Your 7% Bank Return Isn’t Really 7%: The Real Earnings After Tax and Inflation in Nepal

That attractive 7% fixed deposit rate is only part of the story. After a 5% tax and rising inflation, your real return drops significantly. Here’s the simple math every Nepali saver should understand before locking in their money.

Your bank is offering 7%. Here is what you are actually earning.

Before tax. Before inflation. The headline rate on a fixed deposit looks good. The real return after both tells a different story. Here is the math Nepal’s banks do not do for you.

Walk into any commercial bank in Nepal right now and ask about a fixed deposit. The person across the counter will tell you a number between 6% and 8%, depending on the tenure. It sounds straightforward. You deposit Rs 100,000, you earn Rs 7,000 in a year, you walk out better off. That is how most people understand it. It is also not the complete picture, because that 7% is the rate before two things happen to it. The first is a tax. The second is inflation. After both, the number you actually keep is different from the number on the banner.

This piece walks through the math, step by step, using the actual current rates in Nepal. By the end you will know how to calculate the real return on any fixed deposit yourself and why the comparison between FD returns and inflation matters more than the headline rate.

Nepal's commercial banks currently offer fixed deposit rates between 6% and 8% per annum, depending on the bank and the tenure. Development banks offer slightly more. Finance companies sometimes offer higher still, which carries its own risk profile we will come back to.

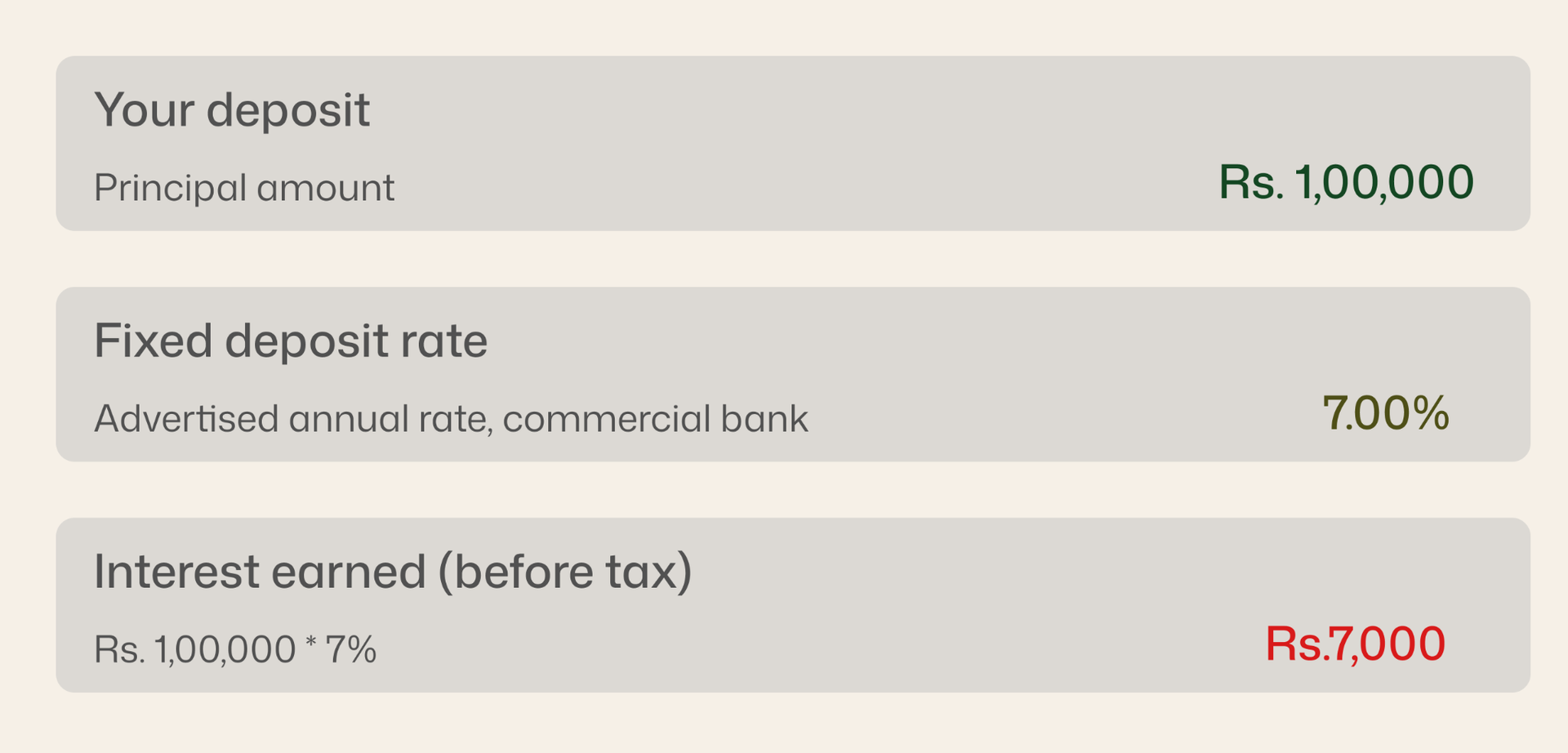

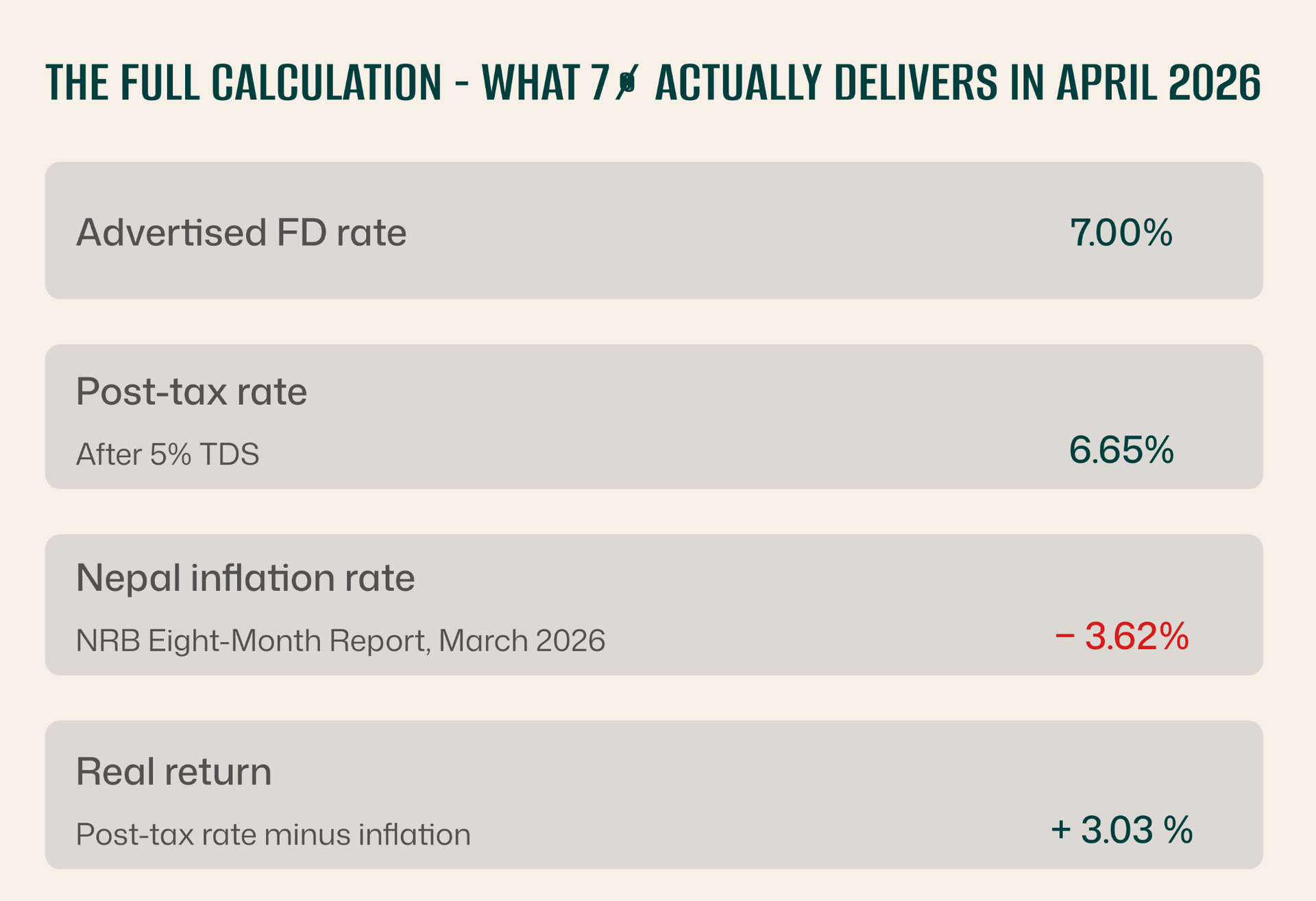

For this calculation we will use 7% per annum, a reasonable midpoint for a one-year fixed deposit at a commercial bank today. The deposit amount is Rs 100,000, because round numbers make the math legible.

So far so good. Rs 7,000 on Rs 1,00,000. That is the number the bank will show you. It is also the last point at which the number looks this clean.

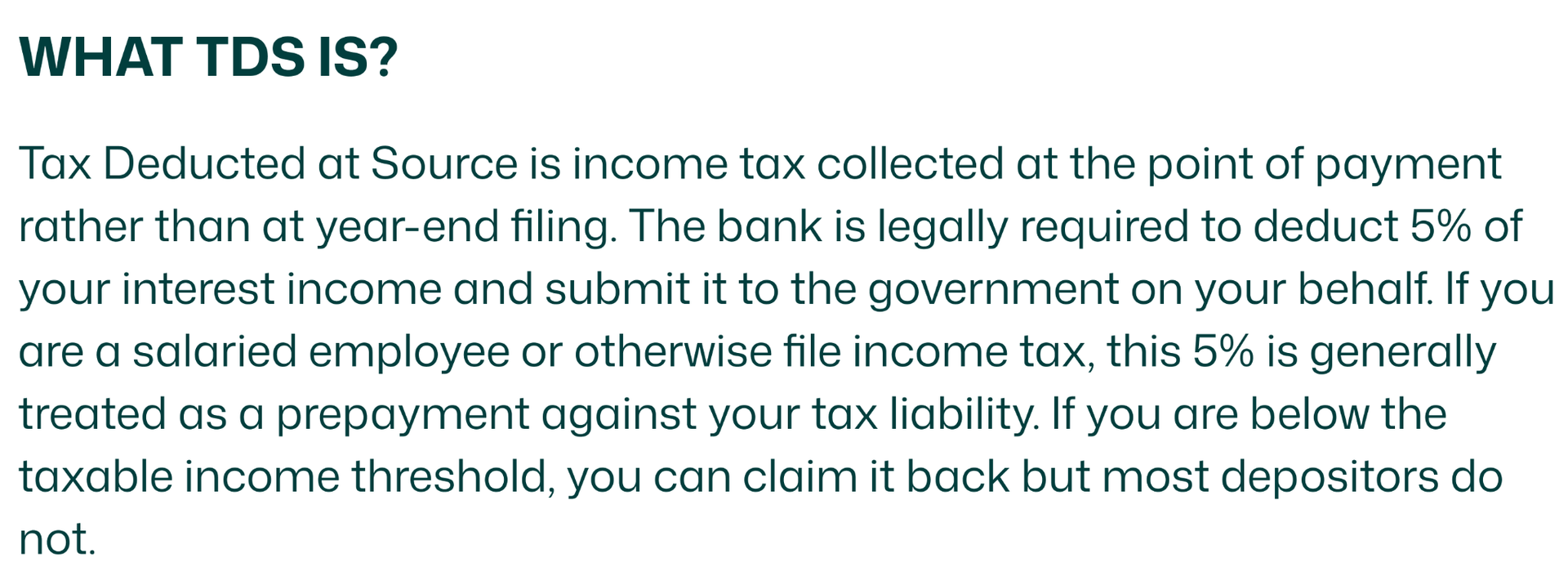

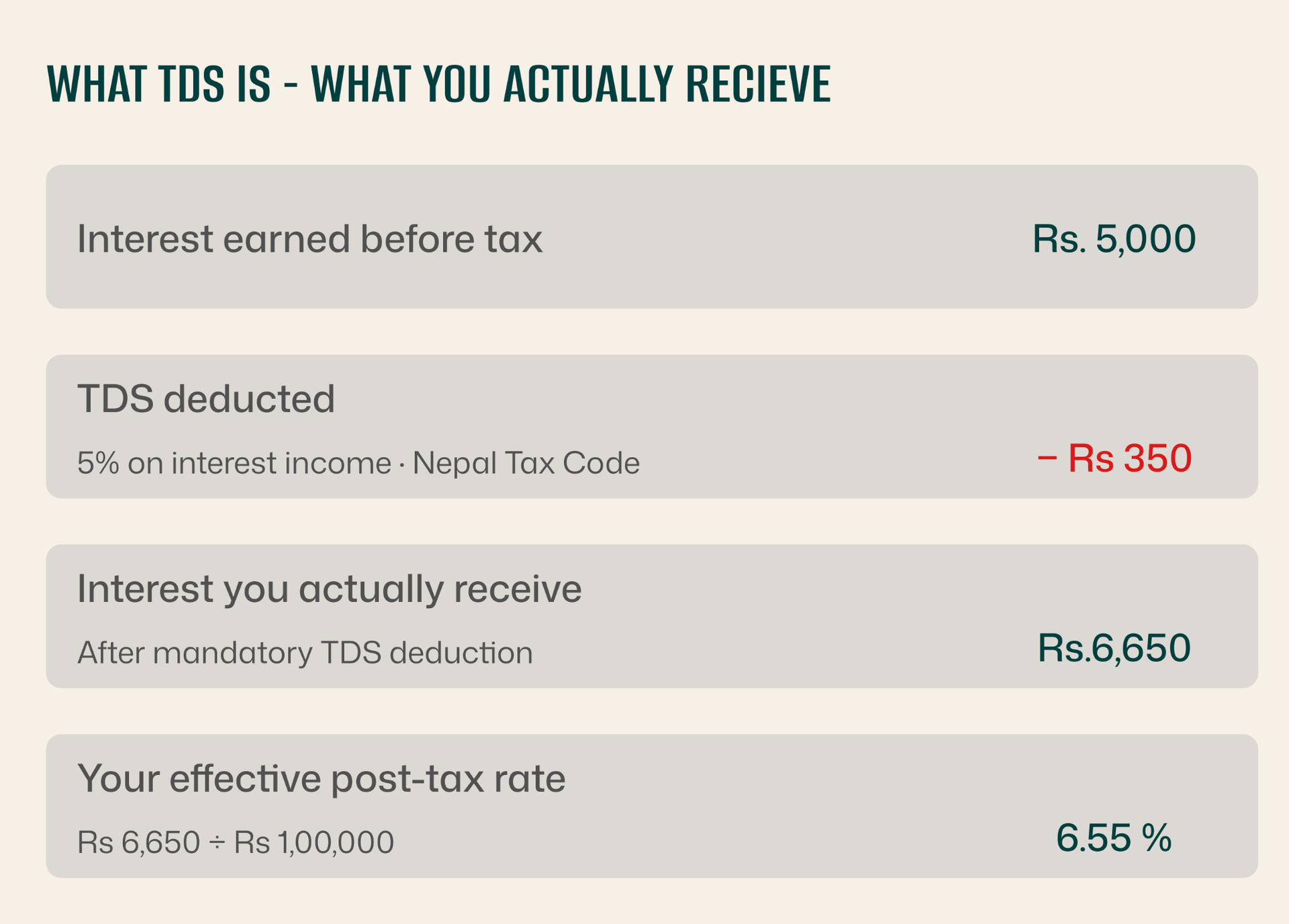

Nepal levies Tax Deducted at Source(TDS) on fixed deposit interest. The current rate is 5% for individual depositors. The bank deducts this automatically before crediting your interest. You do not write a cheque. You do not file a separate return for it. It simply disappears before the money reaches you.

This is the first place the headline rate and the real rate begin to diverge.

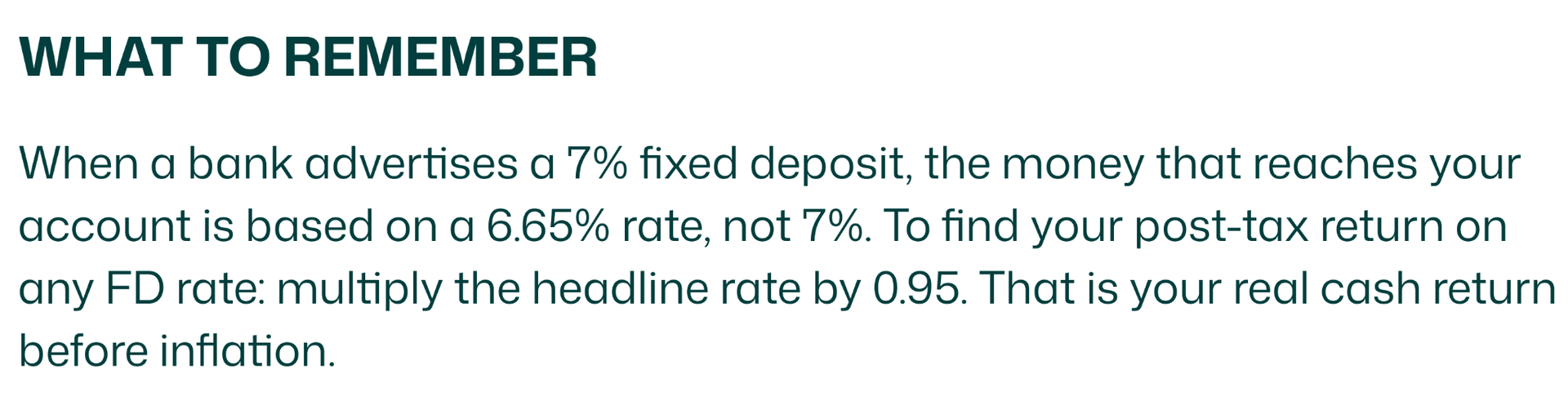

Your 7% fixed deposit is now earning 6.65% in your hands. The Rs 350 is gone, automatically, quietly, before you see the credit. This is not a complaint about the tax system. It is just the first number that needs to be in your calculation when you compare FD returns to anything else.

Your Rs 6,650 in post-tax interest exists in a world where prices are also moving. If prices rise by 3.62% this year which is Nepal's current inflation rate according to the NRB's April 2026 report, then the purchasing power of your money has declined by 3.62%, even as your balance increased by 6.65%.

To find your real return, the return that actually represents a gain in purchasing power, you subtract inflation from your post-tax return. The precise formula is slightly more complex, but the simplified version is accurate enough for practical purposes.

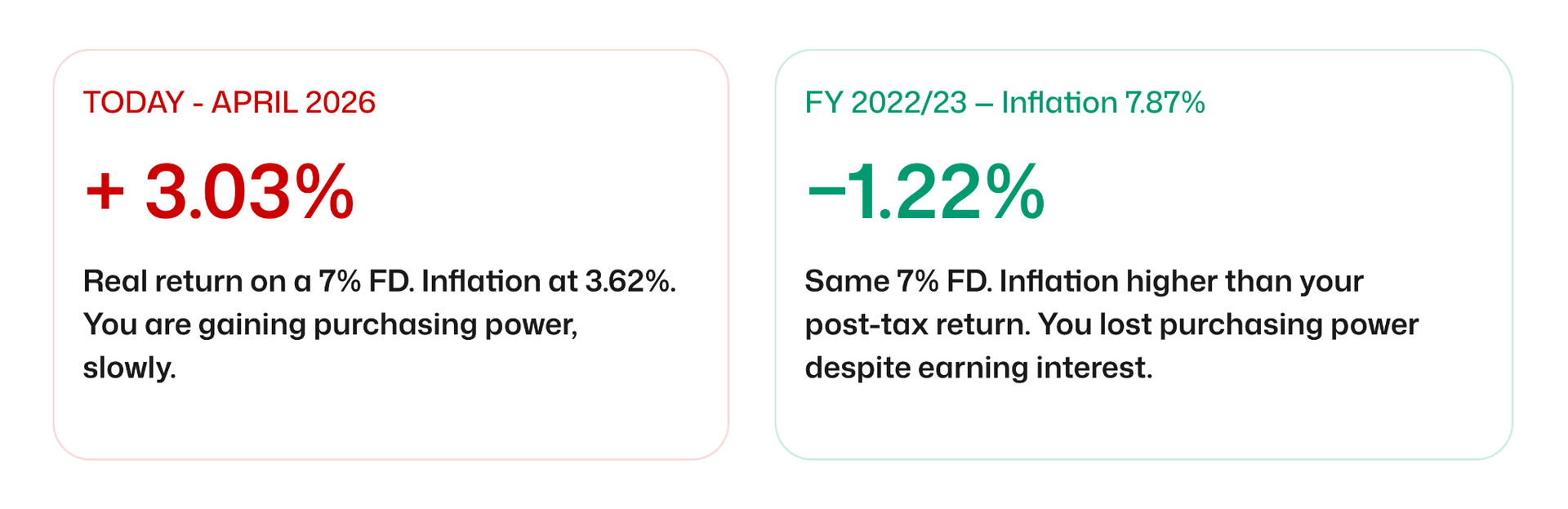

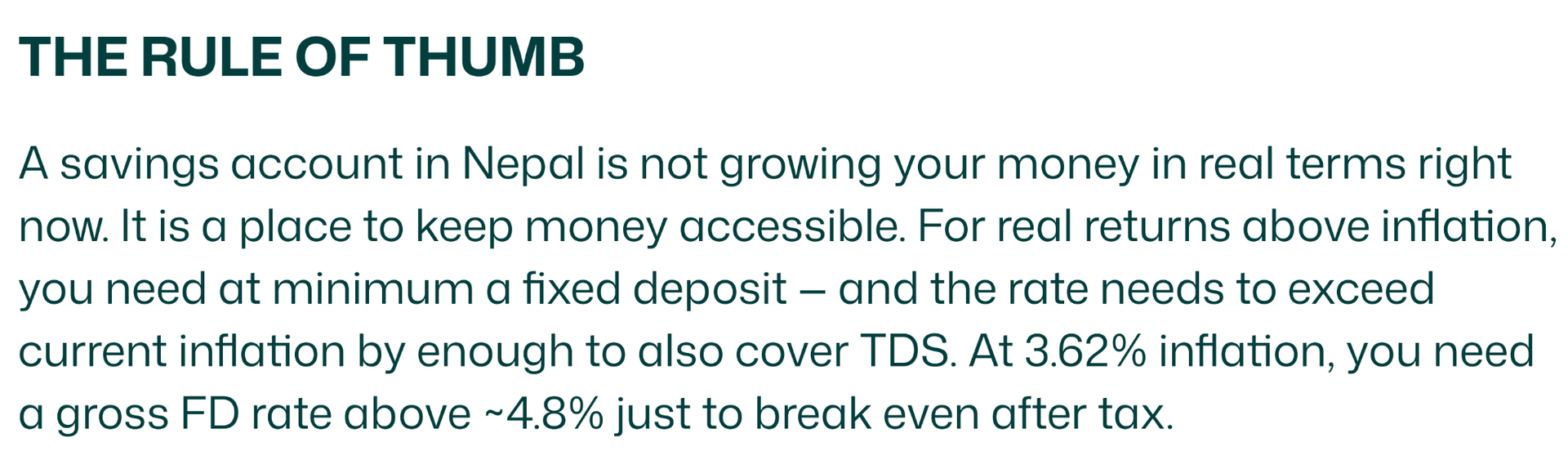

At the current inflation rate of 3.62%, a 7% fixed deposit gives you a real return of approximately 3.03%. Your money grew in purchasing power terms but by 3%, not 7%.

That number changes significantly depending on two variables: the rate the bank is offering, and the inflation rate at the time. Both move. And when inflation is high, as it was in Nepal in FY 2022/23, when it reached 7.87%, the same 7% fixed deposit would have produced a negative real return after tax. You earned interest. You still fell behind inflation.

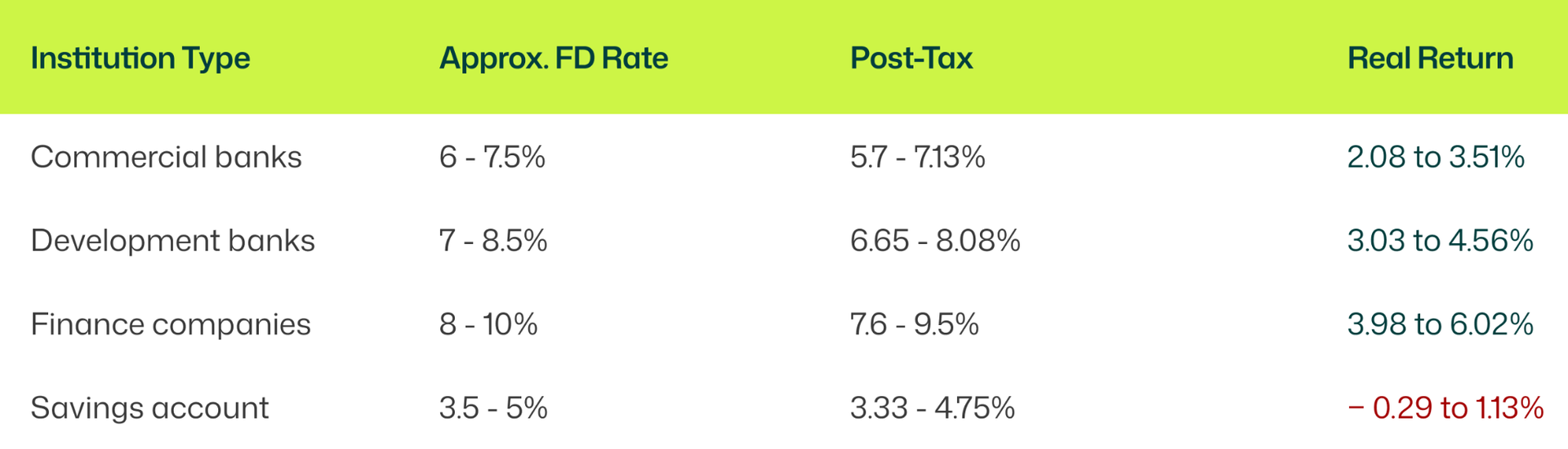

Not all deposits earn the same rate. The type of institution matters, Commercial banks are regulated more tightly and generally offer lower rates than development banks or finance companies. Here is how the real return picture looks across the landscape as of April 2026, at the current inflation rate of 3.62%.

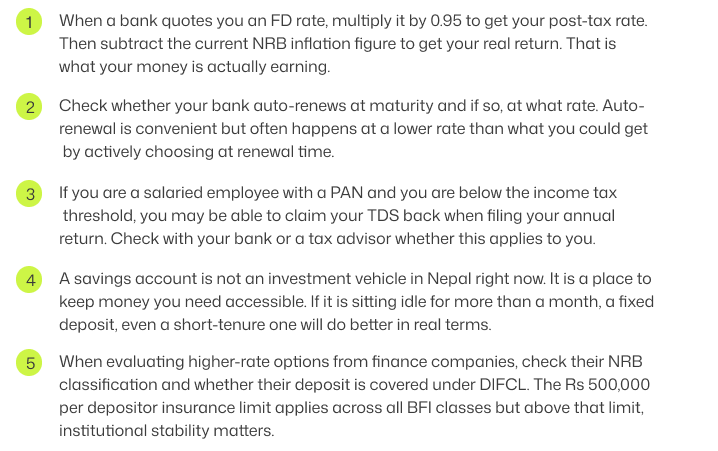

Two things are worth noticing in this table. First, a savings account at current rates may barely beat inflation or fall slightly behind it, most savings accounts in Nepal offer 3.5 - 5%, which after 5% TDS and 3.62% inflation leaves you with a real return close to zero. Second, the higher rates from finance companies come with higher risk. Finance companies are Class C institutions under NRB classification. Their deposit insurance coverage is the same as commercial banks (Rs 500,000 per depositor under DIFCL), but their institutional stability is generally lower.

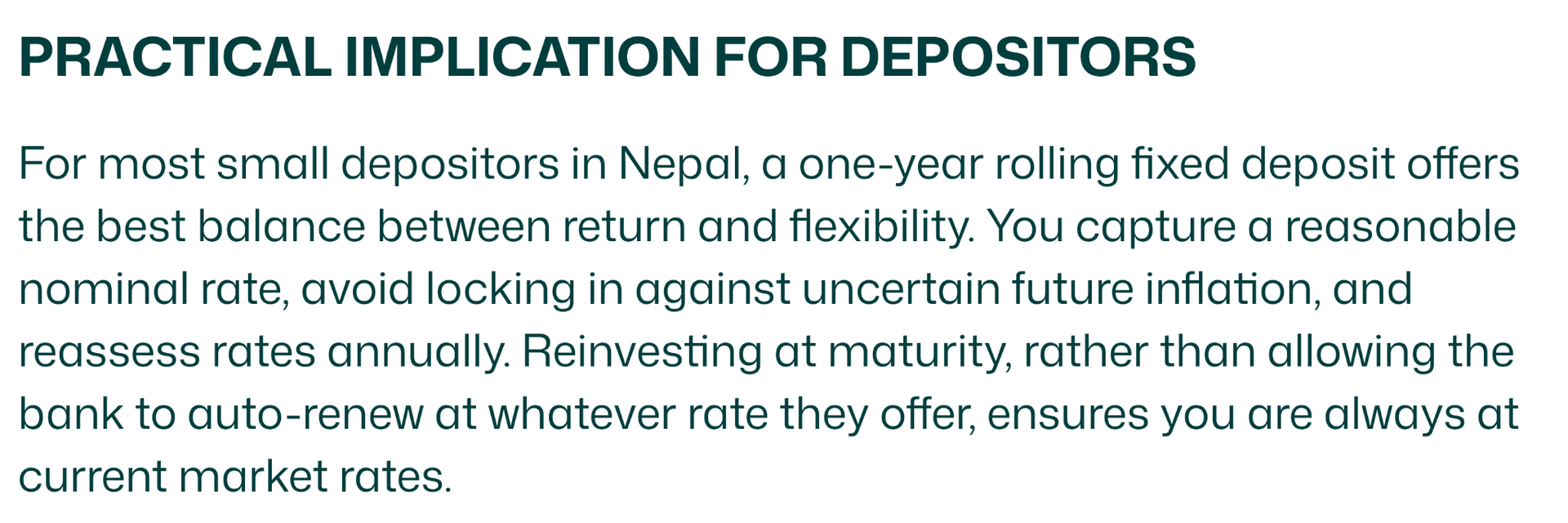

One natural response to low real returns is to extend the tenure, lock the money away for longer, earn a higher rate, and let compounding work. In Nepal, fixed deposits are typically offered in tenures from three months to three years, with longer tenures generally earning higher rates. But two things complicate the compounding story here.

First, TDS is deducted at each interest payout, typically quarterly or at maturity, depending on your agreement. This means compounding happens on the post-tax amount, not the gross amount. The bank may advertise an effective annual yield that assumes gross compounding. The reality is compounding on 95% of the interest each period.

Second, the inflation rate over a multi-year tenure is unknown. If you lock in at 5% for three years and inflation rises to 6% in year two, your real return collapses even as your nominal return stays fixed. Longer tenures offer higher nominal rates but commit you to a fixed real return gamble on future inflation.

The goal of this piece is not to tell you that fixed deposits are bad. They are not. For short-term savings, emergency funds, and capital preservation, a fixed deposit at a regulated commercial or development bank is a reasonable instrument. The goal is to help you read the numbers correctly, so that when you compare a fixed deposit to any other instrument, you are comparing real returns, not headline rates.

The 7% that appears on the banner outside your bank is real. You will earn it. The question is what you earn after the government takes its 5%, and what that remaining amount buys you after inflation has done its work for the year. Right now, with inflation at 3.62%, the answer is approximately 3% in real terms, which is a positive return, and better than recent years. Understanding that number is the difference between knowing your savings are growing and knowing how much.