Why Promoter Shares Trade Below Ordinary Shares in Nepal

The Nepal Stock Exchange has a hidden pricing paradox: identical companies often trade at two very different prices. Promoter shares can sell 10–50% below ordinary shares despite carrying the same dividends, voting rights, and ownership. This article explores how regulation, liquidity restrictions, and market structure create the persistent promoter discount.

On the Nepal Stock Exchange a single firm can wear two prices at once. The gap between them isn't a mistake. It's the price of permission and it quietly inflates the value of the whole market.

On the last trading day of March, a share of Nabil Bank changed hands for about Rs 531. On the same screen, on the same afternoon another share of the same Nabil Bank changed hands for Rs 301. Not a different bank. Not a different class of claim on the bank's profits. The same company priced by the same market on the same day and the second share cost forty-three percent less than the first.

If that sounds like an arbitrage waiting to be closed you are thinking like an economist and not like a regulator. The two Nabils are the ordinary share, ticker NABIL and the promoter share, ticker NABILP. They pay the identical dividend. They carry the identical vote. They have the identical claim on every rupee of Nabil's retained earnings and every rupee it would return in a liquidation. By every measure a company-law textbook recognises, they are the same instrument. And yet one of them is reliably and persistently, a great deal cheaper than the other.

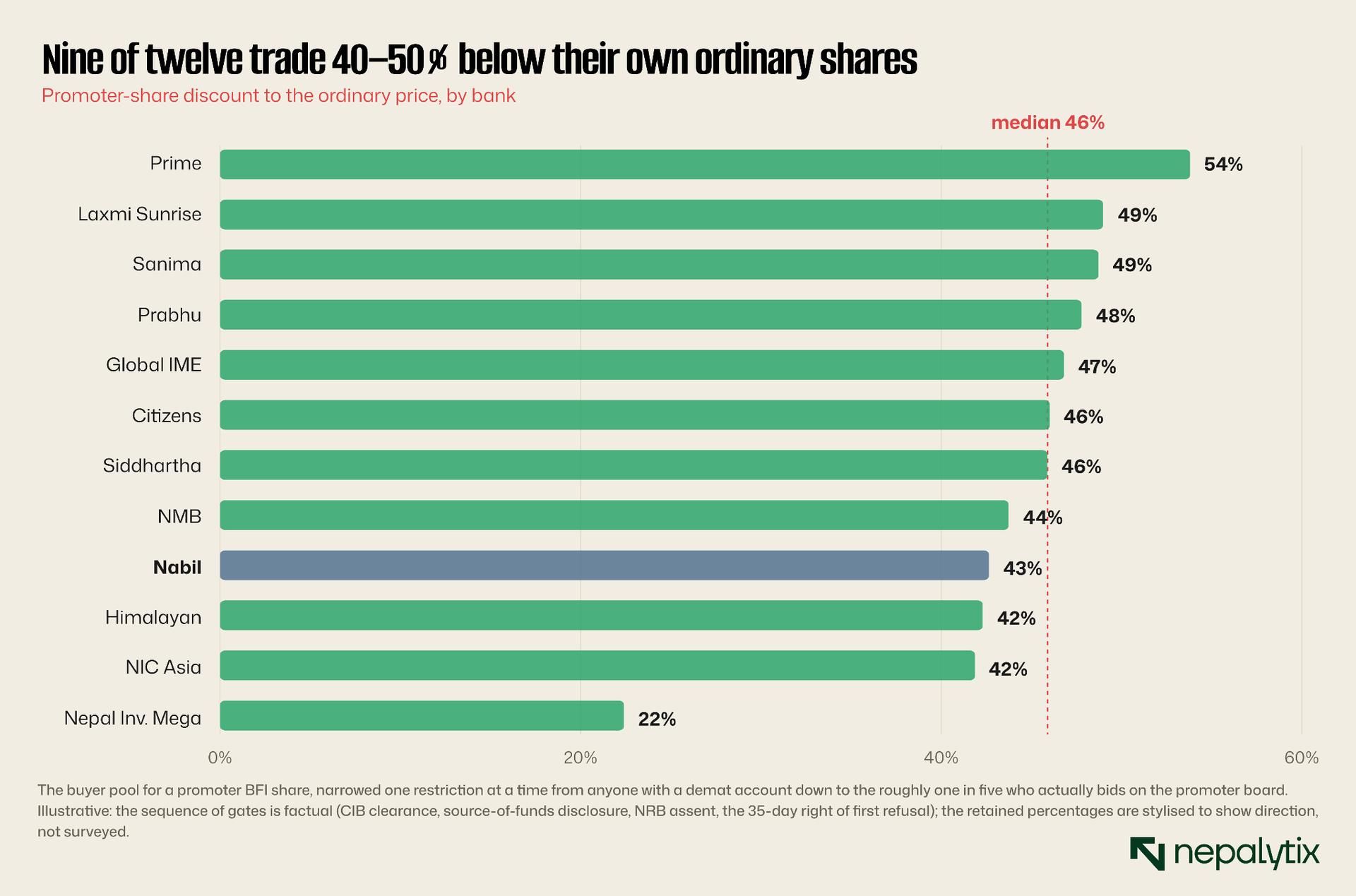

This is not a Nabil quirk. It is the structural signature of the entire Nepali stock market. Scroll the promoter board on the Nepal Stock Exchange and you will find dozens of banks, finance companies and insurers listed twice, once for the public, once for the founders with a wedge of anywhere from ten to fifty percent driven between the two prices. The wedge is so familiar that most investors have stopped asking what it is. This piece asks. The answer turns out to explain not only a curiosity of the order book but a distortion that runs all the way up to the number politicians quote when they want to say the market is too expensive.

The two shares are in every way that pays, the same share

Start with what the promoter shares because the name misleads. A promoter, in Nepali market usage is one of the original investors who put up the capital to found a company and took the founding risk before there was any public market to sell into. When a bank is licensed, its promoters subscribe the bulk of the paid-up capital; later a slice typically thirty percent, sometimes forty is floated to the public through an IPO. The shares the founders keep are promoter shares. The shares the public buys are ordinary shares.

In the developed-market imagination, that founding block ought to be worth more, not less. This is what dual-class structures are for. When Alphabet or Meta or Alibaba carve their equity into two classes, the founders class carries extra votes, and control commands a premium. The insiders shares are the expensive ones precisely because they steer the company. Nepal has built the mirror image of this arrangement, and then inverted its price. Here the two classes vote equally, one share, one vote for promoter and public alike. They earn equally. They rank equally in a wind-up. The promoter share confers no extra control, no preferential dividend, no senior claim. It confers exactly one thing that the ordinary share does not: a set of restrictions on who may own it and how easily it may be sold.

So the Nepali promoter discount is not a control story at all. Strip the word "promoter" of its founder-glamour and what remains is an ordinary economic claim wearing a straitjacket. The market is not paying less for a weaker asset. It is paying less for a less tradeable one. That distinction is the whole of the argument, and almost everyone who complains that the discount is "irrational" has missed it. The discount is not irrational. It is the market doing its job pricing, quite precisely, the cost of the straitjacket.

The discount is the price of permission, not the price of value

What is in the straitjacket? For a bank or financial institution, quite a lot. A promoter share of a Nepali BFI cannot simply be sold to whoever bids highest. The seller must first offer it to the company's existing promoters and wait out a thirty-five-day right of first refusal. The buyer must obtain a clearance letter from the Credit Information Bureau confirming they are not blacklisted. The buyer must be able to disclose the source of the funds. The transaction must pass the scrutiny of Nepal Rastra Bank. And when a block of promoter shares is first listed for trading, the central bank caps the entry price at no more than half the ordinary price, a regulatory haircut applied at birth that the secondary market never fully unwinds.

Each of these is defensible on its own terms and we will come to why the central bank imposes them. But stack them together and you have manufactured an illiquid asset out of a liquid claim. A share you must offer to a closed list of people first that only a pre-cleared buyer may purchase, that a regulator must bless and whose funding you must document is a share that trades rarely, in small size at prices that gap around. And illiquidity has a price. It always has. The academic literature calls it a liquidity discount; the trading desk calls it the cost of not being able to get out. On NEPSE it has a face and a ticker suffix.

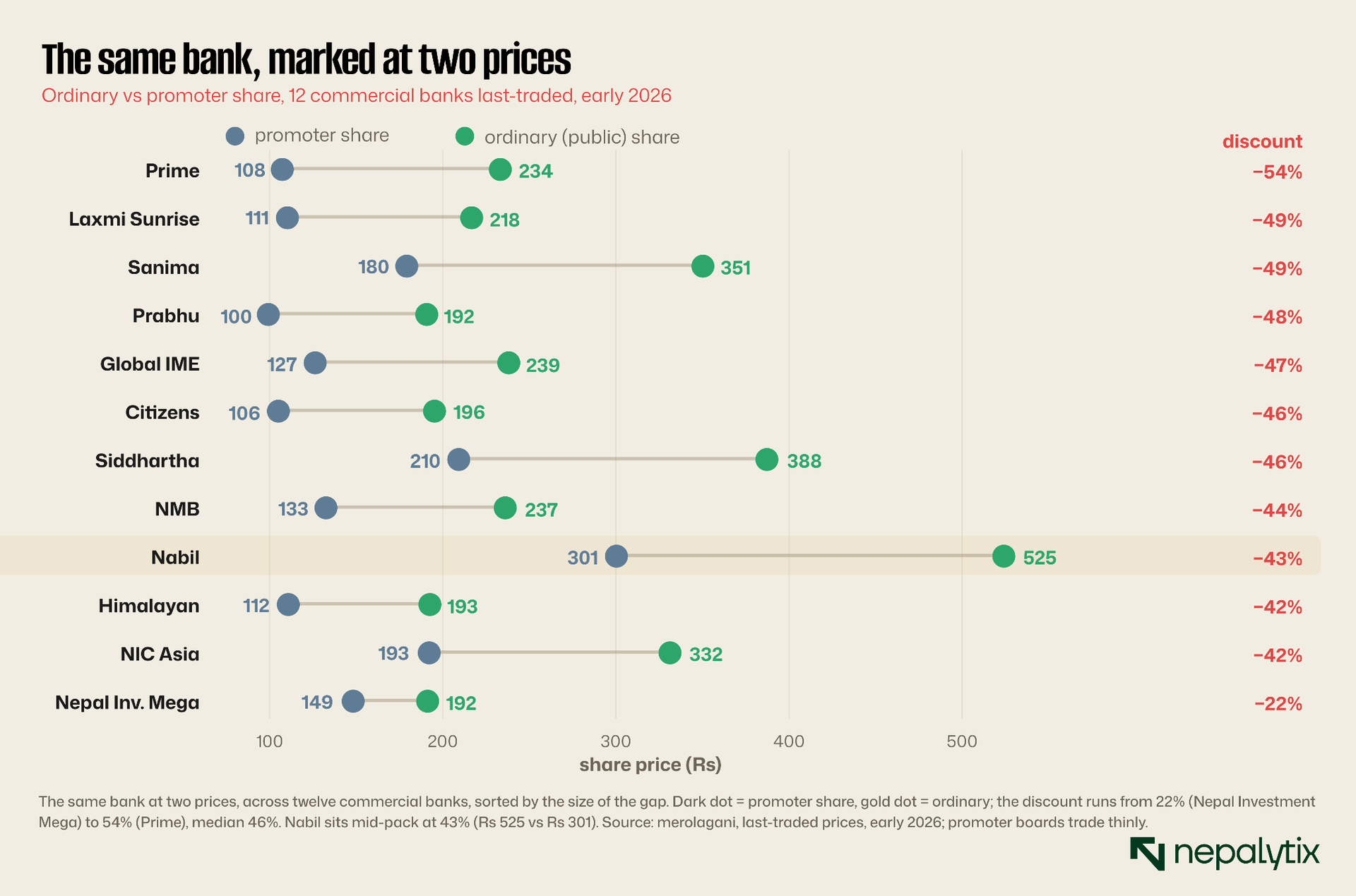

It helps to see the discount not as one number but as a sum of frictions. Take Nabil's current forty-three percent gap and lay it out as a bridge from the ordinary price down to the promoter price.

The decomposition in the middle is illustrative; nobody can hand you an audited breakdown of how many rupees of the gap are "illiquidity" versus "compliance cost." But the endpoints are real, and the shape is the point. Every rupee of the wedge traces back to a restriction on trading the share. Not one rupee of it traces to a weaker claim on Nabil's earnings because there is no weaker claim. The discount is a tax on permission and patience. It is what the market charges you for holding an asset the state has made difficult to move.

This is a liquidity discount and the market has a name for it

Nothing about the promoter discount is exotic. Every market on earth pays less for an asset it cannot easily sell and the professionals have names and formulas for the phenomenon. A block of restricted stock that cannot be sold for a year trades below the freely-marketable shares of the same company; valuation practitioners call the gap a discount for lack of marketability and argue about its size in court. A closed-end fund routinely trades below the net asset value of the very securities it holds, sometimes for years because the wrapper is harder to arbitrage than its contents. Private-company shares change hands below the price a public listing would fetch. In each case the cash flows are not in question; the ease of exit is.

What makes the promoter discount unusual is not that it exists but how large and how durable it is. A marketability discount in a developed market is typically a matter of a lock-up measured in months and a haircut measured in low double digits. Nepal has built a marketability discount with no expiry date and a magnitude that reaches forty and fifty percent. The reason it does not get arbitraged away is instructive. In a normal liquidity discount, an arbitrageur can buy the cheap, illiquid line and wait for it to become liquid. The lock-up ends, the fund liquidates, the private company lists and collects the convergence. That bounded wait is what keeps the discount narrow. In Nepal's banking sector the promoter line has no scheduled path to liquidity at all: no lock-up that ends on a date, no conversion on a timer. The convergence trade has no maturity, which is precisely why the discount can be so wide and stay so wide.

The Kathmandu Post made the comparison years ago. BP trades in both New York and London and the two prices track each other almost exactly because an institution can move shares between the venues freely and any gap is arbitraged shut in short order. NEPSE's two lines cannot be moved between venues, because one of them is legally pinned in place. Same company, same claim, two prices and no mechanism to force them together. The wonder is not that the gap exists. The wonder is that anyone expected a market to close a gap it has been forbidden to close.

A thin market is a cheap market

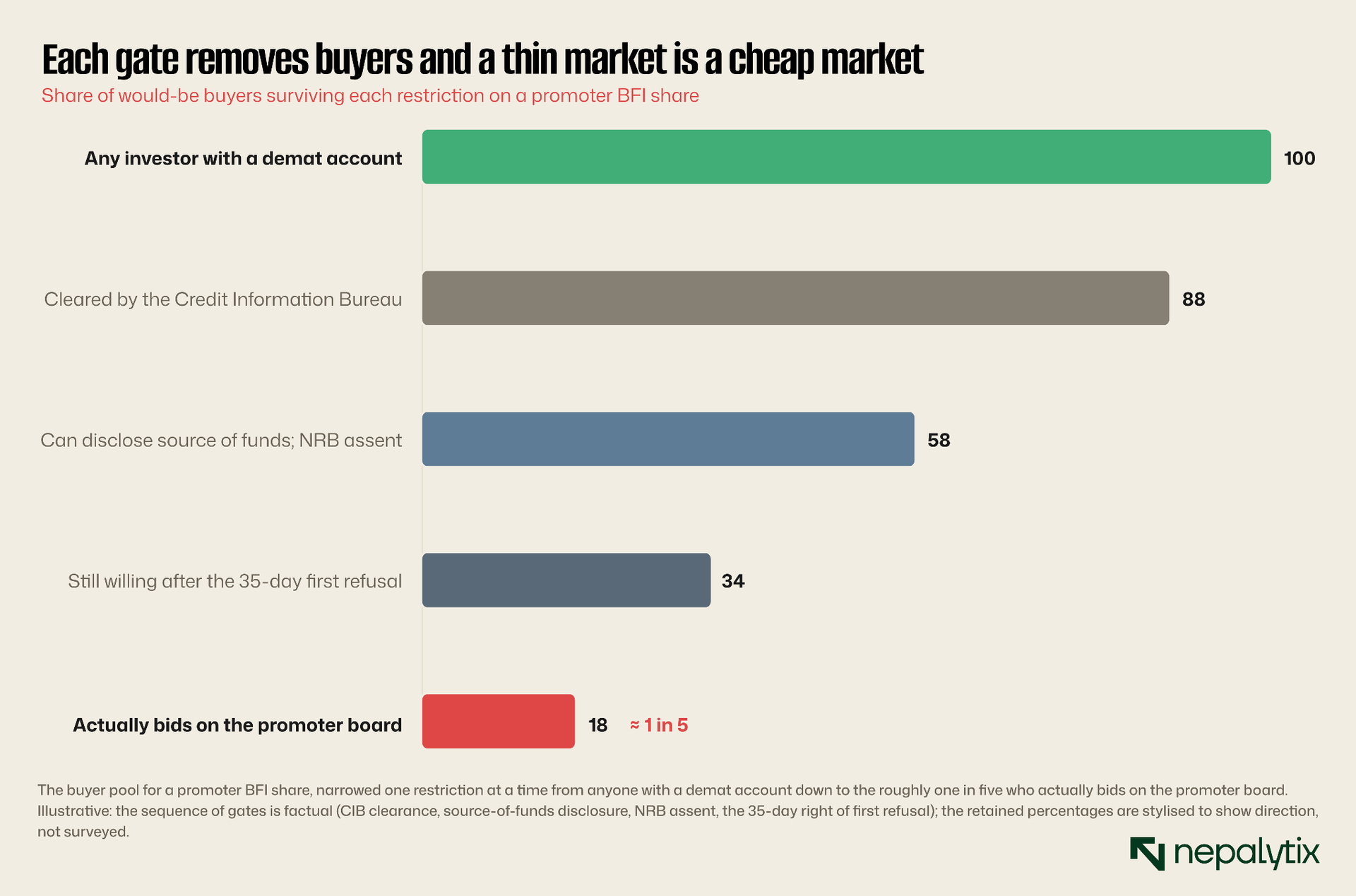

To understand why the tax is so heavy, count the buyers the rules remove. An ordinary Nabil share can be bought by anyone in the country with a demat account and the cash to pay for it several million people. A promoter Nabil share can be bought only by the subset of those people who clear the Credit Information Bureau who can document their source of funds to a bank regulator's satisfaction who are willing to sit through a thirty-five-day first-refusal window during which an existing promoter can step in and take the shares instead and who after all that still want them.

Each gate is a filter, and filters compound. By the time you reach the bottom of that funnel the effective bidding population for a promoter share is a small fraction of the crowd that competes for the ordinary one. Fewer bidders means fewer trades, wider spreads, longer stretches where the share does not trade at all and a price that when it finally prints, prints low. This is not a market failure. It is a market succeeding at pricing exactly what it has been given: a claim that most of the market is forbidden to buy. Take the crowd out of a stock and you take the price out of it too.

You can object that this is all downstream of regulation, and that a rule-free promoter share would trade at parity. It is a reasonable objection. Nepal has, as it happens, run the experiment.

The Nabil experiment: what happens when you remove the rules and the discount stays

Here is the detail that turns this from a story about regulation into a story about markets. Not every promoter share on NEPSE is wrapped in a straitjacket. A handful are, by an accident of history, freely tradeable, legally indistinguishable from ordinary shares in every respect including liquidity. Nabil's is the cleanest case.

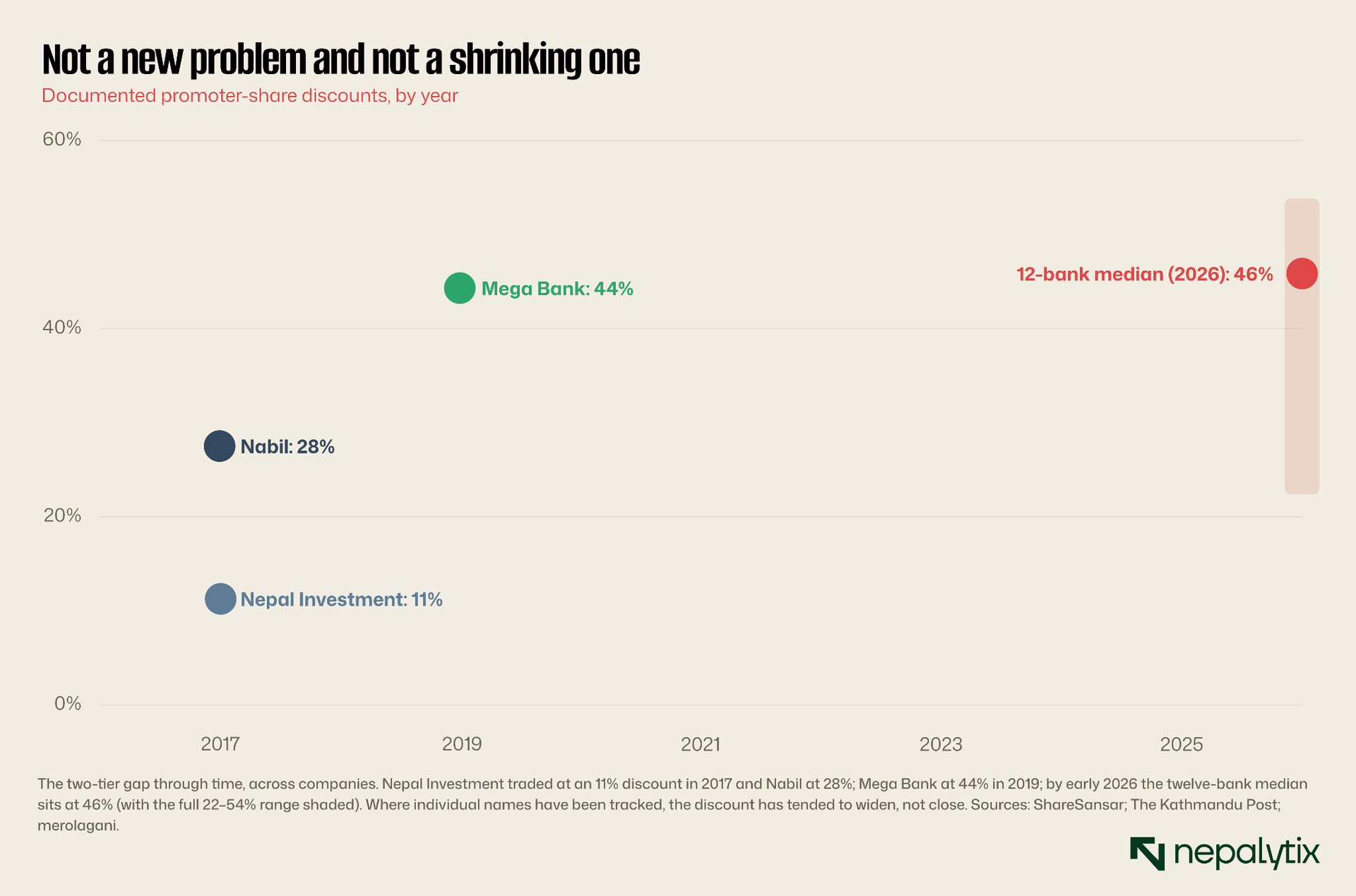

When Nabil was built, its paid-up capital was held roughly half by its foreign joint-venture partner, ten percent by a state insurer, thirty percent by the IPO public, and ten percent by NIDC, a state-owned development bank. Years later, Nepal Rastra Bank issued a directive forbidding one bank from holding shares in another the cross-holding ban and NIDC was forced to offload its ten percent of Nabil. It did so through a series of public auctions. Those shares entered the market as Nabil promoter stock NABILP but carried none of the usual restrictions: any member of the public could buy them at auction on a simple self-declaration of not being blacklisted. Freely tradeable. Same dividend, same vote, same everything as the ordinary share and crucially no illiquidity wrapper.

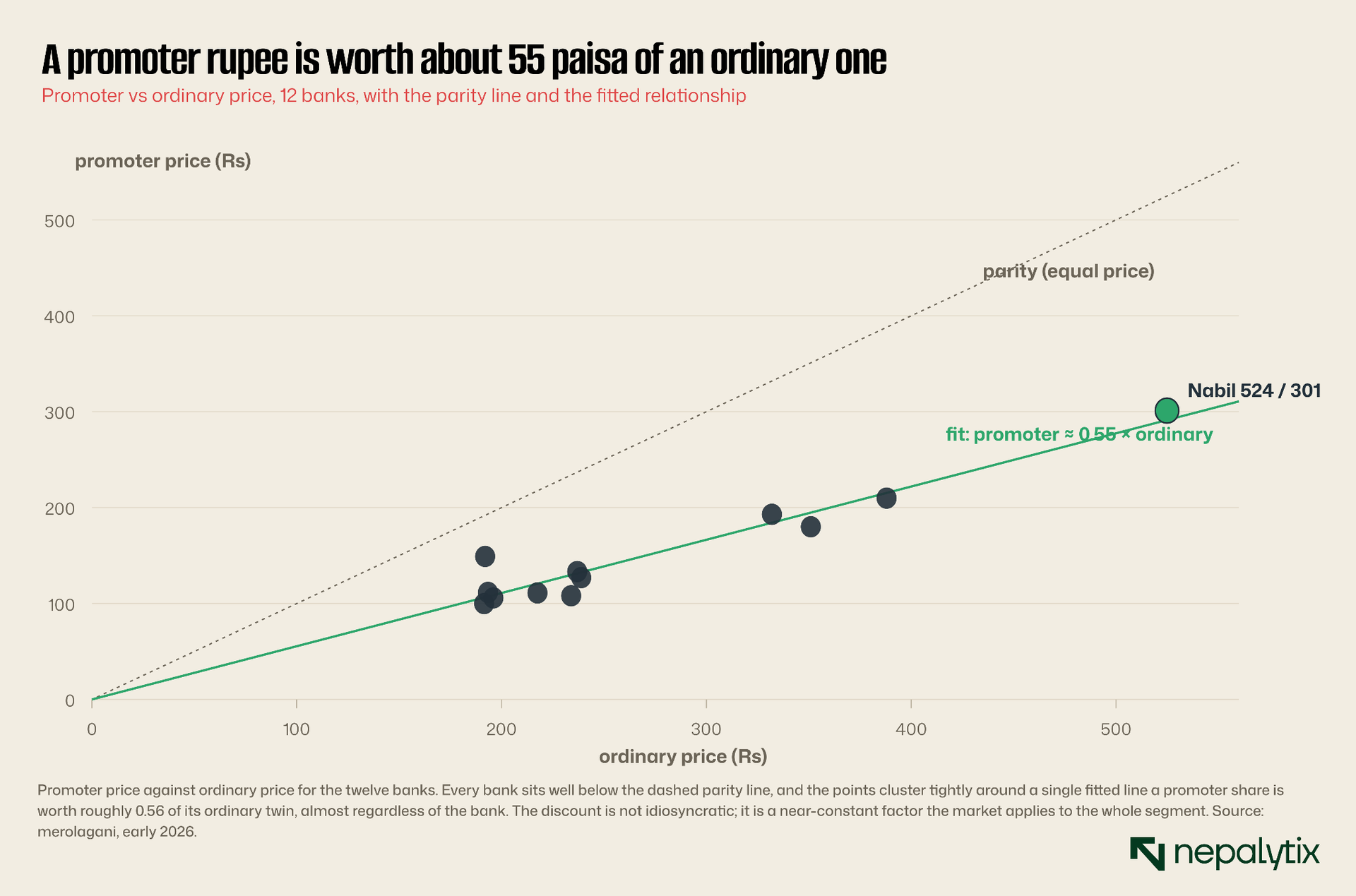

By the logic that the discount is "just" the straitjacket, NABILP should have converged to NABIL almost immediately. It did not. For years the freely-tradeable promoter share traded well below the ordinary share more than fifty percent below at the outset, in the mid-2010s, narrowing to roughly a twenty-eight percent discount by 2017 as investors slowly understood that the two were interchangeable. The gap was closing. The market, people said, was learning.

And then it stopped learning. As of early 2026, with NABIL around Rs 531 and NABILP at Rs 301, the discount on the freely-tradeable promoter share is not twenty-eight percent. It is forty-three percent. It did not converge. It widened and it widened as the broader market fell from its 2021 peak which is the tell. When sentiment sours and liquidity dries up, the market punishes the thinner, less-loved line of stock harder even when that line is legally identical to the one beside it. The straitjacket had already been removed years earlier. The discount survived its removal and then deepened.

The straitjacket was removed years ago. The discount survived its removal and then it grew.

This is the uncomfortable finding at the centre of the two-tier market. Part of the promoter discount is legal friction and you could legislate it away tomorrow. But part of it is pure segmentation, a self-reinforcing habit of the market to treat the promoter line as a second-class security, to trade it thinly to demand a discount for holding it and thereby to keep it thin and discounted. Liquidity is partly a fact about rules and partly a fact about belief. Nabil proves that removing the rules is necessary but not sufficient. The belief has a half-life of its own and on current evidence it is measured in decades.

Is the discount free money? Only if you can afford to wait

The obvious retail reaction to a forty-three percent discount on an identical claim is to buy the cheap one. Same dividend, same vote bought at fifty-seven paisa on the rupee: the running yield on a promoter share is mechanically higher than on the ordinary share because you are buying the same dividend for less money. For an investor who wants income from a bank and never intends to sell, the promoter share is not a trap; it is the better deal and a certain kind of patient Nepali investor has quietly understood this for years.

But call it free money and you will eventually pay for the phrase. The discount is compensation for a real cost and the cost is exit. The day you need to sell you learn what illiquidity means: a promoter share can sit for weeks without a buyer, and when a buyer appears it is on the buyer's terms not yours. You are also exposed to the one risk no dividend can offset that the discount widens rather than narrows. Nabil's freely-tradeable line is the cautionary tale. An investor who bought it in 2017 at a twenty-eight percent discount, reasoning that the gap was closing and convergence was near, has watched the discount grow to forty-three percent instead. The dividends kept coming; the capital gap got worse. Betting on convergence is betting on a shift in market psychology and for bank shares on a discretionary act of the company and the regulator that may never come.

So the honest answer is that the promoter discount is a yield pickup for the genuinely long-term, income-focused holder and a value trap for anyone who might need to sell or who is buying purely to capture a convergence with no scheduled date. Which of those you are is not a market question. It is a question about your own horizon and your own liquidity and it is the question the discount is really asking you.

Now the part that should worry the finance minister

So far this is a story about investors leaving money on the table or not depending on your view of whether a forty-three percent discount on an identical claim is a bargain or a value trap. Reasonable people can trade that position. What is not a matter of opinion is what the two-tier market does to the single most-quoted number in Nepali finance: market capitalisation.

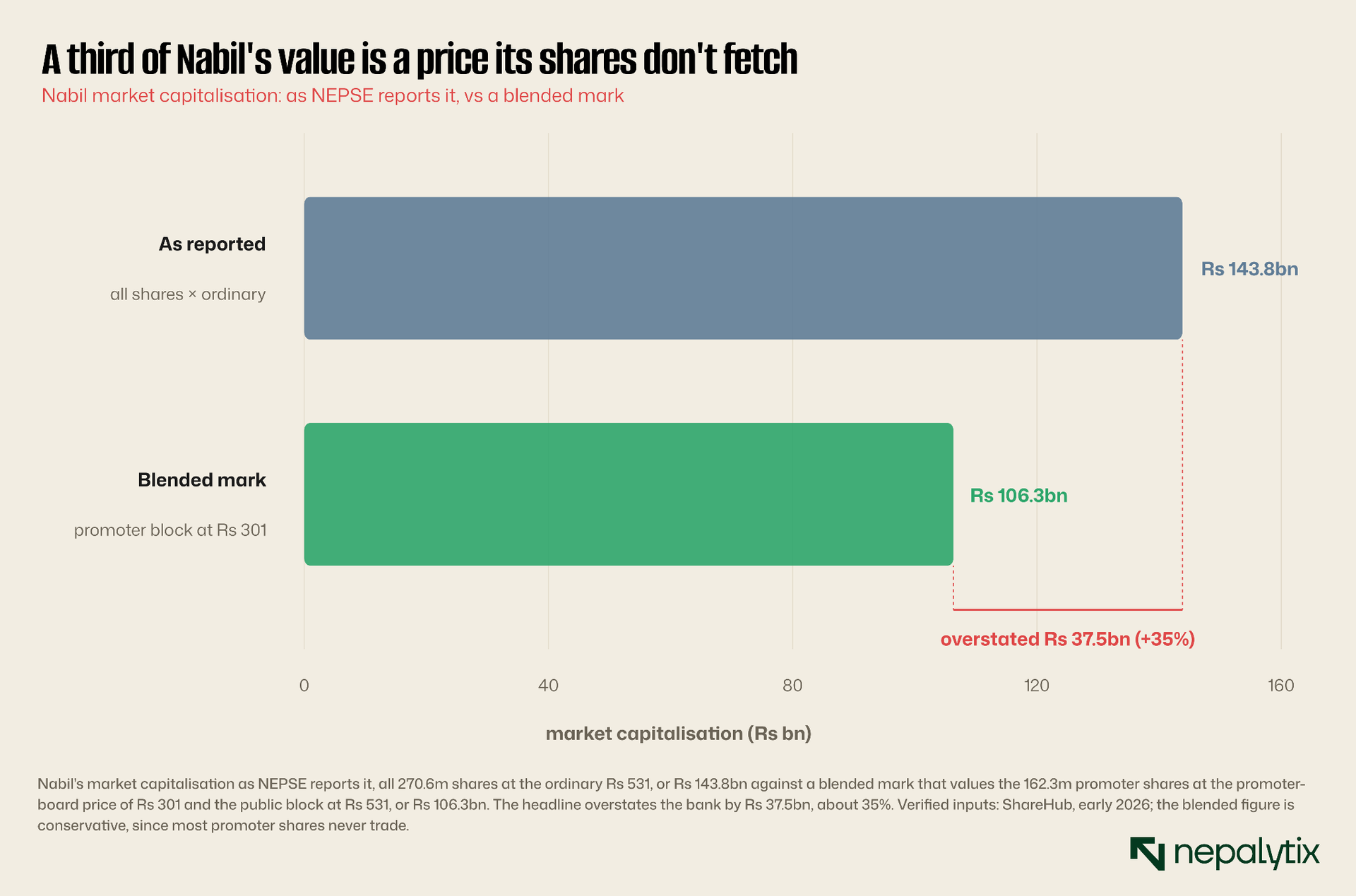

When NEPSE computes the market value of a listed company, it multiplies the total number of shares promoter and public together by the ordinary share price. Every promoter share in the country is marked at the price of the ordinary share, including the majority of promoter shares that trade at a steep discount to it and including the many that do not trade at all. The exchange has a defensible reason: promoter shares are illiquid, their prints are stale, and using a stale promoter price would be its own kind of lie. But the consequence is a systematic overstatement and it is largest exactly where it does the most damage.

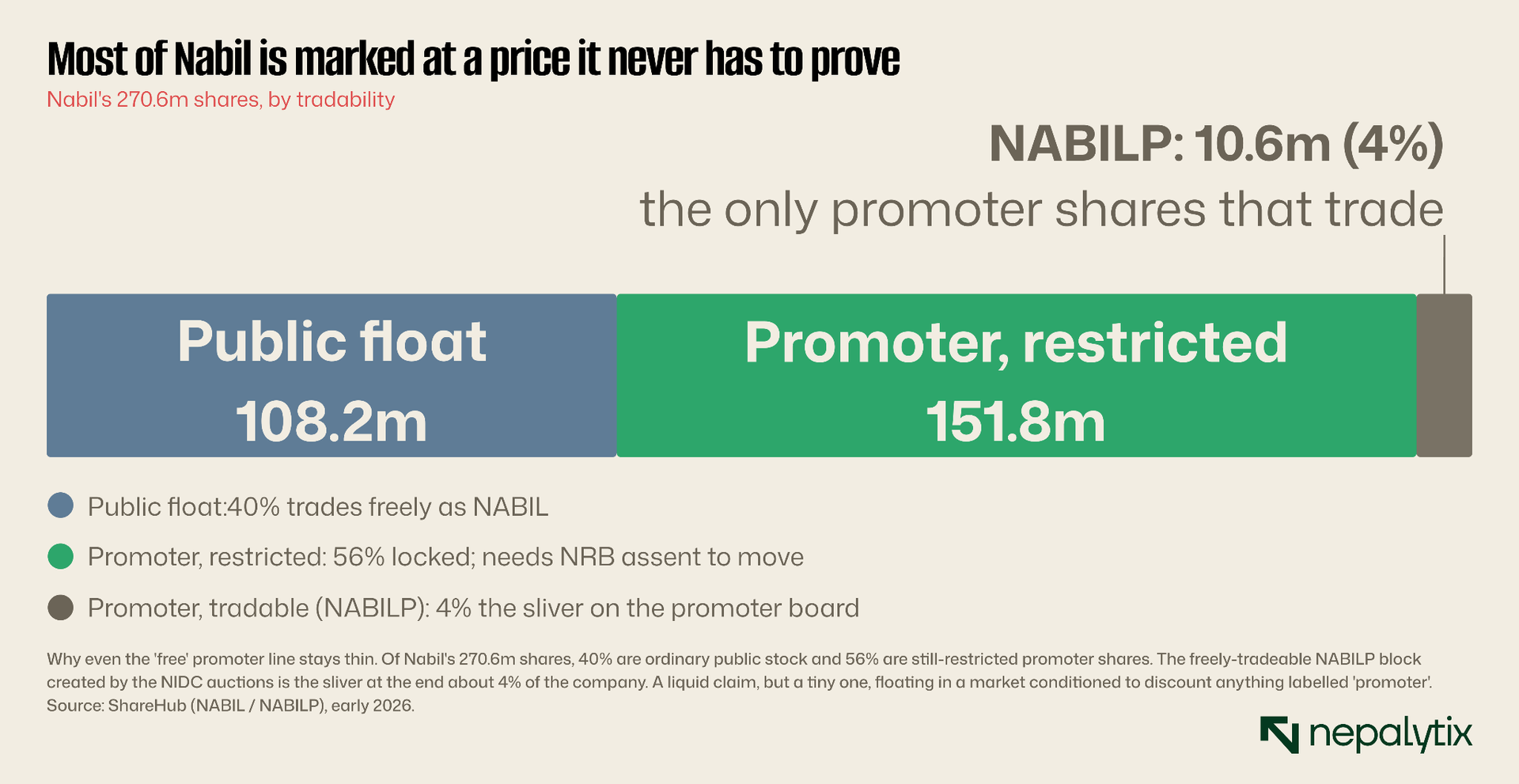

Return to Nabil, where we have clean, current numbers. Nabil has 270.6 million shares outstanding: 60 percent promoter, 40 percent public. NEPSE marks all 270.6 million at the ordinary price of Rs 531 and reports a market capitalization of Rs 143.8 billion. But 162 million of those shares are promoter shares and the market's own promoter board says a Nabil promoter share is worth Rs 301 not Rs 531. Mark the promoter block at the price the market actually assigns it, keep the public block at the ordinary price, and Nabil is worth about Rs 106 billion.

The headline overstates Nabil by roughly Rs 37 billion about a third of the bank and that is the conservative adjustment, because it assumes every promoter share could fetch the Rs 301 that the small freely-traded slice fetches when in reality most of the promoter block is locked and would fetch less if it were forced to market. One bank, one afternoon, a third of its headline value resting on a price its majority shareholders do not command.

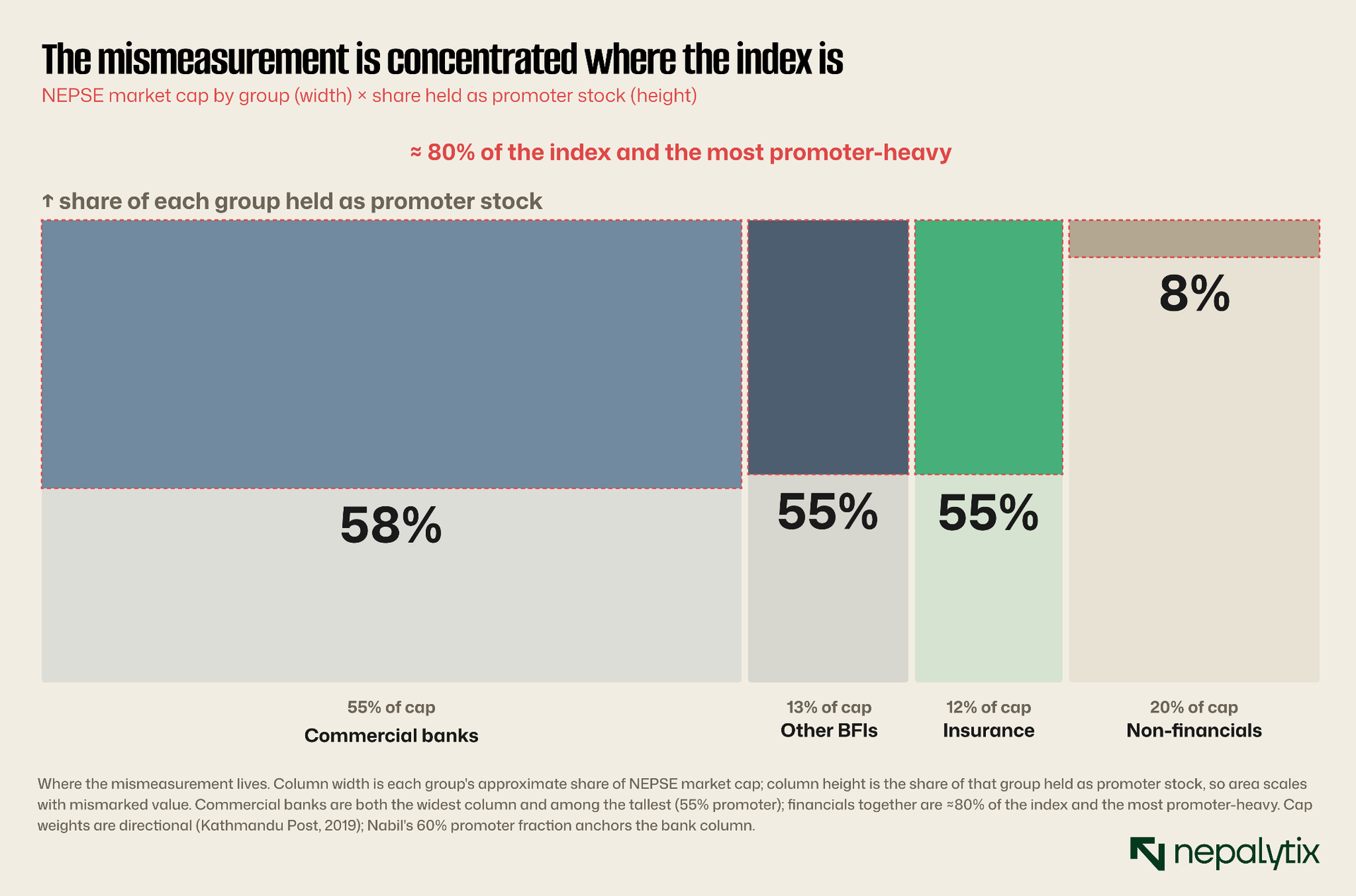

Now multiply. This overstatement is not spread evenly across the market. It concentrates in the companies with the largest promoter block and those are the banks, finance companies and insurers that dominate the index.

Banks, other financial institutions and insurers together make up something on the order of eighty percent of NEPSE's total market capitalization, and they are precisely the companies where promoter holdings run highest half to two-thirds of shares outstanding. The distortion is not a rounding error confined to a sleepy corner of the market. It sits inside the largest, most heavily weighted names, which means it sits inside the index itself, and inside every ratio built on top of the index. Market-capitalisation-to-GDP the number reached for whenever someone wants to argue that Nepali equities are cheap or dear is computed from a market cap that is inflated most in its largest constituents. The country is measuring the size of its stock market with a ruler that stretches most where the market is biggest.

NEPSE already admits the problem in a different window

The most damning fact about the market-cap distortion is that the exchange has already conceded it just not where anyone looks. Alongside the headline index NEPSE computes a free-float index that deliberately excludes promoter holdings, government stakes and other locked-in shares on the explicit reasoning that those shares are not actually available to trade and should not be counted as though they were. The float index exists because someone at the exchange understood, correctly, that valuing locked shares at the market price of unlocked shares gives a misleading picture.

That understanding stops at the index and never reaches the market-capitalisation figure. The same promoter shares the float index strips out as untradeable are marked, in the market-cap calculation, at the full ordinary price the very treatment the float index was invented to avoid. The exchange runs two internally contradictory methodologies side by side: one that says promoter shares are not worth the ordinary price because they cannot trade, and one that says they are worth exactly the ordinary price because it is convenient. The headline number the country quotes is built on the second.

Fixing this does not require abolishing the two-tier market or waiting for banks to convert. It requires only that the market-capitalisation figure adopt the honesty the float index already embodies, marking promoter blocks conservatively or publishing a blended capitalisation beside the headline. It is a reporting choice available today that would pull the most-cited number in Nepali finance closer to the truth while the slower work of convergence proceeds.

How long the two prices stay two prices depends entirely on the sector

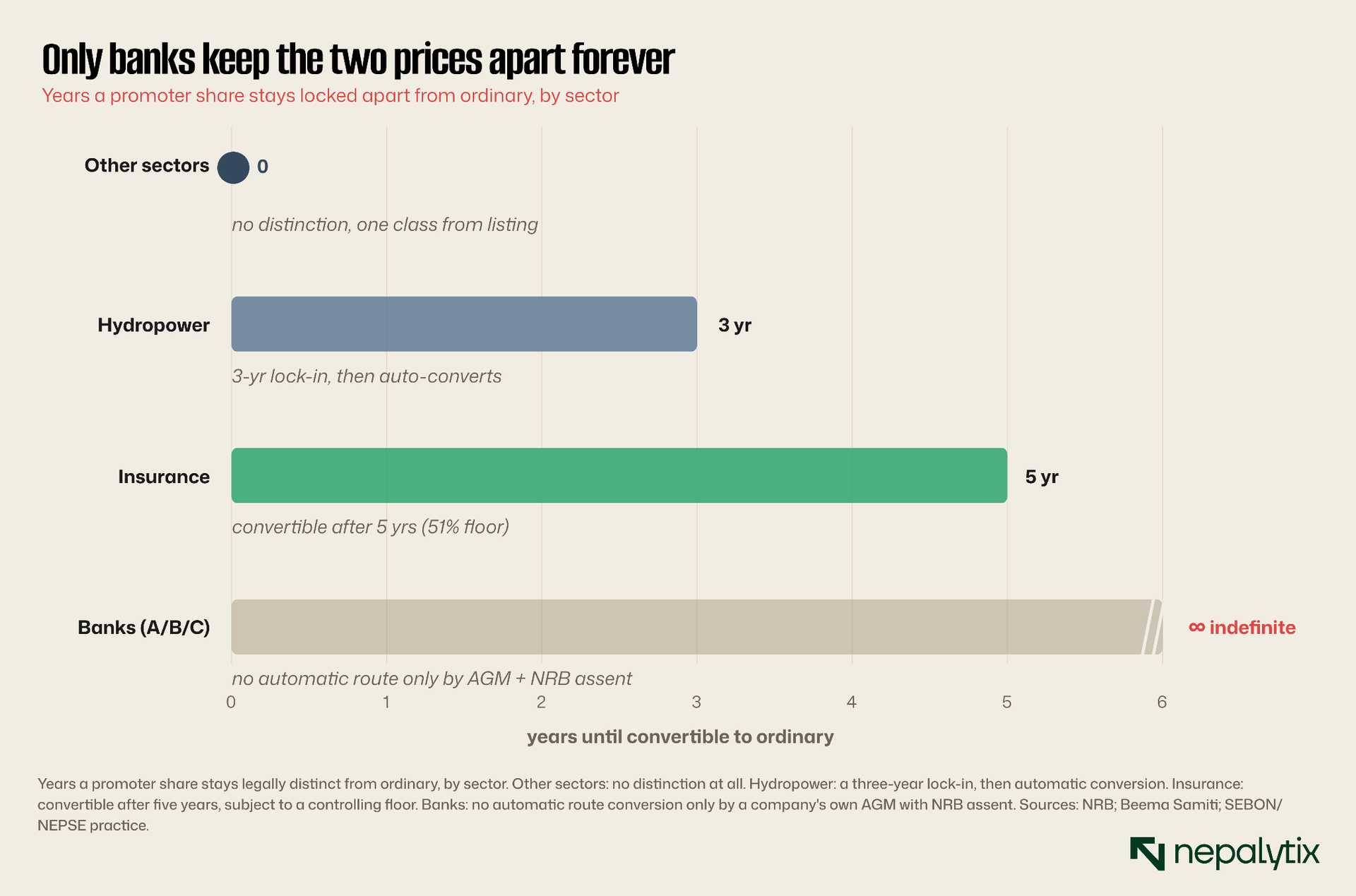

If the two-tier market were a fact of nature, there would be nothing to argue about. It is not. It is a policy choice and the clearest evidence of that is how differently the choice is made across sectors. The promoter–ordinary split is not a feature of Nepali equity; it is a feature of Nepali financial equity and even there it is temporary in most cases and permanent in only one.

In a manufacturing or trading company, there is no promoter board and no discount; the shares are one class from the day they list. In hydropower the sector minting new listings fastest promoter shares carry a three-year lock-in and then convert automatically into ordinary shares, after which the distinction and the discount simply cease to exist. Insurance sits in between: promoters may convert to ordinary after five years, subject to keeping a controlling floor. Only in banking is the split designed to last forever. There is no automatic conversion for a bank's promoter shares. They become ordinary only if the bank's own annual general meeting resolves to convert them and Nepal Rastra Bank assents a discretionary act not a scheduled one.

Three of the four corners of the market in other words have already decided that the two-tier structure is a phase to be grown out of, not a permanent condition. The gap closes on a timer or never opens at all. Banking is the lone holdout, and it holds out for a specific, stated reason.

Why the central bank keeps the wall up and where the argument runs out

Nepal Rastra Bank's defence of the permanent split is not frivolous, and it deserves to be put at its strongest. Banks are not manufacturers. They take deposits from the public. The people who control a bank control other people's money, and the central bank's licence is in part, a judgment about the fitness of those people. If promoter shares could be sold freely to anyone the moment a bank listed, then control of a deposit-taking institution could pass quietly and through the open market, to whoever accumulated enough of the float a blacklisted defaulter, a shell for undisclosed money, a fit-and-proper failure the licensing process was designed to keep out. The right of first refusal, the CIB clearance, the source-of-funds test, the NRB sign-off: each is a gate on who ends up controlling a bank. Given the short and occasionally unhappy history of private banking in Nepal that is not an unreasonable thing to guard.

The trouble is that this argument justifies far less than the structure it is used to defend. It justifies vetting the people who acquire a controlling interest in a bank. It does not justify marking down the small holdings of retail investors who happen to have bought promoter shares at auction and could never assemble control if they tried. It does not justify keeping the two prices apart in perpetuity when insurance in an industry that also holds the public's money in trust, against future claims, manages the same prudential concern with a five-year clock and a controlling floor rather than a permanent wall. And it does not justify the collateral damage: a national market whose headline value is systematically overstated, whose largest companies carry a third of their capitalisation in a price their majority shares do not fetch and whose most-cited valuation ratios are quietly wrong.

There is a cleaner design sitting in plain sight and Nepal already uses it next door in insurance. Vet entry, not exit. Keep every gate that governs who may acquire a controlling block the fit-and-proper tests, the CIB clearance, the NRB approval for any change of control. But put the ordinary retail promoter share on a conversion clock as hydropower and insurance already do so that after some fixed number of years a promoter share held by an ordinary investor becomes an ordinary share, full stop. The regulator keeps its grip on control. The market loses its permanent second class. The mismeasurement drains away as the two prices become one.

The strongest objection to any of this is not prudential but technical, and it deserves a hearing. Convert promoter shares to ordinary and you increase the supply of freely-tradeable stock, sometimes dramatically a bank that is sixty percent promoter-held could more than double its float. In a rising market that supply is absorbed. In a market already grinding down from its 2021 high, a wave of newly-liberated shares looking for buyers could push prices lower, still punishing exactly the ordinary shareholders the reform is meant to serve. This is the fear that keeps even reform-minded participants cautious: that one-share-one-price done abruptly, delivers its long-run benefits by way of a short-run route. It is a real risk and it is why the sequencing matters more than the destination.

But notice that the objection is an argument for phasing, not for permanence. Hydropower and insurance manage the supply problem with a clock precisely so that conversion arrives gradually and predictably priced in years ahead rather than sprung on the market. A banking conversion on a five-year timer, announced well in advance and staggered across institutions would let the float expand at a pace the market can digest the opposite of a shock. The choice is not between a permanent wall and a cliff. It is between a wall with no exit and a ramp with a published gradient. The sectors that already chose the ramp are not visibly worse for it.

The convergence has already started; the only question is the pace

None of this is hypothetical. The convergence is under way, one company at a time, through the discretionary channel that currently exists. Banks whose promoter holdings have drifted down toward the regulatory floor have been converting blocks of promoter shares to ordinary; the SEBON register of converted promoter shares grows steadily; in the same week this piece was written, the promoters of one commercial bank were in the market selling promoter shares into public hands. Nabil itself, years ago resolved at its AGM to convert its freely-tradeable promoter line into ordinary shares precisely to end the confusion of two prices for one company and the fact that a residual NABILP line still trades at a forty-three percent discount today is a measure of how partial and slow the discretionary route is.

That is the real indictment. Not that Nepal chose to vet the owners of its banks it should but that it chose to do so with a permanent, market-wide price distortion when a time-boxed conversion would have achieved the same prudential end. The two-tier market is a solution from an era when the concern was that anyone could seize a bank through the exchange. That concern is real and can be met at the point of control. Everything the two-tier structure does beyond that point: the illiquidity tax on small holders, the inflated market cap, the broken ratios, the second-class security that stays second-class even after its chains come off is costless.

One company should not wear two prices. For most of the Nepali market, it already doesn't or soon won't. Banking is the exception and it is an exception the country has the tools to end without surrendering a single prudential safeguard. Until it does remember what the promoter discount actually measures every time you see it on the screen. It is not the market telling you the share is worth less. It is the market telling you what it costs to be forbidden.

Disclaimer

This report has been prepared by Nepalytix for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities.

The information contained in this report is based on sources believed to be reliable; however, Nepalytix does not guarantee its accuracy, completeness, or timeliness. Opinions, estimates, and projections expressed herein are those of the authors as of the date of publication and are subject to change without notice.

Investing in securities involves risks, including the possible loss of principal. Past performance is not indicative of future results. Readers are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Nepalytix and its contributors may hold positions in the securities discussed in this report at the time of publication or thereafter.

Neither Nepalytix nor any of its affiliates accept any liability for any loss arising from the use of this report or its contents.