The Hydropower Diversification Illusion

Hydropower makes up nearly one-third of NEPSE-listed companies, yet most stocks share the same monsoon-driven risks, buyer, and infrastructure.

Hydropower now accounts for nearly a third of all listed companies on NEPSE. Investors see dozens of stocks, dozens of rivers and dozens of opportunities. But beneath the surface, most of them are exposed to the same monsoon, the same buyer and the same risks.

Hydropower appears to offer investors remarkable choice. There are more than ninety listed companies, spread across different rivers, districts and developers. But most of them operate under nearly identical conditions. They depend on the same monsoon cycle, sell electricity to the same buyer and rely on the same transmission network. The diversification investors see is often far smaller than it appears.

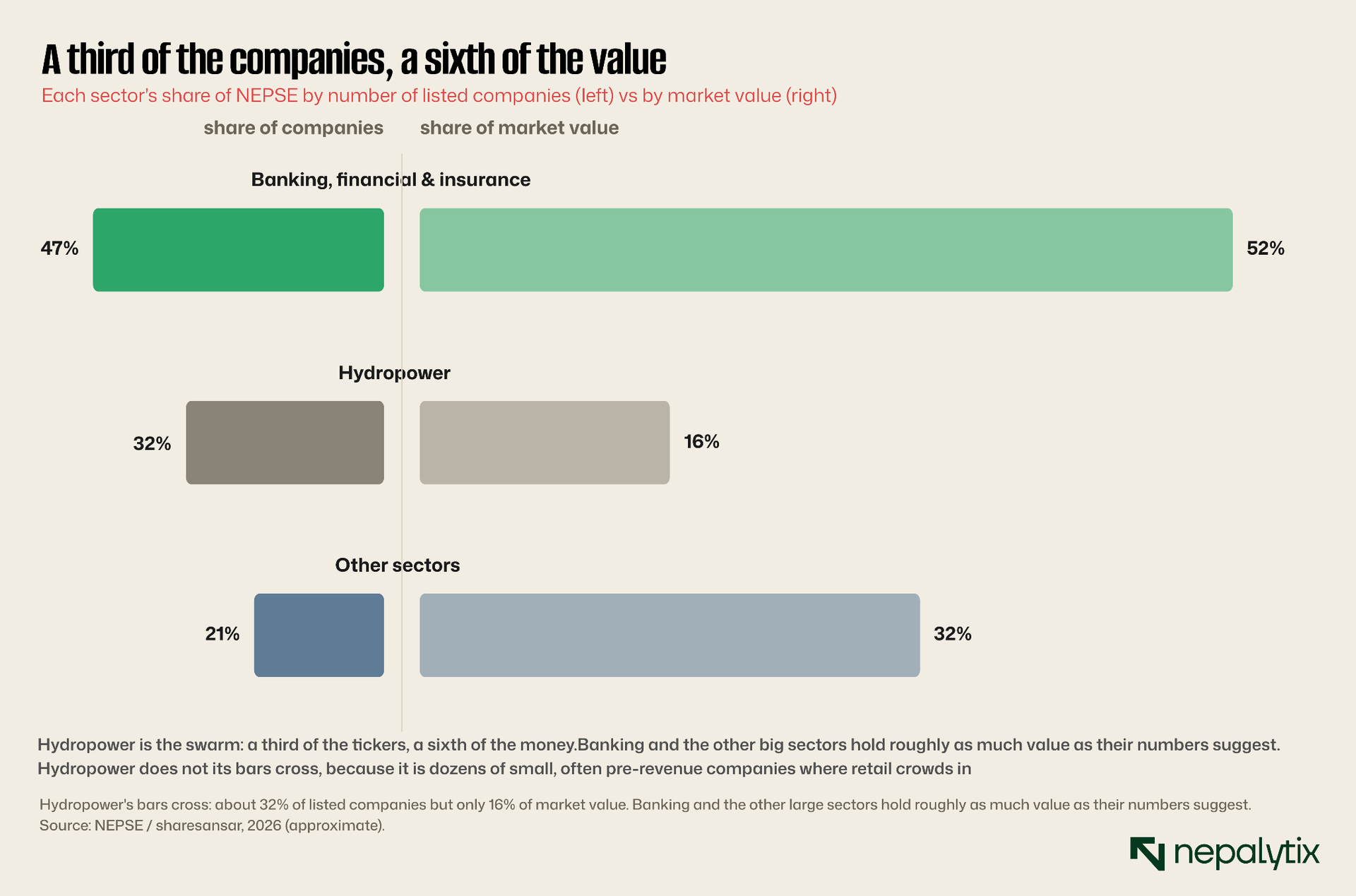

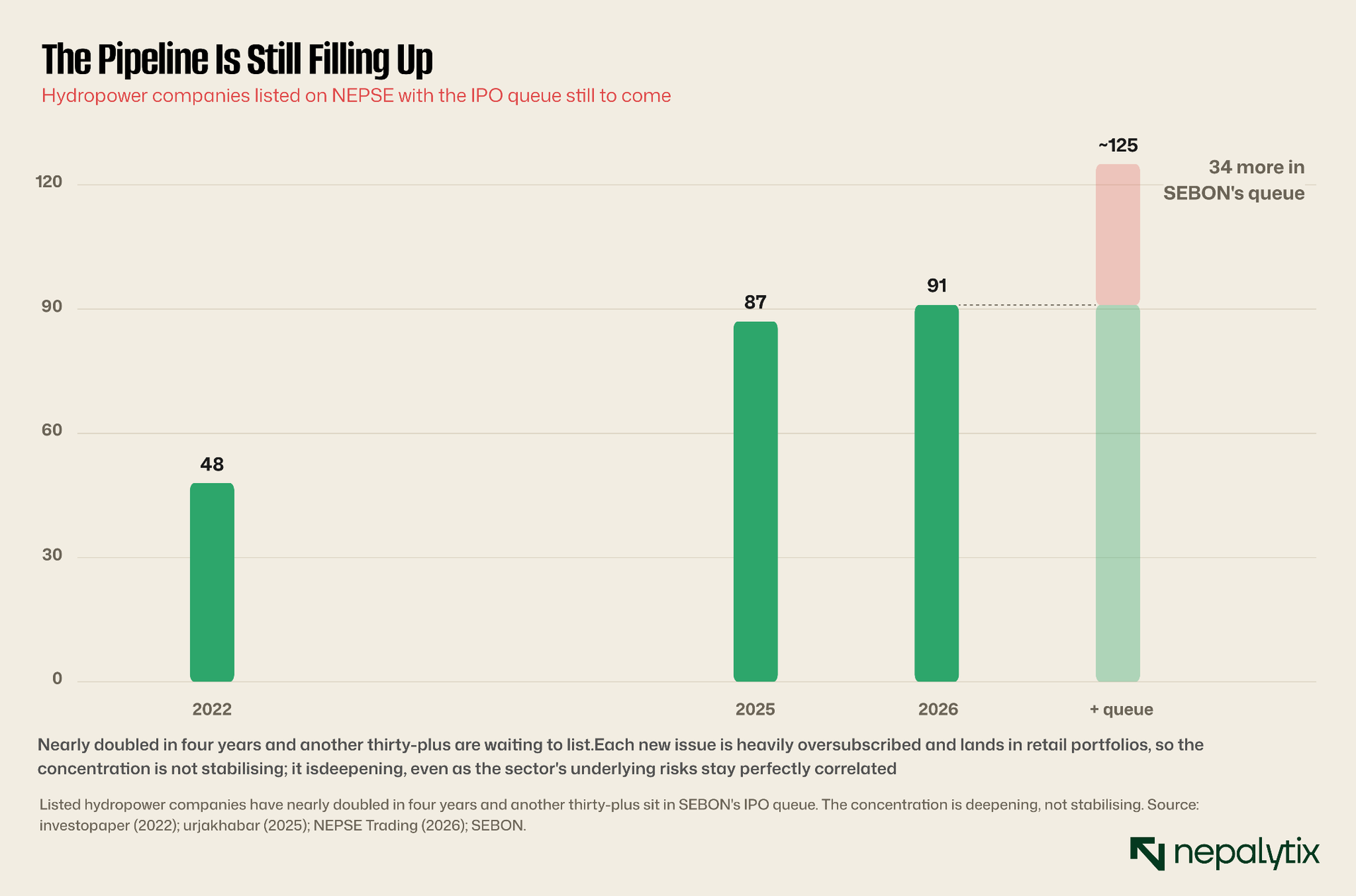

Start with a number that should give Nepal's retail investors pause: of the 284 companies listed on the Nepal Stock Exchange, roughly ninety-one are hydropower close to one in every three names on the board. No other real-economy sector is anywhere near. On paper, that looks like breadth. In practice, it may be one of the most concentrated themes in the market. On the surface that reads as breadth: dozens of companies, dozens of rivers, dozens of separate stories to choose from. Underneath, it is the opposite of breadth.

The tell is the gap between count and value. Hydropower is about 32 percent of the listed companies but only 16 percent of the market's value. Banking, financial and insurance names are the mirror image of fewer relative to their weight, because each is large. Only hydropower shows this lopsided shape, and the shape has a meaning: the sector is a crowd of small companies. Its combined market capitalisation around Rs 701 billion is real money but spread across ninety-one names it averages a fraction of what a single large bank carries.

Small companies are where retail investors concentrate. The share prices are low, the IPOs are cheap to enter and the stories are easy to follow: a new dam, a commissioning date. A large share of these ninety-one are still building their projects with no generation and no revenue yet; their prices move on construction milestones rather than earnings. That is not owning a cash flow. It is underwriting a construction schedule and often pricing it as though everything will go right.

Why Most Hydropower Stocks Rise and Fall Together

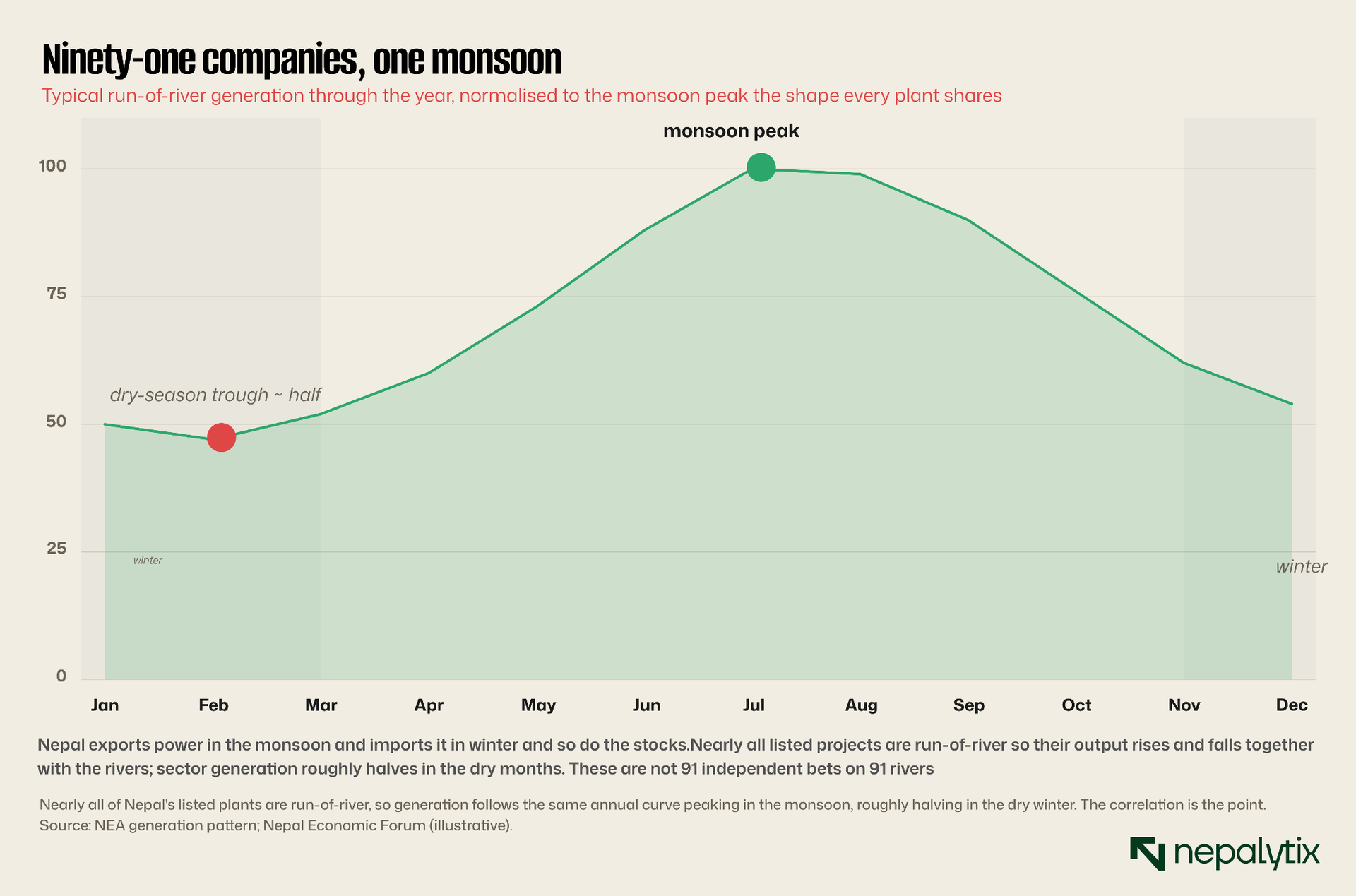

This is what the count-and-value gap only hints at, and it is the real signal. Nearly every listed hydropower company in Nepal runs a run-of-river plant, it generates from the river's flow rather than a large storage reservoir. That design is cheap to build and clean to run, but it chains every one of them to the same master variable: the water. When the monsoon swells the rivers from June to September, the whole sector generates at full tilt. When the dry winter comes and the rivers shrink, sector generation roughly halves. Every plant, on every river, breathes in and out together.

A portfolio of ten hydropower stocks is not ten bets on ten rivers. It is one bet on the monsoon, bought ten times.

There is, in theory, a hedge and the market barely owns it. A storage or peaking plant holds water behind a dam and releases it in the dry months, smoothing the seasonal swing; a portfolio that mixes those with run-of-river projects would genuinely diversify the hydrology. But storage dams are expensive, slow and politically fraught so Nepal has built only a handful and almost none of the ninety-one listed names is one. Investors may own different ticker symbols, but many of the underlying risks remain identical. The companies look different on a portfolio screen. Their economics are often remarkably similar.

The correlation does not stop at the weather. Almost all of these companies sell their electricity to a single buyer, the Nepal Electricity Authority under power-purchase agreements whose rates the government sets and can renegotiate. They lean on the same transmission grid where one missing line can strand a finished plant's output. They face the same licensing regime, the same local-consent frictions, the same competition from Indian imports in the months they can least afford it. Spreading money across ninety-one of them buys a great many tickers and almost none of the underlying diversification.

And the master variable is becoming less reliable, not more. Roughly two-thirds of the flow in Nepal's rivers comes from rainfall and about a third from glacial and snow melt, a balance a warming climate is quietly tilting. As Himalayan glaciers retreat, the dry-season baseflow that keeps winter output from collapsing is thinning, while erratic monsoons swing the wet-season peak around year to year. In one recent dry year, national output fell some twenty percent below even its normal winter level. For a cohort whose entire revenue base is the water in the rivers, a destabilising climate is a direct, correlated hit to ninety-one income statements at once.

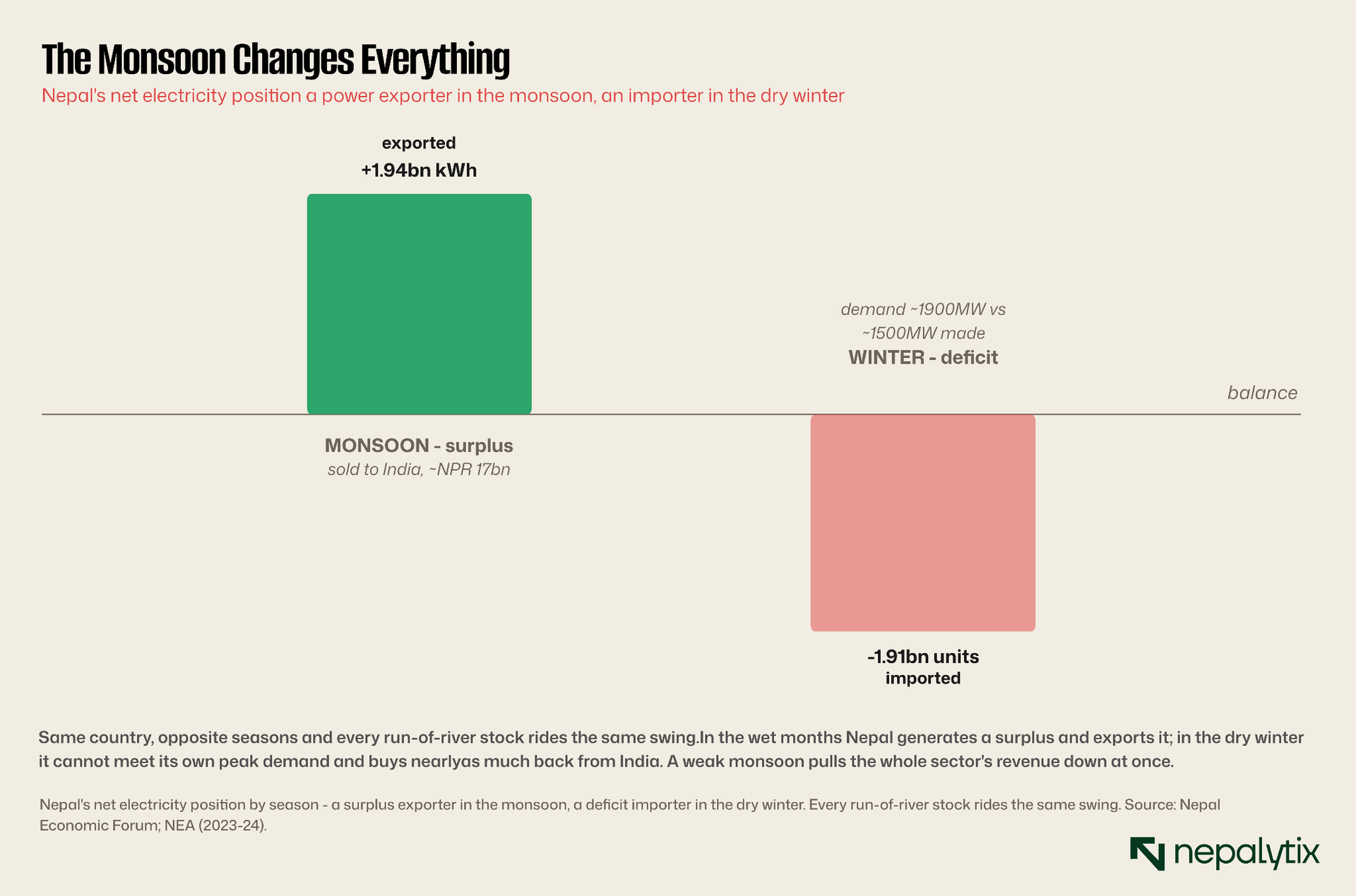

Nepal's Power Surplus Is Seasonal

The swing is large enough to flip the entire country's power balance. In the wet season Nepal generated a surplus and exported electricity to India around 1.94 billion units last year, worth some Rs 17 billion with the figure expected to climb as new lines open. In the dry winter the same country becomes a net importer, buying nearly as much back from India as it sold because domestic output cannot meet a peak demand of roughly 1,900 megawatts against barely 1,500 generated at home.

The same seasonal pattern shows up in company earnings. The single variable that turns Nepal from exporter to importer of the water in the rivers is the same variable that turns ninety-one income statements from full to half and back again. There is no internal hedge inside the sector. A weak monsoon, or a drought year of the kind a warming climate is making more frequent, does not nick one company; it pulls the whole cohort's revenue down together, in the same months, on the same rivers.

Nor does the export story neutralise the swing if anything it sharpens it. Nepal's landmark agreement to sell India up to 10,000 megawatts over the coming decade is built almost entirely on wet-season surplus: it monetises the monsoon glut handsomely, but does nothing for the winter trough, when there is little spare power to sell and a domestic deficit to cover. A poor monsoon is then doubly painful. Less surplus to export at the very moment more must be bought back. The cross-border market deepens the upside; it does not hedge the season that actually threatens the sector's cash flows.

The Trade is Becoming More Crowded

If this were a fixed feature of the market it would be one thing. It is not, it is intensifying. Listed hydropower names have gone from about 48 in 2022 to 91 today and SEBON's IPO pipeline holds another 34 hydropower companies waiting to float more than any other sector by number. The flow runs one way: more hydropower paper into more retail portfolios at richer prices with the same correlated risk underneath every certificate.

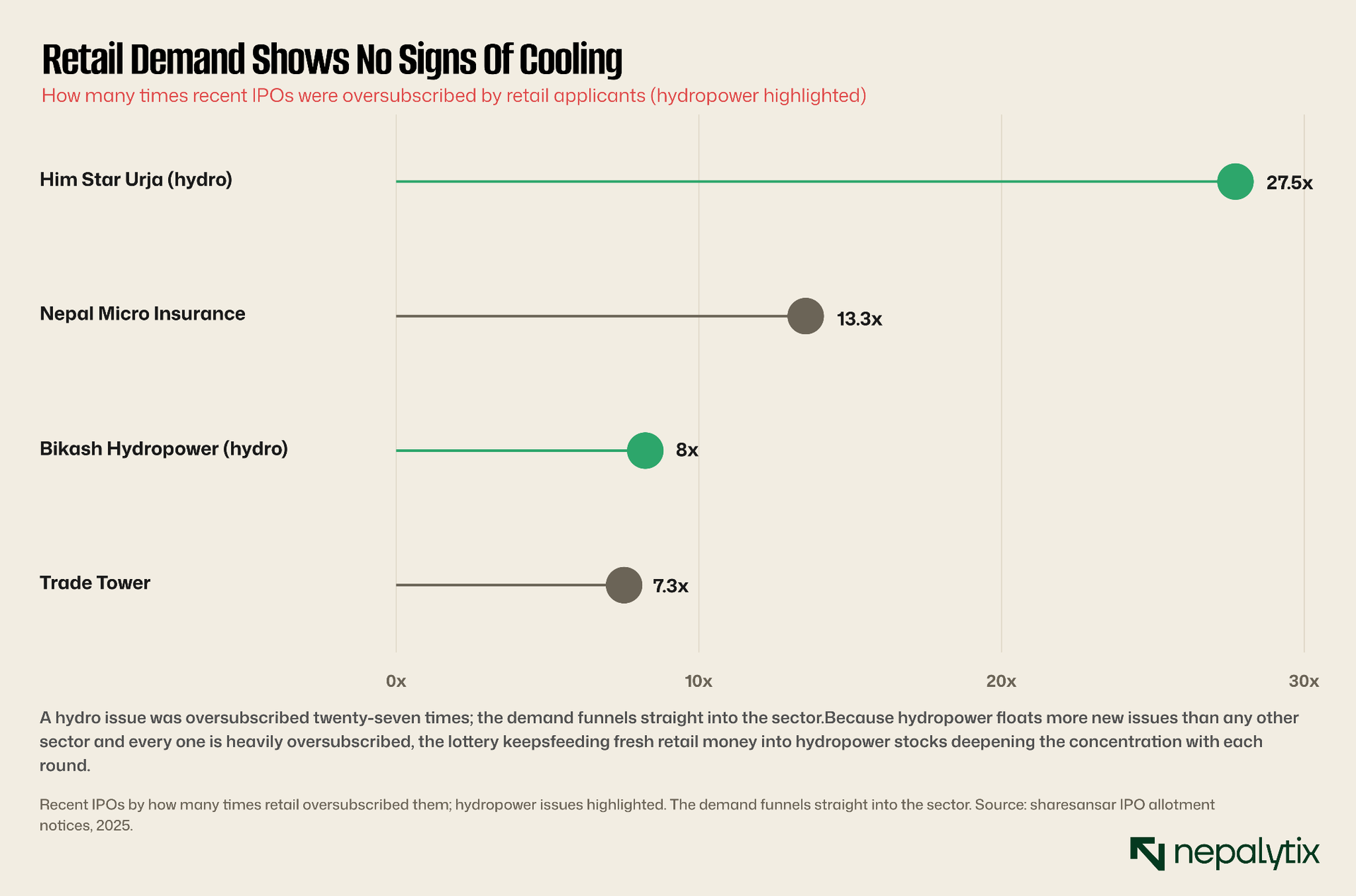

The mechanism is the IPO lottery. A run-of-river issue typically priced at the Rs 100 par, costs as little as Rs 1,000 to apply for, and if the lottery smiles has often doubled or tripled on its first days of trading. Him Star Urja, a tiny hydropower issue, was oversubscribed more than twenty-seven times; Bikash Hydropower, eight. For a saver shut out of an overheated property market and earning little on a bank deposit, that is an almost irresistible proposition and it requires no view on a cash flow at all. Institutional investors are often far more selective, particularly when projects are still under construction. So the float drifts, issue by issue into the portfolios least able to absorb a sector-wide shock.

The timing sharpens it. Online trading accounts have multiplied roughly nine-fold since 2020, to more than six million, just as money has rotated out of a stalled property market and away from thin deposit rates into the exchange. NEPSE's recent rallies have been led, week after week by hydropower turnover. The conditions that built the swarm are not cooling; they are running hot which is exactly when a concentrated position is easiest to keep adding to and hardest to see.

The Opportunity is Real. So Is The Optimism

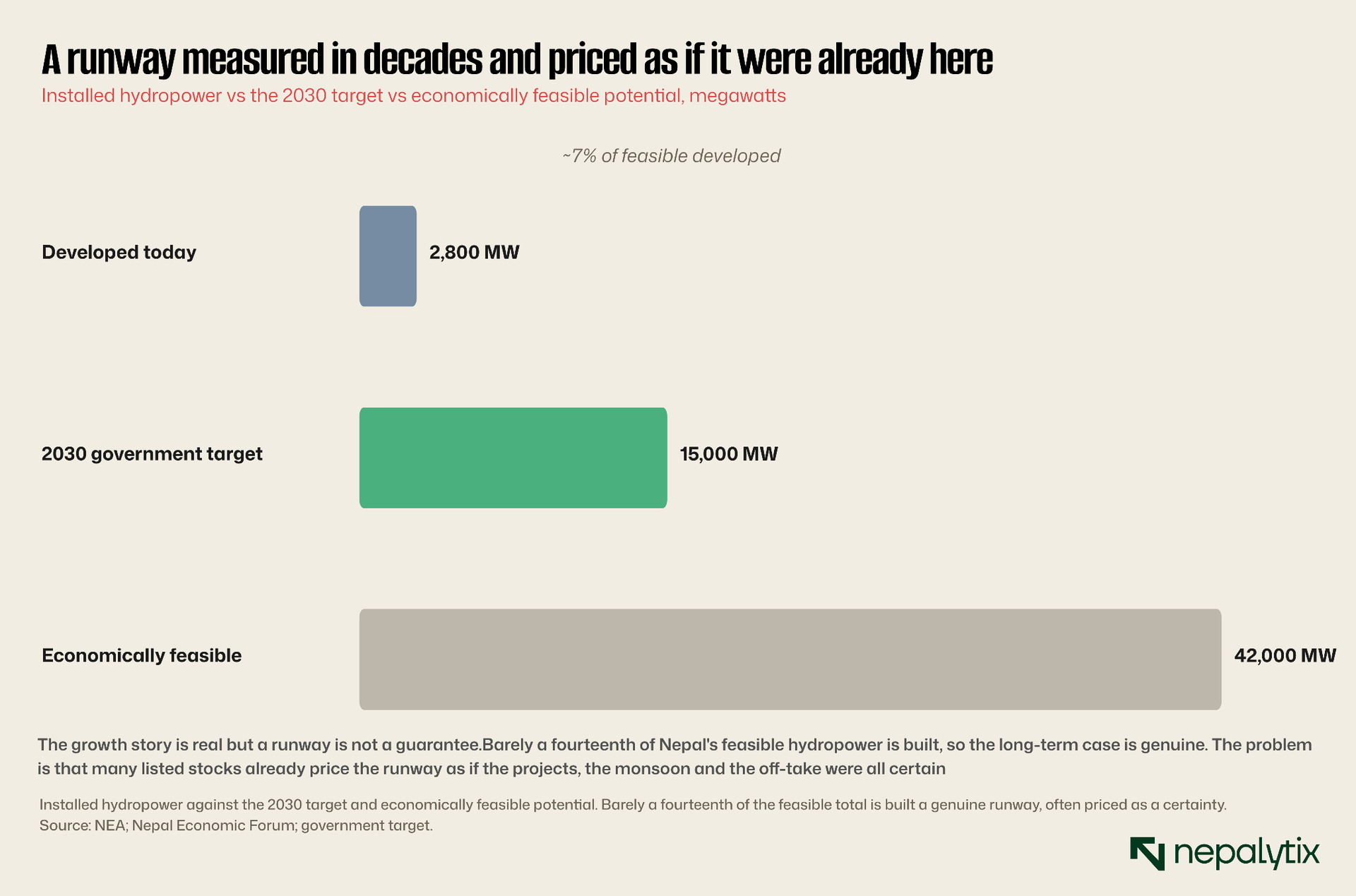

None of this denies the sector's promise, and the bull case deserves a fair hearing. Nepal has built only around seven percent of its economically feasible hydropower; domestic demand is rising, the export agreements with India are real and growing, and the best-run operating companies completed plants, steady generation, and dividend records are legitimate long-term holdings. The growth runway is measured in decades, not years.

But a runway is not a guarantee and the market too often prices it as one. Because so many listed names are still building their share prices are set by milestone announcements and by the momentum of the next oversubscribed IPO rather than by earnings and the sector has at times traded at multiples that would look stretched even for plants already running at capacity. Solu Hydropower was the single best-performing IPO of the current fiscal year - the kind of result that pulls fresh money toward the next hydropower float regardless of its fundamentals. The pricing assumes, implicitly, that the monsoon will cooperate, the agreements will hold, the transmission lines will be built and every construction schedule will be met for all of them, at once.

The construction-stage names carry a second layer of correlated risk that valuations rarely separate out. A company still building its plant has no revenue to value, so its price tracks expectations for the next milestone, the next financing tranche, the commercial-operation date and those expectations are set by the same buoyant sentiment that drives every hydropower IPO. When the sentiment turns, it turns for the whole cohort of pre-revenue names at once, regardless of which river each sits on. Milestone pricing feels company-specific; in practice it is sentiment-specific, and the sentiment is shared.

What Investors May Be Missing

It helps to contrast the two big concentrations on the board. Banking and finance carry more than half the market's value, which sounds alarming until you remember what sits underneath: a few dozen large, regulated separately capitalised institutions with diversified loan books and earnings that do not all move with one input. Hydropower's concentration is the opposite of many small companies whose revenues are driven by a single shared variable owned disproportionately by investors holding only a handful of names each. A shock to banking would be serious and visible. A shock to hydropower would be just as correlated but far less expected by the people holding it.

That is why the 16 percent index weight is misleading. The index is dominated by a handful of giant banks, so 16 percent badly understates where retail money actually sits because retail crowds into exactly the small, cheap, story-driven hydropower names that make up a third of the board. The most exposed investors to this correlation are the least diversified ones in the market, and the index weight is precisely the wrong number to reassure them.

Real diversification inside the sector is possible but it is not what most retail portfolios contain. It would mean leaning toward completed, revenue-generating, dividend-paying plants over construction-stage hopefuls; mixing run-of-river exposure with the handful of storage and peaking projects that hold water for the dry months; and sizing the whole hydropower allocation against genuinely uncorrelated holdings elsewhere on the exchange rather than buying a twelfth power stock. The instinct that builds the swarm that one more hydropower name makes a portfolio safer because it is one more company runs exactly backwards when every company drinks from the same rivers.

What Could Break The Trade

A weak monsoon or a drought year that cuts generation and revenue across the sector at once. A renegotiation of PPA rates that re-prices every developer's cash flow simultaneously. A transmission bottleneck that strands a wave of newly commissioned plants. A run of construction-stage companies missing their commercial-operation dates together. A new hydropower IPO that finally prices cold, signalling that retail appetite has turned. Any one of these would hit not a stock but the whole cohort - and the investors who spread their savings across a dozen hydropower tickers, believing they had diversified, would discover all at once that they had not.

None of this is hidden from the regulator. SEBON's new net-worth screen weeds out the weakest balance sheets, but it does nothing about sector correlation - a portfolio of financially sound run-of-river plants is still a single bet on the monsoon. A concentration this lopsided is the kind of structural risk a maturing market eventually learns to flag and price. Nepal has not yet begun to.

This is not a case against hydropower. Nepal's energy story remains one of the country's most compelling long-term investment themes. It is a case against mistaking quantity for diversification.

Many investors believe owning several hydropower stocks spreads risk. In reality, much of the sector remains tied to the same monsoon, the same buyer and the same infrastructure.The companies may have different names. The underlying bet is often the same.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.