The Take: SEBON Built A Shadow Market

SEBON's attempt to protect investors by tightly restricting IPO approvals has produced the opposite outcome:

A regulator's job is to protect investors. By guarding the gate to its IPO market so jealously, the Securities Board of Nepal has done the opposite - freezing tens of billions of rupees in capital, starving the real economy of equity, and pushing ordinary savers out a side door into an unregulated market with no protection at all. The fix is not a higher gate. It has better plumbing.

Three Repairs For A Broken Market

Make approval a transparent, time-bound, rules-based process not a discretionary favour.

Let the market find the price: extend book-building and retire the blanket Rs 100 par lottery.

Bring the pre-IPO shadow market into the light, and replace the blunt net-worth gate with real disclosure.

Every capital market regulator faces the same temptation: to confuse caution with protection. The Securities Board of Nepal has succumbed to it completely. Confronted with a wave of companies wanting to list many of them small, some financially thin, a great many in hydropower SEBON has responded by all but closing the door. The instinct is understandable. Nepali retail investors have been burned before by weak issuers and a regulator that waves through every applicant fails its mandate. But protection by exclusion has produced a result that is the precise opposite of what it intended, and this submission sets out the evidence for that claim, and three reforms to reverse it.

The charge is simple. SEBON's gate, built to keep bad issuers out, has instead trapped good capital in, bred the conditions for corruption, and driven the very retail investors it exists to protect into an unregulated market where they have no protection whatsoever. A regulator cannot shield savers by shutting the regulated market, because the demand does not vanish, it migrates to wherever it can be met, and what it finds is always riskier than what it left. The answer is not to guard the gate more fiercely. It is to fix the plumbing: the process by which companies are approved, the way their shares are priced, and the unregulated channel that has grown up in the regulated market's absence.

Nepal's IPO Market Is Stuck

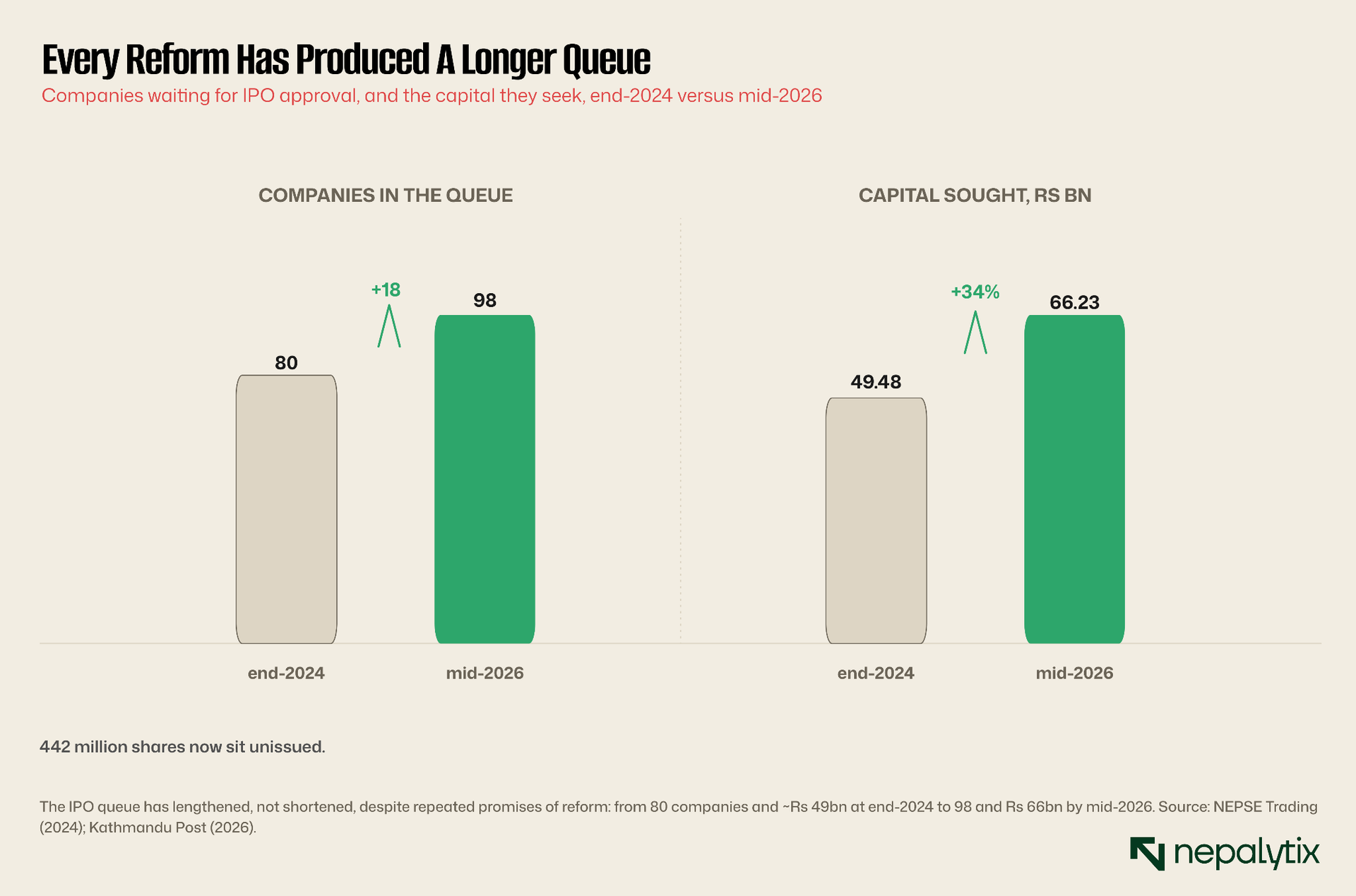

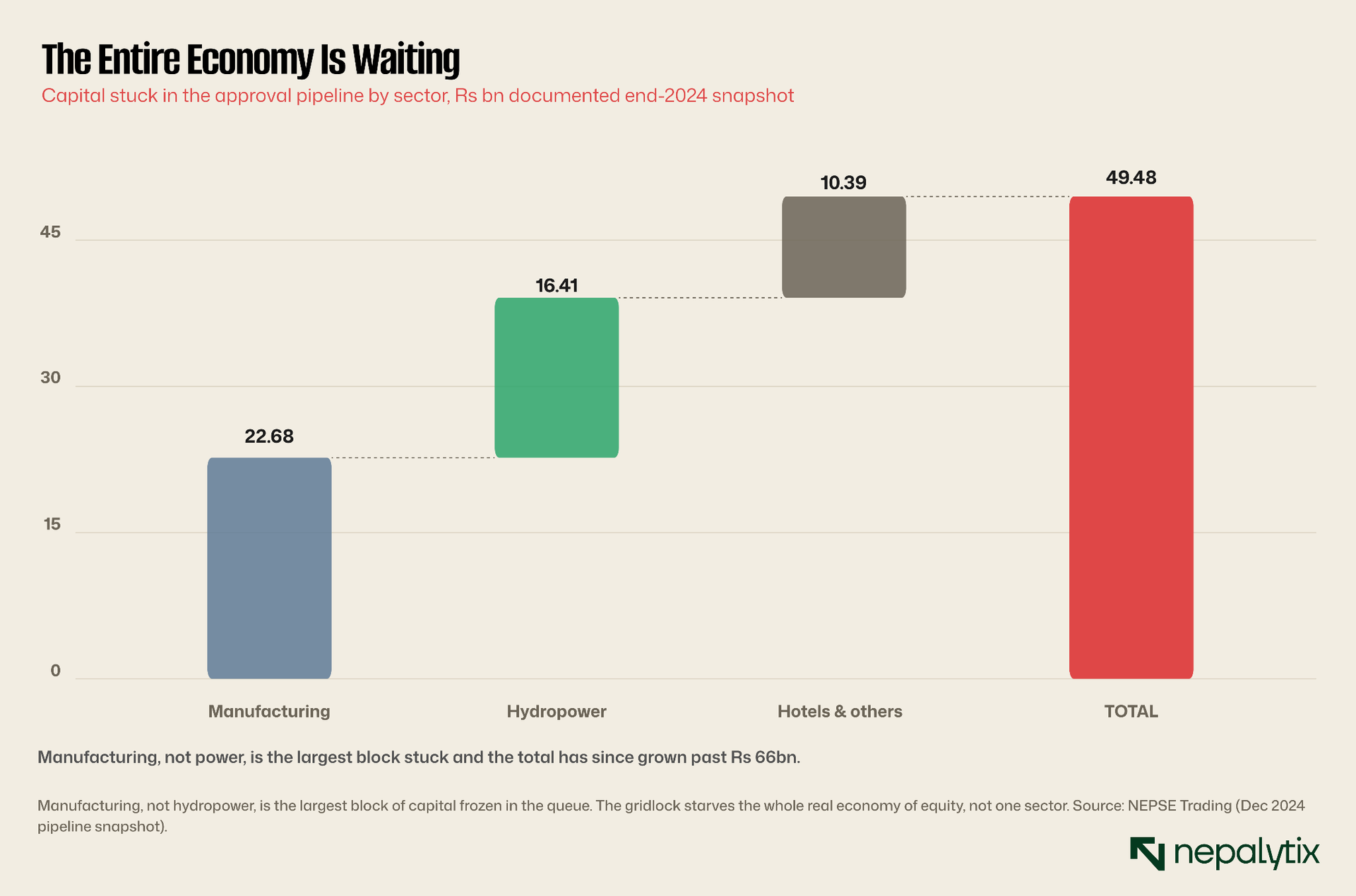

Begin with the scale of the blockage. As of May 2026, ninety-eight companies were waiting in SEBON's IPO queue, seeking a combined Rs 66.23 billion across some 442 million shares. That is not a snapshot of healthy demand awaiting orderly processing; it is a backlog that has been building for years and is still growing. Eighteen months earlier the queue held eighty companies and around Rs 49 billion. Every partial fix announced in the interim has failed to clear it; the line has only lengthened.

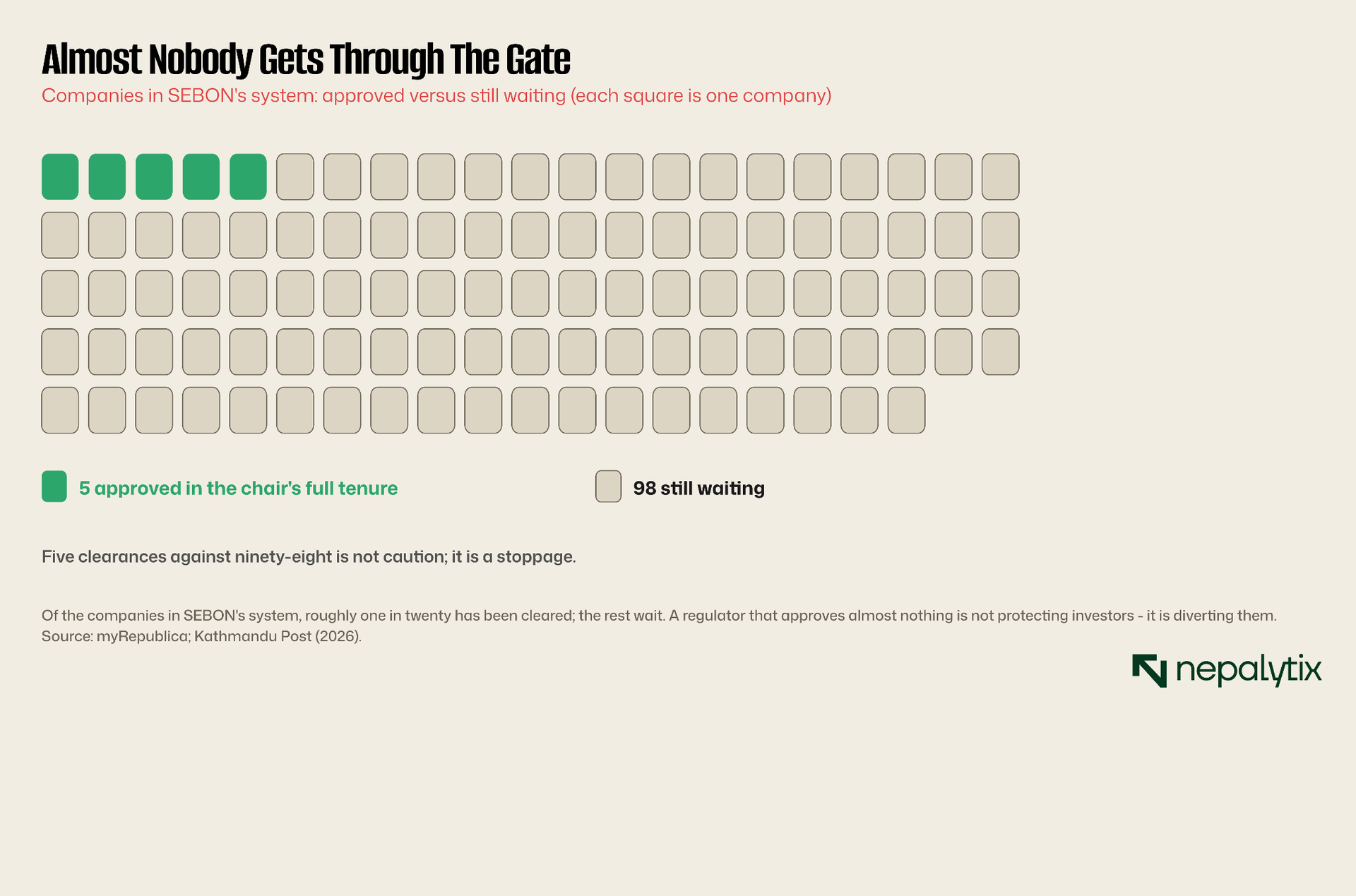

The flow through the gate, meanwhile, has slowed to a trickle. Over the full tenure of the most recent chairman, SEBON granted approval to a mere handful of issues on the order of five - against the ninety-eight left waiting. At one earlier point the board approved a single IPO in the space of a year. This is not the throughput of a cautious regulator carefully vetting a pipeline. It is the throughput of an institution that has for practical purposes stopped functioning in its core role of admitting companies to the public market.

The contrast with what a working pipeline looks like is instructive. Even through the gridlock, the number of companies listed on the Nepal Stock Exchange edged up from 268 to 286 over the year to March 2026 proof that the demand to list is real and continuous. A market with that much pent-up supply and six million investors hungry to buy ought to be among the most dynamic primary markets in the region. Instead the registrations that should be flowing onto the exchange are pooling in a queue, and the gap between the market Nepal could have and the one it has is the measure of the failure.

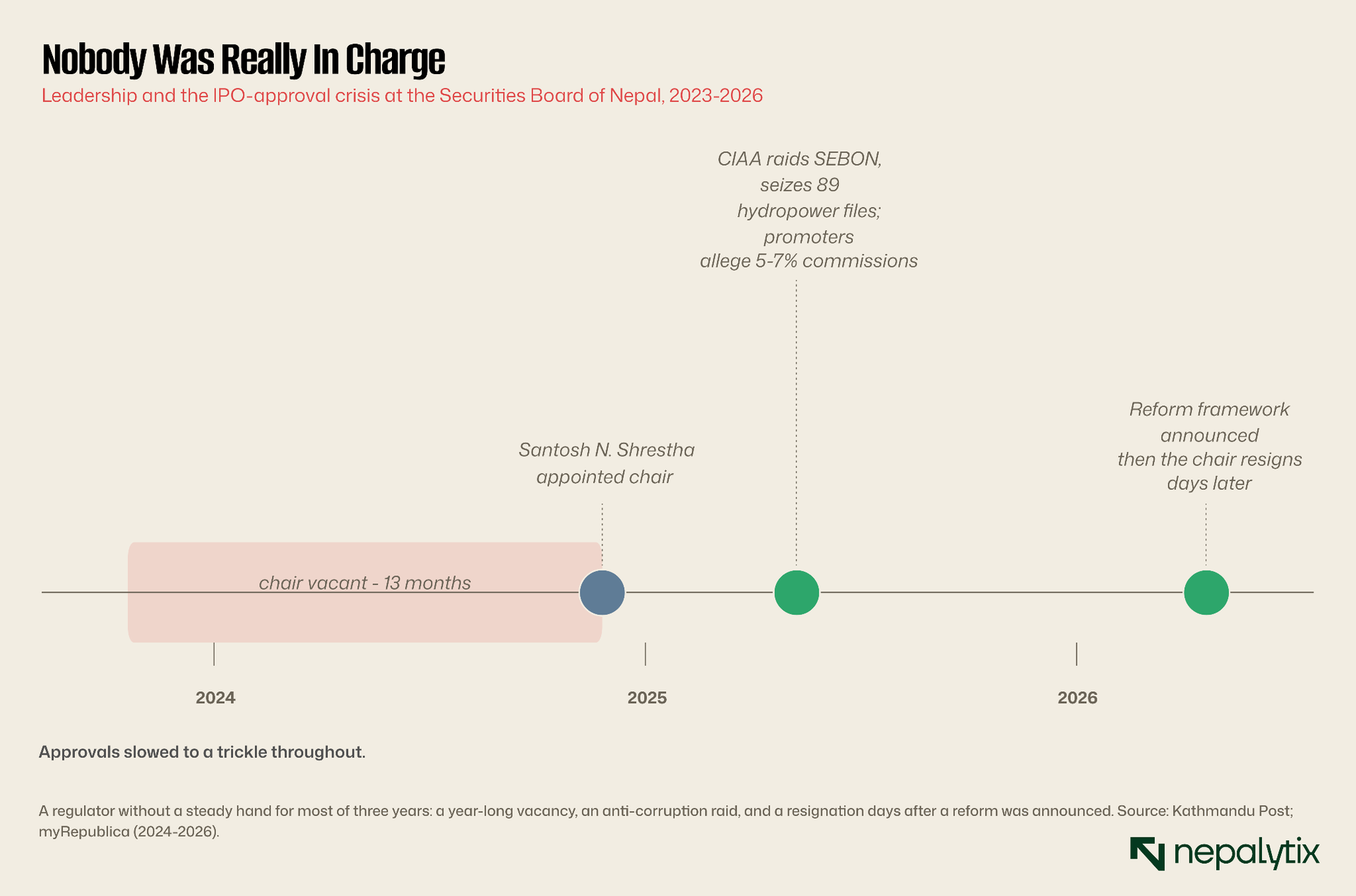

Behind the numbers sits a governance failure that is worth stating plainly because it is the root of everything that follows. SEBON was left without a chairman from late 2023 until November 2024, a full year in which approvals slowed because there was no one with the authority to grant them. The chair who was finally appointed presided, in May 2025, over an extraordinary event: the Commission for the Investigation of Abuse of Authority raided SEBON's own offices and seized the files of eighty-nine hydropower companies following allegations raised in Parliament that board officials had demanded commissions of five to seven percent to clear approvals, with some applications stalled for as long as twenty-two months. Then, in April 2026, the chairman resigned, days after announcing a new 'streamlined framework he would not remain to implement.

A regulator cannot protect savers by shutting the regulated market. The demand does not vanish, it migrates to something worse.

This is the context in which any discussion of IPO reform in Nepal must begin. The problem is not that SEBON vets too carefully; through vetting is exactly its job. The problem is that the vetting has become a bottleneck so opaque, so slow and so vulnerable to discretion that it has stopped protecting anyone and has started, actively, to cause harm. Three reforms would change that. None of them asks SEBON to lower its standards. All of them ask it to make its process faster, fairer and more transparent.

The cost of this paralysis is not abstract. Capital that sits in a SEBON queue is capital that is not building a hydropower plant, a factory or a hotel and in a country whose development is constrained precisely by a shortage of long-term equity, that is a real economic loss compounding by the month. A company that filed two years ago and is still waiting has, in the interim, either delayed its project, financed it with costlier debt, or turned to the unregulated channels described below. None of those outcomes serves the investors SEBON exists to protect, and all of them are the direct product of a queue that does not move.

To put Rs 66 billion in proportion: the 442 million shares awaiting issue would, at par alone, be worth some Rs 44 billion of fresh equity for Nepali companies, and considerably more if priced closer to market. That is not a rounding error in a developing capital market, it is a material fraction of the equity the economy could be raising, held in suspension by an administrative process. And it is worth being clear that this degree of dysfunction is not normal for a securities regulator. In most markets IPO approval is a documentary and disclosure exercise conducted against a clock: the regulator confirms the prospectus is complete and not misleading and either clears it or returns it with specified deficiencies within a defined period. It does not sit as a discretionary arbiter of whether a company deserves to raise capital, holding files indefinitely while it forms a view. Nepal's drift toward the latter model - approval as judgement rather than process is the deeper malady, and the three fixes that follow are, at bottom, three ways of returning SEBON to its role.

Fix One: Turn Approval Into A Process

The first and most urgent reform is to strip discretion out of the approval process and replace it with rules, clocks and sunlight. The single most damaging feature of the current regime is that an applicant has no way of knowing when or whether a decision will come. Files sit. Reasons go unstated. And in the gap between submission and decision, the allegations that produced the CIAA raid become not merely possible but predictable. Where a decision is discretionary, undated and unexplained, the discretion itself becomes something that can be sold.

SEBON should bind itself to a statutory approval clock. An application that meets the published eligibility criteria should receive a decision within a fixed window ninety days is a reasonable benchmark and a rejection should require written reasons that the applicant can address and if necessary, appeal. The law already requires a company to issue its shares within two months of approval; it is the approval stage itself, which has no comparable deadline that has become the black hole. A clock on that stage with the default tilted toward decision rather than indefinite pendency would do more to clear the backlog than any number of 'frameworks' announced and then abandoned.

Alongside the clock should come transparency. SEBON should publish a live register of every pending application: the company, the date filed, the current status, the outstanding requirements and the age of the file. Sunlight is the cheapest anti-corruption tool available. An official cannot quietly hold a compliant file hostage for twenty-two months if the file's age is visible to the applicant, the press and the Parliament. The same register would let SEBON defend itself when delay genuinely is the applicant's fault which the board rightly points out it sometimes is by showing exactly which requirement remains outstanding and since when.

Discretion that cannot be questioned is discretion that will be abused, so the clock and the register need an appeal attached. An applicant told its file is deficient should receive the specific deficiency in writing and a defined route to contest a refusal it believes is unjustified before an authority other than the official who issued it. An appeal mechanism does more than correct individual errors; it disciplines the whole process, because an official who knows that a stalled or arbitrary decision can be reviewed has far less room to extract a price for moving it along.

Eligibility itself should be a published, binary test not a sliding scale administered behind closed doors. Nepal's regime already leans this way a company either clears the minimum net-worth and profitability thresholds or it does not but discretion creeps back in through documentation demands, repeated requests for clarification and the sequencing of multi-agency approvals. That last point deserves its own remedy. An IPO applicant today must satisfy the Electricity Regulatory Commission, the Office of the Company Registrar and SEBON in sequence, each waiting on the last. These should be coordinated into a single, time-bound, preferably parallel process so that an applicant is not bounced between agencies for years. Reformers, merchant bankers and even the Electricity Regulatory Commission's own chair have called for exactly this; what is missing is the will to implement it.

Finally and most structurally SEBON's leadership must be insulated from the political cycle. The year-long vacancy that began the current crisis was not an accident; it was the product of a selection process hostage to government formation and transition. A regulator whose chair's office empties every time the politics shift cannot maintain the institutional continuity that orderly capital markets require. A fixed, staggered term, a transparent and merit-based appointment process, and a clear succession rule when a chair departs would prevent a change of government from once again becoming a year of regulatory paralysis. The fact that the April 2026 framework was announced by a chairman who resigned days later is the whole problem in miniature: in Nepal's current arrangement, reform and continuity are at the mercy of the same political weather.

There is nothing exotic in any of this. India's securities regulator processes draft offer documents against published timelines and issues its observations within weeks not years; many regulators operate an explicit deemed-approval rule, under which silence past a deadline counts as clearance, precisely to remove the incentive to stall. Nepal need not import a foreign system wholesale, but it should adopt the principle they share: that the passage of time must work in the applicant's favour, not the official's. A deadline with a default attached is the difference between a process and a chokepoint.

A predictable objection is that SEBON lacks the staff to clear files faster, and there is something to it the board is thinly resourced for the volume it faces. But under-resourcing is an argument for investing in the regulator's capacity and automating the routine, documentary parts of review not for tolerating multi-year delays as a fact of nature. And capacity is not what keeps a compliant file waiting twenty-two months while a commission is negotiated; discretion is. The clock, the public register and the written-reasons requirement are aimed at that discretion. Whatever genuine capacity gap remains can then be addressed honestly and in the open rather than serving as a permanent excuse for a process that has effectively stopped.

Fix Two: Stop Running IPOs As A Lottery

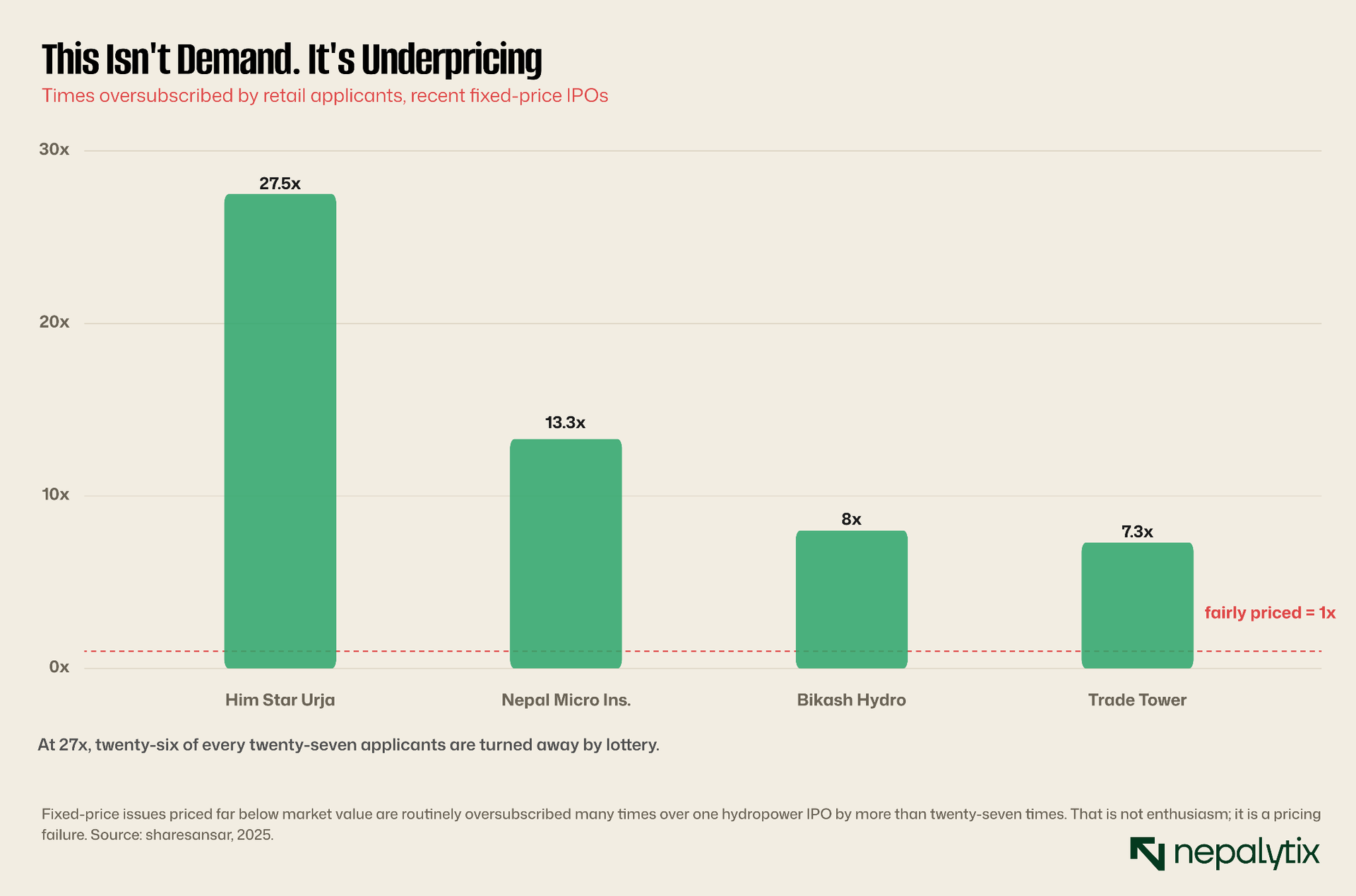

The second reform concerns not how companies are admitted but how their shares are priced once they are. The overwhelming majority of Nepali IPOs are issued at a fixed price of Rs 100 the par value regardless of what the company is actually worth. This single convention is responsible for much of the dysfunction that the casual observer mistakes for healthy enthusiasm. When a share that the market believes is worth several times its issue price is offered at par, the result is not price discovery; it is a stampede.

Consider what oversubscription of twenty-seven times actually means. It means that for every share on offer, twenty-seven applications were submitted, and twenty-six were turned away by lottery. The investors who win the draw capture an immediate near-guaranteed gain when the share lists at a multiple of its issue price; those who lose get their blocked money back and try again next time. The market has become, in effect, a national lottery in which the prize is the gap between the par price and the fair price, a gap created entirely by the decision to issue at par. This is a strange way to run a capital market, and it has two costs that ought to trouble SEBON more than they appear to.

The first cost falls on the issuer, and through it on the economy. A company that sells its shares at Rs 100 when the market would have paid Rs 300 has handed two-thirds of its own value to lottery winners. That is capital the company could have raised for its dam, its factory or its hotel scattered instead across thousands of fortunate applicants. In a country desperate for domestic capital formation, systematically underpricing the equity that companies sell to fund real investment is close to perverse. The second cost is behavioural: a market in which listing-day gains are near-automatic trains an entire generation of retail investors to treat IPOs as free money rather than as ownership stakes to be valued, feeding precisely the speculative froth most visible in construction-stage hydropower that ends in tears when the music stops.

The remedy is price discovery and SEBON already has the tool: book-building under which qualified institutional investors bid to establish a market-clearing price before retail investors are invited in at a modest discount. To its credit, the board's 2026 rules made book-building the standard route for larger corporate issues, set a sensible fifty-unit retail minimum and preserved a ten-percent retail discount to the institutional cut-off price. This is genuine progress and deserves acknowledgement. But it stops well short. Book-building remains confined to the largest issuers, while the great mass of small and hydropower companies exactly the issues that generate the most extreme oversubscription continue to price at par.

SEBON should extend price discovery down the size curve, simplifying the book-building mechanics so that mid-sized issuers can use it without prohibitive cost while keeping the retail protections that make it politically viable: the guaranteed retail tranche, the discount to the institutional price, the floor on units allotted. The objective is not to deny retail investors the upside they enjoy, it is to stop manufacturing that upside by systematically underpricing the nation's capital formation, and to let the price of a company reflect what the company is actually worth. A market that cannot price its own assets is not yet a market; it is a queue with a lottery at the end of it.

The mechanics are well understood and already on Nepal's books. Under book-building, an issuer and its merchant banker set an indicative price band; qualified institutional investors - no single one permitted more than a fifth of the issue - bid within it through an electronic auction; a cut-off price emerges from that demand; and retail investors are then allotted shares at a discount to it. Nepal's existing premium-pricing rules already gesture at valuation discipline, capping a premium at twice net worth per share and tying it to profitability and for hydropower, to construction progress. The tools to price companies at something closer to their worth exist. What is missing is the will to use them beyond a handful of the largest issues.

The behavioural stakes are easy to underestimate. When a market reliably hands out listing-day gains shares issued at Rs 100 routinely opening at two to four times that it teaches investors that the way to make money is to win the allotment lottery, not to assess a business. A whole cohort of Nepal's six million new investors has learned that lesson applying to every issue regardless of quality because the price bears no relation to value and the downside feels capped. Honest pricing would not end retail participation; it would change its character - rewarding judgement over luck, and pointing the speculative energy now pouring into construction-stage hydropower toward companies that can actually be valued. That is a healthier market, and a safer one.

Honest pricing would not end retail participation. It would change its character rewarding judgement over luck.

Why does Nepal default to par in the first place? Largely by habit, and by the politics of access. A par-value issue is simple to administer and, because it guarantees a listing pop, popular with the retail investors and the politicians who speak for them; book-building by contrast asks institutions to set the price and gives retail a smaller, if fairer, reward. The fixed-price model has survived less because it is sound than because its costs are diffuse and its beneficiaries vocal. Good regulation sometimes means choosing the less popular mechanism because it is the correct one and explaining, plainly, why.

Fix Three: Regulate The Market You've Already Created

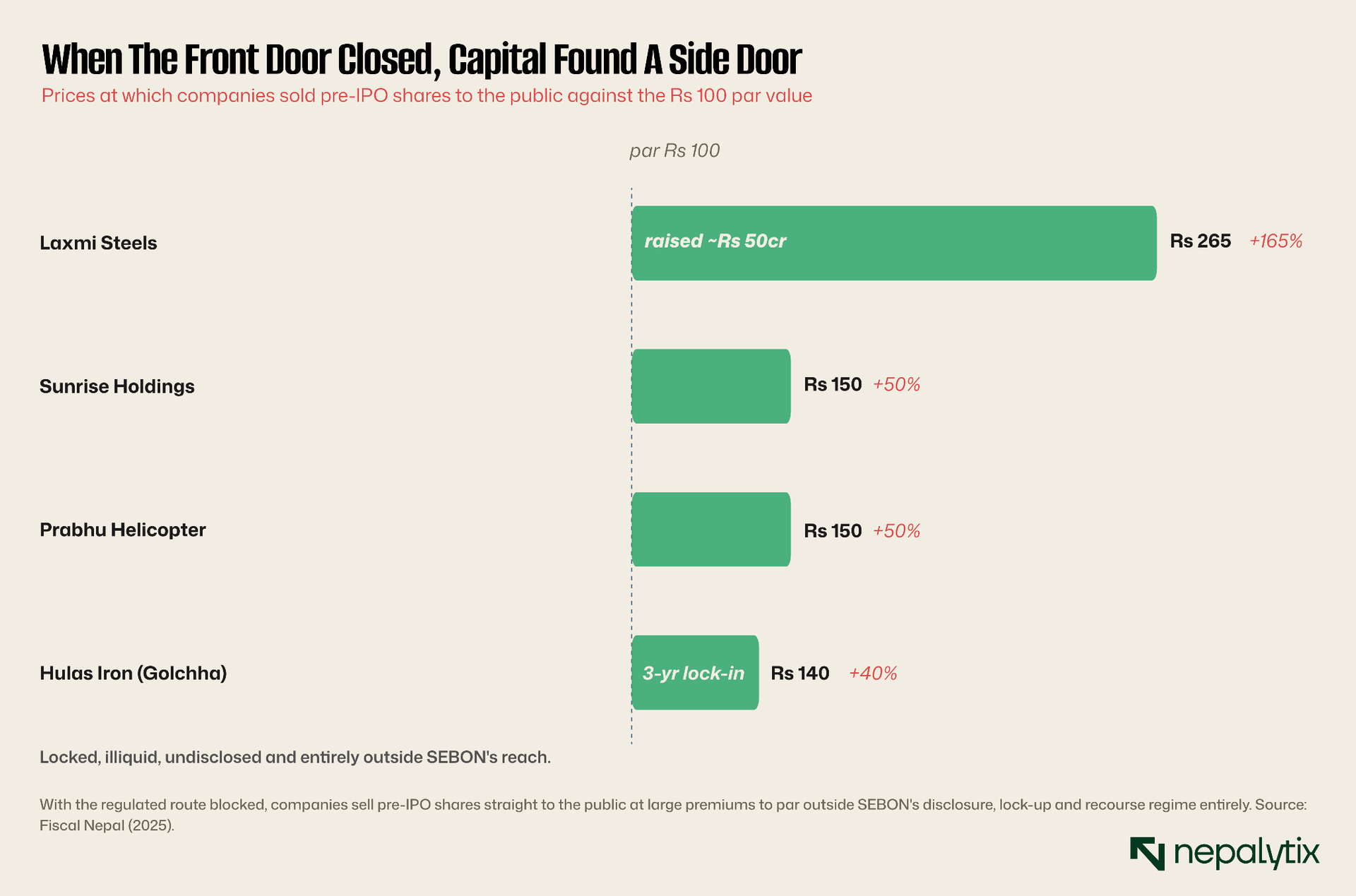

The third reform addresses the most dangerous consequence of the first two failures and the clearest proof that SEBON's caution has backfired. With the front door of the capital market effectively shut, companies and their backers have found a side door. An aggressive and largely unregulated pre-IPO market has grown up in Nepal in which companies sell shares to the public at hefty premiums to par before they have received any SEBON approval at all.

The examples are not marginal. Laxmi Steels sold pre-IPO shares at Rs 265 a 165 percent premium to par raising some Rs 50 crore after weak promoter participation. Hulas Iron, of the prominent Golchha Group has been selling promoter shares to ordinary investors at Rs 140 through a licensed merchant bank, with the shares locked for three years. Sunrise Holdings and Prabhu Helicopter have sold at Rs 150. Merchant bankers encourage retail investors to 'join early' before the IPO on the promise that the shares will later become tradable. What those investors are actually buying is an illiquid, three-year-locked largely undisclosed security, with none of the prospectus disclosure, the lock-up safeguards or the regulatory recourse that a genuine IPO provides. This is the regulated market's protection turned inside out: retail money flowing into exactly the high-risk, low-information instruments that SEBON exists to keep it away from and flowing there precisely because SEBON shut the safer door.

Consider what the buyer of a pre-IPO share actually holds. There is no approved prospectus, so the disclosures a public issuer must make to audited accounts, risk factors, use of proceeds, related-party dealings may simply be absent. There is no regulated secondary market so the shares cannot be sold until they list, if they ever do; the three-year lock-ins now commonly mean the money is committed and illiquid. And there is no recourse: if the promised IPO never materialises, or materialises at a lower price, the investor has bought into a private company with none of the protections that attach to a public one. That is the product being marketed to retail investors as a chance to get in early markets precisely because the regulated alternative is shut.

It is worth dwelling on the perversity of this outcome. The Rs 90 net-worth threshold, the multi-agency vetting, the cautious approvals all of it is justified by SEBON and by the parliamentary committee that pushed for the net-worth rule, as protection for unsophisticated retail investors. Yet the cumulative effect has been to push those same investors into a market with no net-worth test, no disclosure standard and no regulator at all. A gate is only protective if there is no hole in the fence beside it. SEBON has built an ever-higher gate while an ever-larger hole has opened up next to it, and capital along with the savers chasing it has simply walked through the gap.

And the capital that is stuck is not confined to the hydropower sector that dominates the headlines. The single largest block of frozen capital in the pipeline is manufacturing and processing, not power. The gridlock is starving the entire real economy of equity finance at a moment when Nepal needs domestic capital formation more than at any point in its recent history.

The reform here has two parts. First, the pre-IPO market must be brought under a real, enforced regulatory regime before it produces the scandal that merchant bankers themselves are warning of. SEBON has the beginnings of a framework: the 2081 regulations for small and medium enterprises and the Specialized Investment Fund rules already contemplate channelling pre-listing capital through licensed private-equity and venture funds, professionally managed and limited to sophisticated investors, rather than through direct sales to the retail public. That framework should be completed, made mandatory for pre-IPO fundraising of any scale, and enforced so that the on-ramp to a public listing runs through a regulated channel rather than an unregulated one.

Second, SEBON should replace its blunt net-worth gate with substantive disclosure. The Rs 90 threshold is a binary cliff: a company either clears it or is barred, and a strong prospectus cannot make up the difference. That may keep the very weakest issuers out, but it does so at the cost of blocking viable companies and telling investors nothing about the ones that pass. A disclosure-based regime would do the opposite work and do it better. Issuers especially the construction-stage hydropower companies that make up so much of the queue should be required to disclose, in standardised and comparable form, their use of proceeds, their construction and commercial-operation milestones, their related-party exposures and their independent credit ratings, and to keep reporting against those milestones after listing. Protect investors with information and a regulated on-ramp, not with a closed door that breeds a black market beside it.

Nepal has, encouragingly, already sketched the regulated on-ramp this requires. The 2081 regulations create a dedicated platform for small and medium enterprises, letting companies of up to Rs 250 million in paid-up capital register securities under a lighter regime; the Specialized Investment Fund rules allow pre-listing capital to be raised through professionally managed private-equity and venture funds, capped at a couple of hundred sophisticated investors and required to hold real capital of their own. The architecture of a legitimate pre-IPO market already exists on paper. The task is to finish it, make it the only lawful route for pre-listing fundraising at scale and enforce that exclusivity so a company wanting early capital raises it from supervised professional funds not from retail buyers through a merchant bank's mailing list.

Replacing the net-worth cliff with disclosure is the harder and more important half. A disclosure regime does not ask whether a company is rich enough to list; it asks whether an investor has enough information to decide. For Nepal's pipeline that means standardised, comparable prospectuses; for the construction-stage hydropower companies that dominate the queue, it means disclosing licence status, financing, construction milestones and the expected commercial-operation date and then reporting against those milestones every quarter after listing so a missed deadline is visible rather than buried. It means independent credit ratings with real consequences, and clear disclosure of related-party dealings, the area where a closely-held promoter group can most easily disadvantage minority shareholders. Information of that kind protects investors in a way a single net-worth number never can, and it does so without barring viable companies from the market.

SEBON's Case Falls Apart Under Inspection

In fairness, SEBON's own account of the situation deserves to be heard, and parts of it are correct. The board's spokesman maintains that applications remain pending not because of institutional foot-dragging but because the applicant companies themselves have submitted incomplete paperwork or carry unresolved compliance deficiencies that must be fixed before public investors can be exposed to them. The board points to its new April 2026 framework as evidence of reform and notes that more than a dozen companies were in fact approved and listed over the period. And it defends the Rs 90 net-worth threshold as a legitimate investor-protection measure, arguing with the painful history of retail losses to back it that approving financially weak companies would expose ordinary Nepalis with limited financial literacy to exactly the kind of harm that has damaged trust in the market before. These are not bad-faith arguments, and a serious submission should not pretend otherwise.

But they do not survive contact with the evidence. That some delay is the applicants' own fault cannot explain a median stall measured in many months, allegations of percentage commissions serious enough to trigger an anti-corruption raid, or a backlog that grows year after year; those are symptoms of a broken process not of incomplete paperwork. The defence of the net-worth gate, meanwhile, mistakes the question. The issue is not whether weak companies should be screened of course they should but whether a blunt exclusion is the right screen when the excluded capital does not disappear but reappears, unregulated and more dangerous, in the pre-IPO market next door. Protection that creates a riskier alternative is not protection. And the April 2026 framework, whatever its merits was announced by a chairman who resigned before he could implement it which tells you most of what you need to know about the continuity on which any reform depends. SEBON's caution is well-intentioned. Its method is counterproductive, and the evidence for that is now overwhelming.

One further defence deserves a response: that the market is thriving regardless of the index near record highs, new investors pouring in so the gridlock cannot be doing much harm. But a buoyant secondary market is not evidence that the primary market works; it is part of why the par-value lottery and the pre-IPO boom are so frenzied. Rising prices on the exchange make the locked-up shadow shares look like guaranteed winners and the listing pop look like free money, drawing ever more unprotected retail money into both. A bull market is precisely when a regulator should worry most about where that money is going. It would be naive to ignore why this dysfunction persists. A slow, discretionary approval process is not equally inconvenient for everyone; for those positioned to charge for access to it, the bottleneck is the business model, and the CIAA's interest suggests that is not a merely theoretical concern. Reform that replaces discretion with rules, clocks and public registers is therefore not a technical tidy-up but a removal of rents, and it will be resisted by the people who collect them. That is all the more reason to entrench it in hard rules and transparent processes rather than in the good intentions of whichever chair holds office - good intentions, as the last three years have shown, do not survive the next political transition.

Why This Matters Beyond The Market

Nepal is living through a once-in-a-generation expansion of its investing public. Online trading accounts have multiplied many times over in half a decade, to more than six million; savings that once sat in property or bank deposits are looking for a home in the capital market just as the real economy, power, manufacturing, tourism is hungry for the equity that market is supposed to supply. The primary market is the junction where those two needs are meant to meet. A functioning IPO pipeline turns household savings into productive investment and gives savers a regulated, disclosed, liquid way to own a piece of their country's growth.

A broken pipeline fails both sides at once. It starves good companies of the capital they need to build, and it pushes savers toward unregulated risk they are told is a shortcut to wealth. That is the situation Nepal is in now, and it is the direct, traceable consequence of a regulator that has confused guarding the gate with doing its job. The remedy is not to guard the gate more fiercely. It is to make the process transparent and time-bound, to let the market discover honest prices, and to bring the shadow market into the light while swapping a crude net-worth cliff for real disclosure.

None of this is radical. Every one of these reforms has been proposed, in some form, by the market participants who live with the current system and several are half-built in SEBON's own rulebooks waiting to be finished and enforced. What has been missing is not the blueprint but the will, and the institutional stability, to act on it. SEBON's mandate is to protect investors. The best protection it can offer is not a higher wall but a market that works: fast, fair, honestly priced and fully disclosed. The gate was built to protect. It has backfired. It is time to open it carefully, with rules, clocks and sunlight before the shadow market opens it instead, with none of those things at all.

The wider prize is a capital market that can do its job. Nepal's savers are moving out of gold and fixed deposits into equities at a pace few anticipated a decade ago; its companies in power, manufacturing and tourism need patient domestic equity to grow. A primary market that channels the first into the second, quickly, at honest prices and with full disclosure, would be one of the most powerful development tools the country has. The reforms in this submission are not about making life easier for promoters or speculators. They are about letting that machine work.

There is a clock on all of this that has nothing to do with SEBON's own deadlines. The pre-IPO market is growing, retail money is flowing into locked and undisclosed shares, and the gap between the promises made to those investors and the protection they actually enjoy is widening. Markets of that kind do not deflate quietly; they end in a failure visible enough to shake the confidence of the whole investing public the very outcome SEBON's caution was meant to prevent. The board can get ahead of that by opening and fixing the regulated market now or it can wait and manage the fallout later. Only one of those is regulation.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.