How NRIC makes money

Nepal Reinsurance Company Limited (NRIC) sits at the center of Nepal’s evolving insurance landscape and FY 2082/83 has become its biggest stress test yet.

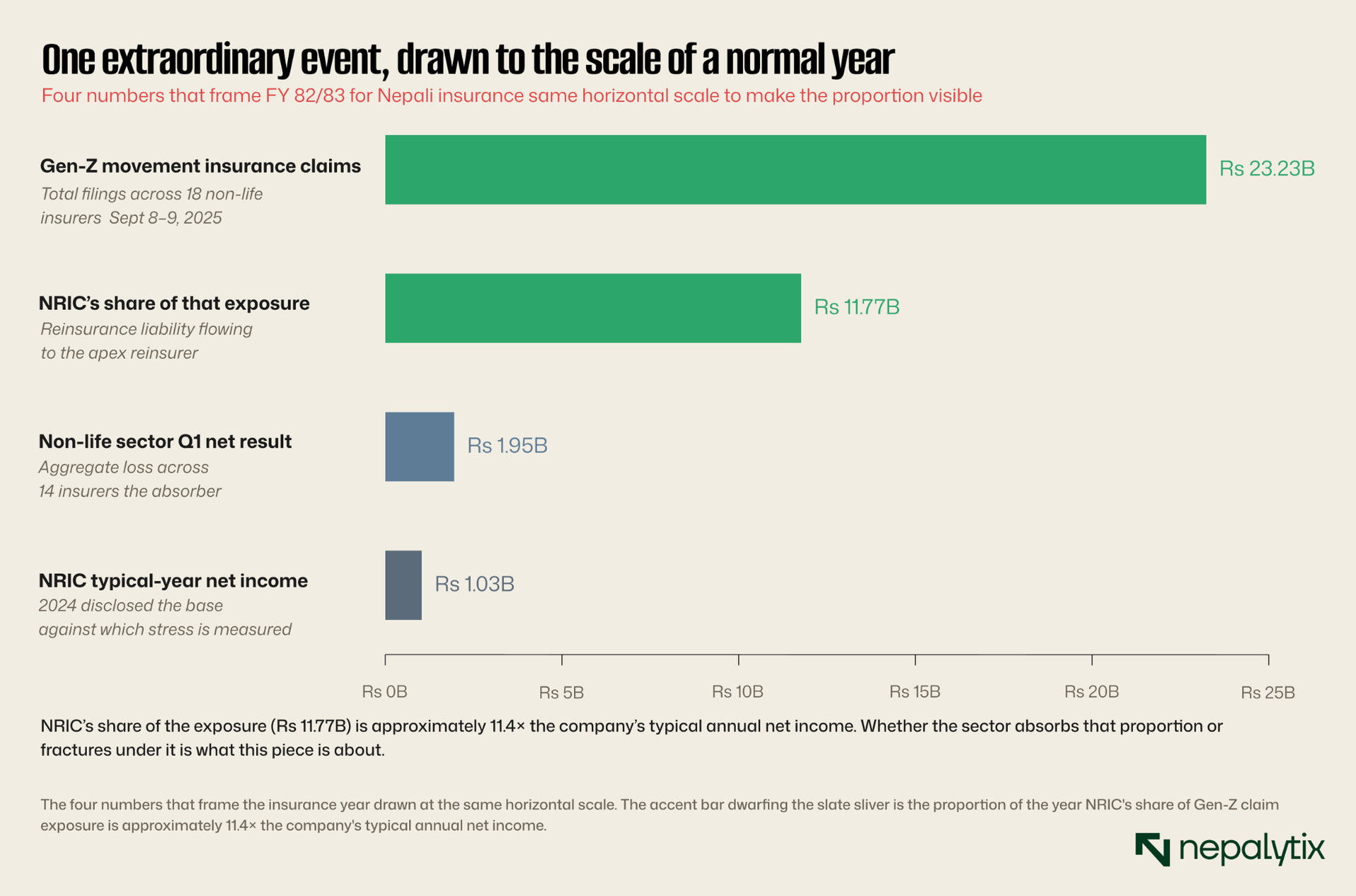

Nepal Reinsurance Company Limited is one of the most analytically interesting companies on the NEPSE board, and one of the least understood by the average Nepali investor who holds it. It is government-affiliated. It is regulated by the Nepal Insurance Authority. It is the apex reinsurer in a small but structurally distinct insurance market. It earns predictable, moderate returns in normal years. And in FY 2082/83 it is sitting at the centre of the largest single insurance event in Nepal's recent history, with reinsurance liability exposure of roughly Rs 11.77 billion against a typical annual net income of Rs 103 crore. To understand what that means and to understand the sector that NRIC underpins requires building a working model of the company from first principles. This piece does that and then puts the model alongside the life and non-life sub-sectors NRIC supports.

The starting point is the structure of the market. Thirty-seven licensed insurance companies operate in Nepal under the Nepal Insurance Authority: fourteen life insurers, fourteen non-life (general) insurers, two reinsurers, and seven micro-insurance entities split between life and non-life. The Insurance Act 2079 BS (2022) replaced the older Insurance Act 2049, renamed the regulator from Beema Samiti to Nepal Insurance Authority and raised minimum paid-up capital to Rs 5 billion. That capital threshold triggered four major mergers in 2022 and 2023 Surya + Jyoti, Sanima + Reliance, Union + Prime + Gurans (forming Himalayan Life), and Prabhu + Mahalaxmi and converted the state-owned Rastriya Beema Sansthan into Rastriya Jeevan Beema Company in November 2023. The sector that exists today is the product of those structural changes, layered on top of a domestic insurance penetration rate of roughly two percent of GDP well below the South Asian average and far below where it will eventually settle.

Two reinsurers in one small market

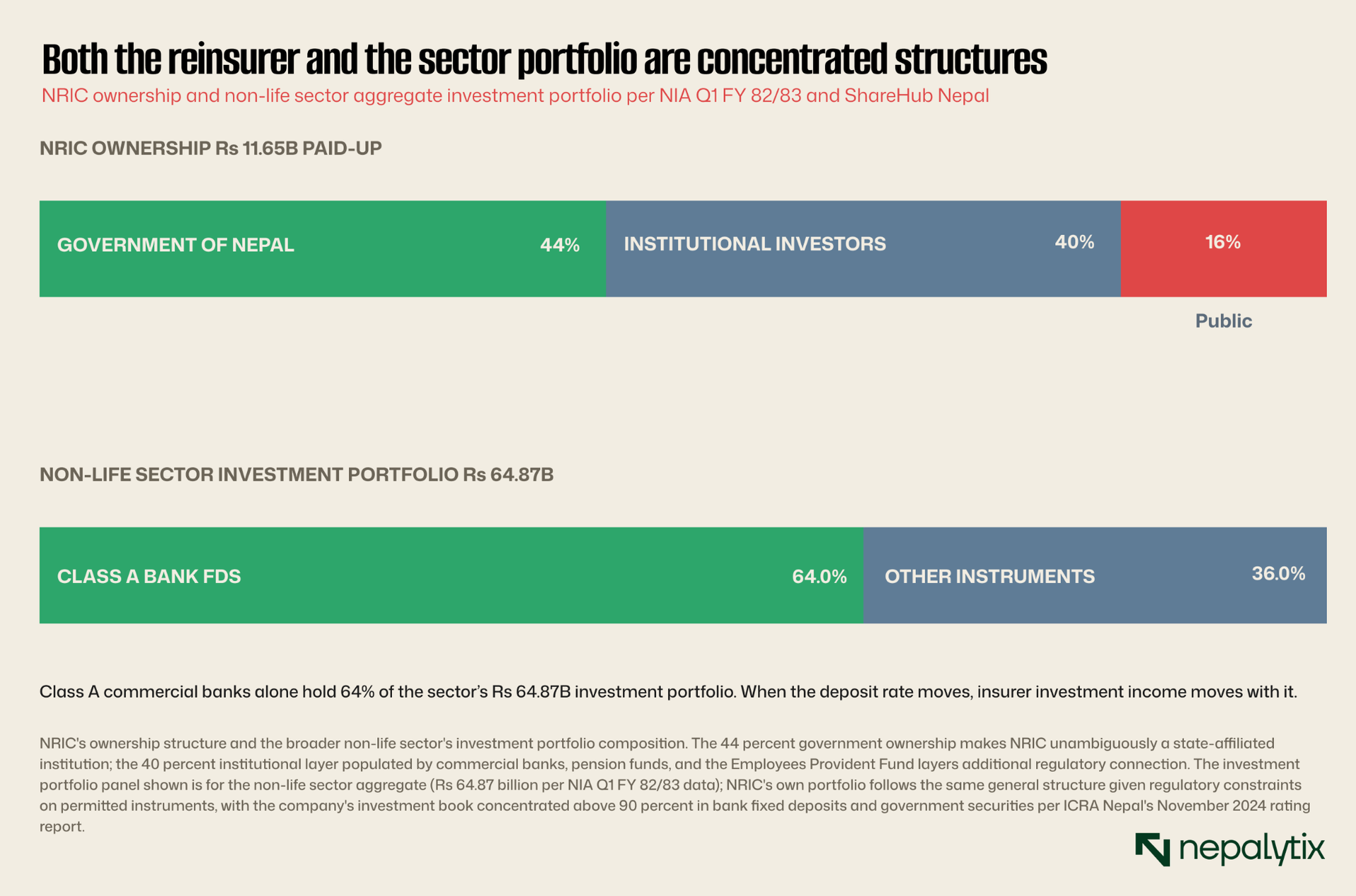

Until January 7, 2024, Nepal Reinsurance Company was the country's only reinsurer. NRIC was founded on December 22, 2014 as the formal corporate successor to the insurance pool established in 2003. The pool itself had been Nepal's improvised response to a problem of timing: at the height of the Maoist insurgency, international reinsurers had effectively exited Nepal, and primary insurers needed somewhere to cede the Riots, Strike, Malicious Damage, and Terrorism (RSMDST) risks that they could no longer reinsure abroad. The Government of Nepal organized the pool. When the insurgency ended, the institutional infrastructure of that pool remained. In 2014, it was formalized into a public-private partnership reinsurer with the Government holding 44 percent of paid-up capital. The remaining ownership today splits between institutional investors at roughly 40 percent and the public at roughly 16 percent following the company's IPO and NEPSE listing.

That history matters because the legacy mandate RSMDST sits at the heart of what NRIC is now being asked to absorb in FY 2082/83. But before getting to that, a description of the company in normal times.

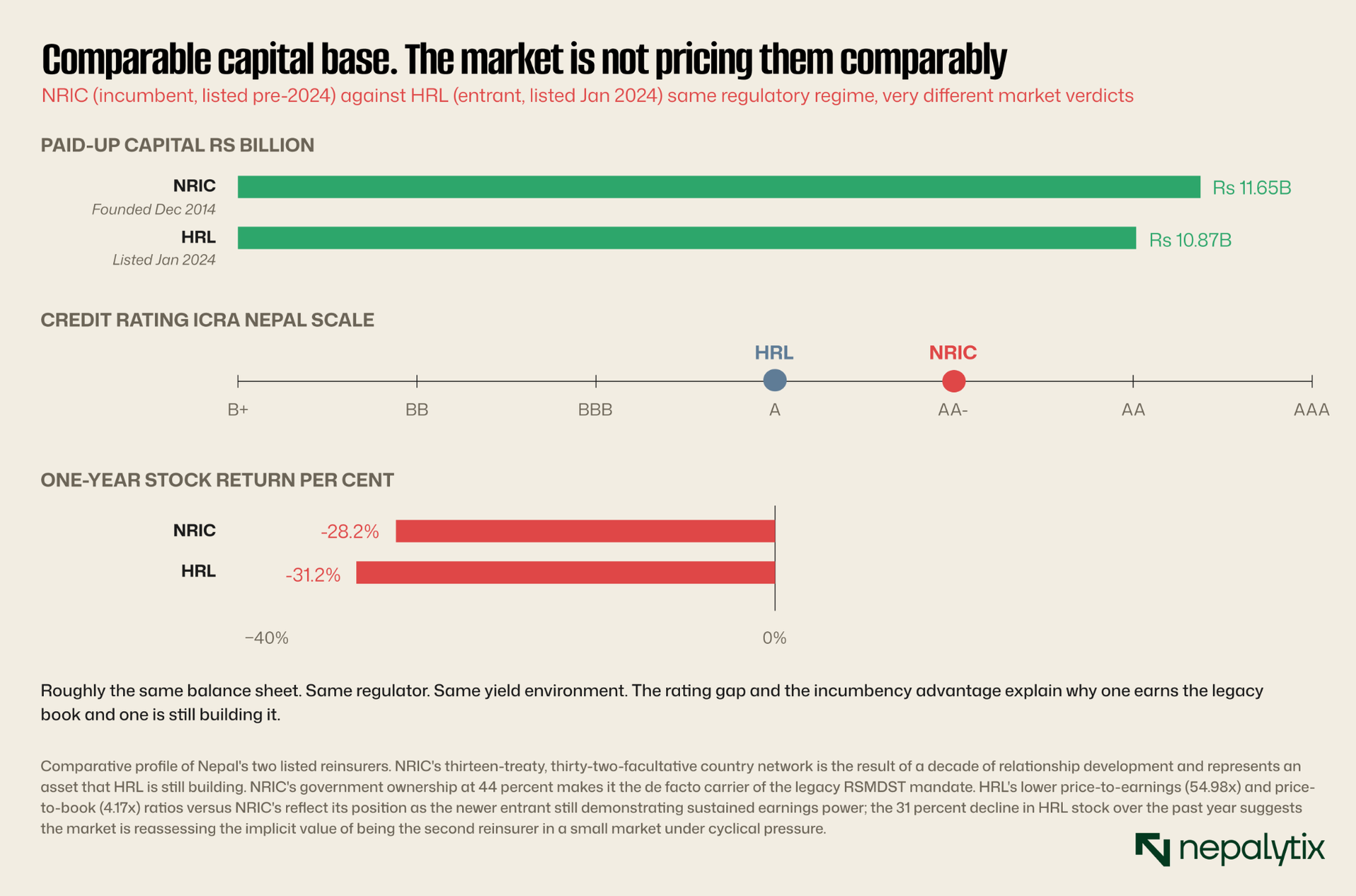

NRIC carries paid-up capital of Rs 11.65 billion. ICRA Nepal rates it AA-, the highest reinsurer rating in the country. It has built treaty reinsurance partnerships in thirteen countries and facultative arrangements in thirty-two countries, a network developed over a decade of relationship investment that makes the company a node in the regional reinsurance market rather than a purely domestic entity. Domestically, NRIC provides reinsurance support to all fourteen life insurers and all fourteen non-life insurers, alongside specialized pools for Motor Third-Party Liability, Foreign Employment, Aviation, and Agriculture. Most cession from the primary insurance sector flows through NRIC.

Himalayan Reinsurance Limited's listing on January 7, 2024 was the first formal end to NRIC's monopoly. HRL came to market with Rs 10.87 billion in paid-up capital slightly smaller than NRIC's and with promoter ownership concentrated in two large government-owned banks and several conglomerate-affiliated entities. International rating agencies assigned HRL AM Best B+ and ICRA-A grades, both investment-grade but a notch below NRIC's AA-. The strategic logic for HRL's existence is straightforward: the structural growth of Nepali primary insurance, particularly as penetration rises from current low levels, creates room for two reinsurers without one needing to displace the other. The Insurance Act 2079 explicitly contemplates a competitive reinsurance market and NIA has supported the diversification on prudential grounds.

The reality of HRL's first eighteen months on the exchange, however, has been challenging. The stock peaked at Rs 1,156 in March 2025 and has since declined to approximately Rs 800, a 31 percent fall from the 52-week high. The decline reflects two pressures. The first is the investment-income squeeze that affects both reinsurers falling bank deposit rates compress investment yield, and HRL feels this acutely because the company is still building scale. The second is the ratings gap: primary insurers seeking the highest-rated reinsurance retrocession default to NRIC when both are available, a structural incumbency advantage that takes years to erode. The competitive equilibrium for the next two to three years is best understood as a duopoly with significant asymmetry, where NRIC retains the legacy book, the government-affiliation signal, and the rating advantage, while HRL competes for incremental new business at the margin.

How NRIC actually makes money

To understand the economics of a reinsurer in a small market like Nepal, it helps to start with how reinsurance differs from primary insurance. A primary insurer collects premium from end policyholders, holds a fund against expected future claims, and earns a margin on the difference between premium collected and claims paid out. A reinsurer's premium does not come from policyholders; it comes from the primary insurers themselves. The primary insurer cedes a portion of the risk on its policies to the reinsurer in exchange for ceding a portion of the premium it has collected. The reinsurer then pools that ceded risk across multiple primary insurers and multiple risk categories. In return for taking on tail-event exposure that any single primary insurer would struggle to absorb alone, the reinsurer earns a margin that is structurally thin in normal years and that becomes critically important when catastrophic events happen.

For NRIC, the underwriting margin on the ceded book is structurally thin most years. The risks ceded are catastrophic-tail risks, large fires, motor pile-ups, aviation incidents, RSMDST-type political violence that are infrequent. In any given fiscal year, claims may be near zero, in which case the reinsurer keeps the bulk of the ceded premium. In occasional years, claims spike dramatically, and the reinsurer absorbs losses against its insurance fund and reserves. NRIC's capital structure is built to absorb this year-to-year volatility through its insurance fund. The reported profit, however, comes mostly from somewhere else.

That somewhere else is the investment portfolio. NRIC, like all Nepali insurers, parks the bulk of its investable assets in bank fixed deposits, government securities and a small allocation to equity and alternatives. Approximately 90 percent of the company's investment book sits in fixed deposits at commercial banks, development banks and finance companies. As of the most recently disclosed period, that portfolio was around Rs 11 billion in scale comparable to the paid-up capital base.

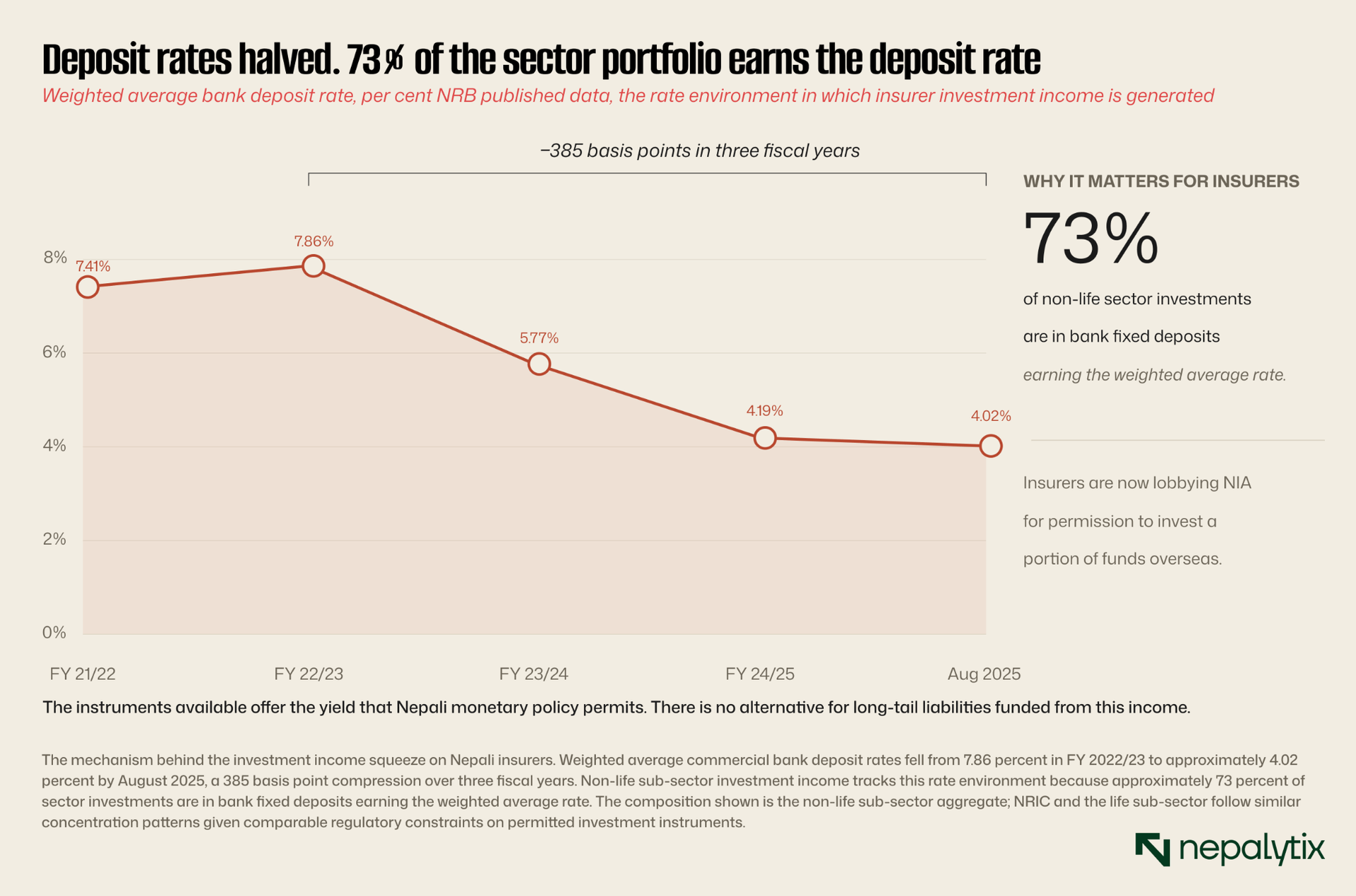

The yield earned on this portfolio drives the bulk of NRIC's reported earnings. The yield trajectory is the key operational variable. Average yield on NRIC's investment portfolio was approximately 6 percent in FY 2016, 7 percent in FY 2017, 10 percent in FY 2018 the company's peak earnings period and approximately 8 percent in FY 2024, with the FY 2022 to FY 2024 average around 8.5 percent per ICRA Nepal's November 2024 rating report. That trajectory tracks the broader Nepali deposit rate environment closely. Weighted average bank deposit rates have fallen from a peak of 7.86 percent in FY 2022/23 to approximately 4.02 percent in August 2025, a decline of 385 basis points in three fiscal years. NRIC's investment yield has fallen with the broader rate environment, although the company's 2024 net income of Rs 103 crore (Rs 1.03 billion) demonstrates that even in the lower-rate environment, the underlying business model remains profitable.

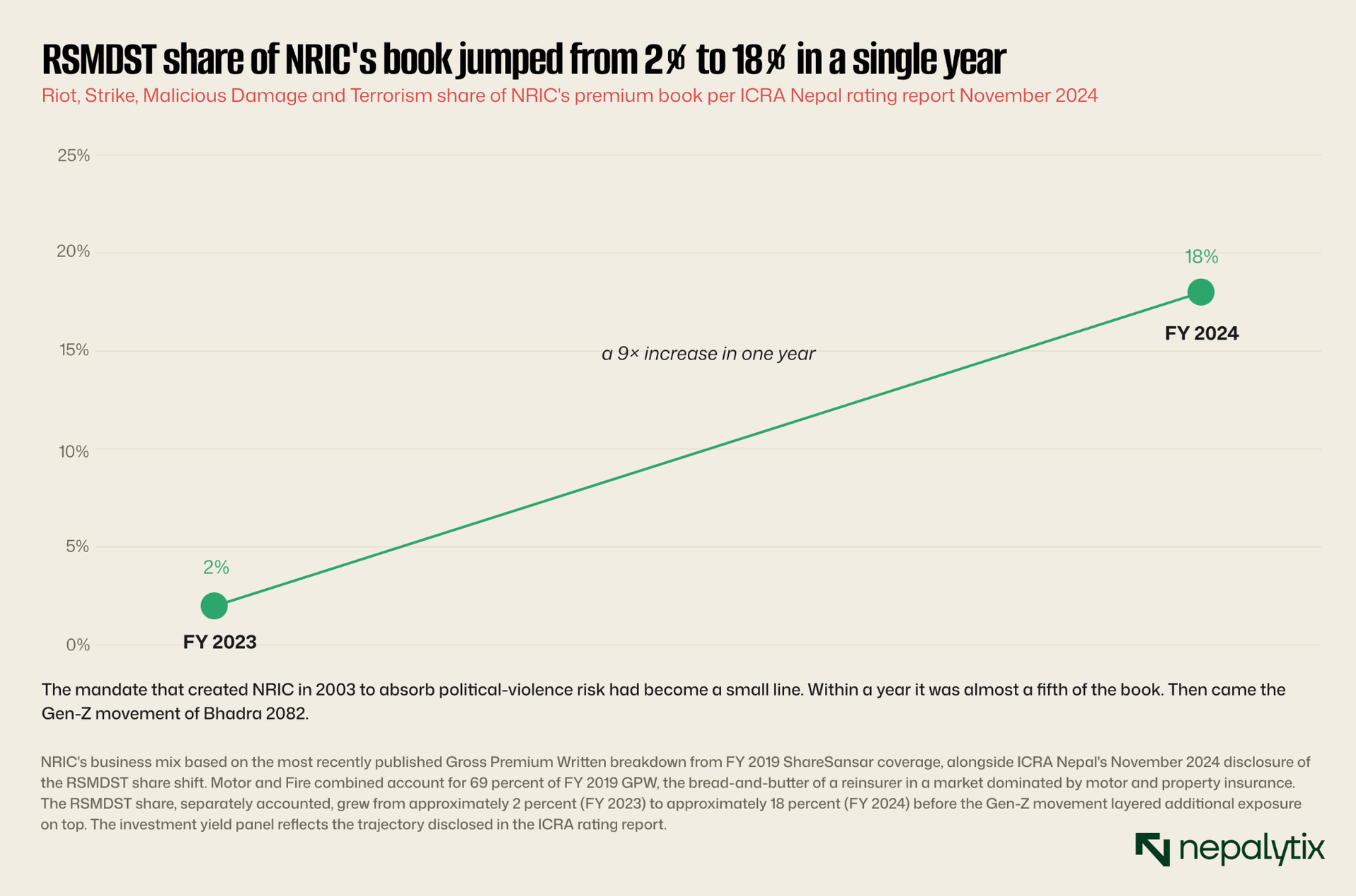

ICRA Nepal's November 2024 rating report flagged one compositional shift that matters considerably for what comes next in this analysis: NRIC's RSMDST portfolio share increased from approximately 2 percent of the underwriting book in FY 2023 to approximately 18 percent in FY 2024. That is roughly a nine-fold increase in the share of the legacy terrorism-and-political-violence mandate in just one fiscal year. The shift happened before the Gen-Z movement of September 2025 added another layer of RSMDST-category exposure on top. Whatever happens next in NRIC's P&L statement, the company that absorbs it has a different risk-share composition than it did two years ago.

The Q3 FY 2081/82 quarterly disclosure provides the clearest recent operational picture of normal-year NRIC. The company reported a total insurance premium of Rs 7.83 billion for the period, a 26.53 percent year-on-year increase from Rs 6.19 billion the prior year. Net insurance premium (after retrocession to international reinsurers) was Rs 7.11 billion, up 38.13 percent year-on-year. Annualized earnings per share rose to Rs 5.45 from Rs 5.36. Net worth per share stood at Rs 149.15. At current market price around Rs 920 (May 25, 2026), NRIC's price-to-earnings ratio based on FY 81/82 full-year EPS of Rs 7.71 stands at approximately 119x, a premium valuation reflecting the company's scarcity value as the established listed reinsurer rather than its earnings fundamentals. The solvency margin stood at 3.65 times as of mid-July 2023 (versus 3.26 times mid-July 2022 per ICRA disclosure), well above the regulatory minimum of 1.5x. NRIC's Q3 FY 82/83 results have not yet been publicly disclosed at the time of writing; the most recent comprehensive disclosure is the FY 81/82 fourth-quarter print.

The economics of NRIC in normal times are therefore reasonably predictable. Premium growth tracks the underlying expansion of Nepal's primary insurance market. Underwriting profit fluctuates around zero in most years. Investment yield, the dominant income source, tracks the prevailing deposit rate environment. The result is a low-but-stable return on equity profile of 9 to 10 percent and return on assets in the 7 to 9 percent range. A government-affiliated, scarcity-priced regulated monopoly with a structurally large investment book and modest but predictable earnings. That is the company as it has operated for the past decade.

The two sectors that depend on NRIC

NRIC's monopoly economics make most sense when seen alongside the two primary-insurance sub-sectors that cede risk to it. The fourteen life insurers and fourteen non-life insurers operating in Nepal collectively buy reinsurance protection from NRIC and HRL but the nature of their books and the dynamics of their earnings differ in important ways. Both sub-sectors are under pressure in FY 2082/83, but for different reasons.

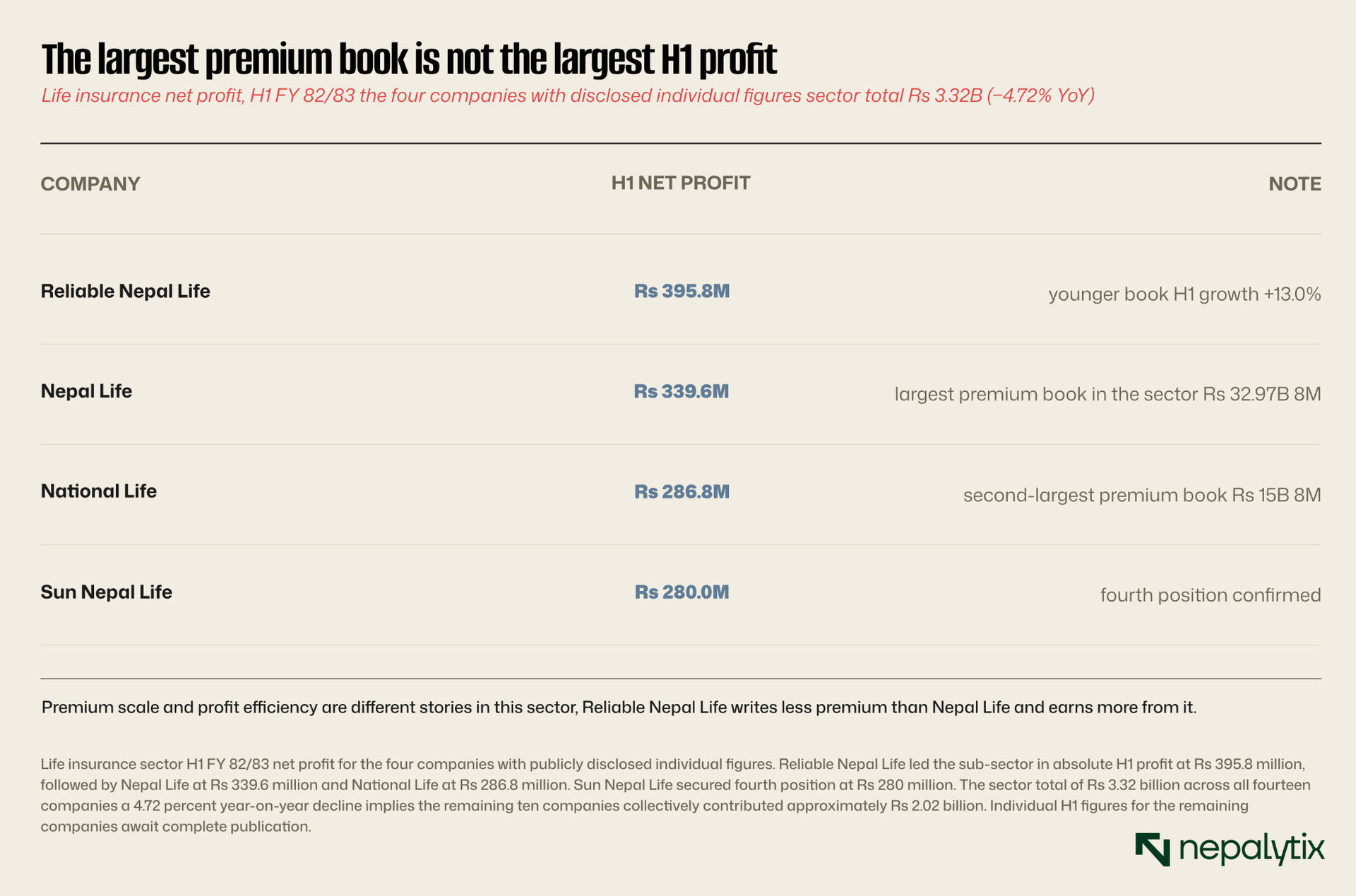

The life insurance sub-sector is structurally healthier. Premium income grew steadily: the fourteen life insurers collectively generated Rs 124.72 billion in gross premium during the first eight months of FY 2082/83, with Rs 28.14 billion from first premiums on new policies and Rs 96.57 billion from renewals on existing policies. The high renewal share is the signal of underlying durability, customers are keeping their policies in force, which is the defining behavioral metric for life insurance. Nepal Life Insurance Company led the sub-sector with Rs 32.97 billion in premium income (8M data), roughly 26 percent of total life sector premium. National Life Insurance Company followed at Rs 15 billion.

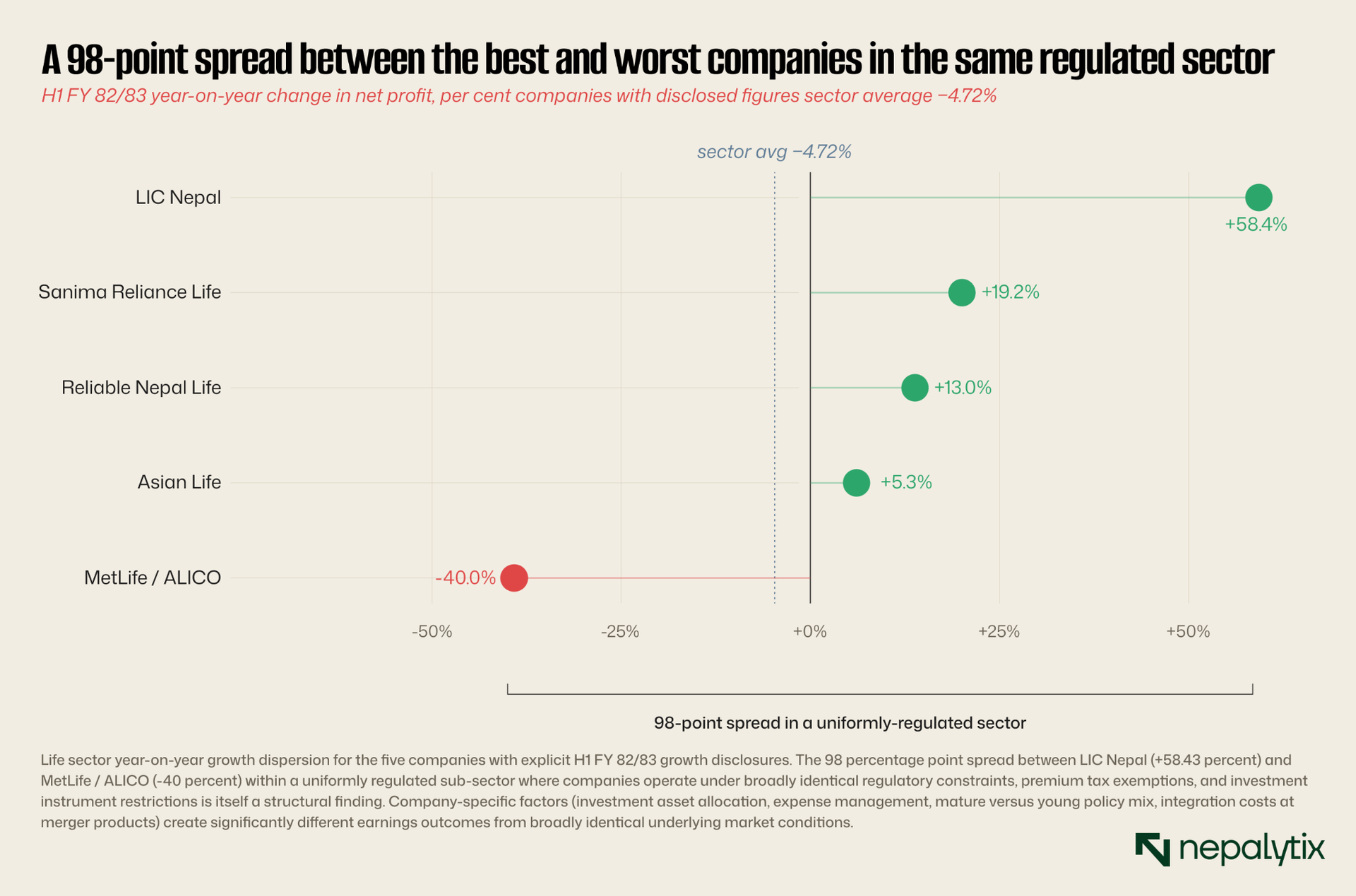

Underneath the steady premium growth, however, the profit picture is more complex. In Q1 FY 2082/83 (Ashwin-end, mid-October 2025), the fourteen life insurers collectively earned Rs 1.97 billion in net profit, a 2.51 percent year-on-year increase. Through H1 FY 2082/83 (Poush-end, mid-January 2026), sector net profit was Rs 3.32 billion, a 4.72 percent decline year-on-year against the Rs 3.48 billion the same companies had reported in H1 FY 2081/82. Premium up, profit down. The contraction reflects the same investment-income squeeze affecting NRIC: the long-tail liabilities that life insurance creates (policies sold today with claims potentially decades out) require steady investment yield to fund, and the falling deposit rate environment is compressing that yield faster than premium growth is compensating.

The intra-sector dispersion in growth rates is large and informative. Nine of the fourteen companies posted profit growth in H1 FY 82/83. Five declined. The magnitudes within that distribution are extreme. LIC Nepal posted a 58.43 percent year-on-year increase in H1 profit, the largest gain in the sub-sector. Sanima Reliance Life grew 19.21 percent. Reliable Nepal Life grew 13.0 percent. Asian Life grew 5.27 percent. At the other end of the spectrum, MetLife / ALICO was identified by NepseTrading as one of the five H1 decliners; the company's FY 81/82 full-year disclosure had shown a 40 percent year-on-year profit decline, and the trajectory appears to have continued through the most recent reporting period.

Why is the dispersion so large within a regulated sector? Three structural factors. The first is policy book maturity. Companies with younger books: Reliable Nepal Life, IME Life, Citizen Life among the more recent entrants have fewer mature claims hitting earnings; companies with older books carry more mature claim exposure proportionally. The second is investment yield differentials. Companies that historically tilted toward longer-duration government securities are now earning closer to 7-8 percent on those holdings versus 4 percent on new bank deposits, a meaningful tailwind for the companies with the right asset allocation entering the rate-decline cycle. The third is the merger-product transition. SuryaJyoti Life, Sanima Reliance Life, Himalayan Life, and Prabhu Mahalaxmi Life are still working through integration costs from their 2022-2023 mergers, and those costs depressed reported H1 profit beyond what underlying operations would suggest.

The life sub-sector's outlook for the second half of FY 2082/83 and into FY 2083/84 depends primarily on the trajectory of the deposit rate environment. If rates continue to fall as the FY 2083/84 monetary policy is likely to direct, life insurer profitability continues to compress despite the durable premium growth. If rates stabilize or reverse, sector profitability improves substantially without any company-specific action required. Premium growth itself remains intact, the customer base is expanding, the product is being sold, and the renewal book is durable. The structural pressure is on the asset side of the balance sheet, not the liability side.

The non-life sub-sector tells a quite different story.

The non-life shock

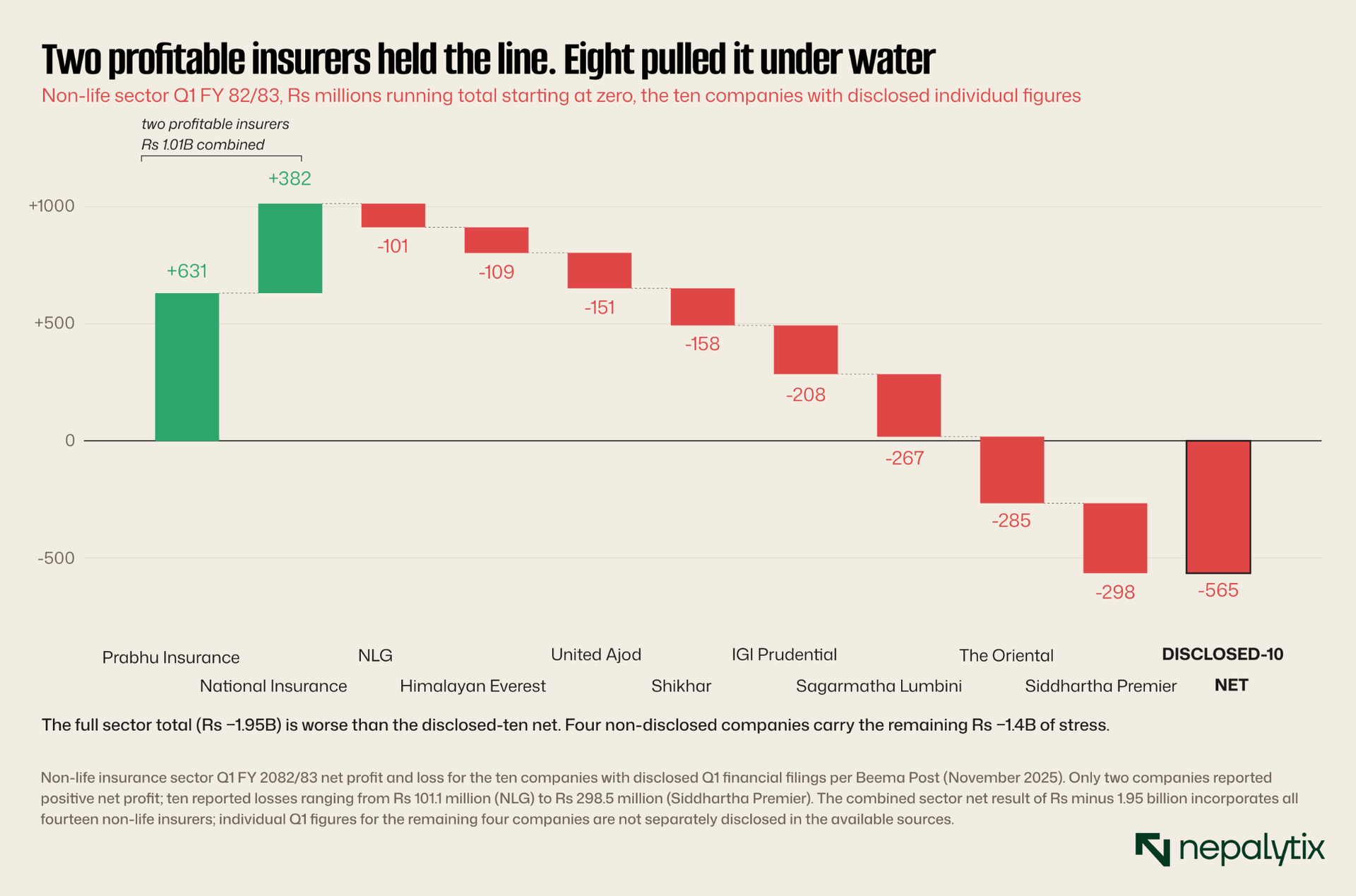

In Q1 FY 2082/83 (Ashwin-end, October 2025), twelve of the fourteen listed non-life insurance companies reported net losses. The sector aggregate net result was Rs minus 1.95 billion, the worst quarterly outcome in recent memory for the non-life sub-sector. Only Prabhu Insurance with Rs 631 million in net profit (up 12 percent year-on-year) and National Insurance Company, with Rs 381 million in net profit (swinging from prior-year loss to profit), escaped the carnage.

The proximate cause of the Q1 shock is identifiable and dated. On Bhadra 23-24, 2082 (September 8 and 9, 2025), the Gen-Z movement protests against government corruption and the social media ban escalated into the most consequential political event in Nepal's recent history. Initial police violence on September 8 killed nineteen protesters; by the end of the protest period the total death toll reached seventy-six with over 2,100 injured per Ministry of Health and Population data. The Oli government fell. Protesters set fire to the Parliament building, the President's Office, multiple government ministries, the residences of senior politicians, and numerous corporate properties. The Nepali Army assumed security control. Sushila Karki was appointed interim Prime Minister on September 12. The House of Representatives was dissolved; fresh elections were held in 2026 with Balen Shah elected.

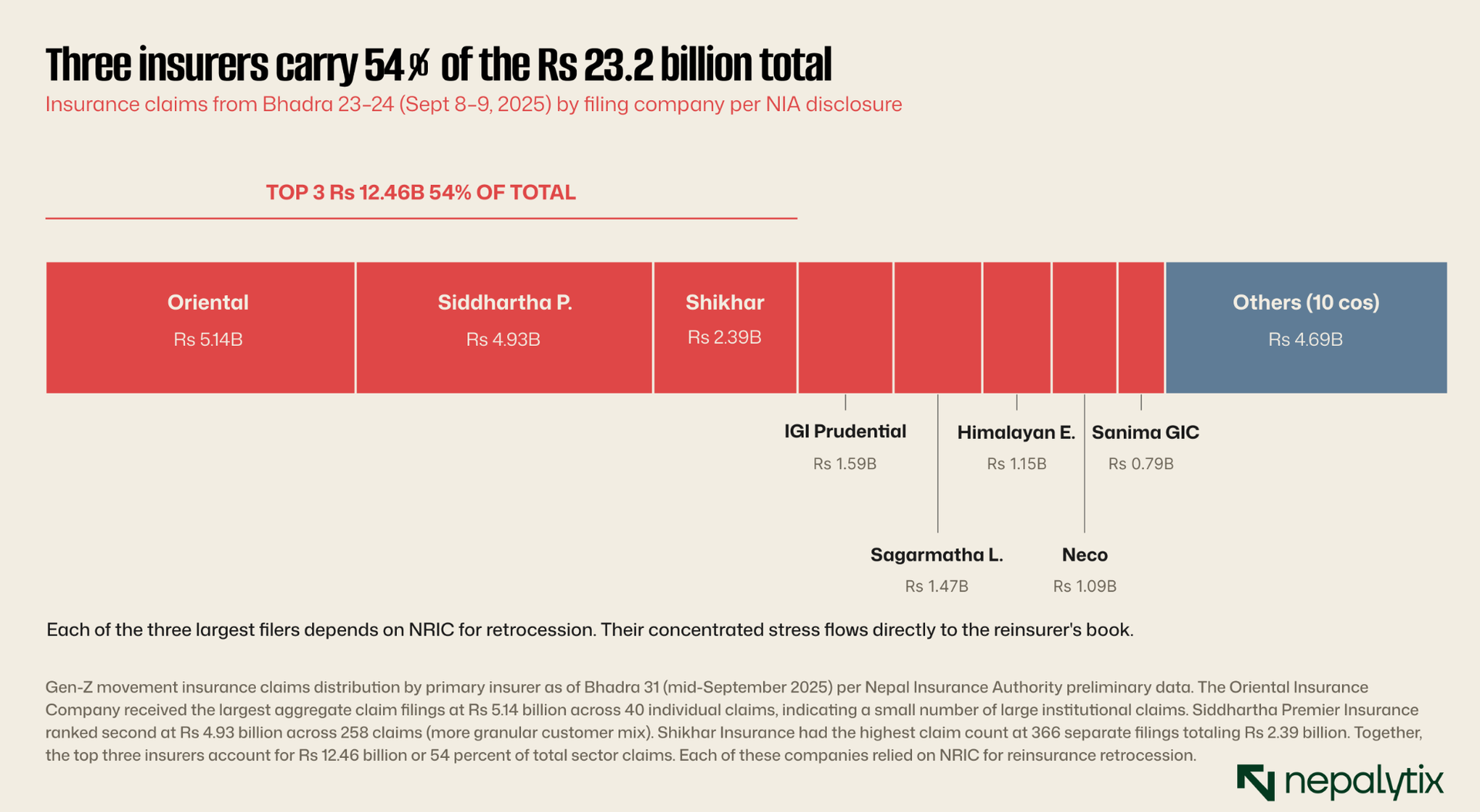

The political consequences of those two days are being absorbed by the country's institutions and will be processed for years. The financial consequences for the insurance sector are by now reasonably documented. According to Nepal Insurance Authority data released by Bhadra 31 (mid-September 2025), 1,984 insurance claims had been filed across eighteen non-life insurance companies for Gen-Z movement damages totaling approximately Rs 23.23 billion. Subsequent estimates by Republica suggest the total exposure could approach Rs 50 billion as final damage assessments complete. The institutions affected and the names matter, because they are the names of the country's largest commercial properties included Bhat-bhateni Superstore outlets at Tangal, Maharajgunj, Chitwan, Chuchchepati, and Koteshwor (the last described as "completely damaged"); Kantipur Media Group; Ullens School; CG Impex and CG Electronics; United Distributors; Ncell; Hilton Hotel; Bagaicha Hotel and Hotel Sarobar in Pokhara; Central Business Park; the Chandragiri and Maulakalika cable car infrastructure; and four commercial bank branches including the Rastriya Banijya Bank New Baneshwor branch where 18 kilograms of gold was looted from vaults.

The Q1 FY 2082/83 financial statements of the non-life insurance sub-sector show the direct mechanical impact of these claims. The companies with the largest claim filings are also the companies with the largest Q1 losses. Siddhartha Premier reported a Q1 net loss of Rs 298.5 million. The Oriental reported a loss of Rs 284.8 million. Sagarmatha Lumbini posted Rs 267.3 million in losses. IGI Prudential, which had been profitable in the same period the prior year, swung to a Rs 207.6 million loss. Shikhar Insurance: the sector market leader by gross premium written reported a Q1 loss of Rs 158.5 million.

The underlying issue behind the concentration of losses is a coverage gap. Most non-life insurers in Nepal sold standard property and asset coverage policies that included general terrorism coverage but had not separately priced or reinsured the specific scenario of politically motivated mass vandalism that the Gen-Z movement represented. As Republica noted in mid-September: "premiums for 'sabotage and terrorism' policies which cover politically motivated violence are comparatively minimal." When the claims arrived, the companies that had inadequately reinsured this specific risk took the entire exposure onto their own balance sheets.

The exposure flowed upstream from the primary insurers to NRIC as the system-wide reinsurer.

"NRIC carries approximately Rs 11.77 billion in reinsurance liabilities from the fourteen non-life insurers' Gen-Z claims."

The Rs 11.77 billion figure comes from multiple primary sources: Republica's September 18, 2025 reporting citing NIA data, People's Review on September 19, and AM Best's September 24 commentary on the systemic event. AM Best's assessment is worth quoting at slightly more length because it frames the question that defines NRIC's FY 2082/83 outlook: capital pressure on Nepal's domestic reinsurers from the Gen-Z event is, in their words, "likely, though retrocession may partially alleviate financial stress," though elevated retention of RSMDST exposures "may still erode their capital buffers, reducing their ability to withstand subsequent shocks over the near term."

The stress test

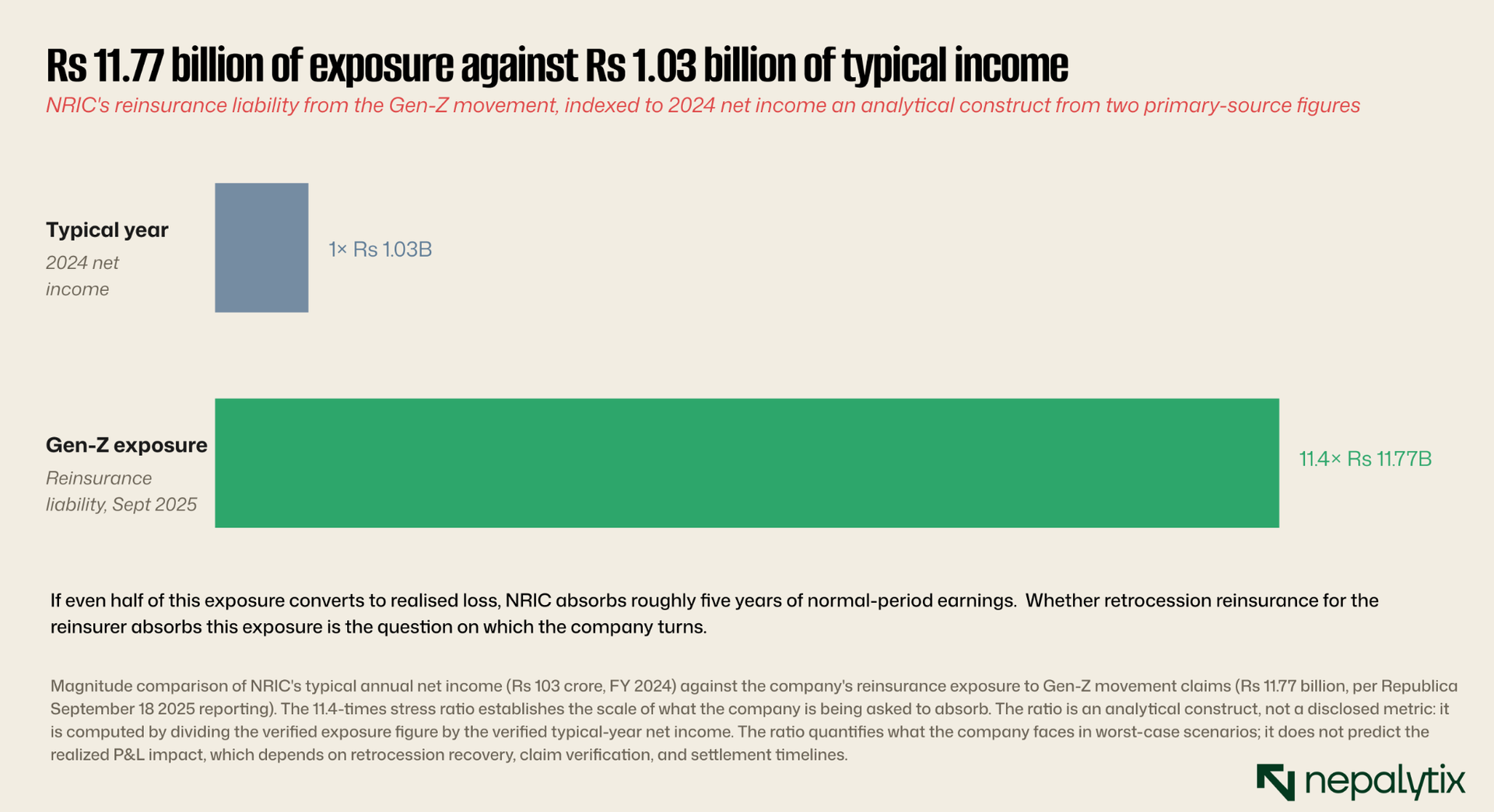

To understand the magnitude of what NRIC is facing, the right comparison is between the Gen-Z reinsurance exposure and the company's typical-year earnings power. In 2024 a representative recent fiscal year NRIC reported net income of approximately Rs 103 crore (Rs 1.03 billion). The Gen-Z exposure of approximately Rs 11.77 billion is therefore approximately 11.4 times typical annual net income (computed from the two verified primary-source figures; not a single disclosed metric).

Three factors will determine how this exposure resolves into actual P&L recognition over the next several fiscal years.

The first is retrocession. NRIC, like all reinsurers globally, cedes a portion of its risk to international reinsurers, the "reinsurer's reinsurer." The thirty-two-country facultative network NRIC has built over the past decade exists precisely for this purpose: to spread tail risk on Nepali exposures across a global pool of reinsurance capital. Whether the Gen-Z movement claims were covered under NRIC's standing retrocession treaties or required separate facultative arrangements is a question only the company's management and underwriters can answer definitively. Public disclosure has not yet specified the proportion. AM Best's September 2025 commentary explicitly contemplated retrocession as a partial mitigant. The company's AA- ICRA rating, reaffirmed in November 2024 before the Gen-Z event, implies confidence in the broader risk management framework. A rating action is a possibility that observers should monitor in the coming quarters.

The second is claim verification timing. Insurance claims of this magnitude do not settle quickly. The NIA-disclosed claim total of Rs 23.23 billion is a preliminary figure based on initial filings. Actual settlement amounts depend on damage verification, policy coverage interpretation, exclusions application, salvage recovery, and in some cases legal proceedings. Realistic settlement timelines extend eighteen to thirty-six months. NRIC will be recognizing claim expenses progressively over multiple fiscal years rather than absorbing it in a single quarter which both spreads the earnings impact and creates uncertainty about ultimate exposure.

The third is the precedent value of the event. The Gen-Z movement is the largest single insurance event in Nepal's recent history, but it is not the first politically-motivated property destruction event the country has seen. The 2003 RSMDST pool was created precisely because the Maoist insurgency had similar (smaller-scale) effects on insurer balance sheets. The 2015 earthquake was a different kind of catastrophic event but had insurance-sector consequences of comparable magnitude. NRIC has institutional experience absorbing systemic claim events. The Gen-Z stress test is the most recent and largest, but it is not unprecedented for the company or the sector.

The most consequential implication for NRIC's next twenty-four months may be less about whether the company survives the Gen-Z claims and more about how it prices RSMDST risk going forward. The market discovery from the event is that the structural pricing of politically-motivated mass-vandalism risk in Nepali insurance was too low across the entire sector. Going forward, primary insurers will need to charge higher premium for this risk; NRIC will need to charge higher retrocession premium to primary insurers; and the international reinsurance market that NRIC cedes to will reprice Nepal as a geography accordingly. The result will be a higher cost of insurance for Nepali consumers and a higher premium income line for NRIC's legacy RSMDST mandate that created the company in 2003 and now defines its forward exposure.

The investment income squeeze

Sitting parallel to the Gen-Z stress test, and arguably more consequential over the long run, is the slower-moving but structurally permanent pressure on insurer profitability from the low interest rate environment. The non-life insurance sub-sector aggregate investment portfolio stood at Rs 64.87 billion as of Q1 FY 2082/83 per NIA data. Of that total, Rs 47.48 billion (approximately 73 percent) was held in fixed deposits at banks and financial institutions, with Class A commercial banks alone accounting for Rs 41.56 billion roughly 64 percent of total non-life sub-sector investment

The mechanism is straightforward. Insurance companies are required by NIA regulation to hold investments primarily in permitted instruments: government securities, fixed deposits at licensed banks and financial institutions, and a limited allocation to equities. The instruments available offer a yield environment determined by Nepali monetary policy. When the rate cycle compresses, as it has since FY 2022/23, insurer investment income compresses proportionally. There is no flexibility for the insurer to seek higher yield elsewhere, and there is no alternative source of return to fund the long-tail liabilities that life insurance creates.

Insurer sentiment on this has shifted noticeably in recent quarters. NIA has received multiple representations from the Nepali insurance industry requesting permission to invest a portion of insurer funds in overseas markets particularly in higher-yielding emerging market sovereign and corporate debt. The structural argument is that current domestic instruments cannot generate the yield needed to fund long-term insurance commitments at current premium pricing. The counter-arguments from NIA and NRB are also reasonable: overseas investment introduces foreign exchange risk to insurer balance sheets, reduces the supply of domestic insurance investment for the banking and government bond markets and creates regulatory supervision complications. The resolution will likely come over the next twelve to eighteen months. NIA has indicated it is open to permitting limited overseas investment under specific conditions. If granted, the rule change would mark a significant evolution in Nepali insurance regulation.

The same structural dynamic domestic capital markets unable to generate sufficient yield in a low-rate environment is what Monday's Signal documented for the credit-demand side. The non-life insurance sector and the productive-credit demand collapse are the two faces of the same underlying coin: Nepal has accumulated more capital than its current real economy can productively absorb at risk-adjusted returns that domestic institutions need to function. The insurance sector experiences this as compressed investment yield. The banking sector experiences it as Rs 838 billion of excess liquidity parked at NRB. Both are consequences of the same structural condition.

What comes next

Looking forward to FY 2083/84 and beyond, three forces will shape the Nepali insurance sector.

The first is continued consolidation. The Rs 5 billion minimum paid-up capital requirement that triggered the 2022-2023 mergers has not run its course. Several mid-tier life and non-life insurers remain close to the regulatory floor. NIA has indicated it would prefer further consolidation toward a smaller number of larger, better-capitalized companies particularly on the non-life side where the Gen-Z movement exposed the concentration of underwriting risk in companies that lack the balance sheet to absorb major events. Additional consolidation appears plausible over the next eighteen to twenty-four months, particularly among smaller non-life insurers, though specific merger announcements depend on individual board and regulatory dynamics that are not externally observable.

The second is regulatory evolution. NIA's annual policy and program framework for FY 2082/83 emphasized enhanced regulatory standards, public awareness campaigns, and capacity-building. The Gen-Z event will accelerate that agenda. Items to watch in the FY 2083/84 framework include explicit terrorism and political-violence pricing guidelines, mandatory minimum reinsurance ratios for catastrophic risks, capital adequacy requirements aligned with international solvency standards, and the long-discussed permission for limited overseas investment for insurers. Each of these would represent a meaningful step toward modernizing the sector's regulatory infrastructure.

The third is the macro picture. Insurance sector profitability is structurally a function of premium growth, underwriting margin, and investment yield. In FY 2082/83, premium growth is healthy, the life sub-sector 8M premium is up year-on-year, the non-life sub-sector 10M premium is up 14.81 percent. Underwriting margin is being stress-tested by Gen-Z claims for non-life and is structurally thin for life. Investment yield is being squeezed by the rate cycle. The forward outlook is therefore primarily a function of where the NRB rate cycle goes next, and Monday's Signal analysis suggested further easing is the more likely path.

For investors in Nepali listed insurance companies specifically, the implications differ by sub-sector. NRIC is best understood as a regulated-utility-style investment: predictable in normal years, stress-tested in extraordinary ones, with valuation driven primarily by scarcity (the established listed reinsurer) rather than earnings growth. HRL is a higher-beta proxy for the same sector with additional execution risk from being the newer entrant. Among life insurers, premium-book scale Nepal Life, National Life, Reliable Nepal Life provides longer-term durability than any single quarter's absolute profit ranking suggests. Among non-life insurers, the Q1 FY 2082/83 losers will likely be the FY 2082/83 multi-quarter underperformers because the Gen-Z movement claim recognition will continue rolling through their P&L statements. The two profitable non-life insurers in Q1 (Prabhu and National) will not necessarily be the structural winners of FY 2082/83 their Q1 outperformance reflects lower direct exposure to the specific Gen-Z claim concentration, not necessarily superior underlying business positioning.

The most important single observation about the Nepali insurance sector in FY 2082/83 is that the assumed correlation between sector earnings and the broader rate cycle has not broken. Insurance, banking, and broader Nepali financial services are all responding to the same monetary policy environment: falling rates, excess liquidity at NRB, compressed investment yields, weak productive credit demand. The Gen-Z movement was a one-time event that overlaid additional stress on the non-life sub-sector. The deeper structural pressure is the same one Monday's Signal documented: the Nepali financial services sector has been built around an assumed yield environment that no longer exists and the next twenty-four months of sector consolidation, regulatory reform, and capital allocation will be defined by adapting to that new reality.

NRIC, as the apex reinsurer in a regulated near-monopoly, sits at the intersection of those structural pressures and the legacy mandate that defines how the sector responds to a tail event. The company that emerged from the 2003 insurance pool to absorb RSMDST risk during the Maoist insurgency now finds its founding mandate at the centre of its FY 2082/83 stress test. That is a kind of corporate symmetry that does not happen by accident.