Why Nepal Shouldn't Rush Into Intraday Trading and Derivatives

Nepal should strengthen NEPSE's settlement, surveillance, and investor protection systems before introducing intraday trading, short-selling, and derivatives.

In late May the government promised intraday trading, short-selling and derivatives for NEPSE. The instinct is right this market is primitive and one-directional. But speed and leverage are the top floor of a building and Nepal has not finished the foundation. Monday’s broker collapse was the foundation failing under the simple market we already have.

Modernise, yes, but in order. Settlement, client-fund protection and surveillance come before intraday, short-selling and derivatives. Build the top floor first and the first squeeze or leveraged blow-up sets reform back a decade.

The Take

On 29 May, presenting the budget for 2083/84, the finance minister told parliament that NEPSE would be restructured and that intraday trading, short-selling and derivatives would arrive in phases, alongside depository receipts to list Nepali firms abroad. Retail traders cheered, and you can see why. The market they trade is slow and one-directional: you settle before you can sell, you cannot bet against a stock you think is absurd, and the trading system has barely changed since 2018. Wanting more is entirely reasonable.

The frustration behind the applause is real and old. The same budget paired the new tools with welcome plumbing promises, a stronger regulator, better investor protection, a zero-tolerance line on cornering and insider trading. The direction of travel is not in doubt. The question this piece asks is narrower and more awkward: in what order should the pieces arrive?

The case for saying yes

Give the reform its due first because the case is genuinely strong. A market where you can only ever bet on prices rising carries a permanent upward bias; bubbles inflate unchecked because no one can lean against them. Short-selling, done properly, is not vandalism. It lets a sceptic put money behind the view that a stock is overpriced and in doing so it punctures manias earlier and makes prices mean something.

The rest of the list has the same logic. Intraday trading adds turnover and lets prices find their level within a day. Derivatives give institutions a way to hedge, the precondition for serious money treating NEPSE as investable rather than as a lottery. Depository receipts open a window to foreign capital. There is even a fair argument for urgency: foundations-first can curdle into foundations-forever, the standing excuse of a regulator that never finishes the groundwork. The argument here is not that Nepal should wait. It is that it should build in the right order, and build fast.

Done well, the package could also change who plays. Derivatives and a borrow market are the instruments institutions use to manage risk; without them, mutual funds, insurers and foreign investors stay marginal and the market remains a retail crowd trading against itself. Part of the case is about growing up the investor base not just lengthening the instrument list.

But you build the bottom rungs first

Every mature market assembled its speed and leverage on top of a foundation it laid first: settlement you can rely on, client money kept legally separate and insured, a fund that makes wronged investors whole, surveillance that catches manipulation before it spreads. Only then did it add margin, intraday, shorting and derivatives. Each upper feature depends on the lower ones, a short-seller needs shares to borrow, a day-trader needs settlement to be fast, a derivatives market needs a clearing house that cannot fail. Nepal is proposing to climb while the bottom rungs are cracked or missing.

India is the obvious template, because it modernised quickly and still respected the order. It built a real regulator in 1992, dematerialised shares in 1996 drove its settlement cycle down through the 2000s and launched equity derivatives only in 2000, once clearing and margin could carry them. The lesson is not that reform must be slow. India moved fast. It moved in dependency order, foundations and features advancing together but never features alone.

The cautionary cases run the other way. Frontier markets that bolted derivatives or margin onto weak clearing and thin surveillance have tended to produce one outcome: an early, confidence-shattering blow-up, a freeze and years of retrenchment. Speed on a soft foundation does not make a fast market. It makes a brief one.

The basic rail is still slow

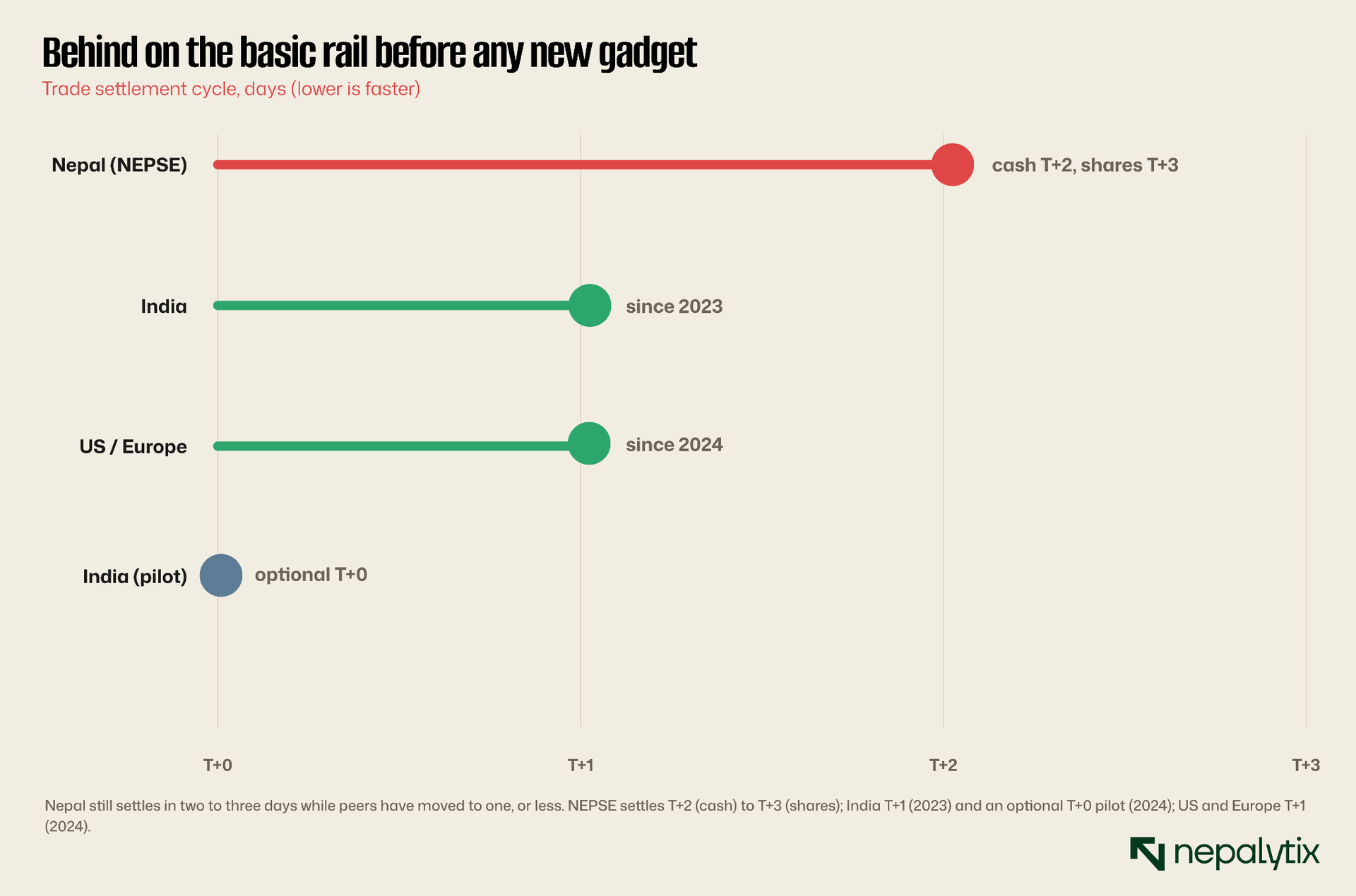

Start with the most basic rail of all, settlement. NEPSE still takes two to three days from trade to the final transfer of cash and shares. That sounds minor until you notice India moved to T+1 in 2023 and is piloting same-day settlement while the United States and Europe went to T+1 in 2024. Intraday trading in particular assumes a clearing backbone and finality at the close that Nepal has not yet built.

Even the upgrade path is slow: as a state-owned exchange, NEPSE procures its technology through a public process measured in years which is part of why the system has aged in place. The announcement is a sentence. The backbone behind it is a multi-year build that has barely begun.

The market you would be leveraging

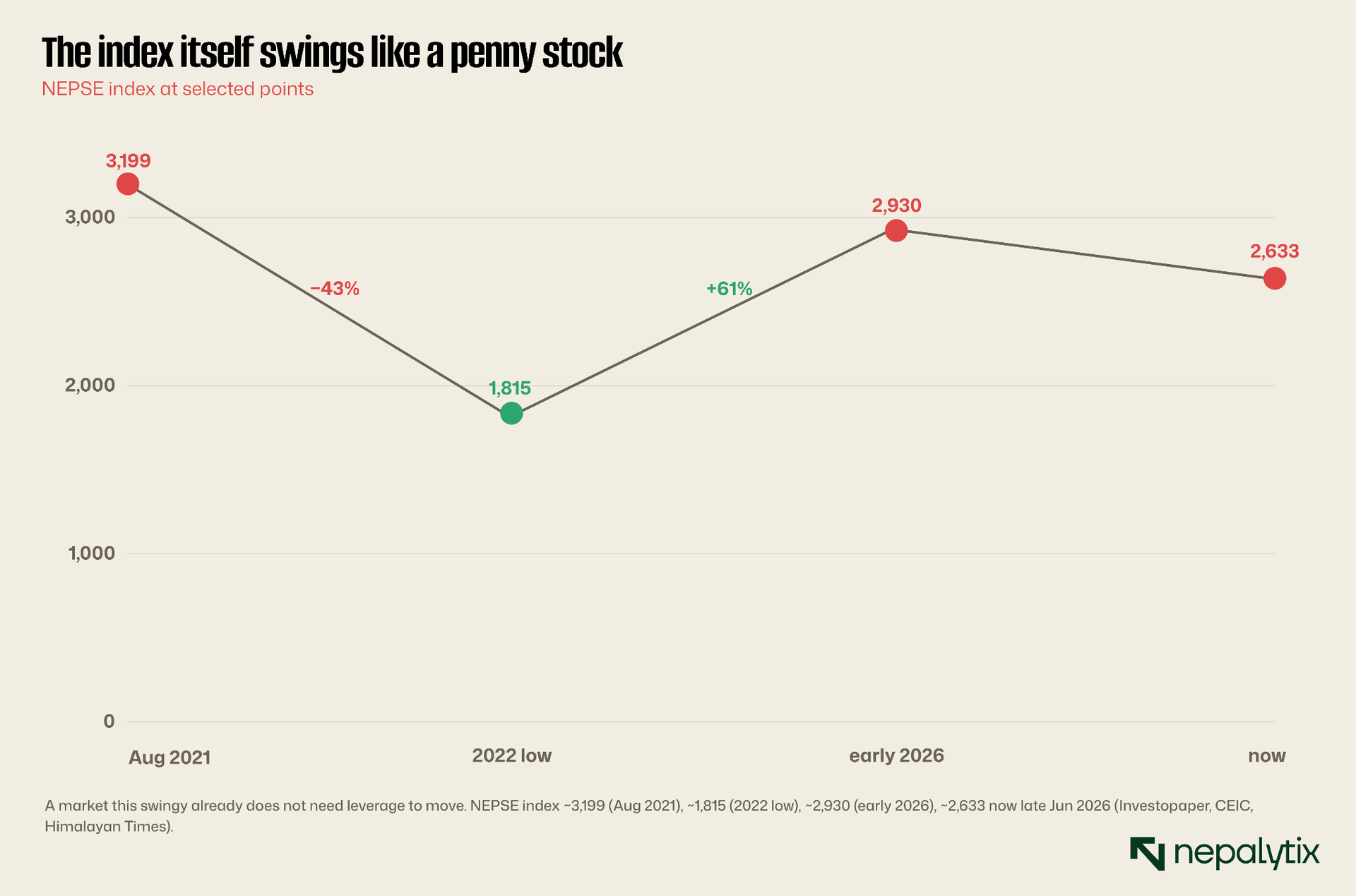

Now consider the raw material these tools would be applied to. NEPSE does not need leverage to move violently; it manages that on its own. The benchmark index touched roughly 3,200 in 2021 fell more than forty percent to around 1,800 by 2022 then climbed back toward 2,900 by early 2026 before slipping again. That is the whole market, not one hot stock, swinging like a speculative bet.

The shape is the point. A market that can halve and then nearly double inside four years is already delivering all the volatility anyone could want, and it is doing it on cash, with no borrowed money amplifying the moves. Leverage does not add opportunity to a market like this. It adds gearing to swings that are already violent.

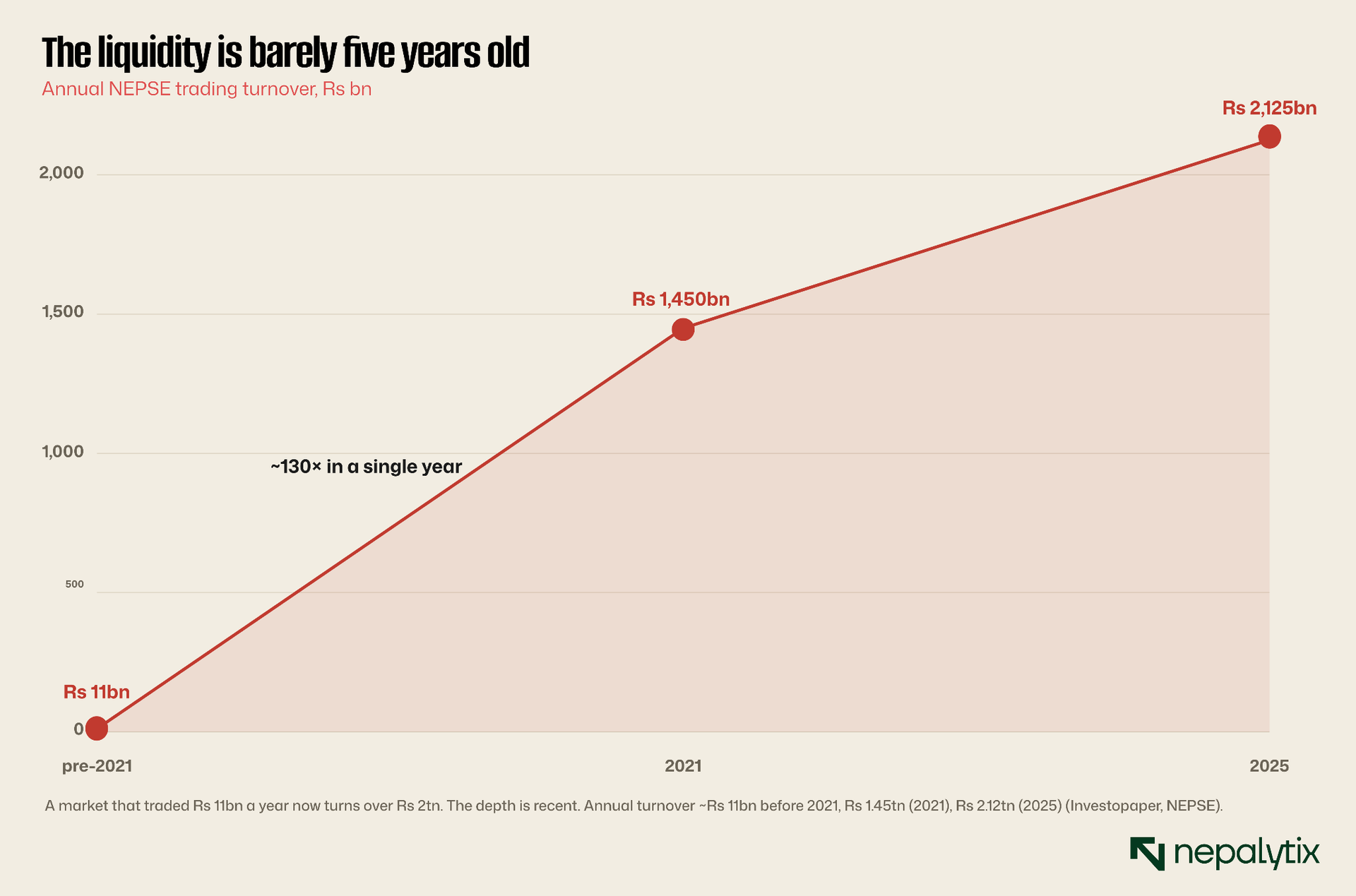

And the depth of that swinging is astonishingly new. For most of NEPSE’s history annual turnover was a rounding error; then it exploded, from roughly Rs 11bn before 2021 to Rs 1.45tn in 2021 and Rs 2.12tn by 2025. A market whose entire liquidity base materialised in the last five years is not a deep, tested pool. It is a young, hot one. Hot money leaves faster than it arrives.

There is no long memory in that line, no decade of steady two-way flow that a derivatives desk or a short book could lean on. The plumbing that intraday and shorting assume, deep, continuous, predictable volume is exactly what a five-year-old liquidity boom has not had time to become.

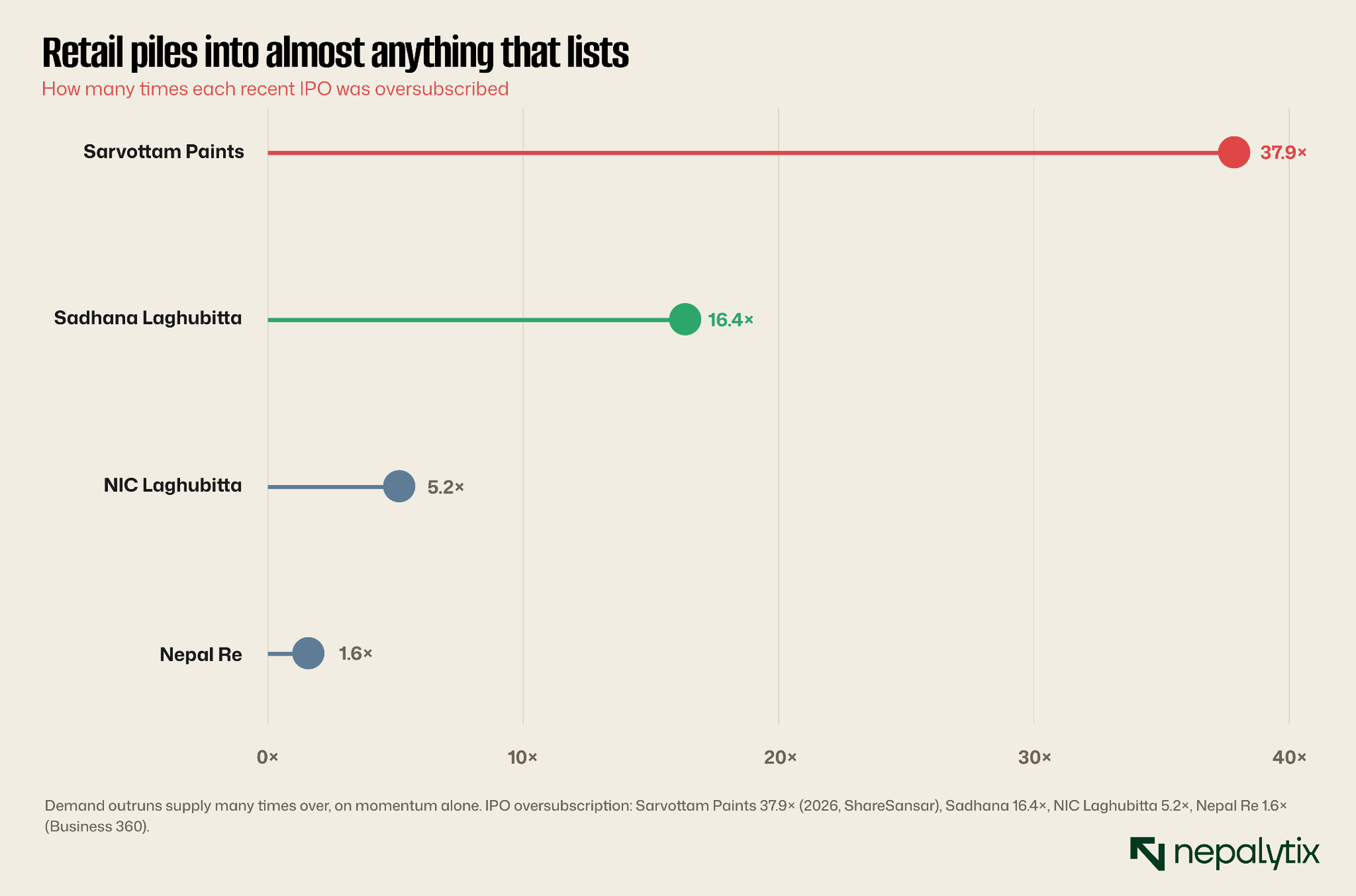

The behaviour on top of that liquidity is feverish. Demand for almost anything that lists runs at multiples of the shares on offer: a recent paints IPO was oversubscribed nearly thirty-eight times, a microfinance issue more than sixteen. This is a market that prices on appetite where new paper is hoovered up almost sight unseen. Layer intraday margin and the right to sell what you do not own onto that temperament and you are not smoothing the market. You are handing it matches.

Oversubscription on that scale is not a sign of depth; it is a sign of a crowd chasing scarcity. The same psychology that bids an IPO thirty-eight times over is the psychology that panics on the way down, and leverage turns that panic into forced selling. You do not want margin calls hitting a market that already moves in herds.

Where the value actually sits

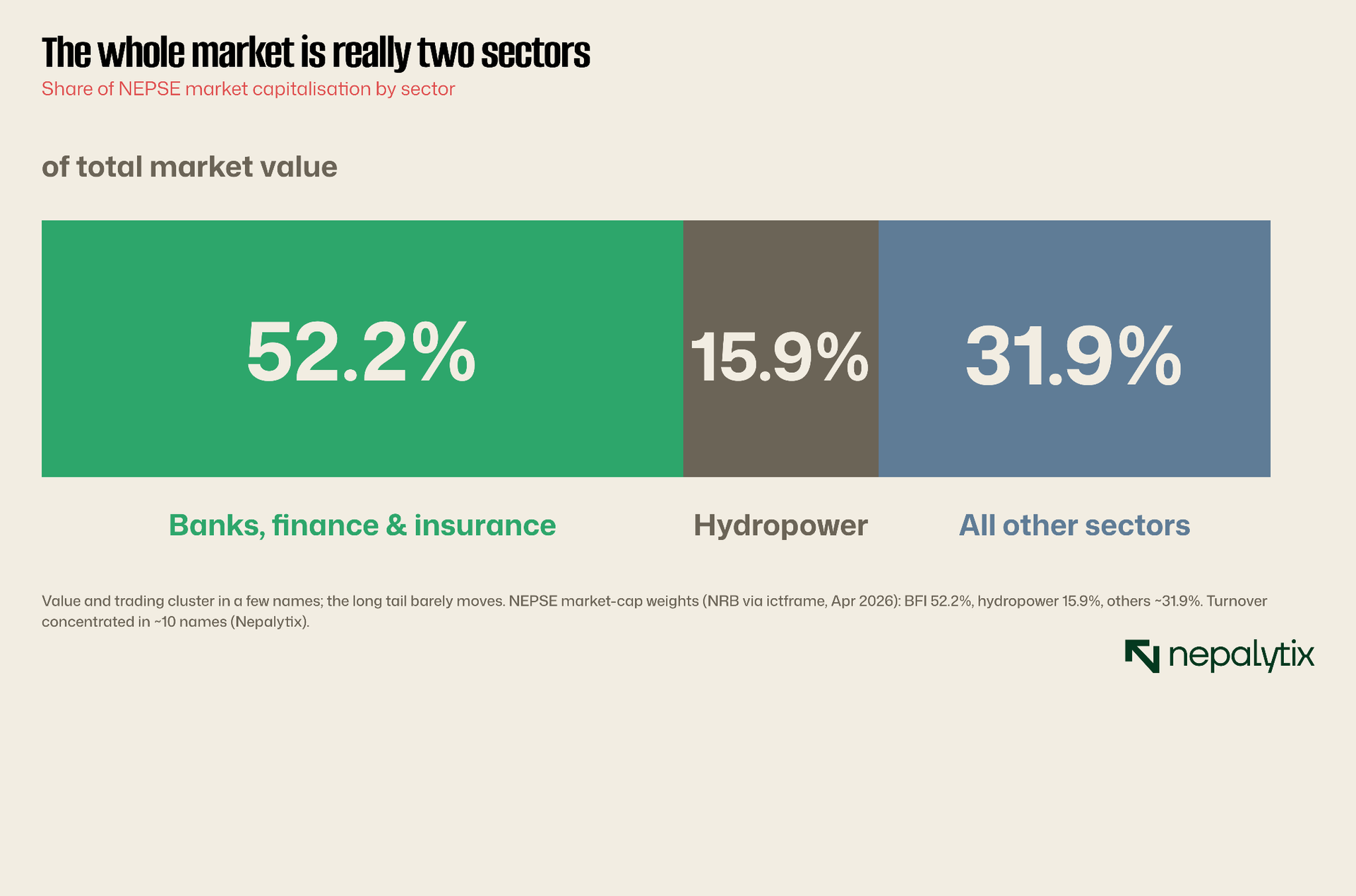

The depth is also narrow. Banks and insurers are more than half the market’s value, hydropower another sixth, and within that core a handful of names carry most of the daily turnover. A thin stock is the easiest thing to squeeze or corner, and short-selling a name that barely trades is an open invitation to the manipulation the budget itself promised zero tolerance for.

So the tradeable market is far smaller than the 286 listings suggest. Most of those names are peripheral, trading rarely and in size that any determined buyer or seller could move. That is the worst possible substrate for short-selling where the danger is precisely that a thinly traded name can be cornered, squeezed or driven by a single large player long before a regulator notices.

This is where the missing prerequisites bite. Short-selling needs a securities-lending market so sellers borrow real shares rather than selling phantom ones; Nepal has none, which is how a short rule becomes naked shorting. Margin trading needs a legal supervised framework with collateral held centrally; Nepal has none, which is why the credit already happens off the books. Derivatives need all of that plus a clearing house with deep capital. And surveillance, the prerequisite behind them all, sits with a regulator that has spent stretches of the past year without a permanent chair.

None of these is exotic. A securities-lending market, central collateral, a clearing house, a funded investor-protection scheme, real-time surveillance, these are the ordinary machinery of any functioning exchange. They are unglamorous, they take years and they do not generate the headlines a short-selling launch does. That is exactly why they get skipped and exactly why skipping them is dangerous.

The collateral that isn’t there

Leverage is supposed to sit on collateral. In a supervised system, margin is posted up front, held centrally, marked to market daily, liquidated automatically on a breach and visible to the regulator throughout. The same credit already exists in Nepal, just informally: nothing posted, held at the broker’s discretion, never marked, rolled over on a handshake, invisible until the day it defaults. The credit is here. Only the safeguards are missing.

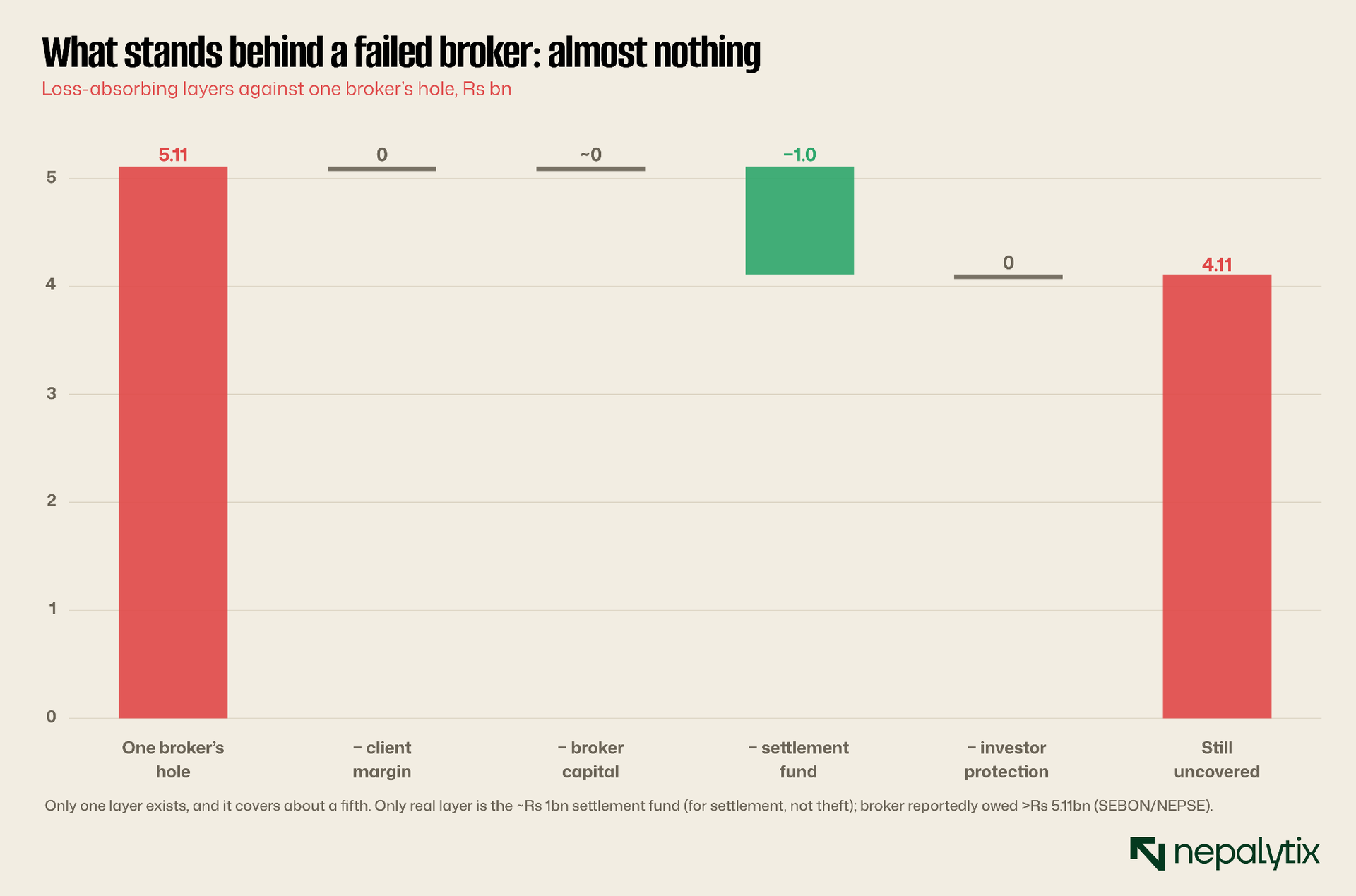

And when that credit detonates, almost nothing stands behind the investor. Walk a failure down through the layers meant to absorb it: client margin, broker capital, a guarantee fund, an investor-protection scheme. Only one of them exists in any real size, a settlement fund of about a billion rupees, and it was built for late settlement not stolen client money. Against one broker’s reported Rs 5bn hole, it covers about a fifth.

Add leverage, two-way bets and derivatives on top of a backstop that is small and that narrowly scopes and the first serious failure is not absorbed. It is socialised or it is simply eaten by the investors unlucky enough to be in the way. Either outcome teaches the public that the market is a trap which is the single most expensive lesson a young exchange can deliver.

Monday’s reminder

None of this is hypothetical because this week supplied the proof. A mid-sized broker was suspended after taking no margin, mixing client money with its own, settling off any clock and running a margin book that is not even legal. That happened under the simple, one-directional market Nepal already has. The reforms propose to add leverage, shorting and derivatives on top of that same plumbing. It is renovating the shopfront while the stockroom stands empty and confidence is the one asset a young market cannot quickly rebuild.

Every blow-up that lands before the safeguards exist does more than cost the traders caught in it. It teaches a generation of savers that the market is rigged, and that lesson is slow and expensive to unlearn.

What ‘foundations first’ is not

This is not a brief delay, and it is worth saying so plainly because gatekeepers have always dressed obstruction up as prudence. Foundations first does not mean features never; it means features in parallel, sequenced by what depends on what. Nepal can be standing up a securities-lending market and a properly funded guarantee scheme in the very year it pilots intraday on its most liquid handful of stocks. What it cannot sensibly do is switch on short-selling before there is anything to borrow or invite leverage onto a broker layer that just proved it cannot hold client cash safely.

Concretely that means a roadmap built on dependencies not a wish list with dates: securities lending and central collateral before short-selling and margin; a funded protection scheme and live surveillance before either; faster settlement before intraday. Publish the order and switch each feature on only once the rung beneath it can bear weight.

The Take

So this is not a vote against modernisation. Nepal should absolutely end the one-way casino, and intraday, short-selling and derivatives all belong in its future. It is a vote for the order of operations. Fix settlement so it is fast and certain. Enforce client-fund segregation and stand up a real investor-protection fund. Build the surveillance to catch manipulation and legalise and supervise margin lending and securities borrowing out in the open. Then and only then phase in the speed and the leverage on a foundation that can bear their weight.

Do it in that order and Nepal gets a genuinely modern market. Do it in reverse, top floor first and the first short squeeze, the first leveraged blow-up, the first clearing failure will not just hurt the traders involved. It will hand every opponent of reform a decade of ammunition. The features the budget named are the right ones. The sequence is the whole game.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.