Upper Tamakoshi: Between Structural Recovery and Seasonal Risk

Upper Tamakoshi Hydropower is at a critical inflection point after delivering two consecutive profitable quarters, a 36% share price recovery from its 2024 low, and its first AGM in nearly three years.

Two consecutive profitable quarters. The first AGM in three years is done and dusted. A share price up 36 percent from its 2024 low. The structural read has held and the market has already started paying for it. What comes next is whether the dry season honours the trajectory or breaks it.

In Summary

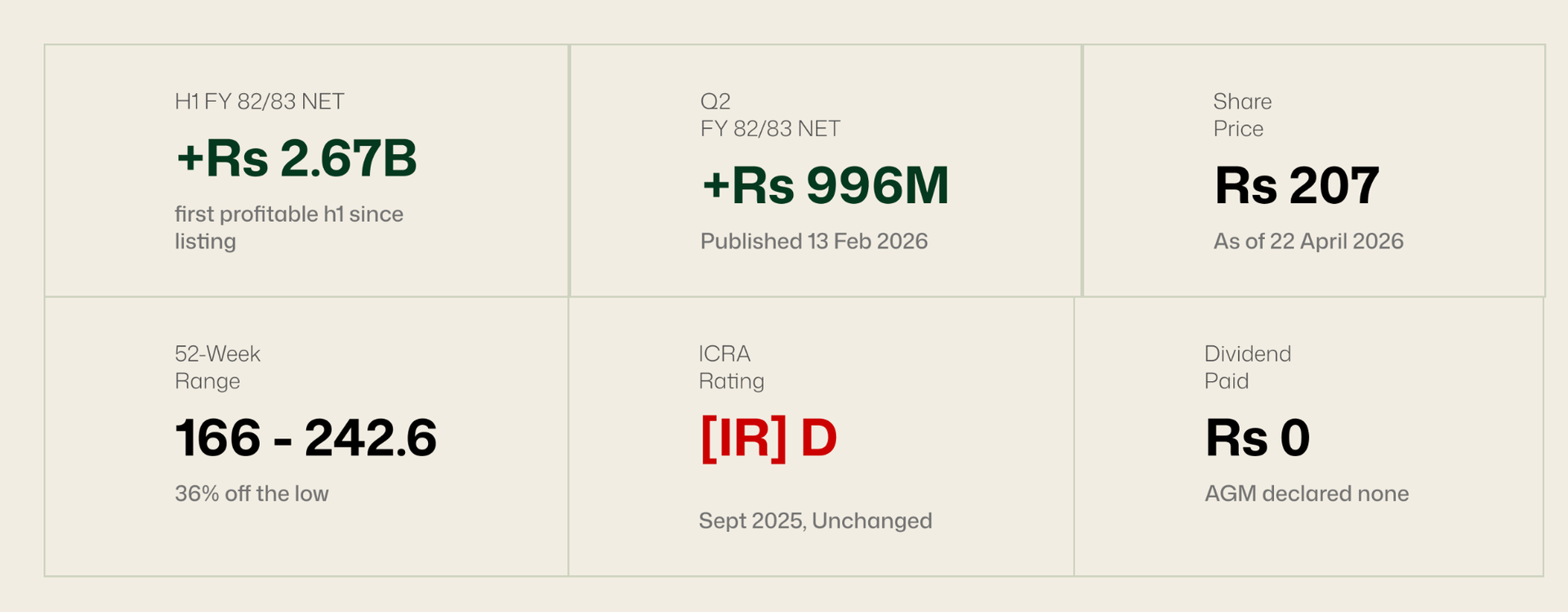

→ Q2 FY 82/83 results published on 13 February 2026 showed a net profit of Rs 996.5 million, the company's second consecutive profitable quarter and a swing of more than Rs 1.8 billion against the Rs 821 million loss reported in Q2 of the prior fiscal year. Cumulative H1 net profit reached Rs 2.67 billion already larger than the entire annual loss the company posted in FY 81/82.

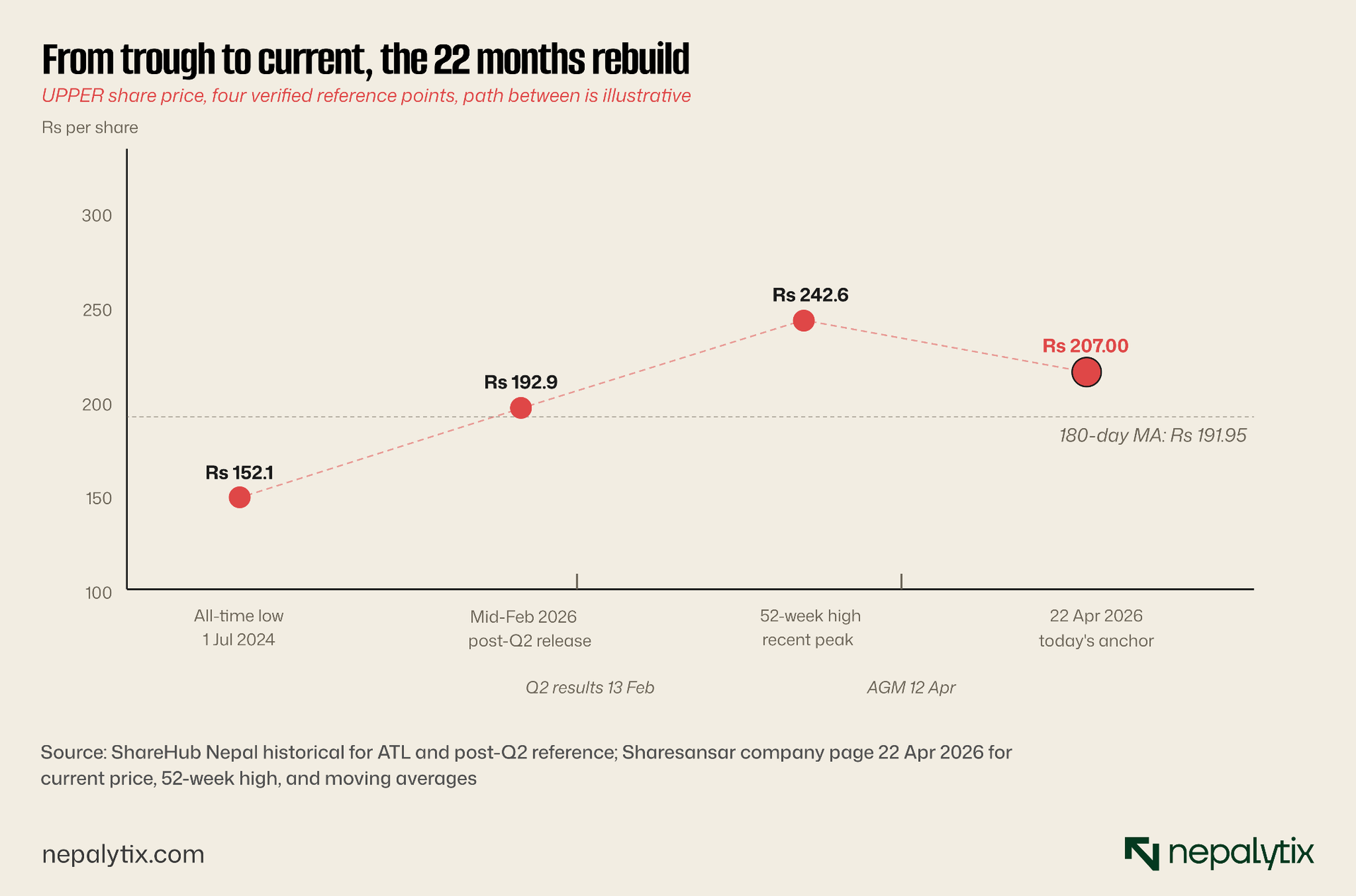

→ The market has registered the change. From a 1 July 2024 all-time low of Rs 152.10, UPPER traded up to Rs 242.60 over the past 52 weeks and was at Rs 207.00 on 22 April 2026 a 36 percent gain from the trough. The 180-day moving average sits at Rs 191.95, the 20-day at Rs 215.56, and short-term moving-average signals have turned bearish from the recent peak even as the long-term trend remains up. The stock is trading on momentum from the operating improvement, not on resolved credit or governance concerns.

→ On 12 April 2026, the company held its combined 16th and 17th Annual General Meetings, the first AGMs convened in nearly three years. Annual reports and financial statements for FY 2079/80 and FY 2080/81 were approved together. The agenda's most-watched item, the appointment of two independent directors was carried forward as a proposal; the post-AGM disclosures available at the time of writing do not explicitly confirm whether the appointments were finalised on the day. No dividend was declared. The ICRA Nepal [ICRANP-IR] D rating remains in place. The "Issuer Not Cooperating" tag remains attached.

→ Two questions now matter more than the third. First: Does Q3 FY 82/83, the first of the two dry-season quarters confirm or break the trajectory? Filing deadline is mid-May 2026; results may already be in by the time this is read. Second: Does the FY 82/83 audited full-year result, expected mid-August, become the company's first net-profitable year since listing? The third question whether ICRA reinstates the company to active cooperation and reconsiders the rating sits on a different clock and is the binding constraint on corporate credit access regardless of equity-side improvement.

The Q1 FY 82/83 print of Rs 1.67 billion in net profit was real, but it landed against a backdrop of debt-service delays, a credit downgrade, an 88-day flood outage, and a three-year governance gap. The structural reading that the debt amortisation curve had begun to bend in the company's favour competed with the seasonal reading that Q1 is the strongest wet-season quarter and that full year results in three prior fiscal years had reverted to loss.

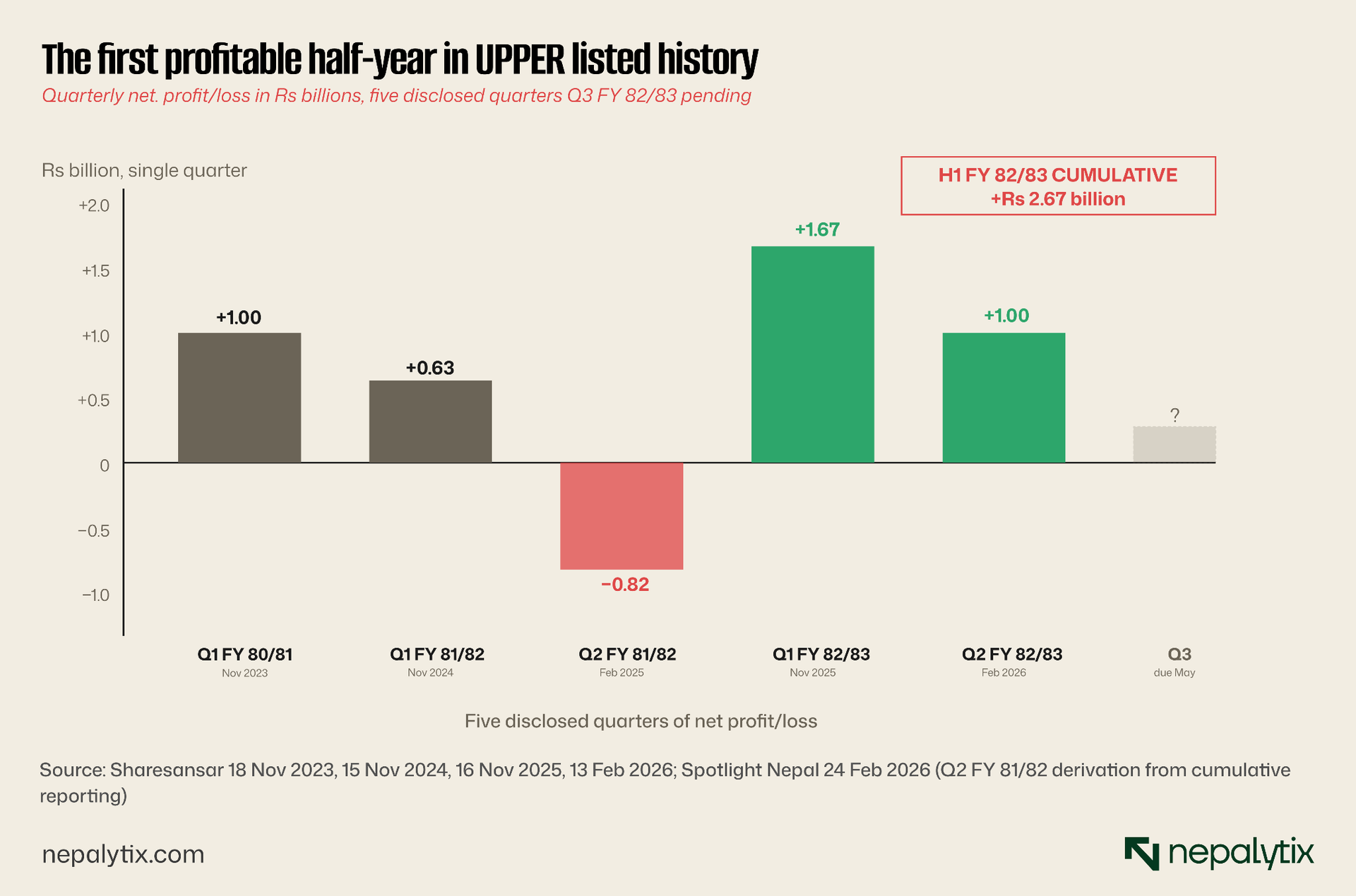

Q2's Rs 996.5 million in net profit published on 13 February was the first piece of evidence in three years that the structural reading is correct. Q2 covers Kartik through Poush, the second wet-season quarter and is historically the second-strongest quarter of the year. Even with the expected sequential decline from Q1, Q2 stayed firmly positive and posted a Rs 1.8 billion year-on-year improvement against the Rs 821 million loss in the same quarter of the previous fiscal year. The half year cumulative of Rs 2.67 billion is by itself larger than the entire annual loss UPPER reported in FY 81/82.

The chart tells the cleanest version of the operating story. In Q1 FY 80/81, the company posted Rs 1.00 billion in profit before reverting to a full-year loss. In Q1 FY 81/82, the print dropped to Rs 0.63 billion before Q2 turned to a Rs 821 million loss and the full year ended at a Rs 2.57 billion deficit. In Q1 FY 82/83, profit jumped to Rs 1.67 billion. Q2 came in at Rs 0.996 billion, still firmly positive and the first time in the company's listed history that two consecutive quarters have printed profit at this magnitude.

The largest plant, the longest wait

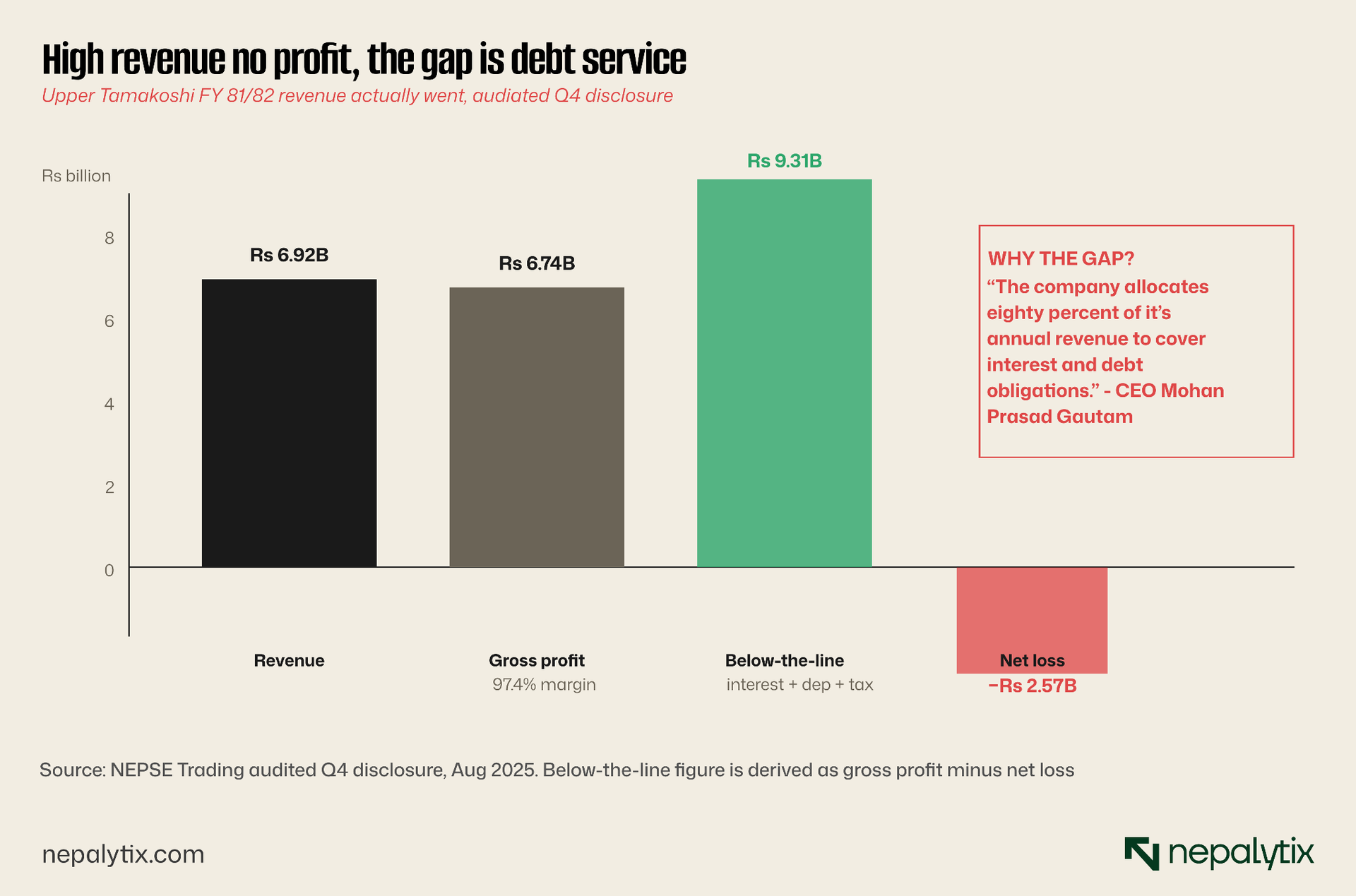

Upper Tamakoshi Hydropower Limited began commercial operation on 11 September 2021. Four and a half years later by the close of fiscal year 2081/82 the company had cumulatively reported losses totalling several billion rupees, paid no dividend, and seen its book value per share fall from Rs 56.88 to Rs 45.34 in a single year. The 456 megawatt installed capacity, the largest of any plant in Nepal, had produced by every reasonable accounting measure, less value for public shareholders than the smaller hydropower projects listed alongside it on NEPSE.

The puzzle resolves once the balance sheet is read alongside the income statement. UPPER is not an operating problem. The plant generates electricity at gross margins above 97 percent entirely normal for hydropower where fuel cost is zero and operating expense is a small fraction of revenue. The problem is what sits below the operating line: a long-term debt load that stood at Rs 73.01 billion as of Q1 FY 80/81 disclosure, has since amortised to Rs 45.36 billion by mid-Ashoj FY 82/83 although the path between those figures has not been smooth. The amortisation has come alongside delays, defaults, and a credit-rating action that took the company from BB& to the agency's default category in a single step. Every rupee of revenue passes through that capital structure on its way to the bottom line.

That structure was put in place during construction. The project's original 70:30 debt-to-equity ratio became progressively heavier through a decade of construction delays, the 2015 Gorkha earthquake, the 2015-16 Madhesh-Terai unrest, the 2020 pandemic each of which extended timelines and capitalised interest into the debt principal. By the time the first turbine spun in 2021, the company carried roughly Rs 76 billion in total borrowings against a Rs 10.59 billion paid-up capital base. In October 2023, the company conducted a 1:1 rights issue that doubled paid-up capital to Rs 21.18 billion. The leverage moved, but it did not move enough to change the underlying arithmetic.

Three forces, one loss

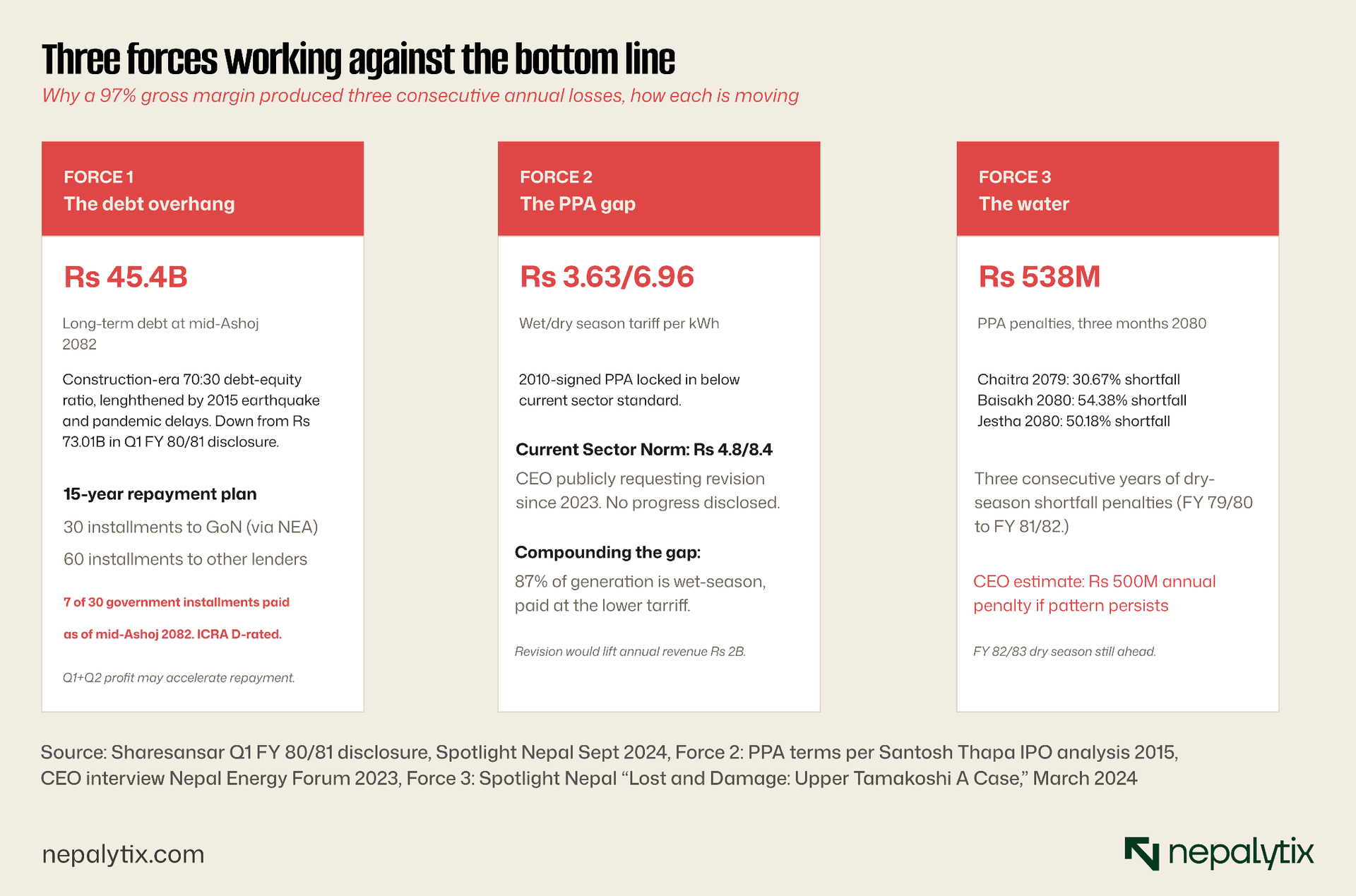

To understand why a 97 percent gross margin business has historically lost money requires reading three separate stress points at once. Each on its own would be manageable. Together, through the construction-era debt build and the operating years that followed, they produced the structural mismatch between what the plant earns and what the financial structure demands. The Q1 and Q2 FY 82/83 results show that the arithmetic has begun to bend but they do not change the underlying mechanics.

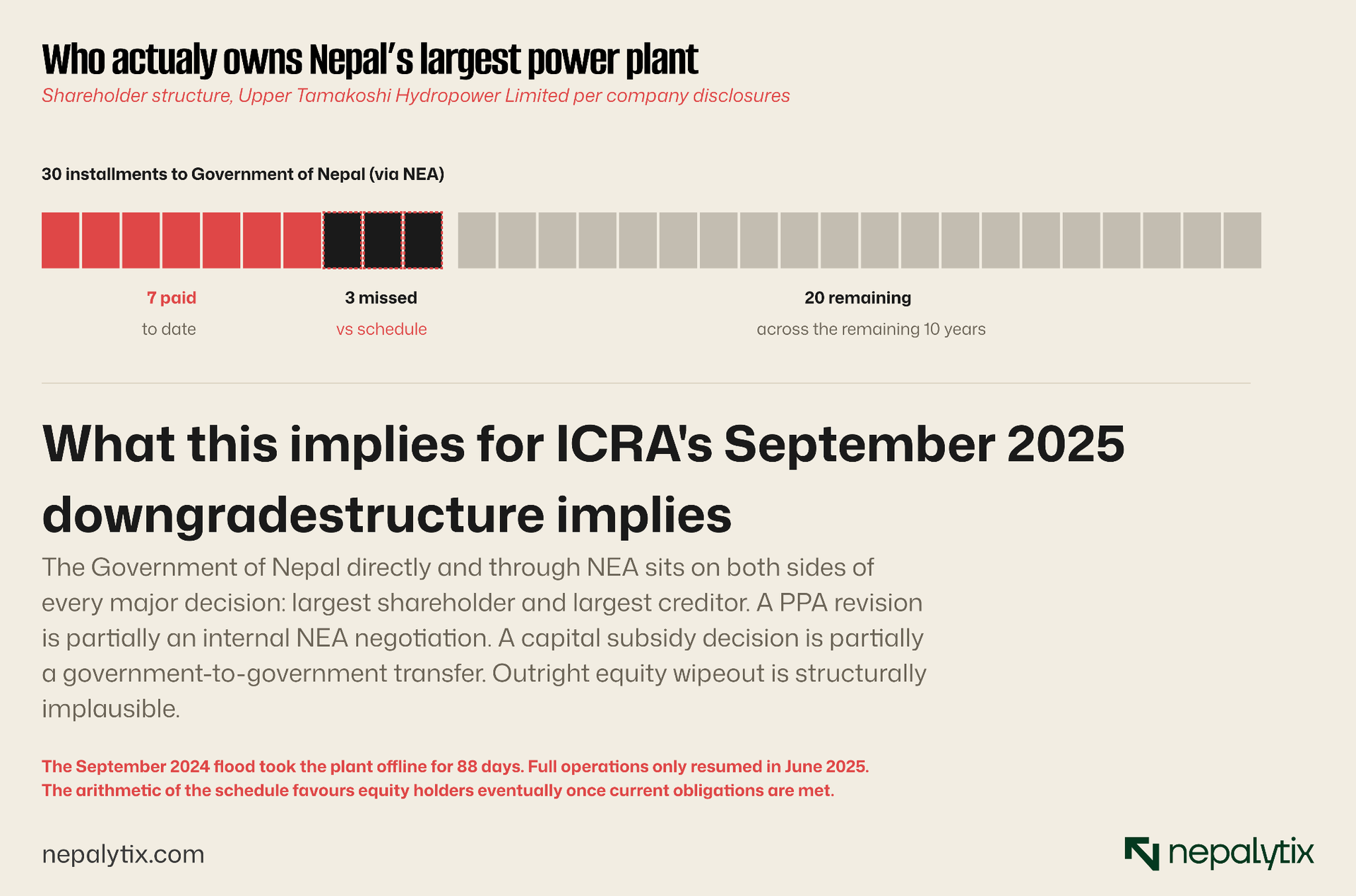

The debt overhang. The long-term debt sits on a 15-year repayment schedule, structured as 30 installments to the Government of Nepal (channeled through NEA) and 60 installments to the basket of institutional lenders that includes Employees Provident Fund, Nepal Telecom, Citizen Investment Trust and Rastriya Beema Sansthan. As of mid-Ashoj of fiscal year 2082/83, the company reported it had paid 7 of 30 government installments and 14 of 60 to other lenders. Five years into a fifteen-year schedule, a fully-current schedule would have completed 10 of 30 government installments. The gap between the schedule and the actual record sits at the heart of the September 2025 ICRA Nepal downgrade. Each year the company pays down debt, the interest expense on the residual balance declines, and a larger share of operating cash flow becomes available to equity but the path between today and that future point now runs through demonstrated repayment ability, not just arithmetic. The H1 FY 82/83 profit creates room to accelerate; whether management has done so is not yet publicly disclosed.

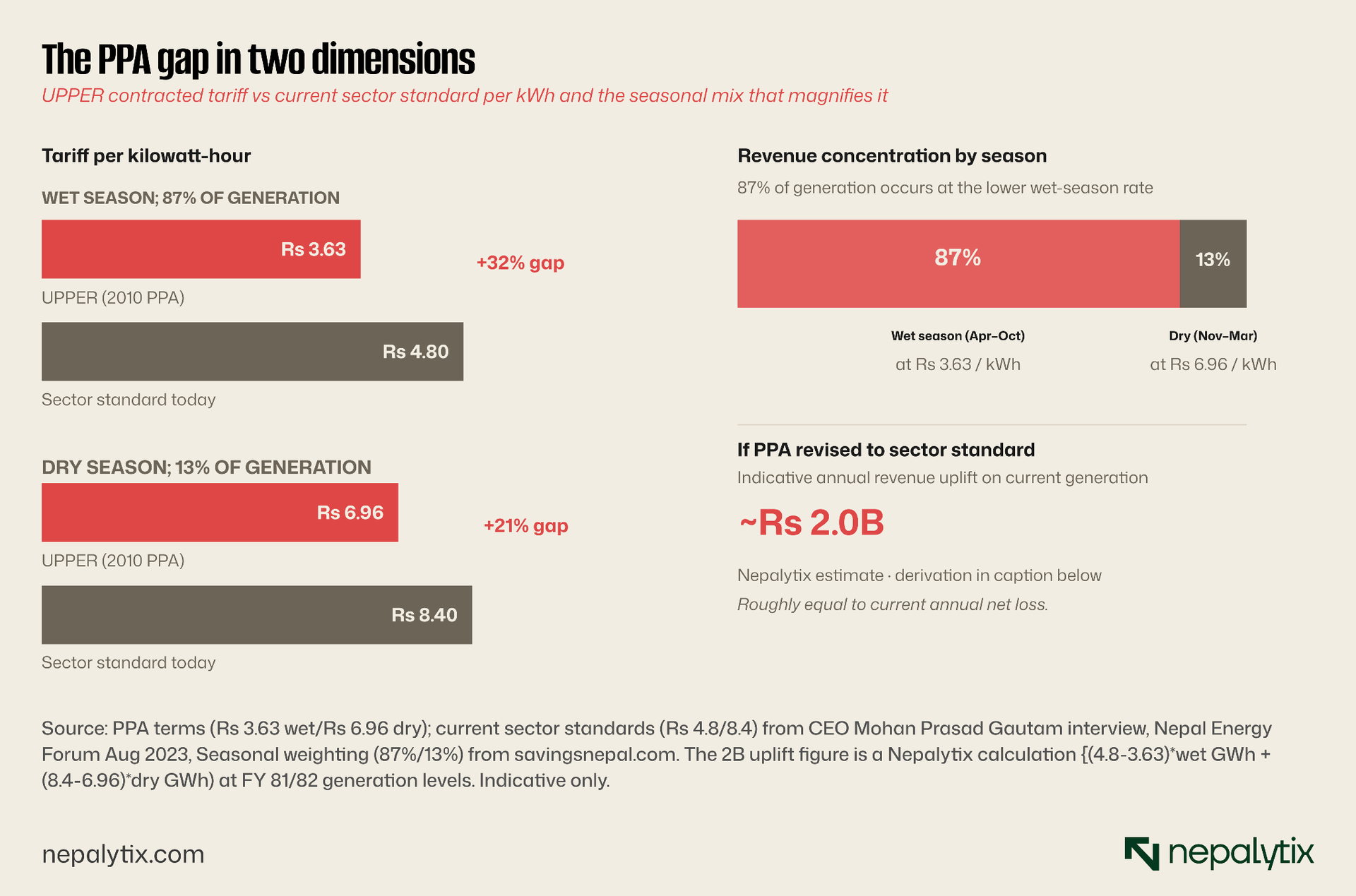

The PPA gap. The Power Purchase Agreement Upper Tamakoshi signed with NEA in 2010 fixed the tariff at Rs 3.63 per kilowatt-hour during the wet season and Rs 6.96 per kWh during the dry season. The current sector standard for similarly-sized projects is Rs 4.80 wet and Rs 8.40 dry. The PPA is structured with a 3 percent annual escalation for the first nine years, after which the rate becomes a flat Rs 5.30 per kWh for the remainder of the 35-year license. Embedded in that structure is a long-running mismatch, the project's revenue per unit is permanently below what newer projects of comparable size earn. CEO Mohan Prasad Gautam has publicly requested PPA revision since taking office in early 2023.

The compounding effect is geographical. Approximately 87 percent of Upper Tamakoshi's annual generation occurs during the wet season when river flow is high and the tariff is low. Only 13 percent comes during the dry months when the tariff is higher. The plant's revenue mix is structurally weighted toward the lower-rate period.

The water. Three consecutive fiscal years, FY 79/80, 80/81 and 81/82 have seen Upper Tamakoshi miss its contracted dry-season energy delivery to NEA. The reason is hydrological: declining river flow during the late-winter and early-summer dry months, attributed to changing snow-melt patterns and reduced winter precipitation. The three-month period of Chaitra-Jestha in fiscal year 79/80 produced PPA penalties of Rs 538 million. The CEO has publicly stated that, if the climate pattern persists the company could face annual penalties approaching Rs 500 million. The FY 82/83 dry season Q3 and Q4 is now the test.

The capital structure, in detail

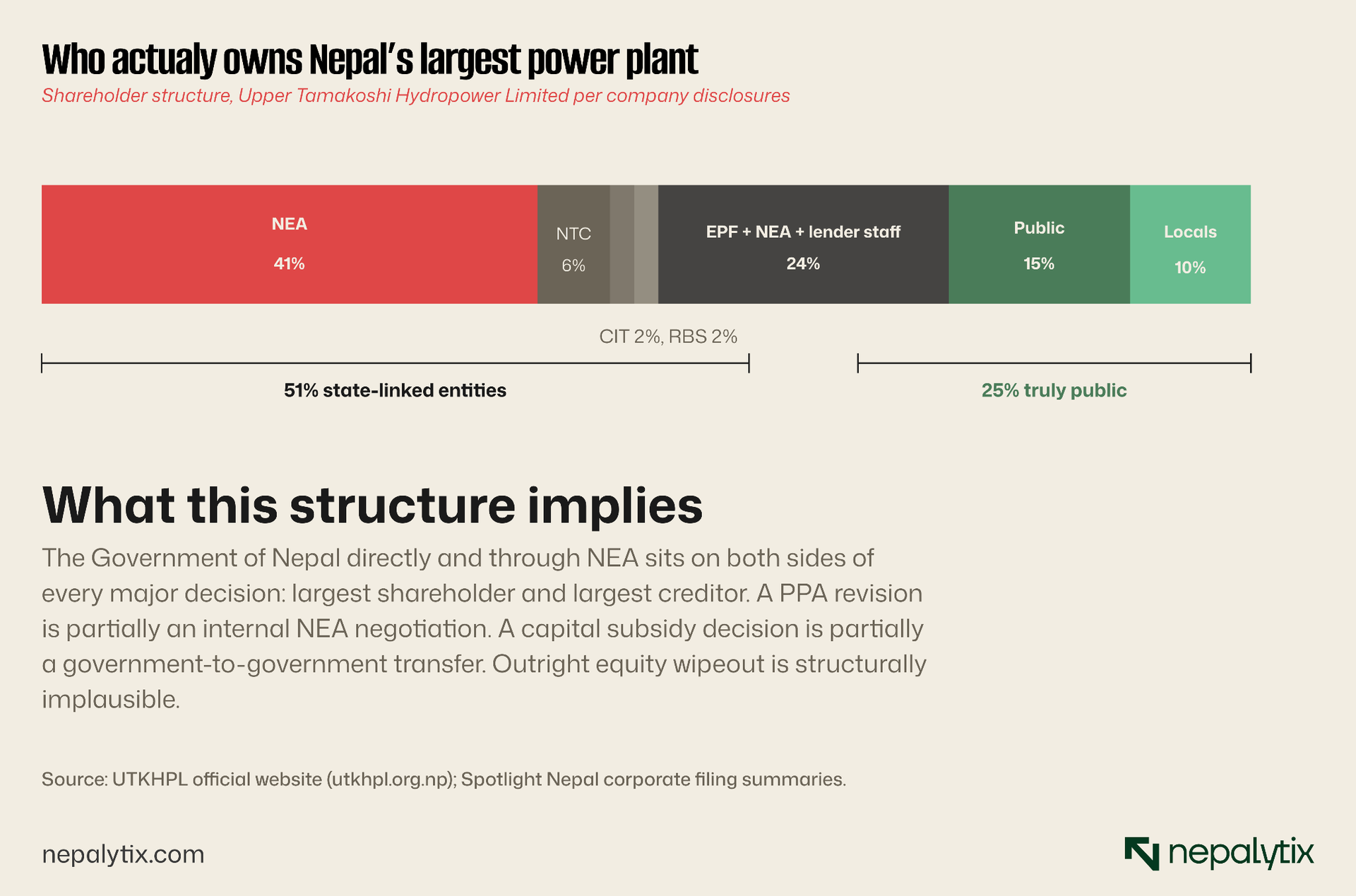

To value any leveraged asset, the shape of the debt matters as much as its size. Upper Tamakoshi's debt is unusual in three respects: it is held by domestic state-linked institutions rather than commercial banks, it is structured on a 15-year amortisation rather than bullet maturities, and the largest single creditor is the Government of Nepal itself, which also happens to be through NEA's 41 percent equity stake, the largest shareholder.

The 15-year amortisation matters. Unlike a bullet-maturity bond that would require refinancing at the end of the term, Upper Tamakoshi's structure is one of steady principal paydown over time. Each successful year reduces the principal, reduces the interest expense on the residual balance, and incrementally moves more of the operating cash flow toward equity. The mathematical inflection point where net income turns positive and stays positive was approaching for several years. The Q1 and Q2 FY 82/83 results suggest it has arrived.

The Rs 2.28 billion capital subsidy from the Government of Nepal is a structural offset that has not yet been deployed. The company is entitled to receive Rs 5 million for every megawatt of installed capacity at the 456 MW project, a one-time grant that can be used either to retire existing debt or to fund the planned Rolwaling diversion. Management has not publicly committed to which use. The H1 FY 82/83 profit may change that calculus.

The market has been listening

UPPER closed at Rs 207.00 on 22 April 2026, against a 52-week range of Rs 166.00 to Rs 242.60. The 120-day moving average sits at Rs 209.83, the 180-day at Rs 191.95. Short-term technical signals turned bearish from the recent peak, MA5 at Rs 213.10 and MA20 at Rs 215.56 both above the current price but the long-term trend has been a sustained rebuild from the 1 July 2024 all-time low of Rs 152.10. The stock has roughly tracked the improving operating data with a lag of a few months, then begun pricing forward.

Two observations from the price path. First, the bulk of the move happened in the months following the Q1 disclosure in November 2025 and continued through the Q2 release in February 2026. The stock that traded under Rs 175 in early January 2026 had reached Rs 242 by April, a 38 percent gain on what was, at the time, two quarters of cumulative profit and the imminent AGM. Second, the most recent print at Rs 207 sits roughly 14 percent below the recent peak, with the 5-day and 20-day moving averages signalling near-term consolidation. The stock is not pricing additional good news.

The 180-day moving average of Rs 191.95 is a useful anchor for what the market thought the company was worth before the operating data started clearly turning. Trading above that line says momentum is intact. Trading below it would say the trade has given up its conviction. The current price sits roughly 7 percent above that line, not aggressive, not exhausted, comfortable.

What the AGM did and didn't do

On 12 April 2026, Upper Tamakoshi held its combined 16th and 17th Annual General Meetings at the Tribhuvan Army Officers' Club, Bhadrakali. The last regular AGM was in Shrawan 2080 (August 2023). The three-year gap, while never formally explained in public disclosures, paralleled the construction-to-operation transition, the rights issue, the 2024 flood, and the ICRA downgrade. The April meeting closed that gap.

What was achieved at the meeting is, in formal terms, substantial. Annual reports and audited financial statements for two fiscal years FY 79/80 and FY 80/81 were tabled and passed. The auditor's reports, profit and loss accounts, balance sheets, cash flow statements, statements of changes in equity and accounting policy disclosures were approved together. A special resolution ratifying past social-support transfers to Dolakha-area institutions in FY 79/80 and FY 80/81, distributions previously made under the board's delegated authority was also approved.

What was not achieved, or where the post-AGM disclosures available at the time of writing do not provide clarity, are the items that mattered most to the equity-side investor case. The two independent director appointments included in the published agenda are not confirmed in publicly accessible AGM-outcome reporting. The reappointment of statutory auditors for FY 82/83 was on the agenda but, again, the outcome is not explicitly confirmed in the brief news coverage available. No dividend was declared. The "Issuer Not Cooperating" tag attached to the ICRA Nepal rating was not addressed in publicly disclosed AGM commentary.

For shareholders, the meeting served two purposes. It restored a formal channel between the company and the public-share holders that had been missing for three years. And it produced the audited records covering the project's first two full operating years, records that will eventually feed into rating agency assessments, lender reviews, and any future PPA revision discussion with NEA. The meeting did not deliver a dividend, a strategic announcement on the Rs 2.28 billion capital subsidy deployment, or new clarity on the path to ICRA reinstatement. Those remain outstanding.

The seasonal test ahead

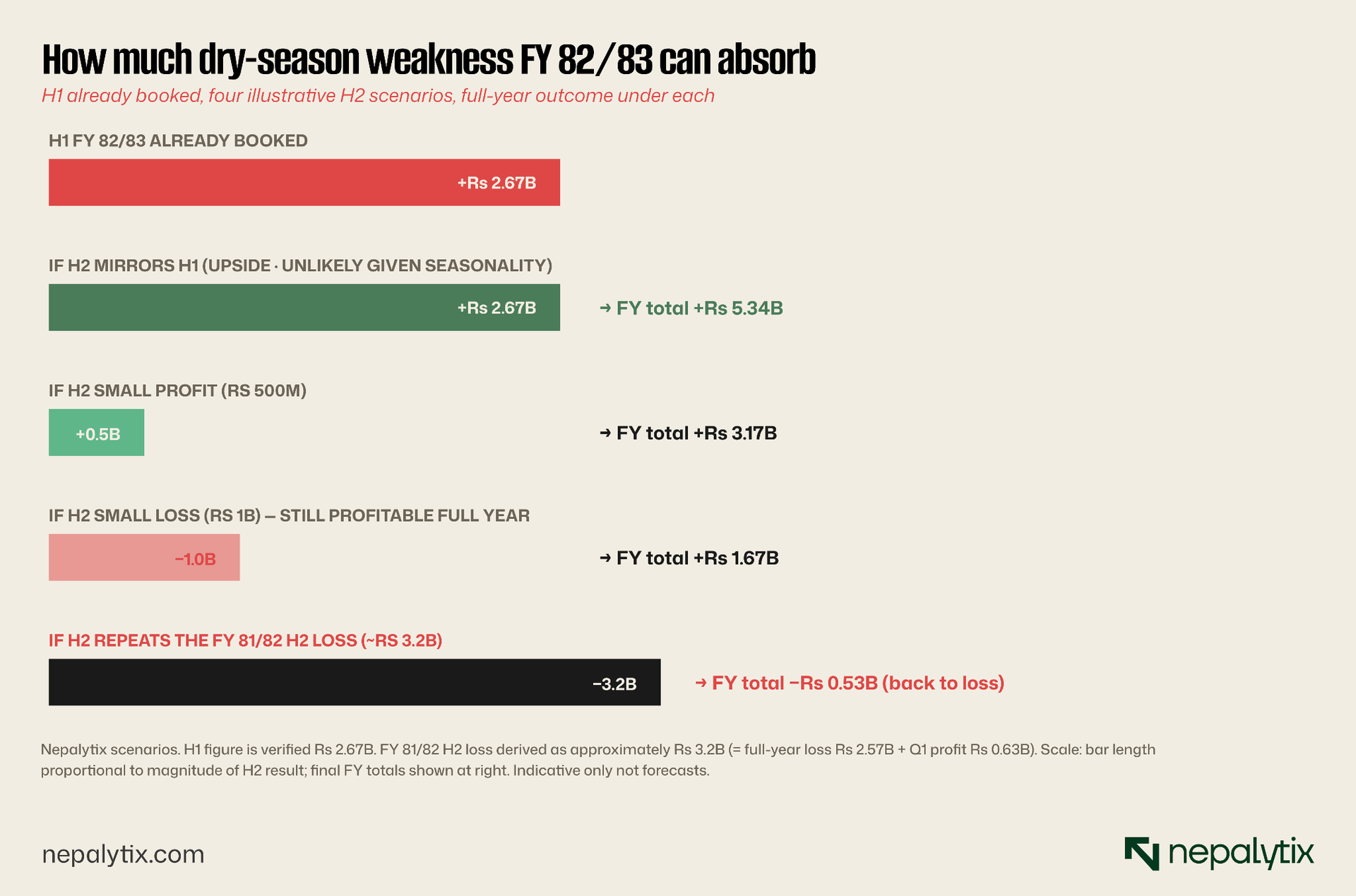

Half-year cumulative net profit of Rs 2.67 billion is, by any reasonable measure, a structural inflection. It is also, in the company's recent operating history, exactly when caution becomes appropriate. In each of the prior two completed fiscal years, the wet-season quarters were profitable. The full year was not. The transition happened in Q3, Q4 or both the dry-season quarters when river flow falls, generation falls and the PPA-linked penalty mechanism turns from theoretical to real.

What's different in FY 82/83 is the base. With Rs 2.67 billion already booked through H1, the company can absorb an aggregate H2 loss of up to roughly Rs 2.66 billion and still end the year break-even. That comfort margin did not exist in FY 80/81 or FY 81/82, when full-year results swung negative on H2 alone. The PPA penalty structure has not changed; the climate-driven dry-season generation shortfalls of the past three fiscal years have not, as of public disclosure, reversed.

The chart says in plain terms the comfort margin for FY 82/83 is now substantial but not infinite. A repeat of last year's dry-season collapse, on the same magnitude would still produce a small full-year loss. A meaningful but lesser dry-season weakness, say a Rs 1 billion H2 net loss would still produce a Rs 1.67 billion full-year profit, which would be the company's first net-profitable year since listing. Almost any H2 outcome short of "as bad as FY 81/82 H2" produces a positive annual result.

The Rolwaling option

Upper Tamakoshi has one structural lever available that no other Nepali hydropower company of comparable size has: the Rolwaling River diversion. Engineering work has been underway for several years to divert the Rolwaling River into Upper Tamakoshi's existing intake pond. Once complete, the diversion will add an estimated 212 GWh of annual energy generation to the existing 456 MW plant without requiring additional installed capacity, additional civil works at the powerhouse or a new PPA. The energy enters the existing infrastructure, is sold under the existing PPA, and accrues to existing revenue.

A separate parallel project, the 22 MW Rolwaling Khola Hydroelectric Project will produce an additional 105 GWh annually under its own PPA. The two projects together would add approximately 317 GWh to Upper Tamakoshi's annual generation portfolio. At UPPER's existing PPA blend, a Nepalytix calculation suggests that it translates to incremental annual revenue in the order of Rs 1.2 to 1.6 billion, the exact figure depending on the seasonal mix of the new generation and the eventual PPA terms for the Rolwaling Khola HEP. Even at the lower end of that range, the addition is meaningful relative to current revenue of Rs 6.92 billion.

The strategic value of the Rolwaling addition lies in its seasonality. The CEO has publicly stated that the diversion will increase dry-season output by approximately 15 percent. The diversion's incremental energy arrives precisely in the months when the existing plant is short of contract obligations, generates penalties, and earns the higher dry-season tariff. In other words, the Rolwaling addition is structured to attack all three of the company's current stress points simultaneously: it adds revenue to amortise debt faster, it adds dry-season generation to reduce PPA penalties, and it earns the higher tariff that the company currently underdelivers on.

The execution risk is not trivial. The 250-metre main diversion tunnel has been opened, but completion is contingent on continued explosives supply and construction logistics. The CEO's public estimate is three years from continuous explosives supply meaning the in-service date depends on when supply begins rather than on the calendar. Until completion, Rolwaling is a call option on the financial structure rather than a confirmed earnings contribution.

Credit, governance, and the things the AGM did not fix

The operating story has moved. The credit story has not. ICRA Nepal's [ICRANP-IR] D rating, issued in September 2025 after the company delayed debt servicing by more than 30 days, remains in place. The agency's subsequent move to flag UPPER as "Issuer Not Cooperating" with a notice for rating withdrawal means the company is no longer participating in active surveillance with the rating agency. There has been no public disclosure of when or whether the company will resume cooperation, what conditions it would need to meet for the rating to be reconsidered or whether the underlying debt-service delays have been cured.

The repayment record shows the gap that triggered the original downgrade. As of mid-Ashoj 2082, the company had paid 7 of 30 installments to the Government of Nepal and 14 of 60 to other institutional lenders against a fully-current schedule that would have completed 10 and 20 respectively. Whether the strong H1 result has translated into accelerated repayment is not disclosed in any public document available at the time of writing. The mid-Ashoj data point predates the strong Q2 result, and the next observable measure of debt-service performance is the audited Q4 release expected in August.

The governance story sits between the operating story and the credit story. The April 2026 AGM closure of a three-year gap was a meaningful structural fix. The retained corporate practice of NEA's Managing Director continuing as Chairman of UPPER, public-investor representation on the board remaining a minority position, no public confirmation of independent director appointments has not changed. Public shareholders received approved annual reports for two years that ended more than three years ago. They did not receive a dividend, a current-year strategic statement, or a corporate roadmap that addresses the ICRA situation.

For the equity case, that distinction matters. Operating recovery is reflected in the share price; the price action from Rs 152 to Rs 207 has done the work of pricing it. Credit recovery requires a different set of disclosures, sustained debt service, ICRA re-engagement, removal of the INC tag, eventually a rating action. None of those events has been signalled by management. Until they are, UPPER trades as a recovering operator with an unresolved credit profile. That is what Rs 207 is paying for.

How UPPER compares to the listed hydropower sector

Two listed hydropower names provide useful comparison points. Chilime Hydropower (CHCL) is the most established large-cap hydropower stock on NEPSE listed since 2005, with an all-time high of Rs 2,794 in 2014 and an established record of dividend distribution. Sahas Urja (SAHAS) is a smaller but newer listing with a strong recent profitability profile. Together they bracket the universe of "operating hydropower companies investors actually compare UPPER against."

Two observations from the table. First, UPPER's market capitalisation now sits close to Chilime's despite UPPER being a 456 MW project versus Chilime's 22 MW standalone, the market has begun to re-rate the size advantage as operating data improves, but the gap to Chilime's full premium has not closed given the unresolved credit profile. Second, the P/B ratios sit close together (UPPER 3.89×, CHCL 3.93×, SAHAS 3.60×) suggesting that the listed hydropower sector trades on a fairly tight book-value band, a multiple that prices the operating asset plus expansion optionality, somewhat independently of current earnings.

For the broader sector context, the first quarter of FY 2082/83 was a strong period for listed hydropower. According to compiled NEPSE filings reported in November 2025, 92 listed hydropower companies posted Rs 5.07 billion in combined Q1 net profit, up 92.92% year-on-year, with only 13 companies in loss (down from 17 the prior year). UPPER's Rs 1.67 billion led the sector, single-handedly representing roughly one-third of total hydropower-sector profit for the quarter.

Financial summary

The table below assembles verified quarterly and annual disclosures into a single financial picture. Multi-year line items below the operating margin are not disclosed at this resolution in public summaries; cells marked "n.d." indicate data not disclosed in the sources reviewed for this piece.

Valuation, given what we now know

With H1 net profit of Rs 2.67 billion booked and 211.8 million shares outstanding, H1 EPS is Rs 12.61. Annualised by simple doubling, full-year EPS would be Rs 25.22. But H2 is unlikely to mirror H1, the dry-season pattern has been consistent for three fiscal years. A more realistic full-year EPS estimate, based on the scenarios in Chart 8, sits in a range of Rs 8 to Rs 15.

At Rs 207.00, that range implies a P/E multiple of 14× to 26×. Both are richer than the headline 6.1× figure that appeared after the Q1 disclosure when the market had not yet absorbed the recovery. Both are below the 73× that Chilime Hydropower currently trades on. UPPER's price-to-book ratio at the current price is roughly 3.89× against the most recently disclosed book value per share of Rs 53.25 broadly in line with the listed-hydropower sector band.

The reading depends on which H2 the company posts. The case for further upside requires H2 to deliver a net result better than a Rs 1 billion loss anything in that band or better confirms the first net-profitable year since listing, and the current multiple looks fair to cheap relative to peers. The case for caution sits with the historical pattern, where each of the last two fiscal years has seen a multi-billion-rupee H2 loss erase the H1 profit and produce a full-year loss. With ICRA still flagging concerns and the climate-driven dry-season vulnerability unchanged, the historical pattern cannot yet be dismissed as resolved.

The right way to read the current price is to recognise what it is and isn't doing. It is not pricing a guaranteed first profitable year at Rs 207 versus a book value of Rs 53.25, the market is paying a 3.89× multiple of book that broadly tracks the listed-hydropower sector, neither a discount for the unresolved credit profile nor a premium for the operating recovery beyond what peers receive. It is, in other words, pricing UPPER as a normal listed hydropower company. That is itself a significant reprice from where it traded twelve months ago, when it priced as a distressed leveraged asset.

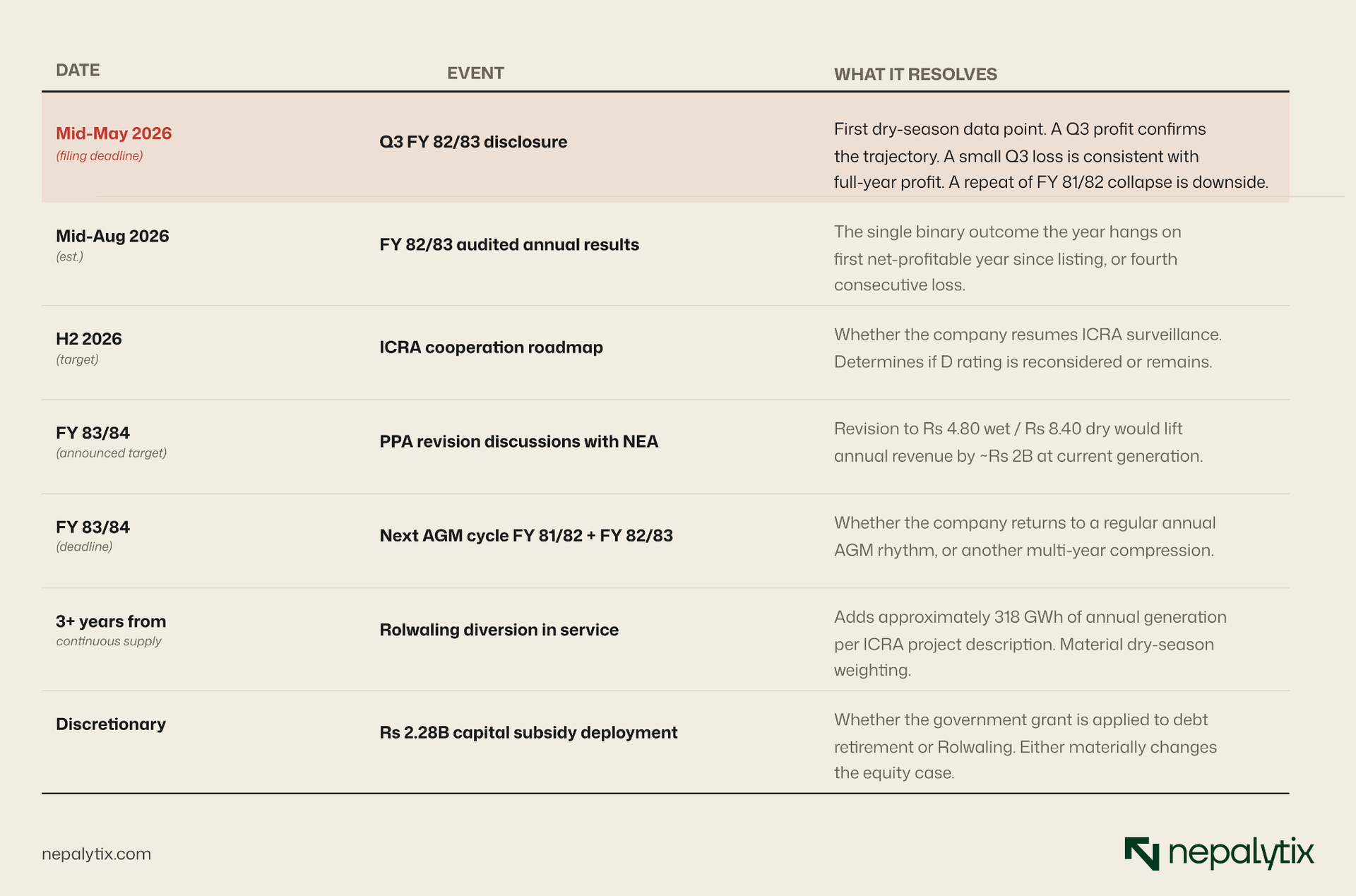

Catalyst calendar: What to watch and when

The closing position

Upper Tamakoshi has run the longest leveraged build, the deepest seasonal P&L volatility, and the worst credit event of any operating hydropower company on NEPSE. It also runs the largest plant, posts the highest single-quarter sector profit, and holds the most consequential capacity-expansion option in Nepali listed energy. The valuation reflects the tension between those two halves of the story, not a resolution of it.

The Q1 and Q2 FY 82/83 disclosures together delivered the first piece of evidence in three years pointing toward structural recovery. The ICRA D rating, the missed AGM cycle ratified only in April 2026, the 88-day flood outage, and the three-installment gap on the government loan all point in the opposite direction. None of these has been resolved at the time of writing. The Q3 disclosure due in mid-May is the next forced data point, and the FY 82/83 audited results in August are the verdict the year hangs on.

For shareholders entering at Rs 207, the upside scenario requires Q3 to print at or above breakeven and the full year to come in positive. For shareholders already holding from below Rs 175, much of the trade has already been done; the question is whether to hold through the dry-season test or take risk off given the still-unresolved ICRA situation. For depositors and bondholders in the broader Nepali financial system, UPPER's credit trajectory remains the single most important determinant; the D rating and INC tag have not been withdrawn.

What changes between now and the audited FY 82/83 result is, in the company's recent history, the entire valuation case. A first net-profitable year would be a structural reset for the equity, the credit and for management's negotiating position with NEA on the PPA. A fourth consecutive net-loss year would push the case back into pure optionality, and the price would re-test. The current Rs 207 on either reading is honest pricing neither cheap nor expensive given the unresolved tail risks.