What are development banks even for?

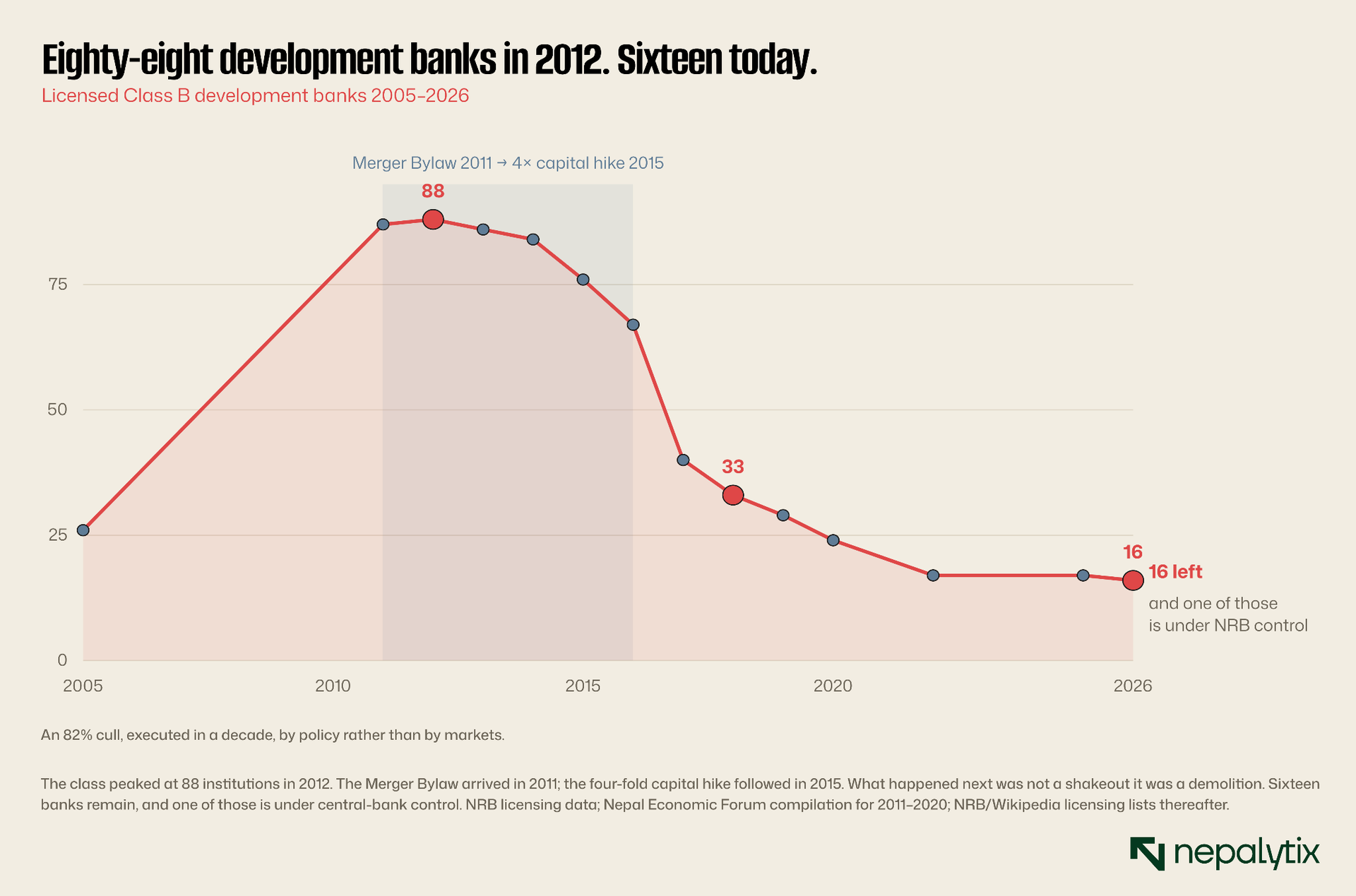

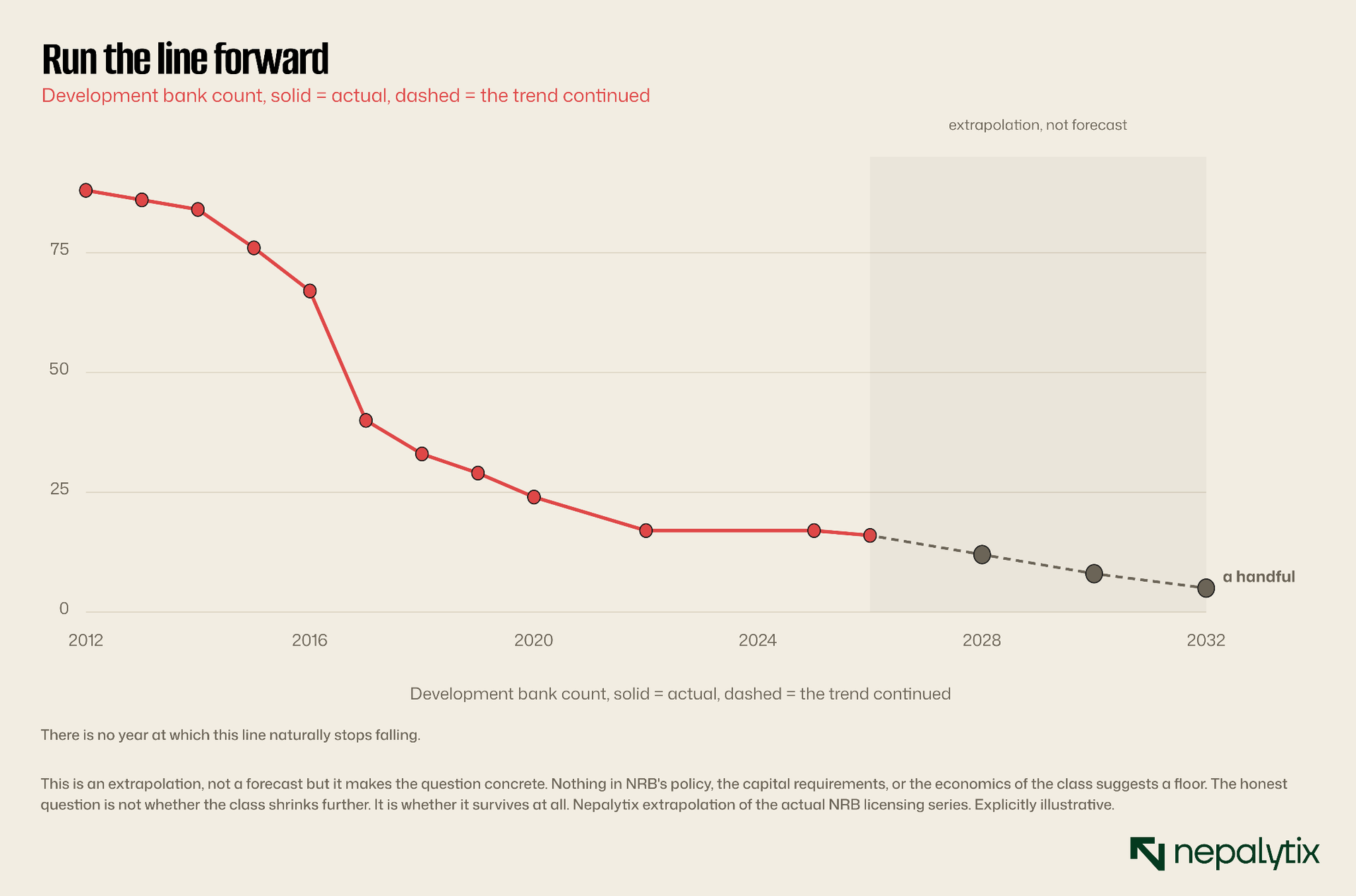

Nepal's development banking sector has shrunk from 88 institutions in 2012 to just 16 today, raising fundamental questions about the future of Class B banks.

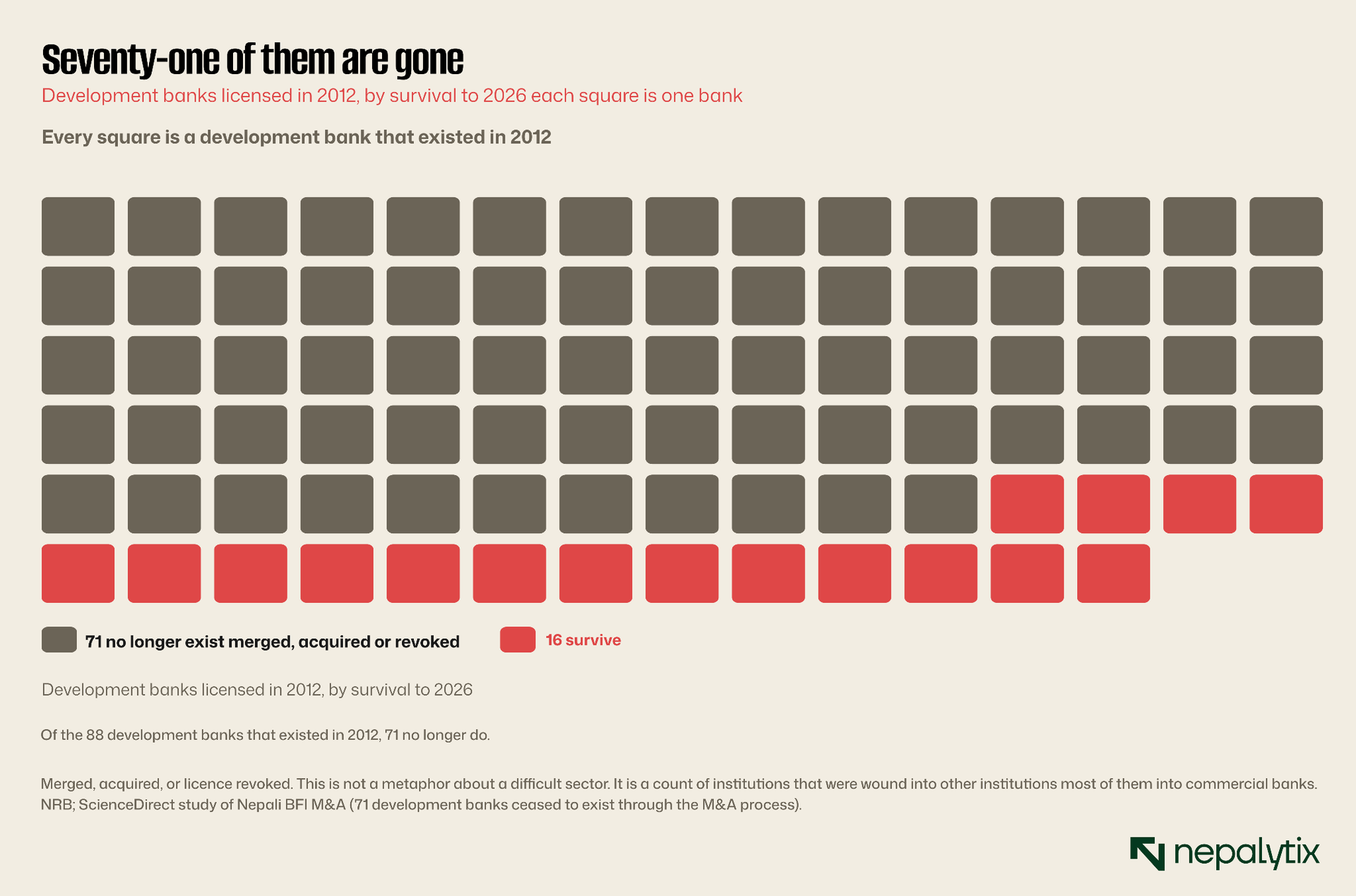

Nepal had 88 development banks in 2012. It has 16 today, and one of those is under central-bank control. This is the story of how a whole class of institutions was dismantled and who actually paid for it.

Ask a banker in Nepal what a development bank is for and you will get a definition rather than an answer. Class B. Licensed under BAFIA. Permitted to take deposits and lend but not to do everything a commercial bank does. Regional or national in scope. It is a description of a legal category and it tells you precisely nothing about why the category should exist.

Push harder and you will get history. Development banks were created to fill a gap to reach the regional borrower, the semi-urban trader, the small manufacturer, the farmer with a hire-purchase agreement, the customer that a Kathmandu commercial bank could not see and did not want. That is a real answer and for a period it was true.

The trouble is that it is an answer about 1996 and this is 2026. The gap has closed. It closed from above as commercial banks grew branch networks into every district in the country and brought cheaper funding with them. It closed from below as microfinance institutions came up-market chasing yield. And what is left in the middle is a class of institution with worse funding than the banks above it, thinner margins than the lenders below it and no obvious reason to exist that anyone can state in a sentence.

This is not rhetorical framing. It is a measurable fact, and the measurement is brutal.

In 2012 there were 88 development banks in Nepal. Today there are 16 and one of those has had its management taken over by the central bank and its shares suspended from trading. Seventy-one institutions that existed inside living memory have been merged, acquired or wound up.

That is not a difficult decade. That is a category being dismantled.

This piece is an attempt to answer the question honestly: what were development banks for what happened to them, who is left and the question that matters if you own one of these stocks does the Class B licence survive the next ten years at all?

How Nepal ended up with eighty-eight of them

To understand the demolition you have to understand the construction because the collapse of the development banks is the direct consequence of how carelessly they were created.

In 1985, Nepal's entire financial system consisted of two commercial banks and two development banks. Financial liberalisation, beginning in the mid-1980s under an IMF-sponsored structural adjustment programme and accelerating sharply after the restoration of democracy in 1990 changed that comprehensively. The state's grip on credit allocation loosened. Private capital was invited in. Joint ventures arrived. And the central bank began handing out licences.

The Development Bank Act of 1996 was the specific instrument. It made it comparatively easy to establish a Class B institution, the capital requirements were low, the geographic remit could be narrow and the regulatory burden was lighter than for a commercial bank. The intention was inclusion: if a commercial bank would not open a branch in Dang or Ilam perhaps a locally-promoted development bank would.

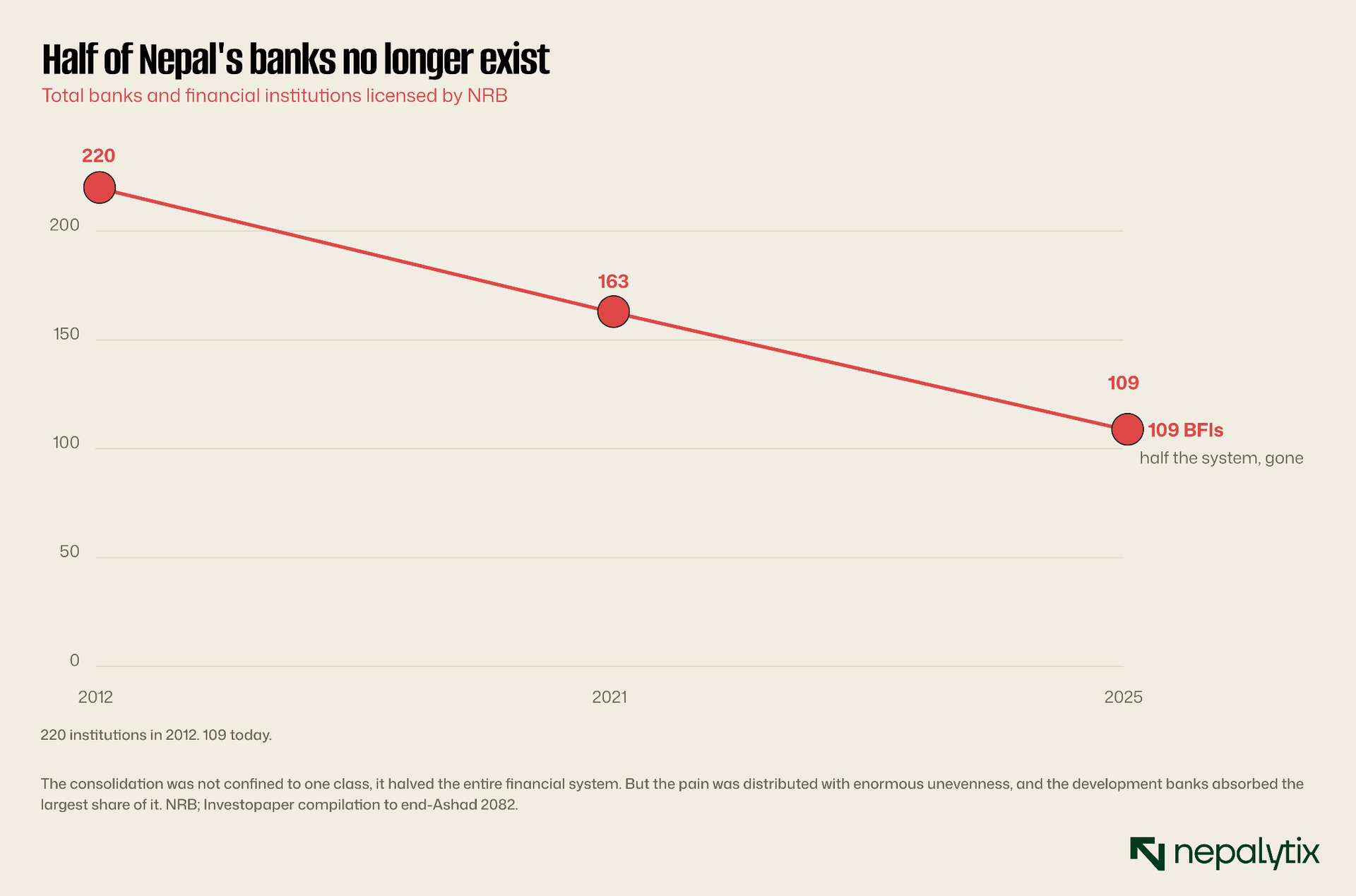

What followed was a licensing boom. From 26 development banks in 2005, the number climbed relentlessly for seven years, reaching 88 by 2012. The wider system swelled with it at its peak, Nepal had 220 licensed banks and financial institutions in a country whose entire economy was smaller than a mid-sized Indian city's. Between 2008 and 2012 alone, 67 new BFI licences were issued.

The results were predictable and NRB's own supervision reports say so with unusual candour. The new institutions did not, in the main, go where they were supposed to go. They clustered in urban areas where the business was easier, and competed ferociously for the same small pool of customers. Capital bases were thin. Governance was frequently poor, insider lending by promoters was endemic enough that a bank run at Nepal Bangladesh Bank in 2006 forced the central bank to take over its management. The regulator by its own account had licensed a system it could not supervise.

Nepal did not build eighty-eight development banks because it needed eighty-eight development banks. It built them because the licence was cheap and the rules were loose.

NRB stopped issuing new A, B and C class licences in 2009. But by then the damage was structural: too many institutions, too little capital, chasing too few good borrowers. The question was no longer whether there would be a consolidation. It was who would pay for it.

Two instruments, one demolition

The clean-up came in two pieces and it is worth being precise about them because together they explain almost the entire shape of Nepali banking today.

The first was the Merger Bylaw of 2011. It created for the first time, a legal pathway for banks to combine and the very first merger under it between Himchuli Development Bank and Birgunj Finance, set the template. The bylaw was permissive rather than coercive: it opened a door and a handful of institutions walked through. The count of development banks drifted from 88 down to the low 80s. It was a nudge.

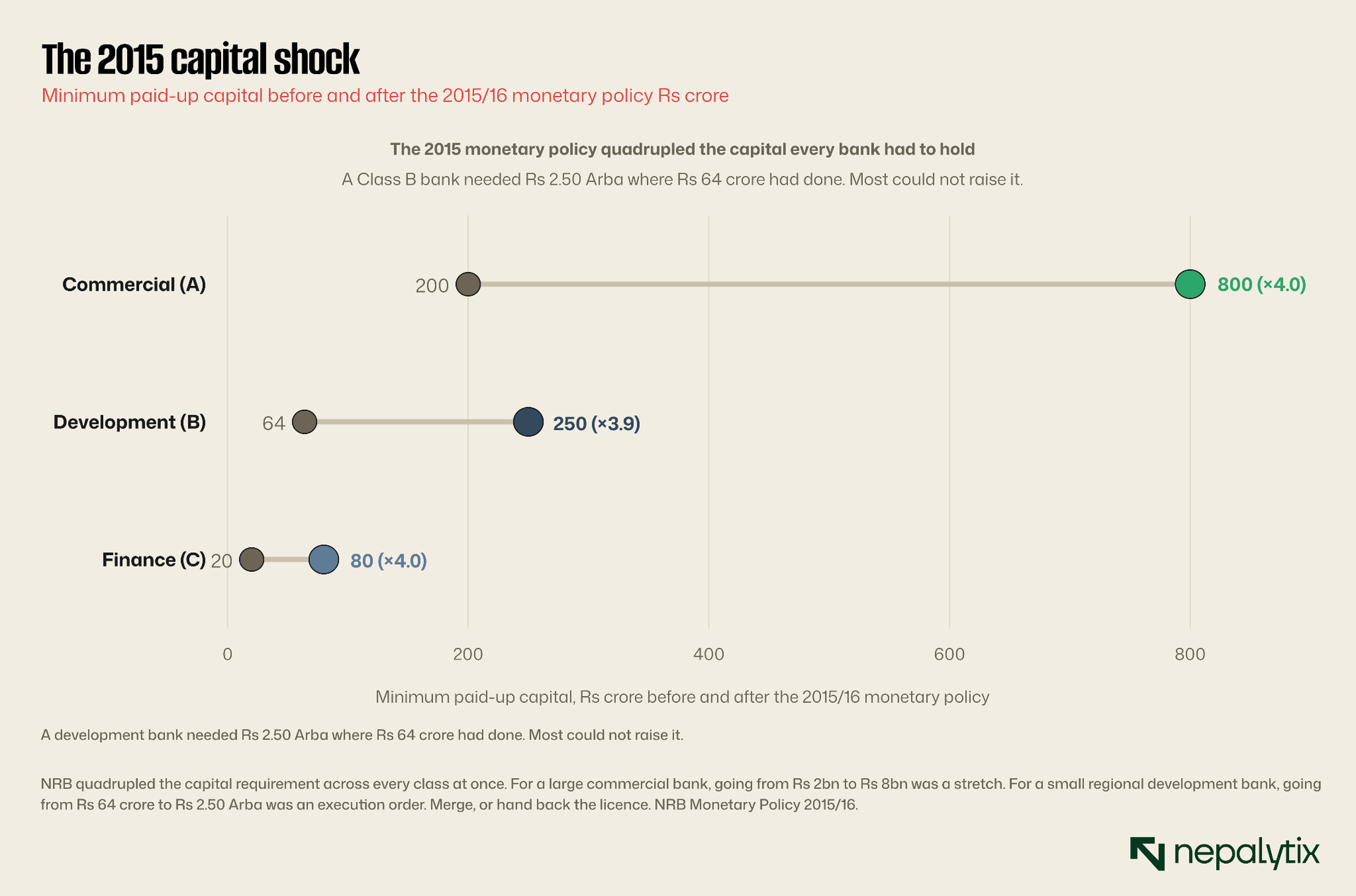

The second was not a nudge. The Monetary Policy of 2015/16 quadrupled the minimum paid-up capital requirement across every class of institution at once.

Look at what that did to a small development bank. Its capital requirement went from Rs 64 crore to Rs 2.50 Arba, nearly a four-fold increase to be met within two years. A regional bank in a provincial town with a modest deposit base and a promoter group of local businessmen had three options. Raise the capital which for most was impossible. Merge with someone who could. Or hand back the licence.

Almost all of them merged. And this is where the story turns, because who they merged with determined everything that followed.

The capital rule was applied to every class. It was survivable for one of them.

Who actually paid for consolidation

The official story of Nepali bank consolidation is a story about systemic stability: too many weak institutions so the regulator forced them into fewer, stronger ones. It is a reasonable story. It is also an incomplete one and the incompleteness is where the argument of this piece lives.

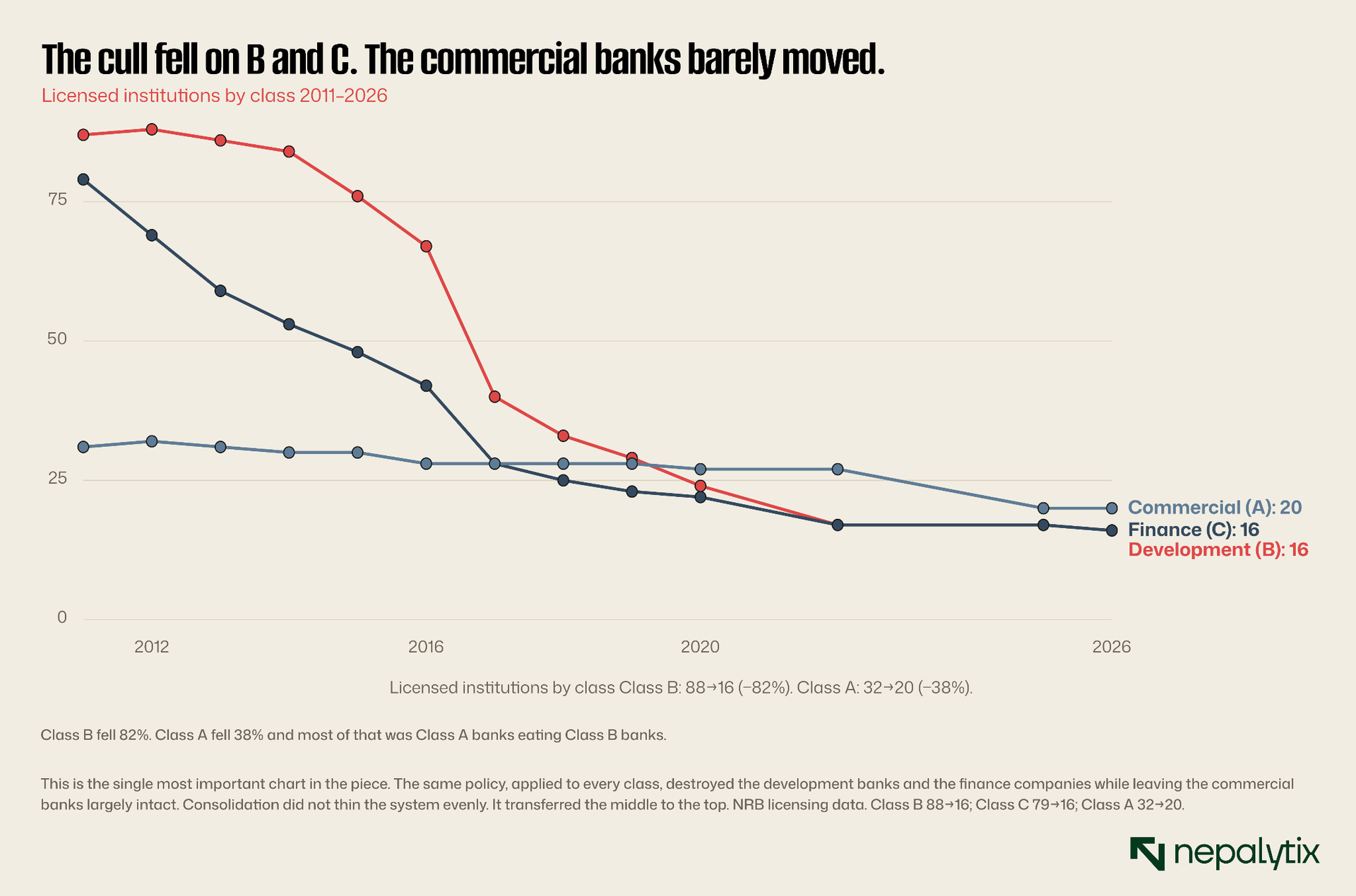

Between 2011 and today, the number of development banks fell from 88 to 16 a cull of 82%. The number of finance companies fell from 79 to 16 a cull of 80%. The number of commercial banks fell from 32 to 20 a decline of 38%, and a substantial part of that came from commercial banks merging with one another, not from being absorbed by anyone.

The same policy. Wildly different outcomes. And when a development bank merged, it usually did not merge with another development bank. It was acquired by a commercial bank Global IME took Reliable Development Bank; Nepal Investment took Ace Development Bank; NMB took Om Development Bank; Kumari took Deva Development Bank; Prime took Kailash Bikas Bank. The list runs on. Seventy-one development banks disappeared, and a large proportion of them disappeared into Class A.

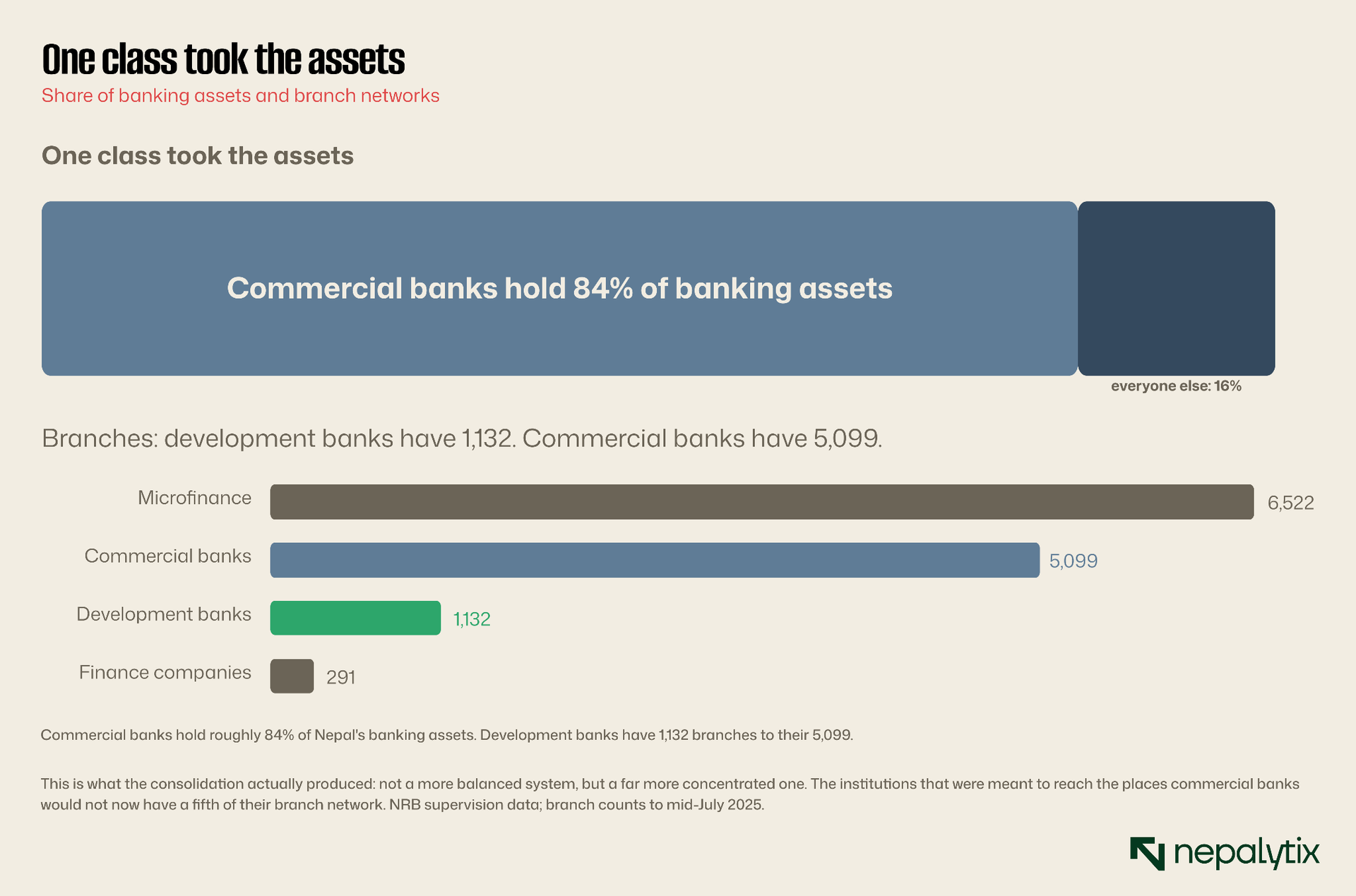

So consolidation did not simply thin the herd. It transferred the middle of the banking system to the top of it. The capital requirement was the mechanism; the acquisition was the transaction; and the outcome was a banking system in which commercial banks now hold roughly 84% of all banking assets.

Read that against the original purpose of the Class B licence and the irony is difficult to miss. Development banks existed to serve customers commercial banks would not serve. The policy designed to strengthen the financial system handed those customers, those deposits and those branch networks to the commercial banks and left the remaining development banks with a fifth of Class A's branch network and a sliver of its assets.

The institutions built to fill the gap were used to fill the balance sheets of the institutions that created it.

What a development bank was actually for

Set the politics aside and ask the economic question honestly, because the answer is not obvious and it matters for what comes next.

There is a genuine, textbook role for a mid-tier bank in a developing economy, and it rests on information. A commercial bank in Kathmandu underwrites on documents, audited accounts, collateral valuations, credit bureau records, formal cash flows. That works beautifully for a garment exporter with proper books. It works badly for a hardware merchant in Butwal whose real creditworthiness lives in his reputation, his family, his twenty years of trading in a town where everyone knows him, and nowhere in any document.

A locally-rooted bank can lend to that man. Its branch manager knows him. It can price the risk on relationship knowledge that no credit model can capture and it can do so profitably because that knowledge is genuinely proprietary nobody else has it. That is the classic case for the community bank, and it is why systems all over the world have historically supported a tier of institutions between the money-centre banks and the micro-lenders.

That case is real. Nepal's development banks, at their best, actually did this. Muktinath's franchise in the western hills, Garima's in the Pokhara belt, Shine Resunga's in the west these were built on exactly this kind of granular, relationship underwriting and their asset quality is the proof that it works.

The case for a development bank was always informational: it knew things about its borrower that a Kathmandu bank could not. Then everyone else learned how to find out.

But the informational advantage was never permanent. It was a temporary rent, earned from the commercial banks absence and the moment the commercial banks turned up, it began to erode.

The gap closed from above

Commercial banks did not stay in Kathmandu. Driven by their own competitive pressures, by NRB's branch expansion requirements and by the simple fact that deposit growth had to come from somewhere, they built out into every district in the country. Today they run 5,099 branches. All but one of Nepal's 753 local levels has a commercial bank branch.

When a commercial bank opens in Butwal, it brings something a development bank cannot match: a structurally lower cost of funds. Bigger, more diversified, better-branded, and able to raise institutional deposits and wholesale funding at rates a Class B institution simply cannot access.

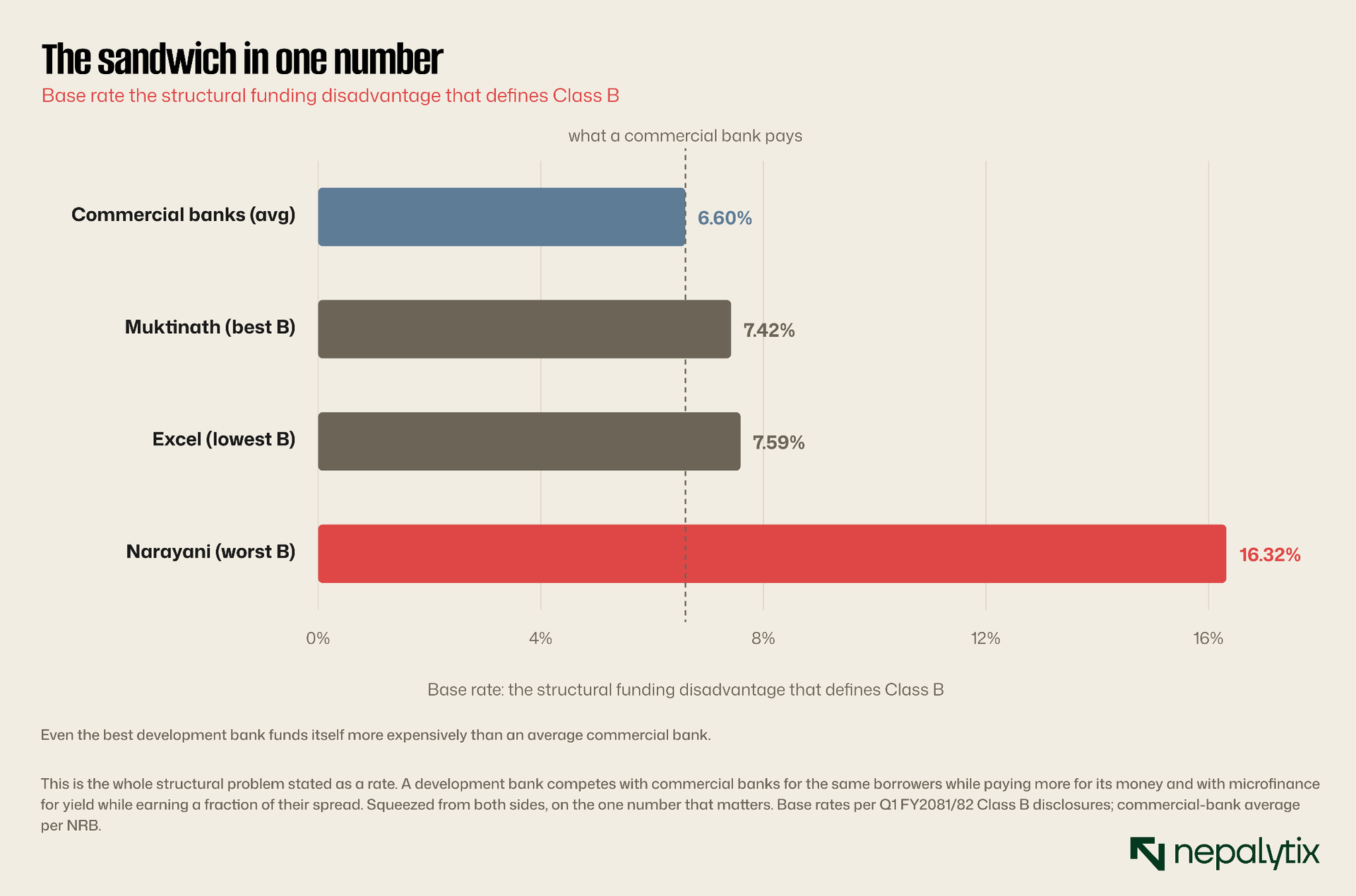

This is the crux and it deserves to be stated plainly. Muktinath, the largest, best-run, most prudently-managed development bank in the country funds itself at a base rate of 7.42%. That is the second-best in its entire class, and it is still worse than what an average commercial bank pays. At the other end of the class, a bank funds itself at 16.32%, which is not a business so much as a slow liquidation.

Now put the two lenders side by side, competing for the same hardware merchant in Butwal. The commercial bank can quote a lower rate and still earn a better spread. The development bank's only defences are speed, relationship and local knowledge genuine advantages, but ones that erode every year as the commercial bank's local branch manager builds his own relationships and its credit models get better at pricing exactly this kind of borrower.

The informational rent decays. The funding disadvantage does not.

And it closed from below

While the commercial banks came down, the microfinance institutions came up.

Class D was created for an even more specific purpose: tiny, unsecured, group-guaranteed loans to the very poor, at yields high enough to cover the enormous cost of administering them. In pursuit of growth, the sector drifted up-market bigger tickets, less-poor borrowers, more commercial lending dressed in microfinance clothing. Nepal's microfinance sector now runs an average NPL above 11%, a fact we examined at length in a separate Signal and it is being consolidated by NRB in exactly the same way the development banks were.

The relevance here is not microfinance's own crisis. It is that as microfinance moved up-market, it began competing for the small-business and semi-urban borrower the development bank's customer while earning a spread a Class B bank could never justify. The middle got squeezed from underneath as well.

So the development bank now sits in a genuinely miserable position. It cannot out-fund a commercial bank. It cannot out-yield a microfinance institution. Its informational advantage, the one thing that was ever genuinely its own, decays a little more every year that a Class A branch stays open down the road. That is what "the squeezed middle" means. It is not a metaphor about difficult trading conditions. It is a description of a business model with no defensible position on either side of it.

What is actually left

Sixteen banks. Eight national, eight regional. One of them, Karnali Development Bank has been declared a problematic institution, its management taken over by the central bank, its shares suspended from trading.

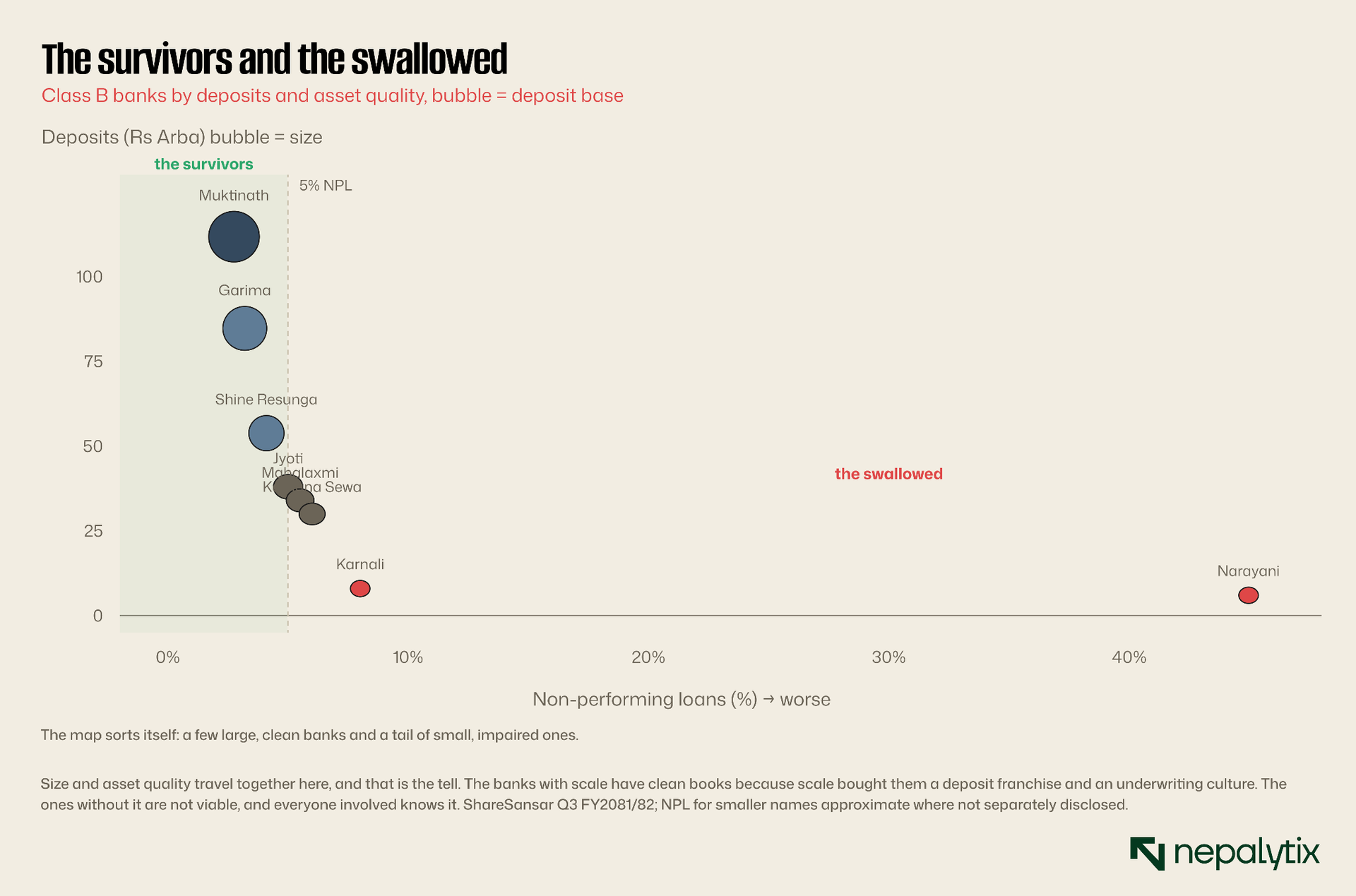

And the sixteen are not sixteen comparable institutions. They are a hierarchy so steep that treating them as a single category is actively misleading.

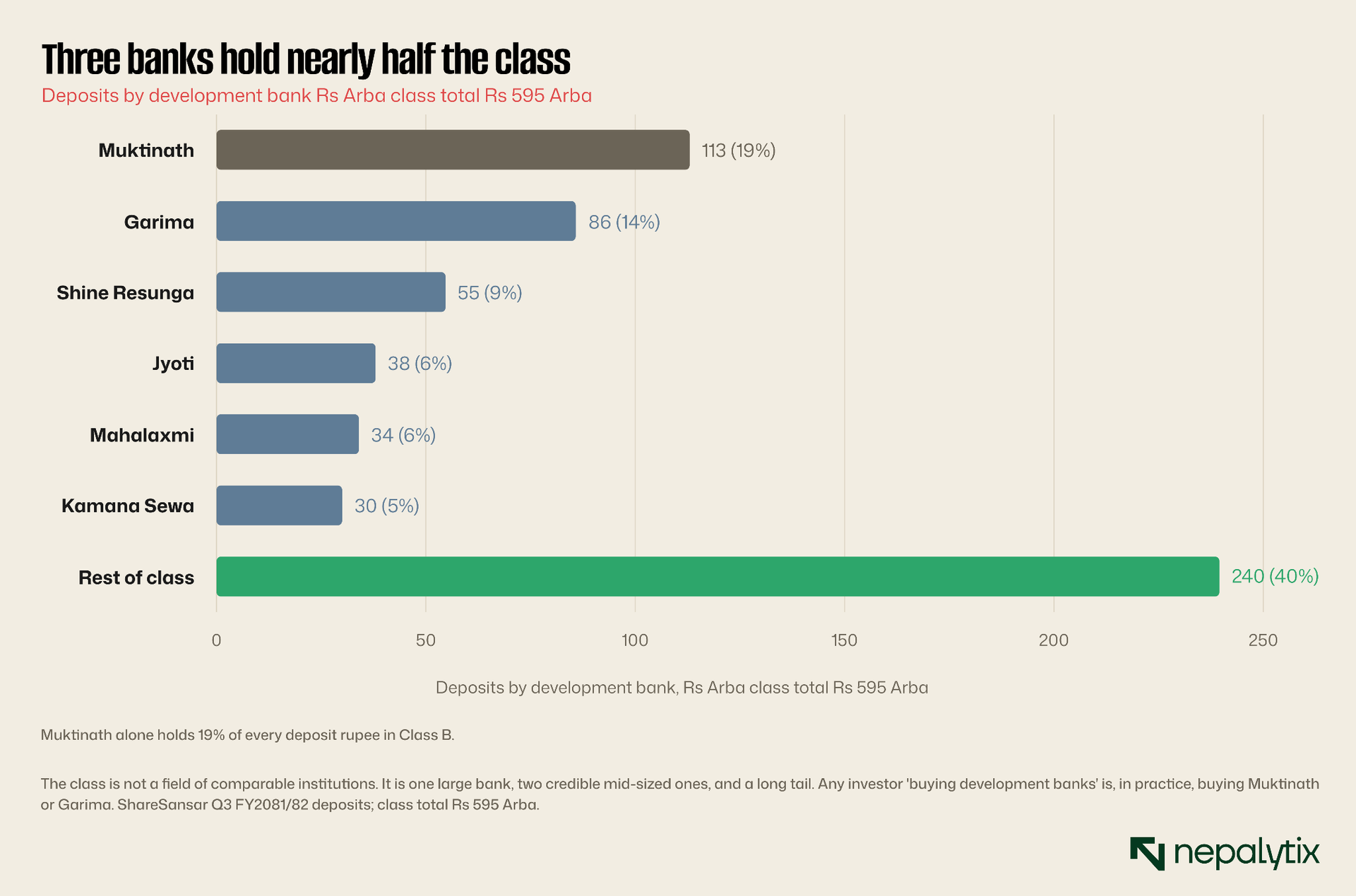

Muktinath holds Rs 113 Arba of deposits 19% of the class total. Garima holds Rs 85.79 Arba. Shine Resunga holds Rs 54.7 Arba. Those three institutions are, between them, close to half of everything Class B holds. Below them, the numbers fall away sharply into banks that are small, regional and in several cases barely viable.

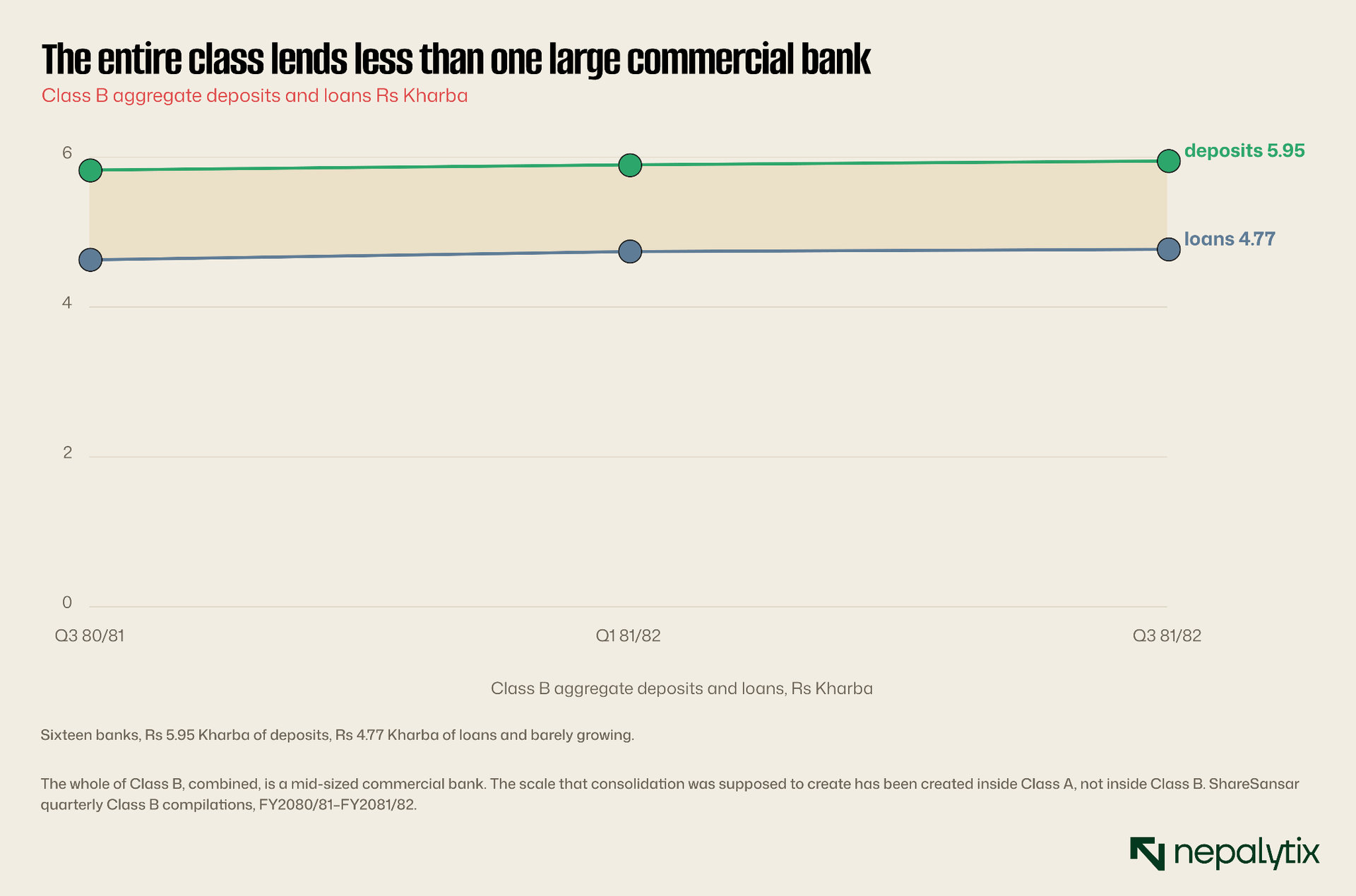

And the entire class, all sixteen banks combined, holds Rs 5.95 Kharba of deposits and lends Rs 4.77 Kharba.

That is the scale of the thing we are debating. The combined lending book of every development bank in Nepal is comparable to that of a single large commercial bank. The scale that consolidation was supposed to produce has indeed been produced inside Class A, not inside Class B.

The survivors are not thriving

The defence of the consolidation policy is that whatever the cost, it left behind stronger institutions. That is a testable claim and the test does not go well.

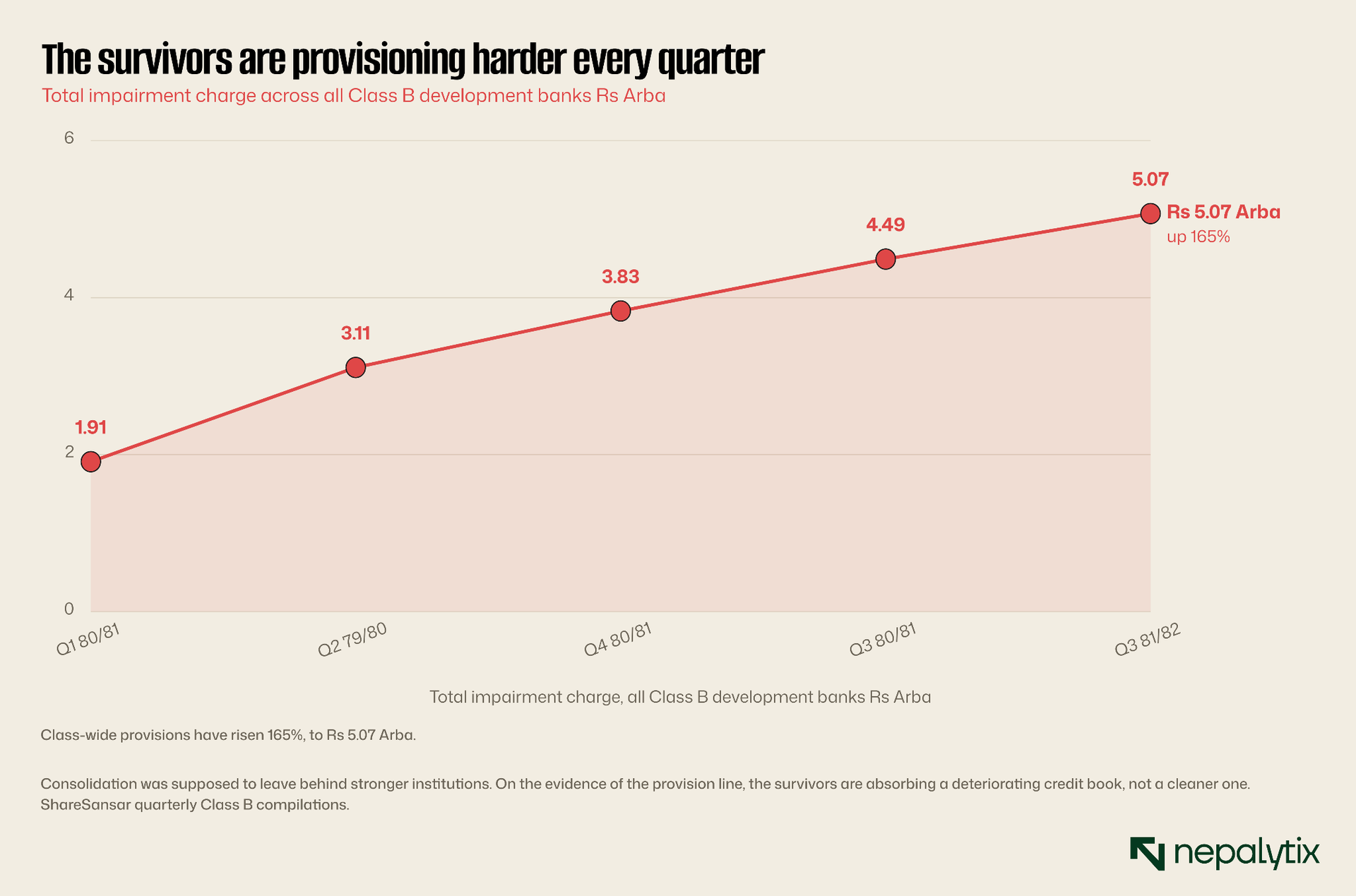

Total impairment across the remaining development banks has risen 165%, to Rs 5.07 Arba. Every quarter, the sixteen survivors are collectively setting aside more against loans going bad. This is not a sector digesting the last of its old problems. It is a sector acquiring new ones.

And the dispersion within it has become extreme to the point of absurdity.

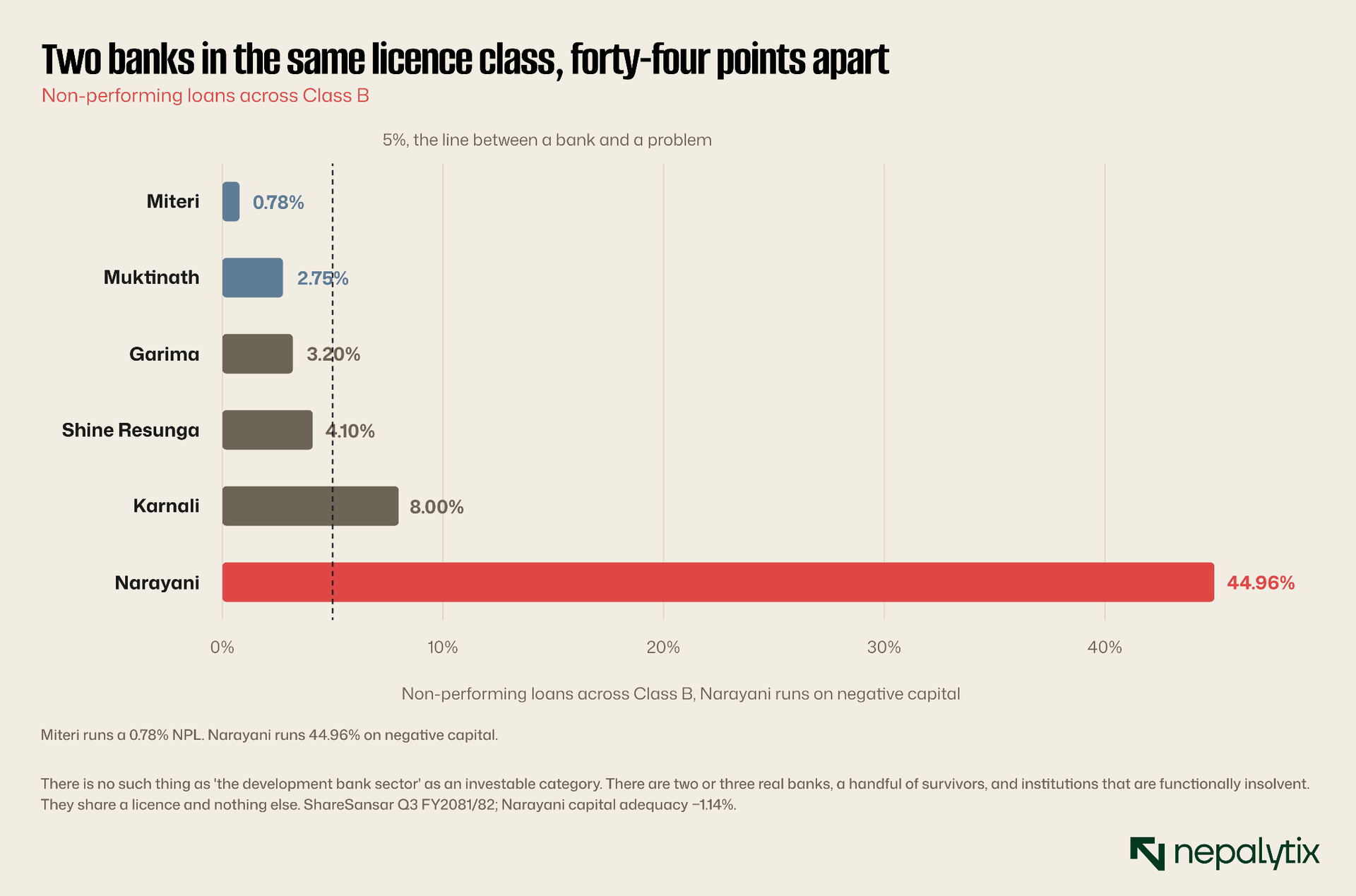

Miteri Development Bank runs a non-performing loan ratio of 0.78% cleaner than most commercial banks in the country. Narayani Development Bank runs 44.96% on capital adequacy of negative 1.14%. That is not a bank with a bad year. That is an institution where nearly half the loan book is not being repaid and the equity has been consumed. It continues to hold a banking licence.

Between those two poles sit Muktinath at 2.75%, Garima, Shine Resunga, and a set of small regional banks of varying quality. Calling this a "sector" and computing a sector average for it is a statistical crime. The average of Miteri and Narayani describes no bank that exists.

Map the class by size and asset quality and it sorts itself into two populations with almost no overlap. The large banks are clean. The small banks are impaired. And that correlation is not a coincidence, it is the mechanism. Scale bought the survivors a cheap deposit base, which bought them the ability to lend selectively which produced the clean book which reinforced the funding advantage. The small banks never got onto that flywheel, and no amount of time will put them there.

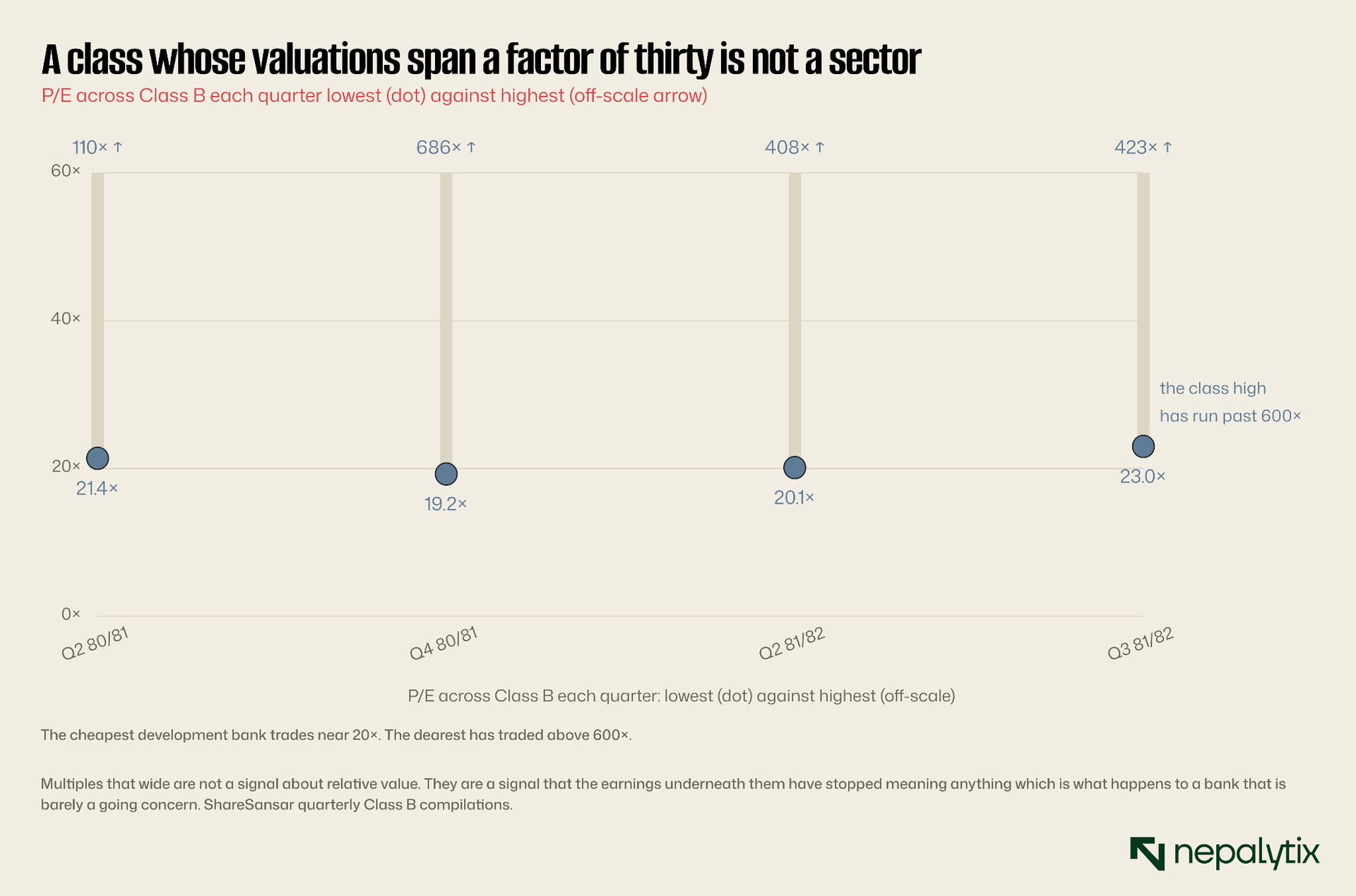

The same logic shows up, savagely, in the market's pricing.

When the cheapest bank in a class trades at 20 times earnings and the dearest at over 600, the market is not making fine distinctions about relative value. It is telling you that some of these institutions have earnings so small, so erratic or so close to zero that the multiple is arithmetically meaningless. You cannot value a bank on a P/E when the E is an accident.

The case for the demolition

Before going further it is worth putting the strongest possible case for what NRB did because this piece has so far been prosecuting and the defence is genuinely serious.

Start with what Nepal actually had in 2012. Two hundred and twenty licensed financial institutions in an economy of roughly twenty million people and a GDP smaller than a mid-sized Indian city's. Eighty-eight development banks, most of them promoted by small groups of local businessmen, most of them thinly-capitalised, many of them lending to companies their own directors controlled. Insider lending was not an occasional scandal; it was a business model. The bank run at Nepal Bangladesh Bank in 2006 caused by exactly this forced the central bank to seize an institution. NRB's own supervision reports from the period describe a system it had licensed and could not supervise.

A regulator looking at that has a real problem. Not an academic one about optimal market structure, a live financial-stability problem in which a dozen small banks could fail in a bad year and the central bank has neither the staff to see it coming nor the resolution machinery to handle it when it arrives. In that situation, forcing consolidation is not an ideological preference. It is risk management.

And it worked, on its own terms. The system is far better capitalised than it was. There are 109 institutions to supervise rather than 220. The kind of promoter-driven insider lending that characterised the 2000s is materially rarer. Nepal has not had a systemic banking crisis, which given what the system looked like in 2012 is not a small achievement and the people who engineered it deserve more credit than this publication's framing has so far given them.

The strongest version of the pro-consolidation case goes further still: that the development banks mostly were not doing the job they existed to do. NRB's own supervision reports note that the new Class B institutions clustered in urban areas rather than the underserved districts they were licensed to reach, and competed for the same customers as the commercial banks rather than finding new ones. If most development banks were simply small, badly-governed commercial banks with a cheaper licence, then consolidating them away costs the country nothing except the illusion of financial inclusion.

The honest counter-argument is not that consolidation was wrong. It is that it was applied without ever asking what was worth keeping.

That case is strong, and any fair reading has to concede most of it. Where it fails is in the indiscriminacy. A capital requirement is a blunt instrument: it does not distinguish between a well-run regional bank with a 1% NPL and a promoter's piggy-bank with a 20% one. It culls by size, not by quality. And so the policy took out both and handed the survivors customers to the institutions that were never willing to serve them in the first place.

A more surgical policy was available and was not attempted: raise governance and supervision standards rather than capital thresholds, resolve the genuinely bad institutions individually and let a smaller number of well-run mid-tier banks continue to exist as mid-tier banks. That is broadly what several other developing systems chose. Nepal chose the blunt instrument, and got a blunt result.

What failure actually looks like

Abstractions about licence classes are easy to argue about. It is worth looking at what the end of a development bank actually looks like on the ground, because two of the sixteen survivors are already there.

Narayani Development Bank reports a non-performing loan ratio of 44.96%. Nearly half its loan book is not being repaid. Its capital adequacy ratio is negative 1.14% meaning that on the regulator's own measure, the equity is gone and the losses have begun eating into the money depositors put in. Its NPL was 35% a year and a half ago and has climbed steadily since. This is an institution that is not recovering, is not being recapitalised and continues to hold a licence to take deposits from the public.

Karnali Development Bank has already crossed the line. NRB has formally declared it a problematic institution, taken over its management, and suspended its shares from trading on NEPSE. Whatever the shares were worth to the people holding them, they are now worth whatever the resolution process eventually says they are worth and those people have no say in it and no exit.

Two of sixteen. Twelve and a half percent of the remaining class is, in practice, already gone.

And it is worth being precise about why they failed, because it was not bad luck. Both are small. Both lacked a deposit franchise, which meant expensive funding which meant they had to lend at rates that only riskier borrowers would accept which produced the bad book, which consumed the capital. It is a doom loop, and it is the same doom loop the funding-cost chart above describes just runs to its conclusion. A bank paying 16.32% for its money cannot lend safely. It can only lend desperately.

That is the mechanism by which a squeezed middle actually dies. Not in a dramatic collapse but in a slow drift up the risk curve forced by a cost of funds it cannot fix until the loan book kills it. And there is nothing in the position of the smaller survivors that makes them structurally different from Narayani. They are simply earlier in the same process.

Which is the sharpest possible argument for why the class does not survive: the ones that are big enough to be safe are big enough to leave, and the ones that are too small to leave are too small to be safe. There is no stable middle position. That is not a prediction. It is the definition of a squeeze.

The three-way endgame

So where does this go? There are exactly three paths, and the class is currently walking all of them at once.

Upgrade. The largest development banks Muktinath and arguably Garima have the scale, the deposit franchise and the profitability of a commercial bank already. Muktinath posted Rs 1.54 Arba of net profit last year, the first development bank in Nepal ever to clear Rs 1.5 Arba and it holds Rs 1.17 Kharba of deposits. The obstacle is capital: Class A paid-up requirements sit far above what these institutions hold so an upgrade means a large equity raise which means dilution before it means a re-rating. But it is the outcome their scale most obviously justifies and it is the only path that preserves the institution intact.

Consolidate. The survivors absorb the tail. Muktinath, in particular has a structural reason to do this: it runs a credit-to-deposit ratio of 87.72% the highest in the class, against a 90% regulatory cap which means it is out of lending headroom and short of deposits. Buying a smaller development bank solves that problem with someone else's deposit base. NRB's merger-first policy actively encourages it. This is the path the economics point at most directly.

Be absorbed. A commercial bank buys the good development banks for exactly what makes them valuable: a deposit franchise in regions Class A is weak in, a clean book, and a relationship underwriting culture that cannot be built from scratch in Kathmandu. This is what happened to seventy-one of their predecessors and it is the path of least resistance for everyone except the shareholders who get paid once and lose the compounding.

Every path out of Class B leads out of Class B. Not one of them ends with a thriving, permanent, mid-tier banking sector.

Notice what all three have in common. Not one of them is "continue as a development bank and prosper." There is no version of the future in which the Class B licence becomes a good place to be. The best outcomes available are exits.

Does the licence survive the decade?

Which brings us to the question in the title and to the only honest way of answering it: look at the line and ask what would stop it.

Eighty-eight to sixteen in fourteen years with no year in which the trend stabilised. Capital requirements that ratchet upward and never down. A regulator whose stated preference, consistently for a decade and reaffirmed in its most recent directives is fewer and larger institutions with merger preferred to incremental capital-raising. Commercial banks that now hold 84% of banking assets and are actively looking for deposit franchises to buy. A remaining class that is provisioning 165% harder than it was that contains an institution on negative capital and another already in central-bank resolution.

What, exactly, is supposed to arrest this?

The honest answer is: nothing currently visible. The likely end state is not sixteen development banks. There are a handful perhaps three or four large ones of which the biggest either become commercial banks or get bought by them and a Class B licence that persists on paper as a legal category with almost nothing inside it.

And it is worth pausing on whether that is actually a good outcome, because the policy debate in Nepal has largely stopped asking. Consolidation delivered real benefits: fewer institutions to supervise, higher capital less of the insider-lending chaos of the 2000s. Those are not small things and anyone who remembers Nepal Bangladesh Bank should be glad of them.

But the cost is real too and it is a cost the policy discussion consistently understates. The development banks were the part of the system that lent on relationships rather than on documents. When they are absorbed into commercial banks, the branch may survive but the underwriting culture usually does not as the acquiring institution imposes its own credit model and the hardware merchant in Butwal who was bankable on his reputation becomes unbankable on his paperwork. Nepal's banking system is now extremely concentrated, extremely document-driven and as the current liquidity glut demonstrates, with banks sitting at a 74% credit-deposit ratio against a 90% cap because they cannot find borrowers they trust increasingly unable to lend to the actual economy in front of it.

There is a version of this story in which Nepal dismantled the only part of its banking system that knew how to lend to Nepalis, and called it prudence.

What this means if you own the stocks

Strip out the policy argument and what remains is a set of quite specific consequences for anyone holding these shares.

Stop thinking of it as a sector. There is no investable "development bank sector" in Nepal. There is Muktinath, which is 19% of the class. There is Garima. There is Shine Resunga. And there is a tail of institutions that range from marginal to functionally insolvent, one of which has already been suspended. A sector average across those is a meaningless number and any screen that produces one is lying to you.

The licence is the valuation. This is the single most important thing to understand. Muktinath trades at roughly 16.7 times earnings and 2.15 times book despite being the largest, most profitable and cleanest-lending bank in its class and its share price is down 78% from its 2016 peak over a decade in which the bank got steadily better. The market is not mispricing the bank. It is pricing the box the bank sits in. No operational result will fix that because operational results are not the problem.

Which means the only thing that matters is the corporate action. An upgrade, an acquisition, or being acquired. Buy these stocks as a bet on a structural event and the good ones are attractively priced. Buy them as growth compounders and you are buying the last ten years again a decade in which excellent execution produced a 78% drawdown.

And the tail is not a valuable opportunity. A small development bank trading at a low price with a high NPL is not cheap. It is a bank whose equity may be worth nothing, in a class the regulator is actively dismantling, with no buyer for its franchise and no capital to raise. Narayani, at 44.96% NPL on negative capital is not a turnaround. It is a resolution waiting for a date.

The market has been telling you the licence is worthless for a decade. The banks kept getting better and the shares kept not caring. That is not a mispricing. That is the answer.

The answer to the question

So: what are development banks even for?

They were for lending to Nepal that commercial banks could not see. It had a real purpose, they were genuinely good at it, and the best of them Muktinath, Garima, Miteri still are. The relationship underwriting that produces a 0.78% or 2.75% NPL in a country where microfinance is running above 11% is not an accident, and it is not something that can be replicated from a credit model in Kathmandu.

But the purpose is not a business model. The economics that once supported that purpose have gone: the funding disadvantage is structural and permanent, the informational advantage decays with every commercial bank branch that opens and the regulator has spent a decade making the licence more expensive to hold and easier to leave. Eighty-eight became sixteen. Seventy-one institutions were absorbed, mostly upward. The survivors are provisioning harder every quarter and the best of them cannot get re-rated no matter what it earns.

The answer, then, is uncomfortable but not complicated. Development banks are for being acquired. That is what the last fourteen years have actually been for. It is what the capital rules were designed to produce, whether or not anyone said so out loud. And it is what the remaining sixteen the good ones by choice and on decent terms, the bad ones by resolution and on none are overwhelmingly likely to do next.

Nepal will end this decade with a banking system of twenty-odd large commercial banks, a shrunken microfinance sector, and a Class B licence that means very little. Whether that system can actually lend to a hardware merchant in Butwal is a question nobody in Kathmandu is currently asking. They should. Because the institutions that used to know how are almost all gone and the ones that took their place are, right now, sitting on sixteen percentage points of lending capacity they cannot find a borrower for.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.