The Take: Why Nepal's NPL ratio is the most misleading number in the BFI sector and the chain that closes when restructured loans roll off

An IMF-mandated audit reveals Nepal’s true banking stress is significantly higher than reported NPL figures, exposing deep structural gaps in loan classification.

For three years, observers have argued the published NPL number understates the structural stress in Nepali banking. The Nepal Rastra Bank's own IMF-mandated loan portfolio review just provided the proof and the IMF has already said the headline number will be revised up.

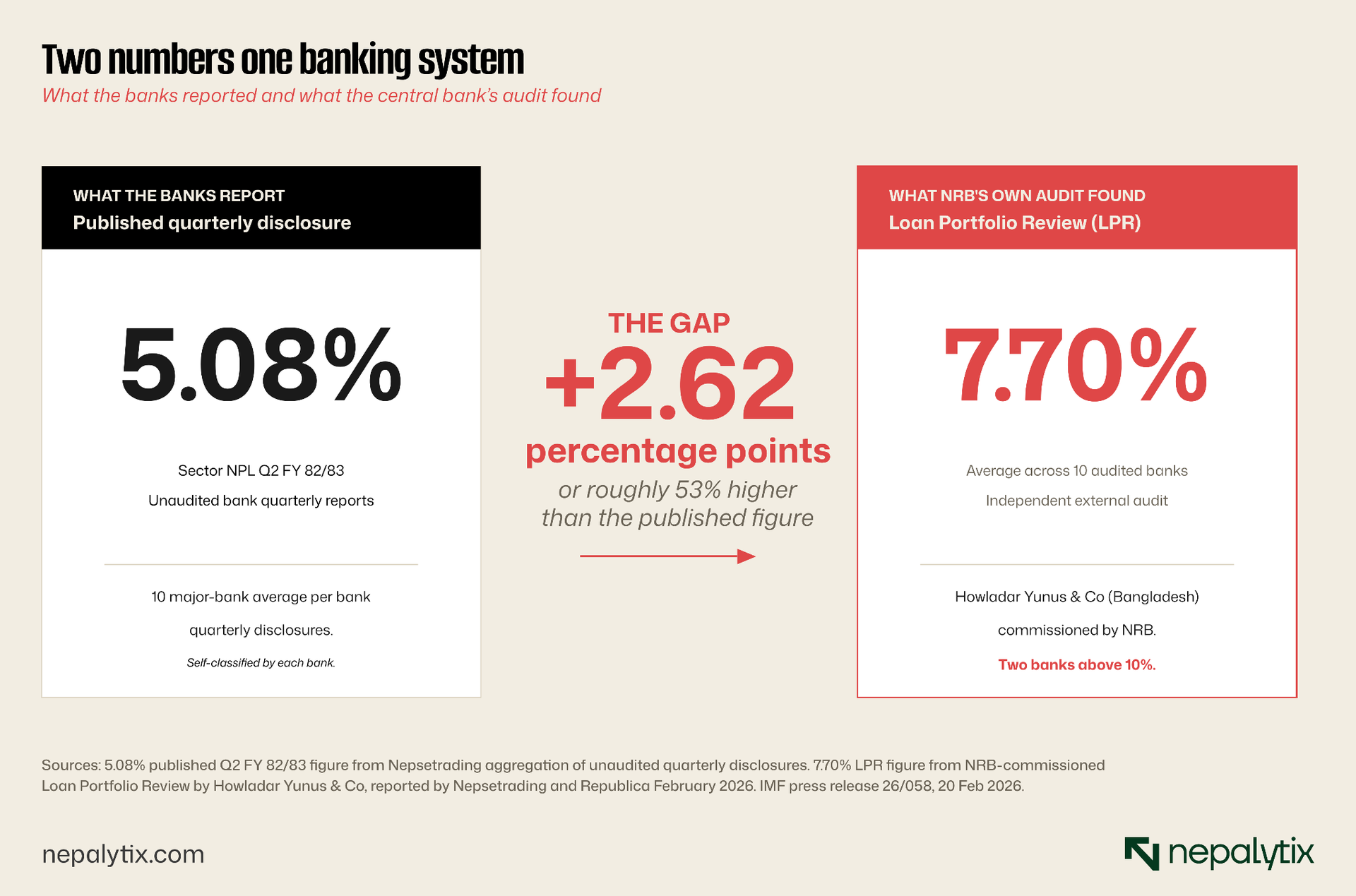

The two numbers above are produced by the same regulator, covering the same banks over the same period. The left number is what Nepal's commercial banks publish in their unaudited quarterly disclosures. The right number is what the central bank found when it commissioned an independent audit of the same loan portfolios. The gap between them is the central fact of Nepali banking in 2026.

For three years, NRB's published NPL ratio has climbed steadily from 3.98 percent in mid-2024 to 4.86 percent in late 2025 to 5.42 percent in early 2026. For three years, observers, commentators, and a long line of reader comments on financial websites have argued the published number understates the structural reality. None of those arguments was empirical. They were structural based on how forbearance windows work on how restructured loans are accounted for on how evergreening can keep loans technically performing.

The IMF in approving Nepal's Extended Credit Facility required a different kind of evidence. It required an independent audit. The Loan Portfolio Review known internally as the LPR was that audit. NRB selected the Bangladeshi consulting firm Howladar Yunus & Co. The contract was signed in 2025 for Rs 6.25 million plus USD 271,670. The firm audited the ten largest commercial banks in Nepal, covering Rs 3.09 trillion in loans 62.38 percent of the entire commercial banking system. The review was completed in late 2025 and early 2026.

Its finding, as reported by Nepsetrading and confirmed in independent reporting by Republica and Nepal Monitor, is the chart above. The audited NPL ratio across the ten banks is 7.70 percent. Two of those ten banks are above 10 percent. The IMF's February 2026 staff statement, after the seventh ECF review, was explicit: "non-performing loans of the financial sector rising to 5.4 percent in January 2026 and are expected to be revised higher based on the recently completed LPR."

What the audit actually found

The Nepsetrading reporting on the LPR captured the specific mechanism the auditors identified, and it was textbook evergreening: "some banks have extended additional loans to large projects in order to classify them as 'performing,' despite insufficient physical progress and weak supporting documentation." In NRB's own loan classification rules, a loan whose underlying project has not made physical progress should be moved from "performing" to one of the watch-list, substandard, doubtful, or loss categories. The auditors found that this was not happening consistently. New loans were being extended to existing borrowers, the proceeds were being used to service old loans, and the old loans stayed in the "performing" bucket while the underlying project remained stalled.

NRB has formally acknowledged the finding. The central bank has announced plans to require additional loan-loss provisioning from institutions that fail to correct the classification weaknesses, and to develop a corrective roadmap addressing the identified shortcomings. The IMF in its February 2026 statement framed the next twelve months around exactly this point: the LPR will provide recommendations for strengthening bank balance sheets and enhancing NRB's regulatory approach. The headline number is going to be revised. The question is by how much.

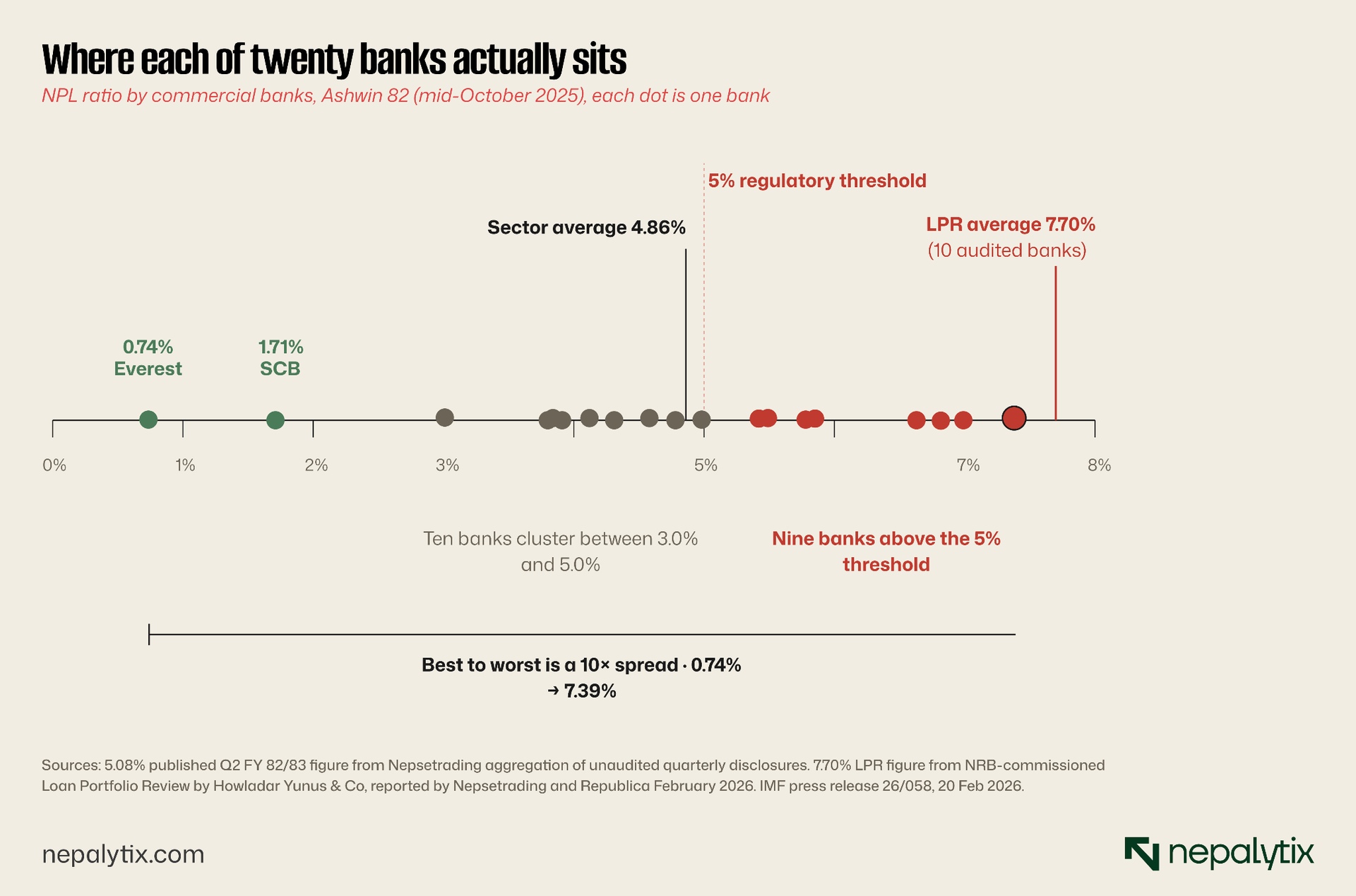

The dispersion the average compresses

The 5.08 percent published figure already conceals enormous variation across banks. Among the twenty commercial banks, the gap between the strongest and the weakest is now an order of magnitude.

Everest Bank's 0.74 percent NPL is ten times smaller than Himalayan Bank's 7.39 percent. The middle cluster, ten banks running between 3 and 5 percent is what holds the sector average down. The red cluster on the right contains nine banks that have already crossed the regulatory threshold. The LPR average of 7.70 percent, drawn as the rightmost red line, sits above where the worst-published bank actually reports, which is the point of the chart. The audit found that, on average across the ten banks it tested, the system as a whole resembles the worst-performing visible bank more closely than the sector average suggests.

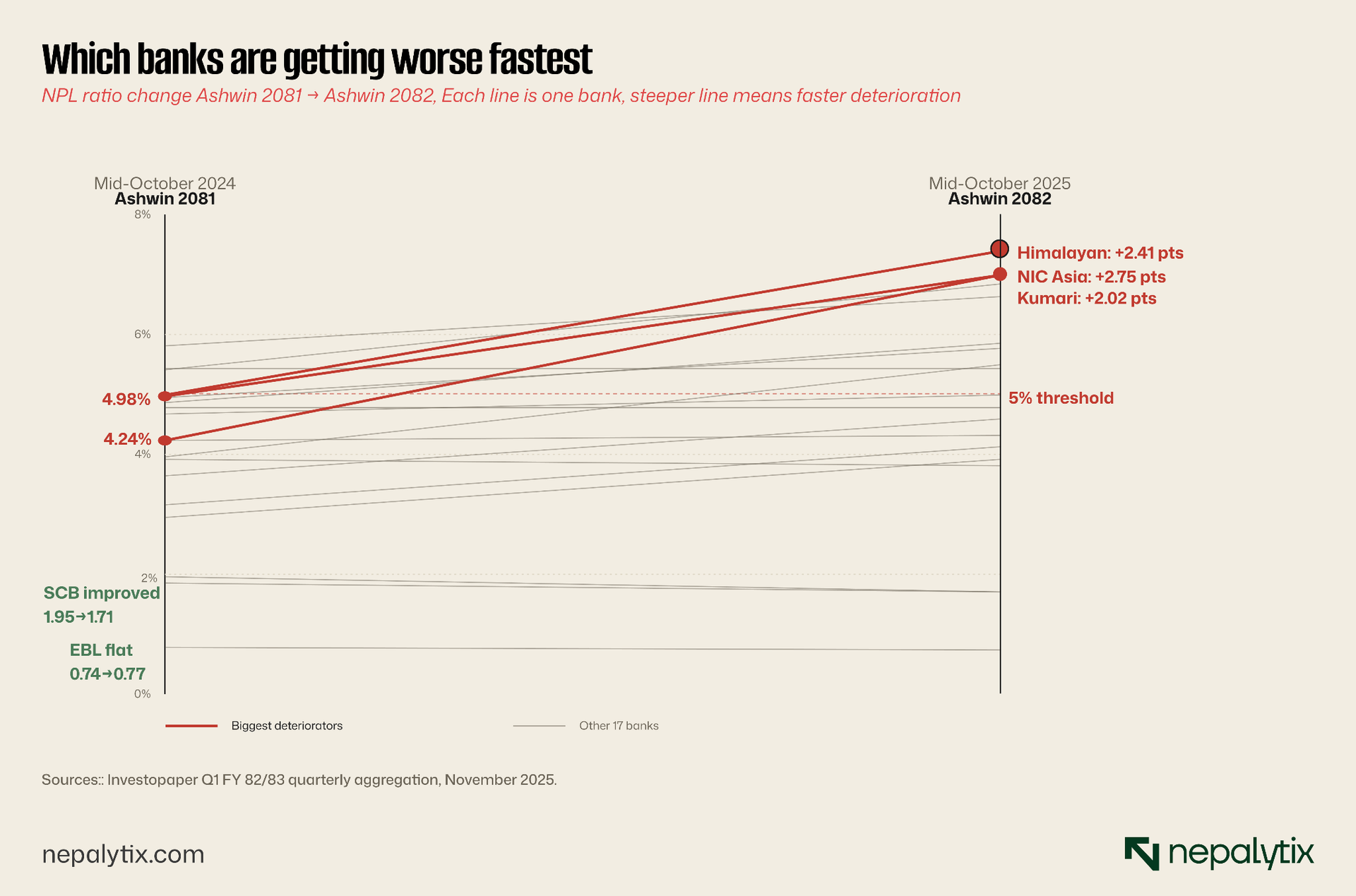

The velocity is uneven

If the level matters, the rate of change matters more. The same dataset, read year-on-year, shows that some banks have deteriorated rapidly over the past twelve months while others have held steady or improved. The slope chart below tracks each of the twenty banks from Ashwin 2081 (mid-October 2024) to Ashwin 2082 (mid-October 2025).

Three banks pull away from the cluster. NIC Asia jumped 2.75 percentage points in twelve months, from 4.24 to 6.99 percent. Himalayan jumped 2.41 points, from 4.98 to 7.39 and per the LPR ten-bank sample, that 7.39 figure is itself probably understated. Kumari jumped 2.02 points. By contrast, two banks held positions or improved: Everest stayed essentially flat at 0.77 to 0.74 percent, Standard Chartered actually improved from 1.95 to 1.71. The sector is not deteriorating uniformly. A subset of banks is deteriorating fast enough to pull the entire average up while most banks stay roughly where they were.

One bank, one year: what an outlier looks like up close

To see what fast deterioration actually means at the bank level, the cleanest case is Himalayan Bank. The published numbers tell the story; the LPR confirms it.

In April 2024, Himalayan Bank was a mid-pack commercial bank. Its NPL ratio of 4.96 percent put it 13th of 20 in the sector, slightly worse than average but inside the regulatory threshold. Twelve months later, the NPL ratio had jumped to 7.68 percent, the bank's net profit had collapsed by 74.33 percent to Rs 500 million, and its capital adequacy ratio had fallen to 10.84 percent, the lowest among all twenty commercial banks. By Ashwin 2082 the published NPL stood at 7.39 percent, making it the most stressed bank in the system on the published metric. Himalayan was one of the ten banks the LPR audited. The audit's finding of 7.70 percent average across the ten with two above 10 percent leaves Himalayan's true position somewhere readers will only learn when NRB publishes its corrective roadmap.

What happened at Himalayan is what the LPR identified happening across the sector. Loans to large borrowers stayed performing on the bank's books while the underlying projects stalled. Provisioning was inadequate. When the auditors arrived and applied NRB's own classification rules strictly, the reported numbers no longer held.

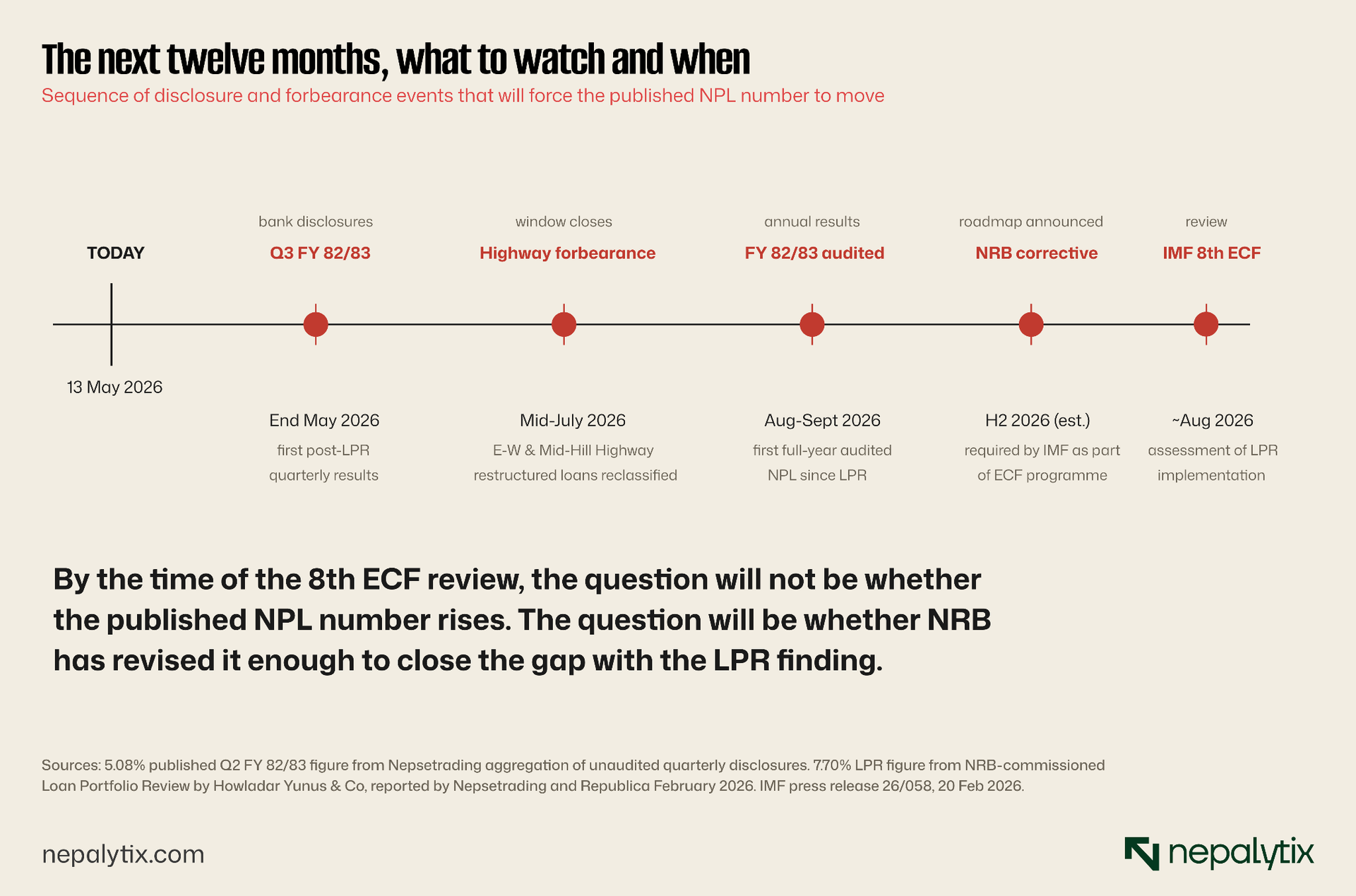

The dates that matter from here

What comes next is calendar-driven. Five dated milestones over the next twelve months will determine how much of the LPR finding ends up reflected in the published numbers and at what speed.

Each event in the calendar is a force pushing the published number toward the LPR finding. Q3 FY 82/83 quarterly disclosures, expected end May 2026 will be the first quarterly NPL reading after the LPR banks under regulatory pressure to reclassify will start showing higher numbers. The closure of the highway-displacement forbearance window in mid-July 2026 will reclassify restructured loans into the NPL bucket where the auditors say they belong. The FY 82/83 audited annual results, the first audited annual NPL since the LPR will be the most credible single data point of the year. The NRB corrective roadmap, when announced, will define the timing and scale of required reclassification. The IMF's eighth ECF review, expected around August 2026, will assess whether NRB has done what it committed to do.

The simpler reading

Until now, the argument that Nepal's NPL ratio understates banking stress was made by analysts and commentators outside the regulatory system. With the LPR, the argument is being made by the regulator itself. The published 5.42 percent figure for early 2026 has been characterised by the IMF, in writing, as a number that is expected to be revised higher. The audit that produced the higher number was commissioned by NRB, conducted by an external firm, paid for in part with public funds, and required as an IMF condition for emergency financing.

That changes the conversation. The question is no longer whether the headline NPL is an accurate measure of banking stress. The question is by how much it has to move, on what timeline, and which banks will be most affected when it does.

When the published 5.42 percent and the audited 7.70 percent reconcile, they will reconcile upward. The only open question is how much of the gap closes through reclassification, and how much through fresh deterioration on top of it.

For depositors, the relevant number remains the bank-specific NPL ratio, not the sector average. For shareholders of listed commercial banks, the relevant variable is which banks are inside the LPR's ten-bank cohort and which are not. For everyone watching Nepal's banking system, the relevant calendar is the one above. The headline number will move. The mechanism by which it moves will determine how disruptive the next twelve months are.