2083/84 budget delivered a long-awaited reform by making capital gains tax on listed shares final, ending years of uncertainty for investors.

The FY2083/84 budget did something genuinely good for investors and something genuinely wrong in the same sentence. It made the capital gains tax on shares final, ending years of filing confusion. Then it raised the rate on long-term holders most of all in a market that has gone nowhere for five years and in the same breath promised to modernise it. This is the case for why the second move undercuts the first.

The Argument

Making capital gains tax final was the right reform and a real one. But pairing it with a rate rise weighted onto patient long-term capital, in a market stuck below its 2021 peak and which the very same budget is trying to fill with new participants, is a contradiction. It raises the toll on the bridge it is widening, taxes inflation as if it were wealth, and collects a rounding error for the trouble. The rate is still low by regional standards. The direction and the timing are the mistakes.

What the budget actually did

Start with the facts because the headline has been blurred by celebration and complaint in roughly equal measure. In the budget for fiscal year 2083/84, presented on 29 May 2026, the government changed the capital gains tax on listed shares in two ways at once. It raised the rate and it changed the rule. The two moves point in opposite directions, which is why the reaction has been so split.

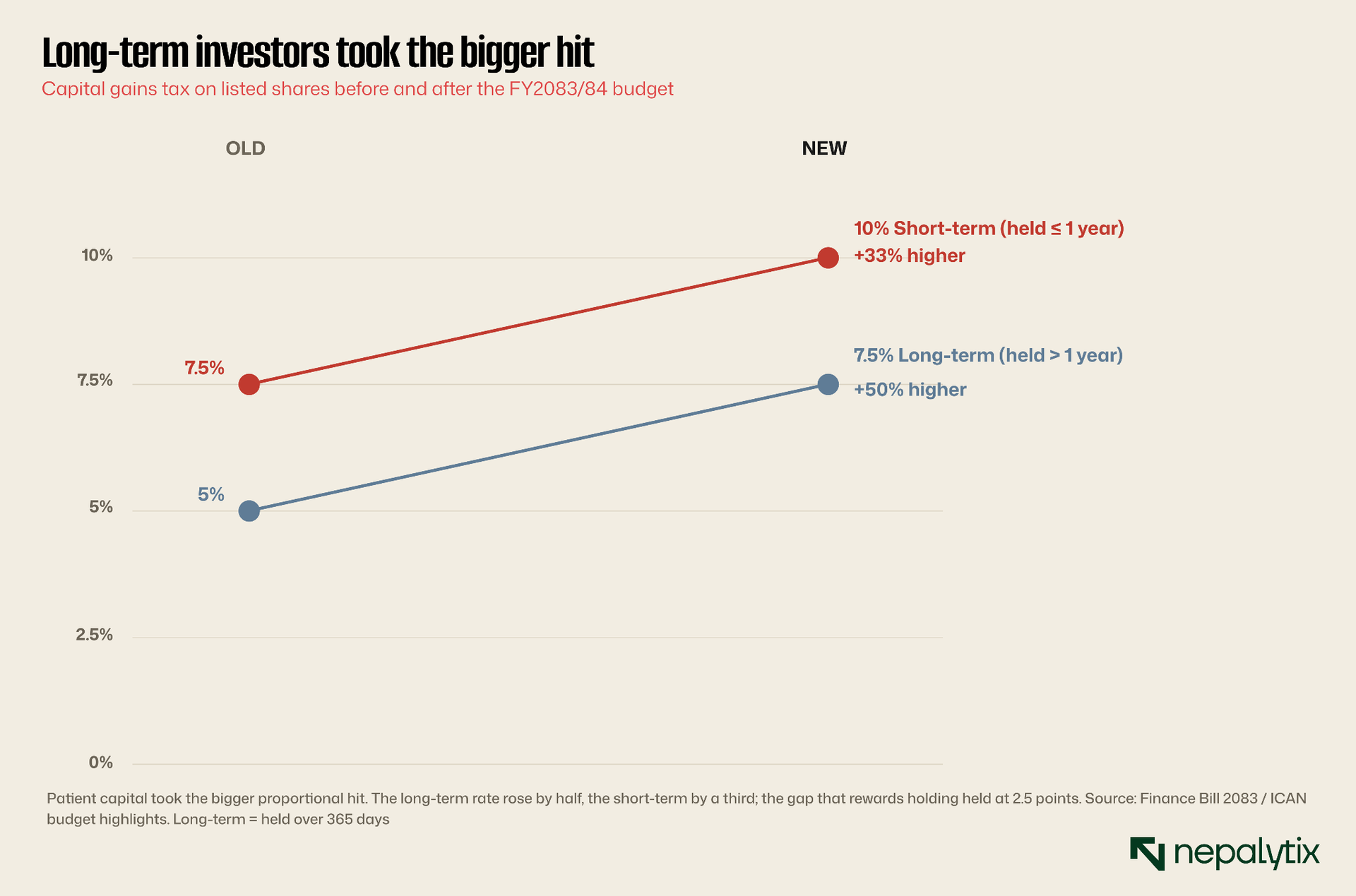

The rate rise is straightforward. Tax on gains from shares held for more than a year went from 5% to 7.5%. Tax on gains from shares held a year or less went from 7.5% to 10%. So the long-term rate rose by half and the short-term rate by a third. The rule change is subtler and on its own welcome: capital gains on listed securities are now a final tax. The amount withheld when you sell closes the obligation. There is no further filing, no pulling the gain into your total income, no risk of it lifting you into a higher personal bracket later. For an investor, the compliance headache that used to follow a profitable year is gone.

Hold both facts in mind together because most of the commentary has picked one and ignored the other. The traders celebrating finality are right that it removes a genuine source of friction and uncertainty. The investors complaining about the hike are right that they will hand over more on every realised gain. The interesting question is not which camp is correct. It is what the combination does, who it helps, who it hurts and whether it fits the rest of what this budget claims to want for the market.

The chart traces the change. Two lines each rising from the old rate to the new. The short-term line ends higher at 10% but the long-term line rises more steeply in proportion, and that detail turns out to matter more than the absolute levels. One mechanical point is worth fixing in place, because it shapes everything that follows. A final tax means the rate is collected at the moment of sale, deducted through the depository and the broker, and that is the end of it: no annual return for the gain, no reconciliation, no later assessment. The dividend tax, separately, was left unchanged at its flat 5%, also final. So the budget's equity-tax package is really three numbers: a 5% tax on dividends, untouched, and capital gains at 7.5% long-term and 10% short-term raised but simplified. Those are the figures every investor now plans around.

How the tax got here

Capital gains tax on shares is not new in Nepal and the history explains why finality mattered so much. For years the regime sat at 5% on long-term holdings and 7.5% on short-term ones withheld at the point of sale by the broker and the depository. On paper it looked simple. In practice it was anything but because the withholding did not always settle the matter.

The confusion came from how the gain interacted with the rest of a taxpayer's income. For a salaried investor or a business owner, a large realised gain could under some readings of the law be added to total income and reassessed at personal rates with the withholding treated as a mere advance. Few investors knew with confidence whether a profitable year would end with a clean slate or a fresh demand from the tax office months later. Brokers fielded the questions and could not always answer them. The uncertainty was a real deterrent, and it fell hardest on the largest, most committed investors, the ones with gains big enough to push them up the brackets.

So when the trading community asked for capital gains to be made final, they were not asking for a tax cut. They were asking for certainty: a single, known rate, settled at sale, with nothing to follow. That is exactly what the budget delivered, and it is why the reform drew genuine praise even from investors who disliked the rate rise that came stapled to it. Understanding that history is the key to reading the budget honestly. The good part answers a long-standing, legitimate complaint.

The bad part is a choice that did not have to be bundled with it. Finality and the rate are separable. The government could have made the tax final at the old 5% and 7.5% and delivered an unambiguous win. It chose instead to use the goodwill of the popular reform as cover for the unpopular rise which is ordinary politics but it means the celebration and the complaint are really about two different decisions that happened to share a sentence.

First, give the budget its due

A fair argument has to start by conceding what is right, and a good deal here is right. Finality is not a cosmetic change. Under the old system, the 5% or 7.5% withheld at sale was, for many investors, only the beginning. Depending on their other income and how the rules were read, a large realised gain could be drawn into total taxable income and taxed again at personal rates that ran as high as 39%. The withholding was a down payment, not a settlement. That uncertainty discouraged exactly the kind of investor the market needs: the one with a large, long-held position who fears that selling will trigger an unpredictable tax bill.

Making the tax final removes that fear. The rate you see is the rate you pay. For a high-income investor who might previously have faced bracket escalation, finality at 7.5% is not a tax rise at all; it is a tax cut, and a meaningful one. That is a genuine improvement to the market's plumbing, and the budget deserves credit for it after years of investors asking for precisely this.

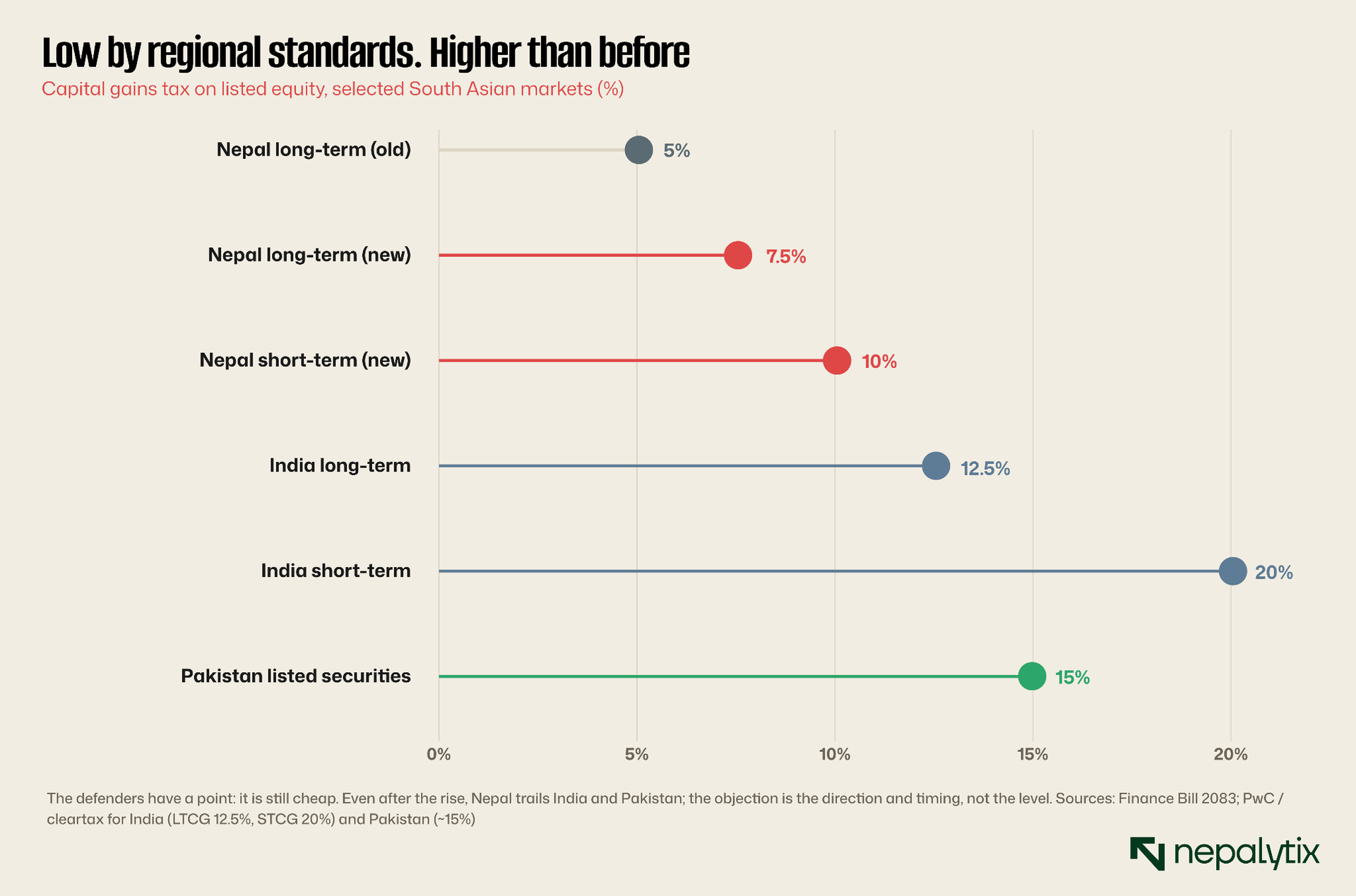

The defenders have a second point and it is also fair. Even after the rise, Nepal's capital gains tax is low by the standards of the neighbourhood. India taxes long-term equity gains at 12.5% and short-term gains at 20%. Pakistan taxes listed securities at around 15%. Nepal's new 7.5% long-term rate sits comfortably below both. A chartered accountant quoted after the budget made the point that the rate remains among the lowest in South Asia signalling a stable and predictable policy environment and on the level of the rate he is correct.

So this is not a story about a confiscatory tax grab. The rate is mild, and the finality is a real gift. If the argument stopped there, the budget would deserve applause. It does not stop there, because a rate is not just a level. It is also a direction and a timing, and on both the budget chose badly.

Holding longer didn't earn a bigger reward

Look again at which rate rose more. The long-term rate, the one that applies to investors who hold for more than a year, went up by half, from 5% to 7.5%. The short-term rate went up by a third. In a tax system that is supposed to reward patient capital over speculation, the budget raised the tax on patience faster than the tax on trading.

The gap between the two rates is what signals the reward for holding. Before the budget, a long-term holder paid 2.5 percentage points less than a short-term trader, 5% against 7.5%. After the budget, the long-term holder still pays 2.5 points less, 7.5% against 10%. The absolute incentive to hold did not improve at all. The budget simply lifted the whole structure, leaving the relative reward for patience exactly where it was while making it more expensive to be an equity investor of any kind. If the goal were to encourage long-term ownership in a market dominated by short-term churn, widening that gap would have been the obvious lever. The budget left it untouched.

There is a quiet regressivity in the combination, too. Finality, as we have seen, is most valuable to the largest investors, the ones who previously risked bracket escalation on big gains. The rate rise, by contrast, lands on everyone who realises a gain, including the small long-term holder who only ever paid the 5% withholding and never worried about brackets at all. For that investor, finality changes nothing, because the withholding was already the end of it. The 50% rate increase, on the other hand, is the whole story. So the budget handed its relief disproportionately to the large and its rise disproportionately to the small. That is a strange distribution for a government that talks about widening participation.

The defenders of the change rarely engage with this distribution because it is uncomfortable. It is easy to argue that the investing class can afford to pay a little more; it is harder to explain why the little more should fall most heavily on the small, long-term holder while the simplification was packaged with flows mostly to the large. A genuinely progressive change would have done the reverse, easing the burden on the small saver building a position over years and asking more of the large, fast trader. The budget got the incident backwards.

None of this is catastrophic at the level of any single trade. Half a percentage point here, a couple there. But tax design is about signals as much as sums, and the signal this sends is the opposite of the one the rest of the budget claims to want.

Higher taxes create a reason not to sel

Beyond the level and the timing, capital gains tax carries a behavioural cost that rises with the rate and it is one a thin market can least afford. The cost is lock-in. A tax charged only when you sell gives every investor a reason not to sell because realising a gain crystallises a bill that holding defers indefinitely.

In a deep, liquid market lock-in is a manageable nuisance. In a market as thin as Nepal's where daily turnover runs to only single-digit billions of rupees and a large share of demat accounts never trade at all, it is a real drag on the one thing the exchange most needs. Every investor persuaded to sit on a position rather than sell it is a unit of supply withdrawn from a market already starved of float. Raising the rate raises the incentive to sit still. A policy ostensibly aimed at a more dynamic market makes its participants less willing to trade.

The 365-day boundary between the short-term and long-term rates adds a second distortion. With short-term gains now taxed at 10% and long-term at 7.5%, an investor sitting on a gain near the one-year mark has a sharp incentive to wait out the calendar rather than sell on the merits, holding a position they would otherwise exit simply to drop a tax bracket. The tax starts making timing decisions that should belong to the investor and the fundamentals. Small distortions, again, but they accumulate in a market where genuine, fundamentals-driven trading is already scarce.

Lock-in also interacts badly with the inflation problem. Because the tax is unindexed and charged on the nominal gain, the longer an investor holds to defer the bill, the larger the inflationary component of the eventual gain becomes, so the deferral that lock-in encourages quietly enlarges the phantom gain the state will one day tax. The investor is pushed to hold and holding makes the eventual tax less fair. It is a small, circular cruelty buried in the mechanics and raising the rate tightens every loop of it.

There is a clean way to avoid all of this: keep the rate low enough that the incentive to freeze is weak. Nepal had the low rate and chose to raise it. Every percentage point added to a capital gains tax buys a little more lock-in, a little less turnover and a little less of the liquidity the exchange is desperate to build. For a market this shallow, that trade was not worth making for the sums involved and it runs directly counter to the budget's own stated wish for a more active, more liquid NEPSE.

A higher toll on a road to nowhere

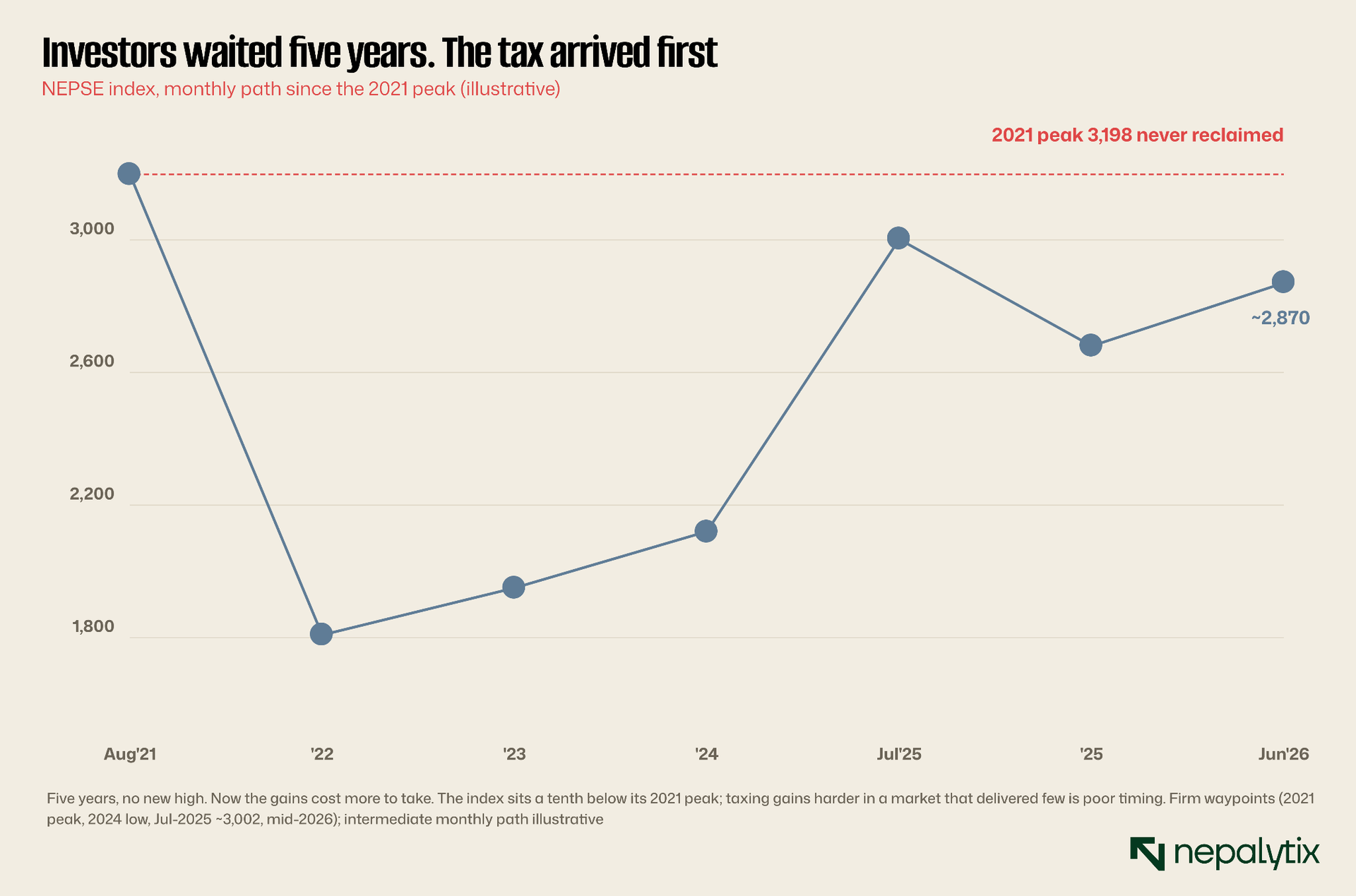

Timing is the second mistake and it is the more glaring one. You raise a tax on gains when there are gains to tax. Nepal's market has not been producing them.

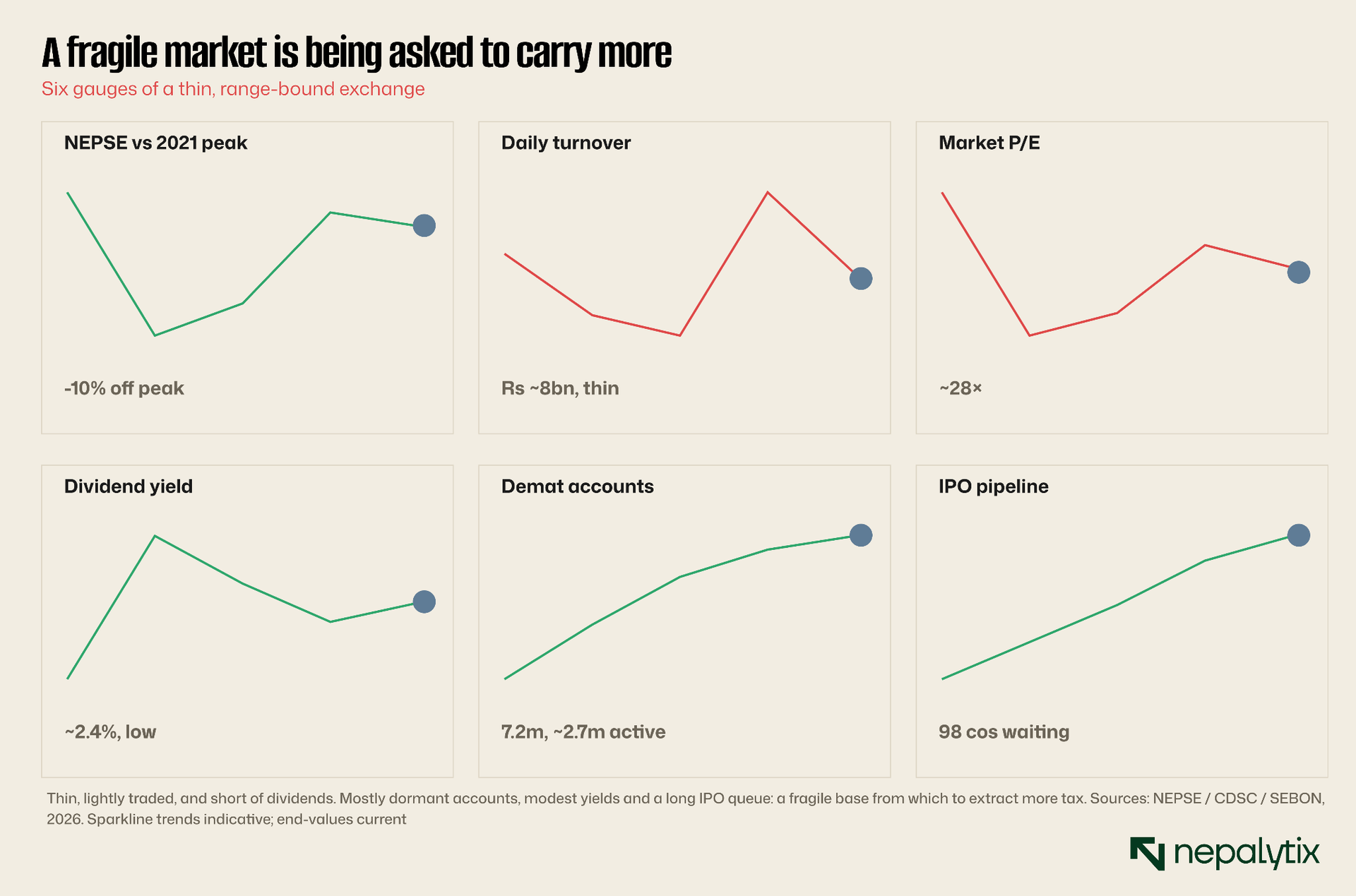

The NEPSE index reached an all-time high of 3,198 points in August 2021. Nearly five years later it has never reclaimed that level. It collapsed toward 1,800 in the bear market that followed, clawed back to briefly touch 3,002 in mid-2025, and has since settled into a range in the 2,700 to 2,900 band. An investor who bought the index at any point near that 2021 peak and held has, in nominal terms, lost money or barely broken even across half a decade. This is not a market delivering a windfall that the state has a strong claim to share. It is a market that has frustrated the people in it.

Raising the tax on capital gains in that context is awkward at best. The gains being taxed more heavily are for many holders, not gains at all but recoveries, the slow grind back toward a purchase price set years ago. The chart shows the shape of it: a peak, a slump, a partial recovery, and a long plateau beneath the line that has not been crossed since 2021. A government raising the levy on profits taken from this market is, for a large share of investors, raising the levy on getting back to even.

Contrast this with how painless the same rise would have felt in a rising market. In a bull run, when investors are sitting on real, comfortable gains, a half-point on the tax is barely noticed and easily justified; the state shares in a prosperity everyone can see. Imposed instead on a market that has frustrated its participants for five years, the same half-point reads as the government reaching for more from people who have made little. The level of the rate did not change between those two worlds. Its reception, and its fairness, did.

The defenders will say a rate set today applies to the gains of tomorrow, and that the market will eventually rise. Perhaps. But the policy was read the moment it was announced and the message investors heard was that the cost of participating just went up while the market that is meant to reward them has been flat for five years. Sentiment is not a footnote in a market this thin. It is most of the story.

Taxing inflation and calling it wealth

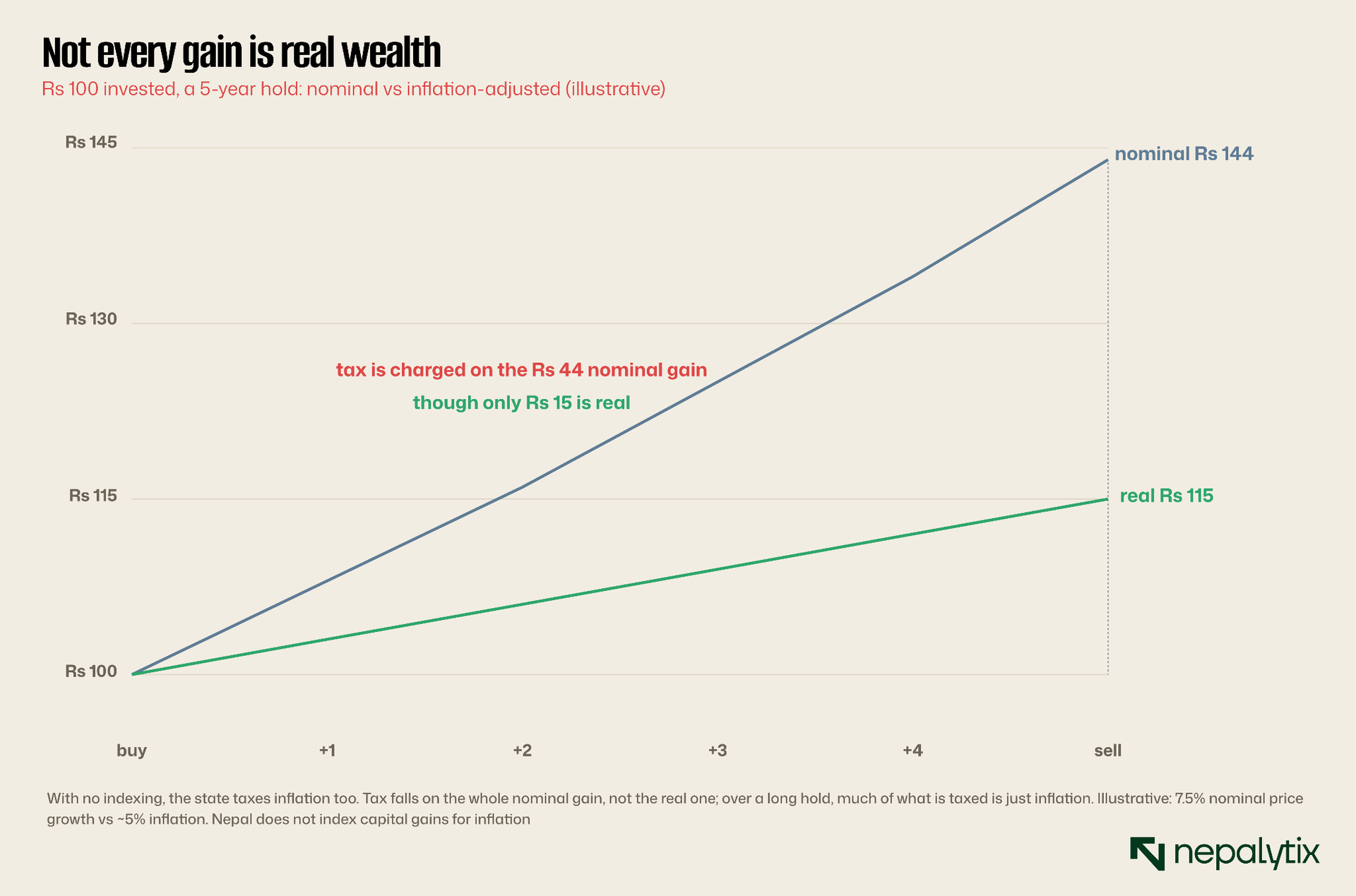

Here is the structural flaw that survives even if the market does recover: Nepal taxes nominal capital gains with no adjustment for inflation. That means a portion of every long-term gain the state taxes is not real wealth at all. It is the erosion of the rupee, dressed up as profit.

The arithmetic is unforgiving over a long hold. Suppose an investor buys a share for Rs 100 and sells it five years later for Rs 144, a nominal gain of Rs 44. If prices rose over those five years, as they always do, a large part of that Rs 44 is simply the higher price level, not a real increase in purchasing power. In real terms the investor might be better off by only Rs 15. Yet the tax is charged on the full Rs 44. The state taxes the inflation it presided over as if the investor had earned it. The longer the hold, the worse the distortion, which means the structure quietly penalises exactly the long-term investor the system claims to favour.

The chart illustrates the wedge: a nominal line climbing to Rs 144 and a real line, after inflation, reaching only Rs 115, with the tax charged against the gap between Rs 100 and Rs 144 rather than the real gain above it. India, for all the noise around its own capital gains changes, has wrestled with this through indexation for decades, allowing investors to uplift their purchase cost by an inflation index before computing the gain. Nepal offers no such relief. A budget that wanted to be fair to long-term investors, rather than merely final with them, would have started here.

This is not a plea for zero tax. It is a plea for taxing the right number. A capital gains tax that falls on real gains is defensible. One that falls on inflation is a stealth wealth tax wearing a capital gains label, and it gets heavier the longer and more loyally you hold.

For now, low inflation hides the problem. With consumer prices rising under 2%, the gap between nominal and real gains is currently modest, and the distortion is small. But that is luck, not design, and it will not last. Nepal's inflation has historically run in the mid-single digits and has spiked higher in bad years; the moment it returns to those levels, the unindexed tax starts biting hard on phantom gains again. A tax structure that is only fair when inflation happens to be low is not a fair structure. It is a fair-weather one, and the weather in Nepal has rarely stayed fair for long.

The budget is sending mixed signals

Now place the tax change next to everything else this same budget promised the capital market because the contradiction is what makes the rate rise more than a quibble.

In the very same speech, the government announced the most ambitious modernisation of the Nepal Stock Exchange in its history. Intraday trading, long demanded, is to be introduced. Short selling and derivatives are coming in phases. Listed companies will be allowed to issue depositary receipts to raise money abroad. Non-resident Nepalis are to be let into the secondary market for the first time. The central bank, in support, cut the mandatory holding period for shares bought by banks from a year to six months. The entire thrust of the policy is to pull more participants and more capital onto the exchange, to deepen a market everyone agrees is too thin.

And then, in the same document, the government raised the cost of being there. This is the contradiction at the heart of the budget's treatment of the market. One set of measures is designed to widen the bridge and invite more people across it. Another raises the price of the crossing. The dashboard of the market the tax now leans on tells you why this matters: a benchmark still below its 2021 peak, daily turnover of only single-digit billions of rupees, dividend yields around 2%, more than seven million demat accounts of which barely a third are active, and a queue of nearly a hundred companies waiting to list. This is a shallow, lightly traded, under-rewarded market. The right policy for such a market is to lower the friction of participating, not to raise it. The budget did both, and the two halves work against each other.

It is possible the government simply did not see the tension, treating the tax line and the market-reform line as separate files written by separate desks. That is the charitable reading. The less charitable one is that the modernisation is the announcement and the tax rise is the substance, and that the new instruments will arrive slowly while the higher charge arrives on day one.

The contradiction is sharpest in the treatment of non-resident Nepalis. The budget makes a point of opening the secondary market to the diaspora for the first time, courting their savings as a new source of capital for Nepali companies. These are exactly the investors with the most options, able to deploy their money in deeper, better-run markets abroad. Inviting them in while raising the tax they will pay on the way out is not how you win a competition for mobile capital. The diaspora investor weighing Nepal against Dubai or New York will notice both the invitation and the cost of entry, and the cost just went up.

The kinder interpretation is that these are early days, and that the modernisation, once delivered, will more than offset a half-point on the tax. That may prove true over years. But markets priced the announcement, not the eventual rollout, and what was announced was a clear, immediate rise set against reforms that are, for now, only promises. Intraday trading and derivatives have been talked about in Nepal for the better part of a decade. The higher rate takes effect with the new fiscal year. An investor comparing a concrete cost today against a contingent benefit tomorrow will discount the benefit, as investors always do, and act on the cost.

The tax burden is larger than it looks

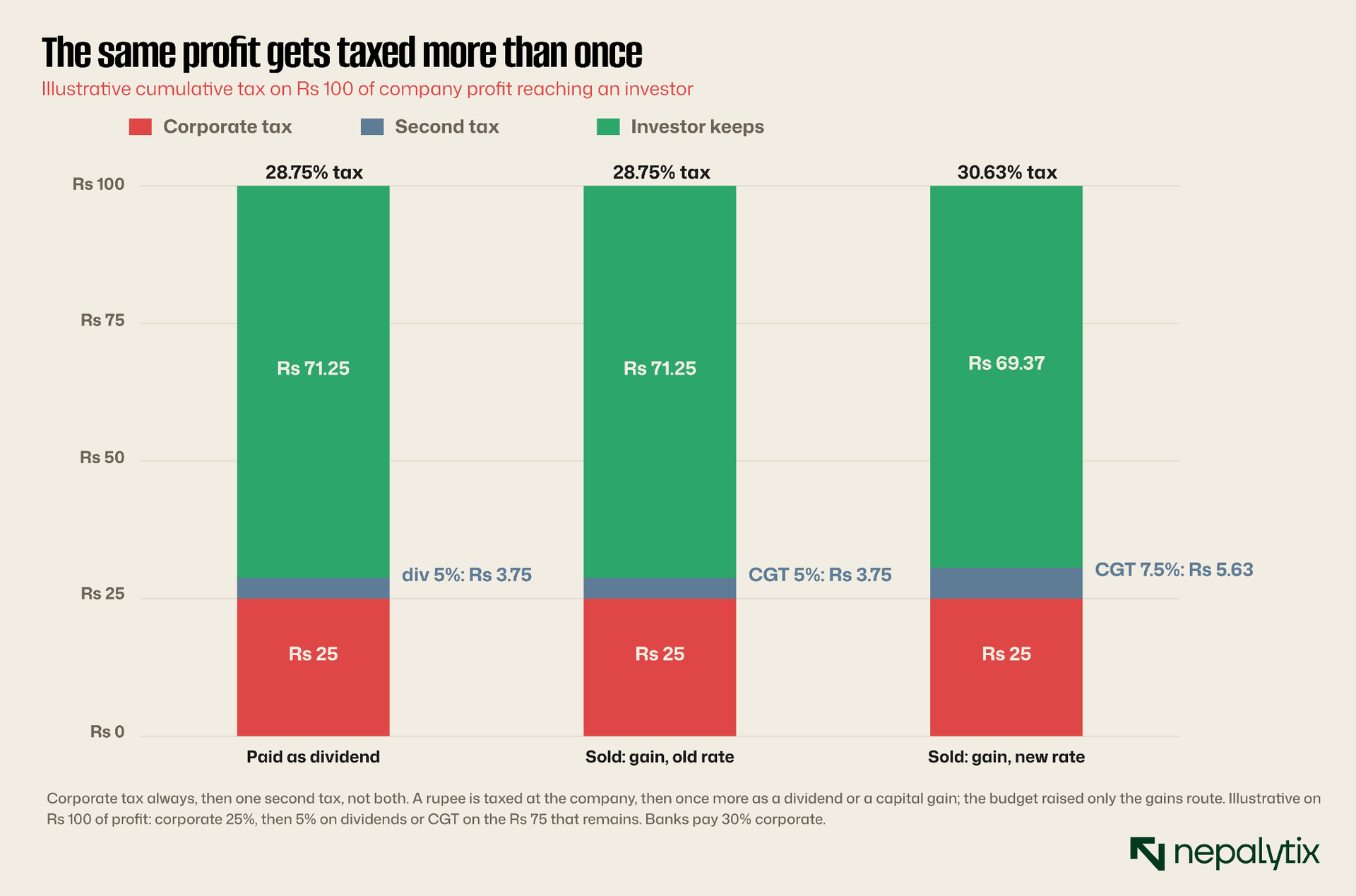

There is a further reason to be careful about nudging the capital gains rate up and it is one the budget debate almost entirely ignored: capital gains tax is the third tax on the same money, not the first.

Follow a rupee of company profit to the investor's pocket. The company earns it and pays corporate income tax, 25% for most firms and 30% for banks, insurers and a few others. What survives is distributed and the dividend is taxed again, at 5%. If instead the value is retained and shows up as a higher share price, the investor who sells pays capital gains tax on the increase. Each of these is defensible alone. Stacked, they mean the effective tax on equity returns in Nepal is considerably higher than any single headline rate suggests and the budget has just thickened the final layer.

The chart stacks the layers on a notional Rs 100 of company profit. Corporate tax takes the first slice, dividend tax the next, capital gains tax another and what reaches the investor is the remainder, a remainder the budget has now trimmed. The point is not that any one of these taxes is wrong. It is that a government deciding whether to raise the capital gains rate should be looking at the whole stack, not the top slice in isolation, and should be asking whether a country that desperately needs domestic equity capital wants to tax the formation of it three times over and then raise the third charge.

This is the unglamorous heart of the case. Equity is the riskiest capital a saver can supply, ranking behind every lender if the company fails. A tax system that takes three bites of the return it offers, and tightens its grip on the last one, is quietly telling savers to keep their money in a fixed deposit, which is precisely where, as our liquidity work this week showed, far too much of it already sits.

The comparison with deposits is the one that should worry policymakers most. Interest on a fixed deposit is taxed once, at a flat 5% withholding, and nothing more. Equity returns, as we have seen, are taxed up to three times. So a saver choosing between the two faces a tax code that treats the safe, unproductive option far more gently than the risky, productive one. That is precisely backwards for a country that needs its savers to fund factories and hydropower rather than park money in the banking system. Every notch the capital gains rate rises widens the gap and nudges the saver back toward the deposit.

A small revenue gain at a larger market cost

If the rate rise carried real money for the Treasury, there would at least be a fiscal case to weigh against the market damage. It does not.

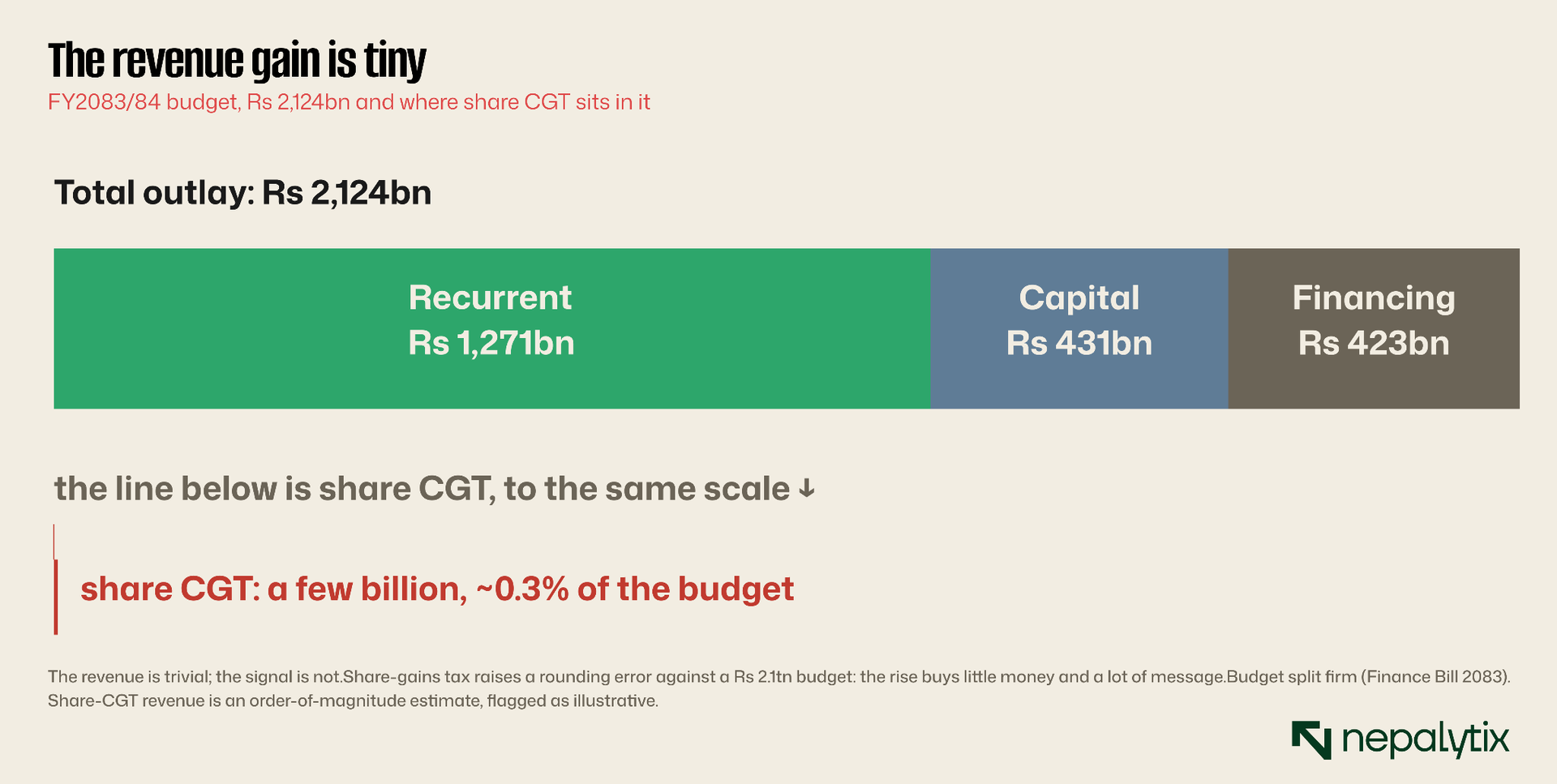

Capital gains tax on shares is a trivial line in the public accounts. Against a total budget outlay of Rs 2,124 billion, the revenue raised from taxing share gains is a rounding error, a few billion rupees in a good year and less in a flat one like this, trivial against the whole. Lifting the long-term rate from 5% to 7.5% does not change that order of magnitude; it nudges a small number slightly higher. The chart sets the share-CGT take against the budget it sits inside, and the sliver is barely visible at the same scale as the Rs 1,270 billion of recurrent spending or the Rs 431 billion of capital spending it is meant to help fund.

This is what makes the move hard to defend on its own terms. A tax change that raised serious revenue could justify some friction; the state has bills to pay. A tax change that raises almost nothing cannot. The rise buys the Treasury very little money and sends the market a clear, discouraging message, which is the worst possible ratio for a policy: minimal gain, maximal signal. If the government needed the revenue, there were far larger and less distorting places to find it. If it did not, there was no reason to unsettle a fragile market for a sum this small.

The fiscal incoherence is worth stating plainly. The same budget cut the top rate of personal income tax from 39% to 29% and doubled the tax-free threshold to Rs 1 million giving up far more revenue than the capital gains rise could ever recover. So the government deliberately forwent a large sum on income tax and then scrambled after a tiny one on share gains. If the concern were the deficit, the income tax cut was the place to look; if it were fairness, a market flat for five years was a strange target. The numbers do not add up to a revenue strategy so much as a political gesture.

The most likely explanation is that the rate rise was not really about revenue at all. It was about being seen to tax the rich, the investing class, in a budget that simultaneously cut the top personal income tax rate from 39% to 29% and doubled the income tax exemption threshold. The capital gains rise is the political counterweight, the bit that lets the budget say it asked something of the wealthy. As politics that may be shrewd. As economics it taxes the wrong thing, at the wrong time, for almost no money.

What would actually work

Criticism is cheap without an alternative, so here is what a budget genuinely trying to help this market would have done, keeping the one good idea it had.

Keep finality. It is the right reform and investors wanted it. The certainty it provides is worth more to the market than the rate is worth to the Treasury and it should stay regardless of what happens to the rate. Then, instead of raising the rate across the board, do three things. Index long-term gains for inflation, so the state taxes real wealth rather than the erosion of the rupee, which would at a stroke make the tax fairer to exactly the patient investors the market needs. Widen the gap between the long-term and short-term rates, rather than lifting both in lockstep, so the code actually rewards holding over churn instead of merely talking about it. And align the tax with the modernisation agenda: if the goal is to pull non-resident Nepalis and new retail money onto the exchange, the rate they meet on arrival should be falling, not rising.

A more radical version would zero-rate genuine long-term holdings entirely, say gains on shares held more than three or five years, as several deeper markets do to encourage exactly the stable, long-horizon ownership that a thin exchange lacks. The revenue forgone would be negligible, for the reasons the previous section laid out and the signal would be powerful: hold for the long term and the state takes nothing. In a market where most accounts are dormant and most activity is speculative, that is a signal worth sending.

Even short of that, a simple annual exemption would have protected the small investor at trivial cost. India shields the first Rs 1.25 lakh of long-term equity gains each year before any tax applies, so the genuinely small saver pays nothing and only sizable gains are taxed. Nepal has no such threshold; the tax bites from the first rupee of gain. A modest annual exemption would have removed most small investors from the tax net entirely, simplified administration, and cost the Treasury almost nothing, since small investors contribute little of the revenue. That the budget raised the rate without adding such a floor tells you how little the small holder figured in the calculation.

None of these is expensive because the tax raises so little to begin with. That is the quiet tragedy of the budget's choice. It had room to be generous to investors at almost no fiscal cost, and it had one genuinely good reform in hand. It chose instead to pair that reform with a rate rise that helps the large, hurts the small, taxes inflation, discourages patience and raises a rounding error, in a market that has not made anyone money in five years.

The honest objection

A column like this owes the other side a fair hearing, so here is the strongest case for what the government did. The state's revenue base is genuinely narrow, its tax-to-GDP ratio low, and a finance minister has every right to ask the investing class to contribute a little more, especially in a budget that cuts taxes substantially for salaried workers and the middle class. A rate that is still among the lowest in South Asia is hardly punitive, and the finality reform is a real and lasting gift that will outlast any grumbling about half a percentage point. On this reading, investors are being asked for a modest contribution in exchange for a major simplification, and they should take the deal.

That case is reasonable and a reader who weighs the simplification more heavily than the rate may fairly conclude the budget got the balance about right. The disagreement is one of judgement, not of fact. But the judgement here rests on three things the defenders tend to skip: that the rise lands hardest on long-term holders and small investors, that it arrives in a market that has been flat for five years and that it contradicts the same budget's loud ambition to deepen participation. Weigh those and the deal looks worse than it is sold as.

The deepest point is the simplest. A country that needs its own citizens to fund its own companies, because foreign capital is scarce and bank credit is mispriced, should make equity ownership easy, cheap and rewarding. This budget made it simpler, which is good, and dearer, which is not. It got the structure right and the rate wrong. Fix the rate, keep the structure, and index the thing for inflation while you are at it, and Nepal would have a capital gains tax worth defending. As it stands, it has one worth arguing about, which is why we have.

One last concession is fair. Tax policy is never made in a laboratory, and a finance minister juggling a narrow revenue base, a restless electorate and a long list of competing demands will not optimise every line. Judged against that messy reality, a small rise in a low tax, bundled with a genuine simplification, is hardly the worst thing in a Rs 2.1 trillion budget. The criticism is not that the change is a scandal. It is that it was an unforced error, a needless bit of friction added to a market the same budget was trying to help, when getting it right would have cost nothing. Good policy is often just the avoidance of cheap mistakes and this was a cheap one.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.